Europe Caps and Closures Market Size, Share, Trends, & Growth Forecast Report By Material (Plastic, Metal, Others), Product Type, Capacity, End-user and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Caps and Closures Market Report Summary

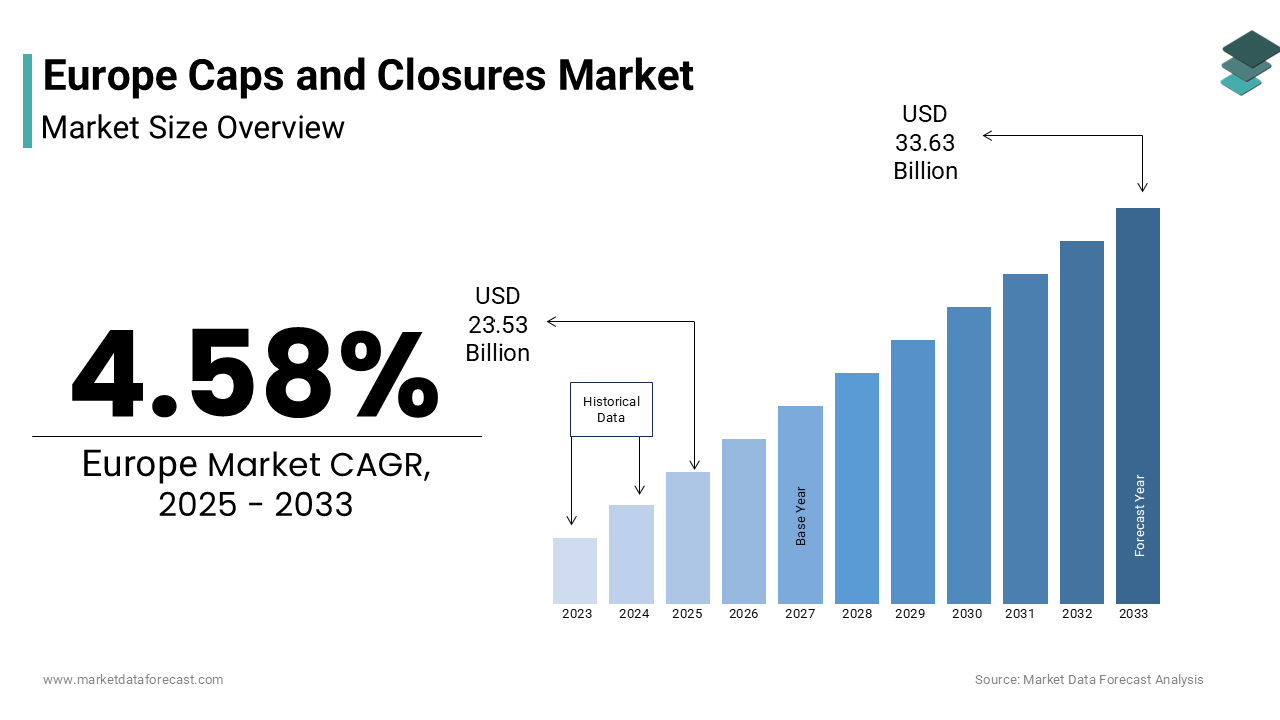

The Europe caps and closures market was valued at USD 22.50 billion in 2024, is anticipated to reach USD 23.53 billion in 2025, and is projected to reach USD 33.63 billion by 2033, growing at a CAGR of 4.58% during the forecast period from 2025 to 2033. The growth of the Europe caps and closures market is driven by stringent EU packaging and circular economy regulations, rising demand for functional and convenience-oriented packaging, and the increasing importance of sustainability, hygiene, and product safety across food & beverage, pharmaceutical, and personal care industries. The transition toward tethered caps, mono-material designs, and recyclable closures, along with enhanced consumer expectations for usability and tamper evidence, is transforming caps and closures from passive packaging components into strategic enablers of regulatory compliance, brand trust, and circular packaging systems across Europe.

Key Market Trends

- Rapid adoption of tethered caps following the EU Single Use Plastics Directive to reduce plastic litter and improve recyclability.

- Growing use of mono-material plastic closures to simplify recycling and comply with circular economy targets.

- Rising demand for convenience-driven closures, including flip-top, sports caps, push–pull, and resealable designs.

- Expansion of child-resistant and tamper-evident closures in pharmaceutical and healthcare packaging.

- Integration of smart and digitally enabled closures, including QR codes, NFC tags, and authentication features for traceability and brand protection.

Segmental Insights

- Based on material, the plastic segment was the largest and held a dominant share of the Europe caps and closures market in 2024. This dominance is attributed to cost efficiency, lightweight properties, chemical resistance, and compatibility with high-speed bottling and capping lines across food, beverage, and personal care applications. Continued innovation in recyclable and mono-material plastic closures has sustained the segment’s leadership despite environmental pressures.

- Based on product type, the screw caps segment accounted for the largest share of the Europe caps and closures market in 2024. The segment’s leadership is driven by universal compatibility, reliable resealability, tamper-evident functionality, and broad usage across beverages, dairy, pharmaceuticals, and household products.

- Based on end-use industry, the food and beverages segment dominated the market in 2024 due to Europe’s extensive dairy, bottled water, soft drinks, and alcoholic beverage industries. High-volume consumption, strict food safety regulations, and the need for extended shelf life continue to support strong demand for advanced closure systems.

Regional Insights

- The Europe caps and closures market shows steady growth across major economies, supported by robust packaging regulations, strong manufacturing infrastructure, and sustainability-driven design innovation.

- Germany was the largest contributor, accounting for 19.5% of the Europe caps and closures market share in 2024, driven by its advanced packaging machinery industry, strong pharmaceutical manufacturing base, and highly developed recycling infrastructure.

- Italy followed closely, supported by its global leadership in wine, olive oil, and bottled water production, along with strong demand for premium aluminum and plastic closures for both domestic consumption and exports.

- France continues to grow steadily due to its large dairy sector, proactive sustainability legislation such as the AGEC Law, and increasing adoption of recyclable mono-material closures by major food and beverage brands.

- The United Kingdom remains a dynamic market, with strong pharmaceutical demand and retailer-led sustainability initiatives driving adoption of child-resistant, tamper-evident, and recyclable closures, despite post-Brexit regulatory adjustments.

Competitive Landscape

The Europe caps and closures market is highly competitive and innovation-driven, characterized by the presence of global packaging leaders and specialized regional manufacturers. Competition is shaped less by price and more by technical capability, regulatory compliance, sustainability innovation, and functional performance. Leading companies are focusing on tethered cap technologies, lightweighting initiatives, recyclable materials, and smart closure solutions to align with EU packaging legislation. Strategic investments in material science, digital traceability, and recycling partnerships are strengthening market positioning. Consolidation remains active as smaller players face rising compliance and tooling costs, while established companies expand through acquisitions and technology upgrades. Prominent players in the Europe caps and closures market include Amcor Plc, Berry Global Group, Inc., AptarGroup, Inc., Silgan Holdings Inc., Coveris Holdings S.A., Gerresheimer AG, ALPLA Werke Alwin Lehner GmbH & Co. KG, Ardagh Group, and HCP Packaging Group.

Europe Caps and Closures Market Size

The europe caps and closures market size was valued at USD 22.50 billion in 2024 and is anticipated to reach USD 23.53 billion in 2025 from USD 33.63 billion by 2033, growing at a CAGR of 4.58% during the forecast period from 2025 to 2033.

Caps and closures refer to components engineered to seal, preserve, and protect packaged goods across food and beverage, pharmaceutical, and personal care sectors. These elements, ranging from screw caps and dispensing closures to tamper evident bands, are indispensable in maintaining product integrity, ensuring regulatory compliance, and enabling consumer convenience. In Europe, the functional design of closures is increasingly shaped by circular economy mandates and evolving hygiene expectations. As per sources, the total amount of packaging waste generated in the EU has shown an overall upward trend over the last decade, despite a slight decrease in the most recent year, intensifying pressure on packaging systems to incorporate recyclable materials and reusable formats. Simultaneously, the European Food Safety Authority has tightened migration limit standards for food contact materials, compelling closure manufacturers to reformulate adhesives and liners. According to research, a significant majority of EU citizens perceive product packaging as an important indicator of a brand's environmental responsibility, which is a key factor influencing regulatory priorities, such as the push for improved closure designs and increased recycling targets. These societal and regulatory currents, though not direct market metrics, define the operational and innovation landscape in which Europe’s caps and closures industry operates, transitioning from passive components to active enablers of sustainability, safety, and brand trust.

MARKET DRIVERS

Stringent EU Packaging and Circular Economy Regulations Drive Sustainable Closure Innovation

The region's regulatory framework exerts powerful influence over cap and closure design, which in turn fuels the growth of the Europe caps and closures market. Specifically, the Packaging and Packaging Waste Regulation and Single Use Plastics Directive mandate recyclability and tethered functionality. Beverage containers sold throughout the EU are now required to have caps that stay connected to the bottle after opening. This requirement applies to all plastic beverage bottles with a capacity of three liters or less. The regulation has led to extensive changes in how closure systems are designed and manufactured across the supply chain. Keeping caps attached to bottles during disposal is a measure intended to help reduce the amount of plastic waste that enters the environment. Compliance has necessitated significant investment in new mold tooling and high speed assembly lines. The implementation of new material requirements is associated with retooling and modification costs for packaging manufacturers. Moreover, the general movement toward enhanced packaging recyclability is accelerating the adoption of mono-material closures. The majority of new closure designs predominantly use materials from the same polymer family, such as polyethylene or polypropylene homopolymers, to assist in simplifying recycling processes. This regulatory impetus is not merely compliance driven; it aligns with Extended Producer Responsibility schemes that shift end of life costs to producers, incentivizing lightweighting and material reduction. Consequently, closures have evolved from commodity components into engineered solutions that directly contribute to brand adherence to Europe’s green industrial policy framework.

Rising Demand for Functional and Convenience Oriented Packaging in Food and Beverage

Changing consumption patterns across Europe, characterized by urbanization, on the go lifestyles, and premiumization, are boosting the expansion of the Europe caps and closures market. This fuels demand for closures that offer dispensing precision, resealability, and user-friendly features. In addition, a portion of the EU population lived in urban or densely populated areas, where single serve and portable formats dominate daily consumption. This shift is particularly evident in dairy and ready to drink beverage segments, where flip top, sports cap, and push pull closures have gained traction. Moreover, aging demographics amplify the need for ergonomic designs. Beverage brands have responded with closures featuring grip enhancements, audible tamper evidence, and controlled pour mechanisms. For instance, premium olive oil producers in Spain and Italy now use pour spouts with anti drip valves, reducing waste and enhancing user experience. These functional upgrades transform closures from passive seals into active touchpoints of brand interaction, aligning product usability with evolving European consumer expectations for convenience without compromising quality.

MARKET RESTRAINTS

Volatility in Polymer Raw Material Prices Constrains Profitability and Planning

Persistent pressure from fluctuating prices of key thermoplastic resins, such as polypropylene and high-density polyethylene, restricts the growth of the Europe caps and closures market. This constitutes a notable share of closure material input. In addition, the European petrochemical industry experienced an increase in polypropylene spot prices due to energy cost spikes and tighter naphtha supply, according to Plastics Europe. This volatility disrupts cost forecasting for closure manufacturers, many of whom operate on narrow margins and lack long term resin contracts with upstream suppliers. Unlike large packaging converters, small and medium enterprises, which form a significant portion of the European closure ecosystem, often absorb these swings, compressing profitability. Bio-based alternatives, such as sugarcane-derived polyethylene, are available but are more expensive and have limited food-grade certifications. This raw material instability not only impedes investment in advanced molding technologies but also complicates compliance with lightweighting targets, as cost constraints may override sustainability goals in procurement decisions. The result is a fragile equilibrium between performance, compliance, and economic viability across the closure supply chain.

Fragmented Recycling Infrastructure Limits Circular Closure Implementation

The fragmented and inconsistent state of municipal recycling systems across member states affects the practical viability of recyclable closure designs, which ultimately hinders the expansion of the Europe caps and closures market. The EU's recycling mandate requires all plastic packaging to be recyclable, but the practical application of collecting and sorting this material varies significantly. One country in Eastern Europe had a recycling rate in the lower range. Another major European country achieved a rate more than double that low figure. The difference between the highest and lowest mechanical recycling rates for post-consumer plastic packaging across Europe was substantial. This disparity creates a critical mismatch. A closure engineered for recyclability in the Netherlands may end up in landfill or incineration in Bulgaria due to inadequate sorting facilities. Furthermore, tethered caps, though legislatively required, pose new challenges for material recovery facilities. In response, some producers resort to oversized or colored caps to improve sortability, but these solutions compromise aesthetics and material efficiency. The absence of a harmonized EU wide collection and sorting standard forces closure designers to adopt lowest common denominator approaches, stifling innovation. Europe's sustainability goals cannot be met because necessary infrastructure investment has not kept pace with the high standards required by advanced closures, which prevents the market from realizing their full circular potential.

MARKET OPPORTUNITIES

Growth in Pharmaceutical and Healthcare Packaging Creates Premium Closure Demand

The expansion of Europe’s pharmaceutical and biotechnology sectors is generating robust demand for high integrity, tamper evident, and child resistant closures that meet stringent regulatory and safety standards. This offers potential opportunities for the expansion of the Europe caps and closures market. The European Medicines Agency authorized numerous new active substances for human use in the European Union, a significant portion of which necessitate specialized containment to maintain their potency and avoid contamination. This trend is amplified by the rise of self-administered therapies, including injectables and oral solids, which rely on closures that integrate with delivery devices or provide clear dosage indication. In Germany and Switzerland, hubs of pharmaceutical manufacturing, demand for aluminum and polymer composite closures with integrated liners grew. Additionally, the EU Falsified Medicines Directive mandates unique serialization and tamper evident features on all prescription drug packaging, compelling closure suppliers to embed breakaway bands, foil seals, or holographic indicators. These requirements elevate closures from passive components to critical safety interfaces. Moreover, aging populations intensify demand for senior friendly yet child safe designs, spurring innovations like push and turn mechanisms with tactile feedback. Unlike commodity closures, these healthcare variants command premium pricing and longer development cycles, offering stable revenue streams and high barriers to entry. The pharmaceutical segment thus represents a strategic growth vector where performance, compliance, and trust converge to redefine closure value.

Adoption of Digital Printing and Smart Closures Enables Brand Differentiation

Advancements in digital decoration and embedded sensing technologies are opening fresh prospects for the expansion of the Europe caps and closures market. This creates the pathway for brand engagement and supply chain transparency through closures. Digital printing on caps, once limited by curvature and material constraints, now allows for high resolution, variable data graphics directly on polyolefin surfaces, enabling batch level customization and anti-counterfeiting. More significantly, the integration of near field communication tags and time temperature indicators into closures is gaining traction in premium wine and vaccine segments. These nascent innovations align with the EU's digital product passport initiatives, which fall under the Ecodesign for Sustainable Products Regulation. As a result, closures are evolving into data carriers that enhance traceability, consumer trust, and regulatory compliance, which transforms a traditionally low visibility component into a strategic brand and sustainability tool.

MARKET CHALLENGES

Counterfeit and Adulteration Risks Undermine Consumer Trust in Sealed Products

Persistent risks of product adulteration and counterfeit refilling, particularly in high value categories like spirits, pharmaceuticals, and premium edible oils, despite advances in tamper evident technologies, challenges the growth of the Europe caps and closures market. Criminal syndicates have developed sophisticated methods to replicate or reuse original closures, compromising product safety and brand reputation. A significant volume of counterfeit alcohol has been seized across the EU. Many instances of these seizures involve bottles that were refilled, using caps that were either authentic or highly similar to the originals. In the pharmaceutical sector, an increase has been noted in the detection of falsified medicines at EU borders. A notable aspect of these cases is the reuse of legitimate child-resistant closures to make the products appear genuine. Traditional tamper bands and induction seals are increasingly circumvented using heat resealing or ultrasonic welding, necessitating multi layer security approaches. However, implementing advanced authentication, such as covert inks, micro text, or digital watermarks, adds cost and complexity that smaller producers struggle to absorb. Consumer awareness remains limited. The risk of malicious closure reuse in Europe will continue to threaten product safety and brand credibility until scalable and affordable anti-counterfeiting solutions become industry-wide standards.

Design Complexity for Multi Material and Reusable Systems Increases Failure Risk

The push toward reusable packaging models and multi material functionality is introducing unprecedented engineering complexity into closure design, which further constrains the expansion of the Europe caps and closures market. This heightens the risk of leakage, malfunction, and user frustration. Systems such as refillable detergent cartridges or returnable glass beverage bottles require closures that withstand repeated opening, cleaning, and resealing cycles while maintaining seal integrity over time. Trends indicate a rise in reported incidents concerning the integrity of containers for household cleaning agents. These issues are often associated with the material performance of components like pump closures after repeated use. Similarly, a related pattern has been noted in the beverage sector, where brands implementing returnable bottle programs are observing an increase in consumer feedback regarding the performance and sealing efficacy of caps. These issues stem from the conflicting demands of durability, material compatibility, and recyclability. For instance, closures combining thermoplastic elastomers with rigid polypropylene offer enhanced grip and sealing but complicate end of life sorting. Moreover, accelerated wear testing standards for reusable closures remain underdeveloped at the EU level, leaving manufacturers to navigate performance validation without harmonized benchmarks. The result is a heightened risk of product recalls, brand erosion, and consumer disengagement with circular packaging initiatives, which affects the very sustainability goals these systems aim to achieve.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Analysed | By Material (Plastic, Metal, Others), Product Type, Capacity, End-user and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Analysed | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Market Leaders Profiled | Amcor Plc, Berry Global Group, Inc., AptarGroup, Inc., Silgan Holdings Inc., RPC Group (now part of Berry Global), Coveris Holdings S.A., Gerresheimer AG, ALPLA Werke Alwin Lehner GmbH & Co. KG, Ardagh Group, and HCP Packaging Group |

SEGMENTAL ANALYSIS

By Material Insights

The plastic segment was the largest segment in the Europe caps and closures market by accounting for a substantial share in 2024. The supremacy of the plastic segment is attributed to versatility, cost efficiency, and compatibility with high-speed capping lines across food, beverage, and personal care sectors. Polypropylene and polyethylene are the most widely used resins due to their chemical resistance, lightweight nature, and suitability for both hot fill and ambient applications. The material’s adaptability to design innovation, such as hinge integration for tethered caps or overmolding for soft touch finishes, further reinforces its lead. Besides, plastic closures enable precise dispensing control in pharmaceutical and cosmetic applications, where metered dosing is critical. Despite environmental pressures, the development of mono material and recyclable closure designs, aligned with the EU Packaging and Packaging Waste Regulation, has sustained plastic’s relevance. Recycling infrastructure improvements, such as automated sorting of polypropylene caps in Germany and the Netherlands, have also mitigated earlier concerns about post-consumer recovery, ensuring plastic remains the material of choice for both legacy and next generation closure systems.

The metal closures segment is expected to exhibit a noteworthy CAGR of 5.8% from 2025 to 2033. The rapid acceleration of the metal closures segment is primarily driven by premiumization in the wine and spirits sector, where aluminum and tinplate closures convey quality, authenticity, and superior hermetic sealing. Metal’s impermeability to oxygen and light preserves product integrity in sensitive applications such as craft beer and edible oils, where oxidation directly impacts shelf life. Furthermore, advances in lightweighting have reduced aluminum cap weight without compromising performance. The material also benefits from Europe’s well established metal recycling streams. These technical and sustainability advantages position metal as a high growth, high value material in segments where product protection and consumer perception intersect.

By Product Type Insights

The screw caps segment led the Europe caps and closures market by holding a 42.1% share in 2024. The prominence of the screw caps segment is credited to universal compatibility with glass and PET containers across beverage, food, and pharmaceutical sectors, coupled with reliable resealability and tamper evident potential. In the dairy industry, for instance, high density polyethylene screw caps with induction seals are standard on milk and juice bottles, ensuring leak proof performance during transport. The format’s mechanical simplicity allows for high speed application reducing production downtime. Additionally, screw caps support diverse functional enhancements, including vented liners for carbonated drinks and child resistant threads for household chemicals. The European Committee for Standardization for plastic screw closures has further harmonized dimensional tolerances, enabling cross border supply chain efficiency. This combination of performance, speed, and standardization ensures screw caps remain the backbone of industrial packaging across Europe.

The tethered caps segment is predicted to witness the highest CAGR of 12.2% during the forecast period due to the EU’s Single Use Plastics Directive, which mandated from July 2024 that all plastic beverage bottles under three liters must feature caps that remain attached after opening. The regulation is designed to stop plastic bottle caps from becoming litter by requiring that they remain attached to their containers, which helps ensure they are recycled along with the bottles. This measure is intended to facilitate the collection and proper disposal of both the cap and the bottle together, supporting overall recycling efforts. The core goal is to reduce the amount of loose cap waste found in the environment. In response, major beverage producers like Coca Cola Europacific Partners and Nestlé Waters have retrofitted billions of bottles with hinge or ring tether systems. The design complexity has spurred innovation in hinge durability and opening torque. Retailers also benefit. Hence, tethered caps are transitioning from compliance obligation to standard industry format, driving unprecedented volume and engineering investment.

By Capacity Insights

The 28 400-neck finish size segment held the leading share of 29.4% of the Europe caps and closures market in 2024. The leading position of the 28 400-neck finish size segment is propelled by decades of infrastructure alignment: bottling lines, capping heads, and quality control systems in major production facilities, from Danone plants in France to Coca Cola bottlers in Spain, are optimized for this dimension. This standard, defined by a 28 millimeter outer diameter and 400 thread count, is the industry norm for still water, soft drinks, juices, and liquid dairy products across the continent. The size balances material efficiency with functional performance, supporting high speed capping while accommodating tamper evident bands and induction seals. Moreover, it is fully compatible with tethered cap mechanisms mandated under EU legislation, enabling seamless regulatory compliance without line retooling. The closure’s wall thickness and thread geometry have been refined over generations to minimize resin use while maintaining torque retention, aligning with lightweighting goals. This deep integration into the packaging ecosystem ensures 28 400 remains the de facto standard for everyday liquid consumption in Europe.

The 38 400-neck finish segment is estimated to register the fastest CAGR of 7.4% from 2025 to 2033. The swift growth of the 38 400-neck finish segment is fueled by rising demand for premium beverages, edible oils, and pharmaceutical syrups that require wider orifice openings for controlled pouring and consumer convenience. In the olive oil sector, producers are increasingly adopting specialized closures designed to improve functionality for consumers. These closures typically incorporate anti-drip spouts and pour control inserts, which help to reduce waste and enhance the overall user experience. This shift towards more premium packaging reflects a broader trend across the industry. Spanish and Italian producers, among others, have notably increased their use of these advanced inserts as they transition towards branded formats that emphasize quality and convenience. Similarly, in pharmaceuticals, this size accommodates child resistant closures with larger internal cavities for desiccants or dispensing mechanisms. The format also supports high integrity sealing for carbonated specialty drinks like craft kombucha, where oxygen ingress must be minimized. Equipment manufacturers such as Krones and Sidel have expanded 38 400 integration into modular bottling lines, reducing conversion costs. The 38/400 closure, meeting European demand for premium liquids, is rapidly adopted for its combined performance and aesthetic qualities.

By End-Use Industry Insights

The food and beverages segment dominated the Europe caps and closures market and captured a 54.1% share in 2024. The growth of the food and beverages segment is propelled by the continent’s dense network of dairy processors, beverage bottlers, and food packers that rely on closures for product safety, shelf life extension, and regulatory compliance. Beverage giants such as AB InBev and Heineken deploy billions of closures annually across beer, soft drinks, and water segments, with specifications varying by carbonation level and container material. The sector’s scale enables closure manufacturers to achieve economies of production, particularly for high volume formats like 28 400 screw caps. Besides, evolving consumer expectations for freshness and convenience, such as resealable snack pouches with zip sliders or flip top yogurt lids, drive continuous design iteration. The European Food Safety Authority’s stringent migration limits for food contact materials further compel closure suppliers to invest in compliant liner technologies. This confluence of volume, regulation, and innovation solidifies food and beverages as the bedrock of Europe’s closure demand.

The pharmaceutical segment is anticipated to witness the fastest CAGR of 8.6% during the forecast period owing to an aging population, rising chronic disease prevalence, and the proliferation of self administered therapies that demand high integrity, tamper evident, and child resistant closures. Many new medications authorized for use are developed as oral solids or liquids that require specific forms of containment. Significant pharmaceutical production in certain European countries contributes to a high regional need for various types of packaging closures, including aluminum induction seals, push-in stoppers, and safety caps that meet regulatory standards. The requirement for unique serialization and tamper-evident features on all prescription medication packaging has increased the complexity and importance of closure systems in ensuring product integrity and safety. Additionally, the rise of biologics and temperature sensitive drugs necessitates closures with integrated desiccants or oxygen absorbers to maintain stability. Hence, the pharmaceutical closure segment offers a high margin, regulation intensive growth corridor.

REGIONAL ANALYSIS

Germany Caps and Closures Market Analysis

Germany was the top performer in the Europe caps and closures market and accounted for a 19.5% share in 2024. The dominance of the German market is primarily driven by its world class packaging machinery industry and stringent adherence to food and pharmaceutical safety standards. Home to global leaders, the country serves as both a producer and consumer of advanced closure systems. Germany’s dual system, managed by organizations like Der Grüne Punkt, ensures high collection rates creating closed loop incentives for closure redesign. The pharmaceutical sector, centered in regions drives demand for high precision closures with tamper evidence and child safety features. Additionally, Germany’s leadership in mechanical engineering enables rapid prototyping of tethered cap molds, supporting the transition mandated by EU legislation. This blend of manufacturing excellence, regulatory foresight, and circular economy infrastructure cements Germany’s position as Europe’s closure innovation engine.

Italy Caps and Closures Market Analysis

Italy was the second-largest country in the European caps and closures market and captured a 15.5% share in 2024. The growth of the Italian market is credited to its global leadership in wine, olive oil, and mineral water production. Italy has a significant output of bottled still and sparkling water, as well as a large volume of wine production, both of which necessitate the use of specialized closures. The diverse needs for sealing these various products drive innovation and efficiency in the closure market. Different types of closures are utilized to maintain the quality and integrity of each beverage type. Aluminum screw caps have largely replaced natural cork in mid tier wines due to consistency and cost, with companies like Guala Closures expanding local production capacity. Export orientation further amplifies scale. A portion of closures produced in Italy serve international markets, particularly in North Africa and Eastern Europe. This combination of agri food dominance, design heritage, and export logistics ensures Italy remains a core pillar of Europe’s closure ecosystem.

France Caps and Closures Market Analysis

France is growing steadily in the Europe caps and closures market, with its massive dairy processing industry and proactive stance on sustainable packaging. The French agricultural sector actively engages in substantial milk production. A significant portion of this milk is then prepared for market using common packaging methods. This typically involves the use of high-density polyethylene, also known as HDPE, bottles. These bottles often incorporate standard safety features, such as tamper evident screw caps and induction seals, before distribution to consumers. Danone’s global headquarters in Paris has driven adoption of recyclable mono material closures across its Activia and Evian lines, influencing supplier behavior nationwide. France also pioneered the AGEC Law, which mandates that all plastic packaging be reusable or recyclable, accelerating closure redesign toward polypropylene homopolymers. In the spirits sector, premium cognac and whiskey producers increasingly use aluminum closures with embossed branding to convey luxury. France stands as a prime example of blending heritage with innovation in closure application, thanks to its significant agricultural yields, proactive regulatory environment, and high consumer environmental awareness.

United Kingdom Caps and Closures Market Analysis

The United Kingdom is gradually expanding in the Europe caps and closures market. It is navigating post Brexit regulatory alignment while advancing circular economy initiatives. Despite departure from the EU, the UK adopted the tethered cap requirement in parallel. The UK’s strong pharmaceutical sector, centered in Cambridge and Oxford, also fuels demand for child resistant and tamper evident closures, with Medicines and Healthcare products Regulatory Agency standards closely mirroring EU norms. Additionally, retailer led sustainability programs push suppliers toward certified recyclable and reusable closure formats. The UK remains a dynamic and highly responsive market to regulation within the European closure landscape, even as it navigates supply chain reconfigurations following Brexit.

Spain Caps and Closures Market Analysis

Spain is anticipated to grow in the Europe caps and closures market from 2025 to 2033 due to its agri food exports and tourism linked consumption. Export markets demand premium formats. In the beverage sector, Iberian bottlers have accelerated adoption of tethered caps ahead of the deadline, supported by local toolmakers in Catalonia. Tourism also drives single serve demand. Closure manufacturers in Valencia and Andalusia have expanded production lines to meet this dual demand from export and domestic channels. With strong agricultural roots and strategic Mediterranean positioning, Spain serves as a vital growth node in Europe’s closure supply chain.

COMPETITIVE LANDSCAPE

Competition in the Europe caps and closures market is intense and innovation driven, characterized by a blend of global industrial giants and specialized regional manufacturers. The landscape is shaped less by price and more by technical capability in sustainable design regulatory compliance and functional performance. Leading players compete through material science breakthroughs such as bio based resins and recycled aluminum as well as smart packaging integrations that support digital traceability. The EU’s stringent packaging legislation acts as both a barrier and catalyst, favoring firms with agile R&D and established recycling partnerships. Consolidation is ongoing as smaller molders struggle with retooling costs for tethered systems while larger entities acquire niche innovators in anti-counterfeiting or dispensing technology. Success increasingly depends on balancing environmental mandates with precision engineering to serve high value segments like pharmaceuticals and premium beverages across diverse national markets.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Caps and Closures Market include

- Amcor Plc

- Berry Global Group, Inc.

- AptarGroup, Inc.

- Silgan Holdings Inc.

- RPC Group (now part of Berry Global)

- Coveris Holdings S.A.

- Gerresheimer AG

- ALPLA Werke Alwin Lehner GmbH & Co. KG

- Ardagh Group

- HCP Packaging Group

Top Players in the Europe Caps and Closures Market

AptarGroup Inc

AptarGroup Inc is a global leader in dispensing and sealing solutions with a strong presence across Europe’s personal care, pharmaceutical, and food and beverage sectors. The company specializes in precision engineered closures that integrate dispensing functionality, child resistance, and sustainability. In recent years, Aptar has expanded its portfolio of mono material and recyclable closures to align with EU packaging regulations. Besides, Aptar enhanced its digital capabilities by embedding QR codes and NFC tags into closures for traceability and consumer engagement, reinforcing its role as an innovator in smart packaging. These initiatives strengthen its global influence while addressing Europe’s circular economy goals.

Crown Holdings Inc

Crown Holdings Inc is a major global producer of metal packaging, including aluminum and steel closures widely used in the European beverage and food industries. The company supplies closures to leading wineries, breweries, and edible oil producers across Southern Europe. It also expanded its production capacity in Spain and Italy to meet rising demand for tethered metal caps compliant with EU Single Use Plastics Directive. Crown’s investment in closed loop recycling partnerships with beverage fillers further bolsters its sustainability credentials. These strategic moves enhance its contribution to both European regulatory compliance and global metal closure innovation.

Guala Closures Group

Guala Closures Group is an Italian based global specialist in aluminum and plastic closures for spirits, wine, and pharmaceutical applications. The company is renowned for its anti counterfeiting technologies, including holographic bands and proprietary thread designs that protect premium brands. It also integrated digital watermarks in collaboration with HolyGrail 2.0 to improve sortability in recycling streams. Guala’s continuous investment in R&D and authentication solutions reinforces its leadership in high value closure segments and solidifies its global footprint through European regulatory and brand protection standards.

Top Strategies Used by the Key Market Participants

Key players in the Europe caps and closures market focus on material innovation by developing mono material and recyclable closures to comply with EU circular economy mandates. They invest heavily in tethered cap technologies to meet the Single Use Plastics Directive requirements effective from 2024. Companies pursue lightweighting initiatives to reduce raw material consumption and lower carbon footprints across the value chain. Strategic collaborations with recycling consortia and digital watermark initiatives like HolyGrail 2.0 enhance post consumer recoverability. Additionally, firms integrate smart features such as QR codes and NFC tags to enable traceability brand authentication and consumer engagement. These strategies collectively drive regulatory alignment sustainability leadership and premium differentiation across Europe’s competitive closure landscape.

MARKET SEGMENTATION

This research report on the europe caps and closures market has been segmented and sub–segmented into the following categories.

By Material

- Plastic

- Metal

- Others

By Product Type

- Tethered Caps

- Push/Pull Caps

- Screw Caps

- Others

By Capacity

- 18-400

- 22-400

- 28-400

- 38-400

- 45-400

- 58-400

- 70-400

- 89-400

- 120-400

- Others

By End-use Industry

- Food & Beverages

- Pharmaceutical

- Consumer Goods

- Personal Care & Cosmetics

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are caps and closures?

Caps and closures are packaging components used to seal containers, ensuring product protection, safety, and convenience.

What is driving growth in the Europe caps and closures market?

Growth is driven by rising packaged food and beverage consumption, pharmaceutical demand, and sustainability-focused packaging regulations.

Which materials are commonly used for caps and closures in Europe?

Common materials include plastics (polypropylene and polyethylene), metals (aluminum and steel), and composite materials.

Which end-use industries dominate the Europe caps and closures market?

Food & beverages, pharmaceuticals, cosmetics & personal care, and household products are the major end users.

Which countries lead the Europe caps and closures market?

Germany, France, the UK, Italy, and Spain are leading markets due to strong manufacturing and retail sectors.

What types of caps and closures are widely used?

Screw caps, flip-top caps, dispensing caps, snap-on caps, and child-resistant closures are widely used.

What role does the food and beverage sector play in market growth?

It is the largest contributor due to high demand for bottled beverages, dairy products, and packaged foods.

What challenges does the Europe caps and closures market face?

Challenges include raw material price volatility, regulatory compliance, and pressure to meet sustainability goals.

What trends are shaping the Europe caps and closures market?

Key trends include sustainable materials, minimalist designs, and customization for branding.

What is the future outlook for the Europe caps and closures market?

The market is expected to grow steadily, supported by sustainability initiatives, innovation, and packaging demand.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com