Europe Aviation Leasing Market Size, Share, Trends & Growth Forecast Report, Segmented By By lease Term, Type, Lessee Type, Aircraft, Lease Structure And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Aviation Leasing Market Size

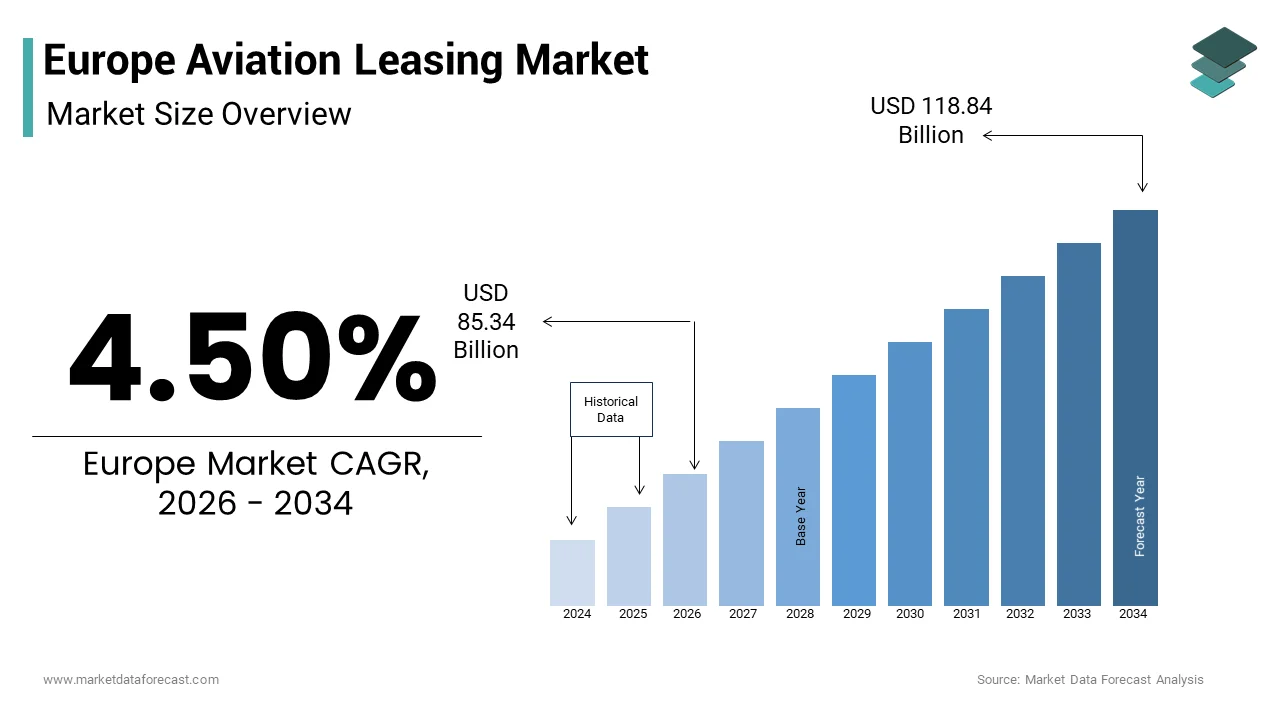

The Europe aviation leasing market size was valued at USD 81.65 billion in 2025 and is anticipated to reach USD 85.34 billion in 2026 to reach USD 118.84 billion by 2034, growing at a CAGR of 4.50% during the forecast period from 2026 to 2034.

Introduction and Market Definition

Aviation leasing is a financing arrangement where an aircraft owner (lessor) allows an airline or operator (lessee) to use an aircraft for a specific period in exchange for regular rent payments, without transferring ownership. This market serves as a critical liquidity mechanism enabling carriers to expand fleets without the substantial capital expenditure associated with direct purchases. Lessors in this domain provide operational and finance leases facilitating fleet modernization and capacity management for both legacy carriers and low cost operators. The strategic importance of this sector is underscored by the high proportion of leased aircraft in European fleets which allows airlines to maintain flexibility amidst fluctuating demand and regulatory shifts. According to Eurostat, the total number of air passengers in the EU reached 973 million in 2023 (a 19% increase from 2022) and further climbed to 1.1 billion in 2024. This growth, which now exceeds 2019 pre-pandemic levels, is driving demand for flexible fleet solutions to manage rising traffic volumes. Furthermore, as per the International Air Transport Association (IATA), the proportion of leased aircraft in the global fleet has stabilized at approximately 58-60%. This trend is heavily anchored in Europe, where Ireland-based entities alone manage over 60% of the global leased fleet, supported by major hubs in the UK and Ireland. The European Green Deal imposes stringent sustainability targets requiring airlines to replace older inefficient aircraft with newer fuel efficient models a transition heavily supported by leasing structures. As per the European Commission the Fit for 55 package aims to reduce net greenhouse gas emissions by at least 55 percent by 2030 driving the need for rapid fleet turnover. Hence, the aviation leasing market acts as an essential enabler of environmental compliance and operational agility in the European aerospace landscape.

MARKET DRIVERS

Accelerated Fleet Modernization Driven by Environmental Regulatory Compliance

The imperative to comply with stringent environmental regulations serves as a top accelerator for the Europe aviation leasing market. The European Union’s Fit for 55 package and the ReFuelEU Aviation initiative mandate significant reductions in carbon emissions compelling airlines to retire older fuel inefficient aircraft and replace them with next generation models such as the Airbus A320neo and Boeing 737 MAX. These newer aircraft offer better fuel efficiency and lower noise footprints which are critical for meeting operational standards at noise restricted European airports. According to the European Environment Agency the aviation sector must reduce its carbon intensity significantly to align with the bloc’s climate neutrality goals by 2050. Leasing provides airlines with the financial flexibility to access these capital intensive assets without depleting cash reserves. The International Air Transport Association notes that replacing older generations of aircraft is the most immediate way for airlines to reduce their carbon footprint. Furthermore lessors are increasingly incorporating sustainability linked loans and green leasing structures which incentivize lessees to operate cleaner fleets. The European Commission emphasizes that a substantial portion of the current European short-haul fleet consists of older-generation aircraft, identifying accelerated fleet renewal as a primary lever for achieving fuel efficiency and noise reduction. This regulatory pressure creates a sustained demand for modern aircraft through leasing channels as carriers seek to balance compliance costs with operational viability. The ability of lessors to absorb residual value risk and provide upgrade pathways makes leasing the preferred strategy for many European airlines navigating the green transition.

Resurgence in Passenger Traffic and Capacity Expansion Needs

The robust recovery of passenger traffic following the pandemic induced downturn has significantly driven demand in the Europe aviation leasing market. Airlines are urgently expanding capacity to meet pent up travel demand and restore connectivity across domestic and international routes. Eurostat confirms that air travel within the European Union has achieved a full recovery, with passenger volumes now matching or exceeding the levels recorded prior to the global health crisis. This surge in demand requires rapid fleet expansion which is often more achievable through leasing than purchasing due to shorter lead times and preserved capital. The International Civil Aviation Organization (ICAO) reports that international flight activity has successfully stabilized following the pandemic, supported by a strong resurgence in travel demand across major global regions. Low cost carriers in particular are leveraging operating leases to scale their operations quickly and capture market share. The European Low Fares Airline Association (ELFAA) indicate that budget carriers continue to gain market share, driven by a consistent increase in passenger demand for affordable point-to-point air travel across the continent. Leasing allows these carriers to adjust fleet size dynamically in response to seasonal variations and route profitability. Additionally the shortage of new aircraft deliveries from manufacturers has increased the value of existing leased assets prompting airlines to extend leases or acquire used aircraft through sale and leaseback transactions. This supply constraint further amplifies the role of lessors in maintaining network stability. The combination of strong demand and supply chain bottlenecks ensures that leasing remains a vital tool for capacity management in the European aviation sector.

MARKET RESTRAINTS

Supply Chain Disruptions and Aircraft Delivery Delays

Persistent supply chain disruptions and prolonged delivery delays from original equipment manufacturers continue to be a major obstacle to the Europe aviation leasing market. Lessors rely on timely delivery of new aircraft to fulfill lease commitments and refresh their portfolios. However industrial challenges including labor shortages raw material scarcity and production quality issues have extended waiting times for new narrow body and wide body aircraft. Research confirms that delivery slots for popular single-aisle aircraft are sold out for nearly a decade, creating a long-term bottleneck that forces lessors and airlines to fundamentally restructure their fleet expansion strategies. Boeing has similarly faced production constraints affecting its 737 MAX and 787 Dreamliner programs. The International Air Transport Association emphasizes that these delays force airlines to keep older aircraft in service longer than planned increasing maintenance costs and reducing operational efficiency. For lessors this uncertainty complicates asset management and residual value projections. ASD Europe warns that the aerospace supply chain remains fragile, with smaller sub-tier suppliers facing heightened insolvency risks due to the volatile combination of rising costs and inconsistent production demands. This instability limits the ability of lessors to offer competitive lease rates and flexible terms. Furthermore the scarcity of available aircraft drives up lease rates which can strain airline budgets and dampen demand for new leases. The inability to secure timely deliveries also hinders the replacement of older less efficient aircraft slowing progress toward environmental goals. Manufacturing capacities must stabilize first. Until then, the leasing market faces limited growth and portfolio optimization.

Volatility in Interest Rates and Financing Costs

The volatility in interest rates and rising financing costs also slow the expansion of the European aviation leasing market. Lessors typically operate with high leverage ratios relying on debt financing to acquire aircraft. Central banks like the European Central Bank and the Bank of England are raising interest rates to combat inflation. Consequently, the cost of borrowing for lessors has increased substantially. The European Central Bank notes that while the aggressive rate hikes of the past have stabilized, the broader financial environment retains a focus on tighter monetary conditions compared to the pre-pandemic era, influencing the long-term cost of borrowing for capital-intensive industries. Higher financing costs are often passed on to airlines in the form of increased lease rates which can reduce the attractiveness of leasing compared to other funding options. Reports from major lessors like AerCap indicate that the higher cost of debt is compressing net interest margins, prompting a more disciplined approach to portfolio growth and lease rate pricing. Furthermore uncertainty about future rate trajectories makes long term financial planning difficult for both lessors and lessees. the Aviation Leaders Report observes that banks have adopted a more conservative stance toward aviation financing, prioritizing lending to top-tier credits and newer asset types to mitigate portfolio risk. This tightening restricts access to affordable capital for smaller lessors and airlines potentially consolidating the market around larger players with stronger balance sheets. The increased cost of hedging against currency and interest rate fluctuations further adds to operational expenses. These financial pressures constrain the growth potential of the leasing market and may lead to a slowdown in new transaction volumes as stakeholders navigate a more expensive capital environment.

MARKET OPPORTUNITIES

Growth of Sale and Leaseback Transactions for Capital Optimization

The increasing prevalence of sale and leaseback transactions creates a new pathway for the growth of the Europe aviation leasing market. Airlines are increasingly selling their owned aircraft to lessors and leasing them back to unlock trapped capital and improve liquidity. This strategy allows carriers to strengthen their balance sheets and invest in other strategic priorities such as digital transformation or sustainable aviation fuel initiatives. According to the International Air Transport Association many European airlines are prioritizing cash preservation and debt reduction in the post pandemic era making sale and leaseback an attractive option. Lessors benefit from acquiring well maintained assets with established lease histories reducing acquisition risk. The European Central Bank’s monetary policy environment has made equity raising challenging for airlines further driving interest in asset monetization. Research indicates that while the market for aircraft acquisitions remains diverse, the preference for various leasing structures fluctuates based on global interest rate environments and the availability of traditional commercial bank debt. This trend is expected to continue as airlines seek flexibility in managing their fleet composition without committing long term capital. Furthermore, the secondary market for aircraft is becoming more liquid providing lessors with exit opportunities. The ability to structure these deals with flexible terms including maintenance reserves and end of lease conditions creates value for both parties. Sale and leaseback remains a key mechanism for optimizing capital structures in European aviation, driven by persistent financial pressures. This trend offers robust growth prospects for lessors.

Expansion into Sustainable Aviation and Green Leasing Structures

The transition toward sustainable aviation exhibits a lucrative opportunity for the Europe aviation leasing market. This growth is propelled by the development of green leasing structures and financing for eco-friendly aircraft. Investors and regulators are increasingly focusing on environmental social and governance criteria driving demand for sustainable investment products. Lessors can capitalize on this trend by offering sustainability linked leases where rental rates are tied to the environmental performance of the aircraft or the airline’s carbon reduction targets. According to the European Commission the ReFuelEU Aviation initiative mandates increasing blends of sustainable aviation fuels creating a market for efficient aircraft that can optimize fuel consumption. Lessors who specialize in acquiring and leasing next generation fuel efficient aircraft position themselves as partners in their clients’ sustainability journeys. Reports from major credit rating agencies observe a significant uptick in aviation lessors utilizing green financing and sustainability-linked instruments, reflecting a broader shift toward ESG-compliant investment in the aerospace sector. As per the European Investment Bank there is substantial capital available for projects that contribute to climate objectives including aviation modernization. By structuring leases that support the adoption of hybrid electric or hydrogen ready aircraft in the future lessors can differentiate themselves in a competitive market. Furthermore, providing data and analytics on aircraft emissions helps airlines meet reporting requirements. This alignment with regulatory and investor expectations opens new revenue streams and strengthens customer relationships in the evolving European aviation landscape.

MARKET CHALLENGES

Residual Value Risk Amidst Technological Obsolescence

Managing residual value risk remains a serious limitation for the Europe aviation leasing market. This is because technological advancements and regulatory changes are threatening the long term value of existing aircraft assets. Lessors must accurately predict the future worth of aircraft over lease terms that can span 10 to 12 years. However the rapid introduction of more fuel efficient models and stricter emission regulations can render older aircraft economically obsolete before the end of their physical life. Acumen Aviation emphasize that estimating the future worth of aircraft is becoming increasingly difficult as overlapping environmental mandates and shifts in asset demand create a highly unpredictable regulatory landscape for lessors. The European Union’s carbon pricing mechanism under the Emissions Trading System increases operating costs for older less efficient aircraft reducing their appeal to lessees. As per the European Environment Agency carbon prices have remained elevated increasing the total cost of ownership for legacy fleets. This dynamic pressures lease rates for older models and increases the risk of early returns or defaults. Lessors may face difficulties remarketing aircraft that do not meet emerging environmental standards leading to potential write downs. Furthermore the unpredictability of future technology breakthroughs such as hybrid electric propulsion adds another layer of complexity to asset valuation. The challenge is compounded by the limited secondary market for older aircraft in regions with strict noise and emission rules. Lessors must continuously refine their risk management strategies and diversify portfolios to mitigate the impact of technological obsolescence on asset values.

Geopolitical Instability and Sanctions Impacting Asset Recovery

Geopolitical instability and the imposition of international sanctions create significant challenges for the European aviation leasing market. This is particularly concerning with regard to asset recovery and cross-border operations. The conflict in Ukraine and subsequent sanctions against Russia have highlighted the vulnerabilities of lessors with exposure to sanctioned jurisdictions. Many European lessors faced difficulties in recovering aircraft leased to Russian airlines resulting in substantial financial losses and insurance disputes. According to the European External Action Service sanctions regimes are complex and evolving creating legal uncertainties for lessors operating globally. The International Air Transport Association reports that the loss of access to the Russian market has disrupted global lease flows and increased risk premiums for other emerging markets. Research from global risk consultants confirms that insurance coverage for political risks and asset seizures has become more difficult to obtain, with insurers tightening policy terms and raising premiums in response to large-scale global losses. Lessors must now conduct enhanced due diligence and implement stricter contractual protections to safeguard their assets. The fragmentation of the global aviation market into distinct geopolitical blocs complicates standard leasing practices. Furthermore the threat of retaliatory measures by other nations poses ongoing risks to asset security. Lessors are reassessing their geographic exposure and diversifying portfolios to reduce concentration risk. The need for robust legal frameworks and international cooperation to enforce lease agreements remains a critical challenge. Until geopolitical tensions ease the aviation leasing sector will continue to navigate a heightened risk landscape requiring careful strategic planning and risk mitigation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.50% |

| Segments Covered | By lease Term, Type, Lessee Type, Aircraft, Lease Structure, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

| Market Leaders Profiled | AerCap (IE), GECAS (US), Air Lease Corporation (US), SMBC Aviation Capital (IE), Boeing Capital Corporation (US), Avolon (IE), Nordic Aviation Capital (DK), CIT Aerospace (US), Macquarie AirFinance (AU) |

SEGMENTAL ANALYSIS

By Aircraft Insights

The narrow body aircraft segment was the largest segment in the Europe aviation leasing market and occupied a 62.1% share in 2025. This prominence of the segment is supported by the high frequency of short to medium haul flights which constitute the backbone of European air travel. The geographical proximity of major European cities favors the use of single aisle aircraft such as the Airbus A320 family and Boeing 737 series. According to sources, domestic and intra European flights accounted for a significant share of total passenger traffic in the European Union in 2023. These routes require aircraft that offer optimal fuel efficiency and lower operating costs per seat which narrow body models provide. Furthermore, the proliferation of low cost carriers across Europe has significantly increased demand for these aircraft types. Leasing companies prefer this segment due to the high liquidity and strong residual value of narrow body assets. The ability to easily redeploy these aircraft among various lessees reduces risk for lessors. Additionally the ongoing replacement of older generation models with neo and MAX variants supports continuous leasing activity. The standardization of maintenance and training for narrow body fleets further enhances their appeal to airlines seeking operational simplicity. Consequently the structural preference for point to point connectivity and cost efficient operations ensures that narrow body aircraft remain the dominant asset class in the European leasing market. The main reason for the dominance of the narrow body aircraft segment is the superior utilization rates and cost efficiency offered by these assets. European airlines operate some of the highest flight frequencies in the world with many aircraft completing six or more sectors daily. This intensive usage generates substantial revenue potential for lessors who benefit from steady lease payments. The operating economics of narrow body jets are particularly attractive in a market characterized by price sensitive consumers and intense competition. Fuel consumption per available seat kilometer is lower for modern narrow body models making them ideal for routes with moderate demand. Lessors capitalize on this demand by offering competitive lease rates for these efficient models. The large installed base also ensures a robust secondary market for parts and maintenance services reducing downtime risks. Furthermore the versatility of narrow body aircraft allows them to serve both leisure and business markets effectively. This adaptability makes them resilient to economic fluctuations as demand shifts between different travel segments. The combination of high asset turnover operational efficiency and broad market applicability cements the narrow body segment as the cornerstone of the European aviation leasing industry.

The wide body aircraft segment is estimated to register the fastest CAGR of 8.4% over the forecast period owing to the recovery of long haul international travel and the increasing demand for premium cargo capacity. As global connectivity restores airlines are expanding their intercontinental networks requiring larger aircraft with greater range and payload capabilities. Wide body leases are essential for carriers seeking to access emerging markets in Asia and Latin America without committing to permanent capital expenditure. A study notes that wide body aircraft contribute disproportionately to airline profits due to higher yield premiums in business and first class cabins. Lessors are responding to this demand by acquiring new generation wide body models such as the Boeing 787 and Airbus A350 which offer improved fuel efficiency. European lessors are well positioned to facilitate this transition by providing flexible lease structures that allow airlines to scale capacity. The scarcity of new deliveries further enhances the value of existing wide body assets in the leasing portfolio. Consequently the strategic importance of long haul connectivity and cargo operations drives the rapid expansion of this segment. The biggest push behind the rapid growth of the wide body aircraft segment is the robust recovery of long haul travel and the sustained demand for premium cargo capacity. Post pandemic travel patterns have shown a strong rebound in leisure and visiting friends and relatives traffic to distant destinations. This surge necessitates the deployment of wide body aircraft to accommodate higher passenger volumes efficiently. Additionally the belly hold cargo capacity of passenger wide body jets has become increasingly valuable as global supply chains stabilize. Research reports that air cargo revenues remain elevated supporting the economic viability of wide body operations. Lessors benefit from this trend as airlines seek to secure long term leases for these high value assets. The introduction of more fuel efficient wide body models has also reduced operating costs making them more attractive for lease. This technological advantage encourages airlines to upgrade their fleets through leasing arrangements. Furthermore the flexibility of operating leases allows carriers to manage capacity risks associated with fluctuating demand on long haul routes. The combination of passenger recovery and cargo strength ensures that the wide body segment experiences sustained high growth rates in the European leasing market.

By Lessee Insights

The airlines segment dominated the Europe aviation leasing market and accounted for a substantial share in 2025. This dominance of the segment is driven by the fundamental role of commercial passenger carriers in driving air transport demand across the continent. Full service legacy carriers and low cost operators alike rely heavily on leased aircraft to manage fleet size and composition effectively. The competitive nature of the European aviation market necessitates constant fleet renewal to offer modern comfortable and fuel efficient services to passengers. Leasing enables airlines to access the latest aircraft technologies without the burden of ownership depreciation. The ability to adjust fleet capacity in response to seasonal variations and route performance is a critical advantage provided by leasing. Furthermore regulatory requirements regarding noise and emissions compel airlines to replace older aircraft rapidly a process facilitated by leasing companies. The established relationships between lessors and major European airline groups ensure a steady flow of transactions. This deep integration of leasing into airline business models ensures that the airlines segment remains the primary driver of market activity and revenue generation in the European aviation leasing sector. The top factor boosting the dominance of the airlines segment is the strategic imperative for capital preservation and fleet flexibility. Purchasing aircraft requires significant upfront investment which can strain balance sheets and limit resources for other critical areas such as marketing and digital transformation. Leasing allows airlines to convert fixed capital costs into variable operating expenses thereby improving liquidity and return on invested capital. A study highlights that operating leases provide off balance sheet treatment for certain structures enhancing financial ratios. This financial engineering is crucial for maintaining credit ratings and accessing capital markets. Furthermore the dynamic nature of air travel demand requires airlines to adapt quickly to changing market conditions. Leasing offers the flexibility to return aircraft at the end of the lease term or extend based on performance. The ability to test new markets with leased aircraft before committing to purchase reduces strategic risk. Additionally lessors often provide maintenance support and technical management services further alleviating operational burdens. These financial and operational benefits make leasing an indispensable tool for European airlines ensuring the continued dominance of this lessee type in the market.

The cargo operators segment is anticipated to witness the fastest CAGR of 9.2% between 2026 and 2034 due to the exponential rise in e commerce and the need for dedicated freighter capacity. While passenger airlines carry significant cargo in belly holds dedicated freighters offer greater volume flexibility and reliability for time sensitive shipments. European logistics hubs such as Leipzig Frankfurt and Paris Charles de Gaulle are expanding their freighter operations to meet this demand. Leasing provides cargo operators with access to specialized aircraft such as the Boeing 777F and Airbus A330 200F without the high capital outlay of purchase. The conversion of passenger aircraft to freighters also creates opportunities for lessors to monetize older assets. Dedicated cargo carriers and integrated logistics providers are increasingly turning to leases to expand their fleets rapidly. The resilience of the cargo sector during economic downturns further enhances its appeal to lessors. As supply chains become more complex and just in time delivery expectations rise the demand for reliable air freight solutions will continue to grow. This structural shift ensures that the cargo operators segment experiences sustained high growth rates outpacing traditional passenger airline leasing in percentage terms. The key force leading the rapid growth of the cargo operators segment is the relentless expansion of e commerce and the strategic focus on supply chain resilience. Consumers increasingly expect fast and reliable delivery of goods which air freight uniquely provides. Traditional maritime shipping disruptions have also prompted businesses to diversify their logistics strategies using air freight for critical components and high value goods. Leasing allows cargo operators to scale their fleets in line with this growing demand without being locked into long term ownership commitments. The International Air Transport Association notes that yield stability in the cargo sector has improved making it a more attractive segment for lessors. Furthermore the availability of converted freighters from the passenger market provides a cost effective source of aircraft for leasing. European lessors are actively participating in this market by acquiring and leasing these converted assets. The ability to offer flexible lease terms helps cargo operators manage cyclical demand fluctuations. As digitalization and globalization continue to drive trade volumes the need for agile and scalable air cargo solutions will intensify. This trend positions cargo operators as a key growth engine for the European aviation leasing market.

By Lease Term Insights

The medium term leases segment held the majority share of 55.2% of the Europe aviation leasing market in 2025. This supremacy of the segment is credited to the balance it offers between stability for lessors and flexibility for lessees. Medium term leases typically ranging from 5 to 12 years align well with the economic life of aircraft and the strategic planning horizons of airlines. For lessors medium term leases provide predictable cash flows and reduce the frequency of remarketing efforts compared to short term agreements. A study indicates that most European airlines prefer medium term structures for their mainline fleets to ensure operational continuity. This segment also facilitates the financing of new aircraft deliveries as manufacturers often require confirmed lease placements. The stability of these agreements helps lessors secure favorable financing rates from banks and investors. Furthermore medium term leases allow for the inclusion of maintenance reserves which protect the asset value over time. This mutual benefit of risk mitigation and operational security ensures that medium term leases remain the preferred choice for the majority of aviation leasing transactions in Europe. The main reason this segment is on top is the optimal balance it strikes between financial stability and operational flexibility. Airlines require certainty in their capacity planning to negotiate slot allocations and build brand loyalty on key routes. Medium term leases provide this certainty without locking carriers into obsolete technology for the entire lifespan of the aircraft. This alignment reduces disruption and cost for both lessors and lessees. Research notes that medium term leases often include provisions for mid lease extensions or early returns giving parties additional flexibility. For lessors the longer duration amortizes acquisition costs and generates stable returns on equity. This reduced risk profile makes them attractive to institutional investors who fund leasing portfolios. Furthermore the ability to renegotiate terms or upgrade aircraft at the end of the medium term allows airlines to adapt to changing environmental regulations. This adaptability is crucial in the context of the European Green Deal which mandates continuous improvements in fleet efficiency. The combination of risk management financial predictability and strategic flexibility ensures the continued predominance of medium term leases in the market.

The short term leases segment is likely to experience the fastest CAGR of 11.5% during the forecast period. This swift expansion of the segment is propelled by the increasing need for operational flexibility amidst market volatility and supply chain uncertainties. Airlines are increasingly using short term leases to cover temporary capacity gaps caused by delays in new aircraft deliveries or unexpected spikes in demand. These leases typically lasting less than 5 years allow airlines to adjust their fleet size quickly without long term commitments. The rise of seasonal tourism in Europe also fuels demand for short term capacity during peak summer months. Lessors benefit from higher lease rates associated with short term agreements which compensate for the increased remarketing effort. The availability of mature aircraft in the secondary market supports this segment by providing ready to fly assets. Furthermore the uncertainty surrounding future fuel prices and regulatory changes makes airlines cautious about long term commitments. Short term leases offer a hedge against these risks allowing carriers to pivot strategies as conditions evolve. This demand for agility ensures that the short term lease segment experiences robust growth rates. The primary factor for the rapid growth of the short term leases segment is the combination of supply chain delays and pronounced seasonal demand spikes. Manufacturing bottlenecks have extended delivery times for new aircraft forcing airlines to bridge the gap with leased units. Research shows that airlines are increasingly relying on short term leases to maintain network integrity during these delays. In addition to supply issues the highly seasonal nature of European travel drives demand for temporary capacity. Popular tourist destinations in Southern Europe experience massive inflows of visitors during summer requiring additional aircraft for only a few months. Lessors have developed specialized products to cater to this niche offering wet leases where crew and maintenance are included. This comprehensive solution simplifies operations for airlines needing quick capacity injections. The higher yields on short term leases also attract lessors looking to maximize returns on older assets. As market volatility persists and travel patterns remain fragmented the need for flexible short term solutions will continue to expand. This structural shift towards agility ensures that short term leasing becomes an increasingly vital component of the European aviation ecosystem.

COUNTRY LEVEL ANALYSIS

Ireland Aviation Leasing Market Analysis

Ireland led the Europe aviation leasing market and captured a 45.7% share in 2025. This leading position of the segment is supported by its favorable tax regime and specialized legal framework. The country is home to the headquarters of the world’s largest lessors including AerCap and Avolon. According to the Irish Aviation Authority (IAA), Ireland serves as the primary global hub for aircraft management and leasing, with a vast portion of the world’s commercial aircraft fleet being owned or managed by entities headquartered within the country. This dominance is driven by a sophisticated ecosystem of legal financial and technical expertise tailored to the leasing industry. The Irish government has consistently supported the sector through policies that encourage foreign investment and intellectual property protection. As per the Department of Finance the aviation leasing industry contributes significantly to the national economy through employment and tax revenues. The presence of major international law firms and accounting practices facilitates complex cross border transactions. Furthermore Ireland’s membership in the European Union provides access to the single market while maintaining distinct regulatory advantages. The country’s robust double taxation treaty network enhances its attractiveness for global lessors. Despite Brexit Ireland has maintained its position as the premier jurisdiction for aircraft leasing in Europe. The concentration of talent and capital ensures that Ireland remains the undisputed center of the European leasing market driving innovation and setting industry standards.

United Kingdom Aviation Leasing Market Analysis

The United Kingdom was the next prominent country in the Europe aviation leasing market and occupied a share of 18.5% share in 2025. The growth trajectory of the UK market is driven by its historical strength in aerospace finance and the presence of major lessors in London. Despite leaving the European Union the UK remains a key player due to its deep capital markets and legal expertise. According to the UK Finance association the country hosts a significant portion of global aircraft leasing activities particularly in structured finance and securitization. London serves as a central hub for arranging syndicated loans and bond issuances for aircraft acquisitions. The English legal system is widely preferred for drafting lease agreements due to its clarity and precedence. As per the Office for National Statistics the financial and insurance activities sector continues to be a major contributor to the UK economy. The UK government has sought to maintain competitiveness through regulatory reforms post Brexit. The presence of major airlines such as British Airways and easyJet creates a strong domestic demand for leasing services. Furthermore the UK’s extensive network of air connections supports a vibrant aviation sector. The combination of financial sophistication legal reliability and operational demand ensures that the UK remains a critical pillar of the European leasing landscape.

France Aviation Leasing Market Analysis

France continues to be a noteworthy player in the Europe aviation leasing market. The market position in France is closely linked to the presence of Airbus the leading aircraft manufacturer in Europe. French lessors benefit from proximity to manufacturing facilities and strong relationships with airline customers. According to the French Ministry of Economy the aerospace sector is a strategic priority with significant government support for exports and innovation. The country is home to several prominent leasing subsidiaries of major banks and industrial groups. These entities leverage their balance sheets to offer competitive financing solutions to airlines across Europe and beyond. INSEE shows that the aeronautical manufacturing sector is a major employer of highly specialized engineering and technical talent, supporting a broad ecosystem of suppliers and service providers throughout the country. The regulatory environment in France emphasizes sustainability driving the development of green leasing products. French lessors are active in promoting the adoption of fuel efficient aircraft in line with national climate goals. Furthermore the strong presence of Air France KLM provides a stable base of domestic demand. The integration of industrial manufacturing with financial services creates a unique ecosystem in France. This synergy ensures that the country remains a significant contributor to the European aviation leasing market.

Germany Aviation Leasing Market Analysis

Germany grew steadily in the Europe aviation leasing market due to the strength of its banking sector and the presence of major industrial conglomerates. German banks and financial institutions are active participants in aircraft financing and leasing often through specialized subsidiaries. According to the German Federal Bank the country’s financial sector provides substantial liquidity for aviation assets. The presence of Lufthansa Group one of Europe’s largest airline operators creates significant demand for leasing services. German lessors often focus on high quality assets and long term relationships with reputable carriers. As per the Federal Statistical Office the transport and storage sector is a key component of the German economy. The country’s emphasis on engineering excellence and reliability extends to its leasing practices. German lessors are known for rigorous asset management and maintenance oversight. Furthermore the government’s support for sustainable aviation fuels and technologies influences leasing strategies. The integration of environmental criteria into financing decisions is becoming more common. The combination of financial depth industrial strength and operational demand ensures that Germany plays a vital role in the European leasing market.

Spain Aviation Leasing Market Analysis

Spain is anticipated to expand significantly in the Europe aviation leasing market from 2026 to 2034 owing to its status as a major tourism destination and the presence of large leisure carriers. Airlines such as Iberia and Vueling rely on leasing to manage seasonal capacity fluctuations and fleet modernization. The Spanish State Aviation Safety Agency (AESA) manages one of Europe's busiest aviation networks, ensuring that the high volume of international and domestic flights, the majority of which are operated by commercial carriers, adheres to strict safety and operational standards. The tourism sector’s sensitivity to economic cycles makes leasing an attractive option for managing risk. Spanish lessors and banks are increasingly active in the market providing localized financing solutions. As per the National Statistics Institute tourism contributes significantly to GDP driving demand for air connectivity. The strategic location of Spain as a gateway to Latin America also enhances its importance. Spanish lessors often facilitate connections between European and Latin American markets. The government’s investment in airport infrastructure supports the growth of the aviation sector. Furthermore the adoption of new technologies and sustainable practices is gaining momentum. The combination of tourism driven demand financial development and strategic positioning ensures that Spain remains a key market for aviation leasing in Europe.

COMPETITIVE LANDSCAPE

The competition in the Europe aviation leasing market is intense and characterized by the presence of large global lessors alongside specialized regional players. Major companies compete based on the quality and age of their aircraft fleets access to capital and ability to offer flexible leasing structures. The market is consolidated with a few key players holding significant influence due to their scale and financial strength. Competition is driven by the need to secure orders for new fuel efficient aircraft from manufacturers which are in high demand due to supply chain constraints. Lessors differentiate themselves through superior customer service technical support and innovative financing solutions tailored to airline needs. The entry of new competitors is limited by high capital requirements and regulatory barriers creating a moat for established firms. However competition remains fierce for prime assets and creditworthy lessees. Pricing pressure exists as lessors vie for market share while managing rising interest rates and operational costs. Strategic partnerships with airlines and manufacturers are crucial for maintaining competitive advantage. The focus on sustainability and environmental governance is becoming a key differentiator as regulators and investors prioritize green initiatives. Companies that adapt quickly to changing market conditions and regulatory landscapes are best positioned to succeed in this dynamic environment.

KEY MARKET PLAYERS

A few of the market players tht are dominating the Europe aviation leasing market are

- AerCap (IE)

- GECAS (US)

- Avolon Holdings Limited

- Air Lease Corporation (US)

- SMBC Aviation Capital (IE)

- Boeing Capital Corporation (US)

- Avolon (IE)

- Nordic Aviation Capital (DK)

- CIT Aerospace (US)

- Macquarie AirFinance (AU)

Top Players In The Market

- AerCap Holdings N.V. stands as a dominant force in the Europe aviation leasing market with its global headquarters located in Dublin Ireland. The company manages the largest fleet of aircraft engines and helicopters worldwide serving a diverse client base of airlines and cargo operators. AerCap recently strengthened its market position through the successful integration of GE Capital Aviation Services which significantly expanded its portfolio and technical capabilities. This strategic move allows AerCap to offer comprehensive lifecycle solutions including parts distribution and maintenance services. The company focuses on acquiring fuel-efficient next-generation aircraft to meet evolving environmental regulations and customer demands. AerCap leverages its scale to secure favorable financing terms and optimize asset utilization across global markets. Its robust balance sheet and access to capital markets enable continuous fleet renewal and growth. By prioritizing operational excellence and customer relationships AerCap maintains its leadership status. The company’s ability to navigate market cycles and provide flexible leasing solutions ensures its continued influence in shaping the European and global aviation leasing landscape.

- Avolon Holdings Limited is a leading global aircraft leasing company headquartered in Dublin Ireland with a significant presence in the European market. The company owns and leases modern fuel efficient aircraft to airlines around the world focusing on long term partnerships and value creation. Avolon recently enhanced its market position by expanding its order book with major manufacturers such as Airbus and Boeing for next generation narrow body and wide body aircraft. This strategy ensures a steady supply of desirable assets for lessees seeking to modernize their fleets. Avolon also invests in sustainable aviation initiatives including the exploration of alternative fuels and carbon offset programs. The company utilizes advanced data analytics to optimize asset management and predict market trends effectively. Its strong financial backing from Bohai Leasing provides stability and resources for strategic acquisitions. Avolon’s commitment to innovation and customer service distinguishes it in a competitive industry. By maintaining a young and efficient fleet Avolon supports airlines in achieving their operational and sustainability goals. This focus on quality and reliability reinforces its reputation as a key player in the European aviation leasing sector.

- Air Lease Corporation is a prominent aircraft leasing company with a substantial footprint in the European market despite being headquartered in the United States. The company specializes in purchasing new commercial jet aircraft and leasing them to airlines globally. Air Lease has strengthened its position in Europe by securing significant orders for fuel efficient aircraft from Airbus and Boeing which are highly sought after by European carriers. The company’s strategy involves placing aircraft with high quality airlines on long term leases ensuring stable cash flows and asset preservation. Air Lease recently expanded its team in Europe to better serve local clients and manage regional operations effectively. The company focuses on maintaining a modern fleet with low environmental impact aligning with European regulatory standards. Its strong relationships with manufacturers allow for preferential delivery slots which are valuable in a supply constrained market. Air Lease’s disciplined approach to capital allocation and risk management supports sustainable growth. By providing reliable access to new technology aircraft Air Lease helps European airlines improve efficiency and reduce emissions. This strategic alignment with market needs ensures its continued relevance and success in the European aviation leasing industry.

Top Strategies Used By The Key Market Participants

Key players in the Europe aviation leasing market primarily focus on fleet modernization by acquiring fuel efficient next generation aircraft to meet environmental regulations and airline demand. Companies strategically pursue mergers and acquisitions to expand their asset base and achieve economies of scale in operations and financing. They also emphasize diversifying their portfolios across different aircraft types and geographies to mitigate risks associated with market volatility. Lessors increasingly engage in sale and leaseback transactions with airlines to provide liquidity while securing long term lease agreements. Another major strategy involves developing sustainable financing instruments such as green bonds to attract environmentally conscious investors and reduce capital costs. Market participants also invest in digital technologies and data analytics to enhance asset management efficiency and predict maintenance needs accurately. Building strong relationships with manufacturers ensures priority access to new aircraft deliveries which are critical for maintaining competitive advantage. These multifaceted strategies enable lessors to navigate complex market dynamics and sustain growth in the European region.

MARKET SEGMENTATION

This research report on the Europe aviation leasing market is segmented and sub-segmented into the following categories.

By Lease Term

- Short-term leases (less than 5 years)

- Medium-term leases (5-12 years)

- Long-term leases (more than 12 years)

By Type

- Operating leases

- Finance leases

- Sale and leaseback

By Lessee Type

- Airlines

- Cargo operators

- Other lessees

By Aircraft

- Narrow-body aircraft

- Wide-body aircraft

- Regional aircraft

By Structure

- Fixed-rate leases

- Variable-rate leases

- Hybrid leases

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe aviation leasing market?

Increasing reliance on leased aircraft and flexible fleet management is driving market growth.

Why are airlines in Europe opting for leasing instead of buying aircraft?

Leasing reduces upfront capital costs and provides operational flexibility.

How would you explain aviation leasing in simple terms?

It is a system where airlines rent aircraft instead of owning them.

Where is aviation leasing most commonly used across Europe?

It is widely used by commercial airlines for short-term and long-term fleet expansion.

What makes aviation leasing important for modern airline operations?

It allows airlines to adjust fleet size based on demand and market conditions.

From a financial standpoint, is aircraft leasing a strategic choice?

Yes, it helps airlines manage costs and improve cash flow efficiency.

What challenges are affecting the Europe aviation leasing market?

Regulatory complexities and high maintenance costs are key challenges.

How is air travel demand influencing this market?

Growing passenger traffic is increasing demand for leased aircraft solutions.

Which leasing models are most common in this market?

Operating leases and ACMI (Aircraft, Crew, Maintenance, Insurance) leases are widely used.

Is the Europe aviation leasing market growing steadily?

Yes, it is expanding with increasing adoption of leasing across airline fleets.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com