Global Biosimilars Market Size, Share, Trends & Growth Forecast Report By Product Type (Protein, Insulin, Human Growth Hormones, Granulocyte Colony-stimulating Factor (G-CSF), Interferons, Recombinant Glycosylated Proteins, Erythropoietin, Monoclonal Antibodies, Follitropin, Recombinant Peptides and Glucagon), Technology, Diseases and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis (2025 to 2033)

Global Biosimilars Market Summary

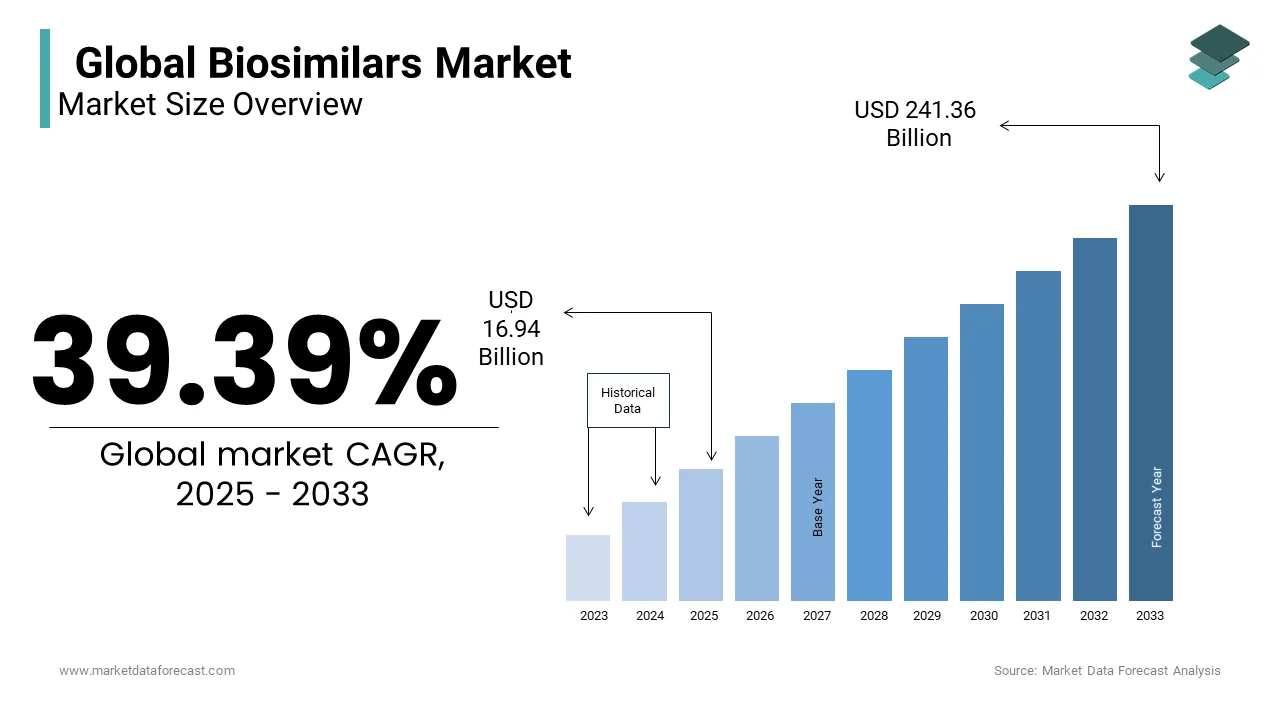

The Global Biosimilars Market size was valued at USD 12.15 billion in 2024 and is anticipated to reach USD 241.36 billion by 2033, growing at a CAGR of 39.39% from 2024 to 2033. The market is gaining momentum due to the rising demand for remote cardiac care, the growing burden of cardiovascular diseases, and technological advancements in AI-powered diagnostics and wearable cardiac monitoring devices.

Key Market Trends & Insights

- Global dominated the global market with a largest share of in 2024.

- Global is projected to grow at the fastest rate between 2024 and 2033.

- Based on technology, the IT services segment is the fastest-growing with a projected CAGR of 39.39%.

- AI and wearable tech adoption are key trends driving innovation in the market.

Market Size & Forecast

- 2024 Market Size: USD 12.15 Billion

- 2033 Projected Market Size: USD 241.36 Billion

- CAGR (2024–2033): 39.39%

- Global: Largest market in 2024

- Global: Fastest-growing region

Global Biosimilars Market Size

The global biosimilars market size was valued at USD 12.15 billion in 2024. The biosimilars market size is expected to have a 39.39% CAGR from 2025 to 2033 and be worth USD 241.36 billion by 2033 from USD 16.94 billion in 2025.

The biosimilars are biologic products that are highly similar to already-approved reference biologics in terms of structure, function, efficacy, and safety, despite minor differences in clinically inactive components. According to the World Health Organization, biosimilars must undergo rigorous comparative studies to demonstrate no clinically meaningful differences from the reference product in terms of pharmacokinetics, immunogenicity, and therapeutic outcomes. The global push toward sustainable healthcare systems has elevated biosimilars as a strategic tool to expand patient access to high-cost biologic therapies used in oncology, autoimmune diseases, and endocrinology. As per the Organisation for Economic Co-operation and Development, biologic drugs account for over 70% of pharmaceutical expenditure growth in high-income countries, despite representing less than 3% of total prescriptions. In response, regulatory bodies such as the U.S. Food and Drug Administration and the European Medicines Agency have established comprehensive approval pathways to ensure scientific rigor while fostering competition. The complexity of biosimilar development necessitates advanced biotechnological infrastructure and deep regulatory expertise, distinguishing it from conventional drug manufacturing.

MARKET DRIVERS

Escalating Healthcare Expenditure and Demand for Cost-Effective Therapies

The relentless rise in global healthcare spending on high-cost biologic drugs, which has created urgent demand for more affordable therapeutic alternatives, is amplifying the growth of the Biosimilars Market. Biologics, used extensively in treating conditions such as rheumatoid arthritis, inflammatory bowel disease, and various cancers, often carry annual price tags exceeding $100,000 per patient in the United States. According to the Centers for Medicare & Medicaid Services, prescription drug spending in the U.S. reached $643 billion in 2023, with biologics accounting for nearly half of this total. This financial burden is unsustainable for public and private payers alike, prompting policymakers to incentivize biosimilar adoption. For example, the introduction of biosimilar infliximab led to a 70% price reduction in several EU countries, as reported by the European Observatory on Health Systems and Policies. In emerging markets such as India and Brazil, where out-of-pocket expenditure constitutes a significant portion of healthcare costs, biosimilars offer a lifeline for patients who would otherwise be unable to afford treatment. The Indian government’s National Health Policy emphasizes biosimilar development as a national priority to improve access to insulin, monoclonal antibodies, and growth hormones.

Increasing Expiry of Biologic Patents and Regulatory Pathway Expansion

The expiration of key patents on blockbuster biologic drugs, which opens the door for biosimilar manufacturers to enter with scientifically validated alternatives, is enhancing the growth of the Biosimilars Market. Over the past five years, patents on major biologics such as adalimumab (Humira), trastuzumab (Herceptin), and rituximab (Rituxan) have lapsed in major jurisdictions, creating one of the largest waves of biosimilar opportunities in pharmaceutical history. According to the IQVIA Institute for Human Data Science, more than 20 biologic drugs with combined global sales exceeding $150 billion annually will face patent expiry by 2028. This milestone has triggered the launch of multiple FDA-approved biosimilars, with projections indicating up to 80% market penetration within three years in competitive environments. Regulatory agencies have also streamlined approval processes to encourage competition; the European Medicines Agency has approved over 80 biosimilars since 2006, while the U.S. FDA has cleared more than 40 as of 2024. Japan’s Pharmaceuticals and Medical Devices Agency has adopted a fast-track review system for biosimilars, reducing approval timelines to under 10 months.

MARKET RESTRAINTS

Physician and Patient Hesitancy Due to Perceived Efficacy and Safety Concerns

The persistent hesitancy among physicians and patients regarding the equivalence of biosimilars to their reference biologics, despite robust regulatory standards, is restricting the growth of the Biosimilars Market. According to a 2023 survey by the American College of Rheumatology, 42% of rheumatologists expressed reservations about switching stable patients from originator biologics to biosimilars, citing concerns about unintended immune responses or loss of efficacy. A study published in Gastroenterology found that only 35% of gastroenterologists in the U.S. routinely prescribed biosimilars as first-line therapy, even when covered by insurance. Patient advocacy groups also report confusion; as per the Crohn’s & Colitis Foundation, over 50% of surveyed patients feared that biosimilars were “generic copies” with inferior quality.

Complex and Cost-Intensive Manufacturing Requirements

The exceptionally high complexity and capital intensity associated with biosimilar production are limiting the growth of the Biosimilars Market. According to the Biotechnology Innovation Organization, the average cost to develop a biosimilar ranges from $100 million to $250 million, with development timelines spanning 7 to 8 years. This is in stark contrast to generic drugs, which can be developed for under $5 million. The need for state-of-the-art facilities further restricts scalability; a single biosimilar manufacturing plant can cost over $500 million to build and validate, as per the International Society for Pharmaceutical Engineering. In emerging markets, such infrastructure is often lacking India, despite being a generics powerhouse, has only a handful of facilities compliant with FDA and EMA standards for biosimilar production, as reported by the Department of Biotechnology, Government of India. Additionally, minor variations in cell culture conditions, temperature, or pH can alter protein folding and glycosylation patterns, potentially affecting clinical performance.

MARKET OPPORTUNITIES

Expansion into Emerging Therapeutic Areas and Pipeline Diversification

The expansion into high-growth therapeutic areas beyond oncology and autoimmune diseases, including neurology, ophthalmology, and rare disea, is anticipated to fuel the growth of the biosimilars Market. Historically, biosimilars have focused on monoclonal antibodies and cytokines, but advances in analytical science and formulation are enabling replication of more complex molecules such as fusion proteins and biosimilar versions of gene therapy vectors. According to the Alliance for Regenerative Medicine, over 30 biosimilar candidates targeting neurodegenerative conditions like Alzheimer’s and Parkinson’s are in preclinical or early clinical development as of 2024.

Growing Government Support and Reimbursement Incentives

The increasing institutional support from governments and public health agencies seeking to reduce pharmaceutical expenditures and improve treatment access is expected to also promote the growth opportunities for the Biosimilars Market. National health systems are implementing policies that mandate or incentivize biosimilar adoption through tendering systems, automatic substitution, and preferential reimbursement. In Japan, the government set a national biosimilar adoption target of 70% by 2025 and introduced price adjustments that penalize hospitals for overuse of originator biologics, as per the Ministry of Health, Labour and Welfare. Developing nations are also embracing biosimilars as a public health strategy, which is South Africa’s Medicines Control Council fast-tracks biosimilar approvals to address HIV and cancer treatment gaps, while Brazil’s Ministry of Health includes biosimilars in its national formulary with guaranteed procurement.

MARKET CHALLENGES

Interchangeability Designation and Regulatory Harmonization Gaps

The lack of global harmonization in interchangeability standards, which hampers cross-border adoption and creates confusion among prescribers and payers, is hampering the growth of the Biosimilars Market. While the U.S. FDA has established a distinct “interchangeable” designation requiring additional switching studies, the European Medicines Agency does not formally recognize interchangeability, leaving substitution decisions to national authorities. According to the Regulatory Affairs Professionals Society, only 8 of the 40 FDA-approved biosimilars in the U.S. have received interchangeable status as of 2024, limiting automatic pharmacy-level substitution. Furthermore, the absence of universally accepted pharmacovigilance protocols for post-marketing surveillance complicates long-term safety monitoring.

Supply Chain Vulnerability and Raw Material Dependency

The fragility of its supply chain, with the reliance on a limited number of suppliers for raw materials such as cell culture media, single-use bioreactors, and chromatography resins, is also expected to limit the growth of the Biosimilars Market. These components are often produced by a handful of multinational manufacturers, creating bottlenecks that can disrupt production. According to the Parenteral Drug Association, over 70% of global bioreactor bags are sourced from three suppliers, making the industry vulnerable to geopolitical disruptions and logistical delays. The COVID-19 pandemic exposed these vulnerabilities between 2020 and 2022, biosimilar manufacturers in Europe and India reported an average 40% increase in lead times for key consumables, as per the International Society for Pharmaceutical Engineering. Additionally, the shortage of qualified personnel for bioprocessing operations exacerbates production risks; a 2023 report by the Biopharma Excellence Center found that 45% of biosimilar facilities in Asia faced delays due to a lack of trained biotechnologists. In the U.S., the FDA identified 12 shortages of bioprocessing materials in 2023 alone, prompting calls for domestic manufacturing expansion.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Technology, Disease & Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Sandoz International GmbH, Wockhardt Ltd, Hospira, Inc., Teva Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories, Biocon Limited, Mylan, Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The Monoclonal Antibodies (mAbs) segment dominated the Biosimilars Market by capturing 48.3% of the share in 202,4, owing to the high therapeutic value and exorbitant cost of originator mAbs, which are used extensively in treating chronic and life-threatening conditions such as cancer, rheumatoid arthritis, and Crohn’s disease. According to the IQVIA Institute for Human Data Science, Humira alone generated $21 billion in global sales in 2022, making it the most lucrative biosimilar opportunity in history. The U.S. entry of multiple adalimumab biosimilars in 2023 led to a projected price reduction of 35% within two years, as per the RAND Corporation.

The Recombinant Glycosylated Proteins segment is projected to expand at a CAGR of 16.3% in the coming years, with the increasing demand for biosimilars of complex glycoproteins such as erythropoietin (EPO) and clotting factors, which require precise post-translational modifications for clinical efficacy. Another factor is the advancement in glycoengineering technologies, enabling manufacturers to replicate complex sugar moieties with higher fidelity. South Korea’s Celltrion and Hanwha have pioneered proprietary platforms that optimize glycosylation patterns, enhancing biosimilarity and reducing immunogenicity. Additionally, emerging markets in Latin America and Southeast Asia are prioritizing local production of glycosylated biosimilars to reduce import dependency.

By Technology Insights

The recombinant DNA technology segment is estimated to lead the biosimilar market during the forecast period. This segment manufactures biosimilar products such as human growth hormones, insulin, and erythropoietin. The advanced technologies help intensify the biosimilar's ability to treat diseases instantly and efficiently.

By Disease Insights

The Oncology Diseases segment was the largest by capturing 42.3% of the Biosimilars Market share in 20,,25 with the widespread use of high-cost monoclonal antibodies and growth factors in cancer treatment, coupled with urgent healthcare system needs to manage escalating oncology expenditures. According to the American Society of Clinical Oncology, biosimilar versions of these agents have reduced treatment costs by 30–50% in the U.S. and Europe, enabling broader patient access without compromising outcomes. For example, biosimilar rituximab adoptionnon-Hodgkinin’s lymphoma therapy led to a 40% increase in treatment initiation within the UK’s National Health Service, as reported by NHS England.

The Chronic and Autoimmune Diseases segment is projected to grow at a CAGR of 15.7% during the forecast period, with the high prevalence of conditions such as rheumatoid arthritis, psoriasis, inflammatory bowel disease, and multiple sclerosis, which require long-term biologic therapy. A major factor is the widespread use of tumor necrosis factor (TNF) inhibitors like adalimumab and infliximab, whose patent expirations have triggered a wave of biosimilar launches. According to the World Health Organization, over 40 million people globally suffer from rheumatoid arthritis, with treatment costs often exceeding $30,000 annually per patient in high-income countries. The introduction of biosimilar adalimumab in the U.S. in 2023 led to a 45% price reduction within six months, as per the RAND Corporation.

REGIONAL ANALYSIS

Europe Biosimilars Market Insights

Europe was the largest contributor to the global Biosimilars Market with 38.2% of the share in 2024. The European Union’s early regulatory pioneering of the first comprehensive biosimilar approval framework in 2006 through the European Medicines Agency has created a stable, science-based environment for market growth. Countries like Germany, Norway, and the Netherlands have implemented centralized procurement and tendering systems that favor biosimilars, leading to market penetration rates exceeding 80% for agents like rituximab and infliximab. National policies play a crucial role in France’s Haute Autorité de Santé mandates biosimilar substitution in hospitals, while Denmark achieved 95% biosimilar use in rheumatology through prescriber incentives. The region also benefits from strong public trust in regulatory standards and widespread physician education initiatives. According to the European Alliance of Associations for Rheumatology, over 70% of European rheumatologists now prescribe biosimilars as first-line therapy. Additionally, Eastern European nations are catching up, with Poland and Hungary integrating biosimilars into national reimbursement lists.

North America Biosimilars Market Insights

North America Biosimilars Market was positioned second by holding 23.5% of the share in 2024. The United States has historically lagged due to complex patent litigation and restricted interchangeability, but recent policy changes are reversing this trend. The Inflation Reduction Act of 2022 eliminated the Medicare Part D doughnut hole, incentivizing insurers to favor lower-cost biosimilars. As per the RAND Corporation, biosimilar adalimumab achieved a 40% market share within nine months of U.S. launch in 2023, a pace unmatched in previous entries. The FDA has approved over 40 biosimilars as of 2024, with 8 designated as interchangeable enabling pharmacy-level substitution.

Asia-Pacific Biosimilars Market Insights

Asia-Pacific Biosimilars Market growth is expected to grow significantly at a significant CAGR by the end of the forecast period. South Korea stands out as a global leader, with domestic companies like Celltrion and Samsung Bioepis dominating the international biosimilar landscape. India, despite regulatory challenges, has become a low-cost manufacturing base, with firms such as Biocon and Dr. Reddy’s launching biosimilars in insulin, filgrastim, and trastuzumab. The Indian government’s National Biopharma Mission has allocated ₹1,500 crore ($180 million) to boost biosimilar R&D, as per the Department of Biotechnology. China is rapidly expanding its biosimilar pipeline over 200 candidates in clinical development, with 30 approved by the National Medical Products Administration as of 2024, according to the Chinese Medical Association. Japan’s aging population and high cancer burden have driven aggressive biosimilar adoption, with the Ministry of Health targeting 70% usage by 2025.

Latin America biosimilars market Insights

Latin America's biosimilars market growth is swiftly emerging, with the adoption influenced by economic volatility and varying regulatory standards. Brazil leads the region with a relatively advanced regulatory framework through ANVISA, which approved its first biosimilar in 2014 and has since cleared over 25 products. As per the Brazilian Society of Clinical Oncology, biosimilar rituximab adoption in public hospitals increased by 55% between 2020 and 2023, driven by federal procurement policies. Mexico has introduced biosimilars into its national formulary, with IMSS and ISSSTE covering treatments for cancer and autoimmune diseases.

Middle East and Africa Biosimilars Market Insights

Middle East and Africa Biosimilars Market is steadily growing in the coming years. The UAE and Saudi Arabia are advancing biosimilar integration as part of broader healthcare modernization under Vision 2030 and similar national strategies. The UAE’s Ministry of Health and Prevention has approved over 15 biosimilars, with hospitals in Dubai and Abu Dhabi transitioning to biosimilar infliximab and rituximab to reduce costs. As per the Saudi Food and Drug Authority, biosimilar adoption in oncology increased by 40% in 2023 due to centralized procurement. In contrast, Sub-Saharan Africa faces systemic challenges, including weak regulatory frameworks, limited cold chain infrastructure, and high out-of-pocket costs. However, initiatives like the African Union’s African Medicines Agency aim to harmonize biosimilar regulations across 55 countries. South Africa has approved several biosimilars, with the Medicines Control Council fast-tracking reviews to improve access to cancer and HIV-related biologics.

KEY MARKET PLAYERS

Sandoz International GmbH, Wockhardt Ltd, Hospira, Inc., Teva Pharmaceutical Industries Ltd., Dr. Reddy's Laboratories, Biocon Limited, Mylan, Inc., Zydus Cadila, Celltrion Inc., Roche Diagnostics, and Cipla Ltd are some of the notable players in the Latin American biosimilars market.

TOP LEADING PLAYERS IN THE MARKET

Celltrion

Celltrion has emerged as a transformative force in the Asia Pacific biosimilars landscape through its pioneering development and commercialization of high-quality monoclonal antibody biosimilars. The company has established a strong regional footprint by securing approvals for products such as trastuzumab (Herzuma), rituximab (Truxima), and infliximab (Remsima) across South Korea, Japan, Australia, and Southeast Asia. In 2023, Celltrion partnered with Japan’s Takeda Pharmaceutical to co-promote Remsima in rheumatology and gastroenterology, enhancing market penetration in a highly regulated environment. It also launched a digital biosimilar education platform tailored for physicians in India and Thailand, addressing awareness gaps and building prescriber confidence. The company invested in cold-chain logistics infrastructure to ensure product integrity across diverse climates.

Samsung

Samsung Bioepis plays a pivotal role in advancing biosimilar accessibility across the Asia Pacific by leveraging cutting-edge biomanufacturing and strategic collaborations. The company has secured regulatory approvals for key products, including benralizumab (Aybintio), adalimumab (Imraldi), and etanercept (Benepali) in multiple APAC markets, with a strong focus on autoimmune and chronic disease therapies. In 2023, Samsung Bioepis entered a distribution agreement with Australia’s Symbion Health to expand Imraldi’s reach in rheumatology clinics, ensuring faster patient access. It also collaborated with Thailand’s Government Pharmaceutical Organization to localize production and reduce dependency on imports. The company’s state-of-the-art Incheon facility operates under global regulatory standards, enabling seamless technology transfer and consistent quality. By integrating real-world data into post-marketing surveillance, Samsung Bioepis strengthens stakeholder trust. Its biosimilar etanercept demonstrated 98% comparability in a multicenter APAC trial, as reported by the Asia-Pacific League of Associations for Rheumatology.

Biocon

Biocon has been instrumental in democratizing access to biosimilars across the Asia Pacific by combining cost-effective manufacturing with scientific rigor and regional adaptability. The Indian biopharma leader has commercialized biosimilars in insulin glargine (Basalog), trastuzumab (Cremula), and pegfilgrastim (Pegbeshely) in India, Malaysia, the Philippines, and Indonesia, addressing gaps in oncology and diabetes care. In 2023, Biocon launched a biosimilar bevacizumab in partnership with Viatris in Southeast Asia, expanding treatment options for cervical and ovarian cancers. It also received approval from Indonesia’s BPOM for its trastuzumab biosimilar, reinforcing regulatory credibility. The company has invested in local clinical trials to generate region-specific efficacy data, enhancing physician acceptance. Through public health collaborations, Biocon supplied over 2 million doses of affordable biosimilars to government hospitals in India under the Pradhan Mantri Jan Arogya Yojana. Its manufacturing facilities comply with U.S. FDA and EMA standards, enabling export readiness.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Biosimilars Market deploy multifaceted strategies to consolidate their global and regional positions. A primary approach is the formation of strategic partnerships with originator companies, distributors, and governments to accelerate market access and build trust. Companies invest heavily in robust clinical and analytical comparability studies to demonstrate biosimilarity and overcome prescriber skepticism. Geographic expansion into high-growth emerging markets is prioritized through localized manufacturing, regulatory submissions, and public health collaborations. Investment in advanced bioprocessing technologies enhances production efficiency and ensures consistency. Companies also focus on post-marketing surveillance and real-world evidence generation to reinforce long-term safety and efficacy. Educational initiatives targeting physicians, pharmacists, and patients are for driving adoption. Additionally, firms are expanding pipelines into complex molecules such as fusion proteins and next-generation monoclonal antibodies to maintain a competitive advantage.

COMPETITION OVERVIEW

The competition in the Biosimilars Market is characterized by a convergence of scientific rigor, regulatory navigation, and strategic commercialization, with a select group of players dominating due to high entry barriers. Established biotech firms such as Celltrion, Samsung Bioepis, and Biocon leverage proprietary manufacturing platforms and extensive clinical data to differentiate their products in a field where perceived equivalence is paramount. The market is marked by intense rivalry in monoclonal antibody biosimilars, where patent litigation, interchangeability designations, and payer contracts determine market share. In the Asia Pacific, local champions benefit from cost advantages and government support, while multinational corporations rely on global regulatory alignment and brand partnerships. Competition is not solely price-driven but increasingly hinges on supply reliability, real-world evidence, and prescriber education. The emergence of high-concentration formulations, pre-filled syringes, and enhanced stability profiles has intensified product differentiation. However, market fragmentation persists due to varying national regulations, reimbursement policies, and physician hesitancy. New entrants face challenges in securing investment for the $100–250 million development cycle and gaining regulatory approval across multiple jurisdictions.

RECENT MARKET DEVELOPMENTS

- In January 2024, Celltrion partnered with Takeda Pharmaceutical in Japan to co-promote Remsima, its infliximab biosimilar, by enhancing market access in rheumatology and gastroenterology through an established distribution network and joint physician education initiatives.

- In May 2024, Samsung Bioepis entered a distribution agreement with Symbion Health in Australia to expand the availability of Imraldi with its adalimumab biosimilar across private hospitals and specialty clinics, strengthening its presence in the chronic disease segment.

- In August 2024, Biocon launched its bevacizumab biosimilar in Southeast Asia in collaboration with Viatris, which is providing a cost-effective treatment option for ovarian and cervical cancers and expanding its oncology footprint in Malaysia, Indonesia, and the Philippines.

- In November 2024, Celltrion initiated a multicenter real-world evidence study across five APAC countries to evaluate the long-term safety and effectiveness of Herzuma, its trastuzumab biosimilar, reinforcing clinical confidence among oncologists and payers.

- In March 2024, Samsung Bioepis collaborated with Thailand’s Government Pharmaceutical Organization to localize the production of biosimilar etanercept by reducing import dependency and ensuring a stable supply for patients with autoimmune disorders in the region.

MARKET SEGMENTATION

This market research report on the global diagnostic imaging market has been segmented and sub-segmented based on type, application, and region.

By Product Type

- Protein

- Insulin

- Human Growth Hormones

- Granulocyte Colony-stimulating Factor (G-CSF)

- Interferons

- Recombinant Glycosylated Proteins

- Erythropoietin

- Monoclonal Antibodies

- Follitropin

- Recombinant Peptides

- Glucagon

By Technology

- Mass Spectroscopy

- Chromatography

- Monoclonal Antibody Technology

- Recombinant DNA Technology

- Nuclear Magnetic resonance (NMR) technology

- Electrophoresis

- Bioassay

By Disease

- Oncology Diseases

- Blood Disorders

- Growth hormone deficiencies

- Chronic and autoimmune diseases

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1.Which segment by disease is expected to dominate in the biosimilars market in the coming years?

Based on the disease, the oncology segment is predicted to rise at a healthy CAGR from 2024 to 2033.

2.How big is the global biosimilars market?

The global biosimilars market size is predicted to be worth USD 241.36 billion by 2033.

3.Which segment by product type is predicted to lead the global biosimilars market?

Based on the product type, the recombinant non-glycosylated protein segment dominated the biosimilars market in 2025 and the domination is expected to be continuing throughout the forecast period.

4.Which region led the biosimilars market in 2024?

Geographically, the North American regional market dominated the biosimilars market in 2025.

5.Which are the key market participants in the global biosimilars market?

Sandoz International GmbH, Wockhardt Ltd, Hospira, Inc., Teva Pharmaceutical Industries Reddy’s Laboratories, Biocon Limited, Mylan, Inc., Zydus Cadila, Celltrion Inc., Roche Diagnostics, and Cipla Ltd are some of the promising companies in the global biosimilars market.

6.Who are the major players identified in biosimilars market reports

Novartis, Pfizer, Amgen, Samsung Bioepis, and Sandoz are prominent market players.

7.Which therapeutic areas drive biosimilars market demand according to reports?

Autoimmune diseases, cancer, and diabetes are major drivers for biosimilars adoption.

8.How do biosimilars contribute to healthcare cost savings based on market report insights?

Biosimilars offer significant cost savings compared to reference biologics, supporting broader adoption

9.What trends are expected in the biosimilars market through 2035?

Sustained growth, increased clinical adoption, and expansion into new indications are projected trends.

10.What distinguishes biosimilars from generic drugs in market analysis reports?

Biosimilars are derived from living cells, require extensive clinical testing, and have stricter regulatory pathways compared to generics.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com