Europe Candy Market Research Report - Segmented Based on Type, Distribution Channel, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis on Size, Share, Trends, & Growth Forecast (2026 to 2034)

Europe Candy Market Report Summary

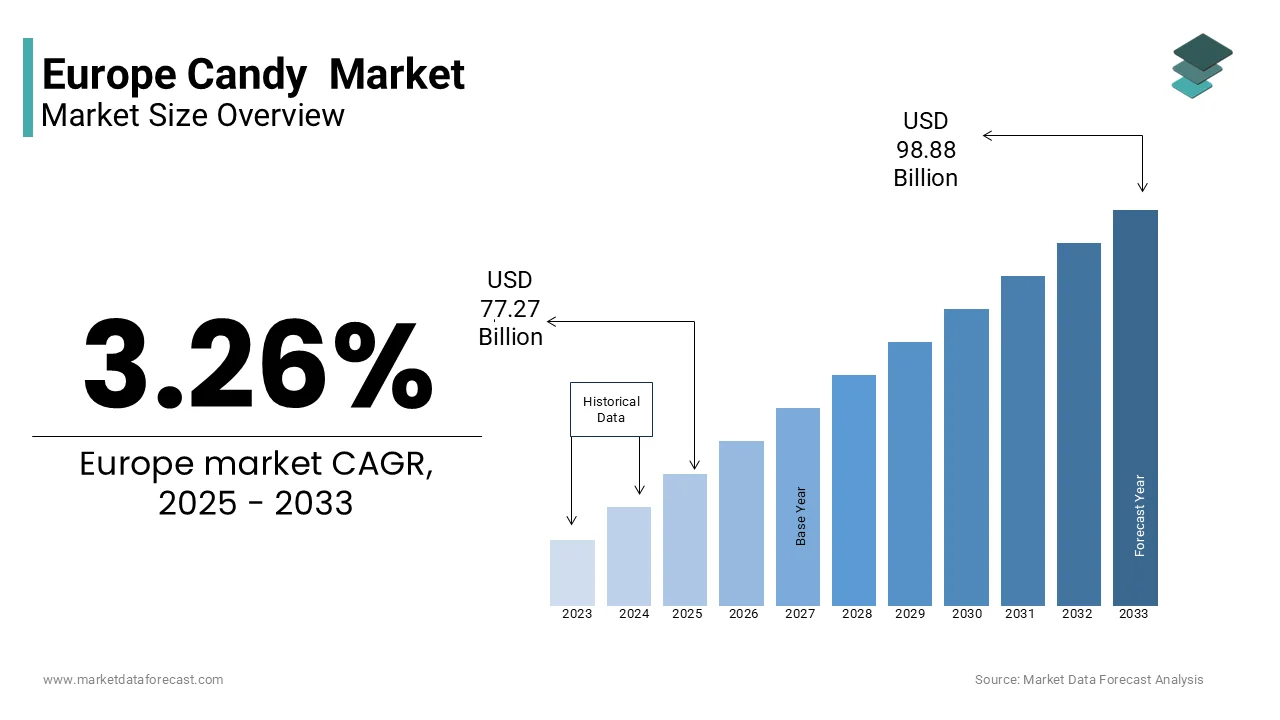

The Europe candy market was valued at USD 77.30 billion in 2025, is estimated to reach USD 79.82 billion in 2026, and is projected to reach USD 103.17 billion by 2034, growing at a CAGR of 3.26% during the forecast period. Market growth is driven by strong consumer demand for confectionery products, rising indulgence consumption patterns, and continuous product innovation in flavors and formats. The popularity of seasonal and premium chocolates, along with gifting culture and festive demand, is further supporting market expansion. In addition, increasing availability through organized retail and online channels is contributing to steady growth across Europe.

Key Market Trends

- Rising demand for premium and artisanal confectionery products is driving market growth.

- Increasing consumer preference for indulgent and impulse purchase items is boosting demand.

- Growing innovation in flavors, ingredients, and packaging is supporting market expansion.

- Expansion of e commerce and organized retail channels is improving product availability.

- Rising demand for sugar reduced and functional confectionery is influencing product development.

Segmental Insights

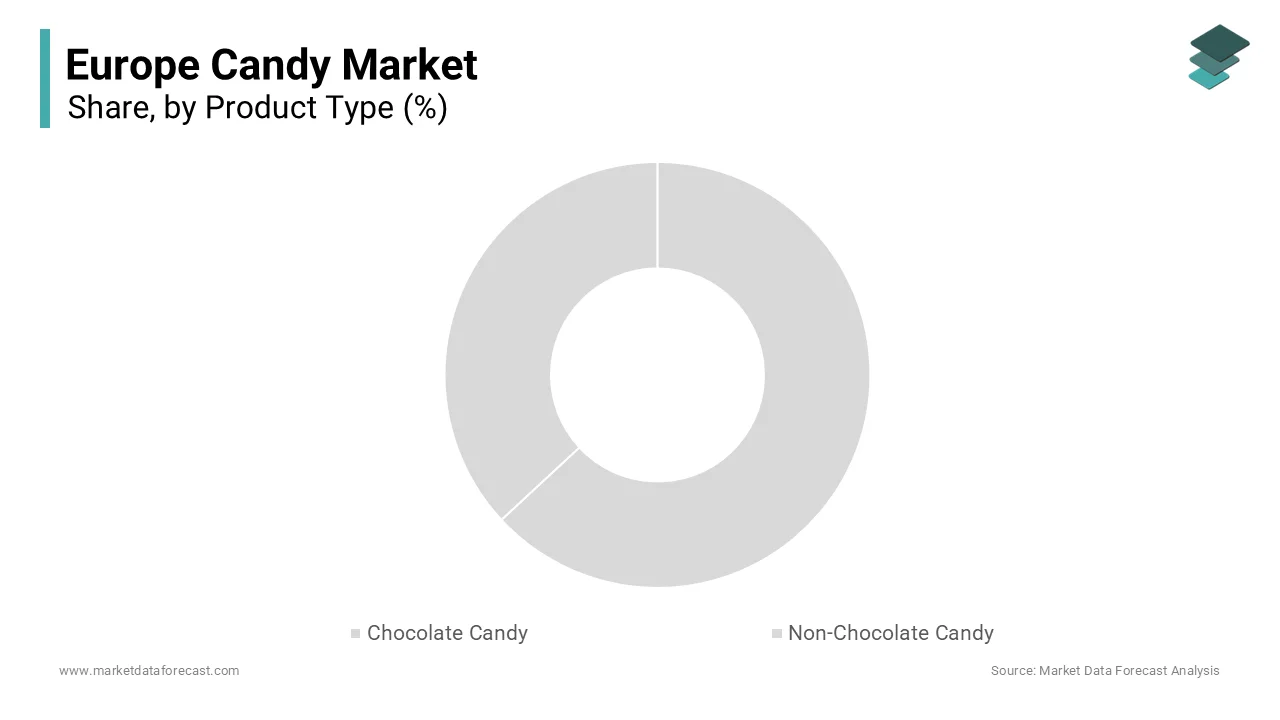

- Based on product type, the chocolate candy segment was the largest and held 58.4% of the Europe candy market share in 2025. This dominance is attributed to high consumer preference, wide product variety, and strong seasonal demand.

- Based on distribution channel, the supermarkets segment accounted for 42.6% of the Europe candy market share in 2025. The segment’s growth is driven by extensive product availability, promotional activities, and consumer convenience.

Regional Insights

- The Europe candy market is experiencing steady growth across key countries, supported by strong consumption patterns and product innovation.

- Germany was the largest contributor, accounting for 21.3% of the Europe candy market share in 2025, driven by high consumption of confectionery products, strong retail infrastructure, and presence of established manufacturers.

Competitive Landscape

The Europe candy market is highly competitive, with key players focusing on product innovation, premium offerings, and expansion of distribution networks to strengthen their market position. Companies are investing in new flavors, healthier alternatives, and branding strategies. Prominent players in the Europe candy market include Arcor, August Storck KG, Yildiz Holding, Cemoi, Chocoladefabriken Lindt and Sprungli AG, United Confectionary Manufacturers, Crown Confectionary Co Ltd, DeMet’s Candy Co, Ezaki Glico Co Ltd, and Ferrero Group.

Europe Candy Market Size

The Europe candy market size was valued at USD 77.30 billion in 2025, and the market size is expected to reach USD 103.17 billion by 2034 from USD 79.82 billion in 2026. The market's promising CAGR for the predicted period is 3.26%.

The candy is a diverse array of confectionery products, including chocolates, gummies, hard candies, and licorice that serve as both indulgent treats and cultural staples. The World Health Organization stated that sugar consumption remains a public health focus, with many European nations implementing stricter dietary guidelines to combat rising obesity rates. The demand for high quality and ethically sourced confectionery continues to rise, which is driven by consumers who view candy as an affordable luxury. The integration of sustainable practices in sourcing cocoa and sugar has become a pivotal factor for brand differentiation. Urbanization trends have also shifted consumption towards convenient, single serve formats suitable for on-the-go lifestyles. The presence of established multinational corporations alongside niche local producers creates a dynamic competitive landscape. Digital transformation in retail has further expanded access by allowing brands to engage directly with consumers through e commerce platforms and personalized marketing strategies.

MARKET DRIVERS

Resilient Consumer Spending On Affordable Luxuries Amidst Economic Uncertainty

The tendency of consumers to prioritize small indulgences during periods of economic uncertainty is major factor propelling the growth of Europe candy market. Known as the lipstick effect, this phenomenon sees individuals purchasing affordable luxury items to maintain morale when larger discretionary spending is curtailed. Confectionery items, being relatively inexpensive compared to other leisure activities or durable goods, offer an accessible form of comfort and reward. In Germany, the largest economy in Europe, retail sales of confectionery remained stable despite inflationary pressures, as reported by the study. This resilience is attributed to the psychological benefit derived from sweet treats, which provide immediate gratification without significant financial burden. Manufacturers have capitalized on this behavior by introducing premium, yet affordably priced product lines that appeal to value conscious shoppers seeking quality. The tradition of gift giving during holidays such as Easter and Christmas further amplifies demand, as candies are perceived as thoughtful and budget friendly presents. Social media influence also plays a role, with viral trends driving impulse purchases of novel and visually appealing candy products.

Innovation In Premium And Artisanal Confectionery Appeals To Discerning Tastes

The growing consumer preference for premium and artisanal confectionery products is significantly driving the Europe Candy Market, as buyers increasingly seek high quality ingredients and unique flavor profiles. Consumers are willing to pay a premium for chocolates made with single origin cocoa, organic sugar, and natural fruit extracts by viewing these products as superior alternatives to mass produced options. The rise of food tourism has also contributed to this trend, with travelers exploring local confectionery specialties as part of their cultural immersion. Brands are responding by launching limited edition flavors and collaborating with local farmers to source exclusive ingredients, thereby creating a sense of exclusivity and authenticity. The emphasis on transparency in sourcing and production processes further enhances brand loyalty among discerning buyers who value ethical standards. This movement towards premiumization allows manufacturers to differentiate themselves in a saturated market and capture higher margins.

MARKET RESTRAINTS

Stringent Regulatory Frameworks On Sugar Content And Labeling Restrict Product Formulations

The implementation of stringent regulatory frameworks regarding sugar content and nutritional labelling by forcing manufacturers to reformulate products and adjust marketing strategies is hampering the growth of Europe candy market. As per the World Health Organization Regional Office for Europe, several countries including the United Kingdom, France, and Portugal have introduced sugar taxes aimed at reducing consumption of high sugar products. These fiscal measures increase the cost of production and retail prices, potentially dampening consumer demand for traditional sugary candies. Additionally, the European Union’s strict regulations on front of pack labeling require clear indication of high sugar, fat, and salt content, which can deter health conscious consumers. The Nutri Score system, adopted by several member states, often assigns lower ratings to conventional candies, influencing purchasing decisions at the point of sale. Manufacturers face the challenge of maintaining taste and texture while reducing sugar levels, which often requires expensive research and development investments. Failure to comply with these regulations can result in penalties and reputational damage.

Rising Health Consciousness And Preference For Natural Alternatives Limit Traditional Sales

The increasing health consciousness, as individuals actively seek healthier snacking options and reduce their intake of processed sugars is another factor hampering the growth of Europe candy market. According to the European Food Information Council, 60% of Europeans are trying to limit their sugar consumption, driven by awareness of links between excessive sugar intake and chronic diseases such as diabetes and obesity. This shift in mindset has led to a decline in the consumption of conventional chocolates and gummies among younger people, who are more informed about nutritional values. The rise of fitness culture and wellness trends further exacerbates this trend, with consumers opting for protein bars, fruit based snacks, and dark chocolate with high cocoa content as alternatives. In Sweden, public health campaigns have successfully reduced candy consumption among children by 25% over the last decade, as reported by the Swedish National Food Agency, influencing family purchasing habits. Parents are increasingly scrutinizing ingredient lists, avoiding products with artificial colors, flavors, and preservatives. This demand for clean label products forces manufacturers to reformulate existing lines or risk losing market share to healthier competitors. The stigma associated with sugary snacks is reinforced by educational initiatives in schools and workplaces, promoting balanced diets.

MARKET OPPORTUNITIES

Expansion Of Plant Based And Vegan Confectionery Opens New Consumer Segments

The rapid expansion of plant based and vegan confectionery is likely to pose as a major opportunity for the growth of Europe candy market. As per ProVeg International, the number of vegans in Europe has doubled in the last five years, with countries like Germany and the United Kingdom, leading this dietary shift. Manufacturers are responding by developing gummies using pectin or agar agar instead of gelatin, and chocolates using oat or almond milk instead of cow’s milk. Brands that clearly label their products as vegan and obtain relevant certifications gain a competitive edge in attracting this conscientious consumer base. The appeal of plant-based candies extends beyond vegans to flexitarians who are reducing their animal product consumption for environmental or health reasons. Innovation in this space includes the use of exotic fruits and superfoods to enhance nutritional profiles and flavor complexity. Retailers are dedicating more shelf space to these specialized products, recognizing their high growth potential.

Adoption Of Sustainable And Eco Friendly Packaging Enhances Brand Appeal

The adoption of sustainable and eco-friendly packaging to enhance brand appeal and meet regulatory expectations is another attribute to impact positively on the growth of Europe candy market. As per the European Environment Agency, plastic waste remains an environmental issue, with consumers increasingly demanding recyclable, biodegradable, or compostable packaging solutions. In response, major confectionery companies are investing in innovative packaging technologies that reduce plastic usage and improve recyclability. In France, legislation mandates that all packaging must be recyclable by 2025, driving companies to redesign their product wrappers and boxes, as per reports. Brands that successfully transition to paper based or bio plastic packaging can differentiate themselves and attract environmentally conscious consumers. Collaborations with packaging suppliers to develop mono material structures that are easier to recycle are becoming common practice. Furthermore, transparent communication about sustainability efforts through labeling and marketing campaigns builds trust and loyalty among buyers who prioritize corporate responsibility. The use of minimal packaging designs also reduces material costs and logistics weight, offering economic benefits alongside environmental ones. Retailers are increasingly favoring suppliers with strong sustainability credentials, providing better shelf placement and promotional support.

MARKET CHALLENGES

Volatility In Raw Material Costs Impacts Profit Margins And Pricing Strategies

The volatility in raw material costs for cocoa, sugar, and dairy by affecting profit margins and forcing difficult pricing decisions is key challenge for the growth of Europe candy market. According to the International Cocoa Organization, cocoa prices reached historic highs in 2024 due to supply shortages in West Africa, exacerbated by climate change and disease outbreaks. Since cocoa is a primary ingredient in chocolate production, these price surges directly impact manufacturing costs, compelling companies to either absorb the losses or pass them on to consumers. Sugar prices have also fluctuated due to weather related crop failures in key producing regions, adding to the cost pressure. Dairy prices remain unstable due to energy costs and feed prices affecting milk production. These fluctuations make it challenging for manufacturers to maintain stable retail prices, risking consumer backlash if prices rise too sharply. Small and medium sized enterprises are particularly vulnerable, lacking the economies of scale to negotiate favorable contracts or hedge against commodity risks. Larger corporations may have more resilience, but they still face pressure to keep products affordable in a price sensitive market.

Supply Chain Disruptions And Labor Shortages Hinder Production Efficiency

The supply chain disruptions and labor shortages are hindering production efficiency and timely product availability, which is ascribed to decline the growth of Europe candy market. As per the European Central Bank, labor shortages in the manufacturing sector have intensified post pandemic, with many factories struggling to find skilled workers for production lines. This scarcity leads to delayed output and increased operational costs by affecting the ability to meet peak demand periods such as holidays. Additionally, geopolitical tensions and logistical bottlenecks continue to disrupt the flow of raw materials from global suppliers. Port congestion and transportation delays increase lead times and inventory holding costs, forcing manufacturers to maintain higher safety stocks. Energy price volatility further complicates operations, as candy production requires consistent heating and cooling processes. High energy costs in countries like Italy and Spain have forced some manufacturers to reduce production hours or temporarily shut down facilities to manage expenses. These operational inefficiencies result in stockouts and lost sales opportunities, damaging retailer relationships and consumer trust. Companies are investing in automation to mitigate labor issues, but this requires significant capital expenditure. The cumulative effect of these supply chain and labor challenges creates a fragile operational environment that threatens the stability and growth potential of the candy market in Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.26% |

| Segments Covered | By Type, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled | Arcor, August Storck KG, Yildiz Holding, Cemoi, Chocoladefabriken Lindt & Sprungli AG, United Confectionary Manufacturers, Crown Confectionary Co. Ltd, DeMet’s Candy Co, Ezaki Glico Co. Ltd, Ferrero Group, and others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The chocolate candy segment was the largest by holding 58.4% of the Europe Candy Market share in 2025. The growth of the segment is driven by continent's rich confectionery heritage in countries like Belgium, Switzerland, and France, where chocolate making is considered an art form. According to the European Chocolate Association, per capita chocolate consumption in Western Europe exceeds 8 kilograms annually, reflecting a strong cultural affinity for cocoa based products. The segment is driven by the continuous premiumization of offerings, with consumers increasingly willing to pay higher prices for single origin, organic, and ethically sourced chocolates. The versatility of chocolate allows it to be integrated into various formats, from filled pralines to seasonal figures by ensuring year round demand spikes during holidays like Easter and Christmas. Furthermore, the perception of dark chocolate as a healthier option due to its antioxidant properties has broadened its appeal among health conscious demographics. Manufacturers leverage this by highlighting high cocoa content and minimal processing in their marketing strategies. The strong presence of established artisanal brands alongside multinational corporations creates a competitive yet robust ecosystem that sustains high volume sales.

The non chocolate candy segment is projected to expand at a CAGR of 4.5% during the forecast period. The growth of the segment is likely to grow with the surging popularity of gummy candies and functional confectionery that offer added health benefits. The innovation in textures and flavors, including sour, spicy, and exotic fruit blends, keeps the category dynamic and engaging for younger consumers who prioritize sensory experiences. Additionally, the integration of vitamins, minerals, and supplements into gummy formats has created a new sub segment of wellness oriented candies. The absence of cocoa also makes these products more affordable to produce and purchase, appealing to budget conscious shoppers during economic uncertainty. Manufacturers are responding by launching sugar free and vegan variants using pectin instead of gelatin, catering to diverse dietary needs.

By Distribution Channel Insights

The supermarkets segment was the largest with 42.6% of the Europe Candy Market share in 2025 with the extensive geographic reach of supermarket chains and their ability to offer a wide variety of candy brands under one roof, facilitating one stop shopping for households. The channel’s strength lies in its capacity to execute large scale promotional campaigns, such as seasonal discounts and bundle offers, which significantly drive volume sales during peak periods like Halloween and Christmas. Consumers prefer supermarkets for their reliable stock availability and the opportunity to compare prices across different brands and package sizes. The organized retail sector in Spain has expanded its shelf space for impulse buy items near checkout counters, increasing visibility and spontaneous purchases, according to the Spanish Federation of Food and Beverage Industries. Supermarkets also provide valuable data analytics to manufacturers, enabling better inventory management and targeted marketing strategies. The trust associated with established retail chains ensures product authenticity and quality, which is for maintaining consumer confidence.

The online sales segment is likely to witness a fastest CGAR of 8.2% from 2025 to 2034 with the increasing internet penetration and the shifting consumer preference for home delivery convenience. As per Eurostat, e-commerce sales in the European Union increased by 14% in 2023, with the food and beverage category experiencing significant uptake among digital native demographics. The online channel allows consumers to access niche, artisanal, and international candy brands that are not available in local physical stores, catering to diverse and specialized tastes. Platforms like Amazon and specialized confectionery websites offer subscription services and bulk buying options, enhancing customer retention and lifetime value. The ability to read detailed product descriptions and customer reviews helps buyers make informed decisions, particularly for premium and dietary specific products like vegan or sugar free candies. Social media integration further drives traffic to online stores through influencer endorsements and targeted advertising.

REGIONAL ANALYSIS

Germany Candy Market Analysis

Germany was the largest contributor in the Europe candy market by capturing 21.3% of share in 2025 due to its large population and high per capita confectionery consumption. The country’s strong tradition of chocolate and gummy candy production, home to major global brands, creates a robust domestic demand base. According to the German Federal Statistical Office, the average German consumes nearly 10 kilograms of confectionery annually, one of the highest rates in the world. The dense network of supermarkets and discount stores ensures widespread availability and competitive pricing, driving volume sales across all socioeconomic segments. The German Confectionery Industry Association reported that domestic production values remained stable in 2023, supported by steady export demand and resilient local consumption. Cultural habits such as the afternoon coffee break often include sweet treats, reinforcing consistent daily demand. The rise of health consciousness has led to a gradual shift towards dark chocolate and sugar free options, prompting manufacturers to innovate their portfolios. Economic stability in the region supports discretionary spending on premium and artisanal candies, particularly during festive seasons.

United Kingdom Candy Market Analysis

The United Kingdom candy market growth was positioned second by holding 15.4% of the share in 2025, characterized by a strong preference for premium chocolates and rapid e commerce adoption. The country’s diverse multicultural population influences flavor preferences, leading to a wide variety of imported and locally produced confectionery items. As per the Office for National Statistics, online retail sales in the UK reached record highs in 2023, with confectionery being a key category for digital purchases. British consumers are increasingly willing to pay for high quality, ethically sourced, and artisanal chocolates, driving growth in the premium segment. The British Retail Consortium indicated that sales of luxury chocolate brands grew by 10% in 2023, reflecting this shift towards indulgence and quality. The prevalence of convenience stores in urban areas also supports impulse purchases of smaller candy items. Health regulations and sugar taxes have prompted manufacturers to reformulate products, leading to a rise in reduced sugar and plant based options. The strong presence of major retailers like Tesco and Sainsbury’s ensures broad market coverage and effective promotional strategies. The cultural significance of gift giving during holidays further boosts seasonal sales volumes.

France Candy Market Analysis

France candy market growth is expected to have steady opportunities in coming years with its renowned artisanal confectionery tradition and strong tourism sector. The country is famous for its high-quality chocolates and traditional sweets, which attract both locals and millions of tourists annually. According to the French Ministry of Economy, the food and beverage sector, including confectionery, contributes significantly to the national economy, with artisanal shops playing a crucial role in brand prestige. French consumers place a high value on quality and origin, preferring products made with natural ingredients and traditional methods. The National Institute of Statistics and Economic Studies reported that household spending on luxury food items remained resilient in 2023, supporting the premium candy segment. Tourism hubs like Paris and Lyon see heightened demand for specialty chocolates and macarons, driving sales in boutique stores. The government’s support for local agriculture ensures a steady supply of high-quality dairy and sugar, essential for premium confectionery. Seasonal events such as Easter and Christmas are major drivers of sales, with families traditionally exchanging high end chocolate gifts.

Italy Candy Market Analysis

Italy Candy Market growth is likely to have a dominant growth opportunities in coming years with a strong preference for local flavors and seasonal confectionery traditions. Italian consumers favor chocolates infused with hazelnuts, pistachios, and citrus fruits by reflecting the country’s rich agricultural heritage. As per the research, confectionery sales peak during traditional festivals, such as Easter and Christmas, where specific shaped chocolates and sweets are customary gifts. The presence of renowned artisanal chocolatiers in cities like Turin and Perugia enhances the market’s reputation for quality and craftsmanship. Economic challenges have led some consumers to trade down to private label brands, but the demand for authentic Italian specialties remains strong. The tourism sector also contributes significantly, with visitors seeking out local delicacies as souvenirs. Retailers adapt by offering localized assortments that cater to regional tastes, ensuring broad appeal. The integration of traditional recipes with modern packaging and marketing strategies helps maintain relevance among younger demographics.

Spain Candy Market Analysis

Spain candy market growth is driven by urbanization and evolving lifestyle habits that favor convenient snacking. The growing urban population in cities like Madrid and Barcelona has increased the demand for on the go candy options, particularly gummies and small format chocolates. Spanish consumers are increasingly open to international brands and novel flavors, expanding the market beyond traditional local sweets. The Spanish Federation of Food and Beverage Industries noted a rise in sales of sugar free and functional candies, aligning with global health trends. Economic recovery post pandemic has boosted consumer confidence, leading to increased discretionary spending on treats. The warm climate also influences consumption patterns, with higher demand for refreshing and fruity candy varieties during summer months.

COMPETITIVE LANDSCAPE

The competition in the Europe Candy Market is characterized by the presence of both multinational corporations and specialized artisanal producers who vie for consumer attention through quality and innovation. Multinational giants leverage their extensive distribution networks and brand recognition to maintain dominance in mainstream retail channels. Meanwhile, local artisans capitalize on traditional recipes and unique flavor profiles to capture niche markets and premium segments. The market sees frequent product launches featuring organic, vegan, and reduced sugar options to address rising health consciousness among consumers. Price competitiveness remains a crucial factor, particularly in economic downturns where value for money drives purchasing decisions. Retailers play a significant role in shaping competition by offering shelf space and promotional support to preferred brands. Digital transformation has intensified rivalry, with companies investing in online sales channels and personalized marketing to engage directly with buyers.

Key Market Players

- Arcor

- August Storck KG

- Yildiz Holding

- Cemoi

- Chocoladefabriken Lindt & Sprungli AG

- United Confectionery Manufacturers

- Crown Confectionery Co. Ltd

- DeMet’s Candy Company

- Ezaki Glico Co. Ltd

- Ferrero Group

Top Players in the Market

- Ferrero Group maintains a dominant presence in the Europe Candy Market through its iconic brands such as Kinder, Nutella, and Ferrero Rocher. The company leverages its strong family owned heritage to build deep consumer trust and loyalty across the continent. Recent initiatives include significant investments in sustainable cocoa sourcing programs to ensure ethical supply chains and reduce environmental impact. Ferrero has also expanded its production facilities in Poland and Germany to enhance local manufacturing capabilities and reduce logistics costs. The corporation actively engages in digital marketing campaigns that highlight family values and shared moments, resonating with European cultural norms.

- Mars Wrigley Confectionery is a key player in the Europe Candy Market by offering a diverse portfolio that includes Mars, Snickers, Skittles, and M and Ms. The company utilizes its global scale to drive innovation and efficiency in product development and distribution. Recent actions involve the launch of plant based chocolate variants to cater to the growing vegan demographic in Europe. Mars Wrigley has also committed to achieving net zero emissions across its value chain by 2050, aligning with stringent European environmental regulations. The firm invests heavily in personalized marketing strategies using data analytics to engage younger consumers through social media platforms. These efforts reinforce its brand relevance and operational resilience in a highly competitive market environment.

- Lindt and Sprungli stands as a premier player in the Europe Candy Market, renowned for its high quality Swiss chocolate and artisanal craftsmanship. The company focuses on premiumization strategies that appeal to consumers seeking luxury and indulgence in their confectionery choices. Recent developments include the expansion of its retail store network in major European cities to enhance direct consumer engagement and brand experience. Lindt has also introduced sustainable packaging solutions made from recycled materials to address environmental concerns and meet regulatory standards. The firm emphasizes transparency in its cocoa sourcing practices, partnering with farmers to improve livelihoods and ensure quality.

Top Strategies Used by the Key Market Participants

Key players in the Europe Candy Market primarily focus on product innovation to meet evolving consumer demands for healthier and sustainable options. Companies are increasingly reformulating recipes to reduce sugar content and incorporate natural ingredients while maintaining taste quality. Strategic investments in eco friendly packaging solutions help brands comply with strict environmental regulations and appeal to conscious consumers. Expansion into e commerce platforms enables manufacturers to reach wider audiences and offer convenient home delivery services. Partnerships with local suppliers ensure secure raw material sourcing and support community development initiatives. Digital marketing campaigns leveraging social media influencers enhance brand visibility and engage younger demographics effectively.

MARKET SEGMENTATION

This Research Report on Europe candy market is segmented and sub segmented into following categories

By Product Type

- Chocolate Candy

- Non-Chocolate Candy

By Distribution Channel

- Supermarkets

- Convenience Stores

- Grocery Stores

- Online

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe candy market?

The Europe candy market includes the production and sale of sugar confectionery such as gummies, hard candies, toffees, caramels, jellies, and similar sweet products consumed across retail and foodservice channels.

2. What factors are driving growth in the Europe candy market?

Key growth drivers include strong cultural demand for confectionery, product innovation, premiumization, seasonal gifting, and expanding retail distribution.

3. What types of candy are most popular in Europe?

Popular candy types include gummies and jellies, hard-boiled sweets, caramels, toffees, mints, and sugar-free candies.

4. How does health consciousness affect the candy market in Europe?

Rising health awareness is increasing demand for reduced-sugar, sugar-free, organic, and natural-ingredient candies.

5. Which distribution channels dominate the Europe candy market?

Supermarkets and hypermarkets hold the largest market share, followed by convenience stores, online retail, and specialty confectionery stores.

6. Which countries are key contributors to the Europe candy market?

Germany, the United Kingdom, France, Italy, and Spain are major contributors due to high consumption and established confectionery industries.

7. What role does product innovation play in market growth?

Innovation in flavors, textures, packaging, and functional candies (such as vitamin-enriched or herbal sweets) supports sustained market growth.

8. What challenges does the Europe candy market face?

Key challenges include sugar reduction requirements, rising raw material costs, and increasing competition from healthier snack alternatives.

9. Who are the key players in the Europe candy market?

Leading companies include Mars, Incorporated, Ferrero Group, Mondelez International, HARIBO GmbH & Co. KG, and Nestlé S.A.

10. What is the future outlook for the Europe candy market?

The market is expected to grow steadily, driven by premium products, clean-label trends, and evolving consumer preferences.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com