Europe Bio Ethanol Market Size, Share, Trends & Growth Forecast Report Segmented By Feedstock (Wheat, Corn, Sugar Beet, Barley, Lignocellulosic Residues (Straw, Corn Stover)), Application, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe Bio Ethanol Market Size

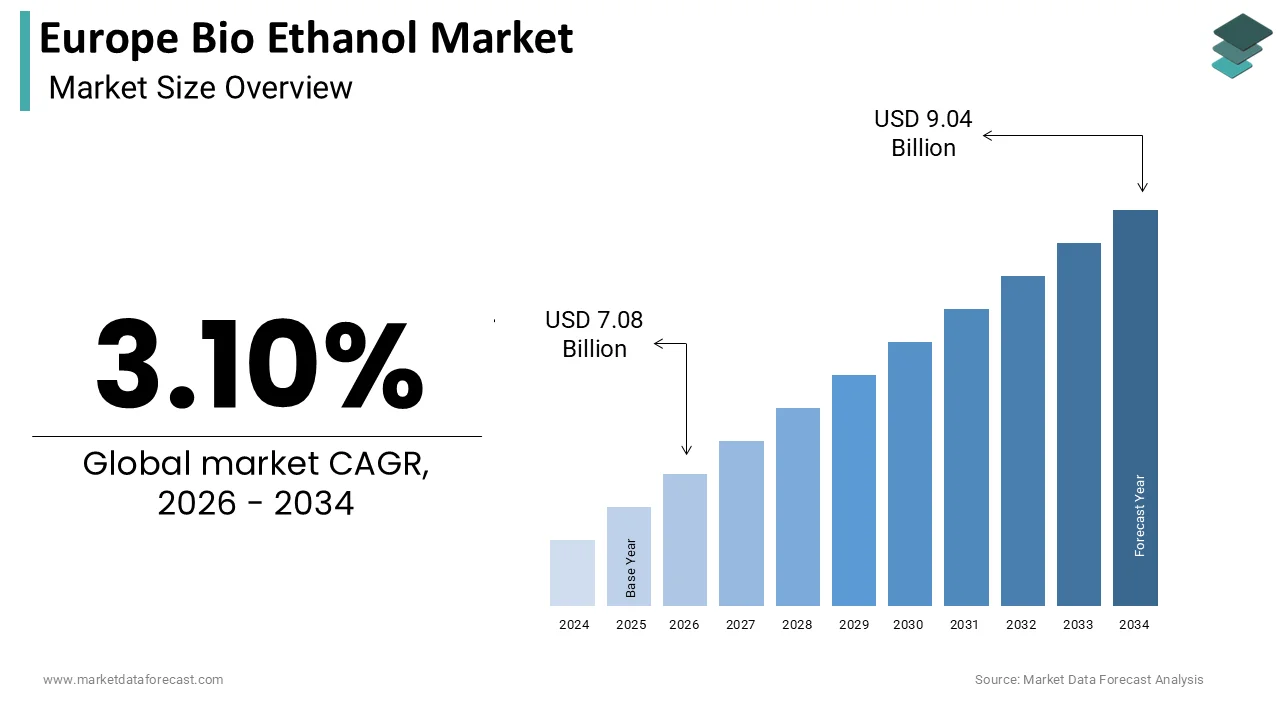

The European bioethanol market size was calculated to be USD 6.87 billion in 2025 and is anticipated to be worth USD 9.04 billion by 2034, from USD 7.08 billion in 2026, growing at a CAGR of 3.10% during the forecast period.

Bioethanol is the production and utilization of ethyl alcohol derived from biological feedstocks such as cereals, sugar beets, and lignocellulosic biomass. This colorless volatile liquid serves primarily as an oxygenating agent in gasoline blends to reduce vehicular emissions and as a foundational chemical for industrial applications ranging from cosmetics to pharmaceuticals. The sector operates under the rigorous framework of the European Union Renewable Energy Directive, which mandates specific blending targets to decarbonize the transport sector. In 2024, the European Union consumed approximately 6.8 billion liters of renewable ethanol for fuel purposes, reflecting a steadfast commitment to displacing fossil fuels, according to data from ePure. The region distinguishes itself through a strong emphasis on sustainability criteria, requiring biofuels to achieve significant greenhouse gas savings compared to conventional fossil fuels. Agricultural output remains the bedrock of this industry, with France and Germany collectively harvesting over 70 million tons of wheat annually, providing a substantial portion of the starch required for fermentation processes as per Eurostat figures. Furthermore, the industrial alcohol sector utilizes roughly 1.2 billion liters of bioethanol for non-fuel applications, driven by the growing demand for bio-based solvents in green chemistry initiatives, according to the European Chemical Industry Council.

MARKET DRIVERS

Legislative Mandates for Greenhouse Gas Reduction in Transport

The stringent legislative framework established by the European Union to curb greenhouse gas emissions within the transport sector is a major factor accelerating the growth of Europe bio ethanol market. The revised Renewable Energy Directive sets a binding target for member states to achieve a 14% share of renewable energy in transport by 2030, with specific sub-targets for advanced biofuels and a cap on food-based fuels that nonetheless secures a baseline demand for conventional ethanol. This regulatory pressure compels fuel suppliers to blend higher proportions of ethanol into gasoline to meet compliance obligations and avoid heavy financial penalties. The mechanism of double-counting for certain waste-based feedstocks further incentivizes the integration of sustainable ethanol into the fuel mix. Additionally, the ReFuelEU Aviation initiative, while focused on Sustainable Aviation Fuels, indirectly supports the ethanol value chain by promoting power-to-liquid technologies where ethanol can serve as an intermediate feedstock. The European Commission estimates that achieving these transport targets will require an annual consumption of over 8 billion liters of renewable ethanol by the end of the decade. Consequently, policy certainty acts as a powerful catalyst, ensuring consistent offtake agreements and encouraging long-term capital investment in production facilities despite fluctuating crude oil prices.

Expanding Demand for Bio-Based Solvents in Industrial Applications

The surging demand for bioethanol as a preferred solvent in the industrial, cosmetic, and pharmaceutical sectors, driven by the broader global shift toward bio-based chemicals, is also elevating the growth of Europe bio ethanol market. Manufacturers are increasingly replacing petroleum-derived solvents with bioethanol due to its lower toxicity, biodegradability, and favorable carbon footprint, aligning with corporate sustainability goals and consumer preferences for green products. The European chemical industry, which accounts for nearly 20% of global chemical sales, is actively reformulating products to meet the Ecolabel criteria and other voluntary sustainability standards that favor renewable ingredients. The pharmaceutical sector specifically relies on high-purity bioethanol for the extraction of active ingredients and the production of sanitizers, a demand stream that stabilized at elevated levels following global health crises. Furthermore, the cosmetics industry, valued at over 84 billion euros in Europe, increasingly markets products as natural or organic, necessitating the use of plant-derived alcohols rather than synthetic alternatives, as reported by Cosmetics Europe. This transition is not merely regulatory but also market-driven, as brand owners seek to differentiate their portfolios through sustainability claims. The robust growth in these downstream industries provides a stable and high-value outlet for bioethanol producers, diversifying revenue streams beyond the volatile fuel market and fostering resilience against policy shifts in the energy sector.

MARKET RESTRAINTS

Volatility in Agricultural Feedstock Prices and Supply

The extreme volatility in the prices and availability of agricultural feedstocks, particularly wheat, corn, and sugar beets, which constitute the majority of input materials, is limiting the growth of Europe bio ethanol market. These commodity prices are highly susceptible to climatic anomalies, geopolitical conflicts, and global trade dynamics, creating unpredictable cost structures for ethanol producers. The ongoing geopolitical tensions in Eastern Europe have disrupted supply chains and reduced the export of grains from the Black Sea region, leading to a 25% spike in cereal prices in 2024 compared to the previous year, according to the Food and Agriculture Organization. This inflation in raw material costs severely compresses profit margins for ethanol manufacturers, who often struggle to pass these increases downstream to fuel blenders or industrial buyers due to fixed contract terms or competitive pressures. Furthermore, the competition for arable land between food production and fuel generation remains a contentious issue, with periodic harvest failures due to droughts or floods exacerbating supply shortages. This dependency on weather-dependent crops introduces a fundamental instability to the production cycle, making long-term planning difficult and deterring potential investors who seek more predictable returns. The lack of diversified feedstock options at a commercial scale further amplifies this vulnerability, leaving the market exposed to the whims of the agricultural calendar and global grain markets.

Regulatory Constraints on Food-Based Biofuel Blending

The regulatory cap imposed on the contribution of food and feed crop-based biofuels toward the renewable energy targets in transport is another factor hampering the growth of Europe bio ethanol market. The European Union's Renewable Energy Directive II explicitly limits the share of biofuels produced from food and feed crops to a maximum of 7% of the final consumption of energy in road and rail transport, with some member states setting even lower ceilings. This policy decision, aimed at addressing the food versus fuel debate and encouraging the shift toward advanced biofuels, effectively places a ceiling on the growth potential of conventional grain-based ethanol, which currently dominates the market. As of 2025, several major member states have already approached or reached this 7% limit, thereby stifling further volume growth for traditional ethanol producers, according to analysis by the Joint Research Centre of the European Commission. The transition to advanced biofuels derived from wastes and residues is technologically complex and capital-intensive, creating a gap that current infrastructure cannot immediately fill. This regulatory uncertainty discourages new investments in first-generation production facilities and forces existing players to navigate a shrinking addressable market for their core products. The ambiguity regarding future revisions of these caps post-2030 adds another layer of risk, causing hesitation among stakeholders to commit to long-term expansion projects.

MARKET OPPORTUNITIES

Commercialization of Lignocellulosic and Waste-Based Ethanol

The accelerated commercialization of second-generation ethanol produced from lignocellulosic biomass and municipal solid waste is creating new opportunities for the growth of Europe bio ethanol market. The Revised Renewable Energy Directive provides strong incentives for these advanced biofuels, including double-counting toward national targets and specific sub-mandates that create a guaranteed market niche. Several flagship projects are coming online across the continent, such as the facility in Romania capable of producing 50 million liters of cellulosic ethanol annually from agricultural residues, signaling a shift toward industrial scalability according to the European Advanced Biofuels Flightpath. The availability of vast quantities of straw, forest residues, and organic waste in Europe provides a robust feedstock base, with estimates suggesting over 200 million tons of agricultural residues are available for energy use each year, as per Eurostat data. Technological advancements in enzymatic hydrolysis and fermentation have reduced production costs, narrowing the price gap with conventional ethanol and fossil fuels. Furthermore, the inclusion of these fuels in the ReFuelEU Aviation regulation opens up the lucrative aviation sector, where ethanol-to-jet pathways are gaining traction. Investors and policymakers view this segment as the future of the industry, offering a pathway to decarbonize hard-to-abate sectors while bypassing the food-versus-fuel controversy. Early movers in this space stand to capture significant market share and benefit from premium pricing mechanisms and government grants dedicated to green innovation.

Integration of Carbon Capture and Utilization Technologies

The integration of Carbon Capture and Utilization technologies within bio ethanol production facilities to enhance the economic viability and environmental profile is additionally expected to promote the growth of Europe bio ethanol market. Fermentation processes inherently generate high-purity carbon dioxide as a byproduct, which can be captured and either sequestered or utilized in various industrial applications, thereby creating an additional revenue stream for producers. The European Union's Innovation Fund has allocated billions of euros to support carbon capture projects, recognizing their critical role in achieving climate neutrality by 2050. Several ethanol plants in France and the Netherlands have already initiated projects to capture CO2 for use in the beverage industry, greenhouse agriculture, and the synthesis of synthetic fuels, turning a waste product into a valuable commodity, according to the Global CCS Institute. The potential to produce negative emission fuels through Bioenergy with Carbon Capture and Storage is particularly appealing, as it could allow the transport sector to offset emissions from other hard-to-decarbonize industries. The synergy between bioethanol production and carbon management not only improves the overall carbon balance of the fuel but also diversifies income sources, shielding producers from volatility in fuel and feedstock markets.

MARKET CHALLENGES

Intense Competition from Electrification in the Transport Sector

The rapid acceleration of electric vehicle adoption, which threatens to erode the long-term demand for liquid transportation fuels, is one of the challenges to the growth of Europe European bioethanol market. The European Union has mandated the cessation of sales of new internal combustion engine cars by 2035, a policy that fundamentally alters the trajectory of fuel consumption in the coming decades. The structural shift implies a peak and subsequent decline in gasoline demand, which directly impacts the volume of ethanol that can be blended into the fuel pool. While ethanol advocates argue for its role in hybrid vehicles and as a feedstock for sustainable aviation fuels, the sheer scale of the electrification push creates a looming overcapacity risk for existing production assets. Refiners and blenders are increasingly cautious about signing long-term off-take agreements for ethanol, anticipating a shrinking addressable market for road transport fuels. The challenge is compounded by the fact that the timeline for fleet turnover means the impact on fuel demand will be felt gradually but inexorably, making it difficult for the ethanol industry to justify massive new investments in first-generation capacity. Producers must urgently pivot toward non-road applications and advanced feedstocks to remain relevant in a post-combustion engine economy, a transition that requires significant technological adaptation and capital reallocation.

Complex Sustainability Certification and Administrative Burdens

The intricate web of sustainability certification schemes and administrative requirements for participants is also impeding the growth of Europe bio ethanol market. The European Union demands rigorous proof of sustainability for all biofuels to qualify for tax incentives and count toward renewable energy targets, necessitating compliance with complex criteria regarding land use, greenhouse gas savings, and biodiversity protection. Producers must adhere to voluntary schemes recognized by the European Commission, such as ISCC or REDcert, which involve extensive auditing, data collection, and chain of custody tracking from the farm to the fuel tank. The administrative burden associated with maintaining this compliance is substantial, particularly for smaller producers and farmers who may lack the resources to manage the requisite documentation and reporting systems. In 2024, the European Court of Auditors highlighted inconsistencies in the verification processes across member states, leading to increased scrutiny and tighter controls that further complicate market access, according to official EU publications. The constant evolution of these regulations, with frequent updates to calculation methodologies and sustainability thresholds, creates a moving target for compliance, increasing the risk of disqualification and financial loss. Moreover, the divergence in national implementation of EU directives leads to a fragmented regulatory landscape, where a producer compliant in one country may face barriers in another.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.10% |

| Segments Covered | By Feedstock, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | POET LLC, ADM (Archer Daniels Midland Company), Valero Energy Corporation, Tereos Group, CropEnergies AG, Verbio SE, Cristal Union, Südzucker AG, Ensus UK Limited, Abengoa Bioenergy |

SEGMENTAL ANALYSIS

By Feedstock Insights

The wheat segment was the largest by holding 42.3% of the European bioethanol market share in 2025, with the abundant agricultural output across Northern and Central Europe, where wheat serves as the most economically viable starch source for fermentation. The sheer scale of cultivation, with the European Union harvesting approximately 135 million tons of wheat annually, provides a consistent and localized supply chain that minimizes logistics costs for producers, according to a survey. The technological maturity of wheat-based fermentation processes has been refined over decades to achieve high conversion rates and yield consistency. Modern biorefineries in Europe can convert one ton of wheat into roughly 380 liters of ethanol while generating valuable co-products like dried distillers' grains with solubles (DDGS) for animal feed by enhancing overall process economics as per industry reports from ePure. The integration of these facilities into the existing agricultural infrastructure allows for flexible operations where producers can switch between fuel and beverage-grade production based on market signals.

The lignocellulosic residues segment is expected to witness the fastest CAGR of 14.2% from 2026 to 2034, with the urgent regulatory push toward advanced biofuels that do not compete with food supplies and offer superior greenhouse gas savings. The stringent mandate under the Revised Renewable Energy Directive, which sets a specific sub-target of 3.5% for advanced biofuels by 2030, creates a guaranteed market pull for cellulosic ethanol derived from straw, wood chips, and agricultural waste. The breakthrough in enzymatic hydrolysis technologies, which have significantly lowered the cost barrier for breaking down complex cellulose structures into fermentable sugars, is propelling the growth of the market. Several commercial-scale facilities, such as the flagship plant in Romania utilizing wheat straw, have demonstrated technical viability and are scaling up operations to meet rising demand. These advanced pathways offer greenhouse gas emission reductions of up to 90% compared to fossil fuels by making them eligible for double-counting mechanisms and premium pricing in carbon markets, as noted by the Joint Research Centre. Investment grants from the EU Innovation Fund further de-risk capital expenditure for these projects, positioning lignocellulosic residues as the cornerstone of the sector's sustainable future.

By Application Insights

The fuel blending segment accounted for a significant share of the European bioethanol market in 2025, with the legislative framework that mandates the mixing of renewable fuels with conventional gasoline to reduce transport emissions. The binding national targets established under the European Union Renewable Energy Directive require member states to ensure that 14% of energy in transport comes from renewable sources by 2030. In 2024, the volume of ethanol blended into transport fuels across the EU reached 6.9 billion liters, a figure that continues to rise as countries phase out pure fossil fuels, according to data from the International Energy Agency. The second driving factor is the widespread compatibility of the existing vehicle fleet with ethanol blends, with over 90% of gasoline cars in Europe certified to run on E10 blends without modification. This high penetration rate ensures that infrastructure upgrades are minimal, allowing for rapid deployment of higher blend levels. Additionally, the oxygenating properties of ethanol improve combustion efficiency and reduce particulate matter emissions, aligning with urban air quality directives that further incentivize its use in densely populated regions. The synergy between regulatory mandates and technical feasibility cements fuel blending as the primary outlet for European bioethanol production.

The cosmetics and personal care sector is anticipated to expand at a CAGR of 9.8% throughout the forecast period, with the shifting consumer paradigm toward natural, organic, and sustainably sourced ingredients in beauty and hygiene products. The escalating demand for bio-based solvents that replace petroleum-derived alternatives, driven by strict ecolabeling standards and consumer preference for green chemistry, is driving the growth of the segment. The European cosmetics market, valued at over 84 billion euros, sees brands increasingly marketing products as "vegan" and "bio-sourced," necessitating the use of ethanol derived from non-GMO and sustainable agricultural practices, according to Cosmetics Europe. The regulatory push for transparency and safety, where bioethanol is perceived as a safer and cleaner ingredient compared to synthetic alcohols, is elevating the growth of the segment. The European Chemicals Agency has tightened restrictions on certain synthetic solvents, prompting formulators to switch to bioethanol, which offers a favorable toxicity profile and biodegradability. Furthermore, the post-pandemic habit of frequent hand hygiene has sustained elevated demand for alcohol-based sanitizers, many of which now prioritize bio-based content to appeal to environmentally conscious consumers.

REGIONAL ANALYSIS

France Bio Ethanol Market Analysis

France was the top performer in the European bioethanol market with 28.4% of the share in 2025, with its vast agricultural capacity and proactive renewable energy policies. The nation leverages its status as the largest cereal producer in the European Union to maintain a robust domestic supply of wheat and sugar beets for ethanol conversion. In 2024, French biorefineries produced over 2.1 billion liters of bioethanol, utilizing approximately 6 million tons of wheat and 3 million tons of sugar beets, according to a survey. The government's Long-Term Energy Plan explicitly supports the development of advanced biofuels, providing financial incentives for plants that integrate carbon capture technologies or utilize waste feedstocks. The widespread availability of E10 and E85 fueling stations across the country facilitates high consumption rates, with bioethanol accounting for nearly 10% of total gasoline sales. Furthermore, the strong cooperation between agricultural cooperatives and industrial processors ensures a stable value chain that benefits rural economies. France also leads in research and development for second-generation ethanol, hosting several pilot projects aimed at commercializing cellulosic production. The strategic alignment of agricultural interests with climate goals creates a resilient market environment where production volumes remain high despite global commodity fluctuations.

Germany Bio Ethanol Market Analysis

Germany bio ethanol market was ranked second by holding 22.7% of the share in 2025, with its advanced processing technologies and strong industrial demand. While domestic agricultural feedstock is significant, Germany distinguishes itself through high-efficiency biorefineries that maximize yield and produce valuable co-products for the animal feed and chemical sectors. The country's Quota Act for biofuels mandates a minimum greenhouse gas reduction threshold for fuel suppliers, driving the adoption of higher-quality and more sustainable ethanol blends. The presence of major chemical conglomerates fosters innovation in downstream applications, expanding the market beyond traditional fuel blending. Additionally, the robust infrastructure for E10 and E25 blends ensures steady consumption in the transport sector.

Spain Bio Ethanol Market Analysis

Spain bio ethanol market growth is likely to witness a prominent growth opportunity in the coming years, with its favorable climate for sugar beet cultivation and its strategic focus on southern crop varieties. The Spanish market relies heavily on sugar beets and cereals, with the southern regions providing ideal growing conditions that allow for competitive feedstock costs. The government has implemented specific measures to support the beet sector, recognizing its importance for rural employment and soil rotation in dryland farming areas. The expansion of E10 blending mandates across the national fuel network has stimulated domestic consumption, reducing reliance on imports. Furthermore, Spain is emerging as a key player in the production of advanced biofuels, leveraging its abundant agricultural residues such as vine shoots and olive pomace for second-generation ethanol projects.

Poland Bio Ethanol Market Analysis

Poland bio ethanol market growth is driven by its rapidly expanding grain processing capacity and strong governmental support for energy independence. As one of the largest producers of rye and wheat in the European Union, Poland utilizes its abundant cereal surpluses to feed a growing number of domestic biorefineries. The national policy framework prioritizes the use of domestic feedstocks to reduce reliance on imported energy, aligning bioethanol production with broader security objectives. The country has also made significant strides in adopting E10 blends nationwide, creating a stable domestic demand base. Poland is increasingly focusing on the modernization of its production plants to meet higher sustainability criteria by enabling access to premium markets in Western Europe. The integration of ethanol production with combined heat and power systems enhances energy efficiency and reduces production costs. Furthermore, the proximity to major Central European markets allows for efficient logistics and distribution.

Netherlands Bio Ethanol Market Analysis

The Netherlands bio ethanol market growth is likely to grow with its role as a major trading hub and center for advanced biofuel innovation rather than solely a production giant. In 2024, the Netherlands handled over 1.5 billion liters of ethanol throughput, facilitating trade between South American producers and European consumers while also supporting domestic blending obligations, according to Statistics Netherlands. The country is a leader in the development of waste-to-energy technologies, with several pioneering projects converting municipal solid waste and industrial off-gases into ethanol. The Dutch government's aggressive climate targets have spurred investment in circular economy solutions, making the nation a testbed for novel production pathways. The presence of major oil refiners and chemical companies drives demand for high-purity bioethanol for both fuel and industrial applications. Additionally, the Netherlands acts as a blending center where ethanol is mixed with gasoline before being transported to neighboring countries via inland waterways.

COMPETITION OVERVIEW

The competition in the European bioethanol market is characterized by a dynamic interplay between large integrated agro-industrial groups and specialized independent producers who vie for dominance through technological innovation and sustainability leadership. Major players leverage their extensive agricultural networks to secure cost-effective feedstock supplies while investing heavily in advanced fermentation technologies to maximize yields and minimize environmental impact. The market landscape features intense rivalry driven by stringent regulatory requirements and fluctuating commodity prices, which force companies to constantly optimize their operational efficiency. Competitive pressure stimulates continuous innovation in second-generation ethanol production, where firms strive to commercialize cellulosic pathways that offer superior greenhouse gas savings. Pricing strategies remain critical as producers balance the need for profitability with the demands of fuel blenders and industrial buyers facing their own margin pressures. Strategic alliances with policymakers and industry associations are common tactics used to shape favorable regulatory frameworks and promote the benefits of renewable ethanol.

KEY MARKEY PLAYERS

A few major players of the European bioethanol market include

- POET LLC

- ADM (Archer Daniels Midland Company)

- Valero Energy Corporation

- Tereos Group

- CropEnergies AG

- Verbio SE

- Cristal Union

- Südzucker AG

- Ensus UK Limited

- Abengoa Bioenergy

Top Strategies Used by Key Market Participants

Key players in the European bioethanol market predominantly employ vertical integration strategies to secure reliable access to agricultural feedstocks and mitigate price volatility associated with global commodity markets. Companies frequently invest in research and development to pioneer second-generation production technologies that utilize waste biomass and avoid competition with food supplies. Strategic partnerships with automotive manufacturers and fuel retailers are common tactics to promote higher ethanol blend levels and expand infrastructure for flex-fuel vehicles. Expansion into adjacent value chains, such as animal feed production and industrial chemical synthesis, allows firms to diversify revenue streams and enhance overall process economics. Mergers and acquisitions are utilized to consolidate market positions and acquire innovative technologies rapidly. Digitalization of supply chains improves traceability and operational efficiency, ensuring transparency from farm to fuel tank.

Leading Players in the European Bioethanol Market

- Tereos stands as a preeminent European agro-industrial group specializing in the transformation of sugar beets and cereals into bioethanol and high-value co-products. The company operates a vast network of production facilities across France and Germany, serving as a critical link between local farmers and the renewable energy sector. Globally, Tereos contributes significantly to the supply of sustainable ingredients for the food and beverage industries while advancing circular economy principles through waste valorization. Recent strategic actions include substantial investments in upgrading fermentation technologies to enhance yield efficiency and reduce carbon emissions. The firm actively collaborates with agricultural cooperatives to secure a stable supply of non-GMO feedstocks, ensuring compliance with stringent European sustainability criteria. Tereos also pioneers the development of advanced biofuels from agricultural residues, positioning itself at the forefront of the second-generation ethanol revolution.

- CropEnergies AG operates as a leading independent producer of bioethanol in Europe with a strong focus on sustainability and resource efficiency. Headquartered in Germany, the company utilizes wheat and rye from regional agriculture to produce renewable fuel and protein-rich animal feed, creating a closed-loop value chain. On the global stage, CropEnergies is recognized for its adherence to rigorous certification standards and its contribution to reducing greenhouse gas emissions in the transport sector. Recent efforts to strengthen its market position include the expansion of production capacity at existing sites and the implementation of advanced energy recovery systems to minimize fossil fuel usage. The company actively engages in research partnerships to develop novel conversion processes for lignocellulosic biomass, aiming to diversify its feedstock base. CropEnergies also emphasizes transparency and traceability in its supply chain, appealing to environmentally conscious consumers and industrial buyers.

- Abengoa Bioenergy maintains a significant presence in the European bioethanol market through its advanced technological capabilities and commitment to sustainable innovation. Although headquartered in Spain, the company operates globally, leveraging its expertise in biotechnology to convert diverse biomass sources into renewable fuels and chemicals. In Europe, Abengoa focuses on the production of second-generation ethanol from agricultural residues, addressing the food versus fuel debate while maximizing environmental benefits. Recent actions to bolster its market standing include the commissioning of flagship commercial plants that demonstrate the viability of cellulosic ethanol at scale. The company actively pursues collaborations with automotive manufacturers and fuel distributors to promote high-blend ethanol fuels and sustainable aviation fuel precursors. Abengoa also invests heavily in carbon capture and utilization technologies to further reduce the carbon footprint of its operations. These forward-looking strategies position Abengoa as a pioneer in the next generation of biofuels, driving the industry toward a more sustainable and diversified future.

MARKET SEGMENTATION

This research report on the European bioethanol market has been segmented and sub-segmented based on feedstock, application & region.

By Feedstock

- Wheat

- Corn

- Sugar Beet

- Barley

- Lignocellulosic Residues (Straw, Corn Stover)

By Application

- Fuel Blending (Transportation)

- Food and Beverages (Spirits, Extracts)

- Pharmaceuticals

- Cosmetics and Personal Care

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key applications of bioethanol in Europe?

Bioethanol is mainly used as a transportation fuel additive (blended with petrol), in industrial solvents, and in alcoholic beverages.

2. What factors are driving the Europe bioethanol market growth?

Government mandates on renewable energy, rising demand for cleaner fuels, and efforts to reduce greenhouse gas emissions are major drivers.

3. What are the major raw materials used for bioethanol production in Europe?

Common feedstocks include wheat, corn, sugar beet, and lignocellulosic biomass.

4. What is the role of bioethanol in reducing carbon emissions?

Bioethanol produces lower greenhouse gas emissions compared to fossil fuels, helping meet climate targets.

5. What challenges does the Europe bioethanol market face?

Fluctuating raw material prices, the food vs fuel debate, and regulatory uncertainties are key challenges.

6. How does EU policy impact the bioethanol market?

Policies like the Renewable Energy Directive (RED II) set targets for renewable fuel usage, boosting demand.

7. What is the future outlook of the Europe bioethanol market?

The market is expected to grow steadily due to stricter emission regulations and renewable energy targets.

8. How does bioethanol compare to biodiesel?

Bioethanol is used in petrol engines, while biodiesel is used in diesel engines; both reduce emissions but differ in feedstock and application.

9. What are the environmental benefits of bioethanol?

It reduces carbon monoxide emissions, is biodegradable, and supports sustainable agriculture.

10. What role do technological advancements play in this market?

Innovations in enzyme technology and biomass conversion are improving production efficiency and reducing costs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com