Global Agricultural Drones Market Size, Share, Trends and Growth Analysis Report, Segmented By Product (Hardware [Fixed Wing, Rotary Blade, Hybrid], Software [Data Analytics, Data Management, Imaging]), Application (Field Mapping, Variable Rate Application, Crop Scouting, Crop Spraying, Livestock, Agriculture Photography And Others) And By Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034

Global Agricultural Drones Market Size

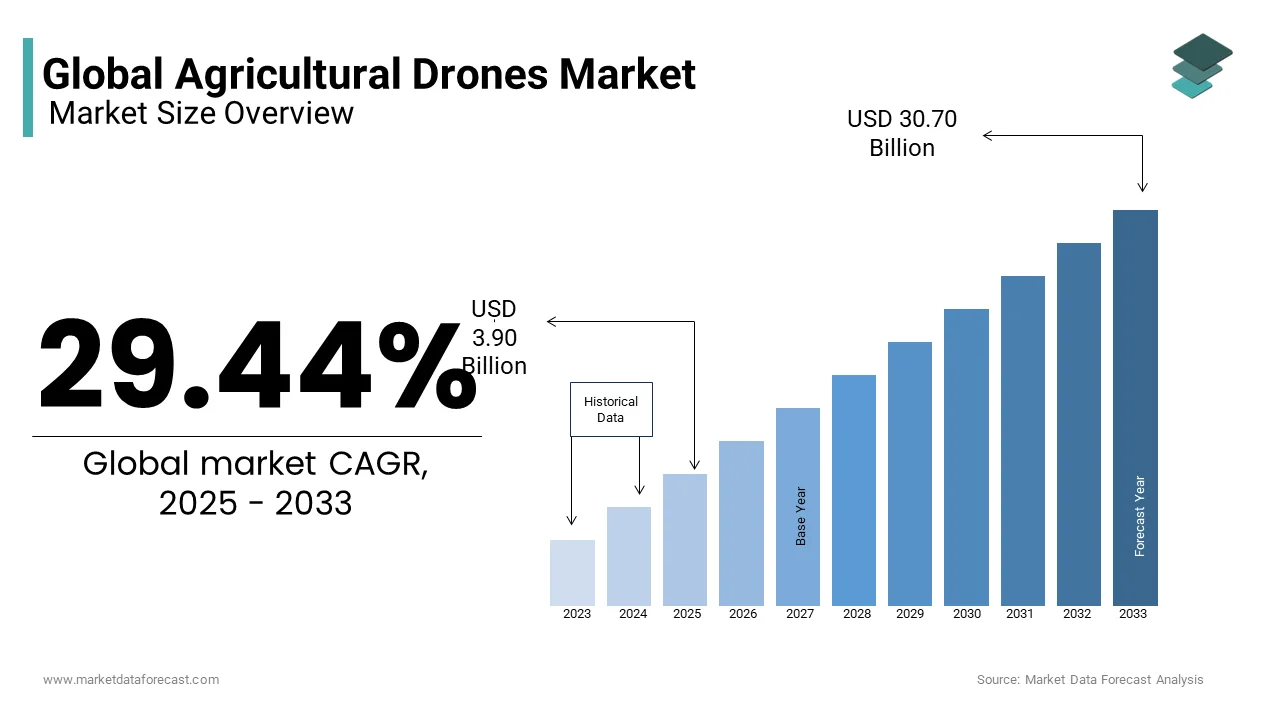

The global agricultural drone market was valued at USD 3.90 billion in 2025 and is anticipated to reach USD 5.05 billion in 2026 from USD 39.78 billion by 2034, growing at a CAGR of 29.44% during the forecast period from 2026 to 2034.

Current Intro: Definition of the Agricultural Drones Market

Agricultural drones refer to unmanned aerial vehicles specifically engineered for applications across crop monitoring,g precision spraying, ng field mapping,, ing and livestock surveillance. These systems integrate advanced sensors, multispectral imaging, and real-time data analytics to optimize agronomic decisions, enhance resource efficiency,,y and reduce environmental impact. Unlike general-purpose drones, agricultural variants are calibrated for low altitude flight, prolonged endurance, and payload adaptability tailored to farming operations. Agriculture remains the single largest consumer of freshwater resources worldwide, a prominent trend consistently highlighted by the FAO, which underscores an ongoing need for more efficient and water-smart technologies. Meanwhile, there is a clear and increasing global trend toward establishing national regulatory frameworks for unmanned aircraft systems (UAS), reflecting a widespread and growing readiness to integrate drones into various civil sectors, including agriculture. The convergence of digital agronomy and autonomous flight is redefining traditional farming paradigms, particularly as labor shortages intensify across major agricultural economies.

MARKET DRIVERS

Precision Agriculture Adoption Drives Demand for Specialized Drone Capabilities

The integration of precision agriculture methodologies has emerged as a major enabler for the agricultural drone market. Farmers increasingly rely on data-driven insights to manage spatial variability in soil health, crop stress, and irrigation needs. Agricultural drones equipped with multispectral and thermal cameras facilitathigh-resolutionon field scouting at a fraction of the time and cost associated with satellite or manual surveying. A majority of large-scale farming operations in one major agricultural region have incorporated precision agriculture technologies into their practices. The adoption of these technologies in that region has shown consistent and notable growth over a recent period. A substantial percentage of commercial farms in another major agricultural union utilized digital monitoring tools. Remote sensing applications, particularly those involving unmanned aerial systems, accounted for a notable share of the digital tools used by these farms. This shift is propelled by the need to comply with stringent agro-environmental regulations, such as the European Union’s Farm to Fork Strategy,gy which mandates a reduction in chemical pesticide use. Drones enable targeted application, thereby aligning with policy-driven sustainability goals while improving input use efficiency.

Escalating Labor Shortages Reinforce the Economic Case for Drone Automation

A chronic scarcity of agricultural labor across both developed and emerging economies has intensified the search for robotic and autonomous alternatives, which further propels the expansion of the agricultural drones market. The agricultural workforce in the European Union is experiencing a consistent and long-term decline. The agro-food sector in high-income countries faces significant and growing labor and skills shortages. This demographic contraction is mirrored globally. The agro-food sector in high-income countries faces significant and growing labor and skills shortages. Agricultural drones alleviate operational bottlenecks by automating tasks such as seeding, pesticide application, and yield estimation, which traditionally require significant manual oversight. For instance, research on agricultural automation indicates that drone-assisted spraying can lead to significant reductions in labor hours compared to traditional methods. The use of drones for agricultural applications, such as in rice paddies, has grown substantially in Japan in recent years, supported by government initiatives. These developments underscore drones not merely as tools of convenience but as essential infrastructure for maintaining agricultural productivity amid a diminishing human labor base.

MARKET RESTRAINTS

Stringent Regulatory Constraints Limit Operational Scalability

Regulatory fragmentation remains a formidable barrier to the agricultural drone market. This is despite technological readiness. Civil aviation authorities impose varied restrictions on flight altitude, payload weight, and visual line of sight requirements, which directly constrain operational efficiency. The European Union Aviation Safety Agency has successfully implemented a consistent, risk-based regulatory system for drone operations across member nations. Authorizations for routine beyond visual line of sight agricultural flights in European Union member states are progressing, but are not yet universally implemented across all nations. This regulatory patchwork hampers cross-border scalability and increases compliance costs for manufacturers and service providers. Moreover, the requirement for operator certification represents a significant adoption hurdle,e particularly for smallholder farmers. The adoption of drone technology and related trained personnel in Southern and Eastern European agriculture is increasing, with some countries showing more rapid progress than others. Consequently, the regulatory environment, while evolving, continues to impede the seamless integration of drones into mainstream agricultural workflows.

High Initial Investment and Fragmented ROI Perception Deter Small-Scale Adoption

The substantial upfront capital required for acquiring and maintaining agricultural drone systems is a significant barrier, particularly for small and medium-sized farms, which hampers the expansion of the agricultural drone market. These farms constitute a significant share of global agricultural holdings. The market for agricultural drones features a wide range of price points; entry-level multirotor and fixed-wing models with basic imaging capabilities are available at more accessible price points, while advanced, large-capacity models incorporating AI analytics and spraying systems represent a significant capital investment. Maintenance software subscriptions and operator training further inflate the total cost of ownership. Surveys indicate that a low proportion of small to medium-sized farms across various regions, including parts of Europe, have adopted drone technology, primarily due to concerns over high initial investment relative to the perceived immediate practical benefits. Unlike large agribusinesses, which achieve economies of scale,e smallholders often lack access to financing mechanisms or cooperative leasing models that could amortize these expenses. Additionally, the absence of standardized metrics to quantify yield gains or input savings undermines confidence in return on investment. Fewer European agricultural extension services provide validated economic models for drone deployment, not leaving farmers to rely on anecdotal evidence or vendor claims, which may inflate performance expectations.

MARKET OPPORTUNITIES

Integration with Farm Management Software Unlocks Data Synergy Potential

The convergence of agricultural drones with digital farm management platforms exhibits a major opportunity for the agricultural drone market. This is achieved by enabling end-to-end data continuity from field capture to agronomic decision-making. Modern drones generate terabytes of geotagged imagery and sensor data, which, when synchronized with cloud-based farm management systems, facilitate predictive analytics, cs variable rate application,ation and compliance reporting. As per a study, a notable share of drone data collected in European agricultural trials was compatible with leading farm management software. This interoperability enhances data utility by contextualizing aerial insights with soil records, weather forecasts, and machinery logs. There is a significant funding commitment aimed at developing integrated digital frameworks for agriculture. The investment specifically supports the creation of farming infrastructures that work seamlessly together, including advanced data collection technologies. Experimental observations from farm trials suggest that integrating autonomous data collection systems with agricultural software can lead to improved resource efficiency in crop management. The trials indicated that farms maintaining consistent crop output while using fewer input resourcesarees possible through the application of these specific technologies. Such synergies not only improve operational efficiency but also strengthen traceability and sustainability documentation essential for meeting evolving market and regulatory demands.

Emergence of Drone as a Service Models Democratizes Access

The proliferation of drone-as-a-service business models is reshaping market accessibility by eliminating capital expenditure barriers and enabling pay-per-use adoption, which is anticipated to contribute to the growth of the agricultural drone market. These service providers deploy certified operators equipped with advanced drones to deliver mapping, spraying, or monitoring services on demand. The number of entities offering specialized agricultural drone services has increased significantly within the region. Policy mechanisms that provide financial incentives are supporting the adoption of digital tools among agricultural producers. The use of drones for specific field applications can lead to reduced expenditures on chemical inputs. Integrating drone-based methods into farm operations has shown enhanced effectiveness in managing field challenges compared to traditional approaches. This model also addresses skill gaps by outsourcing technical operations while allowing farmers to retain control over agronomic decisions. The flexibility, scalability,y and cost transparency of these services are particularly advantageous in regions with fragmented landholdings and limited digital literacy,y thereby expanding the addressable market beyond large commercial farms.

MARKET CHALLENGES

Limited Battery Endurance Constricts Operational Throughput

Persistent limitations in battery technology constrain flight duration and coverage capacity, particularly in large-scale farming environments, despite rapid advancements in drone design, which in turn impedes the growth of the agricultural drone market. Commercial agricultural drones frequently utilize lithium polymer batteries, leading to average flight times that require regular battery changes during field work. Under typical operating conditions with a full payload, the effective flight duration for multirotor spraying drones is generally constrained. The coverage area per flight cycle for these drones is typically limited to a specific range. This inefficiency becomes acute during critical application windows such as pest outbreaks or pre-harvest treatments, where timeliness directly impacts crop outcomes. Across various large farming regions, the requirement for numerous application passes substantially affects the time and resources required for farm work. Alternative power sources, such as hydrogen and hybrid systems, are in development to potentially address these operational requirements. Currently, no systems utilizing these alternative power sources have received official approval for agricultural operations, as they remain in early development stages. Consequently, battery endurance remains a pivotal bottleneck that restricts scalability and cost competitiveness e, especially when compared to ground-based alternatives capable of continuous operation.

Data Privacy and Cybersecurity Concerns Undermine Institutional Trust

The increasing reliance on drone-generated geospatial and agronomic data has triggered legitimate concerns regarding data ownership, security andthird-partyy access, which slows down the agricultural drone market. Agricultural drones collect high-resolution imagery, field boundary coordinates, and crop health indices, which constitute sensitive operational intelligence. A notable majority of individuals working in the agricultural sector have expressed concern regarding the sharing of their operational data with analytics platforms. The primary reason for this reluctance appears to be unclear or ambiguous language within data governance terms offered by these platforms. Reported security events have demonstrated vulnerabilities, leading to the unauthorized access and compromise of sensitive information, such as field maps and resource application patterns. Existing foundational data protection regulations are broad, and specific provisions for agricultural sector data are generally absent, resulting in a lack of clear guidance. An observation across numerous service agreements indicates that only a minority explicitly detail crucial aspects like data ownership, retention periods, and deletion procedures. This opacity erodes trust and discourages data sharing essential for collaborative innovation and benchmarking. The full potential of insights derived from drones may remain unrealized without standardized cybersecurity protocols and transparent data stewardship practices.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 29.44% |

| Segments Covered | By Product, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Trimble Navigation Ltd., DJI Technology, 3D Robotics, PrecisionHawk, AeroVironment, Inc., Parrot SA, and DroneDeploy. |

SEGMENTAL ANALYSIS

By Product Insights

The hardware segment held the leading share of the agricultural drone market in 2024. The leading position of the hardware segment is attributed to its superior maneuverability,y vertical takeoff and landing capability, and suitability for small to medium-sized fields, which characterize much of the global agricultural landscape. As per sources, a notable share of the world’s farms are small,, er making rotary systems particularly relevant for precision tasks such as targeted spraying and close-range scouting. Their operational flexibility in complex terrain and around obstacles further enhances utility in orchards, vineyards,s and hilly regions prevalent across Southern Europe and Southeast Asia. Additionally, rotary drones typically require less infrastructure for deployment compared to fixed-wing systems, which often need launchers or runways. This practical adaptability aligns with the needs of fragmented farming systems and explains their sustained market leadership despite higher energy consumption per unit area covered.

The software segment is likely to experience the fastest CAGR of 22.3% from 2025 to 2033 due to the rising demand for actionable agronomic intelligence derived from drone-collected data. Farmers are increasingly shifting from raw imagery to predictive models that forecast pest outbreaks, optimize irrigation, and estimate yield with high accuracy. Agricultural operations are increasingly adopting aerial surveillance technologies to refine the precision of chemical treatments. Data-driven insights from high-altitude imaging allow for a decrease in the volume of protective treatments applied to cereal crops without compromising the final harvest grade. The implementation of sophisticated computational models facilitates immediate guidance for field management decisions. There is a growing trend among commercial growers in specific European regions to incorporate automated analysis into their standard production workflows. Regulatory pressures such as the European Union’s Sustainable Use of Pesticides Regulation further compel growers to adopt analytics-driven precision tools to document and justify input use. The convergence of edge computing, cloud infrastructure, and open data standards has also lowered barriers to entry, making sophisticated analytics accessible even to mid-sized operations.

By Application Insights

The crop scouting segment dominated the agricultural drone market by accounting for a 34.6% in 2024. The supremacy of the crop scouting segment is credited to the critical need for early detection of biotic and abiotic stressors, including pests, diseases, nutrient deficiencies, es and water stress. Traditional ground-based scouting is time-consuming and often misses early symptoms due to limited field coverage. In contrast, drones equipped with multispectral sensors can scan hundreds of hectares per day, ay generating normalized difference vegetation index maps that reveal plant health variations invisible to the naked eye. Utilizing scouting methods that incorporate unmanned aerial technology has been observed to reduce the amount of time and effort required for field monitoring. Data gathered from aerial scouting methods can potentially enable earlier identification of areas within a field where plant health issues are present. The ability to intervene sooner using these technological observations may assist in avoiding crop losses. Timely interventions for certain types of valuable crops have been shown to help preserve yields. Increased digital literacy among farmers and regulations that reward preventative crop protection strategies mean that crop scouting is still the foundational application accelerating drone adoption globally.

The variable rate application segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 25.1% during the forecast period, owing to the global push toward input use efficiency and environmental compliance. Variable rate application allows farmers to adjust see, ding ferti,lize,r or pesticide rates in real time based on field zone prescriptions derived from drone-generated maps. Agricultural strategies in the European Union increasingly focus on decreasing fertilizer dependency while attempting to preserve overall crop yields. The use of aerial data to guide nutrient application allows for more precise distribution across varying field conditions. This approach to nitrogen management supports the maintenance of crop quality standards alongside improved resource efficiency. Integrating sensor-based technology into organic applications helps livestock operations align with regional environmental standards regarding air quality. Adopting these digital tools provides a method for producers to navigate evolving ecological requirements without necessarily reducing their output. The convergence of regulatory mandates, precision machinery compatibility, and proven agronomic returns has positioned variable rate application as the most dynamic growth frontier in agricultural drone utilization.

REGIONAL ANALYSIS

North America Market Analysis

North America outperformed other regions in the global agricultural drone market by accounting for a share of 32.4% in 2024. The United States drives this dominance through widespread adoption of precision agriculture technologies supported by robust infrastructure, favorable regulations, and strong private sector investment. Agricultural operations cultivating widely grown crops are increasingly integrating data gathered by unmanned aerial vehicles into their management systems. The commercial deployment of unmanned aerial vehicles has accelerated due to recent advancements in operational regulations that permit expanded flight capabilities. Moreover, the presence of leading drone manufacturers like DJI and AgEagle alongside agribusiness giants such as John Deere fosters a tightly integrated innovation ecosystem. Federal programs, including the Environmental Quality Incentives Program, further subsidize drone adoption for conservation planning. These structural advantages, coupled with high farm income levels and digital readiness, ss ensure North America remains the most mature and commercially active region for agricultural drones.

Europe Market Analysis

Europe was the second-largest player in the agricultural drone market by capturing a 28.6% share in 2024. The growth of the European market is attributed to a strong policy-driven approach where sustainability regulations directly incentivize drone use. Countries such as Germany, France, and the Netherlands lead deployment due to advanced farming infrastructure and supportive national schemes. There has been a noted increase in the integration of drone-collected data within farm management software, often supported by government programs. Agricultural policy changes are linking certain farm subsidies to compliance with digital monitoring requirements, which helps embed drone technologies into everyday farming operations. A majority of commercial farms in Western Europe now utilize aerial remote sensing methods, with drones being the most common choice due to their affordability and ease of use compared to other technologies like satellites or manned aircraft. Strict pesticide reduction targets under the Sustainable Use Regulation make drone-based precision application not just beneficial but increasingly essential for regulatory survival.

Asia Pacific Market Analysis

The Asia Pacific is another key player in the agricultural drone market and is distinguished by rapid adoption in high-density agricultural economies. China and Japan are the primary engines of growth, with China alonaccounting for e accounting for a portion of regional drone sales. Agricultural drone deployment has expanded significantly, with widespread application in major grain-producing river basins for crop protection tasks. Financial support programs that offset a portion of equipment expenses have contributed to increased adoption rates among farming collectives. Regions characterized by smaller plot sizes and an aging labor force have seen a notable shift toward drone technology for staple crop management. Unmanned aerial systems are increasingly utilized to address labor shortages and improve efficiency in traditional paddy cultivation. India is emerging as a high-potential market with the National Drone Policy enabling agricultural exemptions and state-level initiatives in Punjab and Maharashtra promoting drone leasing hubs. The region’s combination of policy support, labor scarcity,y and crop intensity creates a uniquely fertile environment for drone expansion.

Latin America Market Analysis

Latin America is growing steadily in the agricultural drone market. Brazil is the unequivocal leader, der driven by its vast soy, bean, corn, and sugarcane plantations that demand efficient monitoring and input management. The use of unmanned aerial systems has become more common in modern farming practices across significant agricultural areas. The concentration of these technologies often correlates with regions known for substantial crop production and large-scale land management. Regulatory changes have enabled more sophisticated operations, including automated crop treatment. The removal of certain legal restrictions has broadened the application of remote sensing and application tools in the field. There is an observable shift towards employing autonomous aerial solutions to improve field efficiency, moving away from manual or traditional mechanical methods. Additionally, the rise of digital cooperatives such as those in Rio Grande do Sul enables smallholders to pool resources for drone services. Argentina and Colombia are also advancing rapidly, particularly in high-value crops like coffee and citrus, where early pest detection is critical. The integration of drone data with satellite-based weather platforms, such as those operated by Argentina, enhances forecasting accuracy. Despite infrastructure gaps in rural areas, the region’s export-oriented agribusiness model and increasing climate volatility are catalyzing drone adoption at scale.

Middle East and Africa Market Analysis

The Middle East and Africaarees predicted to expand in the agricultural drone market from 2025 to 2033, with growth concentrated in select high-potential countries. Israel leads the region through its advanced agritech ecosystem, where companies like Taranis and Saturas have pioneeredAI-enabledd drone analytics for water-stressed environments. Agricultural sectors are increasingly integrating aerial thermal imaging to refine irrigation practices within controlled environments. Regional producers of high-value crops, such as fruit and wine, are turning to autonomous technology to address fluctuations in workforce availability. Drone adoption is becoming a preferred strategy for meeting rigorous international standards for crop quality and consistency. Regulatory frameworks are evolving as a growing number of specialized operators enter the agricultural aviation sector. The transition toward remote sensing tools reflects a broader shift toward precision management in diverse geographic climates. Meanwhile,,l e Morocco and Egypt are piloting government-backed programs to deploy drones for date palm and wheat monitoring under water conservation initiatives supported by the World Bank. The region's capacity for accelerated growth in the coming decade is driven by compelling needs related to acute water scarcity and climate resilience, which outweigh the current constraints of fragmented infrastructure and limited financing for widespread implementation.

COMPETITIVE LANDSCAPE

The agricultural drones market features intense competition characterized by rapid technological evolution and divergent business models. While large multinational firms such as DJI dominate through scale and vertical integration, specialized players like Parrot and AeroVironment differentiate via scientific validation and enterprise-grade reliability. New entrants from the agritech and robotics sectors are increasingly entering the space, often focusing on niche applications such as livestock monitoring or organic farming compliance. Competition extends beyond hardware to software ecosystems, ms data interoperability, and service delivery, including drone as a service models. Regulatory alignment, customer education, and after-sales support have become critical battlegrounds. Price sensitivity in developing regions further intensifies rivalry, prompting companies to adopt leasing financing and bundled service offerings. This dynamic environment demands continuous innovation and adaptive go-to-market strategies to sustain relevance and customer trust.

KEY MARKET PLAYERS

Some of the major players are dominating the global agriculture drone market.

- Trimble Navigation Ltd.

- DJI Technology

- 3D Robotics

- PrecisionHawk

- AeroVironment, Inc.

- Parrot SA

- DroneDeploy

Top Players In The Market

- DJI is a global leader in aerial robotics and has significantly shaped the agricultural drones market through its Agras series of spraying drones and P4 Multispectral models for crop monitoring. The company actively invests in research and development to enhance flight endurance, payload capacity, and AI-driven analytics. In recent years, DJI has expanded its agricultural software ecosystem with DJI Terra and DJI Smart Agriculture Cloudd enabling seamless data processing and fleet management. It has also forged partnerships with agronomic service providers across Asia, Europe,e and North America to deliver integrated precision farming solutions. These initiatives reinforce DJI’s position as a technology enabler that bridges hardware innovation with practical farm-level applications.

- Parrot SA has established itself as a key European player by focusing on high-precision fixed-wing drones tailored for agronomic research and large-scale farming. Its Bluegrass and ANAFI AI platforms integrate advanced multispectral sensors and photogrammetry capabilities to support digital crop scouting and field mapping. Parrot has intensified its collaborations with agricultural research institutions such as INRAE in France and Rothamsted Research in the United Kingdom to validate drone-based phenotyping protocols. The company also launched ParrotFields, acloud-basedd analytics platform that transforms raw drone data into actionable agronomic insights. Parrot solidifies its standing among professional users who demand reliable, compliant drone solutions through a strong emphasis on scientific validation and adherence to regulatory standards.

- AeroVironment Inc leverages its defense and surveillance heritage to deliver rugged agricultural drones with extended range and secure data transmission. Its Quantix and Quantix MV systems are widely used in North and South America for crop health assessment and sustainability reporting. The company has enhanced its market presence through strategic integrations with major farm management platforms, including Granular and John Deere Operations Center. AeroVironment also emphasizes training and certification programs for agronomists and crop consultants to ensure effective drone deployment. Recent investments in edge computing and onboard AI processing demonstrate its commitment to reducing data latency and enablingreal-time decision-makingg directly in the field.

Top Strategies Used By The Key Market Participants

Key players in the agricultural drones market employ product innovation through advanced sensor integration and artificial intelligence to enhance functionality. They pursue strategic partnerships with agronomic service providers, farm machinery manufacturerss and research institutions to embed drone data into existing workflows. Geographic expansion, in particular into emerging markets in Asia andLatin Aricaa, is prioritized through localized support and training. Companies also invest in cloud-based analytics platforms to convert raw imagery into actionable agronomic recommendations. Additionally, they focus on regulatory compliance and operator certification programs to address legal and skill barriers that hinder adoption.

MARKET SEGMENTATION

This research report on the global agriculture drones market is segmented and sub-segmented based on ByProduct, Application, and Region.

By Product

- Hardware

- Software

By Application

- field mapping

- variable rate application

- crop scouting

- crop spraying

- livestock

- agriculture photography

- others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle-East Africa

Frequently Asked Questions

What is the agricultural drones market?

The agricultural drones market includes aerial unmanned vehicles used in farming to monitor crops, apply inputs, map fields, and collect data that help farmers improve yields, reduce costs, and make data-driven decisions.

Why are drones used in agriculture?

Drones enable real-time crop monitoring, precise spraying, early pest/disease detection, soil and field analysis, and yield estimation, improving farm efficiency and resource management.

What drives growth in the agricultural drones market?

Growth is driven by precision agriculture adoption, labor shortages, rising farm costs, demand for sustainable practices, regulatory support, and advancements in drone sensor technologies.

What types of agricultural drones are there?

Common types include fixed-wing drones (for large area surveys), multi-rotor drones (precision spraying and monitoring), and hybrid VTOL systems combining endurance and precision.

How do drones benefit crop scouting?

Drones with multispectral and thermal cameras collect high-resolution imagery to detect crop stress, nutrient deficiencies, water stress, and pest/disease pressure before they are visible to the naked eye.

What is drone spraying in agriculture?

Drone spraying involves applying pesticides, herbicides, fertilizers, and liquid nutrients using drone-mounted spray systems for precise, uniform coverage with reduced chemical use.

Which crops benefit the most from drone use?

Drones are widely used in row crops (corn, wheat, soy), vegetables, orchards, vineyards, rice paddies, and specialty/horticultural crops.

How do drones support precision agriculture?

By providing field data analytics, targeted application zones, reduced overlap, and optimized input use, drones help farmers minimize waste and maximize ROI while protecting the environment.

What are the key trends shaping the agricultural drones market?

Trends include AI-powered image analytics, autonomous flight planning, cloud-based farm dashboards, swarm drone deployments, and integration with farm management software.

What challenges does the agricultural drones market face?

Challenges include regulatory restrictions, data privacy concerns, high upfront costs, limited technical skills among users, and airspace safety requirements.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com