Europe Automated Retail Market Size, Share, Trends, & Growth Forecast Report By Type (Hardware, Software), End User and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Automated Retail Market Report Summary

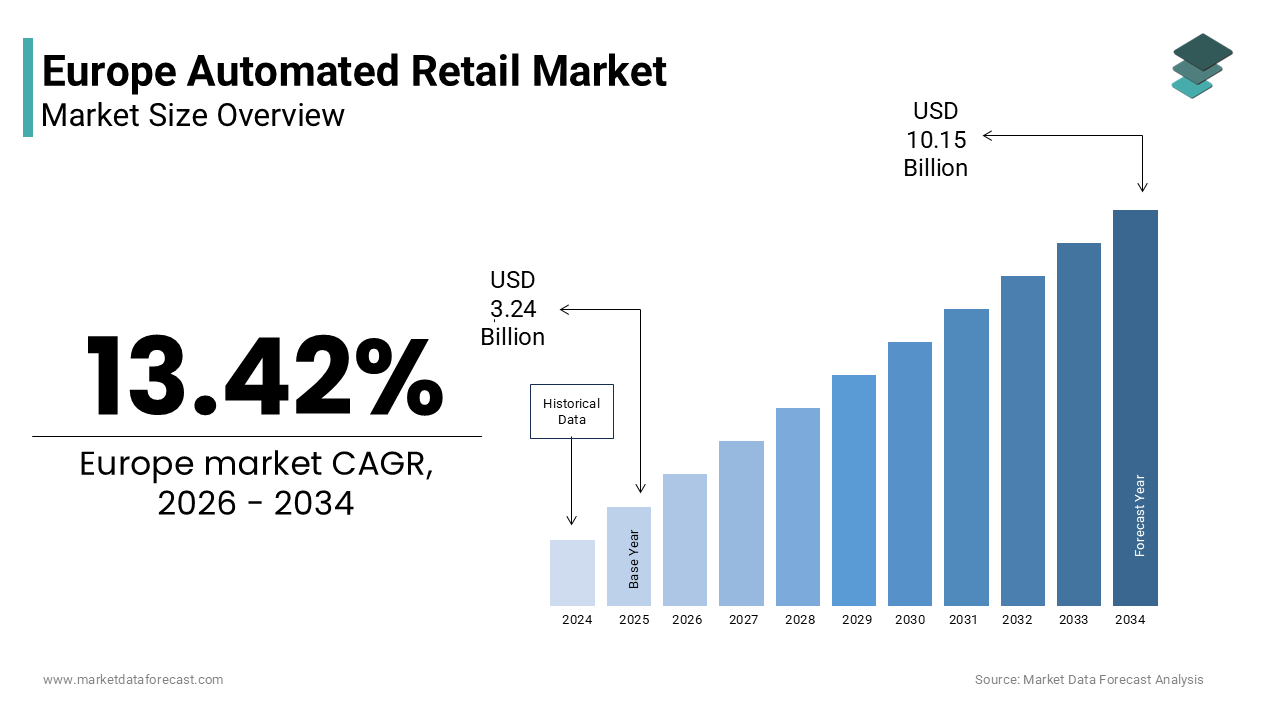

The Europe automated retail market was valued at USD 3.24 billion in 2025, is estimated to reach USD 3.67 billion in 2026, and is projected to reach USD 10.15 billion by 2034, growing at a CAGR of 13.42% during the forecast period from 2026 to 2034. The growth of the European automated retail market is driven by rising labor costs, increasing workforce shortages, and strong consumer preference for contactless and convenient shopping experiences. The adoption of technologies such as artificial intelligence, IoT, and computer vision in vending machines and autonomous kiosks is transforming traditional retail operations. Moreover, the expansion of automated retail into high-traffic locations such as transit hubs, offices, and public spaces is accelerating market growth.

Key Market Trends

- Increasing adoption of smart vending machines and autonomous kiosks powered by AI and IoT technologies.

- Growing preference for contactless payments and 24/7 shopping convenience among urban consumers.

- Expansion of automated retail into non-traditional locations such as airports, offices, and universities.

- Rising use of AI-driven personalization and dynamic pricing in automated retail systems.

- Strong focus on sustainability through energy-efficient machines and reduced food waste.

Segmental Insights

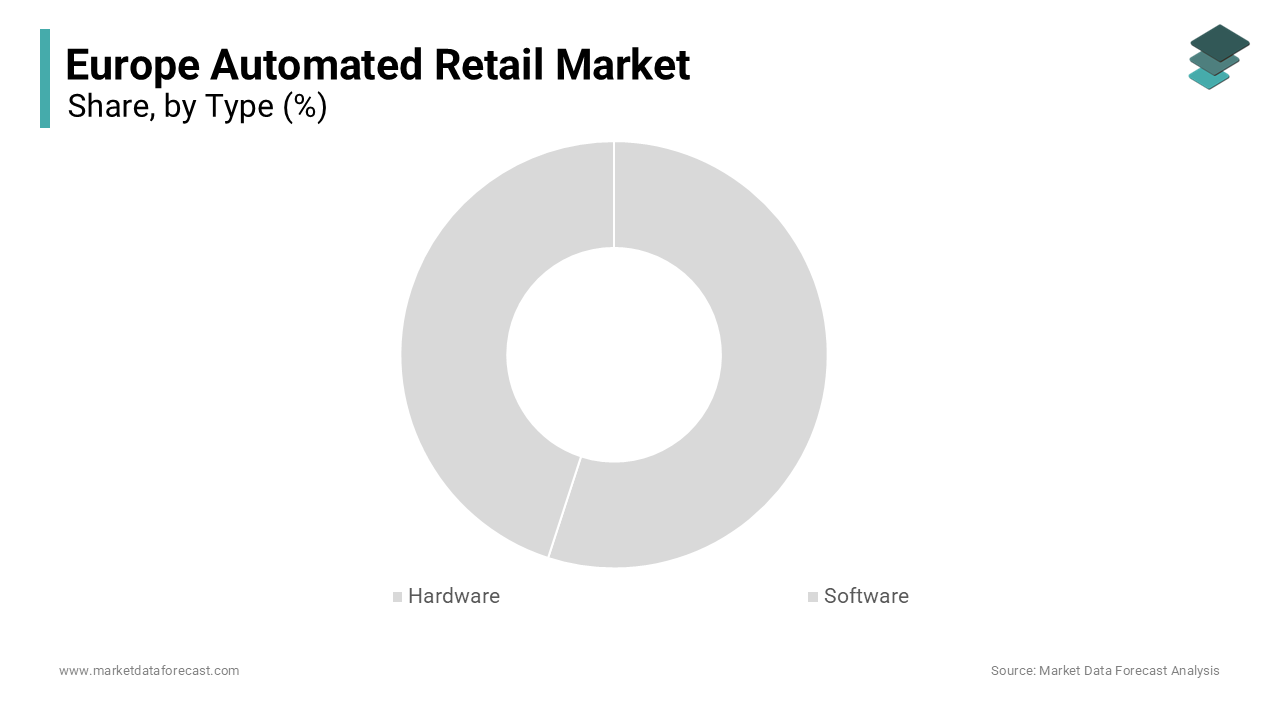

- Based on type, the hardware segment was the largest and held a significant share of the Europe automated retail market in 2025. The dominance is attributed to high capital investment in vending machines, kiosks, and physical infrastructure.

- Based on end user, the grocery segment accounted for the largest share of the Europe automated retail market in 2025. This is driven by rising demand for convenient access to fresh food and ready-to-eat products.

- The software segment is expected to witness the fastest growth, supported by increasing adoption of cloud-based analytics, remote monitoring, and AI-driven operational optimization.

Regional Insights

The Europe automated retail market is expanding across major countries, supported by urbanization, digital payment adoption, and demand for convenience-driven retail solutions.

- Germany was the largest contributor, accounting for 23.1% of the Europe automated retail market share in 2025, driven by strong industrial capabilities, high automation adoption, and advanced infrastructure.

- The United Kingdom holds a significant position due to high urbanization, widespread cashless transactions, and strong retail innovation.

- France is experiencing steady growth, supported by tourism demand, government initiatives, and increasing deployment of automated kiosks.

- Italy and Spain are emerging markets, driven by tourism, urban retail demand, and increasing adoption of automated retail technologies.

Competitive Landscape

The Europe automated retail market is highly competitive, featuring a mix of global technology providers and regional innovators. Companies focus on technological advancements, AI integration, and sustainability to differentiate themselves. Strategic partnerships between hardware manufacturers and software providers are common to deliver end-to-end solutions. Key players are also investing in secure payment systems, remote monitoring, and customer-centric innovations to enhance user experience. Prominent players in the Europe automated retail market include Diebold Nixdorf, NCR Corporation, Zebra Technologies Corporation, Honeywell International Inc., Toshiba Global Commerce Solutions, Fujitsu Limited, KUKA AG, Azkoyen Group, Crane Co., Sanden Holdings Corporation, Glory Ltd., Ingenico Group, Posiflex Technology Inc., Evoke Creative Limited, and Oleaph Group.

Europe Automated Retail Market Size

The Europe automated retail market size was valued at USD 3.24 billion in 2025 and is anticipated to reach USD 3.67 billion in 2026 from USD 10.15 billion by 2034, growing at a CAGR of 13.42% during the forecast period from 2026 to 2034.

Automated retail encompasses a transformative sector where vending machines, smart kiosks, and autonomous stores utilize advanced technologies such as artificial intelligence, computer vision, and Internet of Things connectivity to facilitate unattended transactions. This ecosystem eliminates the need for traditional cashier interactions, offering consumers seamless shopping experiences through cashless payments and real time inventory tracking. The region is witnessing a structural shift in consumer behavior driven by the demand for convenience and contactless services. According to Eurostat, the share of individuals in the European Union who used internet banking for payments reached 63% in 2023, which is indicating a robust digital payment infrastructure that supports automated retail operations. Furthermore, the European Commission reported that the urban population in Europe accounted for 75% of the total population in 2022 and creating dense consumer hubs ideal for high traffic automated retail deployments. The integration of these systems aligns with broader sustainability goals, as automated units often optimize energy consumption and reduce food waste through precise stock management. According to the European Environment Agency, retail sectors are increasingly adopting circular economy principles, with automated systems enabling better tracking of product lifecycles. The regulatory landscape under the General Data Protection Regulation ensures that consumer data collected during these transactions remains secure, fostering trust in digital retail interfaces. This technological evolution redefines the physical retail space and allowing brands to operate in non-traditional locations such as transit hubs and corporate offices, thereby expanding market reach without the overhead costs associated with manned storefronts.

MARKET DRIVERS

Rising Labor Costs and Workforce Shortages Accelerate Automation Adoption

Escalating labor costs and persistent workforce shortages across the European retail sector is a key factor propelling the growth of the European automotive retail market, which is also compelling businesses to seek efficient alternatives to traditional staffing models. According to the European Central Bank, negotiated wages in the euro area increased by approximately 4.5% in 2023and this is reflecting tight labor markets and inflationary pressures that strain operational budgets for retailers. Simultaneously, according to the European Labour Authority, the hospitality and retail sectors faced significant recruitment challenges, with vacancy rates remaining elevated compared to pre pandemic levels. Automated retail systems mitigate these pressures by operating continuously without the need for shift scheduling, breaks, or extensive training programs. These units require minimal human intervention, primarily for restocking and maintenance, which significantly reduces personnel expenses. According to a study by the European Federation of Food, Agriculture and Tourism Trade Unions, the average cost of employing retail staff has risen by 15% over the past five years, prompting operators to explore capital intensive but labor saving technologies. The reliability of automated systems ensures consistent service delivery, unaffected by absenteeism or turnover issues that plague manned stores. Furthermore, the ability to deploy these units in remote or low traffic areas allows retailers to expand their footprint without incurring prohibitive staffing costs. This economic imperative drives investment in smart vending machines and autonomous kiosks, enabling companies to maintain profitability while meeting consumer demand for accessible and convenient shopping options in an increasingly expensive labor environment.

Consumer Preference for Contactless and Convenient Shopping Experiences

The shifting consumer preference towards contactless and convenient shopping experiences is further boosting the regional market expansion. As per a survey conducted by the European Consumer Organisation, 78% of respondents indicated a preference for contactless payment methods following the pandemic, highlighting a lasting change in purchasing behaviors. Automated retail units cater to this demand by offering seamless, cashless transactions through mobile wallets and contactless cards, reducing wait times and physical interactions. The convenience of 24/7 availability appeals to urban populations with irregular schedules and is allowing them to purchase essentials at any time without being constrained by store opening hours. According to Eurostat, the proportion of Europeans living in cities reached 75% in 2022, creating a dense customer base that values immediate access to goods. Automated kiosks located in transit stations, universities, and office buildings fulfil this need for instant gratification and efficiency. The integration of personalized recommendations through AI driven interfaces further enhances the user experience, making interactions more engaging and tailored to individual preferences. The European Commission’s Digital Decade targets aim to ensure that 80% of citizens use digital ID solutions by 2030, facilitating smoother authentication processes in automated retail environments. This alignment with digital lifestyle trends ensures sustained demand for automated retail solutions that offer frictionless and efficient shopping journeys.

MARKET RESTRAINTS

Stringent Regulatory Compliance and Data Privacy Concerns

Strict regulatory frameworks governing data privacy and security is hindering the expansion of the European automotive retail market. The General Data Protection Regulation imposes rigorous standards on the collection, storage, and processing of personal data, including payment details and behavioural patterns captured by smart vending machines and autonomous stores. According to the European Data Protection Board, non-compliance can result in fines of up to 4% of global annual turnover, creating substantial financial risks for retailers and technology providers. Automated retail systems often rely on cameras and sensors to monitor inventory and prevent theft, raising concerns about surveillance and consent among privacy advocates. According to a report by the European Union Agency for Fundamental Rights, public skepticism regarding facial recognition and biometric data usage remains high and potentially hindering the deployment of advanced identification technologies in retail settings. Retailers must invest heavily in secure infrastructure and legal counsel to ensure adherence to these regulations, increasing operational costs and slowing down innovation cycles. Furthermore, varying interpretations of GDPR across member states create fragmentation, complicating cross border expansions for automated retail chains. The need for transparent data handling practices and explicit user consent mechanisms adds layers of complexity to system design and user interface development. These regulatory hurdles discourage smaller players from entering the market and limit the scalability of existing operations, thereby restraining overall market growth and technological advancement in the European region.

High Initial Capital Investment and Maintenance Costs

Substantial initial capital investment and ongoing maintenance costs are further hampering the expansion of the European automotive retail market, which is further limiting market penetration particularly among small and medium sized enterprises. The deployment of smart vending machines and autonomous stores requires significant upfront expenditure for hardware, software integration, and installation infrastructure. According to the European Investment Bank, the cost of implementing IoT enabled retail systems can be three to four times higher than traditional vending setups, posing a financial challenge for retailers with limited budgets. Additionally, the complexity of these systems necessitates specialized technical support for regular maintenance and repairs, which incurs recurring expenses. According to a study by the European Small Business Alliance, nearly 60% of small retailers cite high initial costs as the primary obstacle to adopting digital technologies. The rapid pace of technological obsolescence further exacerbates this issue, requiring frequent upgrades to remain competitive and secure. Energy efficiency standards imposed by the European Union also mandate the use of advanced cooling and lighting systems, adding to the operational burden. While automated retail offers long term savings on labor, the immediate financial outlay deter many potential adopters. The lack of standardized financing options for such specialized equipment further restricts access to capital. Consequently, only well-funded corporations and large retail chains can afford to scale these operations, which is leaving a significant portion of the market underserved and slowing the overall diffusion of automated retail technologies across the continent.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Personalized Customer Engagement

The integration of artificial intelligence into automated retail systems provides a lucrative opportunity for the European automotive retail market. AI algorithms analyze purchase history and real time behavior to offer tailored product recommendations, dynamic pricing, and targeted promotions directly at the point of sale. According to the European Institute for Innovation and Technology, retailers utilizing AI driven personalization have observed a 20% increase in customer retention rates, highlighting the effectiveness of this approach. Smart kiosks equipped with facial recognition and sentiment analysis can adjust displays and suggestions based on demographic profiles and mood, creating a more interactive and appealing shopping environment. The European Commission’s support for AI innovation through funding programs encourages the development of such advanced retail technologies. Furthermore, AI enables predictive inventory management, ensuring that popular items are always in stock and reducing waste from perishable goods. According to a report by the European Retail Round Table, optimized inventory levels can reduce spoilage by up to 30%, contributing to sustainability goals and cost savings. The ability to collect and analyze granular data allows retailers to refine their product offerings and marketing strategies with precision. This data driven approach fosters deeper customer loyalty and increases average transaction values. As consumers increasingly expect personalized interactions, automated retail operators who leverage AI capabilities will gain a competitive edge, unlocking new revenue streams and enhancing brand value in the evolving European retail landscape.

Expansion into Non Traditional and Remote Locations

The expansion of automated retail units into non-traditional and remote locations offers significant growth opportunities for the regional market expansion. Unlike conventional stores, automated kiosks and vending machines require minimal space and infrastructure, allowing deployment in airports, train stations, hospitals, university campuses, and industrial parks. According to Eurostat, the number of passengers using air transport in the European Union exceeded 900 million in 2023, creating high traffic environments ideal for automated retail installations. These locations often lack adequate retail options, particularly during off peak hours, making automated solutions a valuable service for travelers and workers. The European Transport Safety Council highlights the increasing dwell times in transit hubs, providing ample opportunity for impulse purchases. Furthermore, rural areas with limited access to brick and mortar stores benefit from the accessibility of automated retail, bridging the gap in service availability. According to the European Network for Rural Development, improving access to essential goods in remote communities is a priority, and automated retail can play a pivotal role in achieving this goal. The flexibility of these units allows retailers to test new markets with lower risk and investment compared to establishing full scale stores. By strategically placing automated systems in high footfall and underserved areas, operators can capture incremental revenue and enhance brand visibility. This geographic diversification not only expands market reach but also strengthens resilience against fluctuations in traditional retail performance.

MARKET CHALLENGES

Technical Glitches and System Reliability Issues

Technical glitches and system reliability issues is a major challenge to the Europe automated retail market, as any downtime directly impacts revenue and erodes consumer trust in unmanned shopping experiences. Automated retail units rely on complex networks of sensors, software, and connectivity modules that are susceptible to failures due to hardware malfunctions, software bugs, or network interruptions. According to the European Telecommunications Standards Institute, connectivity issues remain a prevalent problem in IoT devices, with approximately 15% of connected retail units experiencing occasional service disruptions. Such incidents can lead to failed transactions, incorrect dispensing of products, or inability to process payments, resulting in customer frustration and negative brand perception. The lack of on site staff means that resolving these issues often requires remote troubleshooting or dispatching technicians, which can cause prolonged periods of unavailability. According to a consumer survey by the European Consumer Centre, 40% of users stated they would avoid using automated retail services again after encountering a technical error. The complexity of integrating multiple technologies increases the likelihood of compatibility issues and system crashes. Furthermore, cyber security threats pose additional risks, as vulnerabilities can be exploited to disrupt operations or steal data. Ensuring high availability and robust performance requires continuous monitoring and proactive maintenance, which adds to operational complexity and costs. Retailers must invest in redundant systems and rapid response protocols to mitigate these risks, yet the inherent unpredictability of technology remains a persistent challenge that hinders seamless customer experiences and market confidence.

Vandalism and Security Threats in Public Spaces

Vandalism and security threats in public spaces constitute a significant challenge for the Europe automated retail market, particularly for units deployed in outdoor or unsupervised locations. Automated retail kiosks and vending machines are vulnerable to physical damage, theft, and tampering, which can result in costly repairs and inventory losses. As per Europol data, property crime rates in urban areas remain a concern, with retail infrastructure often targeted by opportunistic criminals. The absence of human supervision makes these units easy targets for vandalism, including graffiti, broken screens, and forced entry attempts. According to the European Retail Forum, security incidents involving automated retail units have increased by 10% in major metropolitan areas over the past two years, prompting operators to invest heavily in protective measures. Reinforced materials, surveillance cameras, and alarm systems are necessary to deter criminal activity, but these additions increase initial capital expenditures and maintenance requirements. Furthermore, the psychological impact of visible damage can deter potential customers, who may perceive the location as unsafe or the service as unreliable. Insurance premiums for automated retail assets in high risk areas are also elevated, adding to operational burdens. While technological advancements such as remote monitoring and real time alerts help mitigate some risks, they cannot entirely eliminate the threat of physical interference. This security vulnerability limits the feasibility of deploying automated retail solutions in certain high traffic but low security environments, restricting market expansion and requiring careful site selection and risk assessment strategies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13.42% |

| Segments Covered | By Type, End User and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Key Market Players | Diebold Nixdorf, NCR Corporation, Zebra Technologies Corporation, Honeywell International Inc., Toshiba Global Commerce Solutions, Fujitsu Limited, KUKA AG, Azkoyen Group, Crane Co., Sanden Holdings Corporation, Glory Ltd., Ingenico Group, Posiflex Technology Inc., Evoke Creative Limited, and Oleaph Group |

SEGMENTAL ANALYSIS

By Type Insights

The hardware segment dominated the market by holding 66.1% of the European market share in 2025. The leading position of hardware segment in the European market is primarily driven by the substantial capital investment required for the physical infrastructure of automated retail units, including smart vending machines, autonomous kiosks, and robotic store fixtures. According to the European Manufacturing Alliance, the cost of producing advanced IoT enabled retail hardware has remained high due to the integration of sophisticated sensors, cooling systems, and durable materials necessary for public deployment. The initial outlay for these physical assets constitutes the bulk of project costs for retailers entering the automated space. According to data from the International Vending Federation, the average cost of a fully equipped smart vending unit ranges from 5,000 to 15,000 euros, depending on complexity and capacity. This significant financial barrier ensures that hardware remains the largest revenue component in the early stages of market development. Furthermore, the need for regular hardware upgrades to support new payment technologies and enhanced security features sustains demand within this segment. The European Committee for Electrotechnical Standardization mandates strict safety and energy efficiency standards for such equipment, requiring manufacturers to invest in high quality components that comply with regulatory norms. These compliance costs further elevate the value of the hardware segment. Additionally, the expansion of automated retail into outdoor and high traffic locations necessitates robust weather resistant and vandal proof designs, which command premium pricing. Consequently, the tangible nature of hardware investments and their critical role in enabling automated transactions solidify this segment’s leading share in the European market landscape.

However, the software segment is a promising segment and is estimated to grow at a CAGR of 19.1% over the forecast period in the European market owing to the increasing reliance on cloud based analytics and remote management platforms to optimize automated retail operations. According to the European Cloud Partnership, the adoption of cloud computing services in the retail sector has grown by 30% year on year, enabling retailers to monitor and manage distributed networks of automated units in real time. Software solutions provide critical insights into sales trends, inventory levels, and machine performance, allowing operators to make data driven decisions that enhance efficiency and profitability. The ability to remotely update software, troubleshoot issues, and customize user interfaces reduces downtime and maintenance costs significantly. According to a study by the European Software Industry Association, retailers using advanced management software reported a 20% reduction in operational expenses due to improved predictive maintenance and optimized restocking schedules. The scalability of cloud based platforms allows businesses to expand their automated retail networks without proportional increases in administrative overhead. Furthermore, the integration of artificial intelligence algorithms into software systems enables dynamic pricing and personalized marketing strategies, driving higher conversion rates. The European Commission’s Digital Single Market strategy encourages the use of interoperable software solutions, fostering an environment conducive to innovation and growth. As retailers recognize the strategic value of data analytics in competitive positioning, investment in sophisticated software platforms continues to accelerate, propelling this segment’s rapid expansion within the Europe automated retail market.

By End User Insights

The grocery segment led the market by commanding for the highest share of 51.9% of the European market in 2025. The dominance of grocery segment in the European market is fueled by the growing consumer demand for fresh, healthy, and convenient food options available outside traditional store hours. Automated retail units specializing in groceries offer a wide range of products, including fresh produce, ready to eat meals, and beverages, catering to the busy lifestyles of urban populations. According to Eurostat, the consumption of fresh fruit and vegetables in the European Union has remained stable, with a slight increase in demand for pre-packaged convenience items. Automated grocery kiosks located in residential areas, office buildings, and transit hubs provide immediate access to these essentials, which is fulfilling the need for quick and easy shopping solutions. The European Food Information Council notes that 60% of consumers prioritize convenience when purchasing food items, driving the proliferation of automated grocery outlets. Furthermore, advancements in refrigeration technology allow these units to maintain optimal storage conditions for perishable goods, ensuring quality and safety. The integration of smart inventory management systems minimizes waste by tracking expiration dates and adjusting stock levels dynamically. According to the European Retail Round Table, automated grocery solutions have reduced food waste by 25% in pilot projects, aligning with sustainability goals. The ability to operate 24/7 without staffing constraints makes grocery automation an attractive model for retailers seeking to maximize sales potential. This combination of convenience, quality assurance, and operational efficiency solidifies the grocery segment’s leading position in the European automated retail market.

On the other hand, the hospitality segment dominated the market by holding 20.6% of the European market share in 2025 due to the increasing integration of automated retail solutions in hotels, airports, and train stations to enhance guest convenience and service efficiency. According to the European Travel Commission, international tourist arrivals in Europe are projected to exceed pre pandemic levels by 2025, creating a surge in demand for accessible retail services in travel hubs. Automated kiosks in hotels provide guests with 24/7 access to snacks, beverages, and travel essentials, improving satisfaction and reducing staff workload. In airports and train stations, these units cater to travelers seeking quick purchases during layovers or transit. The European Airport Council International reports that passenger throughput in European airports increased by 12% in 2023, highlighting the potential customer base for automated retail. Hospitality providers are adopting these solutions to optimize space utilization and generate additional revenue streams without expanding physical staff. The ability to offer localized and curated product selections enhances the guest experience and reflects brand identity. Furthermore, the contactless nature of automated retail aligns with hygiene preferences prevalent among travelers post pandemic. According to the International Air Transport Association, 70% of passengers prefer contactless services for safety and speed. This strong demand from the travel and hospitality sectors, combined with the operational benefits for providers, propels the rapid growth of this segment in the European automated retail market.

REGIONAL ANALYSIS

Germany Automated Retail Market Analysis

Germany accounted for the leading share of 23.1% of the European market in 2025 due to its strong industrial base, high technological adoption, and dense urban population. The country is a leader in manufacturing advanced vending and kiosk hardware, supported by a robust engineering sector. According to the German Federal Ministry for Economic Affairs and Climate Action, the digitalization of the retail sector is a key priority, with significant investments in IoT and automation technologies. The presence of major automotive and industrial companies creates a large corporate workforce that utilizes automated retail solutions in office parks and factories. According to the German Retail Federation, the demand for convenience foods and contactless payment options has risen sharply, particularly in cities like Berlin and Munich. The country’s strict labor laws and high wage levels incentivize businesses to adopt automation to reduce personnel costs. Furthermore, Germany’s commitment to sustainability drives the adoption of energy efficient automated retail units that minimize waste. The widespread availability of high speed internet infrastructure supports the seamless operation of connected devices. Regulatory frameworks ensuring data privacy and consumer protection foster trust in automated systems. This combination of technological expertise, economic incentives, and consumer demand positions Germany as the dominant market for automated retail in Europe, setting trends for innovation and adoption across the region.

United Kingdom Automated Retail Market Analysis

The United Kingdom occupied a prominent share of the European automotive retail market in 2025 due to its vibrant retail sector and high concentration of urban consumers. The UK has seen rapid adoption of automated retail in transit hubs, universities, and corporate offices, driven by the need for convenient and efficient shopping options. According to the British Retail Consortium, the retail industry faces ongoing labor shortages, prompting retailers to explore automated solutions to maintain service levels. The prevalence of cashless payments in the UK, with over 90% of transactions being non cash, facilitates smooth operations for automated units. According to Office for National Statistics data, the proportion of people living in urban areas in the UK exceeds 80%, creating ideal conditions for high traffic automated retail deployments. The country’s strong startup ecosystem fosters innovation in retail technology, with numerous companies developing novel automated shopping experiences. Government initiatives supporting digital infrastructure development further enhance the viability of these solutions. The UK’s diverse population and multicultural society drive demand for varied product offerings in automated kiosks, from ethnic snacks to healthy meals. Additionally, the focus on reducing food waste aligns with the capabilities of smart inventory management in automated retail. This dynamic environment of technological innovation, consumer readiness, and operational necessity sustains the UK’s prominent role in the European automated retail landscape.

France Automated Retail Market Analysis

France is estimated to showcase a healthy CAGR in the European automotive retail market during the forecast period owing to its strong tourism industry, urban density, and government support for digital innovation. The country is a major destination for international tourists, creating high demand for automated retail services in airports, train stations, and popular landmarks. According to the French Ministry of Economy, the Plan France 2030 includes substantial funding for digital transformation in commerce, encouraging the adoption of automated retail technologies. The presence of major retail chains and food service providers who are experimenting with autonomous stores and smart vending machines contributes to market growth. According to the National Institute of Statistics and Economic Studies, urbanization rates in France continue to rise, with over 80% of the population living in cities. This demographic trend supports the deployment of automated units in residential and commercial areas. The French consumer’s appreciation for quality and convenience drives demand for fresh and gourmet options in automated kiosks. Furthermore, strict labor regulations and high social charges incentivize businesses to automate routine tasks. The country’s commitment to environmental sustainability promotes the use of energy efficient and waste reducing retail solutions. Collaborations between tech startups and established retailers foster innovation in user experience and operational efficiency. This supportive ecosystem of policy, tourism, and urban demand drives the growth of the automated retail market in France.

Italy Automated Retail Market Analysis

Italy is expected to exhibit a notable share of the European automotive retail market during the forecast period owing to the growing focus on modernizing retail infrastructure and enhancing consumer convenience in historic urban centers. The country’s rich tourism sector creates significant opportunities for automated retail in high traffic areas such as museums, railway stations, and city squares. According to the Italian National Institute of Statistics, tourism revenues have rebounded strongly, increasing the demand for accessible and multilingual retail services. Automated kiosks offering local specialties, coffee, and quick snacks appeal to both tourists and residents seeking convenience. The Italian government’s National Recovery and Resilience Plan includes provisions for digitalizing small and medium enterprises, supporting the adoption of automated retail technologies. According to Confcommercio, the main association for trade and services in Italy, there is increasing interest among retailers in automation to address labor shortages and improve efficiency. The country’s strong coffee culture drives demand for high quality automated beverage dispensers in public spaces. Furthermore, the preservation of historic city centers limits the expansion of large retail stores, making compact automated units an ideal solution for retail access. The integration of contactless payment systems, which has accelerated in recent years, facilitates seamless transactions. This blend of tourism driven demand, regulatory support, and cultural preferences supports the steady growth of the automated retail market in Italy.

Spain Automated Retail Market Analysis

Spain is anticipated to account for a notable share of the European automotive retail market during the forecast period owing to its robust tourism industry, favorable climate, and increasing urbanization. The country is a top global tourist destination, generating high foot traffic in coastal areas, cities, and transport hubs where automated retail units thrive. According to the Spanish Ministry of Industry, Trade and Tourism, international visitor numbers have surpassed pre pandemic levels, boosting demand for convenient retail options. Automated vending machines offering beverages, snacks, and sun care products are prevalent in beach resorts and urban centers. The Spanish Retail Federation notes a growing trend towards automation in the hospitality and retail sectors to mitigate labor challenges and improve service availability. According to the National Statistics Institute, the urban population in Spain continues to grow, creating dense consumer bases for automated retail deployments. The warm climate increases demand for cold beverages and refreshments, driving sales in outdoor automated units. Furthermore, the government’s Digital Spain 2026 agenda promotes the adoption of digital technologies in commerce, providing a supportive framework for innovation. The integration of mobile payment solutions and loyalty programs enhances the appeal of automated retail to younger demographics. Collaborations between local entrepreneurs and technology providers foster the development of customized solutions for specific markets. This combination of tourism, climate, and digital advancement drives the expansion of the automated retail market in Spain.

COMPETITIVE LANDSCAPE

The competition in the Europe automated retail market is characterized by intense rivalry among established multinational corporations and innovative regional startups. Major players leverage their extensive manufacturing capabilities and global distribution networks to maintain dominant positions while niche firms focus on specialized technologies and customized solutions. The market exhibits high barriers to entry due to significant capital requirements for research and development and compliance with strict regulatory standards. Companies differentiate themselves through technological superiority ease of integration and superior customer service. Strategic alliances between hardware manufacturers and software developers are common as they seek to offer comprehensive end to end solutions. The rapid pace of technological advancement necessitates continuous investment in innovation to stay ahead of competitors. Pricing pressure from large retail chains influences competitive dynamics prompting firms to demonstrate clear value propositions through cost savings and efficiency gains. The emphasis on sustainability and energy efficiency has become a key differentiator with companies competing to offer eco friendly options. Intellectual property protections encourage innovation but also lead to legal disputes over proprietary technologies. Market participants must navigate complex regulatory landscapes varying across different European countries. This dynamic environment drives consolidation as larger entities acquire smaller innovators to enhance their portfolios. Ultimately the focus remains on delivering seamless convenient and secure shopping experiences to consumers through advanced automated retail technologies.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe automated retail market include

- Diebold Nixdorf

- NCR Corporation

- Zebra Technologies Corporation

- Honeywell International Inc.

- Toshiba Global Commerce Solutions

- Fujitsu Limited

- KUKA AG

- Azkoyen Group

- Crane Co.

- Sanden Holdings Corporation

- Glory Ltd.

- Ingenico Group

- Posiflex Technology Inc.

- Evoke Creative Limited

- Oleaph Group

Top Players in the Europe Automated Retail Market

SandenVendo International Inc.

SandenVendo International Inc. stands as a global leader in vending machine manufacturing with a significant presence in the European automated retail sector. The company specializes in producing high quality refrigerated and ambient vending units that cater to diverse consumer needs across various industries. Its extensive product portfolio includes smart vending machines equipped with advanced telemetry systems for real time inventory management and remote monitoring. SandenVendo recently launched energy efficient models compliant with strict European environmental regulations enhancing its appeal to sustainability conscious operators. The company actively collaborates with local distributors to expand its service network and ensure timely maintenance support. By integrating cashless payment technologies and interactive touch screens SandenVendo improves user experience and operational efficiency. These innovations enable retailers to offer personalized promotions and gather valuable consumer data. The firm continues to invest in research and development to introduce novel features such as age verification systems for restricted products. This commitment to technological advancement and customer satisfaction solidifies its reputation as a trusted partner in the European market. SandenVendo’s strategic focus on reliability and innovation drives its continued growth and influence in the automated retail landscape.

Crane Payment Innovations

Crane Payment Innovations is a prominent provider of payment solutions and vending technologies serving the Europe automated retail market with cutting edge hardware and software. The company offers a comprehensive range of cashless payment devices card readers and bill validators that facilitate seamless transactions for consumers. Its integration of mobile wallet compatibility and contactless payment options aligns with the growing preference for digital payments in Europe. Crane Payment Innovations recently enhanced its suite of telemetry services enabling operators to monitor machine performance and sales data in real time. This capability allows for proactive maintenance and optimized restocking schedules reducing downtime and operational costs. The company also focuses on security features to protect against fraud and ensure safe transactions for users. By partnering with major vending operators and manufacturers Crane Payment Innovations expands its reach and influence in the region. Its dedication to interoperability ensures that its solutions work seamlessly with various vending platforms and systems. This flexibility makes it an attractive choice for retailers seeking to upgrade their existing infrastructure. Through continuous innovation and strategic partnerships Crane Payment Innovations strengthens its position as a key enabler of modern automated retail experiences in Europe.

Azkoyen Group

Azkoyen Group is a leading international company specializing in automated retail solutions with a strong footprint in the European market. The company designs and manufactures innovative vending machines coffee stations and self service kiosks tailored to meet specific client requirements. Azkoyen emphasizes sustainability by developing energy efficient appliances that reduce environmental impact and operating costs. Its recent initiatives include the introduction of smart connectivity features allowing for remote diagnostics and dynamic pricing capabilities. The group actively engages in collaborations with food and beverage brands to create customized vending experiences that enhance brand visibility and consumer engagement. Azkoyen’s focus on user centric design ensures intuitive interfaces and reliable performance across its product range. The company also provides comprehensive after sales support including training and maintenance services to ensure optimal operation of its equipment. By leveraging advanced technologies such as Internet of Things and data analytics Azkoyen helps operators improve efficiency and profitability. Its commitment to quality and innovation has earned it a reputation for excellence in the industry. Azkoyen continues to expand its presence in Europe by adapting to local market trends and regulatory requirements. This strategic approach enables the company to deliver value added solutions that meet the evolving needs of the automated retail sector.

Top Strategies Used by Key Market Participants

Key players in the Europe automated retail market primarily focus on technological innovation to enhance user experience and operational efficiency. Companies invest heavily in integrating artificial intelligence and Internet of Things capabilities into their vending machines and kiosks. This enables real time inventory tracking predictive maintenance and personalized marketing strategies. Strategic partnerships with technology providers and retail chains are common to expand distribution networks and access new customer segments. Manufacturers prioritize sustainability by developing energy efficient models that comply with stringent European environmental regulations. Product diversification is another critical strategy with firms offering specialized solutions for various sectors such as healthcare education and hospitality. Enhancing payment security and supporting multiple cashless options remain top priorities to meet consumer preferences. Companies also emphasize after sales support and maintenance services to build long term relationships with clients. Geographic expansion into emerging markets within Europe helps capture untapped demand. Continuous research and development efforts drive the creation of novel features such as facial recognition and voice activation. These multifaceted strategies enable market participants to maintain competitive advantages and adapt to changing consumer behaviors. By focusing on innovation sustainability and customer centric solutions key players strengthen their market positions and drive growth in the dynamic European automated retail landscape.

MARKET SEGMENTATION

This research report on the Europe automated retail market has been segmented and sub-segmented based on the following categories.

By Type

- Hardware

- POS System

- Self-checkout System

- RFID and Barcode Scanners

- Other Hardware Types

- Software

By End User

- Grocery

- General Merchandise

- Hospitality

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com