Europe Board Games Market Size, Share, Trends, & Growth Forecast Report By Game Type (Monopoly, Scrabble, Chess, Others), Age Group, Sales Channel and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Board Games Market Report Summary

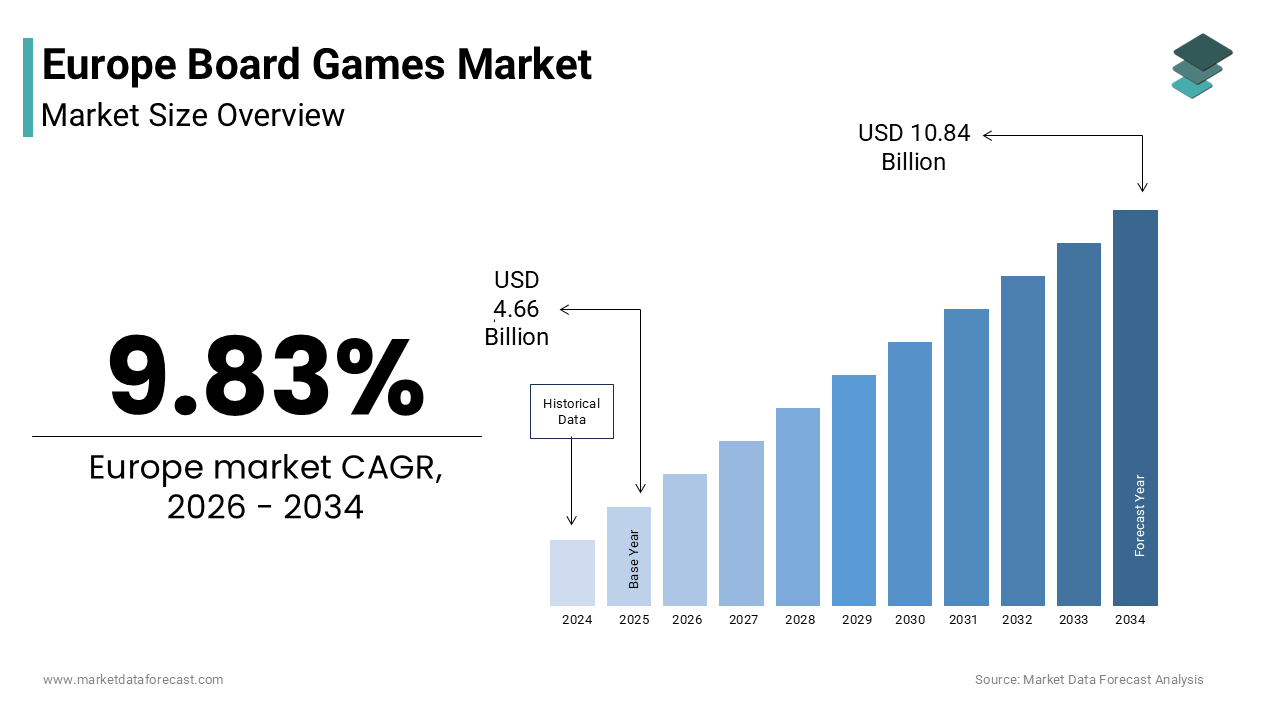

The Europe board games market was valued at USD 4.66 billion in 2025, is estimated to reach USD 5.12 billion in 2026, and is projected to reach USD 10.84 billion by 2034, growing at a CAGR of 9.83% during the forecast period from 2026 to 2034. The growth of the Europe board games market is driven by the increasing demand for offline social entertainment, rising interest in strategy and hobby games, and the growing popularity of board game cafés and community gaming spaces. Consumers across Europe are increasingly adopting board games as a means of social interaction and digital detox, creating strong demand for both family-oriented and complex strategy-based games. Moreover, the integration of board games into educational programs and cognitive development activities is further supporting market growth across households and institutions.

Key Market Trends

-

The growing popularity of strategy-based Eurogames and hobby board games among adult gaming communities.

-

Increasing adoption of board games as educational tools in schools and learning programs.

-

Expansion of board game cafés, gaming clubs, and community play spaces across major European cities.

-

Rising demand for premium and collectible board game editions among enthusiasts.

-

Integration of hybrid technologies and companion mobile apps to enhance traditional board game experiences.

Segmental Insights

- Based on game type, the others segment held the largest share of the Europe board games market in 2025. The dominance of this segment is attributed to the growing popularity of complex strategy games and modern Euro-style board games that emphasize resource management, strategic planning, and immersive gameplay experiences.

- Based on age group, the 5–12 years segment accounted for the largest share of the Europe board games market in 2025. The growth of this segment is driven by the increasing use of board games for educational purposes, family bonding activities, and cognitive development among children.

- Based on sales channel, the specialty stores segment held the major share of the Europe board games market in 2025. The dominance of this segment stems from the ability of specialty stores to provide expert recommendations, in-store demonstrations, and community gaming events that encourage product discovery and customer engagement.

Regional Insights

The Europe board games market is expanding steadily across several countries due to a strong gaming culture, rising interest in social leisure activities, and the presence of established game publishers.

-

Germany held the largest share of the Europe board games market in 2025 and is widely recognized as the birthplace of modern Euro-style board games. The country hosts major gaming conventions such as Spiel Essen and is home to leading publishers such as Ravensburger and Kosmos.

-

The United Kingdom accounted for the second-largest share of the market, supported by a strong network of specialty game stores, gaming cafés, and an active community of hobby gamers and designers.

-

France continues to play a significant role in the market due to the presence of major publishers such as Asmodee and strong government support for creative industries.

-

Italy is witnessing growing demand for strategy games and hobby gaming communities supported by gaming conventions and crowdfunding platforms for independent designers.

-

Spain is experiencing notable growth due to rising interest in social gaming activities, increasing disposable incomes, and the growing popularity of board game cafés and gaming events.

Competitive Landscape

The Europe board games market is highly competitive and characterized by the presence of both large multinational toy companies and a vibrant ecosystem of independent game publishers. Major players leverage strong distribution networks, brand recognition, and licensing agreements with popular entertainment franchises to expand their market presence. Meanwhile, smaller publishers focus on innovation, storytelling, and niche game mechanics to appeal to hobby gamers. Prominent players in the Europe board games market include Hasbro Inc., Mattel Inc., Ravensburger AG, Asmodee Group, Goliath Games, Fantasy Flight Games, Z-Man Games, Days of Wonder, Kosmos, Pegasus Spiele GmbH, HABA, and CMON Limited.

Europe Board Games Market Size

The Europe board games market size was valued at USD 4.66 billion in 2025 and is anticipated to reach USD 5.12 billion in 2026 from USD 10.84 billion by 2034, growing at a CAGR of 9.83% during the forecast period from 2026 to 2034.

Board games represent a vibrant sector dedicated to the design, production, and distribution of tabletop gaming experiences that range from traditional strategy classics to complex modern Eurogames. This industry serves as a crucial counterbalance to digital saturation by fostering face-to-face social interaction and cognitive engagement within households and community groups. The definition of the market has expanded beyond simple entertainment to include educational tools and therapeutic aids that promote mental agility and social bonding. According to Eurostat, European households continue to engage in non-digital leisure activities on a regular basis, which reflects a strong cultural foundation for tabletop gaming. As per the European Union, the creative industries sector that includes game design and publishing employs a significant number of people, underscoring the labor intensity and artistic value inherent in board game production. According to the European Commission, adults in Western Europe enjoy substantial weekly leisure time, providing ample opportunity for analogue gaming sessions. The market is characterized by a high density of independent publishers and designers who prioritize mechanical innovation and thematic depth over mass-market appeal. This ecosystem thrives on a culture of conventions and local gaming clubs that act as vital distribution and marketing channels across the continent.

MARKET DRIVERS

Resurgence of Analog Social Interaction as a Digital Detox

The growing consumer desire to disconnect from screens and engage in tangible social experiences that foster genuine human connection is a major factor propelling the expansion of the Europe board games market. In an era dominated by remote work and virtual communication, families and friend groups increasingly view board games as essential tools for reclaiming quality time without digital distractions. According to the European Consumer Organisation, many Europeans have expressed concern over excessive screen time, leading to a deliberate shift toward analog hobbies. This psychological need for a digital detox drives demand for games that require physical components, eye contact, and verbal negotiation. The trend is particularly strong among millennials and Gen Z demographics who organize dedicated game nights as a form of social ritual. As per national cultural institutes in Germany and France, participation in local board game clubs has shown notable growth, reinforcing the cultural momentum. Consumers perceive these activities as offering higher emotional value compared to passive digital consumption. The tactile nature of moving pieces and shuffling cards provides sensory satisfaction that virtual interfaces cannot replicate. This movement toward intentional unplugging ensures a steady and growing customer base willing to invest in premium physical gaming products.

Expansion of Educational Integration and Cognitive Development Programs

The widespread adoption of board games within educational curricula and child development programs across European schools and institutions is further contributing to the Europe board games market growth. Educators increasingly recognize the potential of modern board games to teach critical thinking, resource management, and collaborative problem-solving skills in an engaging format. According to the European Agency for Special Needs and Inclusive Education, a large proportion of primary schools in the region now incorporate structured gameplay into their weekly lesson plans. This institutional endorsement creates a substantial and recurring demand stream from both public and private educational sectors. Teachers utilize games to illustrate complex concepts in mathematics, history, and language arts, making learning interactive and memorable. Parents also drive this trend by purchasing educational games to supplement school learning and limit passive television viewing at home. The market responds with a surge in titles specifically designed to align with national educational standards and developmental milestones. As per research from the University of Cambridge, children who regularly play strategy games demonstrate measurable improvements in logical reasoning compared to peers who do not. This proven cognitive benefit transforms board games from mere toys into valuable educational investments, securing long-term growth for the sector.

MARKET RESTRAINTS

Escalating Production Costs and Raw Material Volatility

The sharp increase in production costs driven by the volatility of raw material prices and energy expenses is impeding the expansion of the Europe board games market. The manufacturing of board games relies heavily on paperboard, plastics, and specialized inks, all of which have seen substantial price hikes due to global supply chain disruptions and energy crises. According to Eurostat, the producer price index for paper and paper products in the European Union has risen considerably, directly impacting the cost structure of game publishers. Many small and independent studios struggle to absorb these increased costs without passing them on to consumers, which risks pricing out budget-conscious buyers. The reliance on imported components from Asia further exacerbates the issue due to fluctuating freight rates and currency exchange instability. Energy-intensive processes such as die-cutting and plastic molding have become prohibitively expensive in regions with high electricity tariffs. As per the European Game Publishers Association, a significant proportion of member companies delayed new product launches due to unfavourable cost projections. These financial pressures force publishers to reduce component quality or increase retail prices, potentially dampening consumer enthusiasm. The lack of localized manufacturing capacity for certain specialized parts leaves the industry vulnerable to external economic shocks.

Intense Competition from Digital Entertainment and Streaming Services

The fierce competition for consumer leisure time and disposable income from the rapidly evolving digital entertainment and streaming sectors is also inhibiting the regional market expansion. Video games, mobile applications, and on-demand streaming services offer instant gratification and endless content variety that often overshadows the setup time and learning curve associated with board games. According to the Interactive Software Federation of Europe, Europeans spend a significant amount of time playing video games each week, far exceeding time allocated to tabletop gaming. The convenience of accessing high-quality entertainment on smartphones and tablets makes it difficult for physical games to compete for attention, especially among younger demographics accustomed to digital interfaces. Subscription models for streaming platforms provide vast libraries of content for a low monthly fee, creating a perception of better value compared to the one-time purchase of a board game. Marketing budgets for digital titles vastly exceed those of board game publishers, dominating advertising spaces and social media algorithms. The immersive graphics and online multiplayer capabilities of video games appeal to consumers seeking high-stimulation experiences. This constant battle for share of wallet and share of time forces board game creators to work harder to justify the physical purchase and setup effort required by their products.

MARKET OPPORTUNITIES

Integration of Hybrid Technologies and Augmented Reality Features

The convergence of physical gameplay with digital technologies offers a promising opportunity for the Europe board games market to attract tech-savvy consumers and enhance immersion. Developers are increasingly incorporating augmented reality applications, companion apps, and near field communication chips into traditional board games to create hybrid experiences that blend tactile interaction with digital storytelling. According to the Fraunhofer Institute, a significant proportion of European gamers have expressed interest in hybrid games that use smartphones to unlock dynamic content or manage complex game states. This integration allows for solo play modes, automated scoring, and narrative branching that would be impossible with components alone. Publishers can update game content digitally without reprinting physical boxes, extending the lifecycle of products and reducing waste. The use of apps can also lower the barrier to entry by teaching rules interactively, addressing a common pain point for new players. Innovations such as holographic projectors and smart dice are beginning to appear in high-end titles, creating unique selling propositions. This technological evolution positions board games as modern entertainment solutions rather than relics of the past. By embracing digital tools, the market can expand its reach to demographics that previously viewed analog gaming as outdated or too complex.

Growth of Community-Based Gaming Hubs and Experiential Retail

The expansion of dedicated gaming cafes, board game libraries and experiential retail spaces offers a significant opportunity to cultivate community engagement and drive product discovery across Europe. These venues serve as physical incubators where consumers can try before they buy, fostering a deeper appreciation for the diversity of modern board games. According to the European Hospitality Association, the number of board game cafes operating in major urban centers has increased, reinforcing the role of these establishments as social hubs. They generate revenue through entry fees, food and beverage sales, and direct retail partnerships with publishers. They function as spaces that host tournaments, launch events, and learn-to-play sessions, effectively lowering the intimidation factor for newcomers. Retailers who integrate play areas into their stores see higher conversion rates as customers develop emotional connections with games during trial sessions. This model supports the sale of premium and niche titles that might struggle on traditional shelves. Local governments are increasingly supporting these initiatives as part of cultural revitalization programs that encourage social cohesion. The rise of subscription-based library services allows enthusiasts to access a rotating catalog of games for a monthly fee, reducing the financial commitment of ownership. This shift toward experience-driven consumption creates a sustainable ecosystem that nurtures long-term loyalty.

MARKET CHALLENGES

Complexity of Cross-Border Logistics and Distribution Fragmentation

The fragmented nature of logistics and distribution networks across the diverse linguistic and regulatory landscapes of the continent is primarily challenging the expansion of the Europe board games market. Unlike the unified market of the United States, Europe requires publishers to manage multiple localized editions, varying safety standards, and distinct distribution channels for each country. According to the European Logistics Association, cross-border shipping costs for bulky items like board games have increased, driven by fuel surcharges and administrative complexities. Small publishers often lack the resources to navigate the intricate web of import regulations, labeling requirements, and tax regimes in different member states. The need to produce separate rulebooks and packaging for various languages increases production lead times and inventory holding costs. Delays at customs borders can disrupt launch schedules and lead to stockouts during critical holiday seasons. The lack of a centralized pan-European distributor for niche hobby products forces many creators to rely on inefficient direct-to-consumer models. These logistical hurdles create barriers to entry for smaller innovators and limit the geographic reach of new titles. Ensuring timely and cost-effective delivery to retailers and customers remains a persistent operational headache that erodes profit margins.

Environmental Sustainability Pressures and Packaging Waste Concerns

The increasing scrutiny regarding environmental sustainability and the excessive use of plastic packaging poses a significant challenge for board game manufacturers in an eco-conscious European market. Consumers and regulators are demanding greener production methods, yet many games still rely on plastic miniatures, shrink wrap, and non-recyclable composite materials. According to the European Environment Agency, the toy and game sector contributes significantly to plastic waste, generating large amounts of packaging waste annually in the EU. Publishers face the difficult task of redesigning products to meet strict sustainability criteria without compromising durability or aesthetic appeal. Sourcing biodegradable alternatives for components often results in higher costs and limited availability, squeezing already tight margins. Greenwashing accusations can severely damage brand reputation if claims of eco-friendliness are not substantiated by credible certifications. The transition to sustainable supply chains requires substantial investment in research and development which many small studios cannot afford. Retailers are increasingly refusing to stock products with excessive plastic, forcing publishers to rethink their entire design philosophy. Balancing the desire for high-quality, visually stunning components with the imperative to reduce environmental impact remains a delicate and costly endeavour for the industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.83% |

| Segments Covered | By Game Type, Age Group, Sales Channel and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Hasbro Inc., Mattel Inc., Ravensburger AG, Asmodee Group, Goliath Games, Fantasy Flight Games, Z-Man Games, Days of Wonder, Kosmos, Pegasus Spiele GmbH, HABA, and CMON Limited. |

SEGMENTAL ANALYSIS

By Game Type Insights

The others segment led the market by capturing 56.5% of the regional market share in 2025. This dominance has shifted away from traditional classics like Monopoly or Scrabble as European consumers increasingly favor complex mechanics, high replay ability, and immersive narratives. The segment includes thousands of titles from independent publishers that cater to a sophisticated hobbyist base. European gamers, particularly in Germany and France, have cultivated a culture that values "Eurogame" design principles such as resource management, worker placement, and indirect conflict. According to the German Games Institute, sales of strategy-heavy titles have shown significant growth, outpacing traditional family games. This demographic seeks cognitive challenges and social negotiation experiences that classic mass-market games cannot provide. The rise of online communities and review platforms has educated consumers on the vast array of available options, driving demand for niche and premium products. Publishers respond by releasing games with modular boards and variable setups that ensure no two sessions are identical, enhancing long-term value. The willingness of this segment to pay higher prices for quality components and innovative designs further solidifies its market leadership. As the average player becomes more experienced, the demand for deeper gameplay continues to expand the boundaries of this category.

On the other hand, the chess segment is anticipated to showcase the fastest CAGR of 10.4% over the forecast period in this regional market. The massive surge in digital engagement that has successfully translated into increased demand for physical boards and pieces is majorly driving the growth of the chess segment in the European market. Online platforms and streaming events have democratized access to the game, creating millions of new fans who subsequently seek tangible sets for offline play and aesthetic display. According to the International Chess Federation, registered players in Europe have grown significantly, with a notable portion purchasing premium wooden sets and tournament-grade equipment. This "halo effect" from online success has revitalized the physical market, turning chess sets into desirable lifestyle objects and collectibles. High-profile tournaments broadcast globally have elevated the status of grandmasters to celebrity levels, inspiring fans to emulate their heroes. The game's perception as a tool for mental fitness has also boosted sales among adults seeking constructive hobbies. Manufacturers are responding with innovative designs ranging from minimalist modern styles to handcrafted artisan pieces, catering to this broadened appeal. The low barrier to entry combined with infinite depth ensures that new players remain engaged, driving consistent hardware sales.

By Age Group Insights

The age group between 5- and 12-years segment held the dominant position of the Europe board games market by capturing 43.1% of the European market share in 2025. The growth of the age group between 5- and 12-years segment is attributed to the pivotal role board games play in child development, family bonding, and the structured leisure time available to primary school children. In an era of screen saturation, families actively seek analogue activities that promote critical thinking, numeracy, and literacy in an engaging format. According to Eurostat, household spending on educational toys and games for children in this age bracket has increased, which is reflecting a prioritization of developmental value. Parents prefer games that align with school curricula, such as those teaching geography, history, or basic economics, ensuring that playtime contributes to academic growth. The perceived return on investment for these products is high, as they offer hours of reusable entertainment and learning. Marketing campaigns by publishers heavily emphasize these educational benefits, resonating deeply with conscientious parents. Schools often recommend specific titles for home use, further validating parental purchases. The durability and re-playability of these games make them cost-effective compared to single-use digital apps. This alignment of entertainment with educational goals secures the 5 to 12 segment as the cornerstone of market volume.

The age segment above 25 years is anticipated to record a CAGR of 9.4% over the forecast period in the European market. The "adulting" of gaming, where board games are rebranded as sophisticated social lubricants for dinner parties, date nights and hobbyist gatherings is propelling the expansion of the age segment above 25 years in the European market. No longer viewed solely as children's entertainment, modern board games offer deep narratives and strategic challenges that appeal to adult intellects and social needs. According to the European Hobby Association, attendance at adult-focused gaming conventions and local meetups has risen significantly. Adults are organizing dedicated game nights as alternatives to bar hopping or movie watching, seeking interactive and conversation-starting activities. The market responds with titles featuring intricate mechanics, historical simulations, and cooperative scenarios that require mature collaboration. This demographic has higher disposable income, allowing them to invest in premium "deluxe" editions with high-quality components. The stigma around "playing games" as an adult has largely vanished, replaced by a sense of community and identity. Social media groups and podcasts dedicated to hobby gaming further amplify this trend, creating a self-sustaining ecosystem of content and commerce. The desire for meaningful face-to-face connection in a digital world drives this demographic to seek out rich tabletop experiences.

By Sales Channel Insights

The specialty stores segment occupied the major share of 36.5% of the European market in 2025. The ability of specialty stores to provide expert curation and hands-on demonstration opportunities that are crucial for selling complex modern board games is driving the expansion of the specialty stores segment in the European market. Unlike supermarkets or general online listings, specialty staff are knowledgeable enthusiasts who can recommend titles based on specific group dynamics and preferences. According to the data from the European Retail Board Game Association, conversion rates in stores with demo tables are 45 percent higher than in those without, as customers can try before they buy. This tactile experience reduces the perceived risk of purchasing unfamiliar or expensive games. The environment of a hobby shop fosters discovery, allowing browsers to stumble upon niche titles they would never find via algorithmic recommendations. Staff expertise builds trust, encouraging customers to return for advice and new releases. The ability to host in-store events and tournaments creates a loyal local following that views the store as a community hub rather than just a transaction point. This personalized service is particularly valued by the growing segment of hobbyist gamers who seek guidance through the overwhelming array of new releases. The experiential nature of these stores transforms shopping into a leisure activity itself, driving foot traffic and sales volume.

The online/e-commerce segment is a promising segment and is estimated to witness a CAGR of 12.5% over the forecast period. Factors such as the unparalleled variety available, competitive pricing, the sophisticated logistics networks that enable rapid delivery across borders and the ability of e-commerce platforms to offer an unparalleled variety of titles, including rare, out-of-print, and international exclusives that physical stores cannot stock are driving the online segment in the European market. Online marketplaces aggregate inventory from thousands of sellers, giving European consumers access to a global catalog of board games at their fingertips. Data from Eurostat shows that 58 percent of European online shoppers purchased hobby items from cross-border sellers in 2025, seeking titles not available domestically. This infinite shelf space allows niche publishers to reach fragmented audiences across the continent without the need for extensive physical distribution networks. Consumers appreciate the ability to read detailed reviews, watch video tutorials, and compare prices instantly, empowering informed purchasing decisions. The rise of specialized online board game retailers has further professionalized the sector, offering curated bundles and subscription boxes that mimic the discovery experience of physical stores. The convenience of home delivery eliminates geographical barriers, making hobby gaming accessible to those living in rural areas far from specialty shops. As internet penetration and digital literacy continue to rise, the online channel becomes the default choice for informed buyers seeking specific or obscure titles.

REGIONAL ANALYSIS

Germany Board Games Market Analysis

Germany remained as the leader in the European board games market in 2025. Known as the birthplace of modern Euro-style board games, Germany has a deeply ingrained gaming culture that emphasizes strategy, family play, and educational value. The country hosts major international trade fairs such as Spiel Essen, which attract publishers, designers, and enthusiasts from across the globe, reinforcing its role as the hub of innovation. German households have a long tradition of incorporating board games into family life, and this cultural affinity translates into strong domestic demand. Local publishers like Ravensburger and Kosmos dominate the market, while independent designers continue to thrive through crowdfunding and niche distribution channels. With high consumer spending on leisure activities and strong export capabilities, Germany is expected to maintain its leadership position, setting trends that influence board game development across Europe.

United Kingdom Board Games Market Analysis

The United Kingdom held the second largest share of the European market in 2025. The growth of the UK in the European market is driven by a vibrant mix of traditional and modern gaming preferences. The UK market benefits from a strong retail presence, with specialist board game shops and hobby stores flourishing alongside mainstream outlets. The rise of tabletop cafés and community gaming spaces has further boosted engagement, particularly among younger demographics. British publishers such as Games Workshop have achieved global success, while independent designers contribute to a diverse ecosystem of creative titles. The popularity of role-playing and collectible card games complements the board game sector, expanding consumer interest in tabletop entertainment. Online retail and subscription models have also gained traction, making games more accessible to a wider audience. With a combination of cultural enthusiasm, innovative publishing, and strong retail infrastructure, the UK is expected to remain a major growth engine in the European board games market.

France Board Games Market Analysis

France is estimated to capture a prominent share of the Europe board games market during the forecast period owing to the strong government incentives for cultural industries and a thriving creative community. French consumers have a long-standing appreciation for board games, particularly those that emphasize storytelling, design, and artistic presentation. Local publishers such as Asmodee have become global leaders by acquiring international studios and distributing titles worldwide, which strengthens France’s influence on the global stage. The French market also benefits from a dense network of independent designers and small publishers who contribute to innovation and diversity. Board games are widely integrated into family and educational settings, reinforcing their cultural relevance. With government support for creative industries and a strong domestic appetite for innovative play, France is expected to continue modernizing its board game ecosystem, balancing tradition with cutting-edge design and maintaining its position as a resilient and influential market.

Italy Board Games Market Analysis

Italy is anticipated to hold a notable share of the Europe board games market during the forecast period. Italian market is a fragmented but increasingly modernized landscape. Italian consumers traditionally favored classic family games, but recent years have seen a surge in demand for strategy and collectible titles. Regional conventions and gaming festivals have helped foster community engagement, while local publishers are gaining recognition for creative and thematic designs. Rising disposable incomes and growing interest in leisure activities have encouraged households to invest more in board games. Additionally, Italy’s strong tourism sector has created opportunities for themed games and cultural exports, appealing to international audiences. Independent designers are increasingly using crowdfunding platforms to launch innovative projects, expanding the diversity of available titles. With modernization, cultural creativity, and international competitiveness driving demand, Italy is expected to continue its steady growth trajectory, contributing significantly to the overall expansion of the European board games market.

Spain Board Games Market Analysis

Spain is estimated to register a healthy CAGR in the Europe board games market over the forecast period due to a rapidly growing private sector and increasing consumer interest in social entertainment. Spanish households are embracing board games as a popular form of family and group activity, with younger demographics particularly drawn to strategy and cooperative play. Local publishers and distributors are expanding their reach, while international titles are widely available through both retail and online channels. The rise of board game cafés and community gaming events has strengthened engagement, creating vibrant social spaces for enthusiasts. Spain’s cultural emphasis on social interaction aligns well with the collaborative nature of modern board games, driving adoption across diverse age groups. With rising disposable incomes, growing digital retail infrastructure, and strong interest in creative leisure activities, Spain is positioned as a high-potential market with strong future growth trajectories in the European board games sector

COMPETITIVE LANDSCAPE

The competition within the Europe board games market is characterized by a dynamic tension between massive conglomerates and a vibrant array of independent publishers who drive innovation through niche specialization. Large corporations leverage their extensive distribution networks and iconic brand portfolios to dominate mass market channels and secure shelf space in major retailers. Conversely smaller studios thrive by catering to dedicated hobbyists with complex mechanics deep themes and high-quality components that appeal to discerning gamers. The rivalry extends to securing lucrative licensing deals for popular media franchises which serve as critical differentiators for attracting casual consumers. Crowdfunding has emerged as a disruptive force allowing independent creators to bypass traditional gatekeepers and compete directly for consumer attention and funding. Price competition is intense in the family segment while the hobbyist sector competes primarily on design innovation and component quality. Retailers play a pivotal role as gatekeepers prompting manufacturers to offer exclusive variants and promotional support to gain visibility. The rise of digital adaptations adds another layer of competition as companies vie for screen time alongside physical play. Talent acquisition for top designers and artists remains a key battleground as creative excellence drives commercial success in this content-driven industry.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe board games market include

- Hasbro Inc.

- Mattel Inc.

- Ravensburger AG

- Asmodee Group

- Goliath Games

- Fantasy Flight Games

- Z-Man Games

- Days of Wonder

- Kosmos

- Pegasus Spiele GmbH

- HABA

- CMON Limited

Top Players in the Europe Board Games Market

Asmodee Group

Asmodee Group stands as a preeminent force in the Europe board games market by aggregating a vast portfolio of beloved franchises and independent publishers under one corporate umbrella. The company contributes globally by standardizing distribution networks and localization processes that bring diverse European titles to international audiences with speed and quality. Recent actions to strengthen their market position include strategic acquisitions of niche studios specializing in legacy games and role-playing systems to broaden their catalog appeal. They have heavily invested in digital adaptation tools that allow physical games to be played on tablets, bridging the gap between analog and digital entertainment. By fostering direct relationships with local communities through sponsored events and conventions Asmodee ensures brand loyalty remains high. Their focus on sustainable manufacturing practices also aligns with growing consumer demand for eco-friendly products. This comprehensive approach solidifies their reputation as a guardian of gaming culture while driving innovation in game mechanics and storytelling.

Ravensburger

Ravensburger operates as a cornerstone of the Europe board games market leveraging its centuries-old heritage to deliver high-quality family entertainment and educational products. The group plays a pivotal role globally by setting benchmarks for component durability and artistic design that competitors strive to emulate. Recent efforts to bolster their standing involve expanding their licensed product lines based on popular movies and television series to attract younger demographics. They have launched extensive sustainability initiatives aimed at eliminating plastic from packaging and using recycled materials for game boards and pieces. Ravensburger actively collaborates with educational institutions to develop games that support cognitive development and classroom learning objectives. Their investment in augmented reality features adds a modern interactive layer to traditional puzzles and board games. By maintaining strict quality control and fostering a reputation for trustworthiness they secure a dominant position in the family segment. This commitment to excellence ensures their products remain staples in households across the continent and beyond.

Hasbro Gaming (Europe Division)

Hasbro Gaming maintains a formidable presence in the Europe board games market through its ownership of iconic global brands that define the classic gaming experience for generations. The division contributes to the global market by revitalizing timeless franchises with modern updates and thematic variations that resonate with contemporary players. Recent strategic moves include the introduction of premium collector editions and collaborative versions of their flagship titles to engage adult hobbyists. They have expanded their digital ecosystem by integrating mobile apps that enhance gameplay with sound effects and automated rule enforcement. Hasbro actively partners with pop culture entities to release limited edition games tied to current entertainment trends ensuring relevance in a fast-paced market. Their focus on inclusive game design ensures that products are accessible to players of all abilities and backgrounds. By balancing nostalgia with innovation Hasbro continues to drive mass market adoption while exploring new revenue streams through experiential retail and licensing deals.

Top Strategies Used by Key Market Participants

Key players in the Europe board games market primarily employ strategies focused on portfolio diversification and intellectual property acquisition to capture varied consumer segments effectively. Companies frequently engage in licensing agreements with major entertainment franchises to create themed versions of classic games that attract casual buyers and fans alike. Another prevalent strategy involves the integration of digital components such as companion apps and augmented reality features to enhance user engagement and modernize traditional gameplay mechanics. Publishers are increasingly investing in sustainable production methods including the use of recycled materials and plastic-free packaging to align with environmental values of European consumers. Strategic partnerships with crowdfunding platforms allow firms to test new concepts and secure funding directly from enthusiasts before mass production. Expansion into experiential retail through branded cafes and pop-up stores creates immersive environments that foster community building and direct sales. Firms also prioritize localization efforts to ensure games are culturally relevant and linguistically accurate for diverse markets across the continent. These approaches collectively drive growth and resilience in a competitive landscape

MARKET SEGMENTATION

This research report on the Europe Board Games Market has been segmented and sub-segmented based on the following categories.

By Game Type

- Monopoly

- Scrabble

- Chess

- Others

By Age Group

- 2-5 Years

- Between 5 and 12 Years

- Between 12 and 25 Years

- Above 25 Years

By Sales Channel

- Specialty Stores

- Online/E-Commerce

- Hypermarkets/Supermarkets

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com