Asia Pacific Conventional Overhead Conductor Market Research Report – Segmented By Product (ACSR, AAAC, ACAR, AACSR, AAC), Voltage, Application& Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2026 to 2034

Asia Pacific Conventional Overhead Conductor Market Size

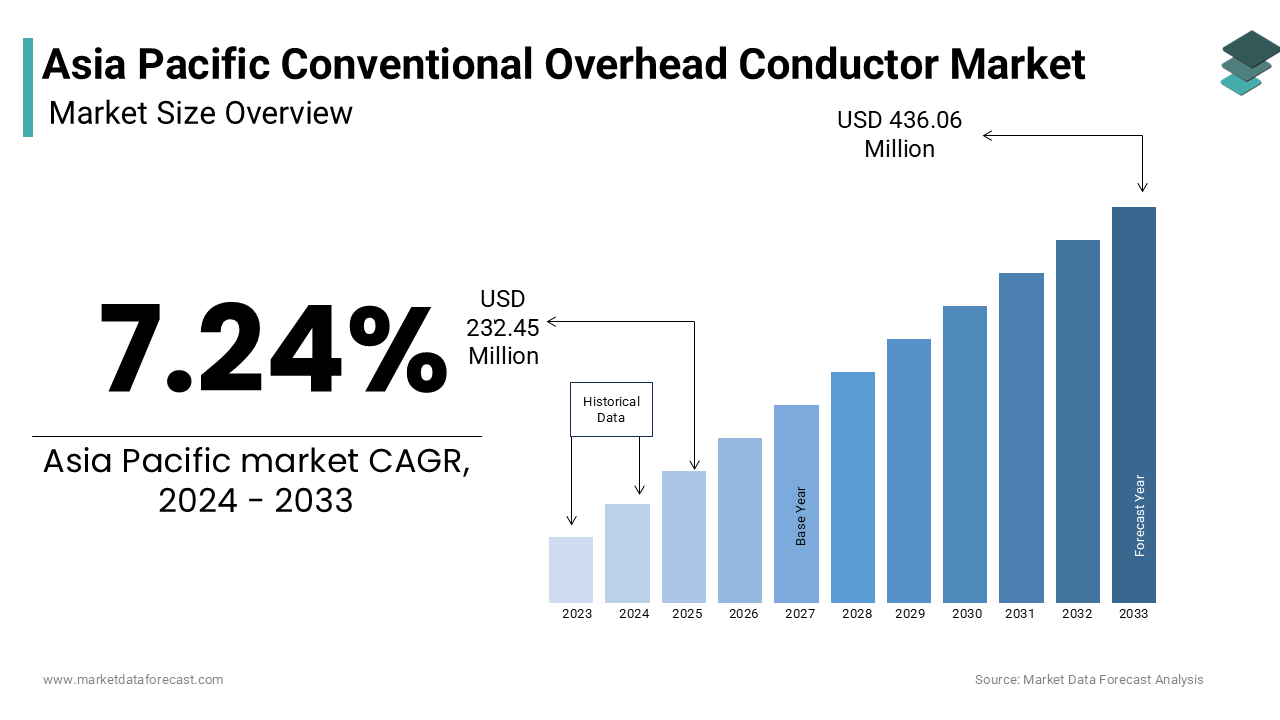

The Asia Pacific Conventional Overhead Conductor Market size was valued at USD 249.28 million in 2025 and is anticipated to reach USD 267.33 million in 2025 from USD 467.63 million by 2034, growing at a CAGR of 7.24% during the forecast period from 2026 to 2034.

The conventional overhead conductors are primarily composed of aluminum conductor steel-reinforced (ACSR), all-aluminum alloy conductor (AAAC), and aluminum conductor alloy-reinforced (ACAR). These conductors, strung across lattice towers and utility poles, facilitate bulk power transfer from generation hubs to load centers in regions where underground cabling remains economically or geographically unfeasible. Their continued dominance is rooted in widespread compatibility with existing infrastructure and ease of installation using standard hardware and practices. Moreover, the World Bank notes that over 180 million people in the region gained access to electricity between 2015 and 2023, largely through overhead line extensions in remote areas. In mountainous regions such as Nepal and northern Vietnam, conventional conductors remain the only viable option for grid expansion due to terrain constraints and logistical limitations.

MARKET DRIVERS

Expansion of Rural Electrification Programs in Developing Economies

The persistent push to achieve universal electricity access across remote areas is a primary driving factor for the growth of the Asia Pacific Conventional Overhead Conductor Market. As per the International Renewable Energy Agency, approximately 120 million people in the region still lacked reliable grid access in 2023, primarily in archipelagic and mountainous areas where underground cabling is impractical. National governments are prioritizing cost-effective overhead line deployment to bridge this gap. In Indonesia, the Ministry of Energy and Mineral Resources extended over 12,000 kilometers of overhead distribution lines in 2022 alone, which is predominantly using ACSR conductors due to their tensile strength and resistance to salt corrosion in coastal zones. The durability of steel-reinforced aluminum under mechanical stress and exposure to monsoon conditions further enhances its suitability.

Replacement of Aging Transmission Infrastructure in Mature Markets

The overhead transmission network in industrialized nation is reaching the end of its operational lifespan with large-scale conductor replacement programs that is bolstering the growth of the Asia Pacific Conventional Overhead Conductor Market. As per Japan’s Federation of Electric Power Companies, over 45% of the country’s 275 kV transmission lines were installed before 1990, with many exhibiting increased sag, corrosion, and fatigue due to prolonged exposure to environmental stressors. The Institute of Electrical and Electronics Engineers notes that retrofitting existing towers with HTLS conductors often demands structural reinforcement, increasing project costs by up to 35%. In Australia, TransGrid and Powerlink Queensland have conducted lifecycle assessments showing that conventional conductors, when properly maintained, can operate reliably for 40 years or more, making them a cost-effective choice for like-for-like replacements.

MARKET RESTRAINTS

Rising Competition from High-Temperature Low-Sag (HTLS) Conductors

The growing adoption of high-temperature low-sag (HTLS) conductors in high-capacity corridors is hampering the growth of the Asia Pacific Conventional Overhead Conductor Market. HTLS conductors, such as aluminum conductor composite core (ACCC) and aluminum-conductor steel-supported (ACSS), offer superior thermal performance by allowing up to 2.5 times more power transfer without increasing tower height or spacing. As per CIGRE, HTLS conductors were used in 42% of new 220 kV and above transmission lines in China between 2020 and 2023, driven by the need to evacuate power from remote renewable zones. In urban fringes and industrial belts where right-of-way is limited, HTLS solutions offer a space-efficient alternative.

Vulnerability to Environmental Degradation in Tropical and Coastal Climates

The conventional overhead conductors are highly susceptible to corrosion and mechanical degradation in the humid, saline, and cyclone-prone environments prevalent is additionally declining the growth of the Asia Pacific Conventional Overhead Conductor Market. As per the Asian Disaster Preparedness Center, over 60% of unplanned outages in coastal transmission networks in the Philippines, Bangladesh, and Vietnam are attributed to conductor corrosion and strand breakage. Similarly, in Odisha, India, post-cyclone assessments by the Central Power Research Institute revealed that 70% of transmission failures during Cyclone Fani (2019) stemmed from corroded steel cores in conventional conductors.

MARKET OPPORTUNITIES

Integration with Hybrid Overhead-Underground Networks in Urban Fringe Development

The expansion of urban peripheries is creating a niche for conventional overhead conductors in hybrid power distribution networks that transition from underground cabling in city cores to overhead lines in suburban and peri-urban zones. This is a specific factor that can propel the growth of the Asia Pacific Conventional Overhead Conductor Market in the coming years. For example, in Hanoi, Vietnam, the Hanoi Power Company uses XLPE cables in the city center but switches to ACSR for radial feeders extending into outlying communes, reducing project costs by 40% as reported by the Vietnam Electricity Group. Similarly, in Jakarta, PLN’s suburban expansion program relies on AAAC conductors for 30 kV feeders serving new housing developments.

Adoption in Temporary and Emergency Power Infrastructure

The rapid adoption of the temporary and emergency power networks due to their rapid deploy ability, ease of repair, and compatibility with modular support structures is additionally to enhance the growth of the Asia Pacific Conventional Overhead Conductor Market. As per the International Federation of Red Cross and Red Crescent Societies, over 75% of post-disaster electrification efforts in the Asia Pacific between 2018 and 2023 utilized ACSR conductors for restoring power after cyclones, floods, and earthquakes.

MARKET CHALLENGES

Increasing Regulatory Pressure to Reduce Line Losses and Improve Efficiency

The regulatory mandates aimed at minimizing technical losses in power transmission and distribution networks are challenging the growth of the Asia Pacific Conventional Overhead Conductor Market. As per the International Energy Agency, the average technical loss in transmission and distribution networks across the Asia Pacific stands at 9.3%, significantly above the global benchmark of 6.5%. Countries like India and Thailand have set national targets to reduce losses to below 6% by 2027, prompting utilities to reassess conductor selection. The Central Electricity Authority of India reports that ACSR conductors contribute to 18–22% of total resistive losses in 33 kV and 66 kV circuits due to their lower conductivity-to-weight ratio. Moreover, Thailand’s Energy Regulatory Commission has linked utility performance incentives to loss reduction, which is accelerating the shift away from standard conductors.

Right-of-Way Constraints and Land Acquisition Delays

The shrinking availability of right-of-way (ROW) and prolonged land acquisition processes in densely populated areas is also to hamper the growth of the Asia Pacific Conventional Overhead Conductor Market in the coming years. According to the United Nations Human Settlements Programme, urban sprawl has reduced available open land, forcing utilities to reroute lines or adopt alternative technologies. In response, Thailand’s Electricity Generating Authority has shifted to HTLS conductors in 60% of new inter-provincial lines to minimize land use. The World Bank notes that conventional conductor projects face 2.5 times more litigation than underground or compact HTLS alternatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.24% |

| Segments Covered | By Product, Voltage, Application and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the rest of APAC. |

| Market Leaders Profiled | Nexans, CTC Global, Sterlite Power, Prysmian Group, Sumitomo Electric Industries, ZTT, APAR Industries, 3M, Gupta Power, ZMS Cable, Hindustan Urban Infrastructure Limited, LS Cable & System, and Eland Cables |

SEGMENTAL ANALYSIS

By Product Insights

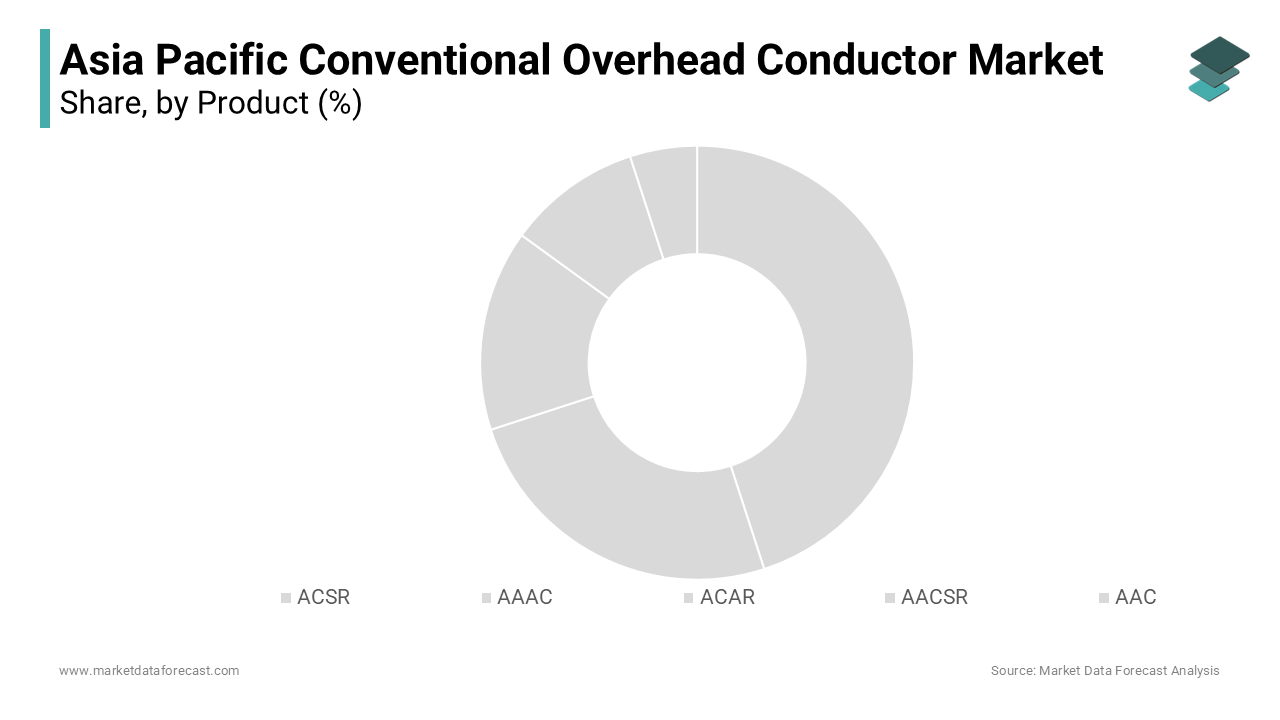

The aluminum conductor steel-reinforced (ACSR) segment was accounted in holding 58.3% of the Asia Pacific conventional overhead conductor market share in 2025. ACSR conductors are extensively deployed in regions exposed to extreme weather, high wind loads, and seismic activity due to their robust steel core, which provides superior tensile strength. In mountainous regions such as Nepal and northern Vietnam, where ice loading and terrain-induced tension are prevalent, the Central Power Research Institute of India found that ACSR can withstand mechanical stresses up to 35 kN, nearly 40% higher than AAAC under identical spans. The Japan Meteorological Agency reports that over 70% of overhead lines in typhoon-prone coastal zones of Kyushu and Shikoku use ACSR for its resistance to galloping and fatigue. Additionally, in desert regions like western India and northwest China, ACSR’s resistance to thermal expansion and contraction ensures long-term stability.

The all-aluminum alloy conductor (AAAC) segment is expected to witness a CAGR of 9.6% in the coming years. AAAC’s monolithic aluminum-magnesium-silicon alloy composition provides exceptional resistance to galvanic and atmospheric corrosion by making it ideal for deployment in saline and polluted environments. As per the National Institute of Oceanography in India, AAAC exhibited only 3% material degradation after 15 years of exposure to marine atmospheres in Goa, compared to 18% for standard ACSR. AAAC’s high strength-to-weight ratio allows for longer spans between support structures, reducing the number of towers required and lowering civil construction costs. The Department of Infrastructure, Transport and Regional Development notes that fewer towers minimize environmental disruption in ecologically sensitive zones. In Malaysia, Tenaga Nasional Berhad reported that AAAC reduced tower requirements by 1,200 units across its Sabah grid upgrade, saving USD 18 million in construction costs.

By Voltage Insights

The 132 kV to 220 kV voltage segment was accounted in holding 54.3% of the Asia Pacific conventional overhead conductor market share in 2025 with the primary sub-transmission tier across the region, linking large power plants, renewable clusters, and cross-border interconnectors to urban load centers. As per the International Energy Agency, over 62% of intra-regional power exchanges in ASEAN occur at 132 kV or 220 kV, with Laos exporting hydropower to Thailand and Vietnam via this voltage class. Similarly, in the Philippines, the National Grid Corporation uses 132 kV lines to integrate Mindanao’s geothermal and hydro resources into the Luzon grid.

The >220 kV to 660 kV segment is projected to grow at a CAGR of 8.9% during the forecast period. The need to transmit bulk power from remote hydropower, wind, and solar zones to coastal megacities is accelerating the deployment of high-voltage overhead lines. As per the International Renewable Energy Agency, China’s Xinjiang and Gansu provinces host over 60 GW of solar and wind capacity, which is requiring 750 kV and 500 kV transmission lines to deliver power to Shanghai and Guangdong. State Grid Corporation commissioned over 18,000 km of 500 kV lines between 2020 and 2023, primarily using ACSR and ACAR conductors.

By Application Insights

The high tension (HT) application segment was accounted in holding 56.3% of the Asia Pacific Conventional Overhead Conductor Market share in 2025. HT lines form the primary distribution tier across rural and peri-urban areas, where they connect substations to end consumers. As per the United Nations Development Programme, over 70% of new electricity connections in Myanmar, Bangladesh, and Cambodia between 2015 and 2023 were made via 11 kV and 33 kV overhead lines using ACSR conductors. HT conductors are increasingly used to interconnect decentralized renewable sources such as solar microgrids and biomass plants. As per the International Renewable Energy Agency, over 12 GW of distributed solar in India is connected at 33 kV, requiring robust overhead lines.

The extra high tension (EHT) segment is likely to grow with a CAGR of 8.7% in the coming years. EHT lines are essential for transporting power from remote renewable zones. As per the International Hydropower Association, Bhutan’s 10 GW hydropower exports to India rely on 220 kV and 400 kV EHT corridors using ACSR conductors. Mega-cities are upgrading EHT networks to handle rising loads. In Tokyo, TEPCO reinforced its 275 kV grid with AAAC conductors to improve reliability.

REGIONAL ANALYSIS

China Conventional Overhead Conductor Market Analysis

China was the largest contributor in the Asia Pacific conventional overhead conductor market with a 34.3% of share in 2025 with the massive grid expansion and renewable integration programs. State Grid Corporation and China Southern Grid are executing a nationwide transmission upgrade, installing over 25,000 km of new overhead lines annually. The National Energy Administration reports that 80% of these use ACSR due to its cost and durability. China also hosts the world’s largest solar and wind capacity, requiring extensive 220 kV and 500 kV evacuation corridors. The country’s domestic manufacturing base, led by companies like Far East Cable and Yangtze Aluminum, produces over 70% of regional ACSR demand.

India Conventional Overhead Conductor Market Analysis

India's conventional overhead conductor market growth is leveraging with the Revamped Distribution Sector Scheme and Green Energy Corridors. Over 100,000 circuit kilometers of HT and EHT lines are under upgrade, predominantly using ACSR and AAAC. Power Grid Corporation installed 3,500 km of new lines in 2023 alone. The Ministry of New and Renewable Energy reports that 40 GW of solar is under construction, necessitating new conductors. Indian manufacturers like Polycab and KEI Industries are scaling production to meet demand.

Japan Conventional Overhead Conductor Market Analysis

Japan Conventional Overhead Conductor Market growth is growing prominently with driven by demand and the replacement of aging infrastructure. TEPCO and Kansai Electric are prioritizing AAAC in coastal zones for corrosion resistance. The Ministry of Economy, Trade and Industry supports R&D in high-conductivity alloys. Japan’s focus on grid resilience and safety ensures steady demand for high-quality conductors.

South Korea Conventional Overhead Conductor Market Analysis

South Korea Conventional Overhead Conductor Market growth is due to the centered on urban reinforcement and industrial supply. The country is upgrading 154 kV and 230 kV lines in Seoul and Busan using AAAC for longevity. Hyundai and Samsung complexes require reliable HT and EHT supply, driving conductor upgrades. The Ministry of Trade, Industry and Energy supports smart grid integration, sustaining market activity.

COMPETITVE LANDSCAPE

The competitive landscape of the Asia Pacific conventional overhead conductor market is defined by a blend of global technology leaders and regionally entrenched manufacturers, each leveraging distinct advantages to capture demand. Multinational corporations such as Prysmian and Nexans emphasize engineering excellence, international certifications, and sustainability compliance, positioning themselves in high-specification projects and regulated markets like Australia and Japan. The absence of a unified regional standard allows for diverse product offerings, fostering competition based on metallurgical innovation, corrosion resistance, and mechanical performance. Price sensitivity in developing economies intensifies rivalry, while in mature markets, technical support and lifecycle reliability are key differentiators. Competition is further shaped by the growing influence of EPC contractors who specify conductors in turnkey projects, shifting procurement dynamics. Localized service networks and rapid delivery capabilities are becoming decisive factors, especially in disaster-prone areas requiring quick grid restoration.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Asia Pacific Conventional Overhead Conductor Market include

- Nexans

- CTC Global

- Sterlite Power

- Prysmian Group

- Sumitomo Electric Industries

- ZTT

- APAR Industries

- 3M

- Gupta Power

- ZMS Cable

- Hindustan Urban Infrastructure Limited

- LS Cable & System

- Eland Cables

Top Players in the Asia Pacific Conventional Overhead Conductor Market

Prysmian Group

Prysmian Group has established a strategic presence in the Asia Pacific conventional overhead conductor market through its advanced manufacturing capabilities and localized technical support. The company supplies ACSR, AAAC, and ACAR conductors for transmission and distribution networks across Australia, Southeast Asia, and India, emphasizing product durability and compliance with IEC and ASTM standards. In 2023, Prysmian expanded its technical service team in Singapore to support grid operators in Indonesia and Vietnam with conductor selection and installation engineering. It also partnered with EnergyAustralia to supply corrosion-resistant AAAC conductors for coastal network upgrades. The company’s investment in R&D has led to enhanced aluminum alloy formulations that improve conductivity and tensile strength.

Nexans

Nexans plays a pivotal role in the Asia Pacific market by delivering high-performance conventional overhead conductors tailored to diverse environmental and operational conditions. The company has supplied ACSR and AAAC conductors for major grid reinforcement projects in Thailand, Malaysia, and New Zealand, focusing on longevity and ease of installation. In 2023, Nexans launched a new range of pre-formed hardware-compatible conductors designed to reduce installation time and mechanical stress during deployment. It strengthened its regional footprint by collaborating with state utilities in India under the RDSS scheme, providing conductors for rural electrification and urban feeders. The company has also integrated lifecycle assessment tools to help clients evaluate environmental impact, aligning with regional decarbonization goals.

Far East Cable Limited

Far East Cable Limited is a dominant force in the Asia Pacific conventional overhead conductor market, leveraging China’s extensive manufacturing ecosystem and export capabilities. The company produces a full range of ACSR, AAAC, and AAC conductors used in national grid projects across Southeast Asia, South Asia, and Oceania. In 2023, Far East expanded its production capacity in Yixing to meet rising demand from Indonesia and Vietnam for rural electrification and industrial supply lines. It has supplied conductors for over 1,500 km of transmission lines in Bangladesh’s Power System Master Plan, emphasizing cost-efficiency and rapid delivery. The company has also invested in automated stranding and quality control systems to ensure consistency.

Top Strategies Used by the Key Market Participants

Key players in the Asia Pacific conventional overhead conductor market are employing a range of strategic initiatives to consolidate their competitive standing. Vertical integration is a primary focus, with manufacturers securing upstream access to high-purity aluminum and steel wire to stabilize supply chains and reduce costs. Companies are expanding regional production and warehousing facilities to shorten delivery cycles and comply with local content regulations. Technical differentiation is achieved through alloy optimization, enhancing conductivity and corrosion resistance without compromising mechanical strength. Strategic partnerships with national utilities and EPC contractors enable firms to participate in large-scale grid tenders and public infrastructure programs. Product standardization in line with IEC, GB, and ASTM specifications ensures cross-border compatibility and regulatory acceptance. Investment in field engineering support and installation training enhances customer confidence and after-sales service. Sustainability branding is increasingly leveraged, with lifecycle analysis and low-carbon production processes used to appeal to environmentally conscious buyers. Digital inventory management and just-in-time logistics are improving responsiveness in fast-moving markets.

RECENT MARKET DEVELOPMENTS

- In March 2023, Prysmian Group expanded its technical support team in Singapore to provide on-site engineering assistance for overhead conductor installation in Indonesia and Vietnam by enhancing service responsiveness and client confidence in tropical grid projects.

- In June 2023, Nexans launched a new range of pre-formed hardware-compatible AAAC conductors in Thailand, designed to reduce installation time and mechanical stress, which is improving deployment efficiency for utilities and EPC contractors.

- In September 2023, Far East Cable Limited inaugurated a new stranding and quality control facility in Yixing, China by increasing its annual overhead conductor production capacity by 25% to meet rising demand from South and Southeast Asia.

- In November 2023, Polycab Industries secured a multi-year supply contract with Bangladesh Power Development Board for 1,200 km of ACSR conductors, which is reinforcing its presence in South Asian rural electrification programs.

- In February 2025, Yangtze Aluminum collaborated with State Grid Corporation of China to co-develop high-conductivity ACSR variants for use in high-load transmission corridors by enhancing performance and strengthening its position in national infrastructure projects.

MARKET SEGMENTATION

This research report on the Asia Pacific Conventional Overhead Conductor Market is segmented and sub-segmented into the following categories.

By Product

- ACSR

- AAAC

- ACAR

- AACSR

- AAC

By Voltage

- 132 kV to 220 kV

- > 220 kV to 660 kV

- > 660 kV

By Application

- High Tension

- Extra High Tension

- Ultra High Tension

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

Who are the key market players in the Asia Pacific Conventional Overhead Conductor Market?

Key players include Nexans, CTC Global, Sterlite Power, Prysmian Group, Sumitomo Electric Industries, ZTT, APAR Industries, 3M, Gupta Power, ZMS Cable, Hindustan Urban Infrastructure Limited, LS Cable & System, and Eland Cables.

How does renewable energy integration impact this market?

The integration of renewable power sources like solar and wind requires efficient overhead conductors to connect new generation sites to the grid.

What challenges affect the Asia Pacific Conventional Overhead Conductor Market?

Challenges include fluctuating raw material costs, environmental concerns, and competition from advanced conductors and underground cabling systems.

What challenges affect the Asia Pacific Conventional Overhead Conductor Market?

Challenges include fluctuating raw material costs, environmental concerns, and competition from advanced conductors and underground cabling systems.

What future opportunities exist in the Asia Pacific Conventional Overhead Conductor Market?

Opportunities include smart grid integration, high-capacity conductors for ultra-high-voltage transmission lines, and modernization of aging power infrastructure.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com