Europe Cell Culture Market Research Report By Product, Application, End User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, Size, Share, Trends, COVID-19 Impact & Growth Forecast (2025 to 2033)

Europe Cell Culture Market Summary

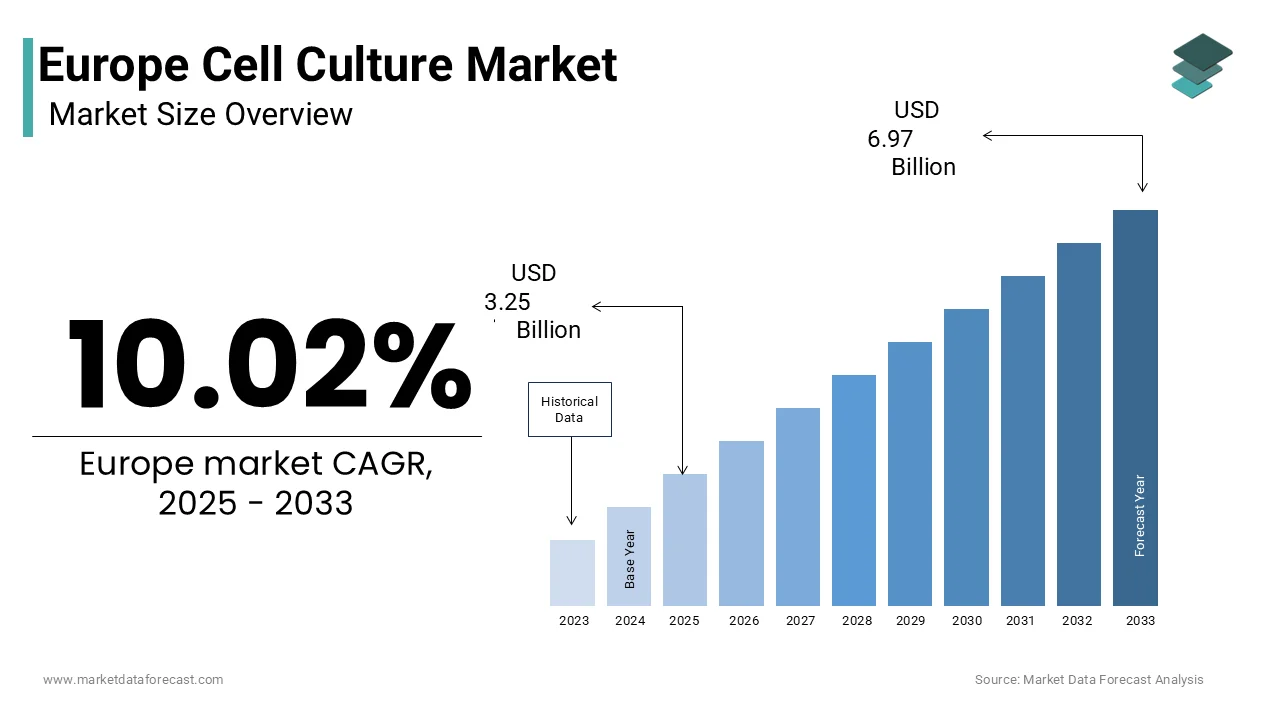

Europe cell culture market was valued at USD 2.95B in 2024, estimated at USD 3.25B in 2025, and is forecast to reach USD 6.97B by 2033 (CAGR 10.02%, 2025–2033) — fuelled by ATMP scale-up, organoid/3D model adoption, and decentralized GMP platforms.

Market Highlights

- 2024 value: USD 2.95 billion

- 2025 (est): USD 3.25 billion

- 2033 forecast: USD 6.97 billion

- CAGR (2025–2033): 10.02%

Quick growth drivers

- Rapid expansion of advanced therapy medicinal products (ATMPs) and CAR-T/allogeneic cell manufacturing.

- Widespread adoption of 3D models & organoids for drug discovery and toxicity testing.

- Demand for GMP-grade, chemically defined & xeno-free media for clinical translation.

- Investments in decentralized/point-of-care manufacturing and single-use closed systems.

- Strong public & private R&D funding across Germany, the UK, France, and research hubs.

Principal restraints

- High capital and operating costs for GMP facilities and closed-system bioprocessing.

- Complex ethical & regulatory oversight for human-derived materials (traceability, consent, GDPR).

- Batch-to-batch variability in biological reagents undermines reproducibility.

- Skills gap in advanced cell processing, bioreactor operation, and 3D/ORGANOID protocols.

High-value opportunities

- AI-powered culture monitoring and predictive analytics to increase reproducibility and reduce hands-on time.

- Decentralized manufacturing (hospital/bedside CAR-T platforms) is expanding point-of-care demand.

- Growth of serum-free & chemically defined media platforms as regulatory/ethical pressure rises.

- Integrated media + single-use bioreactor + analytics bundles for SMEs and hospital labs.

Key operational challenges

- Harmonizing supplier qualification & reference standards to reduce reagent variability.

- Scaling GMP workflows while preserving cell phenotype and potency (QbD demands).

- Training and retaining personnel skilled in cell therapy manufacturing and organoid workflows.

- Ensuring supply-chain resilience for critical media, reagents, and single-use consumables.

Fastest-growing segments

Regenerative medicine & cell therapy: ~14.6% CAGR — highest growth (clinical scale-up demand).

- Serum-free/chemically defined media: ~11.2% CAGR — regulatory & ethical tailwinds.

- Academic & research labs (users): ~10.2% CAGR — public funding for organoids, disease models.

Regional leadership & dynamics

- Germany (34.2%) — largest market: strong biopharma base (Miltenyi, Sartorius), Fraunhofer/FH cores, Paul Ehrlich Institute activity.

- United Kingdom (23.4%) — major R&D and translational hub (Crick, Cambridge), active ATMP ecosystem.

- France — public funding and hospital-based GMP units (Plan France 2030).

- Rest of Europe: growing pockets of capability as decentralized and point-of-care models expand.

What wins commercially

- End-to-end validated workflows (media → closed single-use bioreactor → analytics) that de-risk GMP translation.

- Regulatory-ready product documentation (traceability, COAs) and EU manufacturing footprint.

- Strong scientific partnerships with academic centres to validate organoid/ATMP protocols.

- Digital monitoring + remote QC to support decentralized manufacturing and reproducibility.

Top strategic

Invest in chemically defined media R&D, expand EU GMP capacity (or partnerships), and rapidly integrate AI monitoring + analytics into product suites — while launching clinician training programs to support decentralized manufacturing adoption.

Leading players

Thermo Fisher Scientific · Merck KGaA · Sartorius AG · GE Healthcare · Eppendorf AG · Lonza · Corning · BD · PromoCell · Hi-Media Laboratories

Europe Cell Culture Market Size

The europe cell culture market was valued at USD 2.95 billion in 2024, is expected to have a 10.02 % CAGR from 2025 to 2033, and be worth USD 6.97 billion by 2033 from USD 3.25 billion in 2025.

Cell culture refers to the in vitro growth and maintenance of cells derived from multicellular organisms under controlled laboratory conditions, serving as a foundational technique in biomedical research, biopharmaceutical production, regenerative medicine, and diagnostics. In Europe, cell culture technologies are integral to drug development, vaccine manufacturing, and advanced therapy medicinal products, including CAR T cells and tissue-engineered constructs. The European Union maintains rigorous quality and safety standards under the European Medicines Agency and Directive 2004 23 EC on human tissues and cells, which govern the sourcing, handling, and traceability of biological materials.

MARKET DRIVERS

Expansion of Advanced Therapy Medicinal Products Development

The rapid advancement of advanced therapy medicinal products is driving the growth of the European cell culture market. As per the sources, 38 advanced therapy products received marketing authorization in the EU between 2018 and 2023, with cell-based therapies constituting over 60% of approvals. These include autologous CAR T cell treatments for hematologic malignancies and allogeneic mesenchymal stem cell therapies for graft versus host disease. The production of such therapies requires large-scale expansion of human primary cells under Good Manufacturing Practice conditions, directly increasing reliance on serum-free media, bioreactors, and closed culture systems. National regulatory agencies such as Germany’s Paul Ehrlich Institute have streamlined ATMP clinical trial applications, reducing approval timelines. This regulatory and financial momentum accelerates clinical translation and sustains high demand for specialized culture consumables and platforms across the region.

Rise of Organoid and 3D Cell Culture Models in Preclinical Research

The shift from traditional 2D monolayers to physiologically relevant 3D cell culture models is reshaping preclinical research is escalating the growth of the European cell culture market. Organoids and spheroids better recapitulate tissue architecture, cell-cell interactions, and drug response profiles, making them indispensable in oncology, neurology, and infectious disease studies. The Human Cell Atlas initiative, co-funded by the European Research Council, has generated organoid libraries from over 50 human tissues, all requiring specialized extracellular matrices and differentiation media. Furthermore, the European Centre for the Validation of Alternative Methods now recommends organoid-based assays for hepatotoxicity and neurotoxicity testing by reducing animal use in line with 3Rs principles.

MARKET RESTRAINTS

High Costs and Complexity of GMP Compliant Cell Culture Systems

The expense and operational intricacy of Good Manufacturing Practice compliant cell culture infrastructure, particularly for academic and small biotech entities, is restraining the growth othe f the European cell culture market. Establishing a GMP cell processing facility requires investments exceeding 5 million euros for cleanroom construction, environmental monitoring, and closed-system bioreactors. Additionally, the cost of xeno-free and chemically defined media can exceed 500 euros per liter, with a single CAR T therapy batch consuming up to 20 liters. As per the research, 68% of emerging cell therapy developers cite media and reagent costs as a top barrier to clinical scale-up. Regulatory documentation further adds burden, where the European Medicines Agency requires full traceability of every raw material, including certificates of analysis for fetal bovine serum alternatives. These financial and administrative hurdles limit the scalability of cell-based innovations and delay patient access to novel therapies, especially in Southern and Eastern Europe, where public funding is constrained.

Stringent Regulatory and Ethical Oversight on Human-Derived Cell Lines

The use of human-derived cells in culture is governed by a complex web of ethical and regulatory requirements that slow research timelines and increase compliance costs. The stringent regulatory and ethical oversight on human derived in human-derived cell lines is also hindering the growth of the European cell culture market. Directive 2004 23 EC mandates informed consent, donor screening, and traceability for all human tissues used in research or therapy, enforced by national competent authorities, such as the UK’s Human Tissue Authority and France’s Agence de la Biomédecine. As per the European Society for Gene and Cell Therapy, researchers in Germany and Italy reported average delays of 14 to 18 weeks in obtaining ethical approvals for primary cell studies in 2023. Moreover, the General Data Protection Regulation imposes strict controls on genetic and health data linked to donor samples, complicating multi-center collaborations. Restrictions on embryonic stem cell research persist in countries like Poland and Lithuania, limiting model availability.

MARKET OPPORTUNITIES

Integration of AI-Driven Cell Culture Monitoring Platforms

The incorporation of artificial intelligence and real-time analytics into cell culture workflows to enhance reproducibility and reduce manual intervention is one of the significant opportunities enhancing the growth of European cell AI-powered imaging systems can track confluency, morphology, and contamination in live cultures without labeling, enabling predictive media change or passaging decisions. Companies like CytoSMART Technologies in the Netherlands offer cloud-connected incubator microscopes that feed data into machine learning models for anomaly detection. The Horizon Europe program funded the SmartCulture initiative in 2023 with 28 million euros to develop autonomous culture platforms for stem cell expansion. These digital tools not only improve data integrity but also support compliance with ALCOA+ principles for regulatory submissions, positioning intelligent cell culture as a cornerstone of next-generation biomanufacturing.

Growth of Decentralized Cell Therapy Manufacturing Networks

The emergence of point-of-care and decentralized manufacturing models for autologous cell therapies is creating new demand for compact, automated cell culture systems. This factor is escalating the growth of the European cell culture market. Unlike centralized facilities, decentralized models process patient cells at or near treatment centers by reducing logistics risks and vein-to-vein time. As per the source, 22 hospitals across Germany, France, and the UK implemented bedside CAR T manufacturing in 2023 using closed, functionally automated platforms like the CliniMACS Prodigy. The European Commission’s Joint Research Centre has endorsed CH systems for rural and underserved regions to improve therapeutic equity. These platforms integrate cell isolation, activation, expansion, and formulation in a single device by requiring specialized single-use culture cassettes and pre-formulated media bags.

MARKET CHALLENGES

Batch-to-Batch Variability in Biological Reagents

The inconsistent performance of biological reagents, such as growth factors, sera, and extracellular matrices, undermines experimental reproducibility and therapeutic consistency, which is a challenge for the growth of the European cell culture market. Many culture media still rely on recombinant proteins or animal-derived components, whose activity can vary significantly between lots. Stem cell differentiation failures in European labs were traced to unreported batch variations in commercial growth factor kits. Even serum-free formulations may contain undefined hydrolysates whose composition shifts with raw material sources. While chemically defined media offer a solution, they remain unsuitable for many primary cell types. This variability not only wastes resources but also compromises regulatory filings, highlighting an urgent need for standardized reference materials and stricter supplier qualification across the European supply chain.

Shortage of Skilled Personnel in Advanced Cell Culture Techniques

The rapid evolution of cell culture technologies has outpaced workforce training, creating a skills gap that impedes adoption and operational efficiency. The shortage of skilled personnel in advanced cell culture techniques is significantly declining the growth of the European cell culture market. Complex techniques such as 3D bioprinting, organoid differentiation, and closed-system bioreactor operation require specialized knowledge rarely covered in standard biology curricula. Academic labs often lack resources to train students on industrial-scale platforms, while industry faces high turnover due to competitive global demand. The European Skills Agenda has identified advanced cell culture as a priority competency, yet only 8 member states offer certified vocational programs in cell processing.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product, Application, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Thermo Fisher Scientific, GE Healthcare, Merck KGaA, Sartorius AG, Eppendorf AG, Lonza AG, Corning, Becton, Dickinson and Company, Promocell GmbH, Hi-Media Laboratories |

SEGMENTAL ANALYSIS

By Type Insights

The specialty media segment was the largest by holding 34.3% of the European Cell Culture Market share in 2024 due to its tailored formulations for specific cell types, including stem cells, primary cells, hybridomas, and immune cells. As per the European Molecular Biology Laboratory, advanced therapy and organoid research conducted in EU academic centers in 2023 relied on specialty media from vendors like Thermo Fisher Scientific and Merck. The European Medicines Agency requires chemically defined or xeno-free specialty media for Phase II and III cell therapy trials to ensure batch consistency and reduce immunogenicity risks. Furthermore, national biobanks such as the UK Stem Cell Bank mandate the use of GMP-grade specialty media for master cell bank derivation. This convergence of regulatory expectations, scientific complexity, and therapeutic innovation ensures sustained dominance of specialty media across research and clinical applications.

Serum-free media segment is expected to witness the fastest CAGR of 11.2% from 2025 to 2033 due to regulatory mandates, ethical concerns, and the need for reproducible bioprocessing in biopharmaceutical and cell therapy production. Fetal bovine serum carries risks of pathogen contamination, batch variability, and ethical controversy due to animal sourcing. The marketing authorization applications for advanced therapy medicinal products submitted in 2023 specified serum-free or chemically defined culture conditions. The European Commission’s 2023 update to Directive 2004 23 EC emphasized minimizing animal-derived components in human cell products, further accelerating adoption. Companies like Lonza and Sartorius have developed serum-free platforms for CAR T expansion that reduce production time by 30% while improving T cell persistence. Additionally, the European Federation of Pharmaceutical Industries and Associations reported that 78% of new monoclonal antibody manufacturing processes launched in the EU in 2023 used serum-free CHO cell culture.

By Application Insights

The drug screening and development segment held a significant share of the European cell culture market in 2024, owing to the extensive use of cell culture in target validation, toxicity testing, and lead optimization across Europe’s robust pharmaceutical sector. High-throughput screening platforms utilizing hepatocytes, cardiomyocytes, and neuronal cell lines are now standard in preclinical pipelines to assess metabolic stability and off-target effects. The European Medicines Agency’s 2023 guidance on non-clinical safety studies explicitly endorses human-relevant in vitro models for reducing animal testing under the 3Rs framework. Major companies like Novartis, Roch, and AstraZeneca operate centralized cell culture screening hubs, respectively processing over 50000 compound assays monthly. The integration of 3D spheroids and organ-on-chip models has further increased physiological relevance, enhancing predictive accuracy and reducing late-stage attrition.

The regenerative medicine and cell therapy segment is likely to grow at an anticipated CAGR of 14.6% during the forecast period. These therapies require large-scale expansion under GMP conditions using specialized media bioreactors and closed systems. The European Commission’s ATMP classification provides expedited review pathways with 12 products approved in 2023 alone. National healthcare systems in Germany, France, and the UK have begun reimbursing approved cell therapies, such as Kymriah and Yescart, creating commercial viability. Academic medical centers like Karolinska University Hospital and University Hospital Heidelberg now operate hospital-based cleanrooms for point-of-care manufacturing.

By End User Insights

The biotechnology and pharmaceutical companies segment accounted in holding 46.4% of the European cell culture market share in 2024 due to their high consumption of GMP-grade media reagents and bioreactor systems for drug development and biologics manufacturing. The EU biopharmaceutical sector employed over 900,000 people in 2023 and generated 310 billion euros in revenue, with monoclonal antibody vaccines and cell therapies forming the core portfolio. These products rely on continuous cell culture processes, often using CHO or HEK293 cell lines grown in thousands of liters of serum-free media annually. Regulatory compliance demands extensive documentation, traceability, and quality control for every culture component. Companies like Sano, fi GSK, and BioNTech maintain dedicated cell culture suites with automated monitoring and environmental controls. The European Medicines Agency’s Process Validation guidelines require media lot testing and process consistency across batches, further increasing consumption. This industrial scale, operational rigor, and regulatory dependency ensure that the biopharma sector remains the primary driver of high-value cell culture consumables in Europe.

The academic and research laboratories segment is anticipated to witness the fastest CAGR of 10.2% from 2025 to 2033, driven by massive public investment in basic science organoid technology and disease modeling. Institutions like the Francis Crick Institute and Max Planck Society have established core cell culture facilities offering advanced service, including CRISPR editing, 3D culture, and live cell imaging. The life science PhD programs in Western Europe now include mandatory training in primary and stem cell culture. National initiatives, such as Germany’s Cell Atlas and France’s France BioIma, are going to provide subsidized access to high-end culture platforms. Additionally, the shift toward open science encourages data sharing, requiring standardized media and protocols across labs. This surge in publicly funded discovery science is expanding the user base and accelerating the adoption of next-generation culture technologies beyond traditional industrial settings.

COUNTRY LEVEL ANALYSIS

Germany Cell Culture Market Analysis

Germany was the top performer of the European Cell Culture Market by accounting for 34.2% of the share in 2024, with a world-class biopharmaceutical industry, elite research infrastructure, and strong public funding for life sciences. As per the German Federal Ministry of Education and Research, the country invested in biotechnology R and D with cell-based therapies and organoid models as key priorities. The nation hosts over 30 Fraunhofer and Helmholtz institutes that operate advanced cell culture core facilities serving both academia and industry. Companies like Miltenyi Biotec and Sartori, us headquartered in Germany, are global leaders in cell processing and bioreactor technologies. Additionally, the Paul Ehrlich Institute has approved 18 advanced therapy trials in 2023 alone, demonstrating a streamlined regulatory pathway.

United Kingdom Cell Culture Market Analysis

The United Kingdom was positioned second by capturing 23.4% of the European cell culture market share in 2024 for cell culture innovation anchored by globally recognized research institutions and a mature cell therapy ecosystem. The Francis Crick Institute and University of Cambridge lead in organoid and stem cell research, utilizing over 50000 square meters of dedicated cell culture space. The Medicines and Healthcare products Regulatory Agency has authorized 14 ATMPs since 2020, with streamlined clinical trial processes. The presence of commercial developers like Autolus and Freeline Therapeutics further strengthens industrial demand. This blend of academic excellence, regulatory agility, and commercial translation sustains the UK’s strong market position.

France Cell Culture Market Analysis

France Cell Culture Market growth is driven by centralized research governance, strong hospital-based trials, and national biomanufacturing initiatives. The national Plan France 2030 allocated 1.2 billion euros to advanced therapies, including the construction of eight hospital-based GMP cell production units by 2026. Institutions like Institut Curie and INSERM maintain large-scale culture facilities specializing in dendritic cell and CAR T manufacturing. The National Agency for Medicines and Health Products Safety has reduced ATMP trial approval times to under 60 days. Additionally, French biotech firms, such as Cellectis, are global pioneers in allogeneic cell engineering.

TOP LEADING PLAYERS IN THE MARKET

- Merck KGaA is a leading life science company with a substantial footprint in the European Cell Culture Market through its MilliporeSigma brand. The company offers a comprehensive portfolio, including specialty and serum-free media, recombinant growth factor, and single-use bioreactors tailored for biopharmaceutical and cell therapy applications. Merck supplies GMP-grade cell culture solutions to over 500 academic and industrial clients across Europe. The company expanded its M Lab Collaboration Center in Molsheim, France, to include a dedicated advanced therapy suite for process development. It also launched a chemically defined media platform for allogeneic T cell expansion that reduces differentiation drift. These initiatives reinforce Merck’s role as a strategic partner in Europe’s transition toward standardized and scalable cell culture manufacturing.

- Thermo Fisher Scientific is a global leader in life sciences with deep integration in the European Cell Culture Market through its Gibco and Invitrogen brands. The company provides classical and specialty media serum-free formulations and cell culture reagents used in research, bioproduction, and regenerative medicine. Thermo Fisher operates GMP-compliant manufacturing facilities in Scotland and Germany, ensuring rapid supply across the EU. In early 2024, the company introduced an advanced organoid culture kit optimized for colorectal and pancreatic tumor models developed in collaboration with the Hubrecht Institute. It also enhanced its CTS portfolio with xeno-free cytokines for clinical-scale immune cell expansion. These science-driven innovations strengthen its position as a trusted enabler of both discovery and therapeutic cell culture workflows in Europe.

- Sartorius AG is a Germany-based technology provider specializing in bioprocess solutions with growing influence in the European Cell Culture Market. The company offers integrated systems combining bioreactors, media, and analytics for adherent and suspension cell cultures used in monoclonal antibody and cell therapy production. Sartorius’ AMBR automated micro bioreactor platforms are widely adopted by European pharma for process optimization. Sartorius launched a closed continuous perfusion system for CAR T cell manufacturing at its Göttingen facility,t y enabling high yield expansion with minimal manual intervention. The company also partnered with academic hospitals to validate its media formulations in clinical trials.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Cell Culture Market focus on developing chemically defined and xeno-free media formulations to meet stringent regulatory requirements for advanced therapy medicinal products. They invest in GMP-compliant manufacturing facilities within the EU to ensure supply chain resilience and reduce import dependencies. Companies expand application-specific portfolios through collaborations with academic and clinical institutions to co-develop validated protocols for organoids, immune cells, and stem cells. Strategic enhancement of single-use and closed system technologies supports decentralized and point-of-care manufacturing models. Additionally, firms integrate digital monitoring and process analytics to improve reproducibility and align with Quality by Design principles. These strategies collectively address scientific, regulatory, and operational demands across research and therapeutic segments.

COMPETITIVE LANDSCAPE

The Europe Cell Culture Market features intense competition among global life science leaders, European bioprocess specialists, and niche innovators to offer application-specific solutions. The market is segmented along technical sophistication, with classical media dominated by price competition while specialty answerum-free segments emphasize formulation expertise, regulatory compliance, and technical support. Barriers to entry are high due to the need for GMP certification, stringent quality control, and deep scientific validation. Leading players differentiate through vertical integration, offering end-to-end solutions from media to bioreactors and analytics. Academic and hospital-based developers increasingly demand customizable yet standardized systems, prompting vendors to balance flexibility with reproducibility. Collaboration with public research initiatives and participation in regulatory forums further strengthened the market position.

KEY MARKET PLAYERS

A few prominent companies in the europe cell culture market profiled in this report are

- Thermo Fisher Scientific

- GE Healthcare

- Merck KGaA

- Sartorius AG

- Eppendorf AG

- Lonza AG

- Corning

- Becton, Dickinson and Company

- Promocell GmbH

- Hi-Media Laboratories

MARKET SEGMENTATION

This research report on the europe cell culture market has been segmented and sub-segmented into the following categories.

By Product

-

Equipment

- Bioreactors

- Cell Culture Vessels

- Cell Culture Storage Equipment

- Cell Culture Supporting Equipment

- Consumables

- Sera, Media & Reagents

- Bioreactor Accessories

By Application

- Biopharmaceutical

- Vaccine Production

- Diagnostics

- Recombinant Therapeutic Proteins

- Cancer Research

- Stem Cell Technologies

- Drug Screening and Development

- Tissue Engineering & Regenerative Medicine

- Other Applications

By End-User

- Pharmaceutical and Biotechnology Companies

- Research Institutes

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Who are the major players in the Europe Cell Culture Market?

Leading companies in the Europe Cell Culture Market include Thermo Fisher Scientific, Merck KGaA, Sartorius AG, Lonza, and Miltenyi Biotec. They dominate media, reagents, and equipment, with expansions like Sartorius' German tech center enhancing scalability for biopharma needs

2. What drives the Europe Cell Culture Market growth?

Growth in the Europe Cell Culture Market stems from biopharmaceutical demand, chronic disease research, and tech advances like 3D cultures. Germany's pharma sector holds 29.9% share, while biologics pipelines in the UK and Switzerland increase needs for high-yield media

3. What are key segments in the Europe Cell Culture Market?

The Europe Cell Culture Market segments by media types like serum-free (40% share), classical, and stem cell media; applications include biopharma production, drug screening, and tissue engineering. Equipment like bioreactors and consumables also feature prominently

4. What role does serum-free media play in the Europe Cell Culture Market?

Serum-free media dominates the Europe Cell Culture Market at 40% share due to contamination risks reduction, batch consistency, and animal-free preferences for vaccines and therapies. EU regulations favor it in biopharma hubs (

5. What are applications of the Europe Cell Culture Market?

Applications in the Europe Cell Culture Market span biopharmaceutical production (largest share), drug development, diagnostics, and regenerative medicine. Monoclonal antibodies and cell therapies rely on scalable mammalian cultures

6. What challenges face the Europe Cell Culture Market?

The Europe Cell Culture Market grapples with high equipment costs, infrastructure gaps, and varying EU regulations across countries. These limit scalability despite growth in biologics and research funding

7. How does Poland impact the Europe Cell Culture Market?

Poland grows fastest in the Europe Cell Culture Market via R&D investments, biotech startups, and policies. It supports serum-free media demand amid regional shifts toward Eastern Europe hubs

8. Are there innovations in the Europe Cell Culture Market?

Innovations like 3D cell culture and automation shape the Europe Cell Culture Market, improving precision for drug screening. Companies invest in chemically defined media for better yields in regenerative applications

9. What regulations affect the Europe Cell Culture Market?

Strict EU GMP standards and Horizon programs regulate the Europe Cell Culture Market, favoring serum-free, animal-component-free media. Compliance challenges vary by country but support biologics safety

10. What future trends shape the Europe Cell Culture Market?

Trends in the Europe Cell Culture Market include cell/gene therapy rise, AI-driven optimization, and sustainable media. France and UK lead in scaffolds, with overall CAGR near 10% to 2033 amid vaccine demands

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com