Global eHealth Market Size, Share, Trends & Growth Forecast Report By Type (Telemedicine, Consumer, Information System, HER, ePrescribing, Health Information, mHealth, Health Management and Clinical Decision Support), Services, End User and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2025 to 2033

Global eHealth Market Summary

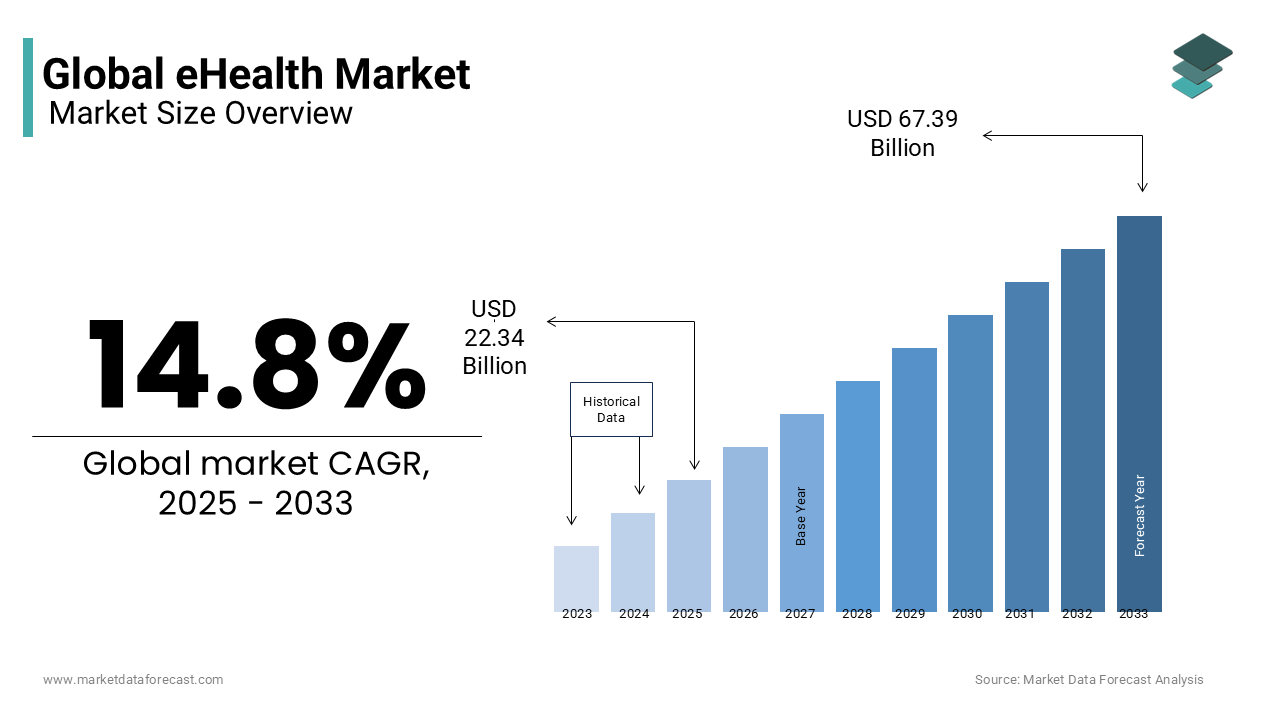

The global eHealth market was valued at USD 19.46 billion in 2024 and is projected to reach USD 67.39 billion by 2033, growing at a CAGR of 14.8% during the forecast period. The rising adoption of digital health solutions, government initiatives to modernize healthcare infrastructure, and increasing demand for remote monitoring and telehealth services are propelling the eHealth market growth worldwide.

Key Market Trends

- Rising adoption of electronic health records (EHRs) for better patient data management.

- Growing use of telemedicine and mobile health applications for remote care delivery.

- Increasing integration of AI, IoT, and cloud technologies in digital health platforms.

- Expanding demand for administrative automation solutions to reduce costs and improve efficiency.

Segmental Insights

- Based on type, the Electronic Health Records (EHR) segment led the market with 27.4% share in 2024, reflecting growing investments in digital patient record management.

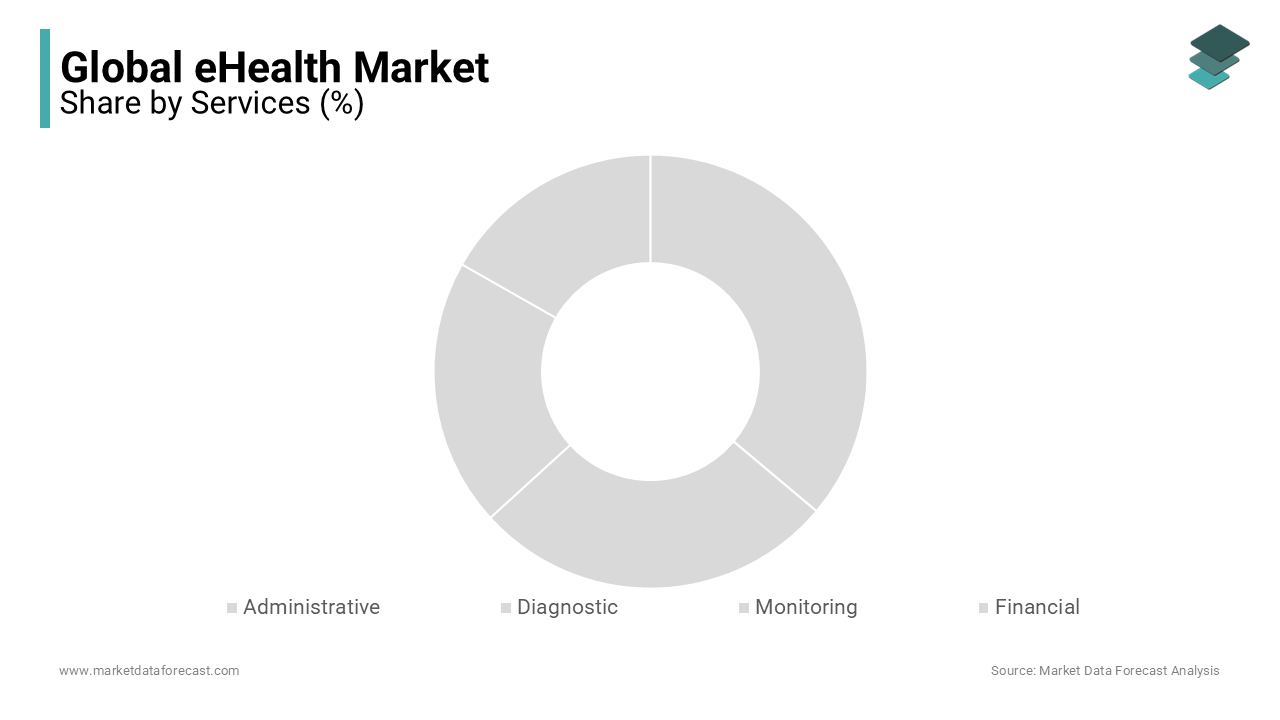

- Based on service, the administrative services segment dominated with 38.6% of the market share in 2024, driven by demand for efficient billing, scheduling, and workflow solutions.

- Based on end user, the healthcare providers segment captured 41.2% of the global market share in 2024, supported by widespread adoption of digital solutions in hospitals and clinics.

Regional Insights

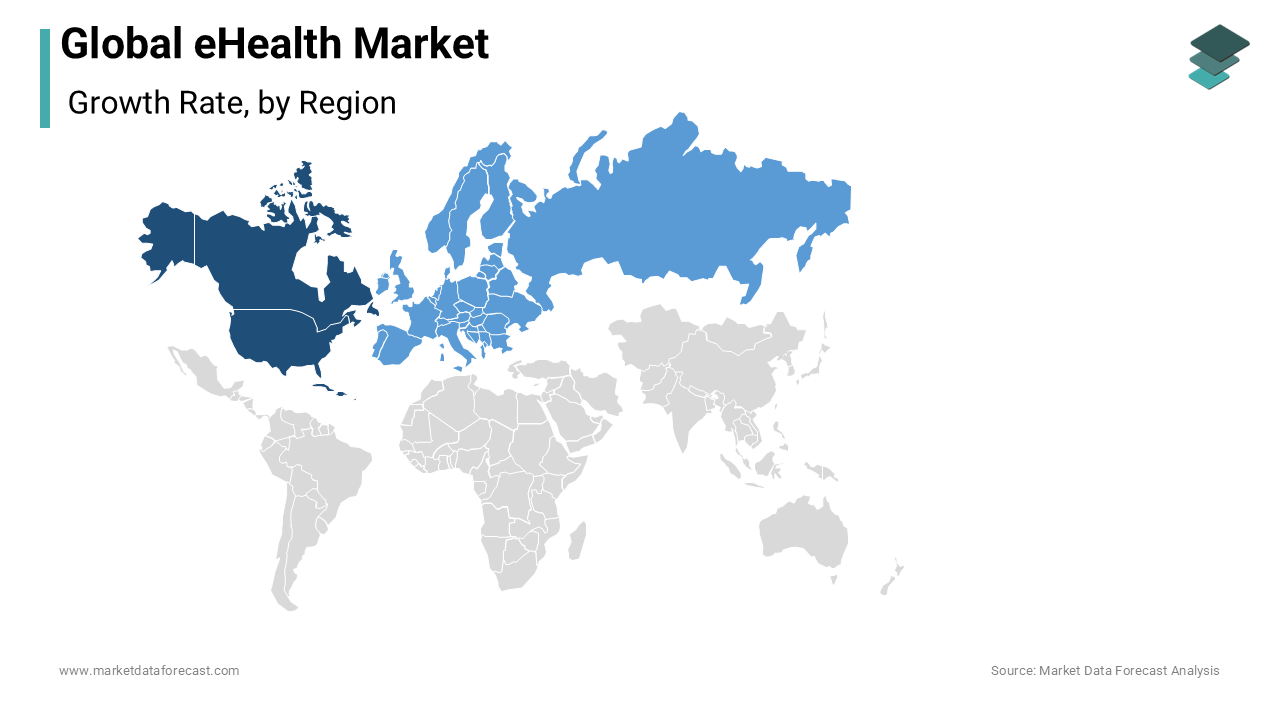

- North America was the largest regional market, accounting for 43.7% share in 2024, supported by advanced healthcare infrastructure, high adoption of digital health platforms, and favorable government policies.

- Asia-Pacific is projected to be the fastest-growing region during the forecast period, driven by rising healthcare digitization, growing smartphone penetration, and supportive government initiatives.

- Europe maintained a strong position, supported by strict regulations for patient data protection and rapid adoption of telehealth platforms.

- Latin America shows growing potential with increasing investments in healthcare IT and digital health startups.

- Middle East & Africa are witnessing steady growth, supported by improving healthcare infrastructure and national eHealth initiatives.

Competitive Landscape

Key players operating in the global eHealth market include Boston Scientific Corp., IBM, Motion Computing Inc., GE Healthcare, Epocrates Inc., Telecare Corp., CompuMed, Medisafe, SetPoint Medical, Doximity, Lift Labs, Proteus Digital Health, and Apple.

Global eHealth Market Size

The global eHealth market is estimated to grow from USD 19.46 billion in 2024 to USD 67.39 billion in 2033, representing a CAGR of 14.8%.

The eHealth market is the fastest-growing area in the health domain. Presently, many eHealth projects are in progress by prominent medical, hi-tech, and government industries, which are trying to capture the advantages of merging health care, the internet, and technologies. Moreover, deploying eHealth solutions and digital transformation of medical systems country-wide enables quick access to information and enhances data exchange. Furthermore, the market continues to expand in the European, Asian, and North American countries. According to the European Commission, Europe is enhancing its maturity in eHealth signals. In 2023, the EU27-average overall composite score rose from 72% to 79%.

MARKET DRIVERS

Accelerated Adoption of Telemedicine Due to Healthcare Access Gaps

The shortage of healthcare professionals and distribution of medical facilities in rural and remote areas with the adoption of telemedicine as a viable alternative to in-person consultations is driving the growth of the eHealth Market. In India, 74% of doctors practice in urban centers, which house only 34% of the population by creating a care deficit in rural regions, as noted by the Indian Medical Association. Similarly, in Australia, the Royal Flying Doctor Service integrated telehealth into its operations, serving 300,000 remote patients annually across the outback, according to the Australian Institute of Health and Welfare. In the United States, the Federal Communications Commission’s Connected Care Pilot Program supported telehealth services for low-income and veteran populations, demonstrating a 35% reduction in hospital readmissions for chronic disease patients.

Proliferation of Wearable Devices and Remote Patient Monitoring

The widespread adoption of wearable health technologies has revolutionized chronic disease management by enabling continuous, real-time physiological tracking outside clinical settings. Devices such as smartwatches, ECG patches, and glucose monitors collect vital data including heart rate, blood pressure, and oxygen saturation by transmitting it securely to healthcare providers for proactive intervention. A 2023 study published in The Lancet Digital Health found that remote monitoring of heart failure patients reduced hospitalizations by 26% over 12 months. In the United Kingdom, the NHS Digital Health Platform deployed 250,000 remote monitoring kits for COPD and diabetes patients, which is improving care continuity and reducing emergency visits, as reported by NHS England.

MARKET RESTRAINTS

Fragmented Regulatory Frameworks and Lack of Interoperability Standards

The absence of harmonized regulatory and technical standards is impeding the growth of the eHealth Market. While some nations have established robust digital health frameworks, others lack the legal infrastructure to govern data exchange, device certification, and cross-border telemedicine. Additionally, proprietary data formats used by EHR vendors often prevent interoperability between hospitals and clinics. The Office of the National Coordinator for Health Information Technology in the U.S. acknowledges that 40% of healthcare providers still face challenges in exchanging patient records due to incompatible systems.

Persistent Digital Divide and Low Health Literacy in Vulnerable Populations

A significant portion of the global population remains excluded from eHealth benefits due to limited digital access, inadequate infrastructure, and insufficient health literacy is also hampers the growth of the eHealth Market. According to the International Telecommunication Union, 2.6 billion people worldwide still lack internet access, with the majority residing in low- and middle-income countries. Even in developed nations, elderly and socioeconomically disadvantaged populations struggle with digital navigation; a 2023 survey by the U.S. National Institute on Aging found that 45% of adults over 75 were unable to independently use a telehealth app. In France, the Haute Autorité de Santé noted that digital exclusion contributes to a 30% lower uptake of e-prescriptions among low-income patients. Language barriers and a lack of culturally adapted interfaces further exacerbate disparities.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Clinical Decision Support and Diagnostics

The incorporation of artificial intelligence into eHealth platforms is unlocking transformative potential in disease prediction, diagnostic accuracy, and personalized care planning is ascribed to bolster the growth of the eHealth Market. According to the U.S. National Institutes of Health, AI-powered tools have demonstrated 95% accuracy in detecting diabetic retinopathy from retinal images by reducing screening delays in primary care. In radiology, Aidoc’s AI platform reduces turnaround time for findings in CT scans by 30%, as validated by the Radiological Society of North America. The UK’s National Health Service has integrated AI into its cancer referral pathways, using predictive models to prioritize high-risk patients by resulting in a 20% faster diagnosis rate, according to NHS Digital.

Expansion of National Digital Health Infrastructure and Government-Led Initiatives

Governments worldwide are investing in centralized digital health ecosystems to improve care coordination, reduce inefficiencies, and enhance public health surveillance. These national platforms integrate EHRs, telemedicine, e-prescriptions, and identity verification into unified systems accessible across providers. According to the World Bank, over 120 countries have launched national eHealth strategies since 2020, with Estonia’s X-Road system serving as a global benchmark for secure data exchange. Rwanda’s national telemedicine network connects all 400 district clinics with Kigali-based specialists by reducing referral times by 60%, as reported by the Rwanda Biomedical Center.

MARKET CHALLENGES

Escalating Cybersecurity Threats to Sensitive Health Data

Growing risks of cyberattacks, data breaches, and ransomware incidents targeting highly sensitive patient information are certainly to pose a challenge for the growth of the e-health market. According to the U.S. Department of Health and Human Services, healthcare organizations experienced 725 reported data breaches in 2023, affecting over 133 million individuals—the highest annual total on record. In 2022, a ransomware attack on Ireland’s Health Service Executive disabled hospital systems for weeks, canceling 6,000 procedures, as documented by the country’s Office of the Data Protection Commission. Medical devices such as insulin pumps and pacemakers are also vulnerable as the U.S. Food and Drug Administration issued 25 cybersecurity alerts for connected devices in 2023 alone. The European Union Agency for Cybersecurity warns that 70% of healthcare providers lack dedicated cybersecurity incident response teams.

Resistance from Healthcare Providers and Institutional Inertia

The widespread adoption is hindered by resistance from clinicians and institutional reluctance to transition from traditional workflows is limiting the growth of the e-health market. Many physicians perceive digital tools as time-consuming, disruptive, or disconnected from clinical realities. A 2023 study by the New England Journal of Medicine found that 58% of U.S. physicians reported burnout symptoms linked to EHR documentation burdens, with some spending nearly two hours on administrative tasks for every hour of patient care. Institutional inertia is further exacerbated by legacy IT systems that are difficult to upgrade and lack integration capabilities. The World Health Organization notes that 60% of public hospitals in Southeast Asia still rely on paper-based records, despite government digitization mandates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2023 to 2033 |

| Base Year | 2023 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By Type, Services, End User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Boston Scientific Corp., IBM, Motion Computing Inc., GE Healthcare, Epocrates Inc., Telecare Corp., CompuMed, Medisafe, SetPoint Medical, Doximity, Lift Labs, Proteus Digital Health, and Apple. |

SEGMENTAL ANALYSIS

By Type Insights

The Electronic Health Records (EHR) segment was the largest by capturing 27.4% of the global eHealth market share in 2024. In the United States, the Centers for Medicare & Medicaid Services’ Meaningful Use program has disbursed over $40 billion in incentive payments since 2011 to hospitals and physicians who adopt certified EHR technology, according to the Office of the National Coordinator for Health Information Technology. As a result, over 96% of non-federal acute care hospitals now use a certified EHR system, a significant increase from just 9.4% in 2008. Similarly, in the European Union, the Digital Health and Care Strategy mandates that all member states implement interoperable EHR systems by 2030, with 18 countries already offering cross-border access to patient records, as noted by the European Commission.

The Clinical Decision Support (CDS) segment is projected to grow at a CAGR of 14.3% from 2025 to 2033. Modern CDS systems are increasingly powered by AI algorithms that analyze patient data to recommend diagnoses, predict risks, and personalize treatment plans. According to the U.S. Food and Drug Administration, over 70 AI/ML-based CDS tools received clearance between 2020 and 2023, including IDx-DR for diabetic retinopathy and Viz.ai for stroke detection. A 2023 study in Nature Medicine demonstrated that an AI-powered CDS model reduced diagnostic errors in radiology by 29% compared to human interpretation alone.e

By Services Insights

The administrative services segment accounted in holding 38.6% of the eHealth market share in 2024. Administrative tasks represent a significant portion of healthcare operations, with hospitals and clinics processing millions of transactions annually related to appointments, coding, and reimbursements. Electronic scheduling systems reduce no-show rates by 25%, as per the American Medical Association, while automated claims processing cuts denial rates by up to 40%, according to America’s Health Insurance Plans. In Canada, the Ontario Health Insurance Plan digitized 98% of physician claims, reducing processing time from 30 to 7 days, as noted by the Ministry of Health.

The monitoring services segment is projected to grow at a CAGR of 13.8% from 2025 to 2033.

Remote monitoring devices such as connected glucose meters, blood pressure cuffs, and wearable ECG patches transmit data to clinicians for proactive intervention. In the U.S., the Centers for Medicare & Medicaid Services reimbursed over 2 million RPM services in 2023, a 300% increase from 2021, as reported by the American Telemedicine Association. In Japan, the Ministry of Health, Labour and Welfare subsidizes home monitoring devices for 3 million elderly patients with heart failure, reducing hospitalizations by 28%, according to the National Cerebral and Cardiovascular Center.

By End User Insights

The healthcare providers segment was the largest by accounting for 41.2% of the global eHealth market share in 2024. In value-based care models, provider reimbursement is increasingly linked to digital reporting and outcomes tracking. In the U.S., Medicare’s Merit-Based Incentive Payment System (MIPS) requires providers to report clinical quality measures through certified eHealth platforms, affecting payments for over 800,000 clinicians, as stated by CMS. In France, the Haute Autorité de Santé ties 30% of hospital funding to digital maturity scores, including EHR usage and data sharing. Similarly, in Saudi Arabia, the Ministry of Health’s Seha performance framework mandates digital reporting for all public hospitals.

The government segment is likely to expand at a CAGR of 12.9% from 2025 to 2033. Governments are launching large-scale initiatives to build interoperable health ecosystems. Estonia’s X-Road system enables secure data sharing across all healthcare providers, reducing duplicate testing by 20%, according to the Estonian Ministry of Social Affairs. In Rwanda, the government partnered with Zipline and Babylon Health to deploy AI-powered telemedicine across all 400 district clinics by improving access for 13 million people.

REGIONAL ANALYSIS

North America was the largest contributor by holding 43.7% of the eHealth market share in 2024. The United States benefits from advanced healthcare infrastructure, strong regulatory support, and high private-sector investment. The Office of the National Coordinator for Health Information Technology confirms that over 95% of hospitals use certified EHRs that are supported by federal incentive programs. Major tech firms like Amazon, Google, and Microsoft are entering the health IT space, accelerating innovation in AI and cloud-based platforms. However, interoperability challenges persist, with 40% of providers reporting difficulties in data exchange, according to the ONC.

Europe was positioned second by holding 26.8% of the global eHealth market in 2024. Germany and the UK have implemented nationwide EHR systems, with Germany’s Gematik overseeing the rollout of the electronic patient record (ePA) to 80 million citizens. The EU’s General Data Protection Regulation (GDPR) ensures high data protection standards, fostering public trust. However, fragmentation remains a challenge; only 14 countries have a fully operational cross-border health data exchange, as noted by the European Commission. Public funding and regulatory alignment are driving steady growth, particularly in telemedicine and AI diagnostics.

Asia Pacific eHealth market is growing lucratively with a significant CAGR during the forecast period. China’s “Healthy China 2030” plan includes a $100 billion investment in digital health, with over 1,500 hospitals adopting AI-powered diagnostics, according to the National Health Commission. India’s Ayushman Bharat Digital Mission has created a national health ID for 500 million people, linking 300,000 facilities. Japan’s aging population has spurred the adoption of remote monitoring, with 1.3 million elderly patients using connected devices, as reported by the Ministry of Health. However, rural-urban disparities and variable internet access limit scalability

COMPETITIVE LANDSCAPE

Key Market Participants

Some of the prominent companies leading the global eHealth market profiled in the report include

- Boston Scientific Corp.

- IBM

- Motion Computing Inc.

- GE Healthcare

- Epocrates Inc.

- Telecare Corp.

- CompuMed

- Medisafe

- SetPoint Medical

- Doximity

- Lift Labs

- Proteus Digital Health

- Apple

The competitive landscape of the eHealth market is characterized by a dynamic interplay between established health IT providers, agile digital health startups, and technology conglomerates entering the healthcare space. Dominant players like Epic and Cerner maintain strong footholds in hospital systems through deeply embedded EHR platforms by creating high switching costs and long-term contractual relationships. However, their scale is increasingly challenged by nimble innovators specializing in niche applications such as AI diagnostics, remote monitoring, and mental health apps, which offer targeted solutions with rapid deployment. Cloud-based infrastructure providers like Amazon Web Services and Microsoft Azure are also reshaping competition by offering secure, scalable backends that enable startups to bypass traditional IT barriers. The market is further complicated by divergent regulatory environments, with varying data privacy laws and interoperability standards across regions influencing product design and market access. Providers are no longer competing solely on functionality but on ecosystem integration, user experience, and the ability to deliver actionable insights from data.

Top Players in the EHealth Market

Epic Systems Corporation

Epic Systems stands as a preeminent force in the eHealth landscape, renowned for its comprehensive electronic health record (EHR) platform used by leading healthcare institutions worldwide. The company has built a reputation for deep clinical functionality, seamless integration across care settings, and robust data interoperability. Its software supports end-to-end workflows, from patient scheduling and clinical documentation to revenue cycle management and population health analytics. Epic’s commitment to data standardization has enabled large-scale health information exchanges, connecting disparate providers within integrated delivery networks. The system’s ability to support complex care models, including value-based care and precision medicine, has made it a preferred choice for academic medical centers and large hospital systems.

Cerner Corporation

Cerner has played a foundational role in advancing digital health through its enterprise-wide clinical and financial systems that power hospitals, clinics, and public health agencies globally. The company’s Millennium platform integrates EHRs, laboratory information, and revenue management into a unified environment, enabling data-driven decision-making and operational efficiency. Cerner has been instrumental in supporting large-scale public health initiatives, including national disease surveillance and pandemic response systems. Its expertise in health informatics and data analytics allows providers to extract actionable insights from clinical data, improving care quality and patient safety. The company emphasizes interoperability and open standards, contributing to industry-wide efforts in health data exchange.

Allscripts Healthcare Solutions

Allscripts has emerged as a versatile leader in the eHealth domain by delivering scalable solutions tailored to diverse healthcare environments, from small practices to large health systems. The company offers a broad portfolio encompassing electronic health records, practice management, telehealth, and population health tools, enabling end-to-end digital transformation. Allscripts places strong emphasis on interoperability, supporting data exchange through FHIR standards and participating in national health information networks. Its Sunrise platform is widely adopted in acute care settings for its clinical depth and adaptability to complex workflows. The company also focuses on enhancing patient engagement through mobile applications and remote monitoring integrations.

Top Strategies Used by Key Market Participants

A primary strategy employed by leading eHealth companies is the development of integrated, end-to-end digital ecosystems that unify clinical, financial, and administrative workflows. By offering comprehensive platforms that span electronic health records, revenue cycle management, telehealth, and analytics, firms create sticky environments that reduce provider dependency on third-party vendors. This vertical integration enhances data continuity, minimizes interoperability issues, and strengthens customer retention. It also enables seamless care coordination across settings, supporting value-based care models that rely on holistic patient data. Companies invest heavily in user experience design and clinical workflow optimization to ensure adoption and minimize clinician burnout, making their platforms indispensable to daily operations.

Another key strategy is strategic partnerships with technology giants, cloud providers, and pharmaceutical companies to expand capabilities and reach. Collaborations with firms like Microsoft, Amazon, and Google allow eHealth vendors to leverage advanced cloud infrastructure, artificial intelligence, and data storage solutions, enhancing scalability and innovation. Partnerships with life sciences companies enable the integration of real-world data into clinical trials and personalized medicine initiatives. These alliances also facilitate entry into new markets and accelerate the development of AI-driven decision support tools, predictive analytics, and genomics platforms, positioning eHealth providers at the intersection of healthcare and digital innovation.

A third strategic focus is the expansion into population health management and preventive care through data analytics and remote monitoring. Leading players are shifting from transactional systems to proactive health platforms that identify at-risk patients, predict disease progression, and enable early interventions.

RECENT HAPPENINGS IN THE MARKET

- In January 2024, Oracle completed the integration of Cerner’s health data platform with its cloud infrastructure, enabling real-time analytics and AI-driven clinical insights across connected healthcare systems. This enhancement is anticipated to improve care coordination and support large-scale public health initiatives.

- In February 2024, Epic Systems launched a new patient-facing application that consolidates medical records, appointment scheduling, and telehealth services into a single mobile interface. This innovation is expected to enhance patient engagement and streamline access to care across its provider network.

- In March 2024, Allscripts partnered with a leading AI health analytics firm to embed predictive risk modeling into its population health management platform. This collaboration is anticipated to strengthen clinical decision support and improve outcomes in chronic disease programs.

- In April 2024, Teladoc Health introduced a new integrated virtual care model combining primary care, mental health, and chronic condition management under a single subscription service. This offering is expected to increase user retention and expand its reach in employer and health plan markets.

- In May 2024, Siemens Healthineers launched a cloud-based imaging informatics platform that connects radiology departments across multiple hospitals for centralized reporting and AI-assisted diagnosis. This advancement is anticipated to enhance diagnostic accuracy and reduce reporting delays in large health networks.

MARKET SEGMENTATION

This research report on the global eHealth market has been segmented based on Type, services, end-user, and region.

By Type

- Telemedicine

- Consumer

- Information System

- EHR

- ePrescribing

- Health Information

- mHealth

- Health Management

- Clinical Decision Support

By Services

- Administrative

- Diagnostic

- Monitoring

- Financial

By End User

- Healthcare Consumers

- Providers

- Government

- Insurers

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

How much is the global eHealth market going to be worth by 2033?

As per our research report, the global eHealth market is forecasted to be worth USD 67.39 billion by 2033.

Which segment by type in the global eHealth market is predicted to lead in the coming years?

The ehr segment by type in the global eHealth market is predicted to showcase the fastest growth rate during the forecast period.

Which region accounted for the largest share in the global eHealth market in 2024?

Geographically, the North American regional market led the eHealth market in 2024.

Which are the companies playing a key role in the eHealth market?

Boston Scientific Corp., IBM, Motion Computing Inc., GE Healthcare, Epocrates Inc., Telecare Corp., CompuMed, Medisafe, SetPoint Medical, Doximity, Lift Labs, Proteus Digital Health, and Apple are some of the notable companies in the global eHealth market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com