Europe Business Aircraft Market Size, Share, Trends, & Growth Forecast Report By Type (Light Jets, Midsize Jets, Large Jets, Very Large Jets, Turboprops), End User, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Business Aircraft Market Report Summary

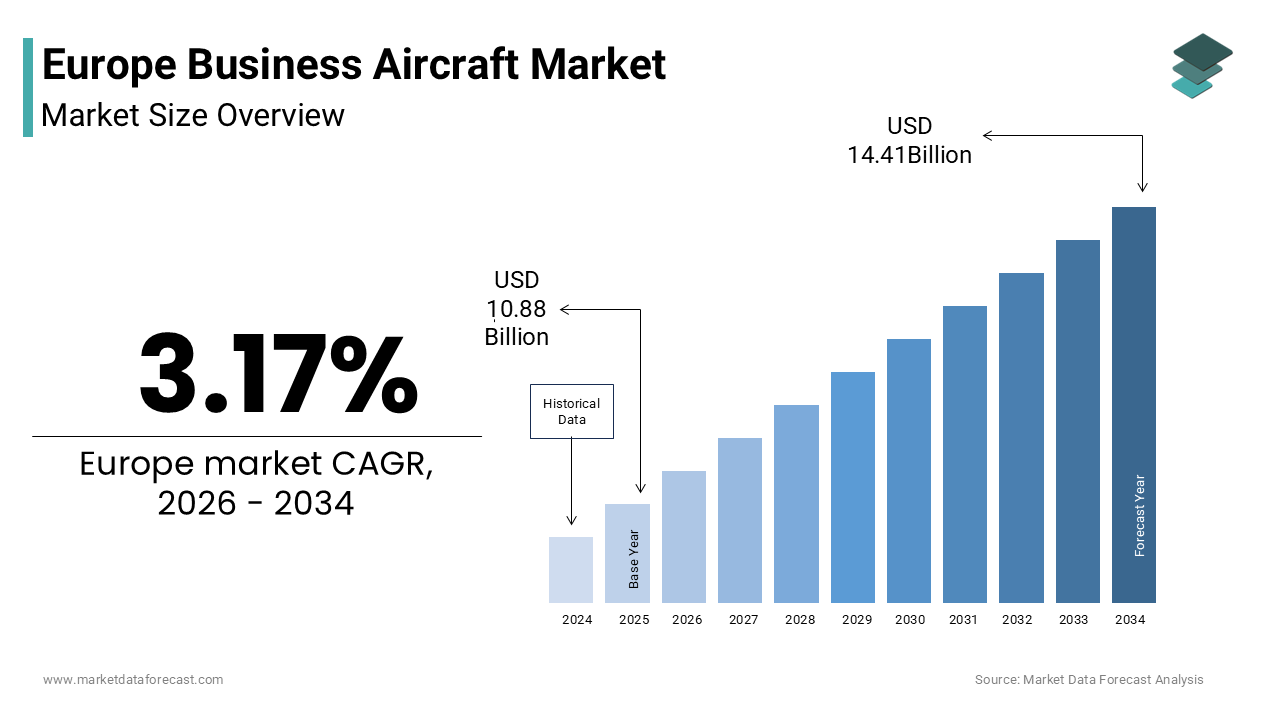

The Europe business aircraft market was valued at USD 10.88 billion in 2025, is estimated to reach USD 11.23 billion in 2026, and is projected to reach USD 14.41 billion by 2034, growing at a CAGR of 3.17% during the forecast period from 2026 to 2034. The growth of the Europe business aircraft market is driven by increasing demand for time-efficient and flexible travel solutions among corporate executives and high-net-worth individuals, along with the rising importance of business aviation in enhancing productivity and connectivity. The recovery of business aviation activity post-pandemic, coupled with growing adoption of charter services and fractional ownership models, is further supporting market expansion. Moreover, the shift toward sustainable aviation fuels, advanced aircraft technologies, and digital booking platforms is reshaping the business aviation landscape across Europe.

Key Market Trends

- Rising demand for time-efficient and flexible travel solutions, enabling executives to access regional airports and optimize productivity.

- Growing adoption of charter services, fractional ownership, and jet card programs, offering cost-effective alternatives to full aircraft ownership.

- Increasing focus on sustainable aviation fuels (SAF) and environmentally friendly technologies to reduce carbon emissions.

- Expansion of digital platforms and on-demand charter services, enhancing accessibility, transparency, and booking efficiency.

- Growing demand for long-range and luxury aircraft among high-net-worth individuals and multinational corporations.

Segmental Insights

- Based on type, the light jets segment was the largest and held a significant share of the Europe business aircraft market in 2025. The dominance of this segment is attributed to their cost efficiency, operational flexibility, and suitability for short to medium-haul routes across Europe’s dense regional airport network.

- The very large jets segment is expected to witness the fastest growth during the forecast period. The growth of this segment is driven by increasing demand for long-range travel, luxury features, and enhanced onboard productivity for intercontinental business operations.

- Based on application, the corporate travel segment was the largest, occupying a prominent share of the Europe business aircraft market in 2025. The dominance of this segment stems from the critical role of business aviation in enabling efficient executive mobility, time savings, and confidential business operations.

- Based on end use, the charter services segment accounted for the largest share of the Europe business aircraft market in 2025. The segment’s leadership is driven by its flexibility, cost-effectiveness, and growing popularity among occasional users and small to medium enterprises.

Regional Insights

The Europe business aircraft market is witnessing steady growth across major economies, supported by strong corporate activity, rising wealth, and demand for premium travel solutions.

- The United Kingdom was the largest contributor, accounting for 22.7% of the European business aircraft market share in 2025, driven by its status as a global financial hub and high concentration of high-net-worth individuals.

- France holds a significant position in the market, supported by its strong luxury tourism sector and central role in European business travel.

- Germany is a key market driven by its robust industrial base, export-oriented economy, and demand for efficient corporate mobility.

- Switzerland is emerging as an important market due to its concentration of wealth, banking sector, and luxury tourism demand.

- Italy is also witnessing growth driven by its luxury industries, tourism sector, and increasing demand for private aviation services.

Competitive Landscape

The Europe business aircraft market is characterized by intense competition among leading aircraft manufacturers focusing on performance, innovation, sustainability, and customer experience. Companies are investing in fuel-efficient aircraft, advanced avionics, and sustainable aviation technologies to comply with stringent environmental regulations and evolving customer expectations. Strategic expansion of service networks, digital transformation, and flexible financing options are further strengthening market positioning. Prominent players in the Europe business aircraft market include Dassault Aviation, Bombardier Inc., Gulfstream Aerospace Corporation, Textron Aviation, Embraer S.A., Airbus Corporate Jets, and Pilatus Aircraft Ltd.

Europe Business Aircraft Market Size

The Europe Business Aircraft Market size was valued at USD 10.88 billion in 2025 and is anticipated to reach USD 11.23 billion in 2026 from USD 14.41 billion by 2034, growing at a CAGR of 3.17% during the forecast period from 2026 to 2034

A business aircraft is a specialized aircraft, typically a jet, turboprop, or helicopter, used by companies, organizations, or individuals to transport personnel or goods to support business operations. These aircraft provide flexible, on-demand travel, allowing passengers to utilize regional airports closer to their destinations, maximizing efficiency and enabling travel on their own schedules. This market serves as a critical component of the broader aviation industry offering time efficiency privacy and access to airports with limited commercial service. The market dynamics are influenced by regulatory frameworks environmental mandates and economic conditions specific to the European region. Eurocontrol confirms that business aviation was the first market segment to fully recover to pre-pandemic activity levels, even outperforming previous records despite broader economic challenges in the aviation industry. The European Business Aviation Association highlights the sector's vital role in the regional economy, noting that it provides hundreds of thousands of highly skilled jobs and facilitates essential connectivity between regions not served by scheduled airlines. The infrastructure includes a dense network of fixed base operators and maintenance facilities primarily concentrated in Western and Northern Europe. Regulatory bodies such as the European Union Aviation Safety Agency enforce strict safety and emission standards that shape fleet composition and operational procedures. The shift towards sustainable aviation fuels and newer more efficient airframes is redefining procurement strategies. Corporate travel policies are evolving to prioritize carbon footprint reduction influencing demand for modern aircraft. The market is characterized by a mix of outright ownership fractional ownership and charter services catering to diverse user needs. Understanding this landscape requires analyzing the interplay between regulatory pressure technological innovation and changing corporate travel behaviors in a post pandemic era.

MARKET DRIVERS

Time Efficiency and Productivity Enhancement for Corporate Executives

The paramount need for time efficiency and productivity enhancement among corporate executives is among the major drivers of the Europe business aircraft market. In an increasingly globalized business environment the ability to conduct multiple meetings in different cities within a single day is a competitive advantage that commercial aviation often cannot provide due to fixed schedules and security protocols. Business aircraft allow executives to bypass congested major hubs and utilize smaller regional airports closer to their final destinations. Research from the National Business Aviation Association highlights that private flight operations provide substantial time-saving benefits by allowing passengers to bypass traditional airport security lines and use smaller, more convenient airports. This time savings translates directly into increased productivity and improved work life balance. Data from the European Business Aviation Association demonstrates that a vast majority of private flights in the region link city pairs that lack any direct commercial airline connectivity, facilitating travel to underserved areas. The flexibility to depart on short notice and adjust itineraries in real time is crucial for managing crises and seizing opportunistic business deals. Furthermore the private cabin environment facilitates confidential discussions and uninterrupted work which is difficult to achieve in commercial terminals. Companies view these operational efficiencies as justifying the higher costs associated with private aviation. The integration of advanced connectivity systems onboard allows for seamless communication ensuring that executives remain productive while in transit. This strategic value proposition sustains demand despite economic fluctuations.

Growing Wealth Among High Net Worth Individuals in Europe

Wealth accumulation among high-net-worth individuals fuels the European business aircraft market. The pre-owned and charter segments are experiencing the highest impact. The number of ultra high net worth individuals in the region has grown steadily providing a larger customer base for private aviation services. Sources indicate that while the total number of ultra-wealthy residents in Europe has experienced fluctuations due to global economic volatility, the region remains one of the world's largest hubs for high-net-worth individuals. This demographic prioritizes luxury convenience and privacy making business aircraft an attractive asset for personal and family travel. The Global Wealth Report shows that despite temporary market contractions, European private wealth remains a significant driver for the high-end luxury and premium services sectors as markets stabilize. Many high net worth individuals opt for fractional ownership or jet card programs which offer the benefits of private aviation without the full responsibilities of aircraft ownership. The desire for health security and social distancing following the pandemic has also accelerated the shift from commercial first class to private jets among this group. Additionally the ability to travel with pets and personalized luggage without restrictive allowances enhances the appeal of private aviation. This growing affluent class ensures a steady demand for both new and pre owned aircraft. The market responds by offering tailored services and flexible financing options to accommodate diverse preferences and budgets.

MARKET RESTRAINTS

Stringent Environmental Regulations and Carbon Emission Targets

The implementation of stringent environmental regulations and carbon emission targets inhibits the growth of the Europe business aircraft market. The European Union is at the forefront of global efforts to reduce aviation emissions through initiatives such as the Fit for 55 package and the ReFuelEU Aviation initiative. These regulations mandate the gradual increase of sustainable aviation fuel usage and impose stricter limits on carbon dioxide emissions. Under the European Commission "Fit for 55" package, the aviation sector is subject to increasingly stringent environmental rules, including a phased withdrawal of free carbon allowances and rising mandates for renewable fuel blending. As per the European Business Aviation Association compliance with these regulations requires significant investment in newer more efficient aircraft and sustainable fuels which are currently more expensive and less available than conventional jet fuel. The potential introduction of carbon taxes on private flights further increases operational costs. Some governments are considering bans on short haul flights where rail alternatives exist which could limit the utility of business aircraft for domestic routes. The public scrutiny of private aviation due to its perceived high carbon footprint per passenger also poses reputational risks for corporate users. These regulatory and social pressures compel operators to rethink their fleets and operations potentially delaying procurement decisions. The transition to green technologies is capital intensive and technologically challenging creating uncertainty for market participants.

High Operational Costs and Economic Volatility

High operational costs and economic volatility are also top factors restricting the expansion of the Europe business aircraft market. This affects both owners and charter clients. The cost of operating a business aircraft includes fuel maintenance crew salaries insurance and hangarage all of which have risen due to inflation and supply chain disruptions. According to Eurostat inflation rates in the Euro area peaked at 10.6 percent in late 2022 increasing the overall cost of living and doing business. As per the International Air Transport Association jet fuel prices remained volatile and elevated throughout 2022 and 2023 significantly impacting operating budgets. Maintenance costs have also surged due to parts shortages and labor constraints in the aerospace sector. Economic uncertainty stemming from geopolitical tensions and potential recessions leads corporations to scrutinize discretionary spending including private travel. Many companies are implementing stricter travel policies requiring justification for private jet use to control expenses. The high fixed costs of ownership make it difficult for some users to justify keeping aircraft during downturns leading to increased sales of pre owned jets which can depress prices. Charter rates have also increased making occasional use less affordable for some clients. These financial pressures constrain market growth and force operators to optimize efficiency and seek cost saving measures. The sensitivity of the market to economic cycles makes long term planning challenging for stakeholders.

MARKET OPPORTUNITIES

Adoption of Sustainable Aviation Fuels and Green Technologies

The adoption of sustainable aviation fuels and green technologies offers a great opportunity for the European business aircraft market. This shift allows the industry to align with environmental goals and enhance its brand image. As regulatory pressure mounts airlines and operators who proactively integrate sustainable practices can differentiate themselves and secure contracts with environmentally conscious corporations. According to the European Business Aviation Association the use of sustainable aviation fuel in business aviation is growing albeit from a low base with several major operators committing to net zero emissions by 2050. As per the International Air Transport Association sustainable aviation fuel can reduce lifecycle carbon emissions significantly compared to conventional jet fuel. Governments are providing incentives and subsidies for the production and use of these fuels creating a favorable economic environment for early adopters. Manufacturers are developing new aircraft models with improved fuel efficiency and lower noise profiles which appeal to regulators and communities near airports. The development of hybrid electric and hydrogen powered aircraft offers long term potential for zero emission flights. Operators who invest in these technologies can future proof their fleets against stricter regulations. Partnerships with fuel suppliers and technology providers enable operators to secure supply chains and share development costs. This transition opens new revenue streams through green charter services and carbon offset programs. Embracing sustainability allows the market to mitigate regulatory risks and attract a new generation of eco conscious clients.

Expansion of Digital Platforms and On Demand Charter Services

The expansion of digital platforms and on-demand charter services is increasing accessibility and transparency for users. This creates major possibilities for the European business aircraft market. Technology driven platforms simplify the booking process allowing clients to compare prices availability and aircraft types in real time. Research indicates that the private flight market is undergoing a rapid digital transformation, with an increasing number of travelers now securing aircraft through automated web and mobile platforms. According to the European Business Aviation Association, the implementation of integrated digital tools has streamlined the interaction between passengers and providers while significantly enhancing the efficiency of back-office flight management. These platforms enable dynamic pricing and better asset utilization for operators reducing empty leg flights and lowering costs for users. The rise of subscription based models and jet cards provides flexible alternatives to ownership appealing to small and medium sized enterprises. Data analytics allow operators to predict demand and optimize fleet deployment enhancing operational efficiency. The integration of artificial intelligence enables personalized recommendations and streamlined customer service. Digital platforms also facilitate transparency in pricing and safety records building trust among new users. This technological evolution democratizes access to private aviation expanding the customer base beyond traditional ultra high net worth individuals. The market can improve efficiency and responsiveness by leveraging digital tools. This allows for better adaptation to changing consumer preferences.

MARKET CHALLENGES

Air Traffic Control Congestion and Slot Restrictions

Air traffic control congestion and slot restrictions at major airports remain a serious hurdle for the Europe business aircraft market. The European sky is one of the most congested in the world leading to frequent delays and cancellations which undermine the time saving benefits of private aviation. According to Eurocontrol air traffic flow management restrictions affected thousands of flights in Europe in 2022 causing significant operational disruptions. As per the European Business Aviation Association business aircraft often receive lower priority for slots compared to commercial airlines during peak times limiting their flexibility. Major hubs such as London Heathrow Paris Charles de Gaulle and Frankfurt have strict slot allocation mechanisms that make it difficult for business jets to secure convenient departure and arrival times. This forces operators to use secondary airports which may be less convenient for passengers and require additional ground transportation. The lack of harmonized air traffic management across European countries exacerbates the problem leading to inefficiencies and increased fuel consumption. Infrastructure investments have not kept pace with demand growth resulting in persistent bottlenecks. These operational hurdles increase costs and reduce the reliability of business aviation services. Operators must invest in sophisticated flight planning tools and maintain flexibility to navigate these constraints. The inability to guarantee timely arrivals can deter potential customers who rely on precision scheduling for business purposes.

Pilot Shortages and Workforce Constraints

Pilot shortages and workforce constraints are creating substantial challenges for the European business aircraft market. As a result, both operational capacity and service quality are suffering. The retirement of experienced pilots combined with insufficient training pipelines has created a gap in the availability of qualified personnel. Multiple studies suggest that the global demand for new flight deck professionals remains high, requiring a steady pipeline of newly trained personnel to support the continued expansion of the aviation sector. As per the European Business Aviation Association recruiting and retaining qualified captains and first officers has become increasingly difficult and expensive for operators. The rigorous training requirements and high costs associated with type ratings for specific aircraft models further limit the pool of eligible candidates. Labor disputes and strikes in the broader aviation sector also disrupt operations and create uncertainty. The shortage extends to maintenance technicians and cabin crew affecting the overall service delivery. Operators are compelled to offer higher salaries and benefits to attract talent increasing operational costs. The reliance on foreign pilots introduces regulatory complexities regarding licensing and visa requirements. The lack of workforce stability affects fleet utilization and customer satisfaction. Addressing this challenge requires long term investments in training programs and collaboration with educational institutions. Without a stable and skilled workforce the market struggles to meet growing demand and maintain high safety standards.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.17% |

| Segments Covered | By Type, End User, Application and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Dassault Aviation, Bombardier, Gulfstream Aerospace, Textron Aviation, Embraer, Airbus Corporate Jets, and Pilatus Aircraft, |

SEGMENTAL ANALYSIS

By Type Insights

The light jets segment dominated the Europe business aircraft market and accounted for a 38.6% share in 2025. This dominance of the segment is mainly driven by the cost efficiency and operational flexibility that light jets offer for short to medium haul routes which constitute the majority of business aviation flights in Europe. These aircraft are ideal for connecting secondary cities and regional hubs where larger airports are congested or inaccessible. A study by the European Business Aviation Association indicates that while light jets perform the greatest frequency of short-haul departures, large-cabin aircraft accumulate the most total time in the air due to the extended duration of international missions. Eurocontrol emphasizes that a vast majority of private flight activity in the region consists of short-range trips, making the efficiency of smaller aircraft highly relevant for the European network. The lower acquisition and operating costs compared to midsize and large jets make them accessible to a broader range of corporate clients and high net worth individuals. Furthermore the improved performance of modern light jets including faster climb rates and better fuel efficiency has enhanced their appeal. Manufacturers such as Cessna and Embraer have introduced models with advanced avionics and comfortable cabins that rival larger aircraft. The ability to deploy these aircraft quickly for urgent travel needs supports their widespread adoption. The dense network of regional airports in countries like Germany France and Italy further facilitates the utility of light jets. These factors collectively sustain the leadership of the light jets segment in the regional market.

The very large jets segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 6.5% during the forecast period owing to the increasing demand for ultra long range connectivity and luxury among ultra high net worth individuals and multinational corporations. These aircraft offer intercontinental range allowing non stop flights between Europe and key global markets such as North America Asia and the Middle East. According to sources, the number of ultra high net worth individuals in Europe continues to grow creating a robust customer base for premium aviation assets. As per the European Business Aviation Association very large jets are increasingly used for global business operations where time efficiency and onboard productivity are paramount. The spacious cabins of these aircraft allow for fully equipped offices conference rooms and sleeping quarters enabling executives to work and rest comfortably during long flights. Recent innovations in cabin technology including enhanced connectivity and air quality systems have further elevated the passenger experience. The recovery of international business travel following the pandemic has accelerated the demand for these high capacity aircraft. Additionally the ability to carry larger groups of executives or family members makes very large jets attractive for corporate fleets and private owners. Manufacturers like Gulfstream and Bombardier continue to introduce models with extended range and improved sustainability features. These attributes drive the rapid expansion of the very large jets segment.

By Application Insights

The corporate travel segment held the prominent share of 65.3% of the Europe business aircraft market in 2025. This position of the segment is attributed to the critical role of private aviation in facilitating efficient business operations. Companies utilize business aircraft to transport executives to multiple locations in a single day bypassing the delays and inconveniences associated with commercial airlines. The flexibility to change schedules at short notice is essential for managing dynamic business environments and responding to emerging opportunities. Furthermore the privacy afforded by private jets allows for confidential discussions and secure handling of sensitive information. The integration of business aviation into corporate travel policies has become more strategic with companies focusing on total trip value rather than just ticket cost. The rise of hybrid work models has also increased the need for flexible travel options that allow executives to visit remote offices and clients efficiently. Corporate fleets and charter services cater to this demand by providing reliable and tailored solutions. The consistent need for efficient executive mobility ensures that corporate travel remains the dominant application in the market.

The Air Taxi Services segment is expected to exhibit a noteworthy CAGR of 8.2% from 2026 to 2034 owing to the emergence of urban air mobility concepts and the digitalization of on demand charter platforms. Although traditional air taxi services using helicopters and small jets have existed for years the integration of advanced booking apps and dynamic pricing models has revitalized this sector. The ability to book single seats on shared flights reduces costs and increases utilization rates for operators. This model appeals to cost conscious users who seek the benefits of private aviation without the expense of full aircraft charter. The development of electric vertical takeoff and landing vehicles eVTOLs is expected to further transform this segment by offering quieter and more sustainable short distance transport within and between cities. Regulatory frameworks in Europe are evolving to support these new technologies creating a favorable environment for innovation. Partnerships between traditional operators and tech startups are accelerating the deployment of air taxi networks. These developments position air taxi services as a high growth area in the business aviation landscape.

By End Use Insights

The charter services segment was the largest segment in the Europe business aircraft market and occupied a 45.8% share in 2025. This prominence of the segment is credited to its flexibility and cost effectiveness for occasional users. Many companies and individuals prefer chartering aircraft over ownership to avoid the high fixed costs associated with maintenance crew and hangarage. Charter services allow users to select the most appropriate aircraft for each trip optimizing cost and comfort. The availability of empty leg flights offers discounted rates making private aviation more affordable for budget conscious travelers. Digital platforms have streamlined the charter process enabling quick comparisons and bookings which enhances user experience. The rise of jet card programs and membership models provides additional flexibility and guaranteed availability for frequent flyers. Charter operators benefit from high asset utilization by serving a diverse client base. The ability to scale usage according to business needs makes charter services an attractive option in uncertain economic conditions. These factors collectively sustain the dominance of the charter services segment in the regional market.

The lease companies segment is predicted to witness the highest CAGR of 5.8% over the forecast period. This swift growth of the segment is driven by the increasing popularity of leasing as a financing solution for acquiring business aircraft. Leasing allows operators and corporations to access modern aircraft without the substantial capital outlay required for outright purchase. Operating leases provide tax advantages and reduce the risk of asset depreciation for lessees. The availability of diverse leasing structures including dry and wet leases caters to different operational needs. Lessors benefit from steady income streams and the ability to remarket aircraft to various clients. The growing interest in sustainable aviation has led to increased leasing of newer more fuel efficient aircraft which are compliant with environmental regulations. Financial institutions and specialized leasing companies are expanding their portfolios to meet this demand. The complexity of aircraft financing and the desire for operational flexibility make leasing an increasingly preferred option. These dynamics support the rapid growth of the lease companies segment in the Europe business aircraft market.

REGIONAL ANALYSIS

United Kingdom Business Aircraft Market Analysis

The United Kingdom was the top performer in the Europe business aircraft market and captured a 22.7% share in 2025 because of its status as a global financial hub and high concentration of wealth. London serves as a central node for international business traffic driving significant demand for private aviation services. The presence of numerous multinational corporations and high net worth individuals sustains a strong market for both charter and ownership. Moreover, the UK's extensive network of regional airports facilitates efficient domestic and international connectivity. Post Brexit adjustments have influenced flight patterns but the demand for private travel remains resilient due to the need for flexible cross border movement. The government's focus on green aviation is encouraging the adoption of sustainable fuels and newer aircraft technologies. The strong legal and financial infrastructure supports complex leasing and ownership structures. These factors maintain the UK's leadership position in the European market.

France Business Aircraft Market Analysis

France followed closely behind in the European market and occupied a share of 18.5% in 2025. This expansion of the French market is propelled by a strong luxury goods industry and tourism sector that drives demand for business aviation. Paris is a major destination for international business and leisure travelers requiring efficient and discreet transport options. The country's central location in Europe makes it a key transit point for intra continental flights. In addition, the French government's support for the aerospace industry fosters innovation and manufacturing capabilities. The prevalence of high end tourism in regions such as the French Riviera boosts seasonal demand for charter services. Regulatory initiatives promoting sustainable aviation are influencing fleet renewal decisions among operators. The strong cultural emphasis on luxury and service quality aligns with the value proposition of business aviation. These elements sustain France's prominent position in the regional market.

Germany Business Aircraft Market Analysis

Germany is another key player in the regional market due to its robust industrial base and strong export oriented economy. The country is home to many Mittelstand companies and multinational corporations that rely on business aircraft for efficient supply chain management and client visits. Frankfurt and Munich serve as key hubs for business flights connecting Germany to global markets. Besides, the federal structure of Germany with multiple economic centers necessitates efficient domestic air connectivity which business aviation provides. The country's commitment to environmental sustainability is driving investments in sustainable aviation fuels and efficient aircraft technologies. The presence of major aircraft manufacturers and suppliers enhances the local ecosystem. Regulatory compliance with strict European standards ensures high safety and operational quality. These factors contribute to Germany's stable and significant market presence.

Switzerland Business Aircraft Market Analysis

Switzerland experienced a consistent growth in the Europe business aircraft market owing to its high concentration of wealth and status as a global banking center. The country attracts ultra high net worth individuals and international organizations who utilize private aviation for discretion and efficiency. The luxury tourism sector particularly ski resorts drives seasonal peaks in demand for charter services. Furthermore, the political stability and favorable business environment attract foreign investment and residency further boosting demand. Switzerland's geographic location in the heart of Europe facilitates easy access to neighboring countries. The emphasis on precision and quality in Swiss services aligns with the expectations of business aviation clients. Regulatory frameworks support safe and efficient operations while addressing environmental concerns. These attributes maintain Switzerland's relevance as a key market in the region.

Italy Business Aircraft Market Analysis

Italy is anticipated to expand significantly in the European market during the forecast period due to its luxury manufacturing sector and vibrant tourism industry. Cities like Milan and Rome are major hubs for fashion design and international business driving demand for private travel. The country's appeal as a tourist destination for high net worth individuals boosts charter demand particularly during summer and holiday seasons. Moreover, the geographical shape of Italy with its elongated peninsula makes air travel efficient for domestic connections. The luxury yacht and automotive industries often intersect with business aviation creating synergies in high end services. Regulatory efforts to improve airport infrastructure and streamline procedures are enhancing operational efficiency. The focus on sustainability is encouraging the adoption of greener technologies among local operators. These factors sustain Italy's position as a notable market in the European business aviation landscape.

COMPETITIVE LANDSCAPE

The competition in the Europe business aircraft market is intense characterized by a few established manufacturers and a fragmented operator landscape. Major players compete on aircraft performance cabin luxury technological innovation and after sales support services. The shift towards sustainability has become a critical differentiator as regulators impose stricter emission standards and carbon taxes. Companies are racing to introduce fuel efficient models and integrate sustainable aviation fuels into their operations. Service quality and network coverage are vital for retaining corporate clients who prioritize reliability and convenience. Price competition exists particularly in the charter and pre owned segments but brand reputation often dictates purchasing decisions in the new aircraft market. Digital platforms are disrupting traditional brokerage and charter models by increasing transparency and ease of access. Consolidation among operators and service providers is occurring to achieve economies of scale. Innovation in urban air mobility and electric propulsion presents future competitive battlegrounds. Manufacturers must balance high development costs with market demand for greener solutions. Customer loyalty is driven by consistent performance and comprehensive support ecosystems. The market rewards those who can deliver superior value while adhering to environmental and regulatory constraints.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe business aircraft market include

- Dassault Aviation

- Bombardier Inc.

- Gulfstream Aerospace Corporation

- Textron Aviation

- Embraer S.A.

- Airbus Corporate Jets

- Pilatus Aircraft Ltd

Top Players in the Market

Dassault Aviation

Dassault Aviation is a leading French aerospace manufacturer renowned for its Falcon series of business jets which are highly regarded in the Europe business aircraft market. The company contributes significantly to the global market by delivering high performance trijet and twin jet aircraft known for their advanced aerodynamics and fuel efficiency. Recent actions include the launch of the Falcon 6X which features the widest and tallest cabin in its class enhancing passenger comfort. Dassault continues to invest in digital flight control systems and sustainable aviation technologies to meet evolving regulatory standards. Its strong presence in Europe is supported by an extensive maintenance network and customer service infrastructure. The company focuses on innovation in avionics and cabin design to maintain its competitive edge. These efforts reinforce its reputation for engineering excellence and reliability in the premium business aviation sector.

Bombardier Inc.

Bombardier Inc. is a Canadian aerospace giant with a substantial footprint in the Europe business aircraft market through its Global and Challenger jet families. The company plays a pivotal role globally by providing ultra long range and super midsize aircraft that cater to diverse corporate and private needs. Recent strategies involve focusing exclusively on business aviation after divesting its commercial aircraft and rail divisions. Bombardier has introduced the Global 7500 and Global 8000 models which offer unprecedented range and cabin space. The company is actively promoting sustainable aviation fuels and carbon offset programs to align with European environmental goals. Its dedicated service centers across Europe ensure high availability and support for operators. Bombardier emphasizes luxury and technological innovation to attract high net worth individuals and corporate clients. These initiatives strengthen its position as a premier provider of business aviation solutions.

Gulfstream Aerospace

Gulfstream Aerospace a subsidiary of General Dynamics is a dominant force in the Europe business aircraft market known for its large cabin and long range jets. The company contributes to the global market by setting benchmarks in speed range and cabin comfort with models like the G700 and G800. Recent actions include achieving numerous speed and distance records which demonstrate the superior performance of its aircraft. Gulfstream is investing heavily in research and development for next generation propulsion systems and sustainable materials. The company has expanded its service network in Europe to provide rapid response and comprehensive maintenance support. Gulfstream focuses on enhancing connectivity and cabin experience through advanced technology integration. Its commitment to quality and innovation ensures strong loyalty among corporate and private owners. These efforts solidify its leadership in the high end segment of the business aviation industry.

Top Strategies Used by the Key Market Participants

Key players in the Europe business aircraft market prioritize product innovation by developing fuel efficient and technologically advanced aircraft to comply with strict environmental regulations. Companies invest heavily in research and development to enhance cabin comfort connectivity and operational performance. Strategic expansion of maintenance repair and overhaul networks ensures high asset availability and customer satisfaction across the region. Manufacturers are increasingly focusing on sustainable aviation fuels and carbon neutral growth initiatives to address ecological concerns. Partnerships with technology firms enable the integration of advanced avionics and digital services. Flexible financing and leasing options are offered to broaden the customer base and mitigate high acquisition costs. Brand differentiation through luxury customization and exclusive services helps retain high net worth clients. These strategies enable companies to navigate regulatory challenges and maintain competitiveness in a dynamic market environment.

MARKET SEGMENTATION

This research report on the Europe business aircraft market has been segmented and sub-segmented based on the following categories.

By Type

- Light Jets

- Midsize Jets

- Large Jets

- Very Large Jets

- Turboprops

By End Use

- Private Owners

- Charter Services

- Lease Companies

- Corporate Fleet Operators

By Application

- Corporate Travel

- Medical Evacuation

- Air Taxi Services

- Cargo Transport

- Government

- Military

By Aircraft Configuration

- Single Pilot

- Multi Pilot

- Commuter

- Special Missions

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com