Europe Aerial Photography Market Size, Share, Trends & Growth Forecast Report By Product Type, By Application, By End User, and By Country (Germany, France, United Kingdom, Italy, Spain & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Aerial Photography Market Size

The Europe Aerial Photography Market was valued at USD 1.32 billion in 2025, is estimated to reach USD 1.48 billion in 2026, and is projected to reach USD 3.64 billion by 2034, growing at a CAGR of 11.93% from 2026 to 2034.

Aerial photography is the practice of capturing images of the Earth's surface or features from elevated, airborne platforms like planes, drones, helicopters, or balloons. This market serves critical functions in urban planning, agriculture, infrastructure inspection, and environmental monitoring by providing precise visual intelligence. In the European context, the market is deeply integrated with digital transformation initiatives across various industries, driven by the need for accurate real-time data. As per Eurostat, 52.7 percent of enterprises in the European Union with ten or more employees used paid cloud computing services in 2025, primarily facilitating email (85.2%), office software (71.7%), and file storage (71.5%). The 75 percent figure represents the EU's Digital Decade target for 2030. Data analytics on satellite (aerial) imagery remains a niche application, performed by only 3.6 percent of enterprises. Furthermore, the European Environment Agency stated that land cover mapping requires consistent and high-quality imagery to monitor changes in biodiversity and land use effectively. The regulatory landscape, shaped by the European Union Aviation Safety Agency, ensures safe integration of drones into airspace, fostering a secure environment for commercial operations. The market is characterized by a shift towards automated data processing and artificial intelligence-driven analytics, which enhance the value proposition of aerial imagery. Industries such as construction and energy rely on these insights for predictive maintenance and project management. Consequently, the demand for specialized aerial photography services continues to grow, supported by technological advancements and stringent regulatory frameworks that prioritize safety and data privacy. This ecosystem enables stakeholders to make informed decisions based on comprehensive spatial information.

MARKET DRIVERS

Expansion of Precision Agriculture Practices

The expansion of precision agriculture practices is a key force behind the growth of the Europe aerial photography market. This is because farmers increasingly adopt data-driven techniques to optimize crop yields and resource usage. Aerial imagery provides detailed insights into plant health, soil conditions, and irrigation needs, enabling targeted interventions that reduce waste and improve productivity. As per forecasts supported by European Commission initiatives, the European precision agriculture landscape is projected to grow significantly through 2027, driven by the need for sustainable farming methods and digital integration. Drones equipped with multispectral cameras capture data that reveals variations in crop vigor, allowing farmers to apply fertilizers and pesticides only where necessary. This approach aligns with the European Green Deal objectives, which aim to reduce chemical pesticide use significantly by 2030. The ability to monitor large fields quickly and accurately reduces labor costs and enhances decision-making speed. Additionally, aerial photography supports compliance with agricultural subsidies and environmental regulations by providing verifiable evidence of land management practices. The integration of this data with farm management software creates a comprehensive ecosystem for modern agriculture. As climate change impacts weather patterns, the need for resilient farming strategies further boosts demand for aerial monitoring solutions. Consequently, the agricultural sector remains a significant contributor to the growth of the aerial photography market in Europe.

Infrastructure Development and Maintenance Requirements

The ongoing infrastructure development and maintenance requirements across the region significantly drive the demand for aerial photography services. This is also a top factor for the expansion of the Europe aerial photography market. Governments and private entities invest heavily in transportation networks, energy grids, and urban facilities, necessitating regular inspections to ensure safety and longevity. As per the European Investment Bank (EIB), total Group financing reached €100 billion in 2025, supporting key policy objectives including social infrastructure and digitalization, while the EU's external Global Gateway strategy mobilized its €300 billion investment target ahead of schedule. Aerial photography offers a cost-effective and safe alternative to manual inspections, particularly for hard-to-reach structures such as bridges, wind turbines, and power lines. High-resolution images and thermal data detect structural defects, corrosion, and heat anomalies before they lead to failures. This proactive approach minimizes downtime and repair costs while enhancing public safety. The use of drones reduces the need for scaffolding and heavy machinery, lowering operational risks for workers. Furthermore, aerial surveys provide accurate topographical data for planning new projects, ensuring efficient land use and regulatory compliance. The integration of building information modeling with aerial data enhances project visualization and coordination among stakeholders. European countries are prioritizing the modernization of aging infrastructure. As a result, the reliance on precise and timely aerial imagery is growing, solidifying its role as an essential tool in the construction and utilities sectors.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Privacy Concerns

Stringent regulatory frameworks and privacy concerns are limiting factors in the European aerial photography market. This limits operational flexibility and increases compliance burdens. The European Union Aviation Safety Agency imposes strict rules on drone operations, including no-fly zones, altitude limits, and licensing requirements for pilots. As per the European Data Protection Board, the General Data Protection Regulation mandates rigorous handling of personal data captured in aerial images, requiring operators to implement robust anonymization techniques. Non-compliance can result in severe penalties and legal actions, discouraging small businesses from entering the market. The complexity of navigating varying national regulations within member states further complicates cross-border operations. Operators must obtain specific permissions for flights in urban areas or near sensitive installations, leading to delays and increased administrative costs. Public apprehension regarding surveillance and privacy invasions also poses challenges, with communities often resisting drone activities in residential neighborhoods. This social resistance can lead to local bans or restrictions, limiting market access. Additionally, the requirement for insurance and certification adds to the operational expenses for service providers. These regulatory and social barriers hinder the widespread adoption of aerial photography services, particularly for small and medium-sized enterprises that lack the resources to manage complex compliance procedures. Consequently, the market faces constraints that slow down growth and innovation.

High Initial Investment and Operational Costs

High initial investment and operational costs associated with advanced aerial photography equipment and skilled personnel are a serious barrier to the Europe aerial photography market. Professional-grade drones, sensors, and processing software require significant capital expenditure, which can be prohibitive for smaller firms. As per the European Small Business Alliance, access to finance remains a critical challenge for small enterprises, limiting their ability to invest in expensive technology. The rapid pace of technological advancement necessitates frequent upgrades to maintain competitiveness, further straining budgets. Additionally, hiring and training certified pilots and data analysts involves considerable time and financial resources. The cost of insurance, maintenance, and regulatory compliance adds to the overall operational burden. For many potential users, the return on investment may not be immediately apparent, leading to hesitation in adopting aerial photography solutions. The economic uncertainty in some European regions exacerbates these financial pressures, causing businesses to prioritize essential expenditures over innovative technologies. Furthermore, the fragmentation of the market means that economies of scale are difficult to achieve for smaller operators. These financial barriers restrict market entry and limit the diversity of service providers, potentially stifling competition and innovation. High expenses are currently hindering broader market penetration. This obstacle will remain until costs decrease or financing options improve.

MARKET OPPORTUNITIES

Integration with Artificial Intelligence and Machine Learning

The integration of artificial intelligence and machine learning into aerial photography workflows provides a significant opportunity for the growth of the European aerial photography market. AI algorithms can automatically analyze vast amounts of imagery to identify patterns, detect anomalies, and generate actionable insights with high accuracy. As per sources, AI spending in Europe is projected to grow substantially through 2027 (surpassing the global growth rate), driven by the need for efficiency and precision in applications like image analysis. In the context of aerial photography, AI enables real-time processing of data, reducing the time required for manual interpretation. This capability is particularly valuable in sectors such as disaster management, where rapid assessment of damage is crucial for emergency response. Automated classification of land cover types supports environmental monitoring and urban planning initiatives. Additionally, predictive maintenance models powered by machine learning can forecast equipment failures based on visual indicators, enhancing operational reliability. The ability to process large datasets efficiently lowers labor costs and improves service scalability. Providers who offer AI-enhanced analytics can differentiate themselves in a competitive market by delivering higher value propositions. Furthermore, the combination of aerial imagery with other data sources, such as IoT sensors, creates comprehensive digital twins of physical assets. This holistic approach opens new revenue streams and strengthens customer relationships, driving sustained growth in the European aerial photography sector.

Expansion into Environmental Monitoring and Conservation

Environmental monitoring and conservation are creating significant prospects for the European aerial photography market. This growth is directly aligned with the continent’s strong commitment to sustainability. Governments and non-governmental organizations increasingly rely on aerial data to track deforestation, monitor wildlife populations, and assess the impact of climate change. As per the European Environment Agency, the establishment of protected areas under the Natura 2000 network requires regular monitoring to ensure ecological integrity. Aerial photography provides a non-invasive method to survey large and remote areas, capturing detailed information on habitat changes and biodiversity trends. Drones equipped with specialized sensors can detect illegal logging, pollution spills, and unauthorized construction activities, supporting enforcement efforts. The data collected aids in the development of conservation strategies and policy formulation. Additionally, aerial imagery supports carbon stock assessments and reforestation projects, contributing to climate mitigation goals. The growing awareness of environmental issues among consumers and investors drives demand for transparent and verifiable sustainability reporting. Companies that specialize in environmental aerial services can capitalize on this trend by offering tailored solutions for regulatory compliance and corporate social responsibility initiatives. This alignment with global sustainability agendas ensures long-term relevance and growth potential for the aerial photography market in Europe.

MARKET CHALLENGES

Data Management and Storage Complexities

Data management and storage complexities pose a major challenge for the European aerial photography market. This is driven by the rapidly accelerating volume of high-resolution imagery generated. Each flight can produce terabytes of data, requiring robust infrastructure for storage, processing, and retrieval. As per sources, the management of unstructured data is a critical challenge, with large enterprises expected to triple their unstructured data capacity by 2028. Furthermore, poor data quality costs organizations an average of $12.9 million annually. Storing this data securely while ensuring quick access for analysis demands significant investment in cloud services and hardware. The need for high-bandwidth connections to transfer large files further complicates operations, particularly in rural areas with limited connectivity. Additionally, maintaining data integrity and preventing loss during transmission and storage requires sophisticated backup and recovery systems. The complexity of managing metadata and ensuring compatibility with various software platforms adds to the operational burden. Organizations must also comply with data retention policies and legal requirements, which vary across jurisdictions. Failure to manage data effectively can lead to inefficiencies, increased costs, and potential legal issues. The lack of standardized data formats and protocols hinders interoperability between different systems and stakeholders. Addressing these challenges requires continuous investment in technology and expertise, which can be resource-intensive for smaller players. Scalable and cost-effective data management solutions are not yet widely available. Therefore, this issue will remain a significant hurdle for the industry.

Weather Dependence and Operational Limitations

Weather dependence and operational limitations are major hindrances to the Europe aerial photography market. This affects the reliability and consistency of service delivery. Adverse weather conditions such as rain, wind, and fog can ground drones and delay projects, leading to schedule disruptions and increased costs. As per the IPCC, climate change is intensifying the frequency of unpredictable weather patterns, which exacerbates operational risks for aerial surveys; reliable forecasting from agencies like the European Centre for Medium-Range Weather Forecasts (ECMWF) is becoming increasingly critical for mitigation. Flight restrictions imposed during poor visibility or high winds limit the windows available for data collection, particularly in regions with volatile climates. This unpredictability complicates planning and resource allocation for service providers. Additionally, certain terrains and environments present physical obstacles that hinder safe operation, such as dense forests or mountainous areas. Battery life limitations further restrict flight duration and coverage area, requiring multiple sorties for large projects. The need for specialized equipment to withstand harsh conditions increases capital expenditures. Moreover, seasonal variations affect demand, with peak periods often coinciding with favorable weather, creating bottlenecks in service capacity. Off-season periods may see reduced activity, impacting revenue stability. These operational constraints require providers to maintain flexible schedules and contingency plans, adding to managerial complexity. Weather-related risks continue to challenge the efficiency and profitability of European aerial photography operations. Mitigation through technological advancements is needed to resolve this.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Airbus Defence and Space, Hexagon AB, Fugro N.V., Nearmap Ltd, EagleView Technologies Inc., Bluesky International Ltd, Eurosense, Hansa Luftbild AG, MGGP Aero, BSF Swissphoto, Aerodata AG, GeoFly GmbH |

SEGMENTAL ANALYSIS

By Product Type Insights

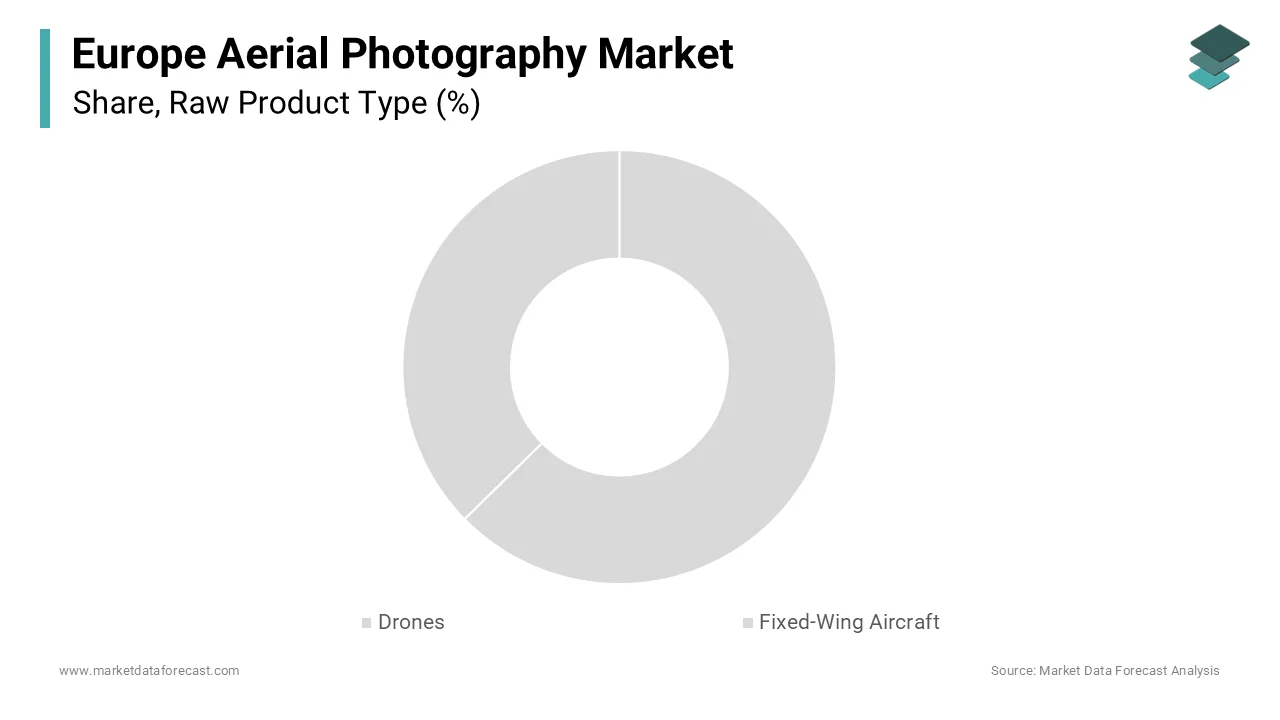

The drones segment was the largest segment in the Europe aerial photography market and occupied a 65.8% share in 2025. This supremacy of the segment is supported by the operational flexibility, cost efficiency, and technological advancements associated with unmanned aerial vehicles. The main driver for this segment is the ability of drones to access hard-to-reach areas without risking human safety. Unlike manned aircraft, drones can operate at lower altitudes and slower speeds, capturing high-resolution imagery with greater precision. This capability is essential for infrastructure inspections, where detailed visual data is required to identify structural defects. Additionally, the lower operational costs of drones make them accessible to small and medium-sized enterprises, expanding the user base. The integration of advanced sensors, such as LiDAR and thermal cameras, further enhances their utility in diverse applications. Regulatory frameworks have evolved to facilitate safe drone operations, reducing barriers to entry. The ease of deployment and rapid data acquisition also contribute to their popularity. Consequently, drones have become the preferred platform for aerial photography, supplanting traditional methods in many sectors due to their versatility and economic advantages.

The fixed-wing aircraft segment is expected to exhibit a noteworthy CAGR of 8.5% during the forecast period. This rapid expansion of the segment is fueled by the increasing demand for large-scale mapping and surveying projects that require extensive coverage areas. One of the major drivers is the need for high efficiency in agricultural monitoring and environmental assessments, where vast tracts of land must be imaged quickly. Fixed-wing platforms can cover hundreds of square kilometers in a single flight, reducing the time and cost per unit area. Advances in autonomous flight technologies have improved the precision and reliability of these aircraft, enhancing their appeal for professional surveyors. Additionally, the integration of hyperspectral sensors allows for detailed analysis of crop health and soil composition, supporting precision agriculture initiatives. Government agencies are increasingly utilizing fixed-wing aircraft for disaster management and border surveillance, driving institutional demand. The ability to carry heavier payloads enables the use of more sophisticated imaging equipment, providing higher-quality data. These factors collectively contribute to the robust growth of the fixed-wing segment in the European aerial photography market.

By Application Insights

The construction segment held the majority share of 30.3% of the Europe aerial photography market in 2025 because of the critical need for accurate site monitoring, progress tracking, and volume calculations in large infrastructure projects. A key driver for this segment is the ability of aerial photography to provide real-time insights into project status, enabling stakeholders to identify delays and optimize resource allocation. Drones equipped with photogrammetry software generate three-dimensional models of construction sites, facilitating precise measurements and clash detection. This technology reduces the need for manual surveys, which are time-consuming and prone to errors. Additionally, aerial imagery enhances safety by allowing inspectors to assess hazardous areas without physical presence. The integration of building information modeling with aerial data improves collaboration among architects, engineers, and contractors. Regulatory requirements for documentation and compliance also drive adoption, as aerial records provide verifiable evidence of work performed. The cost savings associated with improved efficiency and reduced rework further incentivize construction firms to invest in aerial photography services. These benefits establish construction as the leading application sector in the European market.

The agriculture segment is predicted to witness the highest CAGR of 9.2% from 2026 to 2034 due to the increasing adoption of precision farming techniques aimed at optimizing crop yields and minimizing environmental impact. The primary driver is the ability of aerial photography to detect early signs of pest infestations, disease, and nutrient deficiencies through multispectral imaging. This data allows farmers to apply inputs selectively, reducing waste and lowering production costs. The rise of smart farming initiatives has led to the integration of aerial data with automated irrigation and fertilization systems, enhancing overall farm efficiency. Additionally, aerial surveys support compliance with subsidy regulations by providing accurate records of land use and crop types. The scalability of drone technology makes it accessible to farms of all sizes, from small family holdings to large agribusinesses. Climate change pressures further necessitate adaptive management strategies, where timely aerial insights play a crucial role. These factors collectively accelerate the adoption of aerial photography in the agricultural sector across Europe.

By End User Insights

The Commercial segment led the Europe aerial photography market and captured a substantial share in 2025. This leading position of the segment is attributed to the widespread utilization of aerial imagery across various private sector industries, including real estate, media, energy, and telecommunications. The top factor behind this segment is the competitive advantage gained through high-quality visual content and data-driven decision-making. Real estate agents use aerial photography to showcase properties, while media companies utilize it for compelling storytelling in films and news reports. Energy companies rely on aerial inspections to maintain infrastructure integrity, reducing downtime and maintenance costs. The accessibility of user-friendly drone platforms has lowered the barrier to entry, enabling smaller firms to leverage aerial capabilities. Additionally, the growing demand for customized services tailored to specific industry needs supports market expansion. Commercial entities are willing to invest in advanced analytics and processing tools to extract maximum value from aerial data. This broad-based adoption across diverse commercial sectors ensures the continued leadership of this segment in the European market.

The military segment is estimated to register the fastest CAGR of 7.8% over the forecast period, owing to increasing defense budgets and the strategic importance of intelligence, surveillance, and reconnaissance operations in Europe. A key accelerator is the need for real-time situational awareness and border security in an evolving geopolitical landscape. Aerial photography provides critical intelligence for mission planning, target acquisition, and damage assessment. Advanced drones equipped with thermal and night vision capabilities enhance operational effectiveness in diverse environments. The development of indigenous European defense technologies reduces dependency on non-European suppliers, fostering local innovation and production. Additionally, joint military exercises and collaborations among NATO allies drive standardization and interoperability of aerial systems. The integration of artificial intelligence for automated threat detection further enhances the value of military aerial photography. As security concerns persist, the demand for sophisticated aerial surveillance solutions continues to rise, driving rapid growth in the military end-user segment.

COUNTRY LEVEL ANALYSIS

Germany Aerial Photography Market Analysis

Germany dominated the Europe aerial photography market and accounted for a 22.3% share in 2025. This dominance of the German market is driven by a strong industrial base and advanced technological infrastructure, particularly in the automotive and manufacturing sectors. A main fuel for the market in Germany is the rigorous demand for precision engineering and quality control in industrial processes. Aerial photography is extensively used for infrastructure inspection, including bridges, railways, and power grids, ensuring safety and compliance with strict regulatory standards. The presence of leading drone manufacturers and software developers fosters a robust ecosystem for aerial services. Additionally, the agricultural sector in Germany utilizes aerial imagery for precision farming, aligning with national sustainability goals. The government’s support for digital transformation initiatives further accelerates market growth. Regulatory clarity provided by the Federal Aviation Office facilitates safe and efficient drone operations. These factors collectively sustain Germany’s position as the largest and most mature market for aerial photography in Europe.

United Kingdom Aerial Photography Market Analysis

The United Kingdom was the next prominent country in the Europe aerial photography market and occupied a share of 18.2% in 2025. This growth of the UK market is propelled by a vibrant creative industry and a strong focus on infrastructure development. British companies are early adopters of drone technology for media production, real estate marketing, and construction monitoring. A major push for the market is the extensive coastline and diverse landscape, which require regular monitoring for environmental conservation and coastal erosion management. The construction sector also relies heavily on aerial surveys for large-scale projects, such as HS2 and urban regeneration schemes. The Civil Aviation Authority has established clear guidelines for drone operations, promoting safety and innovation. Additionally, the UK’s leadership in artificial intelligence and data analytics enhances the value proposition of aerial photography services. The presence of numerous specialized service providers creates a competitive environment that drives quality and affordability. These dynamics maintain the UK’s status as a key market for aerial photography innovation and adoption.

France Aerial Photography Market Analysis

France plays a major role in the Europe aerial photography market due to its vast agricultural lands and commitment to environmental preservation. Moreover, French farmers are increasingly adopting precision agriculture techniques, utilizing aerial imagery to optimize crop management and reduce chemical usage. A big reason for the market is the government’s emphasis on sustainable development and biodiversity protection. Aerial photography plays a crucial role in monitoring protected areas, forests, and water resources, supporting conservation efforts. The energy sector also utilizes drones for inspecting nuclear power plants and renewable energy installations, ensuring operational safety. The French Civil Aviation Authority has implemented progressive regulations to facilitate commercial drone operations. Additionally, the tourism and media sectors leverage aerial imagery for promotional content, showcasing the country’s scenic beauty. These factors contribute to the steady growth and diversification of the aerial photography market in France.

Italy Aerial Photography Market Analysis

Italy is another major player in the Europe aerial photography market owing to a strong emphasis on cultural heritage preservation and tourism. The country’s rich historical sites and archaeological treasures require regular monitoring and documentation, for which aerial photography is an invaluable tool. A key booster of the market is the need to protect and restore ancient structures using non-invasive techniques. Drones provide detailed images that help experts assess structural integrity and plan restoration projects. Additionally, the agricultural sector in Italy, particularly in regions like Tuscany and Puglia, utilizes aerial imagery for vineyard and olive grove management. The Italian Civil Aviation Authority has streamlined licensing procedures to encourage commercial drone use. The construction industry also adopts aerial surveys for infrastructure projects in urban and rural areas. These elements foster the continued expansion of the aerial photography market in Italy, balancing modernization with heritage conservation.

Spain Aerial Photography Market Analysis

Spain is anticipated to grow notably in the Europe aerial photography market from 2026 to 2034. The market status in Spain is marked by a booming tourism industry and significant investments in renewable energy. Spanish coastal regions and historic cities attract millions of visitors annually, creating demand for high-quality aerial content for marketing and promotion. A key support for the market is the rapid expansion of solar and wind energy facilities, which require regular inspections and maintenance. Aerial photography enables efficient monitoring of large solar farms and wind turbines, ensuring optimal performance and safety. The agricultural sector also benefits from drone technology for irrigation management and crop health assessment. The Spanish State Safety Agency for Air Navigation has established clear frameworks for drone operations, supporting industry growth. Additionally, the construction sector utilizes aerial surveys for infrastructure development and urban planning. These factors support the dynamic growth of the aerial photography market in Spain, driven by diverse industrial and service sector needs.

COMPETITIVE LANDSCAPE

The competition in the Europe aerial photography market is intense and characterized by the presence of global technology giants alongside specialized regional manufacturers. Major players compete on the basis of hardware performance, software integration, and data security features. Differentiation is increasingly achieved through specialized sensors and artificial intelligence-driven analytics that provide actionable insights for specific industries. Regulatory compliance with European Union Aviation Safety Agency standards serves as a critical barrier to entry, favoring established companies with robust legal and technical resources. Price competition is significant in the consumer segment, while professional markets prioritize reliability and support services. Collaborations with local distributors and service providers enhance market reach and customer engagement. The rise of open source platforms encourages innovation but also increases the threat of new entrants. Customer loyalty is driven by ecosystem lock-in, where hardware compatibility with proprietary software creates switching costs. As demand for real-time data grows, the ability to offer rapid processing and secure cloud storage becomes a key determinant of success in this dynamic and evolving market landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Aerial Photography Market include

- Airbus Defence and Space

- Hexagon AB

- Fugro N.V.

- Nearmap Ltd

- EagleView Technologies Inc.

- Bluesky International Ltd

- Eurosense

- Hansa Luftbild AG

- MGGP Aero

- BSF Swissphoto

- Aerodata AG

- GeoFly GmbH

TOP LEADING PLAYERS IN THE MARKET

- DJI Innovation is a global leader in civilian drone technology with a dominant presence in the Europe aerial photography market. The company contributes significantly to the global sector by providing accessible and high-performance unmanned aerial vehicles equipped with advanced imaging sensors. DJI has recently strengthened its position by introducing new enterprise models featuring enhanced obstacle avoidance and longer flight times tailored for professional surveying and inspection tasks. The firm actively collaborates with European software developers to ensure seamless integration of its hardware with data processing platforms. By focusing on user-friendly interfaces and robust build quality, DJI appeals to both commercial operators and hobbyists. Its commitment to regular firmware updates and customer support reinforces brand loyalty. These strategic initiatives maintain their reputation as the preferred choice for reliable and versatile aerial photography solutions across diverse industries in Europe.

- Parrot SA is a prominent French manufacturer specializing in professional drones for the Europe aerial photography market. The company contributes to the global market by emphasizing data security and sovereignty, which are critical concerns for European government and industrial clients. Parrot has recently strengthened its market position by expanding its ANAFI series with specialized thermal and multispectral cameras for agricultural and infrastructure inspections. The firm prioritizes compliance with European regulations, offering secure data storage options that align with local privacy laws. Parrot actively partners with local distributors and service providers to enhance its regional support network. Its focus on open source software allows for greater customization and integration with third-party applications. By targeting niche professional segments with high-value-added features, Parrot differentiates itself from mass market competitors. These actions solidify its standing as a trusted provider of secure and specialized aerial imaging tools in Europe.

- SenseFly SA, a subsidiary of AgEagle Aerial Systems, is a key player in the Europe aerial photography market, renowned for its fixed-wing mapping drones. The company contributes to the global market by delivering precise and efficient solutions for large-scale surveying and agricultural monitoring. SenseFly has recently strengthened its position by launching updated versions of its eBee series with improved battery life and modular sensor capabilities. The firm focuses on providing end-to-end workflows that combine hardware with powerful photogrammetry software for accurate data analysis. SenseFly actively engages with agricultural cooperatives and construction firms to demonstrate the operational benefits of its technology. Its emphasis on ease of use and rapid data processing appeals to professionals seeking efficiency. By maintaining strong relationships with European resellers and offering comprehensive training programs, SenseFly ensures high customer satisfaction. These efforts reinforce its leadership in the professional mapping and surveying segment of the European aerial photography industry.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe aerial photography market predominantly employ strategies focused on technological innovation and regulatory compliance to maintain a competitive advantage. Companies invest heavily in research and development to enhance drone autonomy, sensor resolution, and data processing capabilities. Strategic partnerships with software providers enable integrated solutions that offer comprehensive analytics for end users. Emphasis on data security and privacy aligns with European regulations, building trust among government and enterprise clients. Expansion into specialized verticals such as agriculture and infrastructure inspection allows firms to tailor offerings to specific industry needs. Training and certification programs for pilots ensure safe operations and promote professional standards. Marketing efforts highlight cost efficiency and safety benefits compared to traditional methods. These strategies collectively aim to differentiate products, enhance customer value, and navigate the complex regulatory landscape effectively.

MARKET SEGMENTATION

This research report on the europe aerial photography market is segmented and sub-segmented into the following categories.

By Product Type

- Drones

- Fixed-Wing Aircraft

By Application

- Construction

- Agriculture

By End User

- Commercial

- Military

By Country

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com