Global Cannabis Testing Market Size, Share, Trends, COVID-19 impact & Growth Forecast Report – Segmented By Product & Software, Testing Procedures (Terpene Profiling, Potency Testing, Residual Solvent Screening, Pesticide Screening, Genetic Testing, Heavy Metal Testing and Microbial Analysis), End Users & Region - Industry Forecast from 2024 to 2033

Global Cannabis Testing Market Size

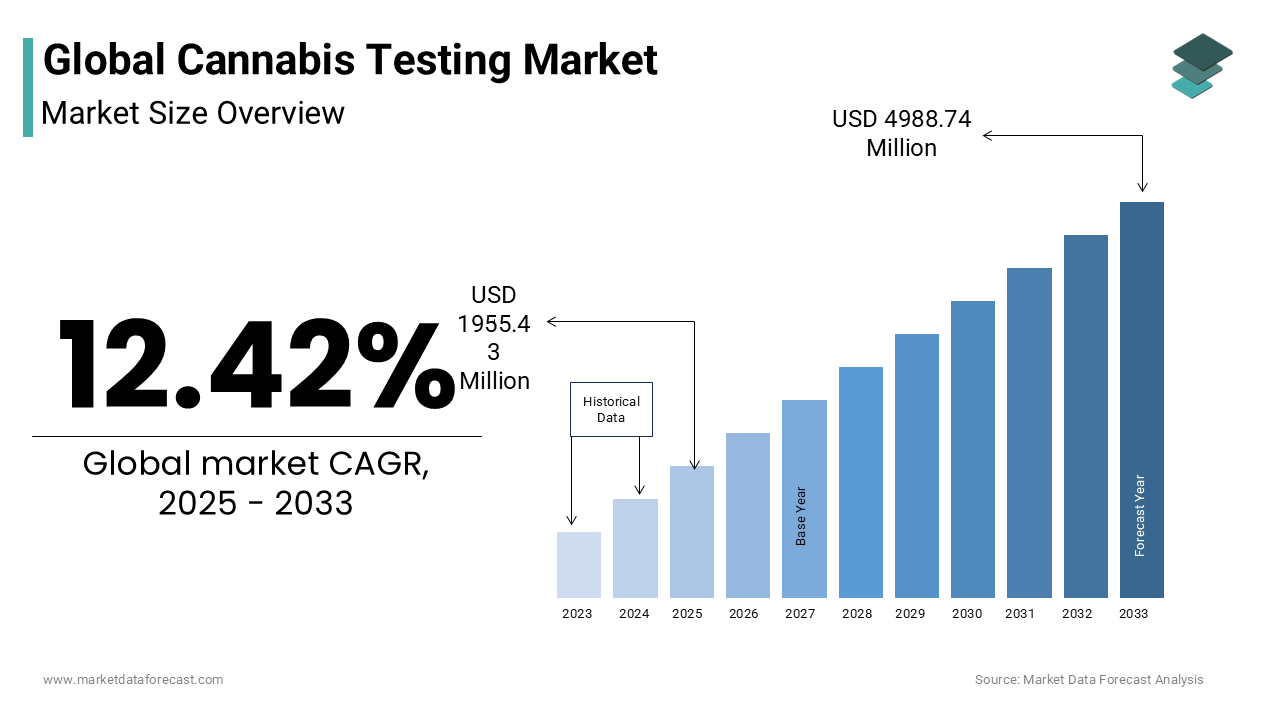

The global cannabis testing market is estimated to grow from USD 1739.40 million in 2024 to USD 4988.74 million in 2033, representing a CAGR of 12.42%.

The Cannabis Testing is designed to evaluate the safety, potency, and compliance of cannabis and cannabis-derived products, including cannabinoids such as THC and CBD. These tests typically include analyses for cannabinoid profiling, terpene content, residual solvents, pesticides, heavy metals, microbial contaminants, and mycotoxins. The integrity of the cannabis supply chain now hinges on precise and reproducible testing methodologies as consumer awareness regarding product safety grows. In the United States, over 30 states have legalized medical cannabis, while 24 allow adult-use, creating a fragmented yet rapidly expanding regulatory landscape that mandates testing at multiple points in the supply chain. Furthermore, Health Canada mandates that all cannabis products undergo rigorous testing before retail distribution, reinforcing the institutionalization of quality control.

MARKET DRIVERS

Escalating Legalization and Medical Integration of Cannabis

The global expansion of legal cannabis frameworks, particularly for medical applications, stands as a pivotal force propelling the growth of the Cannabis Testing Market. As of 2024, 47 countries have enacted legislation permitting medical cannabis, a significant increase from just 8 nations in 2010, according to the United Nations Office on Drugs and Crime (UNODC). This legislative shift is underpinned by mounting clinical evidence supporting cannabinoids in managing chronic pain, epilepsy, and multiple sclerosis. For instance, Epidiolex, a CBD-based medication approved by the U.S. Food and Drug Administration for rare forms of epilepsy, has demonstrated a 50% reduction in seizure frequency in pediatric trials, as reported by the New England Journal of Medicine.

Rising Consumer Demand for Product Transparency and Safety

The modern cannabis consumers exhibit heightened awareness regarding product composition, purity, and labeling accuracy, catalyzing demand for independent, verifiable testing, which is prompting the growth of the Cannabis Testing Market. In California, one of the largest legal markets, the Department of Cannabis Control reported that over 40% of cannabis products failed initial compliance testing in 2022 due to inaccurate THC labeling or microbial contamination. As per the European Monitoring Centre for Drugs and Drug Addiction, unregulated products often contain undeclared synthetic cannabinoids or excessive pesticide residues, posing significant health risks. Consequently, reputable brands increasingly partner with ISO 17025-accredited laboratories to validate claims and build consumer trust.

MARKET RESTRAINTS

Fragmented and Inconsistent Regulatory Standards Across Jurisdictions

The absence of universally accepted regulatory benchmarks is resulting in operational inefficiencies and compliance uncertainty, which is restraining the growth of the Cannabis Testing Market. While countries like Canada and Uruguay have established national testing mandates, others such as the United States operate under a state-by-state regulatory model, which is leading to divergent requirements for analytes, detection limits, and accreditation standards. This lack of standardization complicates multi-state operations for testing laboratories and cultivators alike, increasing costs and delaying market entry. According to the World Health Organization, over 60% of countries with medical cannabis programs lack defined testing protocols, which leaves product safety to the discretion of individual producers. In emerging markets such as Thailand and Colombia, regulatory frameworks are still in developmental phases, with frequent policy reversals disrupting investment in testing infrastructure. The absence of alignment with Codex Alimentarius or International Organization for Standardization (ISO) guidelines further undermines cross-border trade and recognition of test results.

High Operational Costs and Limited Availability of Accredited Laboratories

The establishment and maintenance of compliant cannabis testing laboratories entail substantial capital investment, technical expertise, and ongoing operational expenditures are impeding the growth of the Cannabis Testing Market. A fully equipped cannabis testing facility requires advanced instrumentation such as high-performance liquid chromatography (HPLC), gas chromatography-mass spectrometry (GC-MS), and polymerase chain reaction (PCR) systems, with initial setup costs exceeding $1.5 million, as reported by the American Association for Clinical Chemistry. In Canada, despite a federally regulated market, only 27 laboratories were accredited for cannabis testing as of 2023, according to the Standards Council of Canada, creating capacity constraints and extended turnaround times. In Latin America, where cannabis legalization is expanding, fewer than 10 ISO-accredited facilities exist across the entire region, as noted by the Inter-American Drug Abuse Control Commission. This scarcity forces producers to ship samples internationally, increasing costs and delaying product release. Additionally, the shortage of trained analytical chemists with cannabis-specific expertise exacerbates workforce challenges

MARKET OPPORTUNITIES

Expansion of Medical Cannabis Programs in Emerging Economies

The proliferation of medical cannabis legislation in developing nations is significant opportunity for the growth of the cannabis testing market. As of 2024, countries including Malaysia, Nigeria, and Poland have initiated pilot medical cannabis programs, joining established markets in Israel and Germany. As per the Israeli Ministry of Health, over 40,000 patients are enrolled in its national medical cannabis program, with mandatory testing for all distributed products by creating sustained demand for analytical services. In Africa, the African Union has encouraged member states to explore cannabis for medicinal and industrial use, with Zimbabwe licensing its first commercial cultivation projects in 2023. Similarly, in Southeast Asia, Thailand became the first ASEAN country to legalize medical cannabis in 2019 and has since issued over 400 cultivation licenses, though only a handful of testing facilities meet international standards.

Advancements in Rapid and Portable Testing Technologies

The technological innovation in point-of-care and field-deployable analytical devices is poised to significantly elevate the growth of the Cannabis Testing Market. Traditional laboratory testing often requires 5 to 10 business days for results, which creates bottlenecks in production and distribution. However, emerging technologies such as handheld Raman spectrometers and microfluidic biosensors now enable on-site potency and contaminant screening within minutes. In 2023, the U.S. Department of Agriculture approved the use of portable near-infrared (NIR) spectrometers for hemp compliance testing, allowing farmers to verify THC levels below the federal 0.3% threshold in real time. Companies like Strainprint and Wurk have deployed mobile testing units in Canadian provinces to support remote cultivators by reducing reliance on centralized labs. According to the National Institute of Standards and Technology, these devices achieve up to 92% accuracy in cannabinoid quantification compared to traditional GC-MS methods.

MARKET CHALLENGES

Risk of Sample Tampering and Chain-of-Custody Breaches

The integrity of cannabis samples from collection to analysis with growing concerns over tampering, substitution, and procedural non-compliance undermining test validity is acting as a barrier for the growth of the Cannabis Testing Market. In regulated markets such as Michigan, state audits revealed in 2023 that 12% of licensed testing laboratories had violated chain-of-custody protocols, including unsecured storage and undocumented sample transfers, as reported by the Michigan Department of Licensing and Regulatory Affairs. These lapses compromise the legal defensibility of test results and expose stakeholders to regulatory penalties. The complexity intensifies in multi-party supply chains where samples change hands between cultivators, distributors, and labs, increasing opportunities for adulteration. A 2022 investigation by the Colorado Department of Public Health and Environment identified cases where producers submitted selectively bred "compliance batches" for testing while diverting non-compliant products to market. The absence of standardized tamper-evident packaging and real-time tracking further exacerbates vulnerabilities. As per the International Association for Cannabinoid Medicines, over 20% of failed tests in European medical cannabis programs are attributed to post-harvest contamination due to poor handling. Additionally, the lack of universal digital tracking systems hampers traceability.

Evolving Contaminant Profiles and Emerging Analytical Requirements

The nature of cannabis contaminants, including novel pesticides, mycotoxins, and residual solvents for testing laboratories striving to maintain methodological relevance and regulatory compliance, which is restricting the growth of the Cannabis Testing Market. Furthermore, the rise of solvent-based extraction for concentrates necessitates testing for residual butane, propane, and ethanol at parts-per-million levels, which is requiring sophisticated instrumentation and method validation. According to the American Herbal Pharmacopoeia, 30% of concentrate samples in unregulated markets contain residual solvents above safe limits. Additionally, emerging concerns over nanoparticle contaminants from fertilizers and growth enhancers are not addressed in standard panels.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By Testing Procedures, End User, Product & Software, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Agilent Technologies, Inc., Shimadzu Corporation, Waters Corporation, PerkinElmer, Inc., AB SCIEX LLC, Millipore Sigma, Restek Corporation, LabLynx, Inc. (U.S.), Steep Hill Labs, Inc., PharmLabs, LLC, SC Laboratories, Inc. |

SEGMENTAL ANALYSIS

By Testing Procedures Insights

The potency testing segment was accounted in holding 38.2% of the cannabis testing market share in 2024 with the need to quantify cannabinoids such as THC and CBD, which directly influence product labeling, consumer safety, and regulatory compliance. The surge in medical cannabis adoption and legalization across multiple jurisdictions has intensified the demand for accurate potency assessments. For instance, in the United States, over 3.8 million people were active medical cannabis patients in 2023, as reported by the Arcview Group, which necessitates standardized testing protocols. Regulatory mandates, such as those enforced by the U.S. Food and Drug Administration and state-level cannabis control boards, require all commercial cannabis products to undergo potency verification before sale. Additionally, consumer preference for consistent and reliable product effects drives cultivators and dispensaries to prioritize potency accuracy.

The microbial analysis segment is projected to expand at a CAGR of 14.7% from 2025 to 2033 owing to the rising public health concerns over pathogenic contamination in cannabis products. Unlike potency or terpene profiling, microbial testing addresses direct health risks, including exposure to Aspergillus, E. coli, and Salmonella, which can be life-threatening, especially for immunocompromised patients. The U.S. Centers for Disease Control and Prevention has documented cases of invasive aspergillosis linked to contaminated cannabis use among transplant patients, prompting stringent regulatory responses. Furthermore, the expansion of medical cannabis programs now active in 38 U.S. states and Washington D.C. according to the National Conference of State Legislatures has elevated safety standards. Internationally, the European Medicines Agency has classified microbial contamination as a quality attribute for herbal medicines, influencing testing protocols in EU-adjacent markets.

By End-User Insights

The cannabis testing laboratories segment was the largest and held 45.3% of the share in 2024. These independent and accredited labs serve as the backbone of regulatory compliance, performing mandatory analyses on cannabis products before market entry. According to the American Association for Clinical Chemistry, over 80% of U.S. cannabis testing is outsourced to specialized laboratories due to the high cost and complexity of in-house instrumentation. Additionally, ISO/IEC 17025 accreditation has become a standard requirement, with over 300 cannabis testing labs in the U.S. achieving this certification by 2023, according to the Association of Public Health Laboratories. The absence of in-house testing infrastructure among small cultivators and dispensaries further amplifies reliance on external labs. Canada’s Health Canada requires all licensed producers to use third-party labs for batch testing, contributing to a 12% year-over-year increase in lab testing volume in 2022, as reported by Statistics Canada.

The research institutes segment is likely to grow with an expected to register a CAGR of 13.9% from 2025 to 2033 by expanding scientific inquiry into cannabinoids’ therapeutic potential and the need for standardized testing methodologies. Universities and research centers, including the University of California Center for Medicinal Cannabis Research, are conducting clinical trials on CBD for epilepsy, THC for chronic pain, and minor cannabinoids like CBG for neurodegenerative diseases. Additionally, the U.S. Drug Enforcement Administration increased the number of licensed cannabis research facilities from 3 in 2020 to over 40 in 2023, as confirmed by the Federal Register.

By Product & Software Insights

The analytical instruments segment was the largest by capturing a prominent share of the cannabis testing market in 2024 with the capital-intensive nature of cannabis testing, which relies on high-precision equipment such as high-performance liquid chromatography (HPLC), gas chromatography-mass spectrometry (GC-MS), and inductively coupled plasma mass spectrometry (ICP-MS). These instruments are essential for detecting cannabinoids, pesticides, heavy metals, and residual solvents with regulatory-grade accuracy.

The software solutions segment is likely to grow with an expected CAGR of 16.3% from 2025 to 2033 with the integration of Laboratory Information Management Systems (LIMS) and blockchain-enabled traceability platforms into cannabis testing workflows. Companies like Front Range Biosciences and Proven Data use AI-powered software to predict contamination risks and optimize testing protocols, which is improving turnaround times by up to 30%, according to a 2023 study by the Journal of Cannabis Research.

REGIONAL ANALYSIS

North America Cannabis Testing Market Insights

North America was the top performer of the global cannabis testing market with 52.3% of the share in 2024. Canada was the first G7 nation to legalize recreational cannabis, which is generated $4.4 billion in legal sales in 2023, with Health Canada enforcing strict testing protocols for all licensed producers, as per Statistics Canada. Additionally, the National Institute on Drug Abuse funded over $100 million in cannabis research in 2023, fostering innovation in testing methodologies.

Europe Cannabis Testing Market Insights

Europe cannabis testing market was positioned second with 24.3% of the share in 2024. Germany approved medical cannabis in 2017 and recorded over 200,000 prescriptions in 2022, with the German Federal Institute for Drugs and Medical Devices requiring full contaminant and potency testing for all products. The European Medicines Agency has classified cannabis-based medicines as requiring batch-specific testing for heavy metals, microbes, and solvent residues by aligning with EU pharmacopeial standards. Malta and Luxembourg have legalized adult-use cannabis, creating new testing mandates. The European Commission’s Horizon Europe program funded €25 million in cannabis research from 2021 to 2023, according to the European Research Council, promoting analytical development. Additionally, the EU’s Novel Foods regulation requires safety dossiers for CBD products, involving extensive testing.

Asia-Pacific Cannabis Testing Market Insights

The Asia-Pacific cannabis testing market growth is lucratively growing in the next coming years. Australia’s Office of Drug Control reported over 50,000 medical cannabis prescriptions in 2023, with the Therapeutic Goods Administration requiring full analytical validation for all imported and domestic products. Japan, despite strict laws, permits CBD products with less than 0.01% THC with precise testing over 300 import rejections occurred in 2022 due to non-compliance, according to Japan’s Ministry of Health, Labour and Welfare. India’s CSIR-CIMAP is developing indigenous testing protocols for medicinal cannabis cultivation in Uttar Pradesh and Telangana.

Latin America Cannabis Testing Market Insights

Latin America cannabis testing market growth is likely to grow with the need for standardized testing infrastructure. Colombia, a key exporter, issued over 80 medical cannabis licenses by 2023, with the National Institute of Food and Drug Surveillance (INVIMA) requiring full contaminant screening for export batches, as reported by ProColombia. The country exported over 10 tons of cannabis biomass in 2022, primarily to Europe and Canada, necessitating ISO-compliant testing. Uruguay, the first country to fully legalize cannabis, operates a state-controlled system where all products undergo mandatory potency and microbial analysis, with over 20,000 registered users in 2023, according to the Uruguayan Institute for the Regulation and Control of Cannabis. Brazil’s National Health Surveillance Agency (ANVISA) approved over 20,000 medical cannabis import authorizations in 2022, each requiring analytical certification. Argentina’s Ministry of Health reported over 5,000 registered patients in its national cannabis program by 2023.

Middle East and Africa Cannabis Testing Market Insights

The Middle East and Africa cannabis testing market is expected to have steady pace in the next coming years. South Africa leads the region, with the North Gauteng High Court legalizing personal cannabis use in 2018 and the South African Bureau of Standards developing testing protocols for THC content. The country’s medicinal cannabis market was valued at ZAR 1.2 billion ($65 million) in 2023, with the South African Health Products Regulatory Authority requiring batch testing for all licensed products, as reported by the Industrial Development Corporation. Zimbabwe has issued over 20 cannabis cultivation licenses, with the Medicines Control Authority mandating residue and potency analysis for export-oriented production.

KEY MARKET PLAYERS

Some of the notable participants leading the global cannabis testing market profiled in this report are Agilent Technologies, Inc., Shimadzu Corporation, Waters Corporation, PerkinElmer, Inc., AB SCIEX LLC, Millipore Sigma, Restek Corporation, LabLynx, Inc. (U.S.), Steep Hill Labs, Inc., PharmLabs, LLC, SC Laboratories, Inc., Digipath Labs, Inc., CannaSafe Analytics, Accelerated Technology Laboratories, Inc.

These business leaders have adopted different tactics, such as mergers and acquisitions, to secure a better position in the cannabis testing market.

RECENT MARKET DEVELOPMENTS

- In August 2024, the National Institute of Standards and Technology researchers are considering a new approach of two breath tests administered roughly within an hour. If the research gets a positive result, then this test becomes the first-ever roadside test for cannabis use, which involves two breath tests given at specific intervals.

- In January 2024, the Ontario Cannabis store announced the introduction of a THC testing program. The program involves the provincial cannabis wholesaler, which chooses cultivars with high THC content, which arrive at its warehouse for secondary testing.

- In October 2023, Nova Analytic Labs (Nova) collaborated with Certified Testing and Data (CTND) and launched a cannabis testing method in New York City.

- In April 2023, the California Department of Cannabis Control (DCC) announced the USD 20 million issue for around 16 academic institutions for research to evaluate the complete impact of cannabis.

- In January 2021, MCR Labs, a Massachusetts-based caabis testing firm, opened a laboratory in Allentown and started to approve and analyze product samples for medical marijuana licensees.

- In January 2019, Digipath, Inc. announced an agreement with Cannabis, Inc. to increase its market share in cannabis testing and strengthen its position in the domestic and international cannabis testing market.

MARKET SEGMENTATION

This research report on the global cannabis testing market has been segmented and sub-segmented testing procedures, end-users, products & software, and regions.

By Testing Procedures

- Terpene Profiling

- Potency Testing

- Residual Solvent Screening

- Pesticide Screening

- Genetic Testing

- Heavy Metal Testing

- Microbial Analysis

By End-user

- Cannabis Cultivators

- Laboratories

- Drug Manufacturers & Dispensaries

- Research Institutes

By Product & Software

- Analytical Instruments

- Consumables and Software

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What was the market size of cannabis testing in 2023?

The global cannabis testing market size was worth USD 1539.3 million in 2023.

At what CAGR, the Europe region is growing in the global cannabis testing market?

The cannabis testing market in Europe is projected to showcase a CAGR of 12.1% from 2024 to 2032.

Which segment by testing procedure held the largest share in the cannabis testing market?

Agilent Technologies, Inc., Shimadzu Corporation, Waters Corporation, PerkinElmer, Inc., AB SCIEX LLC, Millipore Sigma, Restek Corporation, LabLynx, Inc. (U.S.), Steep Hill Labs, Inc., PharmLabs, LLC, SC Laboratories, Inc., Digipath Labs, Inc., CannaSafe Analytics, Accelerated Technology Laboratories, Inc. are a few of the major players in the cannabis testing market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com