Asia Pacific Alternative Protein Market Size, Share, Growth, Trends, and Forecast Report – Segmented By Source (Plant-based, Insect-based), Application, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2025 to 2033

Asia Pacific Alternative Protein Market Size

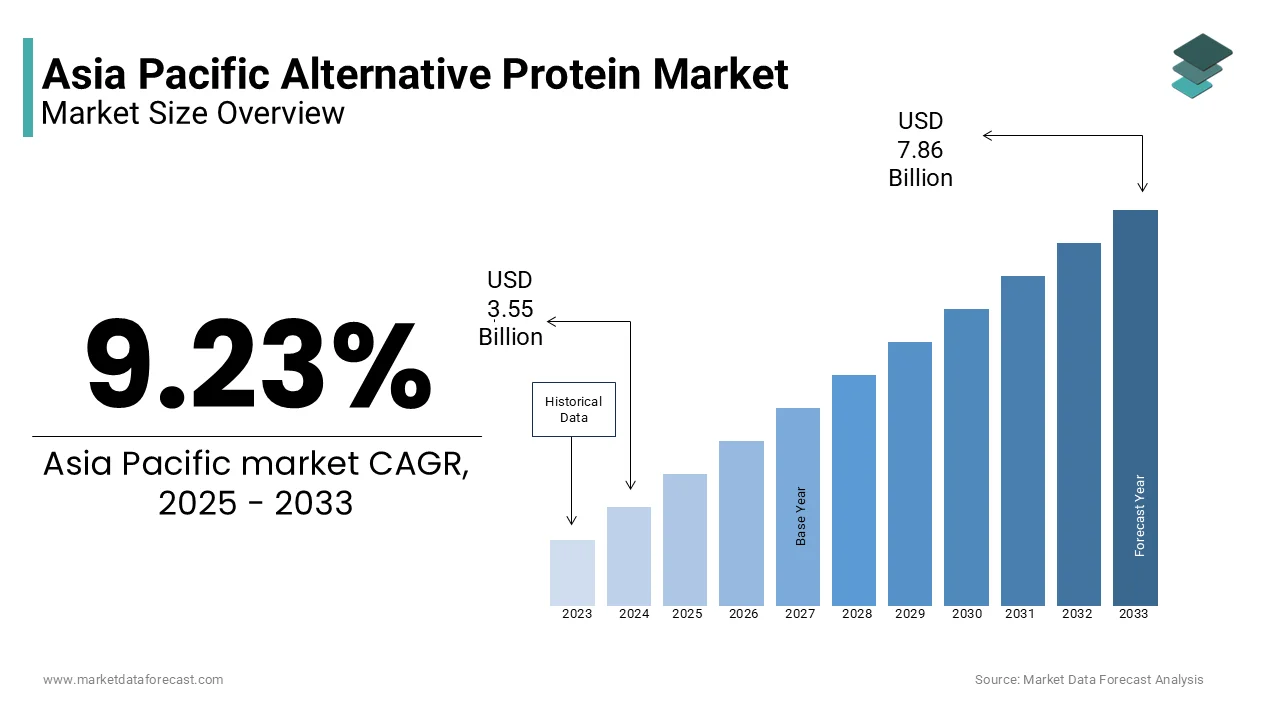

The Asia Pacific alternative protein market size was valued at USD 3.55 billion in 2024, and the market size is expected to reach USD 7.86 billion by 2033 from USD 3.88 billion in 2025. The market's promising CAGR for the predicted period is 9.23%.

The alternative protein for animal feed represents a transformative shift in livestock and aquaculture nutrition, driven by escalating demand for sustainable, resource-efficient, and ethically sound feed ingredients. Alternative proteins in this context refer to non-conventional protein sources such as insect meal, single-cell proteins (e.g., yeast and algae), plant-based proteins (including soy, canola, and legumes), and novel fermentation-derived proteins, which are increasingly being integrated into poultry, swine, aquaculture, and ruminant feed formulations. The region’s burgeoning livestock and aquaculture sectors, coupled with mounting pressure on land and water resources, have intensified the search for viable substitutes to traditional fishmeal and soybean meal. As per the Food and Agriculture Organization of the United Nations, aquaculture production in Asia accounted for over 90% of global output in 2022, placing immense strain on finite marine resources used in feed. Additionally, the region is home to more than 60% of the world’s swine population, as reported by the World Organisation for Animal Health, further amplifying protein demand. Environmental concerns, including deforestation linked to soy cultivation in Southeast Asia and overfishing for fishmeal, have catalyzed regulatory and industry interest in alternative proteins.

MARKET DRIVERS

Rising Aquaculture Intensity and Depletion of Marine Protein Resources

The exponential growth of aquaculture across the Asia Pacific has intensified dependency on high-protein feed ingredients, particularly fishmeal, which is becoming increasingly unsustainable due to overexploitation of wild fish stocks. As per the Food and Agriculture Organization of the United Nations, approximately 25% of global fish catch is reduced into fishmeal and fish oil, with Asia consuming over 60% of this volume. In 2022, China alone utilized nearly 1.8 million metric tons of fishmeal for aquafeed, placing immense pressure on anchovy and sardine populations in the South China Sea and beyond. The collapse of key forage fish stocks, such as the 40% decline in anchoveta biomass off the coast of Indonesia between 2018 and 2021 documented by the Southeast Asian Fisheries Development Center, has disrupted supply chains and inflated prices. This scarcity has compelled feed manufacturers to seek alternatives like black soldier fly (BSF) larvae meal and microalgae, which offer comparable protein profiles.

Escalating Environmental Costs of Conventional Soybean Cultivation

The rising awareness on soybean meal as a primary protein source in swine and poultry feed has triggered severe ecological consequences, which is fuelling the growth of the Asia Pacific alternative protein market. Although much of the soy consumed in the region is imported from South America, its indirect environmental footprint is significant. The embedded carbon cost is staggering: the University of Queensland estimated in 2022 that each ton of soy imported into Asia for animal feed generates an average of 2.8 tons of CO₂ equivalent when land-use change is factored in. In response, countries like Thailand and the Philippines are incentivizing domestic production of alternative proteins to reduce import dependency and environmental liability. Moreover, Singapore-based companies such as Nutrition Technologies have achieved commercial-scale production of fermented microbial protein, reducing water usage by 90% compared to soy processing, as verified by the National University of Singapore’s Environmental Impact Assessment Unit. These advancements are reshaping feed formulation strategies among environmentally conscious poultry integrators in Japan and South Korea, who are adopting low-carbon feed certifications.

MARKET RESTRAINTS

Regulatory Fragmentation and Lack of Harmonized Approval Frameworks

The commercialization of alternative proteins with inconsistent regulatory pathways and the absence of region-wide standards for novel feed ingredients is hampering the growth of the Asia Pacific alternative protein market. As per the Asia-Pacific Economic Cooperation (APEC) Policy Support Unit, only 7 of the 21 APEC economies have formal regulatory guidelines for insect-derived feed, leading to fragmented market access. In India, despite successful pilot trials with BSF meal, the absence of inclusion in the Prevention of Cruelty to Animals (Amendment) Rules has stalled large-scale adoption. Furthermore, the European Union’s restrictive stance on certain alternative proteins indirectly influences Asian regulators, creating a cautious policy environment.

High Production Costs and Limited Economies of Scale

The economic viability of alternative proteins is additionally to hinder the growth of the Asia Pacific alternative protein market. Insect farming, for instance, requires substantial capital investment in climate-controlled facilities and automated harvesting systems. A 2023 analysis by the Commonwealth Scientific and Industrial Research Organisation (CSIRO) revealed that microbial protein facilities in Australia operate at only 45% of optimal capacity due to inconsistent substrate supply and low off-take commitments from feed mills. In India, where smallholder farms dominate livestock production, the price sensitivity of feed buyers further dampens demand for premium-priced alternatives. According to the Indian Feed Manufacturers Association, 78% of poultry integrators are unwilling to pay more than a 15% premium for alternative protein inclusion.

MARKET OPPORTUNITIES

Integration of Circular Economy Models in Urban Agriculture

The proliferation of urban and peri-urban farming in megacities for decentralized alternative protein production through waste valorisation is substantially to pose new opportunities for the growth of the Asia Pacific alternative protein market. Municipal organic waste, which constitutes over 50% of total solid waste in cities like Jakarta, Manila, and Mumbai as per the United Nations Economic and Social Commission for Asia and the Pacific, can serve as a low-cost substrate for insect farming. Black soldier fly larvae can convert food waste into high-protein biomass with a conversion efficiency of 20–25%, as demonstrated by the National Environment Agency of Singapore in its 2022 pilot program at Tuas Nexus. In Bangkok, the Bangkok Metropolitan Administration launched an initiative in 2023 to supply 100 tons of daily food waste to licensed insect farms, potentially yielding 20,000 tons of BSF meal annually. Moreover, Japan’s Ministry of Agriculture, Forestry and Fisheries supports closed-loop systems where restaurant waste is transformed into feed for local poultry farms, reducing dependency on imported soy.

Government-Led Innovation Hubs and Public-Private Research Consortia

The presence of research ecosystems to accelerate the development and commercialization of alternative proteins for animal feed is additionally to enhance the growth of the Asia Pacific alternative protein market. Australia’s FutureFeed initiative, led by CSIRO and funded by the federal government, has successfully demonstrated that red seaweed (Asparagopsis taxiformis) can reduce methane emissions in ruminants by up to 80% while serving as a protein-rich feed supplement. Similarly, India’s Department of Biotechnology launched the Sustainable Animal Feed Innovation Mission in 2022, supporting 17 startups in developing yeast-based and insect-derived proteins. In South Korea, the Ministry of Oceans and Fisheries funds the Marine-Derived Protein Research Center, which achieved a 35% protein yield from microalgae grown in photobioreactors using flue gas from industrial plants. These state-backed initiatives reduce R&D risks and attract private capital.

MARKET CHALLENGES

Consumer and Farmer Skepticism Toward Novel Feed Ingredients

The widespread skepticism among livestock farmers and downstream consumers about the safety and efficacy of alternative proteins is quietly challenging the growth of the Asia Pacific alternative protein market. In rural communities across Indonesia, India, and the Philippines, traditional feed practices are deeply entrenched, and resistance to change is amplified by misinformation. A 2023 survey by the International Livestock Research Institute found that 63% of smallholder poultry farmers in Uttar Pradesh, India, believed insect-based feed would negatively affect egg taste, despite no empirical evidence supporting this claim. In Japan, although retailers like AEON promote low-carbon pork, consumer awareness of alternative feed remains below 20%, according to a 2022 survey by the Japan External Trade Organization.

Supply Chain Fragmentation and Feed Mill Integration Barriers

The integration of alternative proteins into existing feed manufacturing systems is difficult due to the logistical complexities and the fragmented nature of the regional feed industry. Over 80% of feed mills in Southeast Asia are small to medium-sized enterprises, many lacking the equipment to handle novel ingredients with different particle sizes, moisture content, or flow properties, as per the ASEAN Feed Millers Federation. Additionally, inconsistent supply volumes from alternative protein producers disrupt batching schedules. In Malaysia, a 2023 case study by Universiti Putra Malaysia revealed that a 30% fluctuation in spirulina supply led to a 15% increase in production downtime at three major aquafeed plants. Cold chain deficiencies further limit the use of perishable microbial pastes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.23% |

| Segments Covered | By Source, Application, and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Lightlife Foods, Emsland Group, Axiom Foods, AGT Food and Ingredients, Impossible Foods, ADM, Bunge Global SA, Cargill, Ingredion Inc, International Flavors & Fragrances Inc, Tate & Lyle PLC, Kerry Group PLC, Glanbia PLC, SunOpta Inc., and others |

SEGMENTAL ANALYSIS

By Source Insights

The plant-based proteins segment was accounted in holding a prominent share of the Asia Pacific alternative protein market in 2024 with the region’s long-standing integration of soybean meal, canola, and leguminous crops into commercial feed formulations, particularly for swine and poultry. The entrenched infrastructure for processing, storage, and distribution of plant proteins provides a significant competitive advantage over emerging alternatives. Additionally, countries like India and Thailand have expanded domestic pulse cultivation under national protein security initiatives, with India’s Ministry of Agriculture reporting a 12% year-on-year increase in lentil and chickpea production in 2023. The scalability of plant-based systems is further reinforced by established agronomic practices and government subsidies; for instance, Indonesia’s Ministry of Agriculture allocated IDR 4.2 trillion in 2023 to boost domestic soybean farming and reduce import reliance. Moreover, plant proteins benefit from broad regulatory acceptance across the region, unlike novel sources such as insect meal, which face approval delays.

The insect-based segment is likely to grow with an expected CAGR of 26.4% during the forecast period owing to the rising adoption of black soldier fly (BSF) larvae in aquaculture and poultry feed, where their high crude protein content (up to 60%) and favorable amino acid profile rival fishmeal. A pivotal factor accelerating growth is the integration of organic waste streams into insect farming, offering a dual solution to urban waste management and protein scarcity. As per the National Environment Agency of Singapore, over 800,000 tons of food waste were generated in 2022, with 30% now being diverted to licensed insect biorefineries such as EnviroFlight Asia, which converts waste into BSF biomass at a conversion efficiency of 22%. In Thailand, the Department of Alternative Animal Husbandry reported that BSF farms increased from 12 in 2020 to 147 in 2023, supported by subsidies under the Bio-Circular-Green (BCG) Economy Initiative. These policy milestones have catalyzed private investment, with South Korea’s InsectiPro securing USD 45 million in venture funding in 2023 to scale production.

By Application Insights

The swine segment was accounted in holding 42.3% of the Asia Pacific alternative protein market share in 2024 with a direct reflection of the region’s overwhelming concentration of pig populations, with China and Vietnam alone housing over 500 million head more than half of the global total. Soybean meal remains the primary protein ingredient, but rising concerns over supply chain vulnerability have spurred interest in alternatives. In 2022, China imported 97 million tons of soybeans, 80% of which were directed toward swine feed, according to the Ministry of Agriculture and Rural Affairs. Additionally, Vietnam’s Ministry of Agriculture reported a 20% increase in alternative protein adoption in swine diets between 2021 and 2023, driven by outbreaks of African Swine Fever that disrupted traditional feed supply chains. The sheer scale of swine production, combined with national food security imperatives that ensures this segment remains the largest consumer of alternative proteins in the region.

The aquaculture application segment is projected to register a CAGR of 28.1% from 2025 to 2033. The growth of the segment can be attributed to be driven by the depletion of marine resources used in fishmeal production. According to the Indonesia’s Ministry of Marine Affairs and Fisheries mandated a 20% reduction in fishmeal use by 2025 is promoting insect and single-cell proteins.

REGIONAL ANALYSIS

China Alternative Protein Market Analysis

China was the top performer in the Asia Pacific alternative protein market by holding 38.4% of the share in 2024 with its colossal livestock and aquaculture sectors, which consume over 220 million tons of compound feed annually. The urgency to reduce reliance on imported soybeans, which account for 85% of domestic supply, has driven national policy shifts. In 2021, the Ministry of Agriculture and Rural Affairs launched the “Feed Protein Reduction Action Plan,” aiming to cut soybean use by 18 million tons by 2025 through the adoption of alternatives such as fermented rapeseed meal, distillers’ grains, and microbial proteins. Additionally, China is advancing insect farming at scale; the Zhejiang Province government supported the construction of Asia’s largest black soldier fly facility, capable of processing 500 tons of organic waste daily and producing 100 tons of protein meal. The country also leads in single-cell protein R&D, with COFCO Group piloting gas fermentation plants that convert industrial emissions into feed-grade protein.

India Alternative Protein Market Analysis

India alternative protein market was positioned second by accounting for 14.2% of the share in 2024 with its vast and rapidly modernizing livestock sector, which includes the world’s largest bovine population and a poultry industry producing over 5 million tons of feed annually. Rising feed costs, driven by volatile soybean prices and import dependency, have catalyzed the adoption of indigenous protein sources. The Department of Animal Husbandry and Dairying noted that alternative protein usage in commercial feed formulations increased by 22% between 2020 and 2023, particularly in poultry and aquaculture. Additionally, insect farming is gaining traction; the Department of Biotechnology funded 15 startups under the “FeedTech Innovation Program,” including Goa-based Protenga, which operates a 100-ton-per-month BSF facility.

Japan Alternative Protein Market Analysis

Japan alternative protein market is expected to grow with prominent CAGR in the next coming years. The Japanese government’s Green Growth Strategy, launched in 2021, includes specific targets for reducing carbon emissions in animal agriculture, which is sdirectly incentivizing the use of low-impact feed ingredients. Companies like Insect Technology Group have established fully automated BSF facilities in Fukuoka by converting food waste into feed while reducing greenhouse gas emissions by 70%, as verified by the National Institute for Environmental Studies. Additionally, Japan’s aquaculture sector, which produces over 1 million tons of fish annually, is transitioning to algae-based feeds to reduce marine resource dependency, as reported by the Fisheries Research Agency.

Australia Alternative Protein Market Analysis

Australia alternative protein market growth is propelled by the advanced research infrastructure and strong biosecurity standards make it a leader in novel protein development, particularly in ruminant nutrition. This has led to commercial adoption by major beef producers, including Stockman’s Australia, which launched a low-emission beef line in 2022.

COMPETITIVE LANDSCAPE

The competitive landscape of the Asia Pacific alternative protein market for animal feed is characterized by a dynamic interplay between homegrown innovators and multinational entrants, each vying to establish technological and regulatory dominance. Domestic startups in India, Thailand, and Singapore, are leveraging local waste streams and government-backed sustainability initiatives to scale insect and microbial protein production. These firms benefit from agile operations and deep understanding of regional feed requirements, enabling rapid pilot-to-commercial transitions. Simultaneously, global players like Calysta and Ynsect are entering through strategic partnerships with Asian agribusinesses, bringing advanced fermentation technologies and international certification standards. Competition is intensifying around production efficiency, with companies investing heavily in automation, AI-driven monitoring, and bioreactor optimization to reduce costs and improve yield consistency. Regulatory differentiation is another battleground, as early movers gain approval advantages in countries like Japan and Australia, setting precedents for others. Price competitiveness remains a challenge, but firms achieving cost parity with fishmeal or soy are gaining traction.

KEY MARKET PLAYERS

Some of the key players in the Asia Pacific alternative protein market are

- Lightlife Foods

- Emsland Group

- Axiom Foods

- AGT Food and Ingredients

- Impossible Foods

- ADM

- Bunge Global SA

- Cargill

- Ingredion Inc.

- International Flavors & Fragrances Inc.

- Tate & Lyle PLC

- Kerry Group PLC

- Glanbia PLC

TOP PLAYERS IN THE MARKET

- Nutrition Technologies is headquartered in Singapore, is a pioneering force in microbial and insect-based protein development for animal feed across the Asia Pacific. The company specializes in black soldier fly (BSF) larvae cultivation using food waste as a substrate, offering a sustainable alternative to fishmeal in aquaculture and poultry diets. In 2023, it launched a fully automated BSF production facility in Malaysia with a monthly capacity of 150 tons, marking one of the region’s largest commercial-scale operations. The company has partnered with Thai Union Group to supply protein meal for shrimp feed, enhancing traceability and reducing marine resource dependency. Nutrition Technologies also collaborated with the National University of Singapore to refine fermentation techniques that improve amino acid profiles in microbial biomass. In early 2024, it secured regulatory approval from Malaysia’s Department of Veterinary Services for nationwide distribution, accelerating market penetration. Its integration of circular economy principles and focus on food waste valorization position it as a key innovator driving sustainable feed transformation across Southeast Asia.

- Protenga, based in Goa, India, is a leading biotechnology company advancing insect-based protein solutions for animal and aquaculture feed in the Asia Pacific. The company operates a state-of-the-art black soldier fly farming facility capable of processing 100 tons of organic waste daily and producing high-protein insect meal with over 55% crude protein content. In 2023, Protenga partnered with the Indian Council of Agricultural Research to conduct large-scale trials in poultry and fish feed, demonstrating a 14% improvement in feed conversion ratio. The company expanded its operations to Vietnam in June 2023, establishing a joint venture with a local feed mill to supply BSF meal for shrimp farming. Protenga also received funding from the Department of Biotechnology’s National Biopharma Mission to scale up automation and improve larval yield efficiency. In early 2024, it launched a decentralized farming model by enabling smallholder farmers to rear BSF larvae using kitchen waste, thereby promoting rural entrepreneurship.

- Calysta, a global leader in fermentation-derived proteins, has significantly expanded its footprint in the Asia Pacific through its flagship product, FeedKind® protein—a single-cell protein produced from natural gas fermentation. While headquartered in the U.S., Calysta has established strategic partnerships across Japan, South Korea, and China to integrate FeedKind® into aquaculture and swine feed formulations. In 2023, it collaborated with Japan’s Marubeni Corporation to distribute FeedKind® to major aquafeed manufacturers, which is targeting a 20% replacement of fishmeal in shrimp diets. Calysta also partnered with the Chinese Academy of Sciences to evaluate the digestibility and growth performance of FeedKind® in tilapia, yielding positive results in feed efficiency and immune response.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the Asia Pacific alternative protein market for animal feed are deploying strategic partnerships, technological innovation, and geographic expansion to strengthen their positions. Companies are increasingly forming alliances with research institutions to validate the nutritional efficacy and safety of novel proteins by enhancing credibility among feed manufacturers and regulators. Joint ventures with local producers enable faster market entry and adaptation to regional feed formulations. Investment in automation and waste-to-protein infrastructure is accelerating production scalability while reducing environmental impact. Regulatory engagement is another strategy, with firms actively participating in policy consultations to shape approval frameworks for insect and microbial proteins. Some firms are adopting decentralized production models to empower small-scale farmers and reduce transportation costs.

RECENT HAPPENINGS IN THE MARKET

- In June 2023, Protenga, an Indian biotech firm that expanded into Vietnam by establishing a joint venture with AquaLife Feed Mill to supply black soldier fly meal for shrimp aquaculture by enhancing regional supply chain integration and supporting sustainable feed adoption.

- In September 2023, Nutrition Technologies launched a fully automated 150-ton-per-month black soldier fly production facility in Johor, Malaysia, significantly increasing its capacity to supply insect-based protein to poultry and aquaculture feed manufacturers across Southeast Asia.

- In November 2023, Calysta partnered with Marubeni Corporation in Japan to distribute FeedKind® protein to major aquafeed producers, which is facilitating the commercialization of single-cell protein in shrimp and fish diets across the Asia Pacific.

- In January 2024, Thailand’s Department of Livestock Development granted nationwide approval for Nutrition Technologies’ insect meal in poultry and swine feed by enabling broader market access and reinforcing regulatory confidence in novel protein sources.

- In March 2024, Protenga launched a decentralized farming model in rural India, allowing smallholder farmers to cultivate black soldier fly larvae using organic waste, which is promoting local protein production and enhancing rural economic resilience.

MARKET SEGMENTATION

This research report on the Asia Pacific alternative protein market has been segmented and sub-segmented based on the following categories.

By Source

- Plant-based

- Soy protein isolates

- Soy protein concentrates

- Fermented soy protein

- Duckweed protein

- Others

- Insect-based

- Microbial-based

- Bacteria

- Yeast

- Algae

- Fungi

- Others

By Application

- Food & beverage

- Meat analogs

- Bakery

- Dairy alternatives

- Cereals & snacks

- Beverages

- Others

- Animal feed

- Poultry

- Broiler

- Layer

- Turkey

- Swine

- Starter

- Grower

- Sow

- Cattle

- Dairy

- Calf

- Aquaculture

- Salmon

- Trout

- Shrimps

- Carp

- Pet food

- Equine

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia Pacific

Frequently Asked Questions

1. What is the Asia Pacific alternative protein market?

It refers to the regional market for plant-based, insect-based, microbial, and lab-grown proteins used as sustainable alternatives to traditional animal protein.

2. What factors are driving the growth of alternative proteins in Asia Pacific?

Rising health consciousness, environmental concerns, lactose intolerance, and growing vegan and vegetarian populations are key drivers.

3. Which countries lead the alternative protein market in Asia Pacific?

China, Japan, India, Australia, and South Korea are the leading markets in the region.

4. What types of alternative proteins are most popular in Asia Pacific?

Plant-based proteins dominate, followed by insect-based proteins and cultivated (lab-grown) meat.

5. What role do startups play in the Asia Pacific alternative protein market?

Startups are driving innovation in plant-based foods, cultured meat, and fermentation-based proteins across the region.

6. What challenges does the market face?

High production costs, limited consumer awareness in some areas, and regulatory hurdles for lab-grown meat are key challenges.

7. Who are the major players in the Asia Pacific alternative protein market?

Companies such as Beyond Meat, Impossible Foods, v2food, Shiok Meats, and Next Gen Foods are notable players.

8. What impact does government regulation have on this market?

Policies supporting food security, sustainability, and approval of novel protein sources encourage market growth.

9. What technological innovations are driving the market forward?

Advances in fermentation, cellular agriculture, and ingredient processing are making alternative proteins more affordable and appealing.

10. What is the future outlook for the Asia Pacific alternative protein market?

The market is expected to grow rapidly, supported by urbanization, rising disposable incomes, and increasing demand for sustainable diets.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com