Global Biomaterials Market Size, Share, Trends & Growth Forecast Report By Material Type (Ceramic Biomaterials, Metallic Biomaterials, Polymer Biomaterials and Natural Biomaterials, Application and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) - Industry Analysis (2025 to 2033)

Global Biomaterials Market Summary

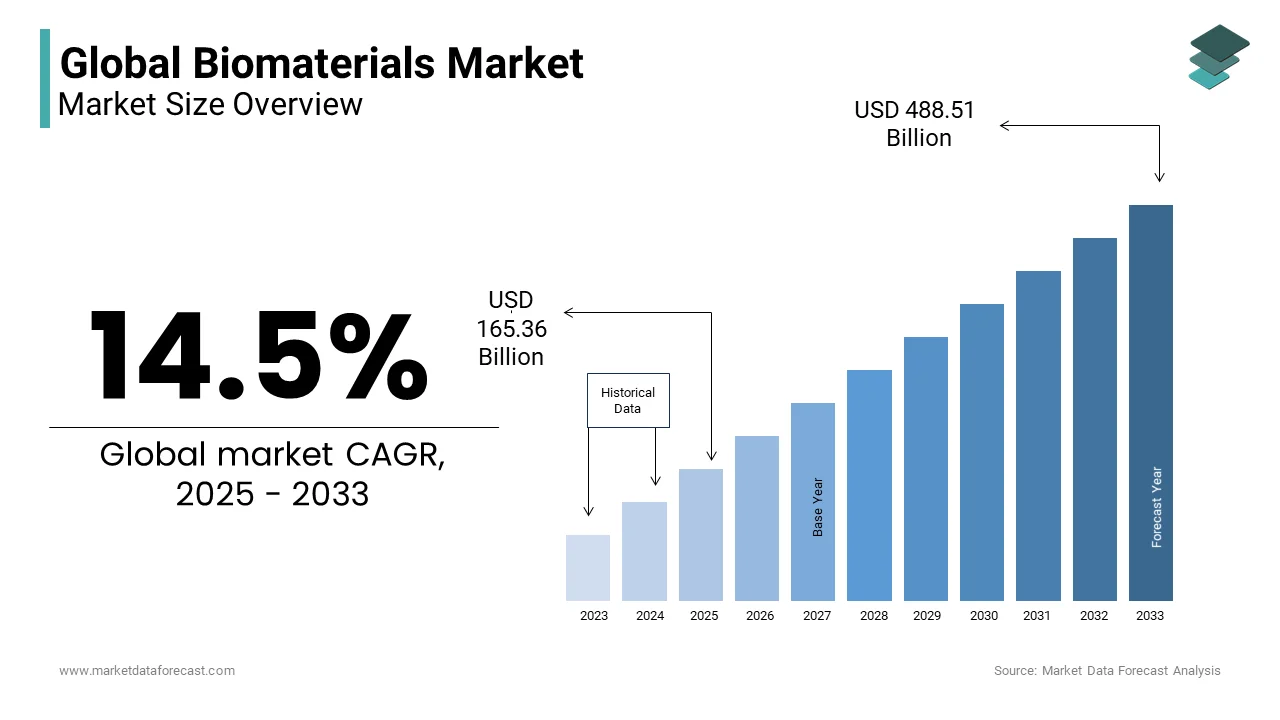

The global biomaterials market was valued at USD 144.42 billion in 2024 and is projected to reach USD 165.36 billion in 2025 before surging to USD 488.51 billion by 2033, expanding at a CAGR of 14.5% from 2025 to 2033. The rising demand for advanced medical implants, regenerative medicine, and tissue engineering solutions, alongside increasing adoption of biomaterials in orthopedics, cardiovascular devices, wound care, and dental applications are propelling the biomaterials market growth worldwide. Continuous innovations in biocompatible polymers, ceramics, and bioresorbable materials are further shaping the market.

Key Market Trends

- Expanding use of biodegradable polymers and bioresorbable implants in medical applications.

- Growing focus on 3D printing of biomaterials for customized implants.

- Rising prevalence of musculoskeletal disorders and cardiovascular diseases boosting biomaterial adoption.

- Increased R&D investments in tissue engineering and regenerative medicine.

- Strategic collaborations between biotech companies and healthcare providers to develop next-gen biomaterials.

Segmental Insights

- Based on biomaterial type, the polymer biomaterials segment dominated the market with 38.2% share in 2024, owing to their versatility, cost-effectiveness, and wide usage in implants and drug delivery systems.

- Based on application, the orthopedic segment accounted for 32.1% of the global biomaterials market share in 2024, driven by rising hip and knee replacement surgeries.

Regional Insights

- North America was the top-performing market, capturing 40.3% of the global share in 2024, supported by advanced healthcare infrastructure and high adoption of innovative biomaterials.

- Europe shows strong growth potential, with rising demand for biomaterials in regenerative therapies and aging population care.

- Asia-Pacific is expected to grow rapidly due to expanding healthcare access, government investments, and increasing medical tourism.

- Latin America is witnessing steady adoption, driven by orthopedic and dental care advancements.

- Middle East & Africa are gradually expanding in biomaterials usage, supported by healthcare modernization and rising chronic disease prevalence.

Competitive Landscape

Key players in the global biomaterials market include Carpenter Technology Corporation (United States), Evonik Industries (Germany), Berkeley Advanced Biomaterials (United States), Royal DSM (Netherlands), BASF SE (Germany), Corbion (Netherlands), Cam Bioceramics B.V. (Netherlands), Celanese Corporation (United States), CoorsTek Inc. (United States), CeramTec (Germany), and GELITA AG (Germany). These companies are focusing on product innovation, partnerships with healthcare providers, and scaling production capabilities to strengthen their global presence.

Global Biomaterials Market Size

The global biomaterials market size was valued at USD 144.42 billion in 2024. The biomaterials market size is expected to have a 14.5% CAGR from 2025 to 2033 and be worth USD 488.51 billion by 2033 from USD 165.36 billion in 2025.

The Biomaterials are biological systems for medical purposes, which range from diagnostics and drug delivery to tissue engineering and implantable devices. The development of smart biomaterials capable of responding to physiological stimuli, such as pH or temperature changes, has further expanded their clinical utility. According to the National Institutes of Health, over 300,000 surgical procedures in the Asia-Pacific region alone involved biomaterial-based implants in 2022, reflecting growing clinical reliance. Furthermore, as per data published by the World Health Organization, the prevalence of musculoskeletal disorders has increased by 25% globally since 2010, directly escalating demand for orthopedic biomaterials. The integration of biomaterials in dental prosthetics, cardiovascular stents, and wound care matrices underscores their multidisciplinary role. Academic and industrial collaboration in countries like Japan and South Korea has accelerated translational research, with over 1,200 peer-reviewed studies on novel biomaterial applications indexed in PubMed in 2023.

MARKET DRIVERS

The rising prevalence of chronic diseases and trauma-related injuries

The rising prevalence of chronic diseases and trauma-related injuries is propelling the growth of the biomaterials market. Cardiovascular diseases, diabetes, and osteoarthritis necessitate long-term medical interventions where biomaterials play a crucial role in implants, scaffolds, and drug delivery systems. As per the Global Burden of Disease Study conducted by the Institute for Health Metrics and Evaluation, non-communicable diseases accounted for 74% of all global deaths in 2021, with cardiovascular conditions alone responsible for over 19 million fatalities. This escalating disease burden has intensified the demand for vascular grafts, biodegradable stents, and artificial joints. In India, the All India Institute of Medical Sciences reported that over 700,000 joint replacement surgeries were performed in 2022, a 40% increase from 2018, driven by aging populations and sedentary lifestyles.

Advancements in regenerative medicine and tissue engineering

Advancements in regenerative medicine and tissue engineering are escalating the growth of the Biomaterials Market. The ability to engineer scaffolds that support cell adhesion, proliferation, and differentiation has revolutionized approaches to organ repair and replacement. As per the U.S. Food and Drug Administration, over 20 tissue-engineered products have received regulatory approval since 2010, including skin substitutes and cartilage repair systems. The Wake Forest Institute for Regenerative Medicine has successfully implanted laboratory-grown bladders in human patients, demonstrating the clinical viability of scaffold-based constructs. Natural polymers such as fibrin and hyaluronic acid, alongside synthetic variants like polylactic-co-glycolic acid (PLGA), are increasingly used to fabricate 3D matrices that degrade in sync with tissue regeneration. In Japan, the approval of a corneal epithelial cell sheet for treating corneal blindness marks a milestone in regenerative therapies reliant on biomaterial carriers. These innovations are not only enhancing clinical outcomes but also reducing dependency on donor organs, with the United Network for Organ Sharing reporting that over 100,000 patients await transplants in the U.S. alone.

MARKET RESTRAINTS

Stringent regulatory pathways and prolonged approval timelines

Stringent regulatory pathways and prolonged approval timelines are hampering the growth of the biomaterials market. As per the U.S. Food and Drug Administration, the average time for regulatory approval of a Class III medical device, many of which incorporate advanced biomaterials, exceeds five years, with nearly 30% of submissions requiring multiple review cycles. In the European Union, the implementation of the Medical Device Regulation (MDR) in 2021 has further intensified scrutiny, requiring robust clinical evidence for legacy devices, leading to delays in market access. Additionally, the complexity of characterizing biomaterial-tissue interactions necessitates costly Good Laboratory Practice (GLP) and Good Manufacturing Practice (GMP) adherence.

High production costs and limited scalability

High production costs and limited scalability of advanced biomaterials are expected to hinder the growth of the Biomaterials Market. The synthesis of biocompatible polymers, such as polyetheretherketone (PEEK) or bioactive glass, involves complex purification processes, sterile manufacturing environments, and stringent quality control, significantly inflating production expenses. Furthermore, the fabrication of 3D porous scaffolds using techniques like electrospinning or selective laser sintering demands specialized equipment and skilled labor, limiting large-scale output. In clinical settings, this translates into high procedure prices; a single biodegradable vascular stent can cost upwards of $5,000, placing it beyond the reach of many healthcare systems. Additionally, supply chain vulnerabilities were exposed during the pandemic; the International Chamber of Commerce reported that 60% of medical material manufacturers in China faced raw material shortages in 2021, disrupting biomaterial production.

MARKET OPPORTUNITIES

Expansion of bioprinting and personalized implant technologies

Expansion of bioprinting and personalized implant technologies biomaterials domain is set to create new opportunities for the growth of the Biomaterials Market. Institutions like the University Medical Center Utrecht have successfully implanted 3D-printed titanium mandibles tailored to individual patients, reducing surgical time and improving aesthetic outcomes. Biomaterials such as beta-tricalcium phosphate and patient-derived hydrogels are being integrated into printing inks to enhance bioactivity. The European Bioprinting Society notes that over 50 hospitals across Germany and the Netherlands have established in-house bioprinting units since 2020. Moreover, the integration of machine learning algorithms allows predictive modeling of scaffold degradation and tissue integration, minimizing trial-and-error in design. In oncology, patient-specific tumor models printed using collagen and alginate matrices are being used to test drug responses, as demonstrated by researchers at the University of Tokyo.

Growth in minimally invasive surgical procedures and implantable devices

Growth in minimally invasive surgical procedures and implantable devices is unlocking new avenues for biomaterial innovation and is additionally enhancing the growth of the Biomaterials Market. The global shift toward ambulatory care and reduced hospitalization periods has elevated the demand for bioresorbable, flexible, and self-deploying materials compatible with laparoscopic and endovascular techniques. As per the Society of American Gastrointestinal and Endoscopic Surgeons, over 70% of abdominal surgeries in developed nations were performed laparoscopically in 2022, up from 50% in 2015. For instance, the FDA-approved absorbable stent Absorb GT1, made from PLGA, dissolves within three years post-implantation, eliminating long-term foreign body risks. The American Heart Association states that over 600,000 coronary stent procedures are performed annually in the U.S., with bioresorbable variants capturing an increasing share. In neurology, flexible neural probes made from polyimide and silk-based biomaterials are enabling chronic brain monitoring with reduced glial scarring, as demonstrated in trials at the Massachusetts General Hospital.

MARKET CHALLENGES

Ensuring long-term biocompatibility and immune response management

Ensuring long-term biocompatibility and immune response management poses a challenging factor for the growth of the Biomaterials Market. As per a longitudinal study published in Nature Materials, nearly 15% of patients implanted with polymeric nerve guidance conduits developed perineural fibrosis within 12 months, impeding neural regeneration. Moreover, degradation byproducts of certain polymers, such as lactic acid from PLA, can lower local pH and trigger osteolysis in orthopedic applications. The Musculoskeletal Transplant Foundation reports that up to 10% of biodegradable interference screws used in anterior cruciate ligament reconstruction required revision due to inflammatory reactions. The heterogeneity of patient immune profiles further complicates standardization. Emerging solutions include zwitterionic coatings and immune-modulating biomaterials that promote regulatory T-cell responses, but their long-term stability in vivo remains under investigation.

The sustainable sourcing and environmental impact

The sustainable sourcing and environmental impact of biomaterial production are inhibiting the growth of the Biomaterials Market. According to the United Nations Environment Programme, the global biomedical manufacturing sector contributes approximately 5% of total healthcare-related carbon emissions, with polymer synthesis being a major contributor. Chitosan purification, for instance, requires concentrated alkali treatments that generate high levels of alkaline wastewater; the Chinese Academy of Sciences estimates that each ton of chitosan produced releases up to 15 cubic meters of contaminated effluent. In synthetic biomaterials, petrochemical-derived precursors contradict sustainability goals despite their performance advantages. Life cycle assessments conducted by the Swiss Federal Laboratories for Materials Science and Technology indicate that the carbon footprint of medical-grade PEEK is nearly three times higher than that of stainless steel.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | Based on Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Key market players | Carpenter Technology Corporation, Evonik Industries, Berkeley Advanced Biomaterials, Royal DSM, BASF SE, Corbion, Cam Bioceramics B.V., Celanese Corporation, CoorsTek Inc., CeramTec, and GELITA AG. |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

SEGMENTAL ANALYSIS

By Biomaterial Type Insights

The polymer biomaterials segment was the largest and held 38.2% of the biomaterials market share in 2024, with the unmatched versatility, tunable mechanical properties, and compatibility with minimally invasive delivery systems. According to the U.S. Food and Drug Administration, over 60% of newly approved implantable medical devices between 2020 and 2023 incorporated polymeric components, with their centrality in modern medical innovation. These materials maintain a moist wound environment, facilitate autolytic debridement, and reduce infection rates. The integration of stimuli-responsive polymers such as thermosensitive chitosan-glycerophosphate systems used in injectable tissue fillers further enhances clinical utility.

The natural segment is projected to grow with a CAGR of 14.7% from 2025 to 2033. Natural biomaterials, including collagen, fibrin, hyaluronic acid, and alginate, are derived from biological sources and are inherently biocompatible, biodegradable, and often pro-angiogenic, making them ideal for tissue regeneration. According to the National Institutes of Health, collagen-based scaffolds were used in over 1.2 million regenerative procedures globally in 2022 in skin grafts, cartilage repair, and dental bone augmentation. Their ability to support cell adhesion and differentiation without triggering significant immune responses gives them a distinct advantage over synthetic counterparts. In ophthalmology, fibrin sealants have replaced sutures in corneal transplantation in over 70% of cases in leading European hospitals, as documented by the European Society of Cataract and Refractive Surgeons, due to their rapid polymerization and minimal tissue trauma.

By Application Insights

The orthopedic application segment accounted in holding 32.1% of the global biomaterials market share in 2024, with the prevalence of musculoskeletal disorders, aging, and rising trauma incidents. Biomaterials such as titanium alloys, hydroxyapatite-coated implants, and ultra-high-molecular-weight polyethylene (UHMWPE) are fundamental to implant durability and osseointegration. Additionally, bone graft substitutes composed of calcium phosphates and demineralized bone matrix have gained traction in spinal fusion and fracture repair.

The tissue engineering application segment is anticipated to grow at a CAGR of 16.3% from 2025 to 2033, owing to the paradigm shift from symptomatic treatment to functional tissue restoration and organ regeneration. Unlike traditional implants, tissue engineering combines biomaterial scaffolds, cells, and bioactive signals to reconstruct damaged tissues by offering long-term solutions for organ failure and congenital defects. The U.S. Department of Health and Human Services notes that over 100,000 patients are on the national transplant waiting list, yet only 40,000 transplants are performed annually, which is creating a gap that tissue engineering aims to bridge. Scaffolds made from decellularized matrices and synthetic polymers are being used to regenerate skin, cartilage, and even cardiac patches. In cardiovascular applications, bioengineered tracheal and vascular grafts have entered clinical trials in Japan and Germany, supported by funding from national health innovation programs.

REGIONAL ANALYSIS

North America Biomaterials Market Insights

North America was the largest contributor in the global biomaterials market with 40.3% of the share in 2024, with a robust innovation ecosystem, high healthcare expenditure, and strong regulatory frameworks that facilitate rapid clinical translation. The United States alone accounts for over 70% of the regional market, driven by a high incidence of chronic diseases and a well-established network of academic-medical-industrial collaboration. Additionally, the U.S. Food and Drug Administration’s Breakthrough Devices Program has accelerated the approval of over 350 novel biomaterial-based devices since 2018, reducing time-to-market by up to 40%.

Europe Biomaterials Market Insights

Europe's biomaterials market held 28.3% of the share in 2024 with its integrated healthcare systems, strong public funding for research, and pioneering contributions to regenerative medicine and sustainable biomaterials. The European Union’s Horizon Europe program has funded over 200 biomaterials-related projects, including the development of immune-modulating coatings and 3D-bioprinted tissues. The European Wound Management Association notes that chronic wounds affect over 4 million patients across the EU, driving demand for advanced hydrogels and antimicrobial dressings. Europe’s balance of regulatory rigor and scientific ambition continues to shape global biomaterials standards.

Asia-Pacific Biomaterials Market Insights

Asia-Pacific biomaterials market growth is lucratively to grow with an expected CAGR in the coming years, owing to the rising healthcare infrastructure, increasing medical tourism, and government-led initiatives to localize high-tech medical manufacturing. China and Japan are the primary contributors, with Japan maintaining a legacy of precision engineering in biomaterials and China rapidly scaling production capacity. The Japanese Ministry of Health, Labour and Welfare approved over 40 regenerative medicine products between 2014 and 2023, including corneal epithelial cell sheets and cartilage implants, under its conditional approval pathway. In China, the National Medical Products Administration fast-tracked 127 biomaterial-based devices between 2020 and 2023, reflecting policy support for domestic innovation.

Latin America Biomaterials Market Insights

Latin America biomaterials market growth is growing with increasing public and private healthcare investment and a rising burden of cardiovascular and orthopedic conditions. The Brazilian Ministry of Health reports that over 150,000 cardiovascular stent procedures were performed in 2022, with growing adoption of drug-eluting and bioresorbable variants. However, import dependency and regulatory fragmentation remain challenges. The region also benefits from medical tourism; Costa Rica and Colombia attract over 50,000 international patients annually for orthopedic and dental procedures, as reported by the Medical Tourism Association.

Middle East and Africa Biomaterials Market Insights

The Middle East and Africa biomaterials market growth is eventually to grow with early stages of development, the region is witnessing accelerated investment in healthcare infrastructure, particularly in the Gulf Cooperation Council (GCC) countries. The United Arab Emirates has emerged as a regional hub, with Dubai Healthcare City hosting over 200 medical technology firms, including biomaterial distributors and research centers. Saudi Arabia’s Vision 2030 initiative includes a $30 billion allocation for healthcare modernization,

KEY MARKET PLAYERS

Some of the noteworthy players in the global biomaterials market covered in this report are

- Carpenter Technology Corporation (United States)

- Evonik Industries (Germany)

- Berkeley Advanced Biomaterials (United States)

- Royal DSM (Netherlands)

- BASF SE (Germany)

- Corbion (Netherlands)

- Cam Bioceramics B.V. (Netherlands)

- Celanese Corporation (United States)

- CoorsTek Inc. (United States)

- CeramTec (Germany)

- GELITA AG (Germany)

TOP LEADING PLAYERS IN THE MARKET

Johnson & Johnson

Johnson & Johnson has long been a pivotal force in the biomaterials domain by leveraging its deep integration across medical devices, pharmaceuticals, and regenerative medicine. Through its subsidiary Ethicon, the company pioneered the use of synthetic absorbable polymers in surgical sutures, setting foundational standards for biocompatibility and degradation control. Johnson & Johnson continues to drive innovation in wound care, orthopedic implants, and cardiovascular devices, embedding advanced biomaterials into solutions that address complex clinical challenges. Its collaborative ecosystem with academic institutions and biotech startups enables rapid translation of research into scalable therapies. The company’s commitment to sustainable biomaterial design and patient-centric engineering reinforces its leadership, influencing global regulatory thinking and clinical adoption patterns across diverse healthcare systems.

Stryker Corporation

Stryker Corporation stands as a dominant innovator in orthopedic and neurosurgical biomaterials, known for its precision-engineered implants and bioactive coatings. The company has advanced the use of porous tantalum and 3D-printed titanium in joint replacements, enhancing osseointegration and implant longevity. Stryker’s focus on material science extends to spinal fusion, where synthetic bone grafts and resorbable scaffolds play a role in minimally invasive procedures.

Zimmer Biomet

Zimmer Biomet has shaped the evolution of musculoskeletal biomaterials through its comprehensive portfolio of joint reconstruction, dental, and spine products. The company has been instrumental in advancing ceramic-on-ceramic bearings, bioresorbable fixation devices, and collagen-based matrices for cartilage repair. Zimmer Biomet’s expertise lies in combining material durability with biological integration, ensuring implants mimic natural tissue mechanics. Its foray into robotic-assisted surgery platforms further amplifies the precision application of biomaterials in complex anatomical environments.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by leading companies is vertical integration of material science with clinical applications by allowing seamless alignment between biomaterial design and therapeutic outcomes. Firms ensure optimal biocompatibility, mechanical performance, and regulatory readiness by embedding material innovation within end-to-end medical device development. This approach enables faster clinical translation and enhances product differentiation in competitive therapeutic areas such as orthopedics and cardiovascular repair.

Another critical strategy is strategic collaboration with academic and research institutions, which provides access to cutting-edge discoveries in regenerative medicine, biodegradable polymers, and immune-modulating materials. These partnerships facilitate early-stage innovation, de-risk development pipelines, and support the co-creation of next-generation technologies such as 3D-bioprinted tissues and smart responsive scaffolds.

Another approach is expansion into emerging markets through localized manufacturing and regulatory alignment, enabling broader patient access and faster market entry. Companies are establishing regional innovation hubs and adapting biomaterial formulations.

RECENT HAPPENINGS IN THIS MARKET

- In September 2024, an international conference at the 2024 Bio Asia-Taiwan was held at the National Taipei University of Technology (NTUT) by the High-Value Biomaterials Research and Commercialization Center (HBRCC). The forum concentrated on models for international partnership in the field of biomaterials and the exchange of experiences between academia-industry collaboration by the attending experts.

- In May 2024, BIO INX, a Bioink technology company, with Readily3D, a volumetric 3D printing firm, to launch new biomaterials for volumetric 3D bioprinting.

- In April 2024, Omid Veiseh, a Rice University bioengineer, and collaborators discovered new formulations for biomaterials that can assist in making a fresh start in treating type 1 diabetes. This will pave the way for a more endurable, tenable, lasting, self-governing method of managing the disease. Further, providing a host immune system to stand and support the existence of implanted insulin-secreting cells in more than 700 million type 1 diabetes worldwide can be transformative.

MARKET SEGMENTATION

This research report has segmented and sub-segmented the global biomaterials market into categories based on biomaterial type, application, and region.

By Product Type

- Metallic Biomaterials

- Polymeric Biomaterials

- Ceramic Biomaterials

- Natural Biomaterials

By Application

- Orthopedic

- Cardiovascular

- Ophthalmology

- Dental

- Plastic Surgery

- Wound Healing

- Tissue Engineering

- Neurological / Central Nervous System

- Urinary

- Other Applications

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1.At What CAGR, the global Biomaterials market is expected to grow from 2025 to 2033 ?

The global Biomaterials market is estimated to grow at a CAGR of 14.5% from 2025 to 2033.

2.How much is the global Biomaterials market going to be worth by 2033?

As per our research report, the global Biomaterials market size is projected to be USD 488.51 billion by 2033.

3.Which are the significant players operating in the Biomaterials market?

Evonik Industries (Germany), Berkeley Advanced Biomaterials (United States), Royal DSM (Netherlands), BASF SE (Germany), Corbion (Netherlands), Cam Bioceramics B.V. (Netherlands), Celanese Corporation (United States), CoorsTek Inc. (United States) are some of the significant players operating in the Biomaterials market

4.Which region is growing the fastest in the global Biomaterials market?

Geographically, the North American Biomaterials market accounted for the largest share of the global market in 2024.

5.What challenges and restraints are discussed in the biomaterials market report?

Challenges include regulatory approvals, biocompatibility, sterilization, and high production costs per the biomaterials market report

6.How is regenerative medicine influencing the biomaterials market according to the market report?

The biomaterials market report shows regenerative medicine is a major growth factor due to increased funding and applications.

7.What advancements are anticipated in the biomaterials market for wound healing?

The biomaterials market report predicts innovations in wound healing biomaterials, including synthetic and natural forms for better skin regeneration.

8.How are government initiatives affecting the biomaterials market as per market reports?

Increased government R&D funding is boosting the biomaterials market, according to various market reports.

9.What role do implantable devices play in the biomaterials market report’s analysis?

Implantable biomaterials for devices like heart valves, stents, joint replacements, and dental implants form a core component of the biomaterials market report.

10.Why is biocompatibility a crucial topic in biomaterials market reports?

The biomaterials market report emphasizes biocompatibility as essential for successful integration, with compatibility issues posing market restraints.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com