Asia Pacific Sports Medicine Market Size, Share, Trends & Growth Forecast Report By Product (Reconstruction and Repair, Support and Recovery Accessories), Application & Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of Asia-Pacific), Industry Analysis From 2026 to 2034

Asia-Pacific Sports Medicine Market Size

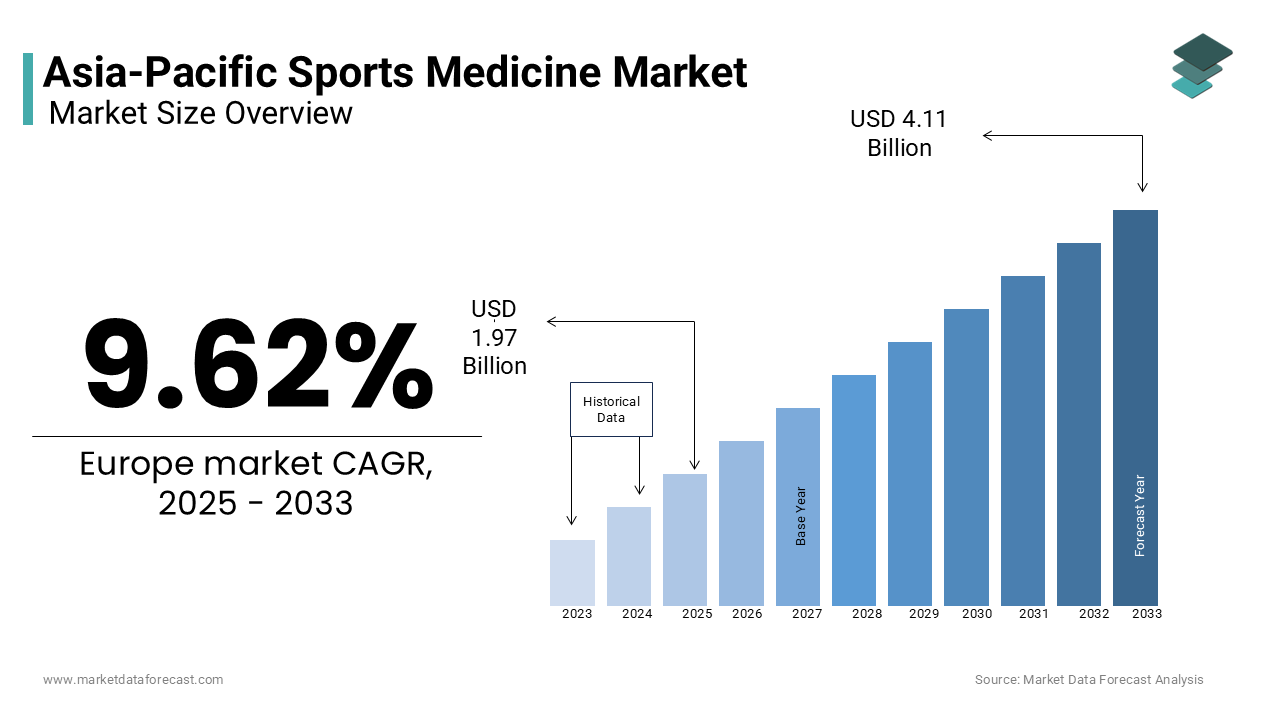

The Asia Pacific Sports Medicine Market size was valued at USD 1.97 billion in 2025 and is anticipated to reach USD 2.16 billion in 2026 from USD 4.50 billion by 2034, growing at a CAGR of 9.62% during the forecast period from 2026 to 2034.

The sports medicine is aimed at preventing, diagnosing, and treating injuries related to sports and physical activity. This includes orthopedic implants, braces and supports, rehabilitation devices, and regenerative therapies. According to the World Health Organization, physical inactivity is a major public health concern in the Asia Pacific region, contributing to rising rates of chronic diseases and musculoskeletal disorders. This has indirectly spurred interest in sports medicine as a preventive and rehabilitative healthcare discipline.

MARKET DRIVERS

Rise in Sports Participation and Injury Incidence

The increasing participation in organized sports and fitness activities, which has led to a corresponding rise in sports-related injuries is accelerating the growth of the Asia Pacific sports medicine market. As per the International Olympic Committee, the number of registered athletes in Asia has grown by over 22% between 2017 and 2023, with countries like China, India, and Indonesia witnessing the most substantial growth. This surge in athletic participation has led to a higher incidence of musculoskeletal injuries, including ligament tears, fractures, and joint dislocations. According to a 2023 study published in the Asia-Pacific Journal of Sports Medicine, sports injury cases in the region increased by 18% annually over the past decade, with knee injuries accounting for 35% of all reported cases. This has created a growing demand for diagnostic imaging, orthopedic implants, and rehabilitation therapies. Additionally, as per the National Sports Development Board of India, over 60% of sports injuries occur in youth athletes, indicating a long-term need for advanced sports medicine interventions. The growing awareness of timely diagnosis and treatment among athletes and coaches has also contributed to the market’s expansion. The increasing number of sports clinics and dedicated rehabilitation centers across urban centers in Australia, Japan, and South Korea further supports this trend.

Advancements in Regenerative Medicine and Minimally Invasive Procedures

The rapid advancement in regenerative medicine and minimally invasive surgical techniques is additionally fuelling the growth of the Asia Pacific sports medicine market. These innovations have significantly improved recovery times and outcomes for athletes suffering from chronic injuries. For instance, stem cell therapy, platelet-rich plasma (PRP) injections, and tissue engineering have gained traction in countries like Japan and South Korea, where healthcare systems support cutting-edge medical research. According to the Japanese Society for Regenerative Medicine, over 12,000 regenerative therapy procedures were performed in 2022 alone, with a significant proportion addressing sports-related injuries. Moreover, the adoption of arthroscopic surgeries, which are less invasive and reduce recovery periods, has risen sharply. As per the Asia-Pacific Arthroplasty Registry, the number of arthroscopic procedures increased by 14% year-over-year in 2023. In addition, the increasing availability of biologics such as visco-supplements and growth factor therapies has further fueled the market. The Australian Orthopaedic Association reported that 40% of orthopedic surgeons in the country now incorporate biologic therapies into their treatment protocols for sports injuries.

MARKET RESTRAINTS

High Cost of Advanced Sports Medicine Treatments

The high cost associated with advanced treatment modalities, which limits their accessibility, especially in developing economies is limiting the growth of the Asia Pacific sports medicine markets. As per a 2023 report by the Asia Pacific Health Policy Forum, the average cost of a PRP injection in India ranges between USD 600 and USD 1,200, which is prohibitively expensive for the average citizen. In the Philippines, where healthcare spending per capita is among the lowest in the region, access to advanced diagnostics and surgical interventions remains limited. Even in more developed markets like Australia, the cost of sports medicine treatments not covered by Medicare can be substantial. The Australian Institute of Health and Welfare noted that over 30% of patients delay or forgo treatment due to financial constraints.

Limited Awareness and Lack of Skilled Professionals

The limited awareness among the general population regarding sports injury prevention and appropriate treatment options is restricting the growth of the Asia Pacific sports medicine market. This is particularly evident in rural and semi-urban areas where access to specialized sports medicine professionals is scarce. According to the Indian Journal of Orthopaedics, only 12% of orthopedic surgeons in India are trained in sports medicine, despite a growing number of sports-related injuries. In Indonesia, as per the Indonesian Medical Association, there are fewer than 200 certified sports medicine specialists for a population exceeding 270 million. This shortage of skilled professionals results in delayed or improper treatment, leading to long-term complications. Moreover, awareness campaigns and preventive education programs are minimal in many parts of the region. As per the Asia-Pacific Journal of Sports Medicine, only 20% of schools in Thailand and Vietnam have access to sports injury prevention programs.

MARKET OPPORTUNITIES

Expansion of Telemedicine and Digital Health Platforms

The rapid expansion of telemedicine and digital health platforms, which are transforming how patients access sports injury consultations and rehabilitation guidance is setting new growth opportunities for the growth of the Asia Pacific sports medicine market. According to the Asia Pacific Telehealth Association, the number of telehealth consultations in the region increased by 45% in 2023 compared to the previous year. In India, the Ministry of Health and Family Welfare reported that over 8 million teleconsultations were conducted in 2022, with a growing share related to musculoskeletal and sports injuries. Furthermore, digital platforms are increasingly integrating artificial intelligence (AI) and machine learning to offer predictive analytics for injury prevention. For instance, in Japan, AI-powered wearables are being used by professional sports teams to monitor biomechanics and reduce injury risks.

Government Initiatives and Public-Private Partnerships in Sports Infrastructure

The increasing government focus on developing sports infrastructure and promoting athlete health through public-private partnerships is also to fuel the growth of the Asia Pacific sports medicine market. Governments across the region are investing heavily in building sports academies, fitness centers, and rehabilitation clinics to support the growing athlete population. According to the ASEAN Sports Development Plan 2025, member countries have committed over USD 5 billion to enhance sports infrastructure and athlete healthcare. As per the Chinese Sports Medicine Association, over 200 sports medicine centers have been established in the last five years with government and private sector collaboration. In Australia, the Department of Health has partnered with private hospitals and universities to create a national sports injury database aimed at improving prevention and treatment strategies.

MARKET CHALLENGES

Regulatory Hurdles and Inconsistent Approval Processes

The inconsistent regulatory environment across different countries, which complicates product approvals and market entry for medical device manufacturers and pharmaceutical companies is hampering the growth of the Asia Pacific sports medicine market. This inconsistency delays the introduction of new technologies and therapies, affecting patient access and hindering market growth. Additionally, in countries like Indonesia and the Philippines, unclear guidelines and frequent policy changes create uncertainty for foreign investors. Furthermore, the lack of standardized clinical trial protocols for regenerative therapies and biologics across the region adds another layer of complexity. In South Korea, while the Ministry of Food and Drug Safety has introduced fast-track approvals for innovative therapies, similar mechanisms are not uniformly available elsewhere.

Cultural and Societal Attitudes Toward Sports Injuries

The prevailing cultural and societal attitudes toward sports injuries in certain countries where traditional beliefs and reluctance to seek timely medical intervention persist is additionally to hamper the growth of the Asia Pacific sports medicine market. In many parts of South and Southeast Asia, there is a tendency to rely on home remedies, alternative medicine, or general practitioners rather than seeking specialized sports medicine care. According to the Asia Pacific Journal of Sports Medicine, a 2023 survey conducted in rural India found that 68% of respondents preferred consulting local healers or using Ayurvedic treatments for musculoskeletal injuries, delaying proper diagnosis and treatment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.62% |

| Segments Covered | By Product, Application and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the Rest of Asia Pacific. |

| Market Leaders Profiled | Smith & Nephew PLC., Arthrex, Inc., Össur hf, Stryker Corporation, Conmed Corporation, Zimmer Biomet Holdings, Inc., Breg, Inc., Mueller Sports Medicine, Inc., Tornier, Inc., Skins International Trading AG, Wright Medical Technology, Inc., DePuy Mitek, Inc., 3M Company Ace Brand, OttoBock Healthcare GmbH and DJO Global, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The reconstruction and repair segment was accounted in holding 58.3% of the Asia Pacific sports medicine market share in 2025 with the rising prevalence of ligament and tendon injuries, particularly among athletes and aging populations. According to the Asia Pacific Orthopaedic Association, anterior cruciate ligament (ACL) injuries alone account for nearly 40% of all knee injuries in the region, with surgical reconstruction being the most common treatment. Additionally, Japan has seen a surge in the use of bioabsorbable implants due to their reduced recovery time and minimal complications. As per the Japanese Society of Arthroscopic Surgery, over 85,000 arthroscopic reconstruction procedures were performed in 2022. The increasing availability of premium orthopedic implants and the presence of global players such as Smith & Nephew and Zimmer Biomet in countries like Australia and South Korea further bolster this segment’s growth. The integration of robotic-assisted surgical systems in sports medicine procedures is also contributing to the expansion of this segment in developed markets.

The support and recovery accessories segment is projected to grow with a CAGR of 11.2% during the forecast period due to the increasing adoption of non-invasive treatment options and the rising awareness regarding injury prevention and rehabilitation. Moreover, the growing popularity of wearable technology in sports rehabilitation is fueling market expansion. According to the Japan Sports Agency, over 70,000 wearable recovery devices were sold in Japan in 2022, with athletes using them for real-time muscle monitoring and post-exercise recovery. In Australia, the National Rugby League has mandated the use of shoulder and knee supports for high-risk players, boosting the demand for recovery accessories.

By Application Insights

The knee injuries segment dominated the Asia Pacific sports medicine market with 32.3% of share in 2024 with the high incidence of anterior cruciate ligament (ACL) tears, meniscal injuries, and patellar dislocations, particularly among athletes involved in high-impact sports such as soccer, basketball, and rugby. According to the Asia Pacific Knee, Arthroscopy and Sports Medicine Society (APKASS), over 1.2 million knee injury cases were reported in the region in 2022, with a significant proportion requiring surgical intervention. In China, the Chinese Sports Medicine Association reported a 20% increase in knee-related hospitalizations between 2020 and 2023, largely due to rising youth participation in sports. Japan, with its aging population, also sees a growing number of degenerative knee conditions, further contributing to market demand.

The head injuries segment is expected to grow with a CAGR of 13.1% over the forecast period owing to the rising awareness of concussions and traumatic brain injuries (TBIs) in contact sports such as boxing, football, and cycling. According to the World Health Organization’s 2023 report on global sports injuries, the Asia Pacific region accounts for over 25% of all sports-related TBIs globally, with Australia and New Zealand reporting the highest per capita incidence. The growing implementation of strict concussion protocols in professional leagues such as the Australian Football League and the Indian Premier League has further boosted the demand for advanced diagnostic tools and recovery therapies. As per the Indian Journal of Neurotrauma, the number of sports-related concussion cases in India increased by 34% between 2020 and 2023. In addition, the adoption of cutting-edge technologies such as impact sensors and neuroimaging is accelerating market growth.

REGIONAL ANALYSIS

China Sports Medicine Market Analysis

China was the top performer in the Asia Pacific sports medicine market by holding 24.3% of the share in 2025 with the rapidly growing sports industry, increasing healthcare expenditure, and government initiatives to promote sports science and athlete health. The Chinese Sports Medicine Association reported that the number of sports medicine clinics in the country has more than doubled since 2018, reaching over 1,500 in 2023. Additionally, the rise in participation in professional and amateur sports, coupled with an aging population suffering from degenerative joint conditions, has significantly boosted demand for orthopedic implants and regenerative therapies. According to the National Medical Products Administration, over 200,000 arthroscopic surgeries were performed in China in 2022, a 22% increase from the previous year. The presence of both domestic and international players such as Zimmer Biomet, Johnson & Johnson, and MicroPort Orthopedics has further strengthened the market.

Japan Sports Medicine Market Analysis

Japan was positioned second in the Asia Pacific sports medicine market with 18.3% of share in 2025 due to strong healthcare infrastructure, high per capita healthcare spending, and emphasis on advanced medical technologies have contributed to its leading position. This has enabled widespread adoption of minimally invasive procedures and regenerative medicine, particularly in sports injury treatment. The Japanese Society of Regenerative Medicine reported that over 12,000 regenerative therapy procedures were conducted in 2022, with a significant portion addressing sports-related musculoskeletal injuries. Moreover, Japan’s aging population has led to a surge in demand for joint replacement and rehabilitation services.

Australia Sports Medicine Market Analysis

Australia sports medicine market growth is driven by a strong sporting culture, well-established healthcare systems, and proactive government policies. The country has one of the highest rates of sports participation globally with over 13 million Australians engaging in regular physical activity, as reported by Sport Australia in 2023. This high participation rate has resulted in a corresponding increase in sports-related injuries, which is fueling demand for advanced diagnostic and treatment solutions. According to the Australian Institute of Health and Welfare, over 300,000 sports-related hospitalizations were recorded in 2022, with knee and shoulder injuries being the most prevalent. The government has responded by investing in specialized sports injury clinics and integrating sports medicine into national health programs.

South Korea Sports Medicine Market Analysis

South Korea sports medicine market is likely to grow with the rapid technological advancements, increasing investment in sports science, and a growing focus on athlete performance optimization. According to the Korea Sports Promotion Foundation, the government invested over USD 900 million in sports development programs in 2023, including the establishment of high-tech sports injury rehabilitation centers. South Korea’s healthcare system supports early diagnosis and treatment through comprehensive insurance coverage, encouraging patients to seek timely medical intervention. As per the National Health Insurance Service, over 80% of sports medicine procedures are partially or fully covered under the national health scheme. The country is also a leader in regenerative medicine and biologics, with institutions like the Korea Advanced Institute of Science and Technology (KAIST) conducting extensive research in stem cell therapy and tissue engineering for sports injuries.

India Sports Medicine Market Analysis

India sports medicine market is expected to grow with the increasing sports participation, rising awareness of musculoskeletal health, and government-backed initiatives to promote athlete healthcare. According to the Ministry of Youth Affairs and Sports, over 500,000 athletes were registered under the Khelo India program in 2023, with a focus on injury prevention and rehabilitation. The Indian Orthopaedic Association reported that sports-related injuries increased by 24% between 2020 and 2023, particularly among youth athletes. In response, the government has established over 100 dedicated sports injury clinics across the country under the Ayushman Bharat initiative. As per the National Health Authority, nearly 2 million sports injury consultations were recorded in 2022, with knee and shoulder injuries being the most common.

COMPETITIVE LANDSCAPE

The Asia Pacific sports medicine market is highly competitive, characterized by the presence of global medical device giants and a growing number of regional players. Competition is driven by continuous product innovation, technological advancements, and the expansion of distribution networks to reach both urban and rural patient populations. Major international players such as Smith & Nephew, Zimmer Biomet, and Stryker maintain a strong foothold in developed markets like Australia, Japan, and South Korea, where healthcare infrastructure supports the adoption of advanced surgical and rehabilitative solutions. However, in emerging economies such as India, China, and Southeast Asian countries, domestic and regional companies are increasingly challenging global firms by offering cost-effective alternatives and leveraging local market knowledge. Strategic collaborations, partnerships with sports organizations, and investments in research and development play a crucial role in maintaining a competitive edge. Additionally, the growing emphasis on digital health solutions, including telemedicine and AI-driven diagnostics, is reshaping market dynamics.

KEY MARKET PLAYERS

A few of the notable companies operating in the Asia Pacific Sports Medicine Market include

- Smith & Nephew PLC

- Arthrex, Inc.

- Össur hf

- Stryker Corporation

- Conmed Corporation

- Zimmer Biomet Holdings, Inc.

- Breg, Inc.

- Mueller Sports Medicine, Inc.

- Tornier, Inc.

- Skins International Trading AG

- Wright Medical Technology, Inc.

- DePuy Mitek, Inc.

- 3M Company Ace Brand

- OttoBock Healthcare GmbH

- DJO Global, Inc

Top Players in the Asia Pacific Sports Medicine Market

Smith & Nephew plc

Smith & Nephew is a leading global medical technology company with a strong presence in the Asia Pacific sports medicine market. The company offers a comprehensive portfolio of products, including arthroscopic devices, orthopedic implants, and advanced wound care solutions tailored for sports-related injuries. In the Asia Pacific region, Smith & Nephew has been instrumental in driving innovation through localized R&D initiatives and strategic partnerships with hospitals and sports academies. Their focus on minimally invasive surgical techniques and regenerative therapies has positioned them as a preferred choice among orthopedic surgeons and sports medicine professionals across Australia, Japan, and South Korea.

Zimmer Biomet Holdings, Inc.

Zimmer Biomet is a major player in the global orthopedic and sports medicine industry, with a strong footprint in the Asia Pacific region. The company provides a wide range of sports medicine solutions, including joint reconstruction implants, biologics, and surgical instruments. In the Asia Pacific region, Zimmer Biomet has been actively expanding its distribution network and investing in digital health platforms to enhance patient outcomes. Their emphasis on training programs for surgeons and collaboration with national sports federations has significantly contributed to market development. The company’s commitment to innovation and regional expansion has made it a key influencer in shaping the sports medicine landscape in countries like India, China, and Australia.

Stryker Corporation

Stryker is a prominent global medical technology company with a robust presence in the Asia Pacific sports medicine market. The company specializes in orthopedic and neurotechnology solutions, offering advanced implants, surgical navigation systems, and rehabilitation devices tailored for sports injuries. In the Asia Pacific region, Stryker has been expanding through strategic acquisitions and partnerships to strengthen its product portfolio and distribution capabilities. The company has also invested in digital platforms and robotic-assisted surgical systems to cater to the growing demand for precision in sports injury treatments. Their engagement with local healthcare providers and sports organizations has enhanced awareness and adoption of modern sports medicine practices in emerging markets across Southeast Asia and Oceania.

Top Strategies Used by Key Market Participants

Strategic Collaborations and Partnerships

A key strategy adopted by leading players in the Asia Pacific sports medicine market is forming strategic collaborations and partnerships with academic institutions, sports organizations, and healthcare providers. These alliances help companies gain insights into regional medical needs, develop tailored products, and enhance clinical training for healthcare professionals. The companies can improve market penetration and ensure their solutions meet the evolving demands of sports medicine in diverse healthcare environments.

Product Innovation and Technological Advancements

Continuous innovation in product design and the integration of advanced technologies are central to maintaining a competitive edge in the market. Companies are investing in research and development to introduce next-generation implants, biologics, and robotic-assisted surgical systems. These innovations not only improve treatment outcomes but also support faster recovery, which is particularly important for athletes. The adoption of digital platforms and wearable technologies further enhances diagnostic accuracy and post-treatment monitoring, strengthening the market position of key players.

Expansion Through Mergers and Acquisitions

Many market leaders are expanding their regional presence through strategic mergers and acquisitions. By acquiring local or niche companies, global players can quickly integrate into new markets, access emerging technologies, and strengthen their distribution networks. This approach allows for faster market entry, particularly in developing economies where regulatory and logistical challenges can be significant. Mergers and acquisitions also enable companies to diversify their product portfolios and enhance service offerings to meet the growing demand for comprehensive sports medicine solutions.

RECENT MARKET DEVELOPMENTS

- In February 2024, Smith & Nephew launched a new line of arthroscopic implants tailored for the Asia Pacific market, which is aiming to enhance surgical precision and recovery outcomes for athletes.

- In May 2024, Zimmer Biomet partnered with a leading sports science institute in South Korea to develop region-specific rehabilitation protocols and training programs for orthopedic surgeons.

- In July 2024, Stryker introduced a digital patient monitoring platform in Australia that designed to support post-operative care and improve long-term recovery tracking for sports injury patients.

- In September 2024, a major Japanese medical device company expanded its distribution network in Southeast Asia by focusing on increasing access to orthopedic braces and recovery accessories.

- In November 2024, an Indian orthopedic solutions provider collaborated with a telemedicine startup to offer remote consultations and physiotherapy guidance for sports injuries across rural and semi-urban regions.

MARKET SEGMENTATION

This research report on the Asia Pacific sports medicine market is segmented and sub-segmented into the following categories.

By Product

- Reconstruction and Repair

- Implants

- Prosthetics

- Arthroscopy Devices

- Fracture and Ligament Repair Products

- Orthobiologics

- Support and Recovery

- Braces and Support

- Thermal Therapy Products

- Topical Pain Relief Products

- Compression Clothing

- Monitoring Devices

- Other Body Support and Recovery Products

- Accessories

By Application

- Head Injuries

- Shoulder Injuries

- Elbow and Wrist Injuries

- Back and Spine Injuries

- Hip and Groin Injuries

- Knee Injuries

- Foot and Ankle Injuries

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com