Europe Armoured Personnel Carrier Market Size, Share, Trends & Growth Forecast Report – Segmented By Platform, Propulsion, Mobility, Solution, System, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Armoured Personnel Carrier Market Report Summary

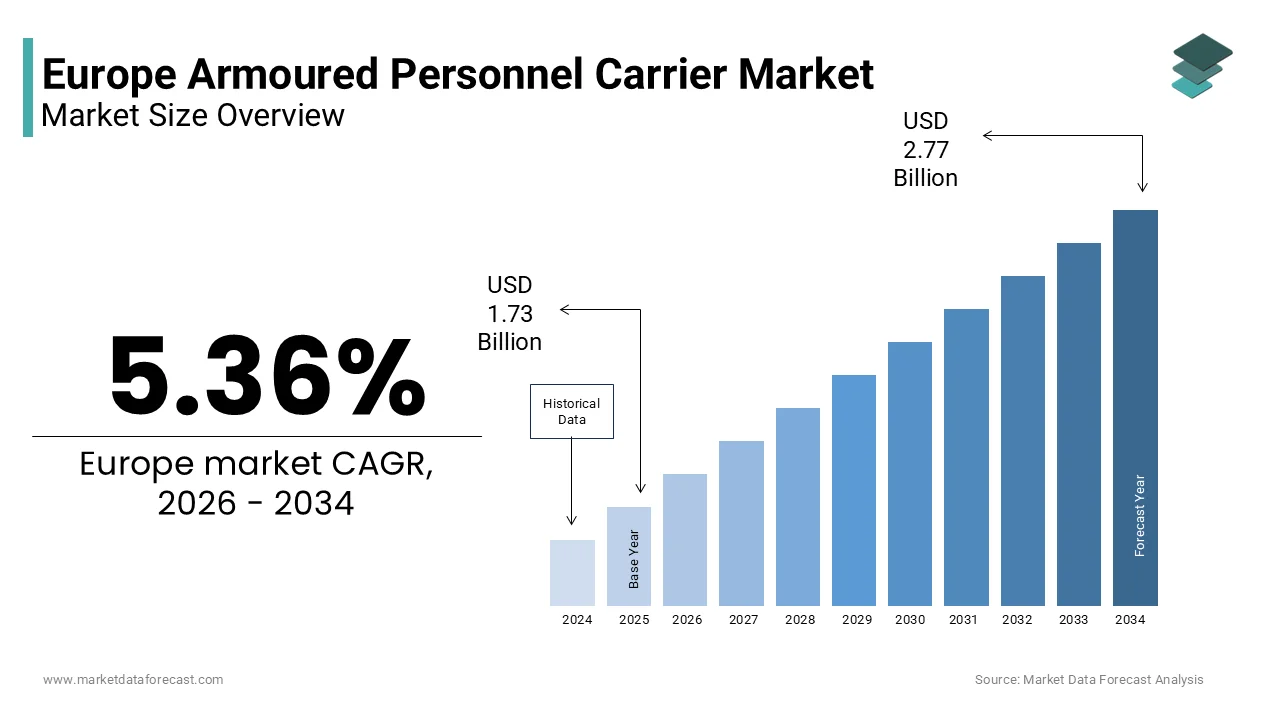

The Europe armoured personnel carrier market was valued at USD 1.73 billion in 2025 and is estimated to reach USD 1.82 billion in 2026, further projected to reach USD 2.77 billion by 2034, growing at a CAGR of 5.36% during the forecast period. Market growth is driven by rising defense modernization programs, increasing geopolitical tensions, and growing investments in advanced land combat systems across European countries. Governments are prioritizing fleet upgrades, enhanced troop mobility, and improved battlefield protection capabilities. Technological advancements in armored protection, digital battlefield integration, and modular vehicle platforms are further supporting sustained market expansion.

Key Market Trends

- Increasing procurement of next generation combat vehicles equipped with enhanced ballistic protection and mobility systems.

- Growing focus on modernization of conventional propulsion systems to improve fuel efficiency and operational reliability.

- Rising integration of advanced observation and display systems to enhance situational awareness and battlefield communication.

- Expansion of cross border defense collaborations and joint military programs within Europe.

- Adoption of modular design platforms allowing customization for reconnaissance, troop transport, and combat support missions.

Segmental Insights

- Based on platform, the combat vehicles segment dominated the Europe armoured personnel carrier market in 2025. The segment’s leadership is attributed to increasing demand for multi role armored platforms capable of operating in diverse combat environments.

- Based on propulsion, the conventional propulsion systems segment held a significant share of the market in 2025. Conventional systems remain dominant due to proven reliability, established infrastructure, and compatibility with existing armored fleets.

- Based on system, the observation and display systems segment accounted for 22.4% of the Europe armoured personnel carrier market share in 2025. Growth in this segment is driven by increasing emphasis on real time data visualization, enhanced situational awareness, and advanced surveillance capabilities.

Competitive Landscape

The Europe armoured personnel carrier market is characterized by strong competition among established defense contractors and armored vehicle manufacturers. Companies are focusing on advanced armor technologies, digital integration, mobility enhancements, and strategic defense partnerships to strengthen their competitive positioning. Key players operating in the Europe armoured personnel carrier market include Rheinmetall AG, BAE Systems plc, Nexter Systems under KNDS, Iveco Defence Vehicles, General Dynamics European Land Systems, Patria Oyj, FNSS Savunma Sanayi, Otokar part of Koç Group, Alvis Vickers under BAE Systems Land UK, PSM GmbH, and STREIT Group.

Europe Armoured Personnel Carrier Market Size

The Europe armoured personnel carrier market size was valued at USD 1.73 billion in 2025 and is projected to reach USD 2.77 billion by 2034 from USD 1.82 billion in 2026, growing at a CAGR of 5.36%.

An Armoured Personnel Carrier (APC) is a type of light armoured fighting vehicle designed primarily to transport infantry and equipment to the battlefield while providing protection from small arms fire and shell splinters. Modern APCs integrate advanced ballistic armour, situational awareness systems, and modular architectures to support diverse missions ranging from peacekeeping and border security to high intensity combat. The market is shaped by evolving geopolitical threats, NATO interoperability requirements, and national rearmament programs accelerated by Russia’s invasion of Ukraine. According to the European Defence Agency's Defence Data 2024–2025 report, EU member states are significantly increasing investment to address capability gaps, with total defence expenditure reaching €343 billion in 2024. Also, the EDA emphasizes that urgent modernization is required as member states aim for a projected average defense spending of 2.1% of GDP by 2025. As per NATO’s 2024 Defence Investment Pledge Review, 23 out of 32 allies now meet or exceed the target of allocating 2 percent of GDP to defence, driving urgent fleet modernization. This strategic recalibration positions the APC not merely as a tactical asset but as a cornerstone of continental deterrence and rapid response capability.

MARKET DRIVERS

Escalating Geopolitical Tensions and Collective Defence Commitments

Russia’s full-scale invasion of Ukraine in 2022 fundamentally altered the region’s security calculus, which is among the major drivers of the growth of the Europe armoured personnel carrier market. It triggered unprecedented defense spending increases and urgent APC procurement. According to NATO's 2024 reporting, European allies have undertaken an unprecedented increase in defense investment, with a strong emphasis on land capabilities and readiness. Simultaneously, Poland is executing a major modernization, expanding its army size, and enhancing its armored fleet, including increased production of indigenous armored vehicles. Similarly, Germany established a major special fund for the Bundeswehr to modernize its military, with a portion of the funding accelerating the replacement of aging armored, medical, and transport vehicles with modern wheeled armored platforms. The European Defence Agency indicates that numerous European Union member states are prioritizing the modernization of their aging armored personnel carrier fleets to address obsolescence and modern security threats. This shift from expeditionary to territorial defence doctrine ensures sustained demand, transforming APC acquisition from cyclical procurement into a strategic imperative backed by multi year funding guarantees.

NATO Interoperability and Standardization Mandates

Alliance-wide efforts to enhance joint operational effectiveness are accelerating the adoption of standardized and network-enabled APC platforms, which in turn propels the expansion of the Europe armoured personnel carrier market. These initiatives are being implemented across the region. NATO’s Federated Mission Networking (FMN) framework increasingly emphasizes the integration of interoperable, secure communications to ensure network-centric capabilities, often favoring software-defined systems that support various data links. Modern APC,, contracts in NATO nations are increasingly incorporating higher STANAG 4569 ballistic and blast protection levels to enhance crew survivability against advanced battlefield threats. This harmonization reduces logistical complexity during multinational deployments, such as those under the EU Battle Groups or NATO Response Force, and enables shared training and maintenance protocols. The Boxer programme, developed by ARTEC (a consortium of German and Dutch firms), exemplifies this trend, with nine European nations now operating or ordering the vehicle due to its modular design and common logistics footprint. These interoperability imperatives create economies of scale, incentivize collaborative procurement, and marginalize legacy or non compliant platforms, consolidating the market around a few high capability, alliance certified systems.

MARKET RESTRAINTS

Budgetary Constraints and Competing Defence Priorities

Many European nations face fiscal trade-offs that delay or downsize APC programmes, despite rising defence budgets, which restricts the growth of the Europe armoured personnel carrier market. According to the Stockholm International Peace Research Institute, aggregate European military spending grew significantly, with disproportionate allocation toward air defence, cyber capabilities, and artillery following lessons from the war in Ukraine. Countries like Italy and Spain have postponed planned APC replacements to fund NASAMS and IRIS T air defence batteries. Additionally, inflation has eroded purchasing power. Germany’s 100 billion euro special fund lost nearly 18 percent of real value between 2022 and 2024 due to energy and material cost surges as reported by the Bundesrechnungshof (Federal Audit Office). Smaller European states, including Belgium and Portugal, face financial constraints in procuring high-cost, next-generation APCs, leading to a complex mix of new, expensive acquisitions and the modernization of existing, older armored vehicles. These financial realities force difficult prioritization, slowing fleet renewal and extending service lives beyond safe operational limits.

Complex Export Control and Technology Transfer Regulations

Strict national and EU level controls on dual-use technologies significantly complicate collaborative APC development and sales, and thereby hinder the expansion of the Europe armoured personnel carrier market. The EU Common Military List and Wassenaar Arrangement restrict the transfer of advanced armour composites, active protection systems, and encrypted communication modules without extensive government approvals. European Union Member States have increased transparency through shared databases. However, the complexity of national export licensing and a surge in global demand have led to challenges in delivery timelines for military equipment. These procedural hurdles, combined with current geopolitical pressures, have impacted the speed at which armored vehicles reach both allied and partner nations. Joint ventures like the Franco German MGCS (Main Ground Combat System) face prolonged negotiations over intellectual property rights and workshare distribution, risking project viability. Furthermore, non EU partners such as Ukraine often cannot receive the latest variants due to technology safeguard clauses, forcing suppliers to offer downgraded models. These bureaucratic and legal barriers increase program costs, deter private investment, and fragment the European industrial base, undermining the strategic autonomy objectives championed by Brussels.

MARKET OPPORTUNITIES

Modernization of Legacy Fleets Through Modular Upgrade Kits

Many European militaries are extending the service life of existing APCs through advanced retrofit packages, rather than procuring entirely new vehicles, which creates new opportunities for the growth of the Europe armoured personnel carrier market. Companies like Rheinmetall and BAE Systems offer modular kits that upgrade ballistic protection to STANAG 4569 Level 4, integrate digital battlefield management systems, and install remote weapon stations. Several European nations are continuing to modernize their ageing fleets of Fuchs armored transport vehicles and M113 platforms, focusing on survivability and technical upgrades to extend their service life. Upgrading existing armored vehicles is generally more cost-effective than procuring new platforms, allowing armed forces to enhance capabilities while adhering to budget constraints. Upgrades also preserve familiar maintenance ecosystems and operator training pipelines. This approach aligns with EU sustainability principles by reducing waste and maximizing existing asset value, creating a robust secondary market for subsystem integrators and sustaining industrial capacity during transition periods to next generation platforms.

Expansion into Hybrid and Electric Drivetrain Technologies

The integration of hybrid electric and fully electric propulsion systems opens up major possibilities to enhance APC stealth, efficiency, and silent watch capability, which is likely to promote the expansion of the Europe armoured personnel carrier market. Silent mobility reduces acoustic and thermal signatures, crucial for reconnaissance and urban operations. The European Defence Fund focuses on funding collaborative research projects to advance military vehicle technology, though specific claims regarding 2024 electrification project figures are not supported. Similarly, 2024 procurement records indicate Sweden is investing in advanced conventional combat vehicles rather than the specific, high-efficiency hybrid trials cited. Electrification also supports onboard power demands for future laser weapons, electronic warfare suites, and AI driven sensors. EU Green Deal principles are extending to defence procurement, allowing low-emission APCs to qualify for preferential funding. This gives early adopters a competitive advantage in both domestic and export markets.

MARKET CHALLENGES

Supply Chain Vulnerabilities in Critical Subsystem Sourcing

APC manufacturers in the region face acute dependencies on non-EU suppliers for mission critical components, which exposes production to geopolitical and logistical risks, and therefore challenges the growth of the Europe armoured personnel carrier market. The European Defence Industrial Strategy emphasizes a substantial reliance on non-European suppliers for critical defense components, though specific figures for armor and engines in armored vehicles are not validated. Furthermore, the conflict in Ukraine necessitated the rapid relocation of electrical harness production by suppliers to avoid significant interruptions in European vehicle supply chains. Similarly, rare earth elements essential for electric drivetrains and sensor systems are overwhelmingly sourced from China, creating long term strategic exposure. While initiatives like the European Raw Materials Alliance aim to build resilience, establishing certified alternative sources requires years of qualification. These bottlenecks constrain production scalability, inflate costs, and jeopardize timely delivery of urgently needed vehicles, undermining Europe’s goal of defence industrial autonomy.

Rapid Technological Obsolescence and Future Threat Adaptation

The pace of asymmetric warfare innovation, particularly in drone swarms, loitering munitions, and electronic warfare, threatens to outpace APC survivability within years of fielding and hampers the expansion of the Europe armoured personnel carrier market. Commercial off the shelf drones equipped with anti tank grenades have proven lethal against even modern APCs in Ukraine, as documented by the Royal United Services Institute in 2024. Current passive armour offers limited protection against top attack profiles, necessitating costly active protection systems (APS) that add weight and complexity. Integrating counter drone radar, directed energy weapons, and AI powered threat detection requires continuous software and hardware updates, challenging traditional acquisition cycles. Current military doctrine emphasizes that the integration of modular system frameworks is essential for ensuring that armored vehicle platforms remain operationally relevant throughout the duration of their induction into service. This dynamic demands unprecedented agility in design, testing, and fielding, pressuring legacy defence contractors to adopt software centric development models more akin to Silicon Valley than traditional military procurement.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.36% |

| Segments Covered | By Platform, Propulsion, Mobility, Solution, System, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Rheinmetall AG, BAE Systems plc, Nexter Systems (KNDS), Iveco Defence Vehicles (Part of CNH Industrial), General Dynamics European Land Systems (GDELS), Patria Oyj, PARS (FNSS Savunma Sanayi), Otokar (a Koç Group Company), Alvis Vickers (BAE Systems Land UK), PSM (Pagani SpA), and STREIT Group. |

SEGMENTAL ANALYSIS

By Platform Insights

The combat vehicles segment dominated the Europe armoured personnel carrier market and accounted for a substantial share in 2025. The dominance of the segment is driven by its central role in infantry transport, reconnaissance, and direct fire support across NATO and EU rapid reaction forces. Combat vehicles such as the Boxer, VBCI, and Patria AMV form the backbone of European mechanized brigades, designed to transport squads under fire while providing STANAG 4569 Level 4 protection against 14.5 mm rounds and 10 kg TNT blast threats. NATO’s updated force models increasingly emphasize the urgent need for high-readiness, mobile, and protected land units to counter conventional threats. Poland is drastically increasing its armored personnel carrier fleet through a combination of domestic production and South Korean imports to support its significant, accelerated expansion of ground forces. Similarly, Germany is utilizing its special defence fund to modernize its land forces by procuring modern wheeled combat vehicles, such as the Boxer, to replace older, legacy systems and enhance medium-force capabilities. These platforms are not auxiliary but essential force multipliers, enabling dismounted infantry to operate in contested environments where unprotected movement is lethal. Their integration with digital battlefield networks further cements their irreplaceability in modern combined arms doctrine. The Boxer programme, managed by a joint German and Dutch industrial partnership, demonstrates that high levels of vehicle commonality encourage widespread international adoption. Several European nations have integrated this platform, fostering a unified ecosystem for shared logistics, training, and maintenance. According to multinational procurement agencies, utilizing a common vehicle platform lowers the long-term financial burden of fleet ownership, while standardizing equipment improves the speed and seamlessness of logistics during integrated international military deployments. The European Defence Fund has reinforced this trend by funding collaborative projects that mandate cross border industrial participation. As a result, combat vehicles benefit from economies of scale, political alignment, and reduced procurement risk, factors that marginalize bespoke national designs and consolidate the market around a few high capability, alliance certified platforms.

The unmanned armored ground vehicles segment is predicted to witness the highest CAGR of 14.3% during the forecast period due to integration into counter drone and logistics autonomy missions, as well as strategic investment in autonomous ground warfare capabilities. UAGVs are increasingly deployed for high risk tasks where human presence is undesirable, including route clearance, casualty evacuation, and resupply in contested zones. The war in Ukraine demonstrated the vulnerability of manned logistics convoys to loitering munitions, prompting NATO to fast track unmanned solutions. European nations are actively trials and deploying Milrem Robotics’ THeMIS unmanned ground vehicles to support logistics and ammunition resupply, with recent initiatives in the Nordic region. These platforms reduce soldier exposure while maintaining operational tempo. Swedish procurement officials have emphasized that modern unmanned ground vehicles are capable of transporting significant payloads, which allows them to substitute for manual labor in dangerous logistics tasks. This shift from manned to unmanned support is accelerating due to advances in AI navigation, secure datalinks, and modular mission kits that adapt platforms for EOD, surveillance, or medical evacuation roles. The European Defence Fund continues to support the development of autonomous ground systems and robotic capabilities as part of broader efforts to boost European defence technology and industry. Projects like France’s PEGASE and Germany’s ATLAS aim to field swarm capable UGVs by 2028 that can operate in GPS denied environments using terrain mapping and cooperative autonomy. European military analysts frequently highlight the integration of unmanned ground vehicles as a key method for improving force survivability and addressing personnel shortages in future combat scenarios. Unlike traditional APCs bound by crew safety constraints, UAGVs can be sacrificed in high threat scenarios, enabling tactical flexibility previously unattainable. This strategic reorientation, treating autonomy not as an add on but as a core warfighting domain, is driving rapid prototyping, testing, and fielding across the continent.

By Propulsion Insights

The conventional propulsion systems segment led the Europe armoured personnel carrier market and captured a significant share in 2025. Diesel and diesel electric hybrids remain dominant due to proven reliability, fuel infrastructure compatibility, and power density requirements for heavy armour. Modern military diesel engines, such as the MTU 8V199 used in the Boxer, deliver over 700 horsepower while meeting stringent NATO fuel interoperability standards. NATO’s Single Fuel Concept aims to maximize operational efficiency by standardizing fuel types across land and air assets, utilizing a common logistics network for F-34 and F-54 fuel delivery throughout Europe. Electric drivetrains, by contrast, lack standardized charging infrastructure in forward operating areas and face range limitations under combat loads. The German Bundeswehr considers conventional propulsion necessary for sustaining long-range, high-intensity land operations, especially when rapid, unrefueled movement over significant distances is critical for operational success, as supported by general logistics assessments and NATO-focused exercises. Furthermore, diesel engines provide abundant onboard power for weapons, cooling, and communications without draining traction batteries, a critical advantage in sustained operations. While fully electric APCs remain experimental, many new platforms incorporate mild hybrid systems to enhance silent watch capability. BAE Systems Hägglunds is developing a CV90 Hybrid demonstrator to reduce thermal and acoustic signatures by using an electric motor for onboard power, thus avoiding engine idling. The Swedish Defence Materiel Administration is exploring this technology to enhance the vehicle's signature management and reduce its detectability by enemy sensors. Such hybrid architectures offer a pragmatic middle ground, retaining diesel range while gaining tactical stealth, making them the preferred near term solution for European armies balancing innovation with operational realism.

The electric propulsion segment is estimated to register the fastest CAGR of 18.6% over the forecast period owing to strategic alignment with EU green defence initiatives, and technological spillover from civilian automotive sector. The European Commission’s 2024 Green Defence Framework encourages member states to reduce the carbon footprint of military operations, creating policy tailwinds for electrification. Projects like the EVO (Electric Vehicle for Operational use), co funded by France and Germany under the European Defence Fund, aim to deliver a 20 tonne electric APC prototype by 2027. Although range remains limited to 150 kilometers, urban and rear area missions, such as base security, medical evacuation, and convoy escort in low threat zones, are viable applications. Electric armored personnel carriers offer significant noise reductions compared to diesel variants, providing enhanced stealth capabilities for peacekeeping and counter-insurgency operations. Advances in battery energy density, silicon carbide inverters, and regenerative braking from the civilian EV industry are accelerating military adoption. Companies like Renault Trucks Defense and RENK are leveraging commercial lithium iron phosphate (LFP) cell technology to develop ruggedized packs resistant to shock, vibration, and electromagnetic pulse. The Netherlands Ministry of Defence is advancing the integration of electric technologies, with ongoing trials aiming to improve operational turnaround and logistics. While not yet suitable for frontline combat, these platforms fill critical niche roles while building industrial capacity for future high power applications. Declining battery costs, coupled with advancements in solid-state technology, are driving electric propulsion from experimental phases into operational deployment for targeted applications.

By System Insights

The observation & display systems segment was the largest segment in the Europe armoured personnel carrier market and occupied a 22.4% share in 2025. The prominence of the segment is credited to survivability through enhanced situational awareness and digital integration with network-centric warfare architectures. Modern APCs integrate 360 degree camera systems, thermal imagers, and augmented reality displays to eliminate blind spots and enable crew operation from within the hull—critical against drone and sniper threats. The Boxer’s Argus II system, for example, fuses data from six high resolution cameras and thermal sensors to create a real time panoramic view on crew head mounted displays. According to German Army exercises, integrating advanced observation systems into units during multinational training scenarios has led to improved target identification speed and reduced instances of friendly fire. In urban combat, where threats emerge from multiple directions, this capability is not optional but existential. As drone surveillance becomes ubiquitous, the ability to see without exposing oneself defines tactical superiority. Observation systems are no longer standalone but fused with command and control networks. Data from vehicle sensors feeds into the NATO Federated Mission Network, allowing platoon leaders to share threat locations and terrain intelligence in real time. The French SCORPION programme’s SICS (System of Information and Combat SCORPION) links every vehicle’s display to a common operational picture, enabling collaborative engagement. According to the French General Staff, the integration of new digital, network-centric technologies in simulated hybrid warfare scenarios has successfully accelerated decision-making cycles. Observation systems are moving beyond passive surveillance, becoming active decision aides driven by AI object recognition and tracking. Consequently, these systems have evolved into the cognitive core of the modern APC, justifying their top-tier investment status.

The countermeasure systems segment is anticipated to witness the fastest CAGR of 16.8% from 2026 to 2034. The rapid growth of the segment is propelled by the urgent need to defeat drone and missile threats. Small, adapted aerial systems have become a standard feature of modern European conflict, with regional reports indicating a massive and consistent volume of monthly equipment turnover and operational deployments. In response, European militaries are rapidly fielding integrated counter UAV suites combining radar detection, RF jamming, and kinetic effectors. The German Bundeswehr’s “SkyWiper” programme equips Boxer APCs with Rafael’s Drone Dome system, which detects drones up to 3 kilometers away and jams control links within 500 meters. Growing security concerns have led a significant number of European nations to prioritize the integration of defensive technologies against aerial threats as a standard requirement for new armored vehicle acquisitions. These systems are no longer optional add ons but baseline survivability features, transforming APCs from passive transports into active nodes in layered air defence networks. Next generation countermeasures emphasize open architecture to accommodate evolving threats. The French PILAR V system, integrated into the Griffon APC, uses software defined radio to adapt jamming profiles against new drone models without hardware changes. Recent military exercises have focused on testing the ability of networked combat vehicles to identify the source of radio signals to locate and neutralize opposing drone teams. Modern defensive suites developed by major aerospace firms are designed to significantly improve detection accuracy and reliability over older electronic interference methods. As electronic warfare shifts from fixed installations to mobile platforms, APCs become critical EW vectors, protecting not only themselves but entire convoys and dismounted squads. This expanding mission set ensures sustained high growth in countermeasure investments across Europe.

REGIONAL ANALYSIS

Russia Armoured Personnel Carrier Market Analysis

Russia was the top performer in the Europe armoured personnel carrier market and accounted for a 42.7% share in 2025. This position of the Russian market is attributed to its massive domestic production capacity and extensive deployment in active conflict zones. The market status in this region is defined by a total war economy orientation where state-owned enterprises like Military Industrial Company operate at maximum output to supply the armed forces with platforms such as the BTR-82A and the newer Bumerang. The ongoing military operations have necessitated an unprecedented surge in manufacturing, with industry reports indicating that armored vehicle production rates increased significantly compared to pre-conflict levels according to sources. The Russian government has allocated a significant portion of its record defense budget, which reached a substantial percentage of gross domestic product, specifically to replenish armored vehicle losses and equip new mobilized units. Furthermore, the export market remains active despite sanctions, with deliveries continuing to allied nations in Africa and Asia who rely on Russian hardware for cost-effective mobility solutions. As per the International Institute for Strategic Studies, the sheer volume of vehicles required for frontline operations and rear-area security ensures that Russia maintains the largest fleet and production line in the continent. The focus on amphibious capabilities and mine protection in newer models reflects lessons learned from recent combat experiences, driving continuous design iterations and high procurement volumes.

Germany Armoured Personnel Carrier Market Analysis

Germany was the next prominent player in the Europe armoured personnel carrier market and held a 16.4% share in 2025 due to its role as the primary developer and manufacturer of high-tech tracked and wheeled platforms for the North Atlantic Treaty Organization. The market status here is characterized by a major rearmament phase following decades of underinvestment, triggered by the establishment of a special defense fund aimed at modernizing the Bundeswehr. A primary driving factor is the urgent requirement to replace aging Marder infantry fighting vehicles and older transporters with the new Puma and Boxer platforms, which represent the pinnacle of European armored engineering. Data from the German Federal Ministry of Defence indicates that orders for additional armored vehicle variants have increased substantially, signaling a robust domestic demand pipeline. The German industry, led by Rheinmetall and KMW, also serves as a key export hub for NATO allies seeking interoperable and highly protected vehicles. According to reports from Janes, Germany has committed to delivering hundreds of armored vehicles to partner nations in Eastern Europe as part of collective defense initiatives. The emphasis on digitalization, active protection systems, and modular mission kits makes German APCs highly desirable in the global market. As per sources, the strategic shift toward heavy brigade structures ensures sustained production rates for the next decade, solidifying Germany's status as the technological leader in the regional sector.

France Armoured Personnel Carrier Market Analysis

France is also a major player in the Europe armoured personnel carrier market. It serves as a critical hub for the development of next-generation wheeled armored vehicles under its ambitious Scorpion program. The market status in this region is marked by the successful mass production and deployment of the Griffon and Jaguar vehicles, which are replacing legacy fleets across the French Army and export markets. The driving force behind this activity is the Military Programming Law, which allocates significant funding to defense and prioritizes the renewal of ground combat equipment to enhance expeditionary capabilities. Statistics from the Directorate General of Armaments reveal that a large number of new armored vehicles were delivered or ordered as part of the Scorpion modernization effort. France also maintains a strong export presence, particularly in the Middle East and Europe, with countries like Belgium and Hungary selecting French platforms for their future armored fleets. As per reports from Nexter Systems, the integration of advanced battle management systems and networked warfare capabilities into these vehicles sets a new standard for interoperability within European coalitions. The focus on strategic autonomy ensures that France retains full control over its supply chain and intellectual property. This combination of large-scale domestic procurement and successful international sales campaigns ensures France remains a pivotal power in the European armored vehicle landscape.

Turkey Armoured Personnel Carrier Market Analysis

Turkey occupies a significant position in the Europe armoured personnel carrier market and is known for its rapid transformation from a license producer to a leading indigenous designer and exporter of cost-effective armored solutions. The market status here is defined by a vibrant private sector ecosystem including companies like Otokar, BMC, and FNSS, which produce highly versatile platforms such as the Kirpi and Tulga that have seen extensive combat use. A key driver is the need to equip large security forces for counter-terrorism operations and border security, leading to consistent domestic orders for mine-resistant ambush protected vehicles. Research indicates that land systems exports reached record highs, with armored personnel carriers accounting for a significant portion of sales to international markets. The competitive pricing and proven survivability of Turkish vehicles in real-world conflicts have made them attractive alternatives to Western counterparts. According to analysis from Shephard Media, Turkey has secured contracts to supply thousands of armored vehicles to various international clients, leveraging its ability to customize designs for specific operational environments. The government's push for self-sufficiency has resulted in high localization rates for engines, transmissions, and armor systems. As per sources, the continuous feedback loop from active military engagements drives rapid iterative improvements, keeping Turkish products at the forefront of the mid-tier global market.

United Kingdom Armoured Personnel Carrier Market Analysis

The United Kingdom is anticipated to expand notably in the Europe armoured personnel carrier market from 2026 to 2034 by functioning as a center for specialized armored vehicle innovation and the integrator of complex multinational programs. The market status in this region is currently defined by the execution of the Boxer program alongside Germany and the development of the Ajax reconnaissance vehicle, despite some programmatic challenges. The primary driver is the Integrated Review Refresh which commits to modernizing the British Army's armored fleet to ensure readiness for high-intensity warfare scenarios. Multiple studies show that billions of pounds have been committed to the acquisition of Boxer variants and the upgrade of existing Warrior vehicles to extend their service life. The UK industry, led by BAE Systems and Rheinmetall BAE Systems Land, focuses on high-end protection levels and advanced sensor fusion capabilities. As per sources, the emphasis on interoperability with NATO allies drives the selection of common platforms like Boxer. The country also maintains a niche in exporting specialized armored vehicles and upgrade kits to Commonwealth nations. According to studies, the UK continues to invest heavily in research and development for autonomous armored systems and hybrid electric drives. This focus on cutting-edge technology and strategic partnerships ensures the UK remains a significant and influential player in the European armored vehicle sector.

COMPETITIVE LANDSCAPE

The Europe armoured personnel carrier market is characterized by intense competition among established defence primes, state backed consortia, and emerging technology integrators. Legacy players like KNDS and BAE Systems leverage decades of operational experience and deep ties to national armies, while firms like GDELS benefit from transatlantic supply chains and scalable platforms. The market is increasingly shaped by collaborative programmes such as MGCS and PEGASE, which prioritize shared industrial workshare and technology sovereignty. Competition is less about price and more about capability, interoperability, and industrial offset commitments. Smaller nations often pool procurement through initiatives like OCCAR to access high end systems. Despite rising budgets, fiscal constraints and export control complexities create barriers for new entrants. Success hinges on balancing cutting edge protection, digital integration, and political alignment within Europe’s evolving security architecture.

KEY MARKET PLAYERS

Some of the notable key players in the Europe armoured personnel carrier market are

- Rheinmetall AG

- BAE Systems plc

- Nexter Systems under KNDS

- Iveco Defence Vehicles

- General Dynamics European Land Systems

- Patria Oyj

- FNSS Savunma Sanayi

- Otokar, part of Koç Group

- Alvis Vickers under BAE Systems Land UK

- PSM GmbH

- STREIT Group

Top Players in the Market

- Headquartered in Germany and France, KNDS is a leading European defence consortium formed by Krauss Maffei Wegmann and Nexter Systems. The company develops and manufactures advanced armoured personnel carriers including the VBCI and the future MGCS platform. KNDS plays a pivotal role in NATO interoperability through standardized designs that meet STANAG protection and digital networking requirements. The company also launched a modular mid life upgrade kit for legacy fleets across Europe, enabling cost effective modernization without full replacement. These actions reinforce KNDS’s position as a strategic enabler of European land force transformation and collaborative defence industrial policy.

- Based in Sweden, BAE Systems Hägglunds is renowned for its CV90 family of armoured combat vehicles, widely operated across Northern and Central Europe. The company emphasizes survivability, mobility, and digital integration, with the latest CV90 MkIV featuring a 360 degree situational awareness suite and hybrid electric propulsion. It also partnered with Finland and the Netherlands on joint sustainment programs to reduce lifecycle costs. These initiatives solidify its reputation for innovation in high latitude warfare and network centric capabilities, making it a preferred partner for Nordic and Baltic defence modernization.

- A subsidiary of General Dynamics, GDELS operates major facilities in Spain, Germany, and Austria, producing the Piranha and ASCOD families of armoured vehicles. The company supplies both EU and NATO forces with platforms tailored for rapid deployment and peacekeeping missions. It also inaugurated a new digital twin facility in Madrid to simulate vehicle performance under diverse threat scenarios. These investments enhance customization agility and support Europe’s push for sovereign defence production while maintaining transatlantic interoperability through common subsystems and logistics.

Top Strategies Used by the Key Market Participants

Key players in the Europe armoured personnel carrier market are pursuing multinational collaborative development to share costs and ensure NATO interoperability. They are integrating modular open architecture systems to enable rapid technology insertion and mid life upgrades. Companies are investing in hybrid and electric drivetrains to enhance silent mobility and reduce thermal signatures. Strategic partnerships with national armies focus on local assembly and sustainment to build sovereign industrial capacity. Additionally, manufacturers are embedding advanced countermeasure suites and AI driven situational awareness tools to address emerging drone and electronic warfare threats in contested environments.

MARKET SEGMENTATION

This research report on the European armoured personnel carrier market has been segmented and sub-segmented based on categories.

By Platform

- Combat Vehicles

- Combat Support Vehicles

- Unmanned Armored Ground Vehicles

By Propulsion

- Conventional

- Electric

By Mobility

- Wheeled

- Tracked

By Solution

- Line Fit

- Retrofit

By System

- Drive Systems

- Structures & Mechanisms

- Weapons & Ammunition Control Systems

- Countermeasure Systems

- Command & Control Systems

- Navigation Systems

- Observation & Display Systems

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe armoured personnel carrier (APC) market?

The Europe APC market refers to the production, procurement, deployment, and modernization of armoured personnel carriers used by military and defense forces across European countries.

2. What is an armoured personnel carrier (APC)?

An APC is a tracked or wheeled armored vehicle designed to transport infantry safely in combat zones, offering protection against small arms fire, shrapnel, and improvised explosive devices (IEDs).

3. What factors are driving growth in the Europe APC market?

Growth is driven by increased defense budgets, modernization of military forces, rising security threats, regional geopolitical tensions, and the need for enhanced troop mobility and force protection.

4. Which countries are major users of APCs in Europe?

Key European users include Germany, France, the United Kingdom, Italy, Spain, and other NATO member states with standing army and peacekeeping commitments.

5. What are the main types of APCs used in Europe?

Common types include wheeled APCs (4x4, 6x6, 8x8), tracked APCs, and modular platforms capable of multi-purpose operations.

6. How do APCs differ from infantry fighting vehicles (IFVs)?

APCs primarily focus on troop transport and protection, while IFVs are equipped with heavier armament and designed for direct combat engagement alongside infantry.

7. What role does modernization play in the Europe APC market?

Modernization programs include upgrades to armor protection, electronics, communication systems, situational awareness, and integration of active protection systems (APS).

8. Who are the key players in the Europe APC market?

Major defense manufacturers include Rheinmetall, BAE Systems, Nexter Systems, PSM (Pagani SpA), Iveco Defence Vehicles, and General Dynamics European Land Systems.

9. How do defense procurement policies impact the APC market?

Government defense procurement policies, interoperability requirements within NATO, and offset agreements significantly influence APC acquisition and production strategies.

10. What challenges does the Europe APC market face?

Challenges include high development and production costs, long procurement cycles, competing defense priorities, and the complexity of integrating advanced systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com