Europe Aircraft Survivability Equipment Market Size, Share, Trends, & Growth Forecast Report By Type (Electronic Warfare Systems, Countermeasure Systems, Survivability Software, Sensor Systems), End user, Platform, Application, Industry and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Aircraft Survivability Equipment Market Report Summary

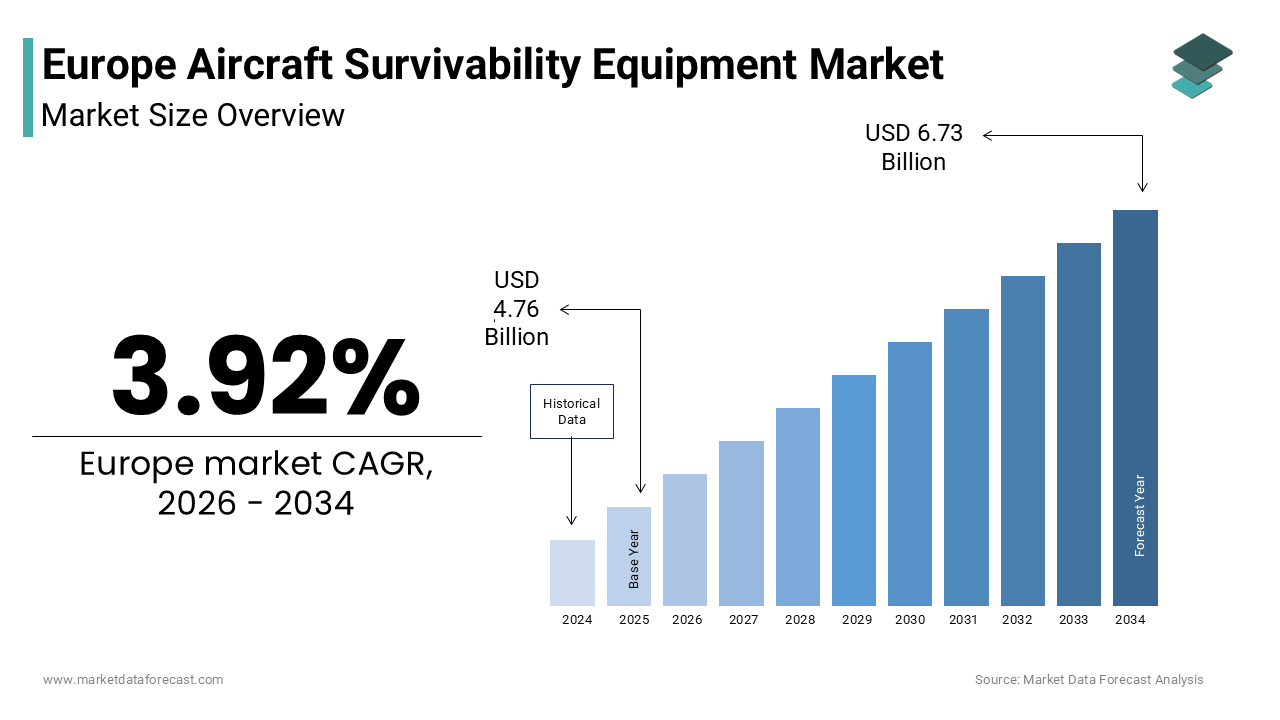

The Europe aircraft survivability equipment market was valued at USD 4.76 billion in 2025, is estimated to reach USD 4.95 billion in 2026, and is projected to reach USD 6.73 billion by 2034, growing at a CAGR of 3.92% during the forecast period from 2026 to 2034. The growth of the Europe aircraft survivability equipment market is driven by rising defense budgets, increasing modernization of legacy aircraft fleets, and the growing complexity of airborne threats such as radar-guided missiles and advanced air-defense systems. Aircraft survivability equipment (ASE) includes technologies like radar warning receivers, missile approach warning systems, electronic countermeasures, and flare/chaff dispensers that help aircraft detect and defeat hostile threats. These systems are primarily installed on military aircraft and UAVs to reduce vulnerability during combat missions. Increasing geopolitical tensions and the need to maintain air superiority are accelerating investments in electronic warfare and countermeasure technologies across Europe.

Key Market Trends

-

Rising deployment of advanced electronic warfare systems to counter sophisticated radar and missile threats.

-

Increasing adoption of AI-enabled cognitive electronic warfare solutions capable of identifying and reacting to threats autonomously.

-

Growing demand for directed energy countermeasures such as laser-based defense systems for aircraft protection.

-

Expansion of survivability technologies in unmanned aerial vehicles (UAVs) as drones become more common in modern warfare.

-

Increasing focus on software-defined survivability systems, allowing updates to threat libraries without hardware replacement.

Segmental Insights

- Based on type, the electronic warfare systems segment held the largest share of the Europe aircraft survivability equipment market in 2025. These systems are essential for detecting, identifying, and jamming hostile radar signals and missile guidance systems, making them a primary layer of defense for modern aircraft.

- The survivability software segment is projected to grow at the fastest rate during the forecast period. The growth is driven by the increasing adoption of open-architecture software platforms that allow continuous updates to counter evolving threats.

- Based on application, the military aircraft segment dominated the Europe aircraft survivability equipment market in 2025. The segment’s dominance is attributed to the growing need to protect fighter jets, transport aircraft, and reconnaissance platforms operating in high-threat environments.

- The unmanned aerial vehicles (UAVs) segment is expected to witness the fastest growth due to the increasing use of drones in surveillance, intelligence gathering, and combat missions.

Regional Insights

The Europe aircraft survivability equipment market is expanding steadily across major European countries due to modernization programs and increasing investments in defense technology.

-

United Kingdom accounted for 24.4% of the Europe aircraft survivability equipment market share in 2025, supported by strong aerospace manufacturing capabilities and modernization programs for fighter aircraft such as Typhoon and F-35 fleets.

-

France holds a major share due to its strong defense industry and the global export success of aircraft such as the Rafale fighter jet equipped with advanced defensive systems.

-

Germany is witnessing growing demand due to modernization initiatives for the Bundeswehr and upgrades to Tornado and Eurofighter aircraft fleets.

-

Italy plays a key role in helicopter survivability systems and defensive avionics used in rotary-wing aircraft.

-

Sweden contributes through advanced electronic warfare technologies integrated into platforms such as the Gripen fighter aircraft.

Competitive Landscape

The Europe aircraft survivability equipment market is highly competitive and dominated by major aerospace and defense companies that focus on advanced electronic warfare technologies, sensor systems, and countermeasure solutions. Companies compete through continuous research and development, strategic partnerships with governments, and participation in multinational defense programs. Increasing investments in artificial intelligence, software-defined avionics, and directed energy technologies are shaping the competitive landscape. Strict regulatory requirements and export controls also create high barriers to entry, limiting the number of companies capable of developing advanced survivability systems. Prominent players in the Europe aircraft survivability equipment market include BAE Systems, Thales Group, Saab AB, Chemring Group PLC, Terma A/S, RUAG AG, Leonardo S.p.A., Elbit Systems Ltd., Northrop Grumman Corporation, and Raytheon Technologies Corporation

Europe Aircraft Survivability Equipment Market Size

The Europe aircraft survivability equipment market size was valued at USD 4.76 billion in 2025 and is anticipated to reach USD 4.95 billion in 2026 from USD 6.73 billion by 2034, growing at a CAGR of 3.92% during the forecast period from 2026 to 2034.

Aircraft survivability equipment encompasses a critical array of defensive systems designed to protect military and specialized civilian aircraft from detection tracking and destruction by hostile threats. This sector includes radar warning receivers missile approach warners laser warning systems and active countermeasure dispensers that deploy chaff or flares to confuse incoming ordnance. The definition has expanded beyond passive protection to include integrated electronic warfare suites capable of jamming enemy sensors and executing cyber defences in real time. According to the European Defence Agency, defense spending among EU member states has reached record levels, which is reflecting an urgent prioritization of force protection capabilities amidst rising geopolitical tensions. As per the International Institute for Strategic Studies, Europe has a significant number of military aircraft requiring modernization, many of which lack contemporary survivability features against advanced surface to air missiles. The operational environment has become increasingly complex with the proliferation of man portable air defense systems and sophisticated radar networks necessitating upgrades to legacy fleets. As per NATO reports, the alliance has identified air superiority as a cornerstone of collective defense, driving substantial investment in next generation survivability technologies. This market is characterized by stringent certification requirements and a shift toward open architecture systems that allow for rapid software updates to counter evolving threat signatures. The integration of artificial intelligence into threat assessment algorithms further transforms these systems into autonomous guardians capable of making split second decisions to ensure mission success and pilot safety.

MARKET DRIVERS

Escalating Geopolitical Tensions and Modernization of Legacy Fleets

The resurgence of great power competition and increased security concerns across the European continent is one of the major factors propelling the expansion of the European aircraft survivability equipment market. Nations are urgently upgrading their aging fighter jets and transport aircraft to withstand modern threats posed by advanced integrated air defense systems and portable missiles. As per the Stockholm International Peace Research Institute, European arms imports have significantly increased in recent years, with a substantial portion allocated to defensive avionics and electronic warfare suites. The conflict in Eastern Europe has starkly demonstrated the vulnerability of unprotected aircraft, prompting governments to accelerate procurement cycles for radar warning receivers and directional infrared countermeasures. According to the European Defence Industrial Development Programme, a majority of funded projects in the aviation sector now focus on enhancing platform survivability through sensor fusion and automated countermeasures. Air forces across the region are extending the service life of fourth generation fighters, which requires installing state of the art protection systems to ensure they can operate safely in contested airspace alongside fifth generation platforms. The imperative to maintain air superiority and protect high value assets like airborne early warning and control aircraft drives sustained demand for comprehensive survivability packages. This strategic shift ensures that defense budgets remain robustly directed toward technologies that guarantee pilot survival and mission completion in high threat environments.

Proliferation of Advanced Threat Technologies and Asymmetric Warfare

The rapid spread of sophisticated anti-aircraft weaponry including dual mode seekers and networked radar systems forces a continuous evolution of defensive capabilities within the European aviation sector, which is further boosting the expansion of the European aircraft survivability equipment market. Adversaries are increasingly employing low observable missiles and infrared search and track systems that render traditional countermeasures ineffective, necessitating the development of multi spectral protection solutions. According to Jane's Defence Weekly, the global inventory of man portable air defense systems has grown in recent years, with many featuring improved resistance to standard flare decoys. This technological arms race compels European manufacturers to innovate rapidly by integrating laser based directed energy weapons and advanced digital radio frequency memory jammers into their product portfolios. As per the Royal United Services Institute, recent conflicts have shown a notable increase in the effectiveness of shoulder fired missiles against unprepared aircraft, underscoring the need for upgraded missile approach warners. The complexity of modern battlefields where threats emerge from multiple domains simultaneously requires survivability equipment capable of managing diverse attack vectors autonomously. Governments are mandating that new aircraft procurements include built in growth potential for future threat counters, ensuring long term relevance. The constant adaptation to asymmetric threats where non state actors possesses high end weaponry further amplifies the demand for ruggedized and highly reliable defensive systems across all aircraft categories.

MARKET RESTRAINTS

Stringent Export Controls and Regulatory Compliance Burdens

The rigorous framework governing the export of dual use technologies and classified defense articles is impeding the growth of the European aircraft survivability equipment market. Manufacturers face complex licensing procedures under the European Union Common Position on arms exports and national regulations, which can delay international sales and limit market access. As per the European Commission, obtaining export licenses for sensitive electronic warfare components often takes several months due to extensive end user verification and political assessments. According to the European Aerospace and Defence Industries Association, a considerable portion of potential contracts with non-EU partners were delayed or cancelled recently due to regulatory hurdles and shifting foreign policy stances. The fragmentation of export rules across different member states creates an inconsistent business environment where companies must navigate varying legal landscapes to sell identical products. Furthermore, strict adherence to International Traffic in Arms Regulations when collaborating with United States based partners adds another layer of bureaucratic complexity. The fear of technology leakage to unauthorized entities leads to overly cautious approval processes that stifle innovation and reduce competitiveness against global rivals with more streamlined export mechanisms. These administrative barriers increase operational costs and discourage smaller specialized firms from entering the global marketplace, thereby constraining overall market expansion.

High Development Costs and Extended Certification Timelines

The exorbitant financial investment required to research, develop and certify advanced survivability systems is further hampering the European aircraft survivability equipment market growth. Creating effective countermeasures against evolving threats demands cutting edge materials, sophisticated algorithms, and extensive testing in realistic combat scenarios, which strains the budgets of even large defense contractors. As per the European Defence Agency, the average cost of developing a new integrated defensive aids suite has risen significantly over the past decade due to the increasing complexity of sensor fusion and processing requirements. Industry financial reports indicate that certification processes involving flight trials and live fire tests can extend project timelines considerably, delaying revenue realization and return on investment. The need to comply with rigorous military standards such as DEF STAN and MIL SPEC ensures safety but adds significant overhead to production costs. Small and medium sized enterprises often struggle to secure the necessary capital to fund these lengthy development cycles, leading to market consolidation where only a few giants dominate. The risk of technical obsolescence before a system reaches full operational capability further deters investment in groundbreaking but unproven technologies. These economic and temporal constraints limit the pace of innovation and restrict the diversity of solutions available to armed forces across the region.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Cognitive Electronic Warfare

The incorporation of artificial intelligence and machine learning into survivability systems offers a promising opportunity in the European aircraft survivability equipment market. Cognitive electronic warfare capabilities enable platforms to learn from encountered signals, adapt their jamming strategies dynamically, and predict enemy actions without human intervention. As per the European Organisation for the Safety of Air Navigation, the adoption of AI driven decision support tools in aviation security is expected to grow significantly, with defense sectors leading the charge. According to the NATO Science and Technology Organization, cognitive systems can enhance reaction times compared to traditional rule-based algorithms. This technological leap allows for the management of spectrum congestion and the identification of novel threat signatures that pre-programmed systems might miss. Manufacturers who pioneer self-learning jamming pods and adaptive radar warning receivers will gain a decisive competitive advantage by offering superior protection in dense electromagnetic environments. The ability to update threat libraries over the air ensures that aircraft remain protected against emerging dangers throughout their operational lifespan. Furthermore, AI facilitates the fusion of data from multiple sensors to create a comprehensive situational awareness picture, enhancing pilot decision making. Embracing these intelligent technologies positions the market to address the escalating complexity of modern aerial warfare effectively.

Expansion of Directed Energy Countermeasure Systems

The development and deployment of directed energy weapons such as high energy lasers and high-power microwaves offer a lucrative opportunity in the European aircraft survivability equipment market. These systems provide an unlimited magazine depth, allowing aircraft to defend against saturation attacks involving multiple simultaneous missile threats without running out of defensive resources. As per the European Defence Fund, several collaborative projects are currently underway to mature laser technologies for airborne applications, with significant funding allocated to overcome size, weight, and power challenges. According to the Centre for European Policy Studies, directed energy countermeasures could reduce the logistical burden on air forces by eliminating the need to constantly reload physical decoys after every mission. The precision of laser beams enables the hard kill of incoming ordnance by damaging seeker heads or structural components, ensuring a higher probability of defeat than soft kill methods. Advances in solid state laser efficiency and thermal management are making these systems viable for installation on tactical fighters and helicopters. The strategic advantage of having a reusable and instantaneous defense mechanism appeals strongly to military planners seeking to enhance mission endurance. Capitalizing on this shift toward energy-based defences opens new revenue streams for companies specializing in photonics and power generation technologies.

MARKET CHALLENGES

Complexity of Integrating Legacy Platforms with Modern Systems

Integrating state of the art survivability equipment into older aircraft fleets is one of the significant challenges to the growth of the European aircraft survivability equipment market. Many legacy fighters and transport aircraft were designed decades ago without the necessary data buses, cooling systems, or electrical capacity to support advanced digital defensive suites. As per the European Aviation Safety Agency, retrofitting programs often encounter unforeseen engineering hurdles that require custom adapters and extensive rewiring, increasing both cost and risk. According to maintenance records of major European air forces, integration issues are a significant contributor to upgrade delays. The lack of standardized interfaces across different aircraft types forces manufacturers to develop bespoke solutions for each platform, reducing economies of scale and prolonging deployment schedules. Ensuring that new sensors do not interfere with existing avionics while maintaining aerodynamic integrity requires sophisticated modeling and simulation efforts. The scarcity of original equipment manufacturer support for obsolete platforms further complicates the process as technical documentation and spare parts become unavailable. Overcoming these integration barriers demands highly skilled engineering teams and innovative miniaturization techniques, which are in short supply. Until seamless interoperability is achieved, the full potential of modern survivability technologies will remain unrealized on a significant portion of the European fleet.

Shortage of Specialized Talent and Supply Chain Vulnerabilities

The acute scarcity of engineers with expertise in electronic warfare, radio frequency engineering, and embedded software development is further challenging the regional market expansion. The specialized nature of this field requires a deep understanding of physics, signal processing, and cybersecurity skills that are increasingly rare in the general labor pool. As per the European Centre for the Development of Vocational Training, the deficit of qualified personnel in the aerospace and defense sector has widened in recent years, hindering the pace of research and development. Industry surveys indicate that a majority of defense contractors report difficulties in recruiting staff capable of designing next generation countermeasure systems. This talent gap is exacerbated by supply chain vulnerabilities, where reliance on imported semiconductors and rare earth materials exposes production to geopolitical disruptions. The concentration of component manufacturing outside Europe creates risks of delays and quality inconsistencies that can halt assembly lines. Furthermore, the long lead times for specialized electronic components complicate project planning and increase the risk of cost overruns. Addressing these human capital and logistical constraints requires significant investment in education, partnerships, and the diversification of supply sources. Without resolving these foundational issues, the market faces bottlenecks that could impair its ability to meet urgent defense requirements.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.92% |

| Segments Covered | By Type, End user, Platform, Application, Industry and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe.

|

| Market Leaders Profiled | BAE Systems, Thales Group, Saab AB, Chemring Group PLC, Terma A/S, RUAG AG, Leonardo S.p.A., Elbit Systems Ltd., Northrop Grumman Corporation, and Raytheon Technologies Corporation. |

SEGMENTAL ANALYSIS

By Type Insights

The electronic warfare systems segment led the market by commanding for the largest share of the European aircraft survivability equipment market in 2025. The growth of the electronic warfare systems segment in the European market is attributed to its critical role as the first line of defense against radar guided threats in modern contested airspace and the escalating sophistication of enemy air defense networks that necessitate advanced jamming and deception capabilities to ensure mission success. According to the European Defence Agency, a significant portion of defense aviation budgets allocated for survivability upgrades in 2023 was directed toward electronic warfare suites to counter next generation radar technologies. As per the Royal United Services Institute, electronic attack capabilities are now considered mandatory for any aircraft operating within high threat environments, leading to widespread procurement across NATO member states. The ability of modern electronic warfare pods to perform simultaneous detection, identification, and jamming of multiple frequency bands provides a tactical advantage that passive countermeasures alone cannot offer. Furthermore, the shift toward networked electronic warfare allows multiple aircraft to share threat data, creating a collective defense shield that enhances overall fleet survivability. These strategic imperatives and the fundamental necessity of spectrum control solidify the leading position of electronic warfare systems in the regional market landscape.

The survivability software segment is projected to register the highest CAGR of 15.5% over the forecast period in this regional market owing to the urgent need to update threat libraries and adaptive algorithms without costly hardware replacements. As per the NATO Science and Technology Organization, the deployment of cognitive electronic warfare software has increased in European test programs since 2022 as forces seek to counter unpredictable threat behaviours. According to the European Defence Fund, significant funding is being channelled into developing open architecture software frameworks that allow for rapid over the air updates to counter emerging dangers instantly. The ability to simulate complex battle scenarios and train defensive algorithms virtually before deployment reduces development cycles and ensures higher effectiveness in actual combat. Additionally, the transition toward software defined radios and processors enables a single hardware platform to perform multiple roles simply by loading different software configurations, enhancing operational flexibility. The cost efficiency of upgrading software compared to replacing entire avionics suites makes this segment highly attractive to budget conscious military planners. The convergence of artificial intelligence and modular coding standards positions survivability software as the most rapidly expanding category in the market.

By Application Insights

The military aircraft segment held the dominant position in the Europe aircraft survivability equipment market by capturing the leading share of the regional market in 2025. The leading position of military aircraft segment in the European market is fueled by the existential requirement to protect state assets and personnel in high intensity conflict scenarios. According to the International Institute for Strategic Studies, Europe maintains a large inventory of military aircraft, many of which are undergoing extensive retrofitting to meet current threat standards. As per the Stockholm International Peace Research Institute, European military expenditure reached record levels in 2023, with a significant portion dedicated to avionic modernization programs for fighter jets, transport planes, and reconnaissance aircraft. The operational tempo of military missions in volatile regions necessitates robust and reliable defensive systems that can withstand saturation attacks and advanced guidance mechanisms. Furthermore, the integration of survivability equipment is often a prerequisite for international arms sales and interoperability within NATO alliances, driving consistent demand. The high value of military platforms and the catastrophic consequences of their loss justify the heavy investment in comprehensive protection suites. These factors collectively ensure that the military sector remains the largest consumer of survivability technologies.

The unmanned aerial vehicles segment is anticipated to witness the fastest CAGR of 17.1% over the forecast period. Factors such as the exponential increase in drone deployments for surveillance and strike missions in contested environments and the recognition that unmanned systems are increasingly targeted by enemy air defenses are propelling the expansion of the UAV segment in this regional market. As per the European Defence Industrial Development Programme, investments in drone survivability technologies have grown significantly in recent years as operators seek to protect high value intelligence gathering and combat UAVs from interception. According to the Joint Air Power Competence Centre, unprotected drones in simulated high threat scenarios face high loss rates, prompting an urgent shift toward integrating miniaturized radar warning receivers and countermeasure dispensers. The development of swarm tactics further amplifies the need for autonomous survivability software that can coordinate defensive maneuvers among multiple units without human intervention. Additionally, the use of drones in forward deployed roles exposes them to man portable air defense systems, necessitating advanced infrared countermeasures tailored for smaller platforms. The versatility of UAVs in performing dangerous missions traditionally assigned to manned aircraft drives the demand for specialized protection kits. The synergy between rising drone adoption rates and the critical need to preserve these assets propels this segment to the forefront of market growth.

By Platform Insights

The fixed wing aircraft segment held the major share of the European aircraft survivability equipment market in 2025 due to the extensive fleet of fighter jets, bombers, and transport planes that form the backbone of European air power. This dominance is driven by the high priority placed on protecting fast-moving and high-altitude platforms that are primary targets for long range surface to air missiles and interceptor aircraft. According to the European Air Group, a majority of survivability equipment contracts awarded in 2023 were designated for fixed wing platforms, reflecting their strategic importance in power projection and deterrence. As per Airbus Defence and Space, upgrade programs for existing fixed wing fleets include comprehensive installations of new radar warning receivers and electronic countermeasure pods to extend service life. The larger size and power generation capacity of fixed wing aircraft allow for the integration of more powerful and complex survivability systems compared to rotary wing counterparts. Furthermore, the requirement for long range strike capabilities necessitates robust protection against diverse threat vectors encountered deep inside enemy territory. These operational requirements and the sheer number of active fixed wing units secure the leading position of this platform segment.

The rotary wing aircraft segment is experiencing the most rapid expansion and is expected to exhibit a CAGR of 14.4% over the forecast period in this regional market owing to the intensifying focus on low altitude operations and urban combat scenarios where helicopters are highly vulnerable. As per the European Helicopter Safety Team, the incidence of shoulder fired missile threats against low flying aircraft has risen significantly, prompting military forces to mandate upgraded protection for all rotary assets. According to the European Defence Agency, procurement of specialized survivability kits for helicopters has increased in recent years as nations prepare for asymmetric warfare and peacekeeping missions. The unique flight profile of helicopters involving hovering and slow speed maneuvers makes them easy targets, requiring highly responsive and automated defensive systems. Additionally, the push to replace aging helicopter fleets with new models like the H145M and NH90 includes factory installed survivability packages as standard equipment. The critical role of rotary wing aircraft in special operations and medical evacuation further drives the demand for maximum protection levels. The combination of heightened threat exposure and fleet renewal initiatives positions rotary wing aircraft as the fastest growing platform category.

REGIONAL ANALYSIS

United Kingdom Aircraft Survivability Equipment Market Analysis

The United Kingdom dominated the aircraft survivability equipment market in Europe in 2025 by holding 24.4% of the regional market share. The dominance of the UK in the European market is attributed to its robust domestic aerospace industry and aggressive modernization programs. The nation serves as the primary hub for developing next generation electronic warfare suites, with major contractors delivering cutting edge solutions for global export. According to the UK Ministry of Defence, the Tempest future combat air programme allocates significant resources toward integrating cognitive electronic warfare and directed energy countermeasures, setting new standards for survivability. The Royal Air Force continuous upgrade of its Typhoon and F-35B fleets ensures sustained demand for advanced radar warning and jamming systems. As per the Society of British Aerospace Companies, defense electronics exports from the UK have grown in recent years, driven by international orders for British made survivability kits. The strong collaboration between government research labs and private industry fosters rapid innovation in threat simulation and countermeasure development. Furthermore, the UK commitment to NATO interoperability drives the adoption of standardized protective architectures across allied forces. The presence of world class testing facilities allows for rigorous validation of systems under realistic combat conditions. The combination of technological prowess, strategic foresight, and industrial capacity solidifies the UK position as the dominant force in the regional market.

France Aircraft Survivability Equipment Market Analysis

France occupied the second largest share of the European aircraft survivability equipment market in 2025. The promising position of France in the European market is attributed to its policy of strategic autonomy and strong export orientation in defense technologies. The country leverages its independent industrial base to produce comprehensive survivability suites that equip its own Rafale and Mirage fleets while attracting international buyers seeking non-aligned solutions. As per the French Directorate General of Armaments, investment in sovereign electronic warfare capabilities has increased to ensure immunity from foreign supply chain disruptions. According to the French Aerospace Industries Association, revenue from defense avionics exports has reached record highs, fueled by demand from Middle Eastern and Asian partners. The French approach emphasizes integrated mission systems where survivability equipment works seamlessly with sensors and weapons to maximize combat efficiency. Government support for research into quantum sensing and laser-based defences positions France at the forefront of future technologies. The emphasis on maintaining a full spectrum of capabilities from detection to hard kill ensures a diverse and resilient product portfolio. These strategic priorities ensure France remains a key growth engine for the European survivability market.

Germany Aircraft Survivability Equipment Market Analysis

Germany retains a prominent spot in the Europe aircraft survivability equipment market. The massive fleet modernization initiatives and commitment to strengthening European defense capabilities are driving the German market growth. The nation is undertaking one of the most extensive upgrade programs in its history to bring its Tornado and Eurofighter fleets up to date with current threat environments. According to the German Federal Ministry of Defence, the special fund for the Bundeswehr has allocated significant resources specifically for avionic improvements, including advanced self-protection systems. The German engineering sector excels in producing high precision sensor systems and electronic countermeasures that are integrated into both domestic and collaborative European projects. As per the German Aerospace Industries Association, contracts for survivability equipment have risen in recent years as part of the broader effort to achieve full operational readiness. The focus on developing common European standards for defensive aids promotes interoperability and reduces costs for partner nations. Furthermore, Germany’s active participation in the Future Combat Air System initiative drives innovation in networked survivability solutions. The strong regulatory framework ensures that all installed systems meet the highest safety and performance benchmarks. The synergy between substantial funding, industrial expertise, and collaborative spirit makes Germany a vital player in the market.

Italy Aircraft Survivability Equipment Market Analysis

Italy represents a key market in Southern Europe. The specialized expertise in protecting rotary wing platforms and naval aviation assets is contributing to the expansion of the Italian market. The Italian aerospace industry has developed renowned survivability solutions tailored for the unique challenges faced by helicopters operating in maritime and mountainous terrains. As per the Italian Ministry of Defence, the renewal of the AW101 and NH90 helicopter fleets includes the installation of state-of-the-art missile approach warners and flare dispensers. According to the Italian Aerospace Industries Association, exports of Italian made defensive systems for helicopters have increased in recent years due to their proven performance in harsh environments. The collaboration with other European nations on joint fighter programs ensures that Italian companies contribute advanced components to multinational platforms. The focus on lightweight and compact systems allows for effective protection without compromising the payload or range of smaller aircraft. Government incentives for research and development encourage the adoption of new materials and miniaturized electronics. Italy’s specific strengths in rotary wing technology ensure a distinct and valuable niche within the broader European landscape.

Sweden Aircraft Survivability Equipment Market Analysis

Sweden is anticipated to account for a notable share of the European aircraft survivability equipment market over the forecast period owing to its legacy of designing highly survivable aircraft like the Gripen and its pioneering work in stealth and electronic warfare technologies. The Swedish market is characterized by a strong emphasis on asymmetric defense strategies where superior situational awareness and electronic attack capabilities compensate for smaller fleet sizes. According to the Swedish Defence Materiel Administration, ongoing upgrades to the Gripen E/F series include some of the most advanced internal electronic warfare systems available globally. The country’s neutral stance historically drove the development of indigenous survivability technologies that are now highly sought after by export customers seeking independent capabilities. As per the Swedish Aerospace and Defence Industry, sales of Swedish made radar warning receivers and jamming pods have grown in recent years, driven by interest from non-NATO nations. The integration of passive sensors and low observable features into aircraft design reduces the reliance on active countermeasures, offering a layered defense approach. The close cooperation between the military and domestic industry facilitates rapid prototyping and fielding of new concepts. The reputation for building rugged and effective systems capable of operating in northern climates adds to their appeal. Sweden’s innovative approach to survivability ensures its continued relevance and influence in the European market.

COMPETITIVE LANDSCAPE

The competition in the Europe aircraft survivability equipment market is characterized by intense rivalry among established defense giants and specialized technology firms who vie for dominance through technological superiority and strategic alliances. Market leaders leverage their extensive experience and deep relationships with national governments to secure major contracts for flagship fighter and helicopter programs. The landscape is highly dynamic with companies constantly striving to integrate advanced artificial intelligence and machine learning capabilities into their defensive suites to counter evolving threats. Regulatory compliance regarding export controls and data security acts as a significant barrier to entry ensuring that only well capitalized entities with robust quality assurance systems can thrive. Price competition remains fierce particularly in retrofit programs where budget constraints force manufacturers to optimize costs while maintaining performance standards. Strategic acquisitions and joint ventures are becoming increasingly common as firms seek to acquire niche technologies or expand their geographical reach rapidly. This competitive environment fosters rapid technological advancement and benefits end users through improved protection levels and innovative solutions across the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe aircraft survivability equipment market include

- BAE Systems

- Thales Grou

- Saab AB

- Chemring Group PLC

- Terma A/S

- RUAG AG

- Leonardo S.p.A.

- Elbit Systems Ltd.

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

Top Players in the Market

BAE Systems

BAE Systems stands as a preeminent global defense contractor delivering advanced electronic warfare and survivability solutions that protect aircraft across diverse operational theaters. The company contributes significantly to the worldwide market by providing integrated defensive aids suites for major fighter programs including the F 35 and Eurofighter Typhoon. Recently BAE Systems has strengthened its position by investing heavily in cognitive electronic warfare technologies that utilize artificial intelligence to adapt to emerging threats in real time. Their strategic focus involves developing next generation radar warning receivers and directed energy countermeasures to ensure air superiority in contested environments. The firm actively collaborates with European governments and NATO allies to enhance interoperability and standardize protective architectures. Continuous innovation in sensor fusion and automated threat response allows BAE Systems to maintain its leadership in safeguarding high value assets. This commitment to cutting edge research and robust manufacturing capabilities secures their role as a critical partner for modern air forces seeking comprehensive survivability.

Leonardo S.p.A.

Leonardo S.p.A. operates as a leading European aerospace and defense giant specializing in sophisticated self-protection systems and electronic countermeasures for rotary and fixed wing platforms. The company plays a vital role in the global market by supplying missile approach warners and laser warning systems that are renowned for their reliability and performance in harsh conditions. Recent actions to strengthen its market position include the launch of new compact defensive suites designed specifically for unmanned aerial vehicles and next generation helicopters. Leonardo has expanded its research facilities to accelerate the development of quantum sensing technologies and advanced jamming capabilities. Their focus on creating modular and scalable solutions allows customers to upgrade existing fleets with minimal downtime and cost. The firm prioritizes international partnerships to integrate its survivability equipment into multinational combat aircraft programs. By leveraging deep expertise in photonics and signal processing Leonardo ensures its products remain at the forefront of aerial defense. This strategic emphasis on innovation and customer tailored solutions solidifies their reputation as a top tier provider in the industry.

Thales Group

Thales Group serves as a powerhouse in the defense electronics sector offering comprehensive survivability portfolios that encompass radar detection identification and neutralization of hostile threats. The company contributes extensively to the global market by delivering state of the art electronic warfare pods and integrated mission systems for a wide array of military aircraft. To strengthen its market position Thales recently unveiled advanced software defined radio architectures that enable rapid reconfiguration against evolving enemy tactics. They have secured major contracts to equip future combat air systems with next generation countermeasure dispensers and cyber hardened communication links. The group actively invests in artificial intelligence driven decision support tools that enhance pilot situational awareness and reaction times during critical engagements. Thales focuses on fostering a resilient supply chain within Europe to ensure uninterrupted production of critical components. Their dedication to open system standards facilitates seamless integration with allied platforms and future upgrades. This holistic approach to defense innovation and strategic autonomy enables Thales to maintain its status as a key enabler of aircrew safety and mission success worldwide.

Top Strategies Used by Key Market Participants

Key players in the Europe aircraft survivability equipment market primarily focus on research and development investments to pioneer cognitive electronic warfare and artificial intelligence driven countermeasures. Manufacturers actively pursue strategic partnerships with government agencies and prime contractors to secure long term supply contracts for next generation combat aircraft programs. Companies are increasingly adopting modular open system architectures to allow for rapid software updates and hardware upgrades without extensive platform modifications. Another major strategy involves expanding production capacities and diversifying supply chains within Europe to mitigate geopolitical risks and ensure regulatory compliance. Firms also prioritize international collaborations to enhance interoperability among allied forces and access broader export markets. Additionally vendors are developing specialized solutions for unmanned aerial vehicles to address the growing demand for drone survivability in contested airspace. These combined approaches enable market participants to navigate complex regulatory environments and capture growth opportunities in a rapidly evolving defense landscape.

MARKET SEGMENTATION

This research report on the Europe aircraft survivability equipment market has been segmented and sub-segmented based on the following categories.

By Type

- Electronic Warfare Systems

- Countermeasure Systems

- Survivability Software

- Sensor Systems

By End Use

- Government

- Defense Contractors

By Platform

- Fixed-Wing Aircraft

- Rotary-Wing Aircraft

By Application

- Military Aircraft

- Commercial Aircraft

- Unmanned Aerial Vehicles

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com