Europe Carnation Market Size, Share, Trends, & Growth Forecast Report By Product Type ( Fresh Cut Flowers, Potted Plants, Seeds, Others), Application, Distribution Channel and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Carnation Market Report Summary

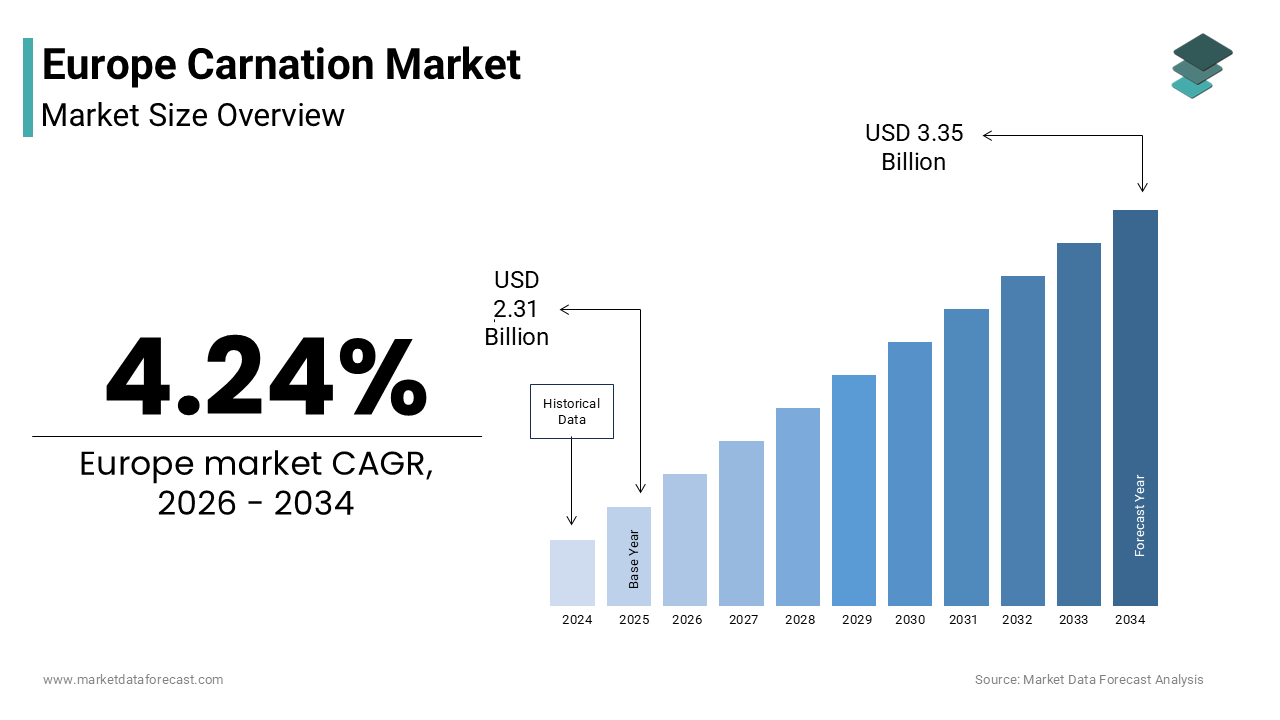

The Europe carnation market was valued at USD 2.31 billion in 2025, is estimated to reach USD 2.46 billion in 2026, and is projected to reach USD 3.35 billion by 2034, growing at a CAGR of 4.24% during the forecast period from 2026 to 2034. The growth of the Europe carnation market is driven by strong cultural and ceremonial significance, rising demand for sustainable and locally grown flowers, and consistent consumption across retail and institutional channels. Carnations remain a staple cut flower due to their long vase life, affordability, and versatility in floral arrangements including weddings, funerals, and public celebrations. Moreover, advancements in breeding, greenhouse cultivation, and traceability certifications are strengthening product quality and sustainability credentials, while expanding applications in cosmetics and natural dyes are creating new value opportunities across the European floriculture sector.

Key Market Trends

-

Sustained demand driven by cultural traditions, ceremonies, and commemorative events across multiple European countries.

-

Increasing consumer preference for locally grown and sustainably certified carnations supporting regional greenhouse production.

-

Continuous breeding innovation enabling new color varieties, improved disease resistance, and extended vase life.

-

The growing popularity of potted carnations as eco-friendly decorative alternatives with longer ornamental value.

-

Rising adoption of digital auction platforms, traceability technologies, and cold-chain logistics to enhance supply chain efficiency.

Segmental Insights

- Based on product type, the fresh cut carnations segment held a prominent share of the Europe carnation market in 2024, supported by their widespread use in bouquets, ceremonial arrangements, and institutional floral services due to durability and visual appeal.

- Based on application, the commercial segment accounted for a significant share of the Europe carnation market in 2024, driven by steady demand from florists, event organizers, hospitality venues, and commemorative institutions requiring reliable floral supply.

- Based on distribution channel, the supermarkets and hypermarkets segment dominated the market with 58.3% share in 2024, attributed to high consumer footfall, impulse purchase behavior, private-label floral programs, and strong cold-chain retail infrastructure.

Regional Insights

The Europe carnation market demonstrates stable growth across key production and consumption regions supported by greenhouse cultivation, cultural usage patterns, and well-established distribution networks.

-

Spain was the largest contributor to the Europe carnation market with a 24.3% share in 2024, supported by favorable climate conditions, extensive greenhouse cultivation, and strong export activity.

-

The Netherlands ranked second, benefiting from advanced greenhouse technologies, breeding innovation, and its dominant role in European flower auctions and logistics.

-

Italy maintains steady demand, driven by ceremonial consumption patterns, organic carnation cultivation, and artisanal floristry traditions.

-

Germany represents a major consumption market, supported by strong supermarket distribution, high per capita flower purchases, and sustainability-focused retail standards.

-

The United Kingdom is experiencing gradual growth, driven by digital gifting trends, locally grown initiatives, and increasing demand for potted ornamental varieties.

Competitive Landscape

The Europe carnation market is characterized by the presence of breeding companies, growers, exporters, auction cooperatives, and distribution specialists competing on quality, sustainability, and supply reliability. Leading players are focusing on developing improved cultivars, strengthening greenhouse efficiency, expanding digital auction participation, and obtaining sustainability certifications to meet retailer requirements. Strategic collaborations with supermarket chains, florists, and e-commerce gifting platforms are further supporting consistent market penetration and volume growth. Prominent players in the Europe carnation market include Dümmen Orange, Selecta One, Syngenta Flowers, Beekenkamp Plants, Florensis, HilverdaFlorist, Fides (Dümmen Orange Group), Queen Flowers Group, Karuturi Global Ltd., and Marginpar BV.

Europe Carnation Market Size

The Europe carnation market size was valued at USD 2.31 billion in 2025 and is anticipated to reach USD 2.46 billion in 2026 from USD 3.35 billion by 2034, growing at a CAGR of 4.24% during the forecast period from 2026 to 2034.

The carnation is the cultivation distribution and retail sale of Dianthus caryophyllus, where a perennial flowering plant valued for its ruffled blooms long vase life and symbolic associations with love admiration and commemoration. Primarily grown in controlled greenhouse environments or open fields depending on regional climate, carnations serve as staple cut flowers in floral arrangements bridal bouquets funerary tributes and institutional gifting across the continent. As per Eurostat, over 1.2 billion stems of carnations were traded within the EU in 2024 reflecting consistent cultural integration into both ceremonial and everyday floral consumption. The spans standard large flowered spray and miniature varieties with color palettes continuously expanded through selective breeding. Production is concentrated in temperate zones with Spain, the Netherlands, and Italy leading domestic supply, while imports supplement seasonal gaps particularly during winter months.

MARKET DRIVERS

Enduring Cultural Significance in Ceremonial and Commemorative Practices

Carnations maintain deep-rooted symbolic relevance traditions, which sustains steady demand irrespective of economic fluctuations. The enduring cultural significance in ceremonial and commemorative practises is majorly propelling the growth of Europe carnation market. In Portugal, red carnations are nationally emblematic commemorating the 1974 Carnation Revolution with annual celebrations driving mass floral purchases each April 25, as documented by the Portuguese National Statistics Institute. Similarly, in Spain and Italy, white carnations are customary in funeral rites and religious processions with the Vatican specifying their use in papal ceremonies according to the Holy See’s Office of Liturgical Celebrations. Mother’s Day remains a critical sales peak; data from the European Florists Federation indicates that carnations accounted for 38% of all flowers gifted on this occasion in 2024 due to their historical association with maternal purity. National holidays, such as Bulgaria’s Rose and Carnation Day further institutionalize consumption. This embeddedness in social rituals ensures baseline demand that transcends trend cycles and supports year-round production planning for growers.

Integration into Sustainable and Locally Sourced Floral Trends

A growing consumer preference for locally grown environmentally responsible flowers is revitalizing European carnation production despite global competition. The integration into sustainable and locally sourced floral trends is escalating the growth of Europe carnation market. According to a 2024 survey by the European Consumer Organisation, 62% of EU floristry buyers now prioritize “locally grown” labels with carnations benefiting due to their adaptability to temperate climates and lower transport footprint compared to tropical imports. Dutch and Spanish growers have responded by obtaining certifications like MPS GAP and Fair Flowers Fair Plants which verify reduced pesticide use water recycling and fair labor practices. In Germany, France, and Scandinavia, farm to vase cooperatives now supply supermarkets with traceable carnation bunches labeled with grower names and carbon metrics. The EU’s Farm to Fork Strategy further incentivizes such practices through grants for closed loop irrigation and biological pest control. This alignment with sustainability values transforms carnations from a commodity into an ethical choice enhancing perceived value and justifying premium pricing in conscious consumer segments.

MARKET RESTRAINTS

Intense Competition from Low Cost Global Imports Undermines Local Growers

The inexpensive imports primarily from Kenya, Ethiopia, and Colombia, where labor and land costs are significantly lower is limiting the growth of Europe carnation market. According to the European Commission’s Directorate General for Trade, over 420 million stems of carnations were imported into the EU in 2024 with Kenya alone supplying 31% of total volume at prices up to 40% below European equivalents. These imports benefit from duty free access under the EU’s Everything but Arms initiative and African Caribbean Pacific agreements, enabling them to dominate price sensitive retail channels like discount supermarkets. Local growers in Southern Europe report shrinking profit margins with many small farms in Andalusia and Sicily ceasing carnation production entirely between 2022 and 2024, as confirmed by national agricultural ministries. Without protective measures or clear origin labeling consumers often unknowingly choose cheaper imports weakening the economic viability of domestic horticulture and threatening rural employment in traditional flower growing regions.

High Input Costs and Stringent Phytosanitary Regulations Increase Operational Burden

Carnation cultivation is increasingly constrained by rising production expenses and rigorous regulatory compliance requirements. The high input costs and stringent phytosanitary regulations increase operational burden is degrading the growth of Europe carnation market. Energy costs for greenhouse heating during winter months, rose by 65% in 2023, according to Eurostat due to post Ukraine war gas price volatility directly impacting Dutch and Belgian growers, who rely on climate-controlled facilities. Simultaneously, the EU’s Sustainable Use of Pesticides Regulation mandates 50% reduction in chemical plant protection products by 2030, forcing rapid transition to biological alternatives that are less predictable and more expensive. Compliance with the Plant Health Law requires extensive documentation traceability and inspection protocols adding administrative overhead. A 2024 study by Wageningen University found that regulatory compliance now accounts for 18% of total operating costs for medium sized carnation farms up from 9% in 2019. These cumulative pressures deter new entrants and accelerate consolidation favoring only large integrated producers with capital to absorb compliance and energy shocks.

MARKET OPPORTUNITIES

Development of Novel Varieties with Extended Vase Life and Unique Aesthetics

Plant breeding innovations are unlocking new potential by addressing key consumer pain points, such as short longevity and limited visual diversity. The development of novel varieties with extended vase life and unique aesthetics is ascribed to bolster new opportunities for the growth of Europe carnation market. European biotech firms and research institutes have developed carnation cultivars with vase lives exceeding 21 days, nearly double traditional varieties as validated by trials at the Royal Horticultural Society in 2024. These include disease resistant strains like ‘Elegance Plus’ and bicolored novelties such as ‘Velvet Flame’ featuring gradient petals. The Netherlands based breeder Dümmen Orange released seven new carnation series in 2024, featuring improved stem strength and heat tolerance enabling better performance in Mediterranean summer conditions. Such advancements allow florists to reduce waste and offer premium bouquets with guaranteed freshness. Retailers like Marks & Spencer and Edeka now exclusively source these enhanced varieties for their branded floral lines capitalizing on quality differentiation in an otherwise commoditized segment.

Expansion into Non Traditional Applications Including Botanical Skincare and Eco Dyes

Carnations are gaining traction beyond floristry through value added applications in cosmetics and sustainable textiles creating alternative revenue streams for growers. The expansion into non-traditional applications including botanical skincare and eco dyes is also enhancing the growth of Europe carnation market. The flower’s high concentration of eugenol and flavonoids has attracted interest from natural skincare brands, where L’Occitane launched a carnation infused facial serum in 2024 sourced from organic farms in Provence leveraging its anti-inflammatory properties. Simultaneously research at the Italian National Research Council confirmed that carnation petal extracts yield stable pink and coral dyes suitable for organic cotton with 80% lower water consumption than synthetic alternatives. This circular economy model enhances farm resilience by monetizing previously discarded biomass and aligns with the European Green Deal’s push for bio based industrial products reducing reliance on volatile cut flower markets.

MARKET CHALLENGES

Climate Change Induced Weather Volatility Disrupts Cultivation Cycles

Unpredictable weather patterns linked to climate change are increasingly destabilizing carnation production is solely a challenge for the growth of Europe carnation market. Unseasonal frosts in early 2024 damaged over 15% of open field crops in central Italy, as reported by Coldiretti the country’s largest agricultural association, while prolonged heatwaves in southern Spain reduced bloom quality and accelerated flowering leading to supply mismatches. In the Netherlands, erratic rainfall disrupted greenhouse humidity control systems causing outbreaks of botrytis with a fungal disease that ruins entire batches. According to the European Environment Agency, the frequency of extreme weather events affecting horticulture has doubled since 2010 with carnations particularly vulnerable due to their narrow optimal temperature range of 15 to 22 degrees Celsius. Without adaptive infrastructure such as hail nets or AI driven climate monitoring small growers remain exposed to yield losses that undermine long term planning and investment.

Labor Shortages in Seasonal Harvesting Hamper Production Scalability

The chronic workforce deficits during harvesting periods due to declining rural populations and reduced availability of seasonal migrant labor is additionally to limit the growth of Europe carnation market. Carnation picking remains largely manual requiring skilled workers to select stems at precise maturity stages, a task not yet fully automatable. According to the European Centre for the Development of Vocational Training, over 30% of horticultural job vacancies in Spain and the Netherlands went unfilled in 2024 with average picker age exceeding 52 years indicating poor generational renewal. The restrictions further limited access to Eastern European labor, historically vital for UK and Irish greenhouses. Consequently, many farms operate below capacity or delay harvests reducing flower quality and market value. Although, robotic prototypes exist their high cost and fragility with delicate blooms limit adoption.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.24% |

| Segments Covered | By Product Type, Application, Distribution Channel and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Dümmen Orange, Selecta One, Syngenta Flowers, Beekenkamp Plants, Florensis, HilverdaFlorist, Fides (Dümmen Orange Group), Queen Flowers Group, Karuturi Global Ltd., and Marginpar BV. |

SEGMENTAL ANALYSIS

By Product Type Insights

The fresh cut carnations segment held a prominent share of the Europe carnation market in 2024 with their entrenched role in ceremonial gifting funerary tributes and institutional floral arrangements where longevity and visual impact are paramount. Carnations’ natural vase life of 10 to 14 days extendable to over 20 days with modern cultivars that makes them economically superior to many alternatives. National holidays, such as Portugal’s Carnation Revolution Day and Bulgaria’s Flower Day drive massive seasonal spikes. Supermarkets, across Germany, France, and Italy dedicate permanent floral sections to pre-arranged carnation bouquets due to consistent weekly demand. Their affordability versatility and symbolic resonance ensure they remain the backbone of commercial floristry despite competition from roses and lilies.

The potted carnations segment is likely to witness a fastest CAGR of 8.9% from 2025 to 2033 owing to the rising consumer interest in living gifts sustainable home decor and extended ornamental value. Unlike cut flowers potted carnations offer weeks or months of bloom with proper care appealing to eco-conscious buyers seeking to reduce floral waste. In Scandinavia and the Netherlands, many Mother’s Day gifts in 2024 were potted plants including miniature carnation varieties bred for compact indoor growth, as reported by national horticultural boards. Urban gardening trends further support adoption with balcony and windowsill cultivation gaining popularity in cities like Berlin and Copenhagen. Breeders like Dummen Orange have launched self branching non pinched potted series that require minimal maintenance enhancing accessibility for novice growers. Retailers, such as IKEA and JYSK now feature these in seasonal home collections capitalizing on the fusion of horticulture and interior design.

By Application Insights

The commercial application segment was accounted in holding a significant share of the Europe carnation market in 2024 from institutionalized demand in floristry events hospitality and public commemoration. Funeral homes, across Italy, Spain, and Greece routinely include white carnations in wreaths and casket sprays as part of longstanding religious customs. Hotels and conference centers in major cities like Paris London and Amsterdam contract weekly floral deliveries featuring carnations for lobby arrangements due to their durability and cost efficiency. National celebrations such as Portugal’s April 25 commemorations or Bulgaria’s May 21 Flower Day generate millions of stems in single day orders. Corporate gifting also contributes significantly with banks telecom companies and government offices using carnation bouquets for client appreciation during holidays. This structured recurring demand provides stable revenue streams for growers independent of retail consumer whims.

The residential use segment is esteemed to grow at a fastest CAGR of 7.6% in next coming years with a broader cultural shift toward home beautification wellness through nature and DIY floral arranging. Post pandemic, 52% of EU households reported increased spending on indoor plants and cut flowers, as per a 2024 Eurobarometer survey. Social media platforms like Instagram and Pinterest have popularized affordable floral styling with carnations featured prominently due to their ruffled texture and color variety. Supermarkets in Germany, and Sweden, now offer “build your own bouquet” stations where consumers mix carnations with greenery fostering engagement. Additionally, urban gardening initiatives in cities like Barcelona and Vienna promote growing dwarf carnation varieties on balconies enhancing emotional connection beyond passive consumption.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest by occupying 58.3% of Europe carnation market share in 2024 from convenience high foot traffic and strategic placement at checkout zones, where impulse purchases thrive. Major retailers like Carrefour, Edeka, Tesco and Auchan, maintain daily floral replenishment ensuring freshness while leveraging private label programs to control pricing. In 2024, over 70% of carnation stems sold in France and Spain moved through supermarket chains often bundled with greeting cards or chocolates for gifting occasions. Their scale enables year-round availability even during off peak seasons through global sourcing networks. Additionally, supermarkets invest in cold chain logistics from distribution centers to store shelves preserving vase life for quality conscious consumers who equate wilted blooms with poor value.

The online stores segment is likely to grow with an anticipated CAGR of 14.2% from 2025 to 2033 with the digital gifting convenience personalized subscription models and next day delivery guarantees. Platforms like Bloom & Wild in the UK and Fleurop in Germany offer curated carnation boxes with hydration pods and care instructions enabling nationwide reach without physical storefronts. Augmented reality features now allow users to preview bouquet sizes in their living rooms reducing return rates. Cross border e-commerce within the EU has also expanded access to specialty growers in the Netherlands and Italy by enabling consumers to order rare spray varieties previously unavailable locally.

REGIONAL ANALYSIS

Spain Carnation Market Analysis

Spain was the largest contributor of the Europe carnation market by holding 24.3% of share in 2024 with the ideal Mediterranean climate extensive greenhouse infrastructure in Almeria and Murcia and deep cultural integration of carnations in festivals and religious rites. Over 12000 hectares are dedicated to carnation cultivation producing more than 500 million, annually primarily for domestic and EU export. The country leads in spray carnation varieties prized for multi bloom stems used in bridal bouquets. Government subsidies under the Common Agricultural Policy support sustainable upgrades including solar powered irrigation and biological pest control.

Netherlands Carnation Market Analysis

The Netherlands carnation market was ranked second by holding 11.2% of share in 2024 with the advanced greenhouse technology and global auction dominance. Dutch growers specialize in large flowered standard carnations with uniform stem length and disease resistance bred through decades of R&D at Wageningen University. Recent investments in geothermal heating and LED supplemental lighting have reduced carbon footprint aligning with EU Green Deal targets while maintaining winter output.

Italy Carnation Market Analysis

Italy carnation market growth is propelled with the strong regional specialization and ceremonial demand. According to Coldiretti, over 65% of Italian carnation use occurs in funerary contexts where white blooms are culturally mandated creating recession resistant demand. The country also leads in organic carnation farming with over 1800 certified hectares supplying premium retailers in Germany and Austria. Local festivals like Rome’s Festa dei Fiori drive seasonal spikes while artisanal florists in Florence and Venice preserve traditional hand tied bouquet techniques that favor carnation texture and longevity over flashier imports.

Germany Carnation Market Analysis

Germany holds 11.2% of the market marked by high per capita consumption and retail sophistication. Its market status reflects disciplined purchasing patterns where carnations rank second only to roses in supermarket floral sections as per GfK consumer tracking. Over 45% of German households buy cut flowers weekly with carnations favored for their price to longevity ratio especially in institutional settings like nursing homes and offices. The country enforces strict labeling requiring origin and cultivation method disclosure empowering conscious buyers to choose local EU grown stems over African imports. Sustainability certifications like MPS ABC are now prerequisites for supermarket shelf placement driving Dutch and Spanish suppliers to adopt cleaner practices to retain access to this critical market.

United Kingdom Carnation Market Analysis

The United Kingdom carnation market growth is anticipated to grow by evolving gifting habits and digital disruption. Urban consumers increasingly prefer potted miniature carnations for apartment gardening while sustainability concerns have revived interest in British greenhouse grown stems despite higher prices. Retailers like Marks & Spencer, now highlight “British Grown” labels to appeal to patriotic and eco conscious shoppers reshaping sourcing dynamics.

COMPETITIVE LANDSCAPE

The Europe carnation market features a complex competitive landscape blending large cooperatives specialized breeders regional growers and global importers. Dutch and Spanish producers dominate domestic supply leveraging advanced greenhouse technology and proximity to key markets while facing pressure from low-cost imports from Africa and South America. Competition centers on quality consistency sustainability credentials and logistical reliability rather than price alone. Supermarkets increasingly dictate terms requiring certified origins reduced carbon footprints and year round availability, which favors integrated players with scale. At the same time niche growers differentiate through heritage varieties organic methods or locally branded bouquets appealing to conscious urban consumers.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Carnation Market include

- Dümmen Orange

- Selecta One

- Syngenta Flowers

- Beekenkamp Plants

- Florensis

- HilverdaFlorist

- Fides (Dümmen Orange Group)

- Queen Flowers Group

- Karuturi Global Ltd.

- Marginpar BV

Top Players in the Market

Royal FloraHolland

Royal FloraHolland is the world’s largest flower auction cooperative and a central pillar of the Europe carnation market through its logistics network breeding partnerships and sustainability initiatives. Headquartered in the Netherlands it connects over 5000 European growers with 120000 buyers across 150 countries facilitating seamless trade of carnations and other ornamentals. The company contributes globally by setting quality standards cold chain protocols and digital trading platforms that shape international floriculture practices. Recently, it launched its “FloraPrime” certification for carnations meeting strict environmental and social criteria including reduced pesticide use and fair labor conditions. It also enhanced its data analytics platform to provide real time demand forecasting helping growers align production with European ceremonial peaks such as Mother’s Day and All Saints Day.

Dümmen Orange

Dümmen Orange is a leading global ornamental plant breeder with significant influence in the Europe carnation market through its innovative genetics and proprietary cultivars. Based in the Netherlands the company develops carnation varieties with extended vase life disease resistance and unique color patterns tailored to European consumer preferences and climate conditions. Its “Elegance” and “Charm” series are widely grown across Spain Italy and Germany for both cut flower and potted applications. It also introduced blockchain enabled traceability allowing retailers to verify origin and sustainability credentials directly from seed to bouquet.

Rudy’s Carnations

Rudy’s Carnations is a prominent Spanish producer and exporter specializing in high quality spray and standard carnations from its integrated greenhouse facilities in Almería. The company plays a vital role in supplying fresh cut carnations to major European supermarket chains and florists particularly in France Germany and the UK. Known for consistent stem length bloom uniformity and post harvest longevity Rudy’s has built strong brand recognition among institutional buyers. In recent developments the company invested in solar powered desalination units to address water scarcity and launched a carbon neutral shipping program using electric refrigerated vans for local distribution. It also partnered with Spanish universities to develop biocontrol solutions against thrips reducing reliance on chemical pesticides in line with EU Green Deal objectives.

Top Strategies Used by the Key Market Participants

Key players in the Europe carnation market are prioritizing sustainability through certifications like MPS GAP and Fair Flowers Fair Plants to meet retailer and consumer demands. They are investing in advanced breeding programs to develop varieties with longer vase life disease resistance and climate adaptability. Vertical integration from seed to shelf ensures quality control and supply chain resilience especially during peak seasons. Companies are adopting digital technologies including blockchain traceability AI driven demand forecasting and e auction platforms to enhance transparency and efficiency. Additionally, strategic partnerships with supermarkets florists and e-commerce gifting platforms help secure recurring volume and expand reach beyond traditional wholesale channels.

MARKET SEGMENTATION

This research report on the Europe carnation market has been segmented and sub-segmented based on the following categories.

By Product Type

- Fresh Cut Flowers

- Potted Plants

- Seeds

- Others

By Application

- Commercial

- Residential

- Others

By Distribution Channel

- Online Stores

- Supermarkets/Hypermarkets

- Specialty St

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com