Global AI in Medical Imaging Market Size, Share, Trends, and Growth Analysis Report, Segmented By Technology, Application, Modalities, End Use, & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2026 to 2034

Global AI in Medical Imaging Market Size

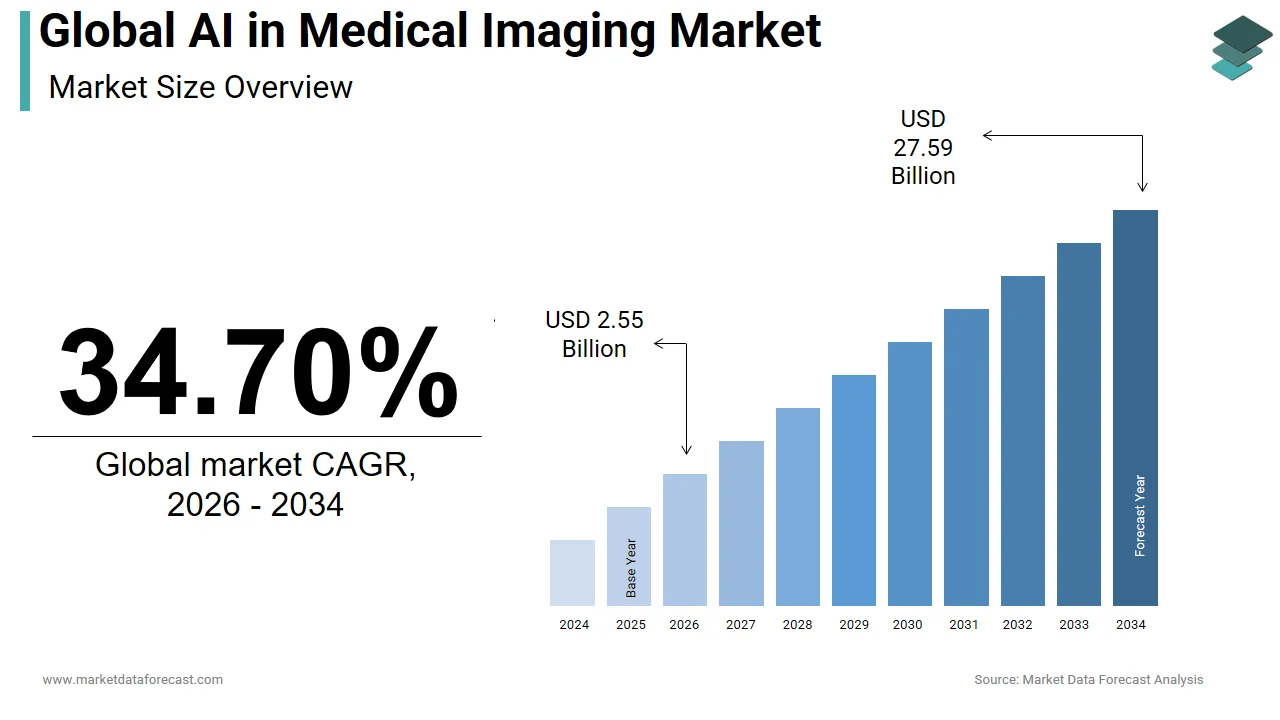

The global AI in medical imaging market reached USD 1.89 billion in 2025, is expected to grow to USD 2.55 billion in 2026, and is anticipated to touch USD 27.59 billion by 2034, at a CAGR of 34.70% from 2026 to 2034.

The AI in medical imaging is the integration of artificial intelligence with deep learning and computer vision algorithms into radiology, pathology, cardiology, and other diagnostic imaging workflows to enhance image interpretation, automate detection, and improve clinical decision-making. These systems analyze vast volumes of imaging data to identify patterns indicative of disease, often with speed and consistency surpassing human capabilities.

MARKET DRIVERS

Rising Global Burden of Chronic Diseases Boosting AI in Medical Imaging

The escalating global burden of chronic diseases including cancer and cardiovascular conditions, is driving the growth of AI inthe medical imaging market. According to the International Agency for Research on Cancer, an estimated 20 million new cancer cases were diagnosed worldwide in 2023, requiring timely imaging for screening, staging, and treatment monitoring. Mammography, low-dose CT for lung cancer, and MRI for prostate and brain tumors are key areas where AI is being integrated to improve detection rates. Similarly, the U.S. Centers for Disease Control and Prevention notes that cardiovascular disease remains the leading cause of death globally, prompting the use of AI in coronary artery calcium scoring and echocardiogram analysis.

Advancements in Computational Power and the Availability of Large Medical Imaging Datasets

The rapid advancement in computational power and the availability of large, annotated medical imaging datasets, which are essential for training robust AI models, is escalating the growth of AI in the medical imaging market. As per the National Institutes of Health, the Medical Imaging Data Resource Center (MIDRC) has compiled over 2 million de-identified imaging studies for AI training, including CT, X-ray, and MRI scans from diverse patient populations. The integration of cloud computing, federated learning frameworks, and secure data-sharing agreements among hospitals is accelerating model development. For instance, the European Imaging COVID-19 AI Database (EICAD) linked 28 hospitals across 12 countries to train AI algorithms for lung lesion detection.

MARKET RESTRAINTS

Lack of Standardized Regulatory Frameworks Hindering AI Adoption

The lack of standardized regulatory frameworks and validation protocols across jurisdictions, which delays clinical adoption and commercialization, is hindering the growth of AI in the medical imaging market. As per the U.S. Food and Drug Administration, while over 700 AI/ML-based medical devices have been cleared since 2015, only 68 are specifically for diagnostic imaging, and most operate under the 510(k) pathway without requiring prospective clinical trials. According to the World Health Organization, only 35% of countries have national policies for AI in health, creating regulatory fragmentation. This inconsistency complicates global deployment, as developers must navigate divergent requirements for data privacy, algorithmic transparency, and clinical validation.

Algorithmic Bias from Non-Representative Training Datasets

The persistent challenge of algorithmic bias due to non-representative training datasets, which can lead to disparities in diagnostic accuracy across demographic groups, is also degrading the growth of AI inthe medical imaging market. A 2022 study by Stanford University found that AI models trained predominantly on data from North American and European populations exhibited up to 15% lower sensitivity in detecting lung nodules in patients of African and Asian descent. According to the Radiological Society of North America, less than 10% of publicly available imaging datasets include comprehensive metadata on race, ethnicity, or socioeconomic status.

MARKET OPPORTUNITIES

AI Integration in Point-of-Care and Portable Diagnostic Systems

The integration of AI-powered imaging tools into point-of-care and portable diagnostic systems in underserved and rural regions is setting up new opportunities for the growth of AI in medical imaging market. AI-enabled handheld ultrasound devices, such as those developed by Butterfly Network, can be operated by non-specialists and use real-time AI guidance to interpret cardiac and abdominal scans.

AI in Predictive and Preventive Imaging for Early Disease Detection

The application of AI in predictive and preventive imaging, where algorithms analyze subtle anatomical and functional changes to forecast disease onset before symptoms appear, is likely to elevate the growth of AI in medical imaging market. The UK Biobank’s AI-driven analysis of cardiac MRIs identified subclinical heart disease in asymptomatic individuals with 88% accuracy, enabling early lifestyle or pharmacological interventions. According to the American Society of Clinical Oncology, integrating such predictive analytics into screening programs could reduce late-stage cancer diagnoses by up to 25%.

MARKET CHALLENGES

Integration and Interoperability Issues with Clinical Workflows and EHR Systems

The integration of AI tools into existing clinical workflows and electronic health record (EHR) systems, which often lack interoperability and standardized data formats, is a challenging factor for the growth of AI in medical imaging market. According to the Office of the National Coordinator for Health IT, only 40% of U.S. hospitals can seamlessly exchange imaging data with external providers, limiting AI model deployment across care networks. Many AI applications operate as standalone "black box" systems, requiring radiologists to switch between platforms, which disrupts workflow and increases cognitive load. Additionally, proprietary data formats such as DICOM are not always compatible with cloud-based AI platforms, necessitating costly middleware solutions.

Legal and Liability Ambiguity in AI-Assisted Diagnoses

The legal and liability ambiguity surrounding AI-assisted diagnoses when errors occur also hinders the growth of AI in medical imaging market. According to a 2023 report by the Brookings Institution, no clear legal framework exists to determine whether responsibility for a misdiagnosis lies with the clinician, the AI developer, or the healthcare institution using the tool. In malpractice cases, courts may struggle to assess whether a physician should have overridden an AI recommendation or if the algorithm itself was flawed. Furthermore, insurance providers have yet to establish standardized coverage policies for AI-related errors.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Application, Modalities, End Use, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | GE HealthCare; Microsoft; Digital Diagnostics Inc.; TEMPUS; Butterfly Network, Inc.; Advanced Micro Devices, Inc.; HeartFlow, Inc.; Enlitic, Inc.; Canon Medical Systems USA, Inc.; Viz.ai, Inc.; EchoNous, Inc.; HeartVista Inc.; Exo Imaging, Inc.; Nano-X Imaging Ltd. |

SEGMENTAL ANALYSIS

By Technology Insights

The deep learning segment dominated the AI in medical imaging market with a significant share in 2025 with its unparalleled ability to analyze complex visual patterns in radiological and histopathological images. According to the National Institutes of Health, deep learning models have achieved radiologist-level accuracy in identifying lung nodules on low-dose CT scans, with sensitivity rates exceeding 94% in large-scale validation studies. The technology’s adaptability to modalities such as MRI, X-ray, and digital pathology has made it the backbone of AI-driven diagnostics.

The natural language processing (NLP) segment is projected to register a CAGR of 18.3% from 2025 to 2033 with the increasing need to extract structured insights from unstructured radiology reports, clinical notes, and electronic health records (EHRs). NLP enables the automated summarization of imaging findings, coding for billing, and integration of diagnostic narratives into AI-powered decision support systems.

By Application Insights

The neurology application segment was the largest and held 36.4% of the AI in medical imaging market share in 2024 with the complexity and urgency of neurological disorders, which require rapid and precise image interpretation. AI tools are extensively used in analyzing brain MRI and CT scans to detect strokes, aneurysms, tumors, and neurodegenerative conditions like Alzheimer’s disease. According to the World Health Organization, stroke is the second leading cause of death globally, with over 12 million cases annually, necessitating immediate imaging assessment. As per the American Heart Association, AI-powered stroke detection systems, such as those from RapidAI and Viz.ai, reduce time-to-treatment by up to 52 minutes by automatically triaging large vessel occlusion cases to stroke teams.

The orthopedics segment is projected to expand at a CAGR of 17.9% during the forecast period. This acceleration is fueled by the rising prevalence of musculoskeletal disorders and the demand for precision in joint and spinal imaging. AI is increasingly deployed to analyze X-rays, MRIs, and CT scans for detecting fractures, osteoarthritis, and spinal misalignments with high reproducibility. According to the Global Burden of Disease Study, over 1.7 billion people suffer from musculoskeletal conditions, the leading cause of disability worldwide. In trauma care, AI tools like those from Gleamer and ContextVision reduce missed fracture rates by up to 30%, particularly in wrist and hip imaging, as confirmed by a 2023 multicenter trial in France. Additionally, AI supports pre-surgical planning in joint replacements by automating bone segmentation and implant sizing.

By End Use Insights

The hospitals segment was accounted in holding a dominant share of the AI in medical imaging market in 2025 with the hospitals’ high imaging volumes, in-house radiology departments, and access to integrated IT infrastructure necessary for AI deployment. Large tertiary care hospitals perform thousands of imaging studies daily, creating need for AI-driven triage and prioritization. Institutions like Johns Hopkins and Charité Berlin have embedded AI into their PACS systems to flag findings such as intracranial hemorrhage and pulmonary embolism in real time. Additionally, academic medical centers are leading AI validation studies, contributing to regulatory approvals and clinical guidelines.

The diagnostic centers segment is projected to grow at a CAGR of 16.7% from 2025 to 2033 with the decentralization of imaging services and the expansion of standalone imaging facilities. These centers, often specializing in MRI, CT, and mammography, are increasingly adopting AI to enhance diagnostic accuracy and operational efficiency in the absence of on-site radiologists. According to the World Health Organization, over 50% of diagnostic imaging in India and Southeast Asia is performed in private imaging centers, many located in tier-2 and tier-3 cities. AI tools enable remote preliminary readings, reducing turnaround time and supporting teleradiology networks.

REGIONAL ANALYSIS

North America AI in Medical Imaging Market Analysis

North America was the top performer in the global AI in medical imaging market with 41.2% of the share in 2024, owing to its advanced healthcare infrastructure, high adoption of digital imaging, and robust regulatory framework for AI validation. Additionally, Medicare’s shift toward value-based care incentivizes hospitals to adopt AI for early diagnosis and workflow optimization.

Europe AI in Medical Imaging Market Analysis

Europe was positioned second by capturing 28.1% of AI in medical imaging market share in 2024, with the strong public healthcare systems, stringent data governance, and growing investment in AI for clinical diagnostics. Countries like Germany, the UK, and France are integrating AI into national radiology networks to address workforce shortages and improve diagnostic consistency. The UK’s National Health Service has funded the NHS AI Lab, allocating £250 million to accelerate AI adoption in imaging, including breast and prostate cancer screening programs.

Asia Pacific AI in Medical Imaging Market Analysis

Asia Pacific AI in medical imaging market growth is ascribed to the growing healthcare infrastructure, rising chronic disease burden, and government-backed digital health initiatives. China and India are leading the region’s adoption, with China’s “Healthy China 2030” plan prioritizing AI in radiology to address a shortage of radiologists, fewer than 2 per 100,000 people, as reported by the Chinese Medical Doctor Association. In India, the National Digital Health Mission is enabling interoperability between imaging centers and EHRs, facilitating AI integration.

Latin America AI in Medical Imaging Market Analysis

Latin America AI in medical imaging market growth is likely to grow with Brazil and Mexico leading in AI adoption within radiology. The region’s growth is driven by rising healthcare privatization and the expansion of diagnostic imaging networks in urban centers. Mexico’s Ministry of Health has initiated pilot programs using AI to detect tuberculosis in rural communities through mobile X-ray units. However, fragmented healthcare systems and limited IT infrastructure constrain widespread deployment. As per the Pan American Health Organization, only 30% of hospitals in the region have fully digitized imaging archives.

Middle East & Africa AI in Medical Imaging Market Analysis

The Middle East & Africa AI in medical imaging market growth is expected to grow, with growth concentrated in the Gulf Cooperation Council (GCC) and select African nations. The UAE and Saudi Arabia are driving demand through national digital health strategies, such as Saudi Vision 2030 and the UAE’s Artificial Intelligence Strategy 2031, which prioritize AI in healthcare transformation. Dubai’s Smart Dubai initiative has integrated AI into radiology workflows across major hospitals, including Rashid and Latifa, to improve diagnostic speed and accuracy. In South Africa, the Council for Scientific and Industrial Research has developed AI models for tuberculosis detection in chest X-rays, addressing a national burden of over 300,000 annual cases, as reported by the National Institute for Communicable Diseases.

COMPETITIVE LANDSCAPE

The competitive landscape of the AI in medical imaging market is characterized by rapid technological iteration, a surge in specialized startups, and increasing consolidation between imaging hardware giants and AI software developers. While multinational corporations like GE, Siemens, and Philips dominate through integrated ecosystem strategies, nimble innovators such as Aidoc, Annalise.ai, and Riverain Technologies are gaining traction with niche, high-accuracy applications. Competition is shifting from standalone algorithm performance to clinical workflow integration, interoperability with PACS and EHRs, and proven impact on diagnostic speed and patient outcomes. Regulatory approval timelines, real-world validation, and ease of deployment are becoming key differentiators. In Asia Pacific and Latin America, local AI firms are emerging to address region-specific disease patterns and infrastructure constraints.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global AI in medical imaging market include

- GE HealthCare

- Microsoft

- Digital Diagnostics Inc.

- TEMPUS

- Butterfly Network, Inc.

- Advanced Micro Devices, Inc.

- HeartFlow, Inc.

- Enlitic, Inc.

- Canon Medical Systems USA, Inc.

- ai, Inc.

- EchoNous, Inc.

- HeartVista Inc.

- Exo Imaging, Inc

- Nano-X Imaging Ltd.

Top Strategies Used by Key Market Participants

Key players in the AI in medical imaging market are leveraging vertical integration of AI into imaging hardware, strategic partnerships with healthcare providers, regulatory acceleration through FDA and CE marking, investment in real-world clinical validation, and expansion into emerging markets via cloud-based and mobile platforms. Companies are embedding AI directly into scanners to enable on-device processing, reducing latency and ensuring seamless workflow integration. Collaborations with academic hospitals and national health systems facilitate large-scale data collection and algorithm training. Firms are also pursuing modular AI applications that can be deployed across modalities and geographies.

Top Players in the AI in Medical Imaging Market

- GE Healthcare has established a significant presence in the Asia Pacific AI in medical imaging market through the deep integration of artificial intelligence into its advanced imaging systems. The company launched its Edison AI Platform across major hospitals in Japan, South Korea, and India, enabling real-time analytics for CT, MRI, and mammography workflows. The company also partnered with Apollo Hospitals in India to deploy AI-powered stroke detection tools across 50+ imaging centers.

- Siemens Healthineers plays a transformative role in advancing AI-powered imaging solutions across Asia Pacific, focusing on workflow optimization and precision diagnostics. The company’s AI-Rad Companion suite, which includes applications for neurology, cardiology, and oncology, has been adopted in leading institutions such as Seoul National University Hospital and Westmead Hospital in Sydney. In 2024, Siemens launched an AI-enhanced MRI quantification tool in Japan for early detection of liver fat and fibrosis, supporting non-invasive diagnosis of NAFLD a condition affecting over 30% of adults in urban Asian populations, as reported by the Asian Pacific Association for the Study of the Liver. The company also established an AI R&D collaboration with the National University of Singapore to develop localized models for stroke and lung disease detection.

- Butterfly Network has disrupted the Asia Pacific medical imaging landscape by combining handheld ultrasound devices with embedded AI to expand access to point-of-care diagnostics. The company’s Butterfly iQ+ device uses AI to guide non-specialist users in acquiring high-quality images. The system reduced misdiagnosis rates by 28% in pilot studies, as documented by Chulalongkorn University. In India, the company collaborated with Narayana Health to integrate AI-powered echo analysis into community screening programs for rheumatic heart disease.

MARKET SEGMENTATION

This research report on the global AI in medical imaging market has been segmented and sub-segmented into the following categories.

By Technology

- Deep Learning

- Natural Language Processing (NLP)

- Others

By Application

- Neurology

- Respiratory and Pulmonary

- Cardiology

- Breast Screening

- Orthopedics

- Others

By Modalities

- CT Scan

- MRI

- X-rays

- Ultrasound

- Nuclear Imaging

By End Use

- Hospitals

- Diagnostic Imaging Centers

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the AI in Medical Imaging Market?

The AI in Medical Imaging Market refers to artificial intelligence technologies and software used to enhance medical image acquisition, processing, interpretation, and clinical decision-making across radiology, pathology, and other diagnostic modalities

2. What are the top technologies in the AI in Medical Imaging Market?

Deep learning, natural language processing (NLP), and computer-aided detection/diagnosis are leading technologies, with deep learning holding the highest market share (58%+) in 2024

3. Which clinical applications drive AI in Medical Imaging Market growth?

Neurology (brain imaging), oncology (cancer screening), pulmonology (lung imaging), and cardiology are the fastest growing segments, with oncology expected to grow by over 30% CAGR

4. What makes AI important for imaging accuracy and efficiency?

AI in medical imaging automates detection of complex patterns, improves diagnostic accuracy, flags subtle abnormalities, assists with quantification, and enhances workflow productivity for clinicians

5. Who are the leading companies in the AI in Medical Imaging Market?

Siemens Healthineers, GE Healthcare, Philips Healthcare, IBM Watson Health, Fujifilm, Aidoc, Arterys, Zebra Medical Vision, Qure.ai, and others are major market players

6. Which regions lead in AI in Medical Imaging Market share?

North America leads with around 43–46% global share (driven by the US), while Asia Pacific is the fastest-growing region due to healthcare digitization and new government initiatives

7. How is AI transforming hospital and imaging center workflows?

AI in medical imaging streamlines image triage, automates repetitive tasks, predicts cases needing urgent review, and reduces radiologist workload while improving throughput

8. What barriers exist to adoption in the AI in Medical Imaging Market?

Key barriers are data privacy concerns, real-world validation, integration complexity, regulatory approvals, and clinical trust in new algorithms

9. How does AI support personalized medicine in medical imaging?

AI enables precision diagnostics—using patient-specific imaging data to tailor clinical decisions and treatment planning, supporting the move toward personalized healthcare

10. How are emerging markets adopting AI in Medical Imaging?

Rapidly growing healthcare infrastructure and proactive government policies in Southeast Asia, India, China, and Latin America are accelerating AI adoption for diagnostic access and efficiency

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com