Africa Used Car Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By Vehicle, Vendor, And Country (Sudan, Egypt, Kenya, Ethiopia, South Africa, Rest of Africa), Industry Analysis From (2026 to 2034)

Africa Used Car Market Size

The Africa Used Cars market size was valued at USD 112.58 billion in 2025 and is anticipated to reach USD 120.12 billion in 2026 to reach from USD 201.81 billion by 2034, growing at a CAGR of 6.70% during the forecast period from 2026 to 2034.

Used cars are second-hand vehicles that include a wide range of cars from nearly new to those several years old. According to the United Nations Environment Programme (UNEP), over 80% of vehicles imported into Sub-Saharan Africa in 2022 were used units, which shows the dominance of the used vehicle segment in the region’s automotive market. Affordability and the availability of dependable models with low mileage have made nations like Kenya, Ghana, Nigeria, and Tanzania important import centers. Additionally, digital transformation is reshaping the sector, with online platforms facilitating vehicle listings, financing, and verification processes.

MARKET DRIVERS

Affordability and Cost-Effectiveness Compared to New Vehicles

The price difference between new and used cars, which makes them affordable for a wider range of buyers, is one of the main factors propelling the African used car market. Used cars, particularly those sourced from Japan and South Korea, offer a viable alternative due to their relatively low prices and high reliability. Furthermore, lending packages specifically designed for used car purchasers are becoming more widely available from financial institutions and fintech businesses, which further improves affordability. In Kenya, banks such as Equity Bank and Cooperative Bank expanded their auto loan portfolios to include used vehicles, which contributes to increased transaction volumes. This affordability factor is especially crucial in urban centers where personal mobility is essential for employment and business activities. Used cars are a crucial alternative for millions of Africans looking for autonomous mobility options, as public transportation networks are frequently insufficient or unreliable.

High Demand for Reliable Japanese-Built Vehicles

The strong desire for Japanese-built cars, which are renowned for their dependability, fuel efficiency, and simplicity of maintenance, is another important factor propelling the used car market in Africa. According to the Japan Automobile Manufacturers Association (JAMA), Africa accounted for nearly 15% of all used car exports from Japan in 2023, with Kenya, Nigeria, and Tanzania being he top destinations. Japanese automakers such as Toyota, Honda, and Nissan dominate the used car imports due to their reputation for longevity and spare parts availability. For instance, according to the Kenya Association of Vehicle Importers and Distributors (KAVID) in 2023, Japanese models account for more than 70% of used car sales in Nairobi. Additionally, these vehicles often come with well-documented service histories and low mileage due to Japan’s strict inspection and maintenance standards. This transparency enhances buyer confidence, especially among first-time car owners. Furthermore, the presence of established after-sales networks across major African cities ensures that maintenance and repairs remain accessible and cost-effective.

MARKET RESTRAINTS

Regulatory Restrictions and Import Policies

Several countries have tightened import laws to reduce the flow of older, less environmentally friendly automobiles, which is one of the main factors impacting the African used car market. According to the United Nations Environment Programme (UNEP), at least ten African countries implemented stricter vehicle import policies between 2020 and 2023, which include minimum age limits and emissions standards. For example, Kenya introduced a policy in 2021 restricting the importation of vehicles older than eight years, while Rwanda imposed similar rules to promote cleaner and safer transportation. These measures have led to a reduction in the supply of budget-friendly models, which had previously dominated the market, particularly among middle-income buyers. Additionally, some countries have introduced higher import duties on older vehicles to discourage their entry. Certain used car categories now cost more in Uganda because customs officers impose various tariff rates depending on the engine size and model year.

Poor Road Infrastructure and Maintenance Challenges

Inadequate road infrastructure remains a major challenge for the African used car market, as poor road conditions increase wear and tear on vehicles, which reduces their lifespan and resale value. According to the World Bank’s 2023 Africa Transport Outlook, less than 40% of Africa’s primary rural roads were paved, and urban roads suffer from chronic potholes and traffic congestion. Potential purchasers have been discouraged from investing in private transportation in nations like Ethiopia and Malawi due to the increased maintenance expenses associated with unpaved roads. According to a 2022 International Road Federation research, truck drivers in Zambia had to pay twice as much for repairs as those in better-maintained areas. Moreover, fuel price volatility and inconsistent power supply affect vehicle usage patterns. In Zimbabwe and Angola, recurrent fuel shortages have disrupted transport operations and reduced vehicle utilization, which leads to declining demand for used cars in some regions.

MARKET OPPORTUNITIES

Growth of Online Used Car Platforms and Digital Marketplaces

The quick growth of digital markets and online platforms that simplify financing, verification, and automobile buying is posing new opportunities for the growth of the African used car market. According to Disrupt Africa, used car e-commerce platforms in Nigeria and Kenya recorded a 35% surge in user engagement in 2023, which reflects growing consumer confidence in digital transactions. Startups such as Cars45 in Nigeria, Dummee in Ghana, and Autochek in East Africa have introduced certified pre-owned programs, vehicle inspections, and online financing solutions. These platforms also integrate mobile payment systems, which allow buyers to make secure transactions without visiting physical dealerships. Additionally, digital technologies improve liquidity and pricing efficiency by allowing sellers to access consumers outside of local marketplaces. The region's increasing smartphone penetration and internet availability contribute to the market's expansion.

Expansion of Financial Services and Leasing Models

The increasing availability of financial services designed for used car buyers presents a significant growth opportunity for the African used car market. Banks and non-bank lenders are introducing flexible financing options such as short-term loans, hire purchase agreements, and micro-leasing schemes designed for used car acquisition. Additionally, peer-to-peer lending platforms and mobile-based credit scoring systems are enabling first-time buyers to access vehicle finance without traditional collateral requirements. Startups like Migo and Branch in Nigeria use smartphone data to assess creditworthiness and approve small loans instantly.

MARKET CHALLENGES

Regulatory Fragmentation Across Regional Markets

The lack of harmonized regulations governing vehicle import safety requirements, taxes, and environmental compliance is acting as a barrier to the growth of the used car market in Africa. Africa comprises diverse legal frameworks that complicate cross-border trade and distribution. According to the African Union, as of 2023, only 12 out of 54 member states had fully aligned their automotive import regulations with the African Continental Free Trade Area (AfCFTA) guidelines. This inconsistency creates arbitrage opportunities but complicates logistics and distribution planning for automakers and distributors. Neighbouring nations like Uganda and Tanzania permit cars up to 15 years old, while Kenya has severe age restrictions on imported second-hand cars, which limit them to eight years old. These discrepancies hinder market integration and customer access by raising operational complexity and driving up vehicle prices. Customs procedures also differ widely, with some nations imposing high tariffs on certain vehicle types.

Inconsistent Power Supply and Fuel Distribution Networks

The unreliable power supply and inconsistent fuel distribution infrastructure are negatively impacting the growth of the African used car market. Many African countries still grapple with frequent electricity outages, which impact vehicle servicing centers, digital platforms, and even basic operations like lighting in used car lots. Fuel availability and pricing volatility further exacerbate the issue. Fuel shortages are common in countries like Zimbabwe and Angola, which interfere with transportation and deter private car ownership. According to the African Energy Chamber, diesel prices in Nigeria surged by 34% in 2023 following subsidy reforms, which directly impact commercial transport operators and fleet owners. Moreover, fuel distribution infrastructure remains underdeveloped in rural areas. Automobile manufacturers have operational inefficiencies in the absence of dependable electricity and fuel supply networks, which raises expenses and reduces customer trust in car ownership.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.70% |

| Segments Covered | By Vehicle, Vendor, And By Region |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Sudan, Egypt, Kenya, Ethiopia, South Africa, Rest of Africa |

| Market Leaders Profiled | Al-Futtaim Group, Abdul Latif Jameel Motors, Yallamotor, AutoTrader South Africa, Cars 4 Africa, Carzami, Autochek Africa, AutoTager, Cars45, KIFAL Auto, PeachCars, Planet42, Sylndr, Mogo Auto LTD, Schulenburg Motors, Euroken Automobiles Ltd, Global Cars Trading FZ LLC, cars2africa, Abi Sayara, CardealerAfricaca, We Buy Cars (Pty) Ltd, OLX Group, CarMax East Africa Ltd. |

SEGMENTAL ANALYSIS

By Vehicle Insights

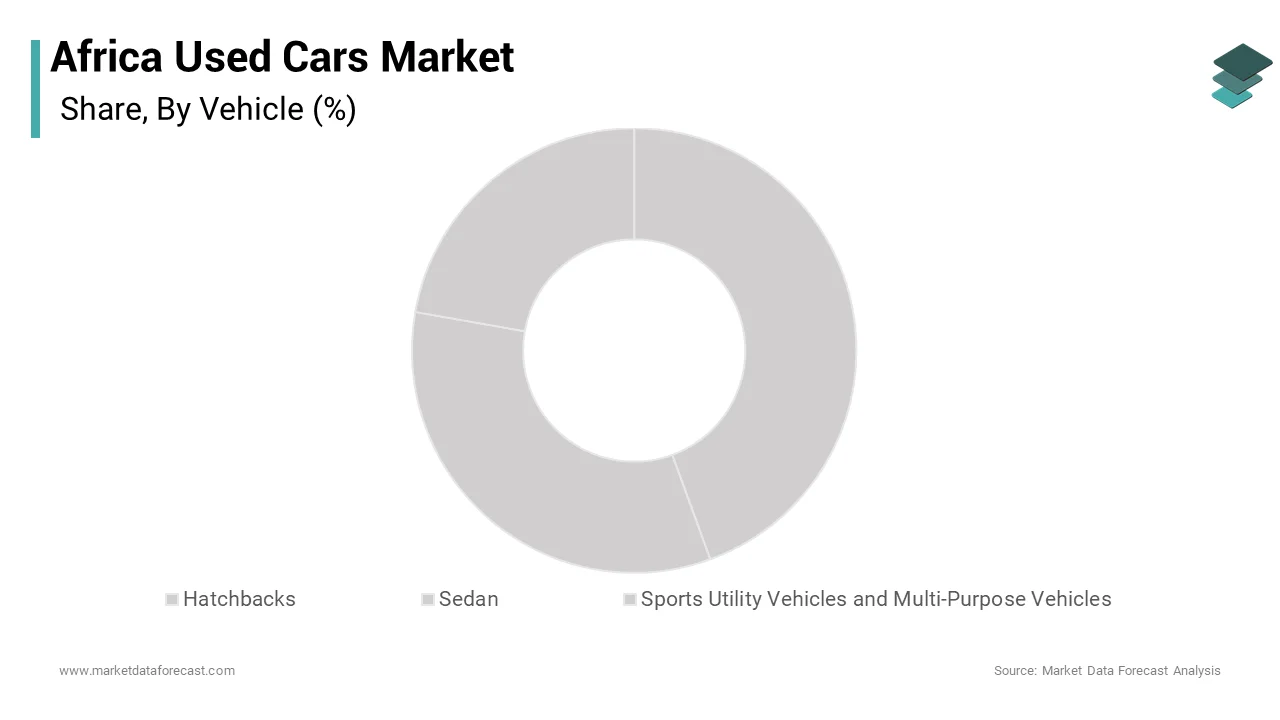

The hatchback segment dominated the African used car market by capturing 48.4% of the market share in 2025. The strong preference for Japanese-built hatchback models, especially the Suzuki Swift, Honda Fit, and Toyota Vitz, which are renowned for their dependability and ease of maintenance, is one of the primary factors driving this trend. Additionally, urbanization and traffic congestion in major African cities such as Nairobi, Lagos, and Accra make hatchbacks more practical compared to larger vehicles. Their compact size makes them perfect for daily travel since it makes navigating through constrained parking spaces and narrow streets simpler. Moreover, financing institutions are increasingly offering auto loan products tailored to hatchback purchases, which enables middle-income earners to access personal transport without excessive financial burden.

The Sport Utility Vehicles (SUVs) and Multi-Purpose Vehicles (MPVs) segment is predicted to witness a CAGR of 7.9% during the forecast period due to shifting consumer preferences toward larger, family-friendly, and rugged vehicles that can navigate both urban and rural road conditions. The growing need for adaptable cars that can handle a variety of terrains, particularly in nations with inadequate road infrastructure, is a major facilitator. In Ethiopia and Tanzania, SUVs such as the Toyota Land Cruiser and Mitsubishi Pajero have gained popularity among business owners and government officials who require durable transportation across unpaved roads. Furthermore, the expansion of ride-hailing services and commercial transport operations has boosted MPV adoption. Companies like Bolt and Uber rely heavily on models such as the Toyota Ipsum and Nissan Serena for fleet expansion, particularly in Nigeria and Ghana, where intercity travel demand is high. Additionally, improved income levels and lifestyle aspirations are driving middle-class consumers toward premium-looking used SUVs.

By Vendor Insights

The unorganized vendor segment led the African used car market share in 2025 with informal dealers, roadside sellers, independent importers, and small-scale traders who operate outside formal regulatory structures but play a major role in vehicle accessibility. The shortage of organized dealership networks in many regions of the continent, especially in rural and peri-urban areas, is one of the primary causes of this segment's domination. According to the African Microfinance Network, over 75% of used cars in West Africa are sold through informal channels, where prices are often lower than in regulated markets. Additionally, consumers prefer the flexibility and negotiation power offered by unregulated vendors, which allows them to secure better deals without the overhead costs associated with official dealerships. In Nigeria, for instance, buyers frequently bypass certified dealerships in favor of independent sellers who offer lower prices and minimal documentation requirements. Moreover, limited access to formal credit and vehicle financing options reinforces the strength of the informal sector. These vendors often provide flexible payment plans or even barter-based transactions, appealing to low-income buyers who may not qualify for bank loans.

The organized vendor segment is predicted to witness a CAGR of 6.2% from 2025 to 2033. Growing customer confidence in official purchase channels, more knowledge of car history and quality assurance, and overall economic development are all factors contributing to this expansion. The growth of fintech-enabled finance options and internet used car marketplaces, especially in South Africa, Kenya, and Nigeria, is one of the main factors. Startups such as Cars45, Dummee, and Autochek introduced vehicle inspection, certification, and mobile-based payment systems that enhance buyer trust and transparency. Additionally, government initiatives aimed at curbing illegal imports and promoting standardized vehicle inspections are encouraging consumers to shift toward organized vendors. In Kenya, the introduction of mandatory pre-shipment inspections under the East African Shipment Inspection Scheme (EASIS) improved vehicle quality standards, which reinforce buyer confidence in certified dealers. Moreover, financial institutions are expanding partnerships with organized vendors to offer structured auto loans and leasing programs, which make it easier for consumers to purchase verified used cars.

COUNTRY-LEVEL ANALYSIS

South Africa Used Cars Market Analysis

South Africa was the top performer in the African used car market and accounted for 28.4% of the market share in 2025. The continent's most established automobile market is still supported by a strong financial system, distribution network, and regulatory environment. The nation's advanced financial structure, which makes it easier for customers to obtain auto finance than in other African countries, is one of the main motivators. Additionally, local production and export-import dynamics contribute significantly to the used car supply chain. According to the National Association of Automobile Manufacturers of South Africa (Naamsa), more than 150,000 old cars were exported in 2023, with Namibia, Botswana, and Lesotho being the main purchasers. Government incentives are also influencing forecasts for the future, such as tax rebates for EV makers and customs easing for regional exports.

Egypt Used Cars Market Analysis

Egypt was positioned second with 14.7% the African used car market share in 2025. Egypt is well-positioned as a major hub in North Africa, due to its sizable population, significant commercial connections, and rising domestic demand for reasonably priced transportation. The development of government-backed import substitution programs, which are intended to increase local assembly operations and lessen dependency on imported new cars, is one of the primary drivers of growth. According to the Cairo Chamber of Commerce, the Egyptian Ministry of Industry announced additional incentives in 2023 for automakers establishing assembly factories, which resulted in a 10% rise in local sales of cars. Additionally, economic reforms and currency devaluation have made locally assembled and imported used cars more attractive to middle-income households. As per the Central Bank of Egypt, auto financing approvals rose by 12% in 2022, which makes car ownership more accessible.

Nigeria Used Cars Market Analysis

Nigeria's used car market is gaining momentum due to a large and youthful population, increasing urbanization, and rising reliance on private transport. The Federal Road Safety Corps reports that over 230,000 secondhand cars entered the nation in 2022, which makes it one of the main growth drivers. Lagos, Abuja, and Port Harcourt have seen a surge in demand for affordable transportation solutions, particularly among small businesses and self-employed individuals. Additionally, the Nigerian government launched the Automotive Industry Development Plan (AIDP) in 2023, which offers tax exemptions for local assembly plants. Nigeria's large customer base and continuous regulatory changes suggest that the used car market has the opportunity to grow in the long run, despite these obstacles.

Morocco Used Cars Market Analysis

Morocco is gaining huge traction with the highest CAGR during the forecast period. Morocco, which serves as a major entry point between Europe and Africa, has established a flourishing automotive sector that draws foreign direct investment (FDI) and eases international commerce. The "Moroccan Automotive Industry Strategy 2030" and other industry upgrading initiatives are major growth drivers. Major players like Renault and Stellantis have established production facilities in Tangier and Casablanca, which utilize Morocco’s strategic location and competitive labor costs to serve both European and Sub-Saharan markets. Infrastructure development and export-oriented policies continue to enhance Morocco’s competitiveness. The government’s focus on electric mobility and green manufacturing is also paving the way for sustainable growth, which makes Morocco a pivotal player in North Africa’s evolving automotive market.

Kenya Used Cars Market Analysis

Kenya's used car market is likely to have significant growth opportunities in the coming years. Kenya is a logistics and distribution hub and one of the economic hubs of the area, which fuels demand for both passenger and commercial cars. The rise of ride-hailing and shared mobility platforms like Uber, Bolt, and Little Cab is a significant growth driver. According to the Kenya Revenue Authority (KRA), used vehicle imports increased by 13% in 2022, with over 120,000 units entering the country, primarily from Japan and the UAE. Additionally, urbanization and improved access to credit have boosted individual car ownership. According to the Central Bank of Kenya, commercial banks increased the size of their car loan portfolios in 2023, with vehicle finance disbursements increasing by 9%. The Standard Gauge Railway and Nairobi Expressway are two examples of infrastructure development that have increased demand for commercial transportation. According to the Kenya Association of Manufacturers (KAM), logistics companies added over 5,000 new trucks in 2022, which enhances freight efficiency.

COMPETITIVE LANDSCAPE

The competition in the African used car market is intensifying as both local and international players seek to capitalize on growing demand driven by affordability, urbanization, and changing consumer preferences. Established multinational brands and exporters continue to dominate due to their brand recognition, consistent vehicle supply, and strong after-sales support systems. These organizations have an advantage in terms of dependability and size due to existing distribution networks and alliances with local importers. Domestic companies and online entrepreneurs are also gaining popularity by providing creative answers to persistent problems, including finance, logistics, and car verification. Online platforms like Cars45 and Autochek have introduced structured processes that bring transparency and trust into a traditionally fragmented and informal market. Global venture capital companies are showing interest in Africa's changing automotive sector by investing in these innovators. Regulatory reforms, taxation policies, and infrastructure development also play a role in shaping competitive dynamics. Governments are pushing for environmental compliance and formalization, and businesses that can manage these challenges while keeping costs low are becoming leaders in this quickly transforming sector.

KEY MARKET PLAYERS

These are the market players that are dominating the African used car market.

- Al-Futtaim Group

- Abdul Latif Jameel Motors

- Toyota Motor Corporation (Japan)

- Yallamotor

- AutoTrader South Africa

- Cars 4 Africa

- Carzami

- Autochek Africa

- AutoTager

- Cars45

- KIFAL Auto

- PeachCars

- Planet42

- Sylndr

- Mogo Auto LTD

- Schulenburg Motors

- Euroken Automobiles Ltd

- Global Cars Trading FZ LLC

- Cars2africa

- Abi Sayara

- Cardealers Africa

- We Buy Cars (Pty) Ltd

- OLX Group

- CarMax East Africa Ltd.

Top Players In The Market

- Toyota is a key player in the African used car market through its extensive export of reliable and durable models such as the Corolla, Vitz, and Land Cruiser. The brand’s reputation for longevity and ease of maintenance has made it the preferred choice among African consumers seeking affordable, high-quality pre-owned vehicles. Toyota contributes significantly to global automotive trade by exporting millions of certified used vehicles annually, with Africa being a major destination. Beyond only car sales, it also shapes local after-sales service networks and the availability of replacement parts, which boosts customer trust in ownership. The company's strong presence in African markets is reinforced by local dealership partnerships and digital initiatives that streamline vehicle sourcing and financing. Toyota is an essential part of the continent's used automobile ecology because it keeps setting standards for quality and dependability.

- Cars45 is a leading online used car marketplace in West Africa that is revolutionizing the way people purchase and sell used cars. Through the implementation of digital transactions, clear pricing, and inspection services, the platform has improved efficiency and confidence in the area's informal automotive sector. Cars45 has impacted how digital platforms function in emerging economies as part of a rising trend of fintech-integrated mobility solutions. Its business model has inspired similar startups across East and Southern Africa, which contributes to the formalization of the used car trade on the continent.

- Autochek is a rapidly expanding pan-African used car platform that connects buyers with verified sellers while providing access to financing, insurance, and logistics support. It has emerged as a key player by addressing critical pain points such as vehicle verification and credit accessibility. Global investors' perceptions of the potential of digital automotive ecosystems in emerging nations are influenced by Autochek, and its influence goes beyond Africa. Its structured approach to used car commerce is setting new standards for transparency and scalability in developing markets. Autochek is changing the used car market by forming cross-border alliances and expanding strategically. This will make vehicle ownership safer and more accessible for African customers and attract worldwide attention to the continent's changing automotive market.

Top Strategies Used By Key Market Participants

- One of the most impactful strategies employed by key players in the African used car market is the adoption of digital platforms and online marketplaces, which enhance transparency, streamline transactions, and expand reach beyond traditional physical dealerships. Customers' interactions with the used car ecosystem are being revolutionized by these platforms, which include vehicle inspections, certification, and even doorstep delivery.

- Another key strategy involves expanding financial inclusion through tailored auto financing products, which will allow a broader segment of the population to access vehicle ownership. Major players work with banks and fintech companies to offer flexible payment options, such as middle-class micro-leasing and installment-based purchasing.

- Companies are increasingly focusing on building standardized supply chains and after-sales service networks to improve customer retention and brand loyalty. This includes certified pre-owned programs, mobile servicing units, and localized spare parts distribution, which ensures long-term value for vehicle buyers and reinforces trust in the used car market.

RECENT MARKET NEWS

- In February 2023, Toyota launched a certified pre-owned vehicle program in Kenya, which aimed at improving buyer confidence by offering inspected and warrantied used cars backed by authorized dealerships.

- In July 2023, Cars45 expanded its operations to Ghana by establishing a new regional hub to facilitate cross-border vehicle listings and increase its footprint in West Africa’s growing used car market.

- In October 2023, Autochek partnered with a Nigerian fintech firm to launch a digital auto loan product, which enables users to finance used car purchases directly through its mobile app without requiring collateral.

- In May 2024, Renault South Africa launched a program for refurbished cars aimed at consumers on a limited budget. These vehicles come with extended warranties and servicing packages.

- In November 2024, Japanese exporter Big Motor expanded its direct-to-consumer model in Tanzania, which reduces intermediary costs and improves access to low-mileage, well-maintained used cars from Japan.

MARKET SEGMENTATION

This research report on the African used cars market is segmented and sub-segmented into the following categories.

By Vehicle Type

- Hatchbacks

- Sedan

- Sports Utility Vehicles and Multi-Purpose Vehicles

By Vendor

- Organized

- Unorganized

By Country

- Sudan

- Egypt

- Kenya

- Ethiopia

- South Africa

- Rest of Africa

Frequently Asked Questions

What is the Africa used cars market?

The Africa used cars market refers to the buying, selling, and import of pre-owned vehicles across African countries, where second-hand cars are a major source of affordable mobility.

What drives growth in the Africa used cars market?

Rapid urbanization, rising demand for low-cost transportation, limited local vehicle manufacturing, and growing imports from Asia, Europe, and the Middle East.

Why are used cars more popular than new cars in Africa?

Used vehicles are significantly more affordable, easier to finance, and more available compared to new models, which often face higher taxes and longer delivery times.

Which countries lead the Africa used cars market?

Nigeria, Kenya, Ghana, South Africa, and Tanzania are major markets due to large populations, active trading hubs, and strong demand from taxi, ride-hailing, and small business sectors.

What types of vehicles are most in demand in the Africa used cars market?

Compact cars, SUVs, pickup trucks, and commercial vans dominate due to their durability, fuel economy, and suitability for varied road conditions.

What challenges affect the Africa used cars market?

Inconsistent import regulations, limited vehicle inspection standards, concerns over vehicle age and emissions, and fluctuating foreign currency rates.

How do import regulations influence the Africa used cars market?

Many countries restrict the age of imported vehicles or impose higher duties, which impacts pricing, supply availability, and consumer choice.

Are electric or hybrid used cars emerging in the Africa used cars market?

Interest is growing, but adoption remains slow due to limited charging infrastructure and higher upfront costs compared to traditional gasoline vehicles.

Who are the key buyers in the Africa used cars market?

Individual consumers, small business owners, commercial fleets, taxi services, and ride-hailing drivers.

What is the future outlook for the Africa used cars market?

The market is expected to expand as digital car marketplaces grow, financing becomes more accessible, and more consumers transition from motorcycles or minibuses to personal vehicles.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com