Europe Aircraft Leasing Market Size, Share, Trends, & Growth Forecast Report By Aircraft Type (Narrow Body, Wide Body, Regional Aircraft), Lease Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Aircraft Leasing Market Report Summary

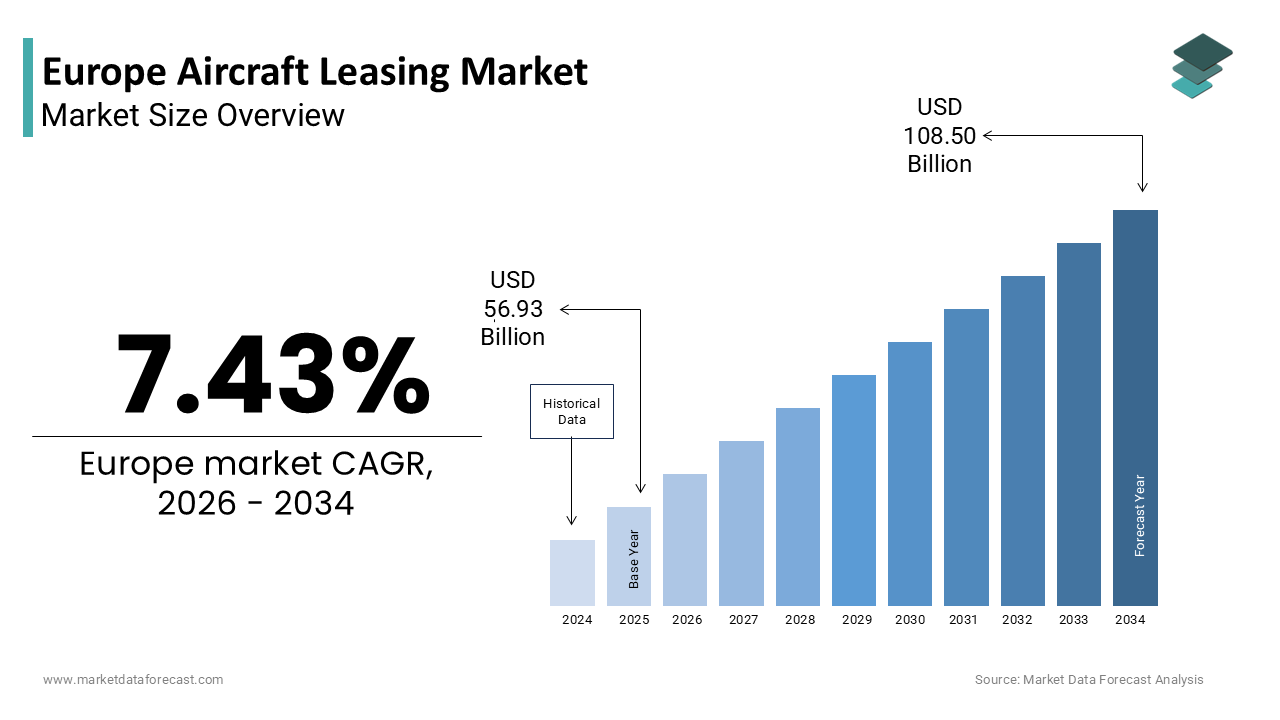

The Europe aircraft leasing market was valued at USD 56.93 billion in 2025, is estimated to reach USD 61.16 billion in 2026, and is projected to reach USD 108.50 billion by 2034, growing at a CAGR of 7.43% during the forecast period from 2026 to 2034. The growth of the market is driven by increasing air passenger traffic, fleet modernization requirements, and the need for flexible financing solutions among airlines. Aircraft leasing enables carriers to optimize capital expenditure, enhance fleet flexibility, and respond quickly to fluctuating demand. Additionally, the rising focus on fuel-efficient aircraft and sustainability regulations (such as the EU Fit for 55 targets) is accelerating the adoption of leased modern aircraft across Europe.

Key Market Trends

- Increasing demand for operating leases and sale-and-leaseback transactions

- Strong shift toward fuel-efficient and next-generation aircraft fleets

- Growing adoption of sustainable aviation fuel (SAF)-linked leasing strategies

- Rising use of digital platforms and AI for asset management and predictive maintenance

- Expansion of short-term wet leasing for seasonal and tourism demand

Segmental Insights

- By Aircraft Type: The narrow-body aircraft segment dominated the market with 61.2% share in 2025, driven by high-frequency short-haul routes and strong demand from low-cost carriers

- The wide-body aircraft segment is projected to grow at the fastest rate due to the recovery of long-haul travel and expansion of intercontinental routes

- By Lease Type: The dry lease segment held the largest share due to cost efficiency and greater operational control for airlines

- The wet lease segment is expected to grow at the fastest CAGR, supported by seasonal demand, tourism growth, and need for short-term capacity expansion

Regional Insights

The market shows strong growth across Europe, supported by aviation demand recovery, regulatory frameworks, and leasing hubs

- Ireland led the market with 41.1% share in 2025, acting as a global aircraft leasing hub due to its favorable tax regime and strong financial ecosystem

- The United Kingdom remains a key market driven by strong aviation finance capabilities and legal infrastructure

- Germany is a significant contributor with strong airline demand and industrial base supporting leasing activities

- France is witnessing steady growth due to Airbus ecosystem support and strong airline presence

Competitive Landscape

The Europe aircraft leasing market is highly competitive, with major global lessors and regional players competing based on portfolio quality, financial strength, and sustainability focus. Prominent players in the Europe aircraft leasing market include, AerCap Holdings N.V., Avolon Holdings Limited, SMBC Aviation Capital, BOC Aviation Limited, Air Lease Corporation, CDB Aviation, Dubai Aerospace Enterprise, BBAM, Jackson Square Aviation, ALAFCO, Aviation Capital Group, Macquarie AirFinance, Nordic Aviation Capital, TrueNoord, and ORIX Aviation.

Europe Aircraft Leasing Market Size

The Europe aircraft leasing market size was valued at USD 56.93 billion in 2025 and is anticipated to reach USD 61.16 billion in 2026 from USD 108.50 billion by 2034, growing at a CAGR of 7.43% during the forecast period from 2026 to 2034.

Aircraft leasing constitutes a pivotal segment within the global aviation finance ecosystem characterized by the temporary transfer of aircraft usage rights from lessors to airlines in exchange for periodic payments. This financial mechanism allows carriers to optimize capital expenditure while maintaining fleet flexibility amidst fluctuating demand patterns. The region serves as a critical hub for international lessors due to its robust legal frameworks and strategic geographic position connecting East and West. According to Eurostat data the European Union recorded approximately 415 billion air passenger kilometers in 2023. This substantial traffic volume necessitates a dynamic fleet management strategy where leasing plays an indispensable role. As per the International Air Transport Association European airlines operated a fleet of nearly 5,800 aircraft in early 2024. The regulatory environment under the European Aviation Safety Agency ensures stringent safety standards thereby influencing lease structuring and asset valuation. Furthermore the presence of major leasing entities in Ireland and the United Kingdom facilitates efficient cross border transactions. The market dynamics are increasingly shaped by sustainability mandates prompting lessors to prioritize fuel efficient models. This transition aligns with the broader European Green Deal objectives and according to the European Commission the Fit for 55 package aims to reduce aviation emissions by 55% by 2030 compared to 1990 levels. Such regulatory pressures redefine asset lifecycles and residual value projections within the leasing portfolio.

MARKET DRIVERS

Surging Passenger Traffic Volumes Drive Fleet Expansion Requirements

The relentless growth in passenger traffic across European corridors is propelling the expansion of the European aircraft leasing market. As per data from Eurocontrol the number of flight movements in Europe reached 10.2 million in 2023. This resurgence in operational frequency demands immediate access to narrow body aircraft which dominate short haul routes within the continent. Airlines prefer leasing solutions to rapidly scale their fleets in response to seasonal peaks and emerging route opportunities thereby avoiding the long lead times associated with new manufacturing orders. According to the International Air Transport Association European carriers experienced a 15% year on year increase in passenger demand during the first half of 2024. This heightened utilization rate accelerates wear and tear on existing assets prompting carriers to refresh their fleets through sale and leaseback transactions. Such arrangements allow airlines to unlock capital tied up in older aircraft while securing newer more efficient models through lease agreements. The flexibility offered by operating leases enables carriers to adjust their capacity in line with volatile demand patterns ensuring optimal load factors and revenue generation. Consequently lessors benefit from sustained demand for modern aircraft types particularly those offering superior fuel efficiency and lower maintenance costs which are increasingly preferred by European operators seeking to enhance operational resilience and profitability in a competitive landscape.

Stringent Environmental Regulations Accelerate Fleet Modernization via Leasing

Rigorous environmental mandates imposed by European authorities are further boosting the expansion of the European aircraft leasing market. The European Union’s Fit for 55 package aims to reduce net greenhouse gas emissions by at least 55% by 2030 and places immense pressure on aviation stakeholders to decarbonize operations. According to the European Environment Agency aviation accounted for approximately 4% of total EU carbon dioxide emissions in 2022. Leasing provides a viable pathway for carriers to replace older less efficient aircraft with next generation models that offer substantial fuel savings and reduced carbon footprints. For instance as per Airbus technical specifications the Airbus A320neo family delivers a 15% reduction in fuel consumption compared to previous generations. Lessors are increasingly curating portfolios rich in such sustainable assets catering to airlines’ urgent need to align with corporate sustainability goals and regulatory compliance. The International Civil Aviation Organization’s Carbon Offsetting and Reduction Scheme for International Aviation further incentivizes the adoption of cleaner technologies making leased modern aircraft an attractive option for cost conscious operators. By leveraging lease structures airlines can mitigate the financial risk associated with rapid technological obsolescence ensuring their fleets remain compliant with future environmental standards. This regulatory driven demand fosters a vibrant leasing market where asset value is closely linked to environmental performance encouraging continuous investment in green aviation technologies and supporting the region’s broader climate action agenda.

MARKET RESTRAINTS

Volatility in Interest Rates Elevates Financing Costs for Lessors

Fluctuating interest rates are hampering the expansion of the European aircraft leasing market, which is directly impacting the cost of capital for lessors and subsequently influencing lease rates charged to airlines. As the European Central Bank adjusted its monetary policy to combat inflation benchmark interest rates reached 4.5% by late 2023 as reported by official bank publications. This tightening of monetary conditions raises the borrowing costs for leasing companies which typically rely on debt financing to acquire aircraft assets. Higher interest expenses erode profit margins and force lessors to pass these costs onto airlines through elevated lease rentals potentially dampening demand for new lease agreements. According to the International Lease Finance Corporation, the cost of funding for aircraft assets increased by approximately 200 basis points between 2022 and 2024. Airlines already grappling with post pandemic recovery challenges may find higher lease rates prohibitive leading them to extend the service life of existing aircraft rather than pursuing new leases. This delay in fleet renewal disrupts the natural cycle of asset rotation resulting in an oversupply of older less desirable aircraft in the secondary market. Furthermore uncertainty regarding future rate trajectories complicates long term financial planning for both lessors and lessees causing hesitation in committing to multi year lease contracts. The interplay between rising financing costs and cautious airline spending creates a constrained environment where transaction volumes may stagnate limiting market growth and forcing participants to seek alternative hedging strategies or equity based funding solutions to mitigate exposure to interest rate volatility.

Supply Chain Disruptions Delay Aircraft Deliveries and Limit Inventory

Persistent supply chain bottlenecks severely constrain the availability of new aircraft thereby restricting the inventory pool for lessors and impeding their ability to meet airline demand in the Europe aircraft leasing market. Original equipment manufacturers face prolonged delays in delivering new planes due to shortages of critical components labor constraints and production inefficiencies. According to Boeing the company delivered 528 commercial airplanes in 2023 while still navigating production constraints. Airbus similarly reported challenges in ramping up production rates with target outputs for the A320 family falling short of initial projections due to supplier issues. These delays limit the flow of fresh assets into the leasing market forcing lessors to compete for a limited number of available aircraft and driving up acquisition costs. Airlines seeking to expand or modernize their fleets encounter longer wait times which may compel them to retain older less efficient aircraft for extended periods. As per the International Air Transport Association the average age of the global commercial fleet increased to 11.5 years in 2023. In Europe this trend exacerbates maintenance costs and operational inefficiencies for carriers while reducing the attractiveness of leasing as a swift solution for capacity enhancement. The scarcity of new deliveries also affects residual value predictions because older aircraft remain in service longer than anticipated which potentially depresses their market worth. Lessors must navigate this constrained supply environment by optimizing existing portfolios and exploring alternative sourcing strategies yet the fundamental imbalance between demand and available inventory remains a significant hurdle to market expansion and operational fluidity.

MARKET OPPORTUNITIES

Integration of Sustainable Aviation Fuels Creates New Lease Structuring Opportunities

The emerging emphasis on sustainable aviation fuels is a lucrative opportunity for the European aircraft leasing market. As the European Union mandates increasing blends of sustainable fuels under the ReFuelEU Aviation initiative airlines require flexible financial instruments to manage the higher operational costs associated with these alternatives. Lessors can develop specialized lease products that incorporate sustainability linked incentives such as reduced rental rates for airlines achieving specific fuel efficiency or emission reduction milestones. According to the International Air Transport Association global sustainable aviation fuel production reached over 600 million liters in 2023. This growing availability enables lessors to partner with airlines in securing long term fuel supply agreements thereby enhancing the overall value proposition of lease contracts. By integrating environmental social and governance criteria into leasing terms lessors can attract environmentally conscious investors and differentiate their offerings in a competitive market. The European Investment Bank has committed billions in funding for green aviation projects providing lessors with access to favorable financing options for sustainable assets. This alignment with regulatory and investor expectations fosters a collaborative ecosystem where lessors act as enablers of the energy transition. Furthermore the development of hybrid electric and hydrogen powered aircraft prototypes offers future prospects for niche leasing segments allowing early movers to establish expertise in emerging technologies. Such strategic positioning not only mitigates regulatory risks but also unlocks new revenue streams through innovative financial solutions tailored to the evolving sustainability landscape of European aviation.

Expansion of Digital Platforms Enhances Asset Management and Transaction Efficiency

The adoption of advanced digital technologies offers significant opportunities for the Europe aircraft leasing market. Digital platforms enable real time monitoring of aircraft performance maintenance schedules and lease compliance reducing administrative burdens and minimizing downtime. According to a study by Deloitte digital transformation in aviation can reduce operational costs by up to 20% through improved data analytics and predictive maintenance capabilities. Lessors leveraging blockchain technology can ensure transparent and secure record keeping for lease agreements title transfers and maintenance histories thereby accelerating transaction timelines and reducing disputes. The European Union’s digital single market strategy encourages the integration of such technologies fostering a conducive environment for innovation in aviation finance. Artificial intelligence tools assist lessors in assessing credit risks predicting residual values and optimizing portfolio allocations leading to more informed decision making and enhanced profitability. As per McKinsey insights airlines and lessors utilizing AI driven analytics have reported a 15% improvement in asset utilization rates. Furthermore digital marketplaces facilitate quicker matching of available aircraft with airline requirements expanding the reach of lessors beyond traditional networks. This technological evolution supports the development of smart contracts that automate lease payments and compliance checks reducing manual intervention and error rates. By embracing digitalization lessors can offer more agile and responsive services meeting the dynamic needs of European airlines while positioning themselves as forward thinking partners in the digital aviation ecosystem.

MARKET CHALLENGES

Geopolitical Instability Disrupts Cross Border Lease Operations and Asset Recovery

Geopolitical tensions is a significant challenge to the Europe aircraft leasing market by disrupting cross border operations and complicating asset recovery processes in conflict affected regions. The ongoing instability in Eastern Europe and other volatile areas has led to the seizure or detention of leased aircraft resulting in substantial financial losses for lessors. According to the International Air Transport Association over 400 aircraft were stranded in Russia following the imposition of sanctions in 2022. These incidents underscore the risks of political interference in contractual obligations forcing lessors to reassess their exposure to high risk jurisdictions. The complexity of legal frameworks across different countries further hinders efforts to reclaim assets leading to prolonged disputes and increased insurance premiums. As per Lloyd’s List Intelligence, insurance costs for aircraft operating in politically unstable regions have risen by 30% since 2022. Lessors must navigate intricate sanction regimes and diplomatic negotiations to protect their interests often requiring specialized legal expertise and resources. This uncertainty discourages investment in certain markets and limits the geographic diversification of leasing portfolios. Furthermore the reputational damage associated with asset losses can affect investor confidence and credit ratings impacting the overall financial stability of leasing firms. To mitigate these risks lessors are increasingly incorporating robust political risk insurance and diversifying their geographic footprint yet the inherent unpredictability of geopolitical events remains a persistent challenge that requires constant vigilance and adaptive risk management strategies in the European context.

Shortage of Skilled Technical Personnel Impacts Maintenance and Asset Value Preservation

A critical shortage of skilled aviation technicians and engineers is further challenging the expansion of the Europe aircraft leasing market, which is affecting maintenance quality and asset value preservation. As airlines expand operations post pandemic the demand for qualified maintenance personnel has outpaced supply leading to delays in routine checks and repairs. According to Boeing the global aviation industry will require approximately 716,000 new maintenance technicians over the next 20 years. This labor shortfall results in extended aircraft on ground times reducing utilization rates and increasing operational costs for lessees. Lessors bear the indirect consequences through diminished asset reliability and potential depreciation in residual values due to inconsistent maintenance standards. The European Aviation Safety Agency has emphasized the importance of rigorous training and certification programs to address this skills deficit yet the pipeline of new entrants remains insufficient to meet current needs. As per data from Eurostat vocational training participation in the European Union was approximately 46% for upper secondary students in 2022. Lessors must collaborate with airlines and training institutions to support workforce development initiatives ensuring that leased assets receive timely and compliant maintenance. Failure to address this human capital challenge could lead to increased safety incidents and regulatory penalties undermining the integrity of the leasing ecosystem. Consequently the industry faces pressure to invest in automated maintenance solutions and upskilling programs to mitigate the impact of labor shortages on asset performance and long term value retention.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.43% |

| Segments Covered | By Aircraft Type, Lease Type and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Key Market Players | AerCap Holdings N.V., Avolon Holdings Limited, SMBC Aviation Capital, BOC Aviation Limited, Air Lease Corporation, CDB Aviation, Dubai Aerospace Enterprise (DAE Capital), BBAM, Jackson Square Aviation, ALAFCO Aviation Lease and Finance Company, Aviation Capital Group, Macquarie AirFinance, Nordic Aviation Capital, TrueNoord, and ORIX Aviation. |

SEGMENTAL ANALYSIS

By Aircraft Type Insights

The narrow body aircraft segment dominated the market by holding 61.2% of the regional market share in 2025. The dominance of narrow body aircraft segment in the European market is attributed to the dense network of short haul routes that characterize European aviation where high frequency and operational flexibility are paramount. According to Eurocontrol data, short haul flights constitute over 70% of all air traffic movements within the European region. These aircraft types offer optimal seat capacity for intra-European travel balancing passenger demand with operational efficiency. As per the International Air Transport Association, narrow body aircraft deliver superior cost per seat mile metrics on routes under 1,500 kilometers. Lessors favor this segment due to higher asset liquidity and broader lessee appeal to ensure consistent lease rates and lower vacancy risks. Furthermore the rapid recovery of leisure travel post pandemic has disproportionately benefited short haul carriers driving immediate demand for leased narrow body units to capture seasonal spikes. The standardization of maintenance procedures and pilot training for these fleets further reduces operational complexities for airlines making leasing an attractive option for capacity expansion. Consequently the entrenched preference for single aisle operations in Europe solidifies the narrow body segment’s leading position supported by sustained order books from manufacturers and strong secondary market values that enhance lessor confidence in long term asset performance.

On the other side, the wide body aircraft segment is anticipated to grow at a CAGR of 9.4% over the forecast period in the European market owing to the resurgence of long haul international travel and the expansion of intercontinental networks. As per the International Air Transport Association, long haul passenger traffic in Europe was expected to grow significantly as part of the broader 12% global passenger growth predicted through 2026. This growth is fueled by increasing connectivity between Europe and emerging markets in Asia, the Middle East, and Latin America, where demand for premium travel experiences is rising. Wide body aircraft, such as the Boeing 787 and Airbus A350, offer superior range and passenger comfort, making them ideal for these lucrative long distance routes. Lessors are increasingly investing in these assets to cater to flagship carriers seeking to enhance their global presence and compete on service quality. The European Commission’s open skies agreements with various international partners have further facilitated route expansion, creating new opportunities for wide body deployments. Additionally, the cargo capacity of wide body aircraft provides an additional revenue stream, enhancing their economic viability for lessors and airlines alike. According to Boeing, the demand for wide body freighters globally will increase significantly, and European carriers will account for a portion of the 20% total freighter fleet growth. This multifaceted demand profile, combined with the strategic importance of long haul connectivity, positions the wide body segment as the fastest growing category in the European leasing market, attracting significant capital inflows and portfolio diversification efforts.

By Lease Type Insights

The dry lease segment accounted for the major share of the European aircraft leasing market in 2025 due to the greater operational control and cost efficiency it offers to airlines, allowing them to manage crew, maintenance, and insurance independently. As per the International Lease Finance Corporation, dry leases provide airlines with the flexibility to integrate leased aircraft into their existing operational frameworks without the constraints of external service providers. This autonomy enables carriers to optimize scheduling, branding, and customer service standards, which are critical for maintaining competitive advantage in the European market. The lower overall cost structure of dry leases, compared to wet or damp arrangements, makes them particularly attractive for long term fleet planning and capacity expansion. Airlines prefer this model for core routes where they have established infrastructure and personnel, ensuring seamless integration and maximum asset utilization. According to Eurocontrol, the majority of scheduled flights in Europe are operated by carriers with in house maintenance and crew capabilities. Lessors benefit from this arrangement through stable long term contracts with creditworthy airlines, reducing administrative burdens and enhancing portfolio predictability. The widespread adoption of dry leases reflects the mature nature of the European aviation industry, where carriers possess the resources and expertise to manage complex operational requirements internally, thereby solidifying this segment’s leadership in the leasing landscape.

However, the wet lease segment is experiencing the fastest growth and is expected to exhibit a CAGR of 10.2% during the forecast period in the Europe aircraft leasing market owing to the increasing demand for seasonal and charter operations. As per the European Travel Commission, summer tourist arrivals in Europe were expected to surpass pre pandemic levels in 2024. Wet leases provide an immediate solution for airlines and tour operators needing to scale up operations without the long term commitment of acquiring assets or hiring additional crew. This model includes aircraft, crew, maintenance, and insurance, and offers a turnkey solution that minimizes operational complexity for lessees. The International Air Transport Association notes that charter flights account for a significant portion of summer traffic in Southern Europe. Lessors specializing in wet leases benefit from higher daily rates and short term contracts, which offer attractive yields despite higher operational involvement. The flexibility of wet leases allows carriers to respond swiftly to market fluctuations, ensuring optimal load factors during high season periods. According to Eurostat, tourism related air traffic in Spain and Greece increased by approximately 15% year on year. This dynamic environment supports the rapid expansion of the wet lease segment, as it addresses the immediate and transient needs of the vibrant European tourism industry.

REGIONAL ANALYSIS

Ireland Aircraft Leasing Market Analysis

Ireland dominated the market by holding 41.1% of the European market share in 2025. Ireland stands as the undisputed global and European hub for aircraft leasing due to a favorable tax regime, specifically the Section 110 special purpose vehicle structure, which has attracted major lessors, such as AerCap and Avolon, to establish their headquarters in Dublin. As per the Irish Aviation Authority, Ireland manages thousands of aircraft valued at hundreds of billions of dollars. The presence of a skilled workforce, specializing in aviation finance, law, and engineering, further reinforces its competitive advantage. The International Air Transport Association recognizes Ireland as the primary jurisdiction for cross border aircraft transactions, facilitating efficient capital flow and asset management. The Irish government’s continued support, through regulatory stability and industry partnerships, ensures that the sector remains resilient amidst global economic shifts. According to the Department of Transport in Ireland, the aviation leasing industry contributes substantially to the national economy, supporting thousands of jobs. This ecosystem enables lessors to offer competitive rates and innovative financial products, attracting airlines from across Europe and beyond. The concentration of legal and technical expertise in Dublin creates a cluster effect that enhances operational efficiency and risk mitigation for leasing companies. Consequently, Ireland’s entrenched position as the premier leasing jurisdiction drives its substantial market share, underpinned by a robust infrastructure that supports the complex needs of the global aviation finance industry.

United Kingdom Aircraft Leasing Market Analysis

The United Kingdom holds a prominent position in the Europe aircraft leasing market and is driven by its historical strength in aviation finance and legal expertise. London serves as a key center for aircraft leasing transactions, leveraging its deep capital markets and sophisticated legal framework based on English law, which is widely preferred for international lease agreements. As per the UK Civil Aviation Authority, the country supports a vast network of lessors and financiers who facilitate billions of dollars in aircraft deals annually. The presence of major global banks and insurance companies in London provides ample funding opportunities for leasing companies, enhancing their capacity to acquire and manage large fleets. The International Air Transport Association highlights the UK’s role in setting industry standards and best practices, influencing global leasing norms. Post Brexit adjustments have introduced some regulatory complexities, yet the sector has demonstrated resilience by adapting to new trade dynamics and maintaining strong international relationships. According to the Aerospace Technology Institute, the UK aviation sector continues to innovate in sustainable finance, attracting green investment for eco friendly leasing portfolios. The country’s robust legal system ensures enforceability of contracts and protection of asset rights, which is critical for lessors operating in multiple jurisdictions. Furthermore, the UK’s strategic geographic position and connectivity make it a vital node for European aviation operations. This combination of financial depth, legal certainty, and strategic importance sustains the UK’s significant market share, positioning it as a critical pillar in the European aircraft leasing landscape.

Germany Aircraft Leasing Market Analysis

Germany is expected to account for a prominent share of the European aircraft leasing market during the forecast period owing to its strong industrial base and the presence of major airlines that actively engage in sale and leaseback transactions. The country’s robust economy supports a high volume of air traffic, creating sustained demand for leased aircraft to maintain fleet flexibility and optimize capital structure. As per the German Federal Ministry for Digital and Transport, the aviation sector is a key component of the national infrastructure, with major carriers like Lufthansa utilizing leasing to manage fleet modernization and expansion. The presence of leading manufacturing facilities for Airbus components in Germany fosters close ties between lessors, manufacturers, and airlines, facilitating efficient asset delivery and maintenance. The International Air Transport Association notes that German airlines are among the most active participants in the European leasing market, prioritizing fuel efficient models to align with stringent environmental regulations. The country’s strong credit rating and stable financial environment attract international lessors seeking reliable counterparties. According to the German Aviation Industry Association, the sector is increasingly focusing on sustainable aviation fuels and digitalization. Germany’s central location in Europe also makes it a logistical hub for aircraft maintenance and repair operations, enhancing the value proposition for lessors. This integration of industrial capability, financial stability, and regulatory compliance supports Germany’s substantial market presence, ensuring its continued relevance in the evolving European leasing landscape.

France Aircraft Leasing Market Analysis

France is predicted to showcase a healthy CAGR in the European aircraft leasing market over the forecast period due to the presence of Airbus and a strong domestic airline sector. The proximity to Airbus headquarters in Toulouse facilitates closer collaboration between lessors, manufacturers, and airlines, enabling quicker access to new aircraft models and customized leasing solutions. As per the French Civil Aviation Authority, the country’s strategic focus on aerospace innovation supports a vibrant ecosystem for aviation finance and leasing activities. Major French airlines, including Air France KLM, actively utilize leasing to manage fleet composition and respond to market demands, contributing to steady transaction volumes. The International Air Transport Association highlights France’s commitment to sustainable aviation, with government incentives promoting the adoption of fuel efficient aircraft through leasing arrangements. The country’s robust legal framework and experienced financial institutions provide a secure environment for leasing transactions, attracting international investors. According to the French Ministry of Economy, the aerospace sector is a key driver of economic growth, with leasing playing a crucial role in maintaining competitiveness. France’s emphasis on research and development in aviation technologies also creates opportunities for lessors to invest in next generation assets. This synergy between manufacturing prowess, regulatory support, and airline demand sustains France’s significant market share, positioning it as a key player in the European aircraft leasing industry.

COMPETITIVE LANDSCAPE

The competition in the Europe aircraft leasing market is characterized by intense rivalry among established global giants and specialized regional players who vie for dominance through asset quality and financial strength. Major lessors differentiate themselves by offering comprehensive solutions that extend beyond simple financing to include technical support and fleet advisory services. The market exhibits high barriers to entry due to significant capital requirements and complex regulatory compliance needs which protect incumbent positions. Competitive dynamics are heavily influenced by the ability to secure favorable financing terms and maintain strong relationships with original equipment manufacturers for timely aircraft deliveries. Companies strive to optimize their portfolios by balancing mature assets with new generation models to manage risk and maximize returns. The emphasis on sustainability has become a key differentiator with lessors competing to offer green leasing products and support airline decarbonization goals. Digital capabilities also play a crucial role in enhancing operational efficiency and customer experience giving technologically advanced firms a competitive edge. Geopolitical factors and economic volatility add layers of complexity requiring agile risk management strategies. The consolidation trend continues as larger entities acquire smaller competitors to achieve scale and broaden their service offerings. This competitive landscape drives innovation and efficiency ultimately benefiting airlines through improved service quality and flexible leasing options in the European region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Aircraft Leasing Market include

- AerCap Holdings N.V.

- Avolon Holdings Limited

- SMBC Aviation Capital

- BOC Aviation Limited

- Air Lease Corporation

- CDB Aviation

- Dubai Aerospace Enterprise (DAE Capital)

- BBAM (B&B Air Acquisition)

- Jackson Square Aviation

- ALAFCO Aviation Lease and Finance Company

- Aviation Capital Group

- Macquarie AirFinance

- Nordic Aviation Capital

- TrueNoord

- ORIX Aviation

Top Players in the Europe Aircraft Leasing Market

AerCap Holdings N.V.

AerCap Holdings stands as a preeminent force in the global aviation leasing sector with its headquarters situated in Dublin Ireland. The company maintains an extensive portfolio comprising thousands of aircraft engines and helicopters serving clients worldwide. Its strategic acquisition of GE Capital Aviation Services significantly expanded its asset base and operational reach across European markets. AerCap focuses on optimizing fleet composition by investing in fuel efficient next generation aircraft that align with stringent environmental regulations. The company actively engages in sale and leaseback transactions to provide liquidity for airlines while securing long term revenue streams. Recent initiatives include partnerships with sustainable aviation fuel providers to support decarbonization efforts within the industry. AerCap leverages advanced data analytics to enhance asset management and predict maintenance needs effectively. This technological integration improves operational efficiency and reduces downtime for lessees. The firm continues to strengthen its market position through disciplined capital allocation and robust risk management practices. By maintaining strong relationships with original equipment manufacturers AerCap ensures timely access to new deliveries. This approach allows the company to meet evolving customer demands and maintain a competitive edge in the dynamic European leasing landscape.

Avolon Holdings Limited

Avolon Holdings operates as a leading global aircraft leasing company headquartered in Dublin Ireland with a significant presence in the European market. The company manages a modern and diverse fleet of aircraft leased to airlines across various continents. Avolon emphasizes sustainability by prioritizing investments in fuel efficient technologies and supporting the transition to greener aviation solutions. Its strategic partnerships with financial institutions enable flexible financing structures that cater to the unique needs of airline customers. Avolon recently expanded its portfolio through the acquisition of CIT Aerospace which enhanced its scale and diversified its asset mix. The company focuses on providing comprehensive leasing solutions including operating leases and structured finance products. Avolon leverages its technical expertise to offer value added services such as fleet planning and asset trading. This holistic approach strengthens client relationships and drives long term growth. The firm actively participates in industry forums to shape regulatory frameworks and promote best practices. By maintaining a strong balance sheet and accessing global capital markets Avolon ensures financial stability and resilience. Its commitment to innovation and customer centric strategies positions it as a key contributor to the evolution of the European aircraft leasing ecosystem.

BOC Aviation Limited

BOC Aviation Limited is a prominent aircraft leasing company based in Singapore with substantial operations and influence in the European market. The company specializes in acquiring and leasing new and used commercial jet aircraft to airlines globally. BOC Aviation focuses on building long term partnerships with carriers by offering tailored leasing solutions that enhance fleet flexibility. The company has consistently expanded its order book with leading manufacturers such as Airbus and Boeing to secure future deliveries. Recent actions include the placement of significant orders for narrow body aircraft to meet rising demand from European low cost carriers. BOC Aviation emphasizes rigorous asset management practices to maintain high utilization rates and preserve residual values. The company actively engages in sale and leaseback transactions to support airline liquidity and fleet modernization initiatives. Its strong financial profile enables access to competitive funding sources which supports continued growth and expansion. BOC Aviation also prioritizes environmental social and governance criteria by investing in sustainable aircraft technologies. The firm collaborates with industry stakeholders to promote responsible aviation practices and reduce carbon emissions. Through strategic investments and operational excellence BOC Aviation reinforces its position as a trusted partner in the European aircraft leasing market.

Top Strategies Used by Key Market Participants

Key players in the Europe aircraft leasing market predominantly employ portfolio modernization strategies to align with environmental regulations and enhance asset value. Companies actively invest in fuel efficient next generation aircraft such as the Airbus A320neo and Boeing 737 MAX families to meet airline demand for sustainable operations. Strategic mergers and acquisitions serve as another critical approach enabling firms to expand their asset base and achieve economies of scale. Lessors frequently engage in sale and leaseback transactions to provide airlines with immediate liquidity while securing long term leasing contracts. Diversification of funding sources through green bonds and sustainability linked loans helps companies reduce capital costs and attract environmentally conscious investors. Digital transformation initiatives are increasingly adopted to streamline asset management improve predictive maintenance and enhance transaction efficiency. Lessors also focus on geographic diversification to mitigate risks associated with regional economic fluctuations and geopolitical instability. Collaborative partnerships with original equipment manufacturers ensure priority access to new deliveries and favorable pricing terms. These multifaceted strategies enable market participants to maintain competitive advantages optimize operational performance and navigate the complex regulatory landscape of the European aviation sector effectively while ensuring long term profitability and resilience.

MARKET SEGMENTATION

This research report on the Europe Aircraft Leasing Market has been segmented and sub-segmented based on the following categories.

By Aircraft Type

- Narrow Body

- Wide Body

- Regional Aircraft

By Lease Type

- Wet Lease

- Dry Lease

- Damp Lease

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com