Africa Insurance Market Size, Share, Trends & Growth Forecast Report By Type (Life Insurance, General Insurance), Distribution Channel (Insurers, Insurance Brokers and Agencies, Banks, Others), and Country (Sudan, Egypt, Kenya, Ethiopia, Ghana, South Africa, Rest of Africa) – Industry Analysis, 2026 to 2034

Africa Insurance Market Size

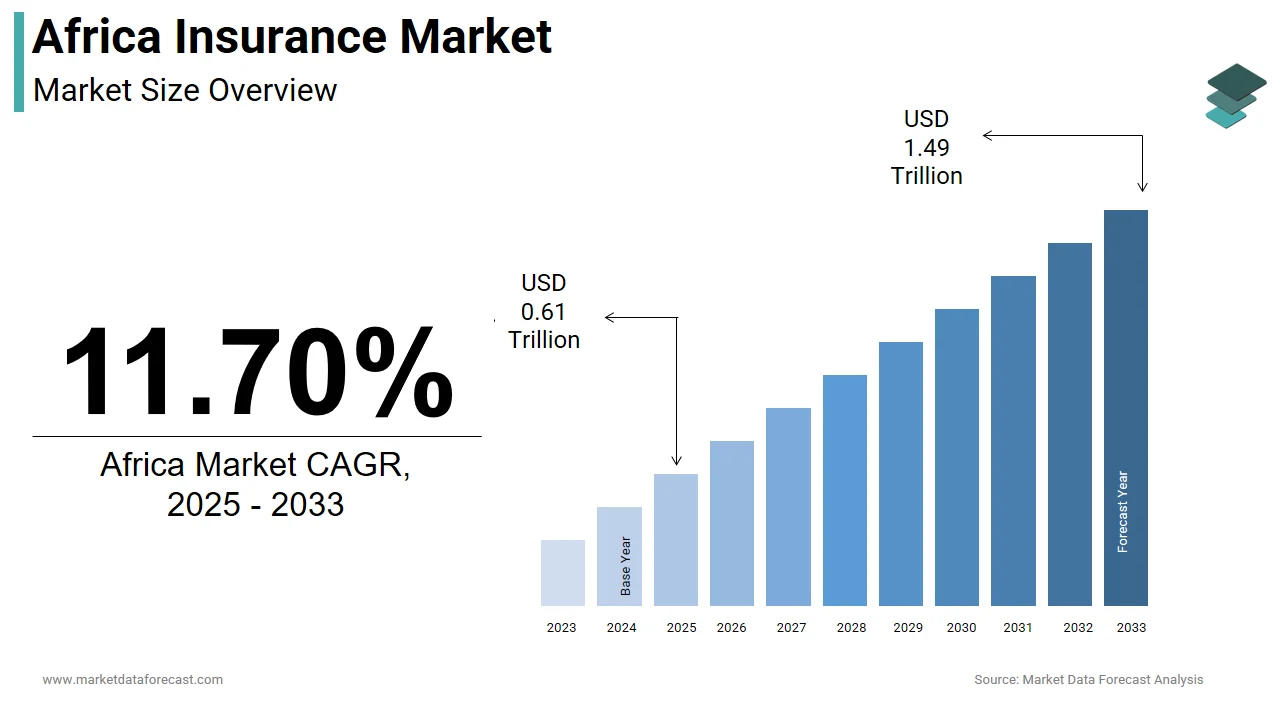

The Africa insurance market was valued at USD 0.61 trillion in 2025, is estimated to reach USD 0.68 trillion in 2026, and is projected to reach USD 1.65 trillion by 2034, growing at a CAGR of 11.70% from 2026 to 2034.

The African insurance is a fragmented yet evolving financial ecosystem with low penetration and significant regional disparities.

MARKET DRIVERS

Rising Urbanization and Informal Sector Vulnerability

The urbanization across Africa is accelerating at an unprecedented pace, with the United Nations projecting that the continent’s urban population will double from 567 million in 2021 to over 1.2 billion by 2050. In Nairobi, for instance, over 70% of motorcycle taxi operators now subscribe to some form of accident insurance, indicating a behavioral shift toward formal risk mitigation. The concentration of economic activity in urban centers also enables insurers to reduce distribution costs through agent networks and digital platforms by improving scalability.

Expansion of Mobile Financial Services

The proliferation of mobile financial services has emerged as a transformative enabler for insurance uptake across Africa. This infrastructure has allowed insurers to bypass traditional distribution bottlenecks and offer pay-as-you-go microinsurance products via mobile platforms. The integration of insurance into mobile wallets reduces transaction costs, enhances customer trust, and allows for real-time claims processing by making coverage accessible to previously excluded populations.

MARKET RESTRAINTS

Low Financial Literacy and Trust Deficit

The widespread adoption of financial literacy and public mistrust in formal financial institutions are limiting the growth of the African insurance market. According to the World Bank’s 2021 Global Findex Database, only 43% of adults in Sub-Saharan Africa could correctly answer basic financial literacy questions related to interest rates, inflation, and risk diversification. This knowledge gap is compounded by historical experiences of claim denials, opaque policy terms, and aggressive sales practices, which have eroded consumer confidence.

Macroeconomic Instability and Currency Volatility

The macroeconomic instability, particularly currency depreciation and inflation, which undermines the operational viability of insurance firms across much of Africa, is also hampering the growth of the African insurance market. Insurers, especially life and health providers, face challenges in pricing long-term policies when future liabilities cannot be reliably forecasted in local currencies. In Nigeria, the naira depreciated by over 60% against the US dollar between 2022 and 2024, forcing insurers to hold larger foreign exchange reserves or limit product offerings, according to the National Insurance Commission. This volatility discourages investment in insurance infrastructure and restricts product innovation in indexed or savings-linked policies that require stable monetary conditions to function effectively.

MARKET OPPORTUNITIES

Climate-Linked Insurance for Agricultural Economies

Agriculture is the backbone of many African economies, showcasing huge opportunities for the growth of the African insurance market. Over 60% of the workforce in countries like Malawi and Uganda, according to the Food and Agriculture Organization. However, climate change has intensified droughts, floods, and erratic rainfall, which are threatening livelihoods and increasing demand for risk transfer mechanisms. Index-based agricultural insurance, which pays out based on weather triggers rather than individual loss assessments, has gained traction as a scalable solution. Ethiopia’s index insurance pilot, supported by the World Food Programme, covered over 300,000 smallholder farmers in 2022 alone.

Regulatory Harmonization through African Union Initiatives

The African Union’s Agenda 2063 and the establishment of the African Continental Free Trade Area (AfCFTA) have catalyzed efforts toward financial sector integration, including insurance regulation. Regional blocs such as ECOWAS and SADC are advancing mutual recognition agreements that allow insurers licensed in one member state to operate across borders with minimal additional oversight. In East Africa, the Insurance Regulatory Authority of Kenya and Uganda’s Insurance Regulatory Authority have implemented joint audits since 2022 by reducing duplication and compliance costs.

MARKET CHALLENGES

Data Scarcity and Actuarial Modeling Limitations

The absence of reliable, granular risk data necessary for accurate actuarial modelling is ascribed to bolster the growth of the African insurance market. In motor insurance, inconsistent traffic accident reporting limits the ability to assess risk exposure, with less than 40% of road fatalities officially recorded in countries like Tanzania and Cameroon, as per the World Health Organization. This data deficit forces insurers to rely on proxies or conservative assumptions, leading to either overpricing that deters customers or underpricing that jeopardizes solvency.

Talent Shortage in Specialized Insurance Functions

The shortage of skilled professionals in underwriting, actuarial science, and claims management is significantly inhibiting the growth of the African insurance market. As of 2023, the continent had fewer than 500 qualified actuaries, with over 70% concentrated in South Africa, according to the Actuarial Society of South Africa. This scarcity is particularly acute in emerging markets such as Angola and Ethiopia, where complex regulatory environments and product diversification require advanced technical expertise. The Insurance Institute of Ghana reported in 2022 that only 28% of mid-level insurance employees possessed formal qualifications in risk management or actuarial studies. Training programs remain limited, and brain drain to international markets further exacerbates the gap.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Sudan, Egypt, Kenya, Ethiopia, Ghana, South Africa, Rest of Africa |

| Market Leaders Profiled | Progressive Corporation, Zurich INS Group, HDI V.a.G., MetLife Inc., Centene Corporation, State Farm Group, Elevance Health, Inc., AXA S.A., Allianz SE, UnitedHealth Group Incorporated, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The life insurance segment was the largest and held 58.2% of the African insurance market share in 2024, with the relatively mature financial sector and a culture of long-term savings. As per the South African Reserve Bank, life insurance premiums reached ZAR 386 billion (approximately USD 20.8 billion) in 2023, underpinned by endowment policies, retirement annuities, and investment-linked products. The segment benefits from structured distribution through employer-sponsored group schemes, which cover nearly 42% of formal sector employees, as reported by the South African Institute of Risk and Insurance Management. Additionally, rising awareness of financial protection in the face of high HIV/AIDS-related mortality historically incentivized uptake, while evolving products now cater to middle-income households seeking wealth accumulation and estate planning solutions.

The general insurance segment is expected to grow with an expected CAGR of 9.4% in the coming years, owing to the rising regulatory mandates and socioeconomic shifts that are increasing demand for non-life coverage. Simultaneously, health insurance is gaining traction due to strained public healthcare systems. In Kenya, private health insurance enrollment grew to 14.3 million in 2023 from 9.8 million in 2020, as documented by the Ministry of Health.

By Distribution Channel Insights

The direct distribution by insurers segment was accounted in holding 44.3% of the share in 2024 with the entrenched presence of large, vertically integrated insurance companies that maintain in-house sales forces and proprietary customer service networks. Moreover, the scalability of direct channels allows insurers to retain higher margins and maintain control over customer experience, which is critical in markets with low trust in intermediaries.

The “Others” category is registering a CAGR of 12.7% in the coming years with the rapid adoption of smartphone-based financial services and the proliferation of API-driven partnerships between insurers and tech firms. Similarly, in Ghana, the integration of funeral and health microinsurance into mobile wallet transactions led to a 35% rise in first-time insurance buyers among informal workers between 2022 and 2023, according to the National Insurance Commission. These models lower entry barriers, enable pay-per-use pricing, and leverage existing user behavior by making them uniquely suited to Africa’s mobile-first, low-income majority population.

COUNTRY-LEVEL ANALYSIS

South Africa Insurance Market Insights

South Africa was the top performer in the African insurance market by occupying 62.3% of the share in 2024, with a sophisticated and well-capitalized insurance sector, with a penetration rate of 12.4% of GDP, far exceeding the continental average of 3.2%, as noted by the Insurance Regulatory Authority of Kenya. Life insurance dominates, driven by a large formal workforce, institutional investment frameworks, and mandatory retirement savings vehicles.

Egypt Insurance Market Insights

Egypt insurance market was positioned second with 8.7% of share in 2024. Additionally, motor insurance penetration has risen to 31% of vehicles, up from 19% in 2020, driven by stricter enforcement of compulsory coverage laws. The Central Bank of Egypt reported that digital insurance transactions increased by 64% in 2023, reflecting growing consumer comfort with online platforms.

Kenya Insurance Market Insights

Kenya insurance market growth is ascribed to grow with a balanced mix of life and general insurance, with health and motor segments experiencing rapid growth due to urbanization and rising vehicle ownership.

Nigeria Insurance Market Insights

Nigeria insurance market growth is likely to grow with an expected CAGR in the coming years. The introduction of the National Health Insurance Scheme Act in 2022 expanded coverage mandates by aiming to enroll 100 million Nigerians by 2027, as stated by the Federal Ministry of Health. Motor insurance penetration remains below 15%, but enforcement efforts have led to a 24% year-on-year increase in premiums in 2023. Structural challenges persist, but policy reforms and tech innovation are laying the foundation for future scale.

COMPETITION OVERVIEW

The competitive landscape of the Africa insurance market is marked by a mix of entrenched regional giants and agile digital disruptors. Established insurers like Sanlam and Old Mutual leverage brand equity and extensive distribution networks, while local players focus on niche segments and community-based models. Intensifying competition is driven by digital innovation, with new entrants leveraging mobile technology to offer low-cost, on-demand coverage. Regulatory divergence across countries creates both barriers and opportunities, enabling first-movers to establish dominance in underpenetrated markets. Price differentiation is limited due to high operational costs, pushing firms toward service innovation and customer experience enhancement. Strategic alliances with telecoms and banks are redefining distribution, making partnerships a key differentiator.

KEY MARKET PLAYERS

Some of the noteworthy companies in the African insurance market profiled in this report are

- Progressive Corporation

- Zurich Insurance Group

- HDI V.a.G.

- MetLife Inc.

- Centene Corporation

- State Farm Group

- Elevance Health, Inc.

- AXA S.A.

- Allianz SE

- UnitedHealth Group Incorporated

TOP LEADING PLAYERS IN THE MARKET

- Sanlam is headquartered in South Africa and operates as a pan-African financial services group with a deep-rooted presence across 30 African countries. The company has strategically expanded beyond traditional life insurance into asset management, banking, and digital financial solutions. In 2023, Sanlam launched a continent-wide digital transformation initiative, integrating AI-driven underwriting and customer service automation across its subsidiaries in Kenya, Nigeria, and Ghana. It also intensified its focus on inclusive insurance, introducing low-cost funeral and health microinsurance products via mobile platforms. Sanlam’s partnership with Safaricom in East Africa enabled seamless integration of insurance into M-Pesa transactions, significantly expanding reach among unbanked populations.

- Old Mutual maintains a formidable footprint across Africa, delivering life, short-term, and asset management services in key markets including South Africa, Zimbabwe, Nigeria, and Malawi. The company has prioritized operational restructuring to enhance agility, completing its demerger into four independent entities by 2023 to allow region-specific strategic focus. In 2024, Old Mutual launched a digital-first platform in Nigeria called “OmniLife,” which leverages mobile technology and behavioral analytics to offer personalized life insurance plans. It also strengthened its climate resilience portfolio by underwriting index-based agricultural insurance in partnership with the African Risk Capacity. environments.

- African Insurance Limited, a leading non-life insurer based in Kenya, has expanded its operations across East and Central Africa, offering motor, health, property, and liability insurance. The company has distinguished itself through rapid digital adoption, launching a fully automated claims processing system in 2023 that reduced settlement times from seven days to under 48 hours. In 2024, AIL introduced drone-based risk assessment for commercial property insurance in Uganda and Rwanda, enhancing underwriting accuracy. It also partnered with regional healthcare providers to establish a cashless medical network by improving service delivery for policyholders. AIL’s focus on customer-centric innovation and operational efficiency has enabled it to capture growing demand in the SME and transport sectors. Its commitment to regulatory compliance and transparency has strengthened its reputation as a reliable insurer in fast-evolving markets.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the African insurance market are deploying targeted strategies to expand reach and enhance competitiveness. Digital transformation is a primary focus, with insurers investing in mobile platforms, AI-powered underwriting, and cloud-based policy administration systems to improve efficiency. Strategic partnerships with fintechs and telecom operators enable embedded insurance models, particularly in microinsurance. Companies are also localizing product design to align with regional risk profiles, such as climate-indexed agriculture policies or pay-as-you-go health coverage. Geographic expansion through joint ventures and regulatory compliance in emerging markets like Ethiopia and Sudan is gaining momentum. Additionally, talent development and data infrastructure investments are being prioritized to support long-term scalability and regulatory adherence across diverse jurisdictions.

RECENT MARKET DEVELOPMENTS

- In February 2023, Sanlam launched a digital microinsurance platform across its East African subsidiaries, which is integrating with mobile money providers to offer instant funeral and health coverage, significantly expanding access in rural Kenya and Uganda.

- In June 2023, Old Mutual partnered with the African Risk Capacity to roll out drought-indexed insurance for smallholder farmers in Malawi and Zambia by enhancing its footprint in climate-resilient agricultural insurance.

- In September 2023, African Insurance Limited deployed drone technology for property risk assessment in Rwanda and Tanzania by improving underwriting precision and reducing claims fraud in commercial portfolios.

- In January 2024, Sanlam acquired a 49% stake in Nigeria-based fintech startup Coveriko, strengthening its digital distribution capabilities and access to informal sector customers.

- In March 2024, Old Mutual launched OmniLife, a mobile-first life insurance platform in Nigeria, utilizing behavioral analytics and USSD technology to deliver affordable, customizable policies to low-income urban populations.

MARKET SEGMENTATION

This Africa insurance market research report is segmented and sub-segmented into the following categories.

By Type

- Life Insurance

- General Insurance

By Distribution Channel

- Insurers

- Insurance Brokers and Agencies

- Banks

- Others

By Country

- Sudan

- Egypt

- Kenya

- Ethiopia

- Ghana

- South Africa

- Rest of Africa

Frequently Asked Questions

1. What is the Africa Insurance Market?

The Africa Insurance Market includes the sale and servicing of life and non-life (general) insurance products for individuals and businesses across African countries, aiming to cover risks and provide financial protection

2. Which insurance segment accounts for the largest share in the Africa Insurance Market?

Life insurance holds the largest market share in Africa, driven by demand for family and income protection as well as rising awareness of retirement planning needs

3. Which countries lead the Africa Insurance Market?

South Africa dominates the market, followed by Morocco, Nigeria, Egypt, Kenya, and Algeria, due to greater financial development and regulatory maturity

4. What are the key drivers for growth in the Africa Insurance Market?

Drivers include a growing middle class, financial inclusion initiatives, increased insurance awareness, digital distribution, government policies, and collaborations with banks/fintech

5. What is the current insurance penetration rate in Africa?

Insurance penetration averages around 3% of Africa’s GDP, which is less than half the global average, with significant variance by country (South Africa over 11%, Kenya about 2.2%, Tanzania 0.62%)

6. How is technology transforming the Africa Insurance Market?

Digital platforms, mobile-first solutions, Insurtech startups, automated claims management, and mobile money integration are expanding insurance access and convenience

7. What is microinsurance and what role does it play in Africa?

Microinsurance targets low-income populations with affordable life, health, and agriculture products, helping to close protection gaps and extend financial services

8. Which companies are major players in the Africa Insurance Market?

Top firms include African Life Assurance, Liberty Holdings, Old Mutual Group, Sanlam, Santam, Misr Insurance, and Société Nationale Des Assurances, among others

9. Are non-life insurance categories expanding in Africa?

Yes, property, auto, liability, fire, and health insurance products are seeing rapid growth, especially with greater infrastructure development and regulatory reforms

10. What are the main challenges facing the Africa Insurance Market?

Low insurance awareness, complex regulations, distribution inefficiencies, low per capita income, product innovation gaps, and economic volatility are core challenges.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com