Europe Air Defense System Market Size, Share, Trends & Growth Forecast Report By Component ( Weapon System, Fire Control System, Command and Control System, Others), Type, Platform, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2025 To 2033

Europe Air Defense System Market Size

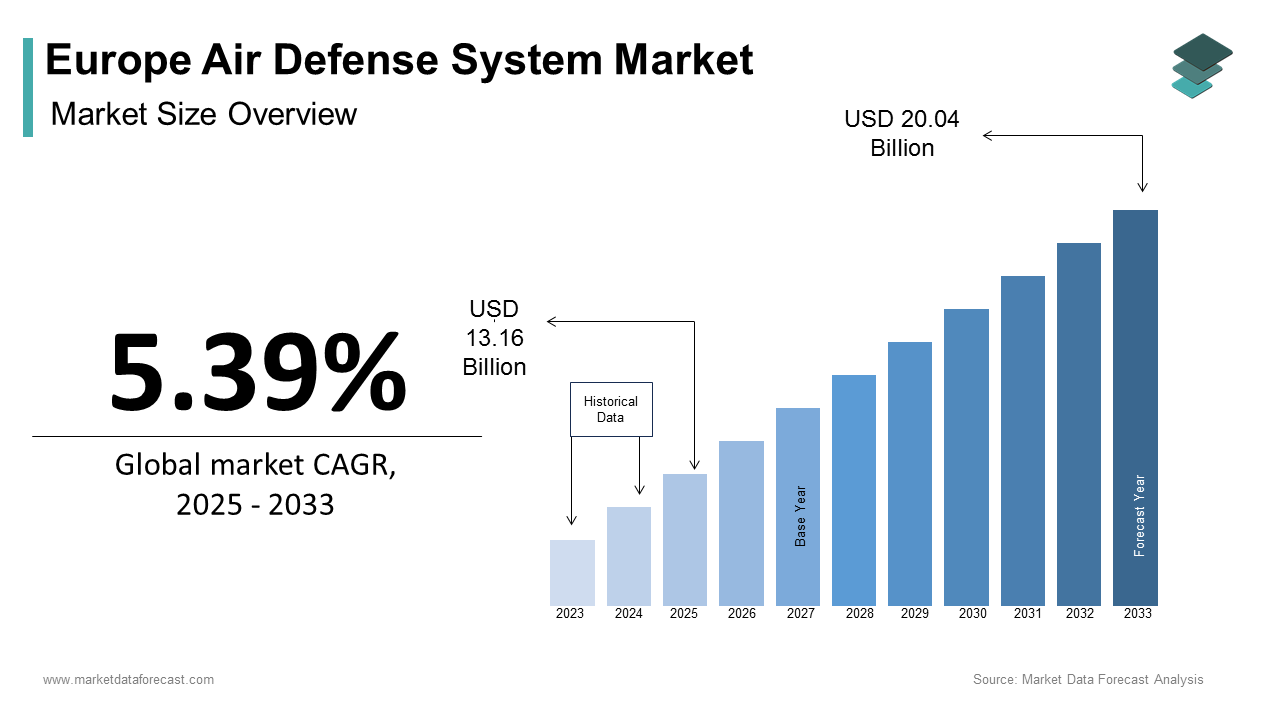

The European air defence system market size was calculated to be USD 12.49 billion in 2024 and is anticipated to be worth USD 20.04 billion by 2033 from USD 13.16 billion in 2025, growing at a CAGR of 5.39% during the forecast period.

Air defense systems are an array of radar-guided interceptors, command and control infrastructures, and counter aerial threat platforms engineered to detect, track, and neutralize airborne hazards ranging from manned combat aircraft to autonomous drones and cruise missiles. Unlike legacy point defense setups, contemporary European doctrine emphasizes a multi-layered integrated architecture capable of addressing hybrid threats in both conventional and asymmetric warfare environments. More than 20 EU member states have formally acknowledged critical gaps in low-altitude airspace monitoring, especially below 3000 meters, where miniaturized unmanned systems operate undetected. According to the European Union Aviation Safety Agency, 120 unauthorized drone incidents near European airports, energy plants, and military installations in 2023. As per the European Commission, many EU countries lack standardized data exchange protocols for integrated air picture generation, which undermines coordinated response mechanisms under the EU’s Permanent Structured Cooperation framework.

MARKET DRIVERS

Escalating Geopolitical Tensions and Border Airspace Violations

The growing military posturing along Europe’s eastern and southern borders has triggered a continent-wide urgency to reinforce national and collective air defense readiness, which is one of the key factors propelling the growth of the European air defense systems market. Since Russia’s full-scale invasion of Ukraine in February 2022, NATO air policing missions have significantly increased year on year, according to NATO’s 2023 Air Policing Activity Report. Baltic states and Black Sea allies routinely report intercepts of Russian Tu-955 and Su-27 aircraft operating in international airspace with provocative flight patterns. Finland’s Ministry of Defence reported 17 such encounters in 2023, while Sweden logged 16 unauthorized approaches near Gotland. The battlefield use of Iranian-made Shahed 136 loitering munitions in Ukraine has exposed vulnerabilities in legacy radar systems, prompting rapid investments in counter-drone capabilities. Germany’s 2024 defense budget includes 1 billion euros dedicated to mobile short-range air defense units for forward base protection. Poland finalized a 4.6-billion-dollar acquisition of Patriot Advanced Capability 3 systems, explicitly citing ballistic and cruise missile threats from neighbouring regions. This strategic recalibration reflects a doctrine shift toward layered area denial systems designed to intercept threats before they reach population centers or critical infrastructure.

Mandated Modernization of Aging Cold War Era Platforms

A significant portion of Europe’s air defense inventory remains rooted in Cold War-era designs that are increasingly obsolete against modern aerial threats, which is further contributing to the air defense systems market expansion in Europe. According to the Stockholm International Peace Research Institute, many short-range air defense launchers in Central and Eastern Europe were deployed before the mid-1990s and lack modern digital networking or electronic counter-countermeasure resilience. For instance, the French Crotale and German Roland systems have limited integration with NATO’s Integrated Air and Missile Defense frameworks, which constrains real-time coordination during joint operations. This technological obsolescence has forced national rearmament cycles to accelerate. As per the European Defence Agency, the average service life of European air defense missile systems often exceeds recommended operational ceilings. Spain has already retired its entire Hawk missile battery, while Hungary began deploying NASAMS to replace Soviet era S 125 Neva systems. These modernization mandates are not merely tactical upgrades but foundational requirements to comply with NATO’s readiness benchmarks, which emphasize interoperability sensor-to-shooter linkages across all member air defense networks.

MARKET RESTRAINTS

Persistent Budgetary Fragmentation and Interoperability Deficits

Despite shared security imperatives, European defense spending remains highly decentralized, leading to redundant procurement and interoperability failures, which are significant impediments to the European market growth. According to the European Defence Agency, collaborative defence equipment procurement by EU member states stood at around 18% in 2022, which is below the 35% benchmark. This fragmentation results in parallel maintenance ecosystems across numerous distinct short-range air defense platforms. Nations like Romania continue operating analog P-18 radars alongside digital command posts, creating data translation bottlenecks during coalition operations. The Netherlands relies on the U.S. Integrated Battle Command System for sensor fusion, while Italy uses national middleware incompatible with French networks. As per European Defence Agency analyses, a significant share of national air defense budgets is consumed by legacy platform sustainment rather than new capability development. Without standardized communication protocols and shared logistics frameworks, Europe’s collective air shield remains a mosaic of isolated nodes rather than a unified defensive continuum.

Regulatory and Export Control Barriers Affecting Technology Access

Stringent national export regulations and U.S. International Traffic in Arms Regulations significantly delay the integration of advanced components into European air defense systems, which further restrains the regional market growth. According to the European Parliament’s defense industrial strategy, many critical subsystems, such as missile seekers and phased array transmitters, are sourced from non-EU suppliers subject to political licensing reviews. These constraints have caused significant delays in system fielding for multinational programs like MEAD, as noted in audit reviews. Even within the differing national security clearance protocols, they impede the free flow of sensitive technical data. French and Swedish defense firms have publicly cited restrictions on sharing radar waveform libraries, which are essential for electronic countermeasure development. Such regulatory asymmetries not only inflate program costs but also reduce Europe’s ability to rapidly iterate on emerging threat responses, particularly in domains like directed energy and artificial intelligence-enabled target discrimination, where timely data integration is paramount.

MARKET OPPORTUNITIES

Joint European Development of Next Generation Integrated Air Defense

Europe is strategically co-investing in sovereign next-generation air defense architectures to reduce external dependencies and ensure technological autonomy, which is a promising opportunity for the European air defense systems market. The TWISTER program, led by France, Germany, and Italy, has secured EU funding under the European Defence Fund. Designed as a scalable system of systems, TWISTER will unify radar, command, missile, and cyber electronic warfare functions into a single open architecture capable of countering hypersonic and swarm threats. Complementing this long-term vision, the European Sky Shield Initiative has grown to include numerous nations with pooled procurement commitments, according to the German Federal Ministry of Defence. This initiative has already compressed delivery timelines through consolidated logistics and shared maintenance hubs. Meanwhile, the European Innovation Council has granted significant funding to startups developing AI-driven threat prioritization engines and gallium nitride-based solid-state radars. These initiatives collectively aim to establish a resilient EU-based supply chain for critical air defense technologies, helping to circumvent foreign export controls that have historically delayed system deployment.

Integration of Artificial Intelligence and Autonomous Sensor Fusion

The incorporation of artificial intelligence into air defense command and control is emerging as a high-impact opportunity to manage complexity and accelerate decision cycles, which is further anticipated to provide lucrative growth possibilities to the European air defense systems market. According to NATO Allied Command Transformation, AI-enabled systems reduced simulated engagement timelines during the 2024 Steadfast Defender exercise by autonomously correlating data from radar, RF detection electro-optical sensors. European defense contractors such as Thales and Leonardo are now embedding machine learning algorithms that can differentiate between decoys, cruise missiles, and commercial aircraft with high accuracy, as validated in joint French Italian trials. National programs are also advancing. The UK’s Dragonfire laser demonstrator integrates AI-driven beam control to track and engage multiple fast-moving drones simultaneously. Meanwhile, Finland’s Indra-led air surveillance modernization project uses neural networks to predict intrusion routes based on historical drone flight patterns. As per the European Defence Agency, these AI layers are projected to cut operator cognitive load and reduce false alarm rates compared to rule-based legacy systems. This digital transformation not only enhances defensive precision but also enables smaller nations to operate sophisticated networks with limited personnel, which is a critical enabler for Europe’s distributed defense strategy.

MARKET CHALLENGES

Emergence of Drone Swarm and Standoff Weapon Threats

The current air defense networks of Europe are increasingly mismatched against low-cost, high-volume aerial threats, which is primarily challenging the air defense systems market growth in Europe. During NATO’s 2024 Steadfast Defender exercise, defenders faced simulated attacks involving large numbers of synchronized drones employing swarm logic to overwhelm engagement capacities. Commercial drones modified for military use now constitute a majority of airspace violations in sensitive European zones. These platforms exploit radar blind spots by flying at very low altitudes and using mesh networking to maintain coordination without centralized control. Concurrently, the proliferation of long-range standoff weapons like Russia’s Kh-101 cruise missile, which has a verified range exceeding 2500 kilometers, enables strikes from deep within adversary territory beyond the reach of most European interceptors. Existing systems, such as Patriot, require expensive interceptors costing millions of dollars per shot, which is making cost exchange ratios unsustainable against drone swarms priced at a few hundred dollars each. Until directed energy or electronic attack systems achieve operational maturity, Europe remains exposed to saturation attacks that exploit the kinetic cost asymmetry inherent in current defenses.

Industrial Capacity Constraints and Skilled Workforce Shortages

The defense industrial base of Europe lacks the scalable production capacity and specialized workforce needed to meet accelerated air defense modernization demands, which is also challenging the regional market growth. According to the European Defence Agency, few EU nations maintain active missile final assembly lines, and current capacity constraints limit annual interceptor output. This bottleneck is exacerbated by acute shortages of engineers with expertise in radio frequency systems, embedded software, and propulsion. As per Eurofound, significant shortages of qualified radar systems engineers across major European defense hubs, including Toulouse and Bremen. Moreover, the supply chain for rare earth elements and high-performance semiconductors remains heavily dependent on non-EU sources. As per the European Commission, high import reliance on gallium and germanium used in phased array radars, with a substantial share sourced from China, creates strategic vulnerabilities. These structural limitations not only delay system deliveries but also constrain the ability to surge production during crises. Without targeted investments in vocational training, secure materials sourcing, and digital twin-enabled manufacturing, Europe’s ambition to field a continent-wide integrated air defense shield by 2035 remains at significant risk of schedule slippage and capability gaps.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.39% |

| Segments Covered | By Component, Type, Platform, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Airbus, Thales Group, Leonardo S.p.A., Saab AB, MBDA, Rheinmetall AG, BAE Systems, Kongsberg Gruppen, Raytheon Technologies, Diehl Defence |

SEGMENTAL ANALYSIS

By Component Insights

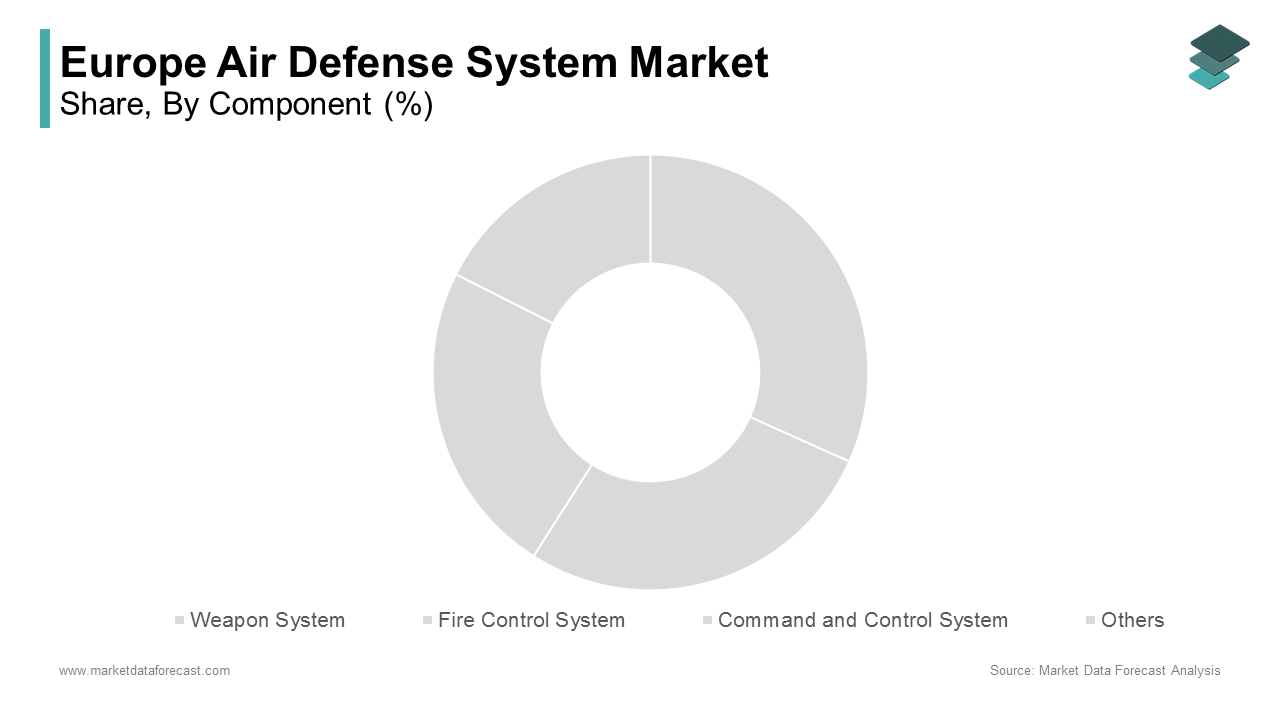

The weapon system segment commanded 40.8% of the European air defense systems market in 2024. The dominance of the weapon system segment in the Europe air defense systems market is majorly driven by the urgent need to replace aging missile inventories and acquire next-generation interceptors capable of countering emerging aerial threats, and the large-scale depletion of missile stocks due to wartime transfers to Ukraine. According to the International Institute for Strategic Studies, European NATO members have donated large quantities of surface-to-air missiles since 2022, including Stingers from Germany and Starstreaks from the UK, which have forced rapid replenishment cycles. Poland’s Wisła program represents a multi-billion-dollar commitment to Patriot air and missile defense. Additionally, the shift toward multi-role interceptors such as the Aster 30 Block 1NT used in the SAMP T system enables engagement of both aircraft and tactical ballistic missiles, thereby increasing per-unit value and procurement volume. France and Italy have jointly committed significant funding through 2028 to expand Aster missile production at MBDA’s Bourges facility, which now operates at high capacity to meet European and export demand.

The command-and-control system segment is projected to grow at the highest CAGR of 10.4% over the forecast period in the European air defense systems market, owing to the continent’s strategic pivot toward integrated and interoperable air defense networks under frameworks like the European Sky Shield Initiative and NATO’s Integrated Air and Missile Defense. European nations are prioritizing the replacement of stovepiped national command posts with shared battlefield management systems. Germany’s deployment of the Extended Air Defense Task Force command suite enables real-time coordination between Patriot NASAMS and future TWISTER batteries across four allied nations, as documented in the Bundeswehr’s 2024 interoperability report. The UK is pursuing a common sensor-to-shooter architecture linking radar data from land, naval, and airborne platforms. The European Defence Fund announced close to 1 billion euros of investment in 2024 calls, including projects for C2 modernization, such as AI-assisted threat correlation engines and secure tactical data links resistant to electronic warfare. These investments reflect a doctrinal shift from platform-centric defense to network-centric operations, where command and control become the central nervous system of layered air defense.

By Type Insights

The missile defense systems segment held the major share of the European air defense systems market in 2024. The growth of the missile defense systems segment in the European market is driven by the growing threat of ballistic and cruise missile attacks, particularly from Russia’s Kalibr and Iskander systems, which have ranges capable of striking deep into European territory. Poland’s Wisła program, which includes Patriot fire units and a large inventory of interceptors, constitutes one of the largest air defense investments in Central Europe. Romania has activated Patriot batteries under the NATO missile defense umbrella, while Spain is upgrading its ground-based air defense systems to engage ballistic threats. Many EU member states now classify tactical ballistic missile defense as a top-tier national security priority. Furthermore, the U.S. European Phased Adaptive Approach has spurred host nation investments in Aegis Ashore infrastructure, with Romania’s Deveselu site requiring substantial national support for maintenance and force protection.

The C-RAM segment is promising and is estimated to expand at a CAGR of 12.08% over the forecast period, owing to the increasing use of indirect fire and loitering munitions in hybrid conflict scenarios, particularly along Europe’s southern periphery and in expeditionary operations. Germany has deployed counter-rocket artillery and mortar systems to its forward bases, where they provide 360-degree protection against mortar and drone threats. The Netherlands is enhancing its future air defense architecture specifically to counter asymmetric rocket attacks on military camps and critical infrastructure. European programs have awarded funding to consortia developing laser and microwave-based C RAM solutions that offer near infinite magazine depth at a fraction of kinetic intercept costs. The battlefield experience in Ukraine, where frequent mortar and rocket attacks have targeted rear echelon positions, has amplified European urgency to field mobile C RAM units that can protect logistics hubs, airfields, and command centers against low altitude saturation strikes.

By Platform Insights

The missile defense systems segment held the major share of the European air defense systems market in 2024. The growth of the missile defense systems segment in the European market is driven by the growing threat of ballistic and cruise missile attacks, particularly from Russia’s Kalibr and Iskander systems, which have ranges capable of striking deep into European territory. Poland’s Wisła program, which includes Patriot fire units and a large inventory of interceptors, constitutes one of the largest air defense investments in Central Europe. Romania has activated Patriot batteries under the NATO missile defense umbrella, while Spain is upgrading its ground-based air defense systems to engage ballistic threats. Many EU member states now classify tactical ballistic missile defense as a top-tier national security priority. Furthermore, the U.S. European Phased Adaptive Approach has spurred host nation investments in Aegis Ashore infrastructure, with Romania’s Deveselu site requiring substantial national support for maintenance and force protection.

The C-RAM segment is promising and is estimated to expand at a CAGR of 12.08% over the forecast period, owing to the increasing use of indirect fire and loitering munitions in hybrid conflict scenarios,o s particularly along Europe’s southern periphery and in expeditionary operations. Germany has deployed counter-rocket artillery and mortar systems to its forward bases, where they provide 360-degree protection against mortar and drone threats. The Netherlands is enhancing its future air defense architecture specifically to counter asymmetric rocket attacks on military camps and critical infrastructure. European programs have awarded funding to consortia developing laser and microwave-based C RAM solutions that offer near infinite magazine depth at a fraction of kinetic intercept costs. The battlefield experience in Ukraine, where frequent mortar and rocket attacks have targeted rear echelon positions, has amplified European urgency to field mobile C RAM units that can protect logistics hubs, airfields, and command centers against low altitude saturation strikes.

REGIONAL ANALYSIS

Germany Air Defense Systems Market Analysis

Germany held the leading position in the European air defense systems market in 2024 by holding 22.6% of the European market share. The dominance of Germany in the European market can be credited to both massive procurement programs and its role as a hub for European defense industrial collaboration. The Bundeswehr’s special fund supports air defense modernization, and in March 202,4, Germany awarded a $1.2 billion Patriot contract and provided initial funding for the TWISTER program. As per the German Federal Ministry of Defence, many of these systems are sourced from domestic or joint European suppliers such as Diehl Defence and MBDA Deutschland, ensuring technology retention and export control autonomy. Germany also hosts the European Sky Shield Initiative coordination cell, and the initiative includes about 20 European nations with substantial commitments to joint procurement frameworks. Furthermore, its defense industrial base supports tens of thousands of high-tech jobs in rad, ar missile, and C2 development, reinforcing its strategic centrality in continental air defense architecture.

France Air Defense Systems Market Analysis

France commanded a substantial share of the Europe air defense systems market in 2024. The unwavering commitment of France to strategic autonomy and indigenous technological development is propelling the French market growth. The French Ministry of Armed Forces has committed significant funding through 2030 to modernize national air defense, including the deployment of SAMP T batteries upgraded with Aster 30 Block 1NT missiles capable of intercepting medium-range ballistic threats. As per the Direction Générale de l’Armement, France operates a vertically integrated air defense supply chain from radar development at Thales to missile production at MBDA’s Bourges facility. France also leads the FCAS combat air system, which includes a next-generation airborne early warning and control function to support ground-based defenses. France’s defense exports surged in 2024, with air defense systems accounting for a substantial share of sales, primarily to Greece, India, Iraq, and Qatar, underscoring its dual role as a national protector and global technology provider.

United Kingdom Air Defense Systems Market Analysis

The United Kingdom is estimated to account for a prominent share of the European air defense market over the forecast period, owing to the distinct emphasis on expeditionary and naval integrated capabilities. The UK’s Future Anti-Air Ground Environment program will replace the aging Rapier system with a layered architecture combining Sky Sabre medium-range and future directed energy short-range systems. Sky Sabre batteries are integrated with NATO data links, enabling real-time data exchange with allied forces. The Royal Navy’s six Type 45 destroyers provide the backbone of maritime air defense, and the Sea Viper system has achieved successful intercepts during NATO’s Formidable Shield exercises. Additionally, the UK announced a£ 1.6 billion package to supply 5,000 air defense missiles to Ukraine, including Starstreak and Martlet systems. This blend of global reach, national resilience, and alliance interoperability defines the UK’s unique market position.

Poland Air Defense Systems Market Analysis

Poland is estimated to register a healthy CAGR in the European air defense systems market during the forecast period. The largest national rearmament program since the end of the Cold War is driving the market growth in Poland. According to the Polish Armaments Agency, Poland’s air defense investments through 2035 cover four complementary systems creating a seamless multi-layered shield. In 2024, Poland signed a contract to produce 48 Patriot M903 launchers under the Wisła program’s second phase. Poland’s eastern border is defended by a dispersed network of air defense batteries with expanded radar coverage supporting operations inland. Poland has also established maintenance and training centers for Patriot and CAMM systems in collaboration with Raytheon and MBDA, which is creating a sovereign sustainment capability. This unprecedented scale reflects Poland’s frontline status in NATO’s deterrence posture and its commitment to achieving full air defense autonomy by 2030.

Italy Air Defense Systems Market Analysis

Italy is expected to exhibit a steady CAGR in the Europe air defense systems market during the forecast period due to deep multinational integration and maritime focus. As a core partner in the SAMP/T system alongside France, Italy operates 10 fire units equipped with Aster 30 missiles and has committed 1.2 billion euros through 2028 to upgrade them for anti-ballistic roles. The Italian Navy’s fleet of 10 FREMM frigates and two Horizon destroyers form the nucleus of EU naval air defense, with the SAAM system providing area protection in the Mediterranean. Over half of Italy’s national air defense expenditures since 2022 have supported joint European programs, including TWISTER and the European Sky Shield Initiative. Italy also hosts the NATO Integrated Air and Missile Defense Centre of Excellence in Cremona, which coordinates doctrine development and interoperability testing for 32 allied nations. This dual land, naval, and alliance-oriented strategy positions Italy as a key enabler of collective European air defense resilience, particularly in the strategically vital central Mediterranean corridor.

COMPETITION OVERVIEW

Competition in the Europe air defense systems market is characterized by a strategic interplay between sovereign European champions and established U.S. defense primes. European firms such as MBDA and Thales leverage deep integration with national armed forces and policy mandates for strategic autonomy to secure long-term development contracts. Meanwhile, American companies like Raytheon maintain dominance through proven systems such as Patriot and NASAMS, which offer immediate interoperability with NATO standards. The competitive landscape is further intensified by joint multinational programs like TWISTER and SAMP T that blend industrial participation across borders, creating complex supply chain alliances. Emerging entrants from Israel and Turkey are also gaining traction through specialized counter-rocket and drone technologies. This dynamic environment fosters innovation but also pressures legacy vendors to accelerate digital transformation and cost efficiency to retain relevance amid rapidly evolving threat architectures.

KEY MARKET PLAYERS

A few major players of the Europe air defense systems market include

- Airbus

- Thales Group

- Leonardo S.p.A

- Saab AB

- MBDA

- Rheinmetall AG

- BAE Systems

- Kongsberg Gruppen

- Raytheon Technologies

- Diehl Defence

Top Strategies Used by the Key Market Participants

Key players in the Europe air defense systems market are prioritizing strategic co-development initiatives to enhance sovereign capability and reduce transatlantic dependency. They are investing heavily in next-generation interceptor technologies that counter drone swarms and hypersonic threats through solid-state propulsion and networked guidance systems. Companies are establishing regional sustainment hubs to ensure rapid maintenance, training, and logistics support for allied forces. Collaborative framework agreements under the European Sky Shield Initiative and Permanent Structured Cooperation enable bulk procurement cost sharing and interoperability standardization. Additionally, firms are embedding artificial intelligence into command and control layers to accelerate threat discrimination and reduce operator workload in high-intensity scenarios.

Leading Players in the Market

MBDA

MBDA is a leading European missile systems consortium formed by Airbus, BAE Systems, and Leona, and plays a central role in Europe’s air defense ecosystem through its Aster CAMM and Mistral missile families. The company supplies critical interceptors for major platforms, including SAMP T and Sea Viper, and is the prime contractor for the next-generation TWISTER program. In 2024, MBDA expanded its Bourges missile production facility in France to meet surging European demand and signed a strategic cooperation agreement with Germany’s Diehl Defence to co-develop counter-drone effectors, enhancing its role in layered defense architectures across the continent.

Raytheon

Raytheon, a principal U.S. defense contractor, maintains deep integration within the European air defense landscape primarily through its Patriot and NASAMS systems. The company has secured multiple contracts across Poland, Germany, and the Netherlands to deliver fire units, MSE interceptors, and system modernization kits. In early 2025, Raytheon completed the delivery of Patriot hardware for Poland’s Wisła program and established a regional sustainment hub in Düsseldorf to support long-term maintenance logistics and training for allied forces, reinforcing its operational footprint in Europe.

Thales

Thales is a pivotal French technology group delivering advanced radar command and control and electro-optical sensors that form the backbone of European air defense networks. Its Ground Master radar family equips over 15 European nations, while its contribution to the FCAS program includes next-generation threat detection modules. In November 2024, Thales unveiled an AI-powered air surveillance demonstrator capable of tracking over 1000 simultaneous tracks, including low radar cross-section drones. The company also partnered with the UK Ministry of Defence to integrate its cybersecurity protocols into Sky Sabre, enhancing resilience against electronic warfare, a move that solidifies its position as a trusted sovereign technology provider.

MARKET SEGMENTATION

This research report on the Europe air defense system market has been segmented and sub-segmented based on component, type, platform, and region.

By Component

- Weapon System

- Fire Control System

- Command and Control System

- Others

By Type

- Missile Defense System

- Anti-aircraft System

- Counter Rocket, Artillery, and Mortar (C-RAM) System

By Platform

- Airborne

- Land

- Naval

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers of the market?

Key drivers include rising geopolitical tensions, increased defense spending by European countries, technological advancements, and the need for modernizing aging military infrastructure.

2. Who are the major players in this market?

Key players include Airbus, Thales Group, Leonardo S.p.A., Saab AB, MBDA, Rheinmetall AG, BAE Systems, Kongsberg Gruppen, Raytheon Technologies, and Diehl Defence.

3. Which countries are leading in the European air defense system market?

Major contributors include the United Kingdom, France, Germany, Italy, and Sweden, owing to their strong defense budgets and indigenous defense manufacturers.

4. How is NATO influencing the air defense market in Europe?

NATO initiatives and collaborations have encouraged standardization, joint procurement, and strategic deployment of air defense systems among member countries.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com