Asia Pacific Cosmetic Preservatives Market Size, Share, Growth, Trends, and Forecast Report – Segmented By Product, Application, Raw Material, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2025 to 2033

Asia Pacific Cosmetic Preservatives Market Size

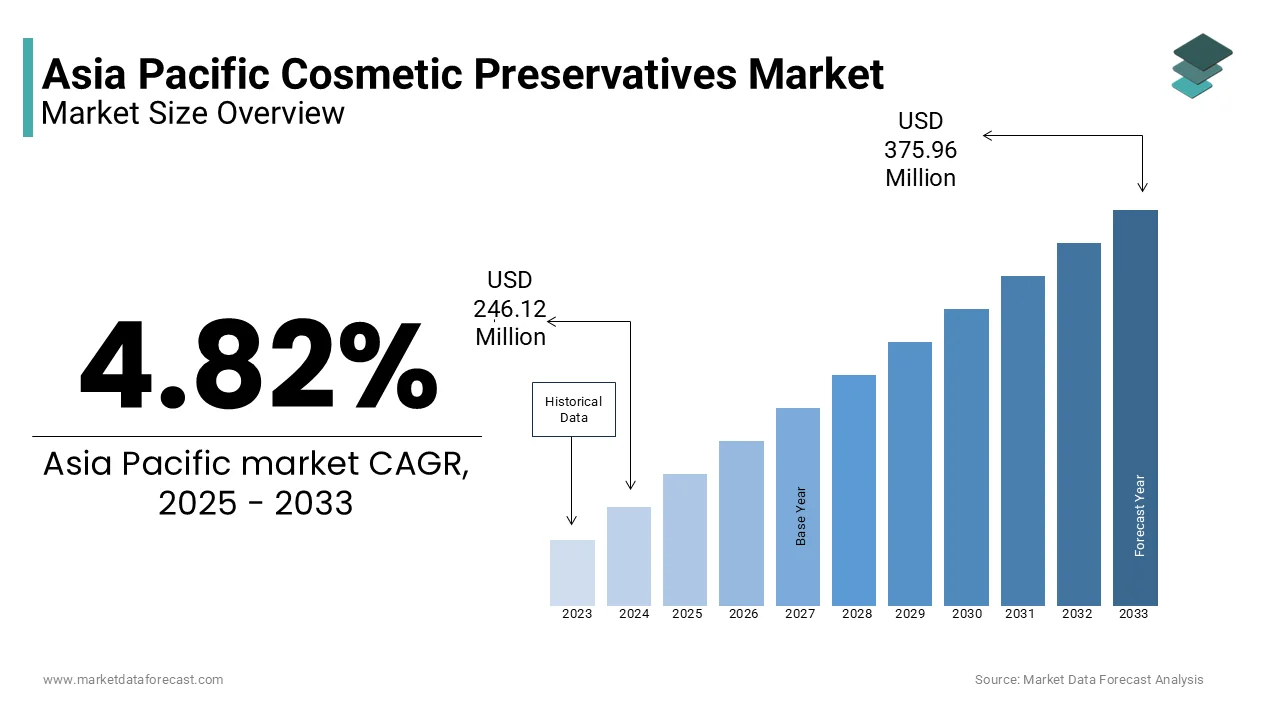

The Asia Pacific cosmetic preservatives market size was valued at USD 246.12 million in 2024, and the market size is expected to reach USD 375.96 million by 2033 from USD 257.98 million in 2025. The market's promising CAGR for the predicted period is 4.82%.

The cosmetic preservatives are chemical and natural agents used to inhibit microbial growth and extend the shelf life of skincare, haircare, makeup, and personal hygiene products. Preservatives such as phenoxyethanol, benzyl alcohol, parabens, and emerging bio-based alternatives like radish root ferment filtrate are maintaining product safety in humid tropical climates where microbial contamination risks are elevated. As per the Asia Pacific Cosmetics Regulation Harmonization Group, over 68% of liquid and cream-based cosmetics launched in Southeast Asia between 2022 and 2023 required broad-spectrum preservation due to high water content and minimal processing heat.

MARKET DRIVERS

Proliferation of Water-Based and Natural Formulations

The shift toward water-rich and natural cosmetic formulations is driving the growth of the Asia Pacific cosmetic preservatives market. According to the Korea Cosmetic Industry Association, water-based skincare products accounted for 74% of new product launches in South Korea in 2023, a 22% increase from 2021. Thailand’s Cosmetic Producers Association noted that 60% of new natural skincare lines in 2023 used multi-preservative blends combining phenoxyethanol with ethylhexylglycerin or caprylyl glycol to ensure efficacy. Japan’s Shiseido Research Center has also documented a 40% rise in the use of fermentation-derived preservatives in water-based products since 2022.

Regulatory Mandates for Microbial Safety and Product Stability

The stringent regulatory requirements are compelling manufacturers to adopt robust preservative systems to ensure product safety and compliance is additionally to enhance the growth of Asia Pacific cosmetic preservatives market. In China, the National Medical Products Administration mandates that all multi-use, water-containing cosmetics undergo challenge testing per ISO 11930 standards, a requirement enforced since 2021. As per the China Cosmetic Regulation Enforcement Report 2023, over 1,400 cosmetic products were rejected during import clearance due to inadequate preservation efficacy, a 38% increase from the prior year. The ASEAN Cosmetic Directive was adopted by all ten member states that enforces harmonized preservation limits and bans certain formaldehyde-releasing agents, pushing manufacturers toward compliant alternatives. Furthermore, as per the Singapore Health Sciences Authority, 42% of locally tested cosmetic samples in 2023 exceeded microbial load limits, reinforcing the need for effective preservation.

MARKET RESTRAINTS

Consumer Resistance to Synthetic Preservatives

Growing consumer awareness toward synthetic preservatives is degrading the growth of the Asia Pacific cosmetic preservatives market. Ingredients such as parabens, formaldehyde donors, and isothiazolinones have faced intense scrutiny due to perceived health risks, despite regulatory endorsements. According to a 2023 consumer survey by NielsenIQ in Japan, South Korea, and Australia, 67% of respondents actively avoided products containing parabens, with 52% citing concerns over endocrine disruption. The Australian Competition and Consumer Commission received over 1,200 consumer complaints in 2023 related to skin irritation from "natural" preservative systems, indicating formulation instability. Furthermore, as per the Japan Dermatological Association, the incidence of contact dermatitis from cosmetic preservatives rose by 18% between 2021 and 2023 due to inadequate substitutes.

Climatic Challenges Affecting Product Integrity

The tropical and subtropical climates prevalent to cosmetic product stability, increasing the burden on preservative systems is additionally to hinder the growth of the Asia Pacific cosmetic preservatives market. High temperature and humidity accelerate microbial proliferation and chemical degradation, particularly in water-based formulations stored without refrigeration. According to the Thai Meteorological Department, average relative humidity in Bangkok exceeds 75% for nine months of the year, with temperatures frequently surpassing 32°C—conditions ideal for mold and bacterial growth. The Vietnam Food Safety Authority reported in 2023 that 31% of cosmetic samples collected from retail outlets in Ho Chi Minh City showed microbial contamination, primarily in unrefrigerated lotions and liquid foundations. In the Philippines, the Department of Science and Technology documented a 25% higher spoilage rate for water-based cosmetics compared to those in temperate regions. These environmental stressors necessitate higher preservative concentrations or multi-system approaches, which can conflict with consumer demands for minimal ingredient lists. Additionally, rural distribution networks with inconsistent cold chains exacerbate the problem, hich is forcing brands to over-engineer preservation systems, increasing costs and limiting shelf-life predictability.

MARKET OPPORTUNITIES

Advancements in Bio-Based and Fermentation-Derived Preservatives

The innovation in bio-based and fermentation-derived preservatives is set to pose new opportunities for the growth of the Asia Pacific cosmetic preservatives market. Consumers and regulators alike are favoring sustainable, naturally sourced alternatives that offer effective microbial control without synthetic labels. Radish root ferment filtrate, leucidal liquid, and cultured dextrose are gaining traction as broad-spectrum preservatives in premium and natural product lines. According to the Japan Bioindustry Association, sales of fermentation-derived preservatives in Japan increased by 39% in 2023, with Shiseido and Pola Orbis integrating them into over 40 new product launches. South Korea’s Amorepacific has developed a proprietary lactic acid bacteria ferment that extends shelf life by 30% compared to traditional systems, as confirmed by internal stability testing in 2023. These developments align with circular economy goals and offer brands a pathway to differentiate through sustainability and science-backed efficacy.

Expansion of E-Commerce and Direct-to-Consumer Skincare Brands

The rapid rise of e-commerce and digital-native beauty brands for innovative and stable preservative systems is additionally to fuel the growth of the Asia Pacific cosmetic preservatives market. Platforms like Tmall, Lazada, and Nykaa have enabled niche brands to reach mass audiences, but with it comes the challenge of ensuring product integrity during extended logistics cycles. According to the Asia Pacific E-commerce Logistics Council, the average delivery time for cosmetics in Southeast Asia is 6.8 days, with products often exposed to high heat and humidity during transit. In response, direct-to-consumer brands such as The Ordinary (operating in India and China) and Dear, Klairs (South Korea) are reformulating with enhanced preservative blends to withstand distribution stress. Additionally, subscription-based skincare services in Australia and Japan require longer shelf lives, pushing brands toward synergistic systems combining phenoxyethanol, caprylyl glycol, and glyceryl caprylate.

MARKET CHALLENGES

Balancing Efficacy with Skin Compatibility

Formulators face persistent challenge in achieving microbial efficacy without compromising skin tolerance with rising prevalence of sensitive skin conditions, which is likely to inhibit the growth of the Asia Pacific cosmetic preservatives market. According to the Asian Society of Dermatology, the incidence of cosmetic contact dermatitis in urban populations across China, Japan, and South Korea rose from 8.3% in 2020 to 11.7% in 2023, with preservatives identified as the leading cause in 42% of cases. According to the Korean Food and Drug Safety Ministry, 1,152 adverse event notifications in 2023 linked to preservatives, prompting a temporary suspension of certain isothiazolinone-based products. The Japan Dermatological Society emphasizes that Asian skin types, which are more prone to irritation and post-inflammatory hyperpigmentation, require gentler preservation approaches. This delicate balance forces brands to adopt complex multi-preservative systems or invest in encapsulation technologies to minimize direct skin contact. However, such innovations increase R&D costs and regulatory scrutiny by making it difficult for smaller players to compete, thereby constraining market-wide formulation progress.

Fragmented Regulatory Landscape Across Countries

The lack of harmonized regulatory standards for cosmetic preservatives complicates compliance and slows product innovation, which is additionally to inhibit the growth of the Asia Pacific cosmetic preservatives market. Each country maintains distinct permissible concentration limits, banned substances, and testing protocols, forcing manufacturers to reformulate for individual markets. For example, while Japan permits up to 1.0% phenoxyethanol in leave-on products, Indonesia restricts it to 0.75%, and Australia requires specific labeling for concentrations above 0.5%. As per the Pacific Chemical Council, a single preservative system may require up to 14 different regulatory submissions to cover major APAC markets. Additionally, China’s National Medical Products Administration mandates full microbial challenge testing for all new products, a process that takes 28 days and costs over USD 15,000 per formulation. These disparities increase time-to-market and compliance costs, discouraging small and mid-sized brands from regional expansion.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.82 % |

| Segments Covered | By Product, Application, Raw Material, and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Akema S.R.L., Ashland Inc, BASF SE, Clariant AG, Evonik Industries AG, Lanxess AG, Symrise AG, Celanese Corp, Tate & Lyle Plc, and INEOS Group Holdings SA., and others |

SEGMENTAL ANALYSIS

By Product Insights

The paraben esters segment was accounted in holding 38.3% of the Asia Pacific cosmetic preservatives market share in 2024 due to their proven efficacy, broad-spectrum antimicrobial action, and cost efficiency in preserving water-based formulations. Methylparaben and propylparaben are particularly favored in multi-component skincare and haircare products across China, India, and Southeast Asia, where high humidity necessitates robust preservation. According to the China National Medical Products Administration, over 62% of registered lotions and creams in 2023 contained paraben esters, reflecting regulatory acceptance and formulator reliance. Their stability across a wide pH range and compatibility with other preservatives make them ideal for complex emulsions. The Indian Drug Manufacturers’ Association confirmed that 70% of Indian-manufactured facial toners and conditioners continue to use parabens due to their long-established safety profile under national guidelines. Furthermore, Japan’s Pharmaceuticals and Medical Devices Agency has reaffirmed the safety of parabens at concentrations up to 1.0%, supporting their continued use in sensitive skin products.

The organic salts segment is lucratively to grow with an expected CAGR of 10.7% during the forecast period with the rising demand for multifunctional, skin-friendly preservatives such as sodium benzoate, potassium sorbate, and calcium salicylate, which are perceived as safer and more natural. These compounds are increasingly used in synergistic blends with phenoxyethanol or caprylyl glycol to enhance efficacy while minimizing irritation. Australia’s National Industrial Chemicals Notification and Assessment Scheme has also observed a surge in notifications for organic salt-based systems, with 142 submissions in 2023 alone up 41% from 2022. Additionally, Thailand’s Department of Industrial Works has included potassium sorbate in its list of approved bio-preservatives for eco-labeled cosmetics, accelerating adoption in green-certified products.

By Application Insights

The facemasks, sunscreens, scrubs & lotions segment was accounted in holding 44.3% of the Asia Pacific cosmetic preservatives market share in 2024 with the high water content and multi-phase nature of these products, which create ideal conditions for microbial proliferation, especially in humid environments. These products require effective preservation to prevent contamination during storage and post-opening use. In India, the Central Drugs Standard Control Organization recorded a 35% increase in preservative-related compliance checks for lotions and scrubs in 2023, reflecting intensified regulatory scrutiny. Furthermore, Indonesia’s BPOM confirmed that 58% of contaminated cosmetic products seized in 2023 were from the lotion and mask category. The rise of at-home skincare routines, accelerated by post-pandemic consumer behavior, has increased product usage frequency and exposure to contamination, necessitating robust preservation.

The toothpaste and mouthwash segment is esteemed to grow with a CAGR of 9.4% in the coming years with the increasing recognition of oral microbiome balance and the need for effective preservation in aqueous oral formulations. According to the Indian Dental Association, 78% of commercially available mouthwashes in India contain at least two preservatives, typically a combination of sodium benzoate and cetylpyridinium chloride, to ensure long-term stability. In China, the National Health Commission reported that over 400 million units of functional toothpaste were sold in 2023, many of which contain herbal extracts and probiotics that require enhanced preservation. Additionally, Australia’s Dental Board noted a 22% increase in consumer complaints related to spoiled mouthwashes between 2021 and 2023, prompting brands to reformulate with more stable systems.

By Raw Material Insights

The synthetic segment was the largest by accounting for a dominant share of the Asia Pacific cosmetic preservatives market in 2024 with the synthetic preservatives remain the backbone of microbial protection due to their proven efficacy, consistency, and cost-effectiveness. Australian Institute of Food Science and Technology also confirmed that synthetic systems are 3.2 times more effective than natural alternatives in inhibiting Pseudomonas aeruginosa, a common contaminant in water-based cosmetics.

The natural raw material segment is anticipated to witness a CAGR of 12.1% from 2025 to 2033 owing to the escalating consumer demand for clean, transparent, and sustainable beauty products, particularly in urban centers across Japan, South Korea, and Australia. Natural preservatives such as radish root ferment filtrate, rosemary extract, and leucidal liquid are increasingly adopted in premium and organic skincare lines. India’s Ministry of AYUSH has also promoted the use of neem and tulsi extracts as preservative boosters in Ayurvedic cosmetics, with over 120 formulations approved in 2023. However, natural preservatives often require synergistic blends and have shorter shelf lives, which is prompting investment in stabilization technologies.

The natural raw material segment is anticipated to witness a CAGR of 12.1% from 2025 to 2033 owing to the escalating consumer demand for clean, transparent, and sustainable beauty products, particularly in urban centers across Japan, South Korea, and Australia. Natural preservatives such as radish root ferment filtrate, rosemary extract, and leucidal liquid are increasingly adopted in premium and organic skincare lines. In Japan, the Japan Organic Cosmetics Association reported that 63% of new organic product launches in 2023 featured natural preservatives, up from 41% in 2021. South Korea’s Amorepacific has integrated fermented radish root into 28 of its 2023 skincare launches, citing consumer preference for microbiome-friendly preservation. Additionally, Australia’s Clean Beauty Council noted a 47% increase in products labeled “naturally preserved” between 2022 and 2023. India’s Ministry of AYUSH has also promoted the use of neem and tulsi extracts as preservative boosters in Ayurvedic cosmetics, with over 120 formulations approved in 2023. However, natural preservatives often require synergistic blends and have shorter shelf lives, prompting investment in stabilization technologies. Despite higher costs and formulation complexity, their alignment with clean beauty, eco-labeling, and sustainability goals is driving rapid adoption, particularly among digital-native and premium brands seeking differentiation in a crowded market.

REGIONAL ANALYSIS

China Cosmetic Preservatives Market Analysis

China was the top performer of the Asia Pacific cosmetic preservatives market with 33.3% of share in 2025. The country produces over 2.1 million tons of skincare and haircare products annually, according to the National Bureau of Statistics, most of which require preservation due to high water content and extended shelf-life expectations. In 2023, over 8,400 new cosmetic products were registered, 67% of which contained phenoxyethanol or parabens, as per the China Cosmetics Regulatory Database. Additionally, the rise of local KOL-driven brands on platforms like Tmall and Douyin has accelerated product innovation, increasing demand for stable, safe preservatives. The government’s “Made in China 2025” initiative has also incentivized domestic production of specialty chemicals, reducing reliance on imports.

Japan Cosmetic Preservatives Market Analysis

Japan was ranked second by occupying 19.2% of the Asia Pacific cosmetic preservatives market share in 2024. Japanese consumers prioritize product safety, longevity, and mildness, which is leading to widespread use of well-studied preservatives like phenoxyethanol and sodium benzoate. The Pharmaceuticals and Medical Devices Agency enforces strict limits on microbial contamination, requiring all multi-use products to pass ISO 11930 challenge tests. According to the Japan Cosmetic Industry Association, 91% of facial lotions and emulsions launched in 2023 contained dual or triple preservative systems to ensure stability. The aging population has also increased demand for preservative-stable, low-irritant formulations for sensitive skin.

India Cosmetic Preservatives Market Analysis

India cosmetic preservatives market is esteemed to grow with the rising disposable incomes and urbanization. The Central Drugs Standard Control Organization has updated its cosmetic guidelines to mandate preservative efficacy testing by aligning with international standards. The popularity of gel-based cleansers and herbal toners in humid regions like Kerala and West Bengal has increased microbial risk, necessitating robust systems. Additionally, the rise of D2C brands such as Plum and Mamaearth has driven demand for transparent, safe preservation, with 74% of their products using phenoxyethanol-based blends, according to internal brand disclosures.

South Korea Cosmetic Preservatives Market Analysis

South Korea cosmetic preservatives market is growing steadily with the growing advanced skincare formulation and preservation technology. The country’s leadership in K-beauty has made it a global influencer in product stability, efficacy, and sensory experience. As per Korea Food and Drug Safety Ministry, 83% of skincare products launched in 2023 contained at least two preservatives to ensure shelf-life integrity. Amorepacific and LG Household & Health Care have pioneered cold-process formulations that rely on synergistic preservative blends to avoid heat degradation. In 2023, the Korea Institute of Science and Technology developed a nano-encapsulated phenoxyethanol system that reduces skin penetration by 40%, enhancing safety without compromising efficacy.

Australia Cosmetic Preservatives Market Analysis

Australia cosmetic preservatives market growth is solely growing with prominent opportunities in the next coming years owing to the high consumer awareness, strict safety standards, and a preference for natural, non-irritating ingredients. The Therapeutic Goods Administration mandates full preservative efficacy testing for all imported and domestically produced cosmetics, with over 1,100 dossiers submitted in 2023 alone. According to the Clean Beauty Australia Network, 58% of new product launches in 2023 featured “paraben-free” or “formaldehyde-free” claims, driving demand for alternatives like phenoxyethanol and organic salts. Additionally, the Australian Competition and Consumer Commission has cracked down on misleading “natural” claims, pushing companies toward verifiable, science-backed preservation.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific cosmetic preservatives market is shaped by a dynamic interplay between global chemical leaders and regionally focused innovators, all vying to address the dual demands of microbial safety and consumer acceptability. Multinational corporations such as BASF, Shin-Etsu, and Croda leverage technological superiority, regulatory expertise, and established supply chains to dominate high-performance segments, particularly in Japan, South Korea, and China. Their strength lies in offering preservatives with proven efficacy, consistency, and compliance with international standards. At the same time, regional players and specialty chemical firms are gaining ground by focusing on cost-effective solutions and natural alternatives tailored to local preferences in India, Southeast Asia, and Australia. The rise of clean beauty, e-commerce brands, and Ayurvedic or herbal cosmetics has intensified competition in the natural preservatives segment, prompting innovation in fermentation-derived and plant-based systems. Market differentiation is increasingly based on technical support, formulation compatibility, and sustainability credentials rather than price alone. Regulatory fragmentation across countries adds complexity, favoring companies with strong compliance infrastructure.

KEY MARKET PLAYERS

The key players in the Asia Pacific cosmetic preservatives market include

- Akema S.R.L.

- Ashland Inc.

- BASF SE

- Clariant AG

- Evonik Industries AG

- Lanxess AG

- Symrise AG

- Celanese Corp.

- Tate & Lyle Plc

- INEOS Group Holdings SA

TOP PLAYERS IN THE MARKET

- BASF is a leading innovator in the Asia Pacific cosmetic preservatives market, supplying high-performance synthetic and bio-based preservation systems tailored to regional formulation needs. The company’s Acticide™ and Euxyl™ product lines are widely used in water-based skincare, haircare, and hygiene products across China, India, and Southeast Asia. BASF has strengthened its regional footprint by establishing application laboratories in Shanghai and Mumbai, enabling formulators to test preservative efficacy under tropical conditions. In 2023, the company launched Acticide PE 100 XP, a formaldehyde-free, broad-spectrum booster designed for sensitive skin formulations, which was rapidly adopted by K-beauty and Ayurvedic brands. It also expanded its collaboration with Indian contract manufacturers to support clean-label reformulations.

- Shin-Etsu Chemical is a dominant force in the Asia Pacific cosmetic preservatives market, renowned for its high-purity methylparaben and phenoxyethanol, which are integral to skincare and personal care products across Japan, South Korea, and China. Leveraging its expertise in silicones and organic chemicals, the company produces preservatives with exceptional stability and low impurity profiles, meeting stringent regulatory standards. In 2023, Shin-Etsu introduced a new grade of ultra-low-endotoxin phenoxyethanol for use in baby care and ophthalmic cosmetics, responding to rising demand for dermatologically safe ingredients. The company also enhanced its supply chain resilience by increasing production capacity at its Niigata facility to meet growing regional demand. Its close partnerships with Japanese and Korean OEMs allow rapid integration of its preservatives into premium product lines. Additionally, Shin-Etsu has invested in lifecycle assessments to demonstrate the environmental safety of its products, supporting brands pursuing eco-certifications.

- Kao Corporation plays a pivotal role in the Asia Pacific cosmetic preservatives market through its in-house development and integration of preservation systems into its extensive portfolio of consumer brands, including Bioré, Jergens, and Attack. The company emphasizes mild, multi-functional preservation that aligns with its “safety-first” formulation philosophy, particularly in products for sensitive and pediatric skin. Kao has developed proprietary preservation blends combining phenoxyethanol with natural-derived boosters like ethylhexylglycerin to reduce irritation while maintaining efficacy. In 2023, it launched a new sulfate-free, paraben-free facial cleanser line in China and Southeast Asia, utilizing a synergistic system that passed ISO 11930 challenge tests under tropical storage conditions. The company also collaborates with Japanese dermatological institutes to validate the skin compatibility of its preservative systems.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Asia Pacific cosmetic preservatives market are deploying multifaceted strategies to maintain competitive advantage amid evolving consumer and regulatory pressures. Firms are investing in regional R&D hubs to tailor preservative efficacy to tropical climates and local formulation practices. Vertical integration is common, with leading suppliers securing control over raw material sourcing to ensure purity and supply continuity. Strategic collaborations with cosmetic manufacturers and regulatory consultants enable faster compliance with diverse national standards. Capacity expansion is evident in Japan, China, and India, where new production lines are being commissioned to meet rising demand. Companies are also enhancing technical support services, offering formulation guidance and challenge testing assistance to clients. Digital engagement platforms are being introduced to streamline customer onboarding and product selection. Additionally, sustainability is a growing focus, with investments in bio-based feedstocks and recyclable packaging for preservative ingredients. These strategies collectively enable key participants to balance efficacy, safety, and regulatory alignment while strengthening client loyalty and market responsiveness.

RECENT HAPPENINGS IN THE MARKET

- In February 2023, BASF launched Acticide PE 100 XP, a formaldehyde-free preservative booster, in Shanghai, which is targeting sensitive skin formulations and expanding its portfolio for clean beauty brands across Asia Pacific.

- In May 2023, Shin-Etsu Chemical introduced a new ultra-low-endotoxin grade of phenoxyethanol at its Niigata facility, enhancing product safety for use in baby care and ophthalmic cosmetics in Japan and export markets.

- In July 2023, Kao Corporation initiated a collaboration with the University of Tokyo’s Dermatology Research Center to evaluate the skin compatibility of its next-generation preservation blends under high-humidity conditions.

- In October 2023, BASF expanded its technical service team in Mumbai by deploying formulation specialists to support Indian cosmetic manufacturers in transitioning to compliant, low-irritancy preservative systems.

- In January 2024, Shin-Etsu Chemical increased production capacity for methylparaben at its Yokkaichi plant by 20%, which is reinforcing supply stability for key customers in South Korea.

MARKET SEGMENTATION

This research report on the Asia Pacific cosmetic preservatives market has been segmented and sub-segmented based on the following categories.

By Product

- Formaldehyde Donors

- Inorganics

- Paraben Esters

- Alcohols

- Phenol Derivatives

- Quaternary Compounds

- Organic Salts

- Others

By Application

- Conditioners & Shampoos

- Facemasks, Sunscreens, Scrubs & Lotions

- Shower Cleansers, Soaps and Shaving Gels

- Powder Compacts and Face Powder

- Toothpaste and Mouthwash

By Raw Material

- Synthetic

- Natural

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia Pacific

Frequently Asked Questions

1. What is the Asia Pacific cosmetic preservatives market?

It is the regional market for chemical and natural preservatives used in cosmetics and personal care products to prevent microbial growth and extend shelf life.

2. What drives the demand for cosmetic preservatives in Asia Pacific?

Growing demand for skincare and personal care products, rising consumer awareness of hygiene, and expanding beauty industries drive the market.

3. Which countries dominate the Asia Pacific cosmetic preservatives market?

China, Japan, South Korea, and India are the leading markets due to large consumer bases and strong cosmetic industries.

4. What types of preservatives are commonly used in cosmetics?

Parabens, phenoxyethanol, formaldehyde releasers, organic acids, and natural preservatives are widely used.

5. What challenges does the Asia Pacific cosmetic preservatives market face?

Stringent regulatory requirements and rising concerns over the safety of synthetic preservatives pose challenges.

6. Who are the major players in the Asia Pacific cosmetic preservatives market?

Key players include BASF SE, Clariant AG, Lonza Group, Ashland Inc., and Symrise AG.

7. What role do regulations play in this market?

Government policies and cosmetic safety regulations shape preservative usage, particularly for parabens and formaldehyde releasers.

8. What is the growth outlook for the Asia Pacific cosmetic preservatives market?

The market is expected to grow steadily, supported by rapid urbanization, rising disposable incomes, and increased beauty product consumption.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com