Africa Mobile Money Market Size, Share, Trends & Growth Forecast Report By Technology (USSD, Mobile Wallets, Others), Business Model (Mobile Led Model, Bank Led Model), Transaction Type (Peer to Peer, Bill Payments, Airtime Top-ups, Others), and Country (Sudan, Egypt, Kenya, Ethiopia, Ghana, South Africa, Rest of Africa) – Industry Analysis, 2026 to 2034

Africa Mobile Money Market Size

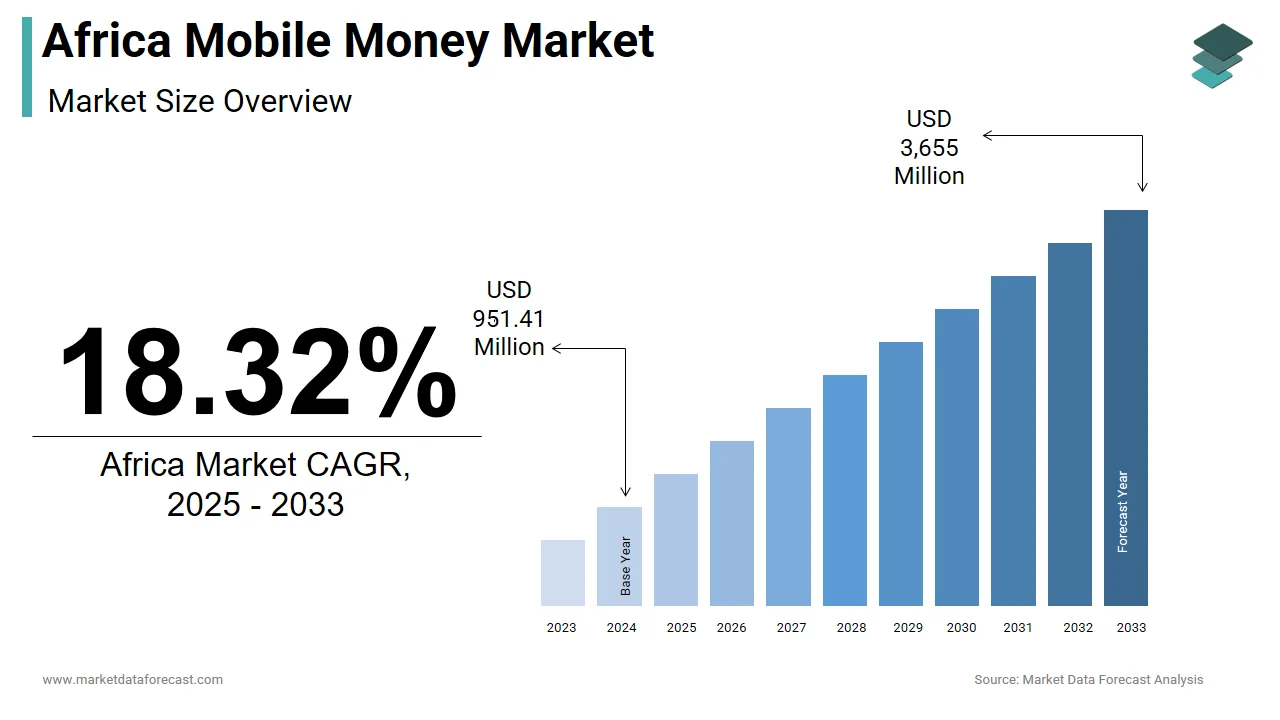

The African mobile money market was valued at USD 951.41 million in 2025, is estimated to reach USD 1,126 million in 2026, and is projected to reach USD 4,324 million by 2034, growing at a CAGR of 18.32% from 2026 to 2034.

Mobile money refers to the ecosystem of digital financial services that enable individuals to conduct monetary transactions via mobile devices, particularly in environments with limited access to traditional banking infrastructure. As of 2023, over 709 million registered mobile money accounts existed across Sub-Saharan Africa, according to the Global System for Mobile Communications Association (GSMA), reflecting the profound integration of mobile-based financial tools into daily economic life. In countries like Uganda and Tanzania, mobile money penetration exceeds 60% of the adult population, as per the World Bank’s Global Findex Database. The sector has become a critical conduit for salary disbursements, utility payments, and cross-border remittances, especially in rural areas where only 43% of adults have access to formal bank branches, as per the Alliance for Financial Inclusion. These dynamics underscore mobile money’s role as a foundational layer of financial inclusion across the continent.

MARKET DRIVERS

High Unbanked Population and Expanding Financial Inclusion Initiatives

The vast unbanked population is a primary driver of the African mobile money market. It stood at approximately 350 million adults in Sub-Saharan Africa as of 2023, according to the World Bank’s Global Findex. Traditional banking infrastructure remains sparse, with only one bank branch per 100,000 people in nations like Malawi and Niger, as per the International Finance Corporation. Mobile money circumvents this gap by enabling account access through basic feature phones, requiring neither internet connectivity nor physical proximity to financial institutions. In Kenya, where mobile money was pioneered through M-Pesa, over 82% of adults now use digital financial services, as per the Central Bank of Kenya. Governments across the region, including those in Ghana and Rwanda, have implemented national financial inclusion strategies that explicitly promote mobile wallets as a primary access tool, further accelerating adoption and embedding mobile money into the socioeconomic fabric.

Proliferation of Mobile Network Coverage and Affordable Handsets

The rapid expansion of mobile network infrastructure has been instrumental in scaling mobile money adoption across Africa. As of 2023, 84% of the continent’s population lived within areas covered by a 3G or 4G signal, according to the International Telecommunication Union (ITU). This connectivity growth has been complemented by the availability of low-cost smartphones. Increased handset affordability has enabled broader demographic access, particularly among rural populations and low-income earners. In Senegal, mobile money transaction volume surged by 41% between 2022 and 2023 following a national rollout of 4G in secondary towns, as per the Central Bank of West African States. This synergy between network reach and device accessibility continues to lower entry barriers, making mobile money the default financial interface for millions.

MARKET RESTRAINTS

Fragmented Regulatory Frameworks Across Jurisdictions

One of the most significant impediments to the African mobile money market is the lack of harmonized regulatory policies across national borders. Also, only some of the 54 African nations have fully aligned their digital financial regulations with the Financial Action Task Force (FATF) standards on anti-money laundering. This fragmentation complicates cross-border interoperability and discourages regional scalability. For instance, mobile money users in the East African Community cannot seamlessly transfer funds between Kenya’s M-Pesa and Tanzania’s Tigo Pesa. Furthermore, sudden policy shifts, such as Uganda’s 2018 mobile money tax, which led to a 43% drop in transaction volume within six months, according to the Bank of Uganda, demonstrate the vulnerability of the sector to inconsistent governance, undermining long-term stability and investment confidence.

Persistent Digital Literacy Gaps in Rural and Elderly Populations

Despite technological advancements, low levels of digital literacy remain a critical barrier to mobile money adoption, particularly among older adults and rural communities. According to UNESCO, only a limited share of adults in rural Mali and Burkina Faso can perform basic mobile-based tasks such as sending a text or navigating a menu. This deficiency limits the ability of users to independently operate mobile money platforms, often necessitating reliance on agents, which increases transaction costs and risks of fraud. In Nigeria, a notable share of non-users cited lack of understanding as the primary reason for not adopting mobile wallets. Additionally, a 2023 study by the African Development Bank revealed that women in rural areas are 30% less likely than men to use mobile money due to lower literacy and phone ownership rates, further constraining market inclusivity.

MARKET OPPORTUNITIES

Integration with Agricultural and Micro-Enterprise Value Chains

Mobile money presents a transformative opportunity to integrate informal economic sectors, particularly agriculture, into formal financial ecosystems. As per the Food and Agriculture Organization (FAO), smallholder farmers constitute over 60% of Africa’s workforce, yet fewer than 15% receive digital payments for their produce. Mobile wallets are increasingly being leveraged to disburse input subsidies, facilitate crop sales, and deliver microloans. In Zambia, the Electronic Voucher and Input Delivery System (e-VIPS) enabled a substantial number of farmers to purchase seeds and fertilizer via mobile money. Similarly, platforms like Agri-wallet in Kenya allow farmers to save, borrow, and insure harvests through mobile interfaces. These integrations not only enhance financial resilience but also create recurring transaction flows that deepen user engagement and platform stickiness.

Expansion of Mobile Money into Cross-Border Remittances and Regional Trade

The African mobile money market is poised to revolutionize cross-border remittances. Traditional remittance channels remain costly, with average fees exceeding 8%, but mobile-based solutions offer a cheaper, faster alternative. Additionally, regional trade is increasingly relying on mobile wallets for B2B micro-payments, especially among informal traders. Such developments signal a shift toward a unified digital financial infrastructure across the continent.

MARKET CHALLENGES

Cybersecurity Threats and Rising Mobile-Based Financial Fraud

The rapid growth of mobile money has attracted sophisticated cybercriminal activity, posing a growing threat to user trust and system integrity. According to INTERPOL’s Cybercrime in Africa report, mobile financial fraud incidents increased across West and East Africa compared to the previous year. In Nigeria, the Economic and Financial Crimes Commission recorded a notable number of cases of SIM-swap fraud targeting mobile money. Many users lack awareness of phishing tactics, and weak authentication protocols in some platforms exacerbate vulnerabilities. As transaction volumes grow, the absence of continent-wide cybersecurity standards and real-time fraud monitoring systems presents a systemic risk to the sector’s sustainability.

Liquidity Management and Network Sustainability

A critical operational challenge facing the African mobile money market is the persistent issue of agent liquidity imbalances, where agents lack sufficient cash for withdrawals or float for deposits. This disrupts service availability and diminishes user confidence, particularly in remote areas. The problem is compounded by inefficient cash-in/cash-out logistics and limited access to banking services for agents. Without scalable liquidity solutions, such as interoperable float exchanges or agent banking partnerships, the last-mile delivery model remains fragile and economically unsustainable.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Business Model, Transaction Type, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Sudan, Egypt, Kenya, Ethiopia, Ghana, South Africa, Rest of Africa |

| Market Leaders Profiled | MTN, Orange, M-Pesa, Tigo-Pesa, Safaricom PLC, Airtel Money, and others. |

SEGMENTAL ANALYSIS

By Technology Insights

The USSD (Unstructured Supplementary Service Data) segment remained the dominant technology in the African mobile money market by capturing 63.5% of total transaction volume in 2024. This dominance is sustained by its compatibility with basic feature phones. Unlike internet-dependent applications, USSD operates on 2G networks, ensuring functionality in remote and low-connectivity regions. In countries like Niger and Malawi, where smartphone penetration remains low, USSD is the primary interface for financial transactions. As per the Central Bank of West African States, 89% of mobile money interactions in the WAEMU region occur via USSD, underlining its critical role in financial inclusion. Its simplicity, low data cost, and universal carrier support make it the most accessible digital financial channel for rural and low-income populations.

The mobile wallets segment is expanding at a CAGR of 16.8% from 2026 to 2034. It is driven by rising smartphone adoption and data affordability. As of 2023, the average cost of 1GB of mobile data in Africa had declined to $1.85, a 42% reduction from 2020, as per the Alliance for Affordable Internet. This has enabled greater uptake of app-based wallets such as M-Pesa’s smartphone interface, Airtel Money, and MTN Mobile Money. In Kenya, mobile wallet transactions grew year-on-year, with smartphone-based transfers now accounting for a notable share of all digital payments. These platforms offer enhanced features, including savings accounts, credit scoring, and merchant payments, increasing user engagement. Additionally, integration with e-commerce platforms and QR-based payments is accelerating adoption among urban consumers and small businesses, positioning mobile wallets as the future core of digital finance.

By Business Model Insights

The mobile-led model segment holds a commanding share of the African mobile money market in 2025. This model, pioneered by Safaricom’s M-Pesa in Kenya, enables telcos to issue e-money, manage agent networks, and facilitate transactions without direct banking intermediation. Its success stems from the extensive reach of mobile networks, covering 94% of the African population, as per the International Telecommunication U, compared to the limited footprint of bank branches. The agility of telecom operators in deploying agent networks, coupled with their customer-centric design, has allowed them to dominate last-mile financial delivery, particularly in rural and informal economies.

The bank-led mobile money model is expanding at a CAGR of 10.3% during the forecast period. This growth is driven by increasing regulatory support for bank-fintech partnerships and the formalization of digital finance ecosystems. In Nigeria, the Central Bank’s licensing of Payment Service Banks (PSBs) in 2021 enabled banks like Polaris Bank and FCMB to offer mobile wallets with full interoperability. The integration of mobile money with core banking systems allows for seamless access to credit, savings, and insurance products, enhancing financial depth. Additionally, the rise of open banking frameworks in countries like South Africa and Kenya is enabling banks to leverage telco distribution while maintaining compliance and risk control, fueling the model’s resurgence.

By Transaction Type Insights

The Peer-to-peer (P2P) transactions segment led the Africa mobile money market by representing 52.5% of total transaction volume in 2024. This dominance is credited to the continent’s reliance on informal remittance networks, where individuals transfer funds to family members in rural areas. In Uganda, P2P transfers accounted for $28.6 billion in transaction value in 2023, a 29% increase from the previous year, as per the Bank of Uganda. The absence of formal banking channels makes mobile money the preferred method for personal fund transfers, especially during seasonal migrations and crises. The immediacy, low cost, and ease of use further reinforce its entrenched position in daily financial behavior.

The bill payments segment is growing at a CAGR of 15.1% during the forecast period and is driven by urbanization and digithe tization of public utilities. Across major African cities, governments and service providers are migrating to electronic billing systems to reduce revenue leakage and improve efficiency. Similarly, Kenya Power saw an increase in on-time electricity payments following the expansion of its mobile payment gateway. Additionally, the proliferation of digital TV, the internet, and municipal services has expanded the bill payment ecosystem. As urban populations grow, demand for automated, mobile-based utility settlements is accelerating, making this segment a key growth engine.

COUNTRY-LEVEL ANALYSIS

Kenya Mobile Money Market Insights

Kenya stood as the trailblazer in Africa’s mobile money landscape by commanding 24.7% of the regional transaction value in 2024. The country’s dominance is anchored in the success of M-Pesa, which processes over $50 billion in transactions annually and serves 31 million active users. Mobile money penetration exceeds 82% of the adult population, the highest in Africa, according to the World Bank’s Global Findex. Kenya’s regulatory environment has been instrumental, with the Central Bank adopting a sandbox approach that allowed rapid innovation while managing risk. The integration of mobile money with microfinance, agriculture, and health sectors has deepened its utility.

Tanzania Mobile Money Market Insights

Tanzania is also a key player in the African mobile money market. The country has experienced exponential growth in mobile money usage, with transaction value reaching $62 billion in 2023, a 33% year-on-year increase. This surge is fueled by a dense agent network and widespread adoption in rural trade. The government’s push for digital tax collection through mobile platforms has further institutionalized usage. Moreover, Tanzania’s interoperability framework, launched in 2021, allows seamless transfers between Vodacom’s M-Pesa, Airtel Money, and Tigo Pesa, enhancing user convenience. These factors have solidified Tanzania’s position as a high-volume, high-utility mobile money economy.

Uganda Mobile Money Market Insights

Uganda is emerging as one of the fastest-maturing ecosystems. With over 28 million registered accounts and a transaction value of $32 billion in 2023, mobile money has become integral to both urban and rural economies. The National Payment System Act of 2020 strengthened regulatory oversight, boosting consumer confidence. Mobile money is widely used for agricultural payments. Additionally, the rollout of 4G in secondary towns has enhanced app-based wallet usage. The country’s low average transaction fee of 1.2%, among the lowest in East Africa, has further stimulated adoption, driving sustained growth.

Ghana Mobile Money Market Insights

Ghana accounts for a notable share of the African mobile money market. The country’s growth is largely propelled by state-led digital transformation initiatives, including the Ghana.Gov platform, which integrates mobile money for tax payments, utility bills, and social disbursements. Over 80% of government-to-person payments are now made digitally, as per the Ministry of Finance. The introduction of the Mobile Money Interoperability Platform in 2021 enabled cross-network transfers, increasing transaction efficiency. Smartphone penetration, now at 58%, is accelerating the shift from USSD to app-based wallets.

COMPETITIVE LANDSCAPE

The African mobile money market features intense competition shaped by telecom giants, fintech innovators, and emerging bank-led platforms. Incumbents like Safaricom, MTN, and Airtel dominate through expansive agent networks and brand trust, while new entrants leverage agile technology to offer specialized services. Competition is increasingly shifting from transaction volume to value-added features such as credit access, savings tools, and merchant ecosystems. Regulatory divergence across countries creates both entry barriers and differentiation opportunities. Interoperability remains a contested frontier, with some nations mandating cross-platform transfers while others lag. The rise of super apps integrating payments, commerce, and identity is redefining competitive dynamics. Ultimately, success hinges on technological resilience, last-mile reach, and the ability to align with national financial inclusion objectives in a highly fragmented yet rapidly digitizing landscape.

KEY MARKET PLAYERS

Some of the noteworthy companies in the African mobile money market profiled in this report are

- MTN

- Orange

- M-Pesa

- Tigo-Pesa

- Safaricom PLC

- Airtel Money

TOP LEADING PLAYERS IN THE MARKET

- Safaricom, the Kenyan telecommunications leader, pioneered M-Pesa in 2007, transforming mobile money into a foundational financial infrastructure across East Africa. The company has continuously evolved its platform by integrating lending, savings, insurance, and merchant payment solutions, enhancing user engagement beyond basic transfers. It has also expanded M-Pesa’s utility into cross-border remittances, enabling instant transfers to Uganda, Tanzania, and Rwanda. The company strengthened its technological backbone by partnering with Vodafone and Visa to enhance transaction security and interoperability. Furthermore, Safaricom’s investment in fiber-optic networks and cloud-based services has improved platform reliability, reinforcing trust and scalability across high-traffic urban and remote rural regions.

- MTN Group operates one of the most extensive mobile money ecosystems in Africa, active in over 18 countries, including Nigeria, Ghana, and Côte d’Ivoire. The company has prioritized interoperability, launching cross-network transactions in key markets to break down service silos. It also forged strategic alliances with financial institutions such as Standard Bank and Ecobank to expand access to credit and savings products. MTN’s collaboration with the Bill & Melinda Gates Foundation supported agent network digitization, improving liquidity management in rural areas. Additionally, the company has invested in AI-driven fraud detection systems to enhance transaction security. These initiatives reflect MTN’s commitment to building a seamless, secure, and inclusive digital financial ecosystem across the continent.

- Airtel Africa has strategically expanded its mobile money footprint across 14 African nations, with a strong presence in Nigeria, Kenya, and Zambia. The company has focused on enhancing platform functionality by introducing Airtel Money Pay, a QR-based merchant payment system that supports small businesses. It also integrated its platform with government digital initiatives, facilitating the disbursement of social welfare funds in Uganda and Zambia. Airtel’s investment in USSD optimization has improved transaction speed and reliability, particularly in low-bandwidth environments. The company has further strengthened its agent network by digitizing float management and introducing real-time monitoring tools. These efforts have positioned Airtel as a key enabler of digital financial inclusion, especially in underserved and rural communities.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the African mobile money market are deploying interoperability, digital platform integration, agent network digitization, strategic partnerships with financial institutions, and expansion into value-added services such as microloans, insurance, and merchant payments to consolidate their market presence. Companies are investing in AI-driven fraud detection, enhancing cybersecurity, and leveraging data analytics for credit scoring. Regulatory compliance and alignment with national digitalization agendas are prioritized to ensure scalability. Telecom operators are also upgrading legacy USSD systems while simultaneously promoting smartphone-based wallets to capture evolving user preferences. These strategies collectively aim to deepen user engagement, improve service reliability, and expand financial inclusion across diverse demographic and geographic segments.

RECENT MARKET DEVELOPMENTS

- In February 2023, Safaricom expanded Fuliza overdraft services to include small business owners in Kenya, enabling credit access for over two million enterprises and deepening financial inclusion.

- In May 2023, MTN Group launched the Mobile Money Super App in Uganda, integrating payments, banking, and e-commerce to enhance user engagement and transaction frequency.

- In July 2023, Airtel Africa partnered with Mastercard to introduce prepaid virtual cards in Nigeria, allowing mobile wallet users to conduct online and international transactions securely.

- In October 2023, MTN achieved full interoperability between its mobile money platform and rival networks in Ghana, facilitating seamless cross-provider transfers.

- In January 2024, Safaricom integrated M-Pesa with Kenya’s National Hospital Insurance Fund, enabling digital premium payments and claims processing for millions of citizens.

MARKET SEGMENTATION

This Africa mobile money market research report is segmented and sub-segmented into the following categories.

By Technology

- USSD

- Mobile Wallets

- Others

By Business Model

- Mobile Led Model

- Bank Led Model

By Transaction Type

- Peer to Peer

- Bill Payments

- Airtime Top-ups

- Others

By Country

- Sudan

- Egypt

- Kenya

- Ethiopia

- Ghana

- South Africa

- Rest of Africa

Frequently Asked Questions

1. Who are the leading players in the Africa Mobile Money Market?

Major providers include M-Pesa (Safaricom/Vodacom), MTN MoMo, Airtel Money, Orange Money, Tigo-Pesa, and PalmPay, as well as banks, fintechs, and super-app platforms.

2. Which regions lead in mobile money adoption within Africa?

East Africa (notably Kenya, Tanzania), West Africa (Ghana, Nigeria), and North Africa (Egypt, Morocco) are leading, with Uganda also showing high transaction intensity

3. What are the key drivers of growth in the Africa Mobile Money Market?

Drivers include rising smartphone penetration, expanding agent networks, government support for financial inclusion, growing e-commerce, cross-border remittances, and digital innovation

4. How is mobile money contributing to Africa’s economy?

Mobile money added roughly $190 billion to sub-Saharan Africa’s GDP in 2023 and supports economic empowerment for millions through business payments, remittance flows, and digital services

5. What services are offered by mobile money in Africa?

Beyond money transfers, offerings now include loans and credit, insurance, merchant payments, pay-as-you-go utilities, and integration with e-commerce and digital lending services

6. How is cross-border payment handled in the Africa Mobile Money Market?

Interoperability improvements and regulatory harmonization are allowing mobile money users to send and receive cross-border remittances across multiple African countries

7. How secure is the Africa Mobile Money Market?

Major platforms are strengthening user authentication, deploying multi-factor security, and employing AI-driven fraud prevention, with ongoing regulatory focus on data privacy and consumer safety

8. What are the main challenges for mobile money in Africa?

Challenges include infrastructure gaps, regulatory fragmentation, limited interoperability, fraud risks, and the persistent gender gap in account ownership

9. What role does mobile money play in rural Africa?

Mobile money is a lifeline for rural populations, providing access to formal financial services where banks are scarce, promoting economic inclusion and resilience.

10. How does mobile money support small businesses in Africa?

It enables SMBs to easily collect digital payments, manage working capital, access microloans and insurance, and participate in the regional digital economy.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com