Europe Chemical Logistics Market Size, Share, Trends & Growth Forecast Report, Segmented By End-User, Mode of Transport, Service, Cargo Form, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Chemical Logistics Market Size

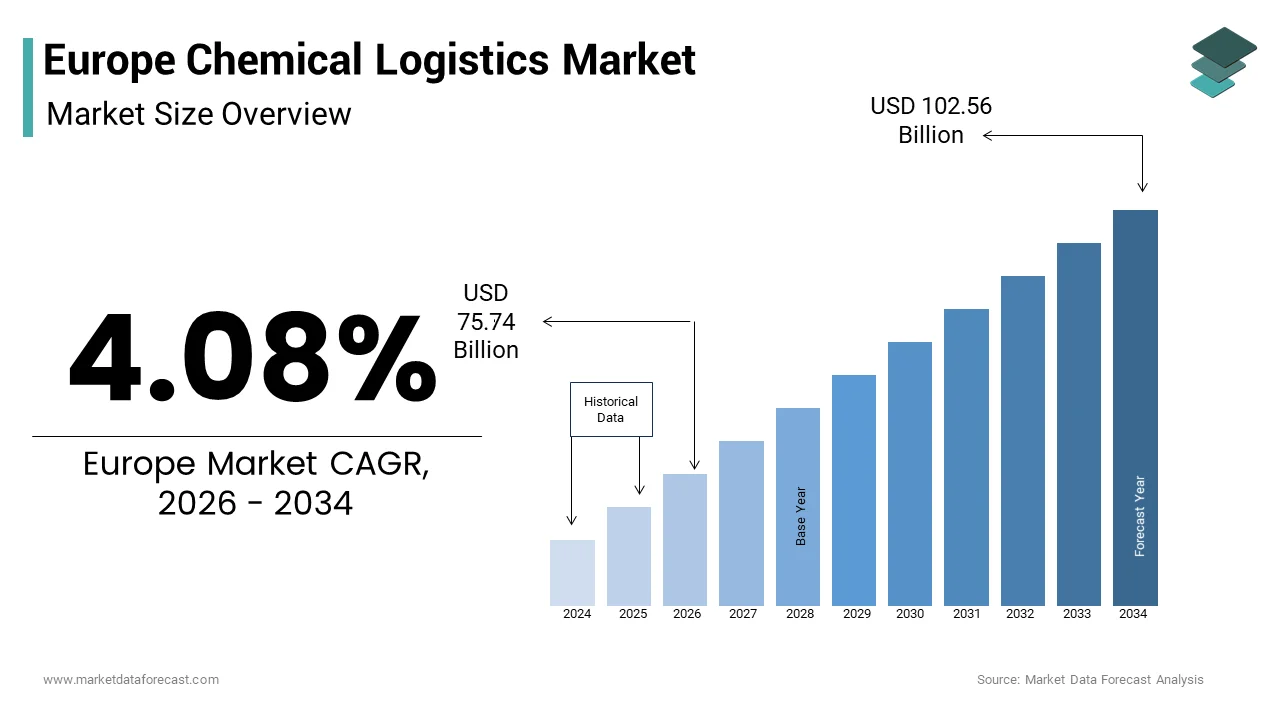

The Europe chemical logistics market size was valued at USD 72.75 billion in 2025 and is anticipated to reach USD 75.74 billion in 2026 to reach USD 102.56 billion by 2034, growing at a CAGR of 4.08% during the forecast period from 2026 to 2034.

Introduction and Market Definition

The chemical logistics is the specialized storage transportation and distribution of chemical substances, across the continent ensuring strict adherence to safety and regulatory standards. As per the European Chemical Industry Council, the chemical industry in Europe generates annual sales exceeding 500 billion EUR and employs approximately 1.2 million people directly. The logistical framework supporting this vast output requires intricate coordination due to the hazardous nature of many products involved. Regulatory compliance is paramount with operators needing to navigate a complex web of environmental and safety laws. According to the European Agency for Safety and Health at Work, incidents involving dangerous goods transport decreased by 12% over the last decade due to improved handling protocols. The infrastructure includes dedicated terminals pipelines rail networks and specialized fleet vehicles designed to handle liquids gases and solids. The geographic density of chemical production clusters in countries such as Germany France and the Netherlands necessitates efficient cross border logistics solutions. The shift toward sustainable practices influences logistical choices with companies increasingly opting for lower carbon emission transport modes. The integration of digital tracking systems enhances visibility and security throughout the supply chain.

MARKET DRIVERS

Stringent Environmental Regulations Drive Adoption of Green Logistics Solutions

The implementation of rigorous environmental policies to adopt sustainable practices and cleaner technologies is driving the growth of Europe chemical logistics market. The European Green Deal aims to make Europe the first climate neutral continent by 2050, which imposes strict emissions targets on all industrial sectors including logistics. As per the European Commission, transport accounts for approximately 25% of total greenhouse gas emissions in the EU prompting aggressive decarbonization strategies. Chemical logistics companies must invest in low emission vehicles and optimize routes to reduce their carbon footprint. The use of liquefied natural gas and electric trucks for short haul distributions is gaining traction among leading service providers. This modal shift is particularly relevant for bulk chemical transport, where timing flexibility allows for slower but greener transport modes. Regulatory pressure also extends to packaging and waste management requiring logistics firms to implement circular economy principles. Companies are developing closed loop systems for intermediate bulk containers to minimize waste and resource consumption. The Carbon Border Adjustment Mechanism further incentivizes low carbon logistics by imposing costs on high emission imports. Logistics providers, who proactively adopt green technologies gain a competitive edge in securing contracts with environmentally conscious chemical manufacturers.

Growth in Specialty Chemicals Production Increases Demand for Precision Handling

The expanding specialty chemicals segment drives the need for highly specialized and precise logistical services, which is additionally boosting the growth of Europe chemical logistics market. Unlike bulk commodities specialty chemicals often require specific temperature controls humidity regulation and contamination prevention measures during transit. These high value products include pharmaceutical intermediates electronic chemicals and advanced polymer additives which demand exceptional care in handling. Logistics providers must maintain certified clean rooms and specialized storage facilities to preserve product integrity. According to the European Pharmaceutical Manufacturers Association, the pharmaceutical industry relies on just in time delivery models, which require zero tolerance for logistical errors or delays. The complexity of handling diverse chemical formulations necessitates advanced tracking and monitoring systems to ensure quality assurance throughout the supply chain. Temperature sensitive products require real time data logging to prove compliance with storage conditions upon delivery. The customization of logistics solutions becomes a key differentiator as standard services fail to meet the nuanced requirements of specialty products. Small batch sizes and frequent deliveries characterize this segment requiring flexible and responsive distribution networks. Logistics partners must possess deep technical knowledge of chemical properties to handle emergencies effectively. The rise of personalized medicine and niche industrial applications further amplifies the need for precision logistics. Providers investing in specialized infrastructure and trained personnel capture higher margins in this growing segment.

MARKET RESTRAINTS

Infrastructure Bottlenecks Impede Efficient Cross Border Transportation

The aging infrastructure and congestion at key transport hubs create significant hurdles, which is significantly degrading the growth of Europe chemical logistics market. Many rail networks and inland waterways suffer from capacity constraints and maintenance backlogs, which delay shipments and increase costs. As per the European Court of Auditors, only 60% of the transport network core corridors are fully compliant with required standards leading to frequent disruptions. Chemical transporters face particular challenges when navigating congested ports and border crossings where security checks and customs procedures add considerable time. The Rhine river a vital artery for chemical transport experienced low water levels in recent years which reduced barge carrying capacity by up to 50% during peak drought periods. Road transport faces similar issues with traffic congestion in major industrial regions such as the Ruhr area in Germany and the Po Valley in Italy. The lack of integrated multimodal terminals forces reliance on road transport for last mile delivery which is less efficient and more expensive. Infrastructure investment has not kept pace with the growth in chemical production and trade volumes. Political fragmentation among member states complicates coordinated infrastructure planning and funding. Logistics providers must build buffer times into their schedules which reduces asset utilization and profitability. The inability to predict transit times accurately undermines the reliability of supply chains.

Labor Shortages and Skill Gaps Constrain Operational Capacity

The shortage of qualified personnel, which limits operational expansion and service quality is another attribute declining the growth of Europe chemical logistics market. The specialized nature of chemical transport requires drivers and handlers with specific certifications and training in hazardous materials handling. As per the International Road Transport Union the European trucking industry faces a deficit of over 400000 drivers with the situation exacerbated by an aging workforce. The retirement of experienced workers creates a knowledge gap that is difficult to fill with new entrants who lack specialized chemical handling expertise. Training programs for dangerous goods advisors and safety officers are lengthy and costly which discourages rapid workforce scaling. The stringent regulatory environment requires continuous professional development, which adds to the burden on employers. Retention rates remain low due to the demanding nature of the work and competition from other sectors offering better working conditions. The lack of standardized certification recognition across borders complicates the deployment of international drivers and staff. This financial pressure squeezes margins for logistics providers who must pass costs onto customers or absorb them. The skill gap also affects warehouse operations where precision in loading and unloading hazardous materials is critical to safety. Automation offers a partial solution but cannot fully replace the judgment and flexibility required in complex logistical scenarios.

MARKET OPPORTUNITIES

Digitalization of Supply Chains Offers Enhanced Visibility and Efficiency

The adoption of digital technologies to enhance transparency and operational efficiency is setting up the growth of Europe chemical logistics market. Internet of Things sensors and blockchain platforms enable real time tracking of shipments and immutable recording of handling conditions. For chemical logistics, this technology ensures compliance with safety regulations by providing auditable data on temperature pressure and location throughout the journey. Smart containers equipped with sensors can alert operators to deviations from specified parameters allowing for immediate corrective action. This predictive capability minimizes the risk of accidents and delays, which is crucial for hazardous materials. The integration of artificial intelligence helps in demand forecasting and resource allocation reducing idle time for specialized assets. Digital platforms facilitate seamless communication between shippers carriers and regulators streamlining documentation and customs clearance processes. The use of electronic waybills and automated reporting reduces administrative burdens and errors. Customers increasingly demand end to end visibility which digital tools provide effectively. Logistics providers, who invest in digital infrastructure differentiate themselves through superior service quality and reliability. The data generated also supports sustainability initiatives by identifying inefficiencies and optimizing fuel consumption. The transition to digital operations requires cultural change and investment but yields substantial long-term benefits. Early adopters gain a competitive advantage in attracting high value clients who prioritize transparency and control.

Expansion of Circular Economy Models Creates New Reverse Logistics Streams

The shift toward a circular economy in the chemical industry generates new opportunities for reverse logistics and waste management services, which is another attribute to enhance the growth of Europe chemical logistics market. Regulations mandating higher recycling rates and extended producer responsibility require efficient systems for collecting and returning chemical waste and packaging. As per the European Commission, the circular economy action plan aims to double the circular material use rate in the EU by 2030 creating demand for specialized reverse logistics. Chemical logistics providers can expand their service portfolios by offering collection transportation and preprocessing of hazardous waste for recycling or disposal. The recovery of solvents catalysts and other valuable chemicals from industrial processes requires careful handling and segregated transport streams. This model requires robust tracking and cleaning infrastructure which logistics firms can provide as a value added service. The integration of reverse flows with forward logistics optimizes asset utilization and reduces empty runs. As per BASF the implementation of chemical leasing models involves the service provider managing the entire lifecycle of the chemical including take back and regeneration. This approach shifts the focus from product sales to service delivery creating long term customer relationships. Logistics providers who specialize in circular supply chains position themselves as strategic partners in sustainability efforts. The complexity of handling mixed waste streams requires advanced sorting and identification technologies.

MARKET CHALLENGES

Geopolitical Instability Disrupts Energy and Raw Material Supply Lines

The geopolitical tensions and conflicts in neighboring regions to the stability of chemical logistics is likely to be a challenge for the growth of Europe chemical logistics market. Dependence on imported raw materials and energy sources makes the supply chain vulnerable to external shocks. As per the International Energy Agency Europe reduced its reliance on Russian pipeline gas by 80% in 2023 but still faces volatility in energy prices and availability. Chemical production is energy intensive and any disruption in supply affects production volumes and subsequently logistics demand. The rerouting of trade flows due to sanctions and conflicts increases transit times and costs for maritime and land transport. The security of transport corridors becomes a concern with increased risks of sabotage or interception in unstable regions. Logistics providers must constantly assess and mitigate these risks which adds complexity to planning and insurance costs. The fragmentation of global trade blocs leads to stricter border controls and customs inspections slowing down cross border movements. As per the European External Action Service, the diversification of supply sources requires establishing new logistical connections which take time to mature. The uncertainty discourages long term investment in infrastructure and fleet expansion. Companies must maintain higher inventory levels as a buffer against supply disruptions which ties up capital. The political landscape influences trade agreements and tariffs affecting the competitiveness of European chemical exports. Navigating this volatile environment requires agility and robust risk management frameworks. The potential for further escalation keeps the sector on high alert affecting operational confidence.

Cybersecurity Threats Endanger Critical Logistics Infrastructure and Data

The increasing digitization of chemical logistics exposes the sector to heightened cybersecurity risks, which threaten operational continuity and data integrity. The cybersecurity threats endanger is also to degrade the growth of Europe chemical logistics market. Logistics networks rely on interconnected systems for tracking scheduling and communication making them attractive targets for cyberattacks. As per the European Union Agency for Cybersecurity, the number of ransomware attacks on transport and logistics companies increased by 40% in 2023. For chemical logistics, the consequences are severe as loss of control over hazardous material movements can lead to safety incidents. The integration of third party vendors and partners expands the attack surface requiring comprehensive security protocols across the ecosystem. Legacy systems used in some warehouses and vehicles often lack adequate protection making them vulnerable to exploitation. As per the European Chemical Industry Council, cyber resilience is now a top priority for supply chain security alongside physical safety measures. The theft of sensitive customer data and proprietary formulation information poses additional reputational and financial risks. Regulatory requirements such as the NIS2 Directive mandate stricter cybersecurity measures for essential entities including logistics providers. Compliance requires significant investment in security infrastructure and staff training. The shortage of cybersecurity experts in the logistics sector complicates defense efforts. Companies must implement zero trust architectures and regular penetration testing to identify vulnerabilities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.08% |

| Segments Covered | By End-User, Mode of Transport, Service, Cargo Form, And Region |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | DHL Supply Chain (Germany), Kuehne+Nagel (Switzerland), BASF SE, DB Schenker (Germany), DSV (Denmark), P. Moller – Maersk (Denmark), GEODIS (France), CEVA Logistics (France), DP World (UAE), Bertschi AG (Switzerland), HOYER Group (Germany), Odyssey Logistics & Technology (U.S.), H. Robinson (U.S.), XPO Logistics (U.S.), Nippon Express (NX Group) (Japan), Bulkhaul Limited (U.K.) |

SEGMENTAL ANALYSIS

By End User Industry Insights

The basic commodity chemicals segment was accounted in holding 32.3% of Europe chemical logistics market share in 2025 due to the massive volume of bulk materials required for industrial manufacturing. The extensive production of foundational chemicals, such as ethylene, propylene, and benzene, which serve as building blocks for countless downstream products. As per the European Chemical Industry Council, basic chemicals account for approximately 60% of total chemical production volume in Europe necessitating robust and high capacity logistics networks. The first major driver is the integrated nature of chemical production clusters known as Verbund sites which rely on continuous flow logistics. These sites primarily located in Germany and the Netherlands require constant input of raw materials and output of intermediates via pipeline and rail. This scale creates a structural demand for heavy duty logistics infrastructure that smaller segments cannot match. The second driver is the cost sensitivity of commodity chemicals which forces manufacturers to prioritize the most economical transport modes. Rail and inland waterways offer significantly lower costs per tonne kilometer compared to road transport. The reliance on these high volume low margin flows ensures that basic commodities remain the backbone of the chemical logistics sector. The stability of demand from construction automotive and packaging industries further cements this segment's leading position.

The specialty chemicals segment is likely to register a fastest CAGR of 5.8% from 2026 to 2034 with the increasing complexity and value of chemical formulations. The rising demand for high performance materials in electronics pharmaceuticals and advanced automotive applications. The need for precision handling and temperature controlled logistics to maintain product integrity. Specialty chemicals often have strict shelf lives and sensitivity to environmental conditions requiring specialized infrastructure. Logistics providers are investing heavily in smart containers and real time monitoring systems to meet these stringent requirements. The second driver is the fragmentation of supply chains as manufacturers shift toward customized small batch production. This trend increases the frequency of shipments and the need for flexible distribution networks. The higher value density of these products allows logistics providers to charge premium rates for specialized services. The expansion of the electric vehicle sector also boosts demand for battery electrolytes and advanced polymers which fall under the specialty category. As per the International Energy Agency electric vehicle sales in Europe reached 3.2 million units in 2023 creating new logistical pathways for battery materials.

By Mode of Transport Insights

The road transport segment was the largest by holding 32.4% of the Europe chemical logistics market in 2025 due to its unparalleled flexibility and ability to provide door to door service. This mode accounts for the largest share of chemical freight movements particularly for short to medium distances and last mile delivery. The extensive network of highways and roads connecting industrial clusters with consumption centers, across Europe. Road transport offers the agility required for just in time delivery models, which are prevalent in the automotive and consumer goods sectors. The ability to handle diverse cargo types from bulk tankers to packaged drums makes road transport versatile for various chemical products. The lack of direct rail or waterway connections to many final destinations, which necessitates road transport for the final leg of the journey. Even when bulk chemicals are moved by rail or ship they often require transshipment to trucks for distribution to end users. The development of specialized tanker trucks with advanced safety features has also enhanced the reliability of road transport for hazardous materials. Regulatory harmonization through the ADR agreement facilitates seamless cross border movement of dangerous goods by road.

The rail transport segment is esteemed to witness a fastest CAGR of 4.5% from 2026 to 2034 with the sustainability mandates and infrastructure improvements. The shift toward greener logistics solutions is prompting companies to move bulk chemical shipments from road to rail to reduce carbon emissions. The superior environmental performance of rail transport, which produces significantly lower greenhouse gas emissions per tonne kilometer. As per the European Environment Agency rail freight emits approximately 80% less carbon dioxide than road freight making it an attractive option for companies aiming to meet sustainability targets. The European Green Deal and subsequent regulations are incentivizing this modal shift through carbon pricing and subsidies for green transport. The second driver is the investment in modernizing rail infrastructure and increasing capacity on key corridors. The Trans European Transport Network policy prioritizes the development of rail freight corridors to enhance efficiency and reliability. The ability of rail to handle large volumes of bulk liquids and gases efficiently makes it ideal for long distance transport between major chemical hubs. The integration of digital signaling systems and automated terminals is improving transit times and reducing bottlenecks. As per the European Commission the goal is to double rail freight traffic by 2050 which will further accelerate growth in this segment. The combination of regulatory support and operational improvements positions rail as the fastest growing mode for chemical logistics.

By Service Insights

The transportation and distribution segment was the largest by occupying 45.3% of the Europe chemical logistics market share in 2025 due to the continuous and high volume nature of chemical shipments. The geographic dispersion of chemical production facilities and consumption, which necessitates extensive distribution networks. Chemical manufacturers rely on third party logistics providers to manage complex transportation routes across multiple countries. As per the European Chemical Industry Council, the chemical industry relies on logistics partners for over 80% of its transportation needs the dependency on external service providers. The complexity of handling hazardous materials requires specialized fleets and trained personnel which transportation specialists provide. The globalization of supply , which increases the distance and complexity of chemical shipments. Even within Europe cross border trade requires sophisticated logistics coordination to comply with varying national regulations. According to study, the demand for integrated transportation services in the chemical sector grew by 6% in 2023 driven by the need for end to end visibility. The ability to offer multimodal solutions combining road rail and sea transport enhances the value proposition of transportation providers.

The green logistics services segment is likely to register a fastest CAGR of 7.2% from 20926 to 2034, driven by stringent environmental regulations and corporate sustainability goals. Companies are increasingly seeking logistics partners who can offer low carbon solutions and help them meet their environmental social and governance targets. The implementation of carbon reporting requirements, which force companies to track and reduce the emissions associated with their supply chains. As per the European Commission, the Corporate Sustainability Reporting Directive requires large companies to disclose their environmental impact including logistics emissions. This regulatory pressure creates demand for green logistics services such as carbon neutral shipping and eco-friendly packaging. The second driver is the willingness of customers to pay a premium for sustainable logistics solutions. Many chemical manufacturers are integrating sustainability into their procurement criteria preferring partners with certified green practices. Logistics providers are responding by offering services such as biofuel powered transport and optimized route planning to minimize fuel consumption. The development of circular economy models also contributes to growth as providers offer waste management and recycling logistics.

By Cargo Form Insights

The bulk form segment was accounted in holding a significant share of the Europe chemical logistics market in 2025 due to the large volumes of liquid and gaseous chemicals transported for industrial use. Bulk chemicals, such as acids alkalis and solvents are typically moved in tank containers tank trucks or via pipelines. The economies of scale associated with bulk transport, which significantly reduces the cost per unit of chemical shipped. Large chemical producers prefer bulk handling to minimize packaging costs and handling time. The extensive network of pipelines and dedicated tank terminals supports this high volume flow. The continuous nature of chemical production processes, which require steady input of raw materials and output of products is propelling the growth of segment. Bulk transport allows for seamless integration with production facilities through direct loading and unloading systems. The standardization of tank containers and ISO tanks enables intermodal transport combining rail sea and road modes. The reliability and efficiency of bulk transport make it the preferred choice for commodity chemicals.

The temperature controlled form segment is expected to grow at a fastest CAGR of 6.5% during the forecast period with the increasing demand for sensitive chemical products. The expansion of the biopharmaceutical industry, which relies heavily on temperature controlled logistics for vaccines and therapies. The complexity of maintaining precise temperature conditions throughout the supply chain requires specialized equipment and monitoring systems. The increasing regulation regarding product quality and safety, which mandates strict temperature control for certain chemicals is also elevating the growth of segment. Deviations from specified temperature ranges can render products unusable leading to significant financial losses. According to the World Health Organization, up to 50% of vaccines are wasted globally due to logistics failures highlighting the critical need for reliable temperature controlled transport. Logistics providers are investing in active cooling systems and real time temperature monitoring to ensure compliance. The rise of personalized medicine and clinical trials also contributes to growth as these applications require small batch temperature controlled shipments.

COUNTRY LEVEL ANALYSIS

Germany Chemical Logistics Market Analysis

Germany was the top performer in the Europe chemical logistics market by capturing 32.4% of the Europe chemical logistics market share in 2025 with the robust industrial base and central geographic location. As per the German Chemical Industry Association, VCI the chemical industry in Germany generated sales of 230 billion EUR in 2023 supporting a vast logistics network. The presence of major chemical manufacturers, such as BASF, Bayer, and Evonik, which require extensive domestic and international logistics services is also promoting the growth of the market in this country. These companies operate large Verbund sites that rely on integrated transport systems including pipelines rail and inland waterways. The strong emphasis on innovation and sustainability also drives the adoption of advanced logistics solutions.

France Chemical Logistics Market Analysis

France chemical logistics market was positioned second by holding 24.6% of share in 2025 with a major producer of specialty chemicals and cosmetics, which require sophisticated logistics services. The strong presence of global players, such as TotalEnergies and Arkema, which operate large production facilities and require efficient supply chain management. These companies export a significant portion of their production necessitating reliable maritime and land transport links. The strategic location of French ports, such as Le Havre and Marseille, which serve as gateways for chemical trade with Africa and Asia. These ports handle millions of tonnes of chemical cargo annually supporting international logistics operations. The government’s support for industrial reindustrialization is also boosting domestic chemical production and logistics activity.

Italy Chemical Logistics Market Analysis

Italy chemical logistics market growth is likely to have a significant growth opportunities in coming years with its specialized chemical industry and strategic Mediterranean location. The country is a leading producer of pharmaceuticals and fine chemicals which require precise and reliable logistics services. The concentration of pharmaceutical manufacturing in regions, such as Lombardy and Lazio, which generates high demand for temperature controlled and secure logistics. Italy is one of the largest pharmaceutical producers in Europe requiring sophisticated cold chain infrastructure. The importance of port infrastructure in cities like Genoa and Trieste, which facilitate chemical imports and exports. These ports serve as key entry points for raw materials and exit points for finished products. The growing focus on sustainable chemistry and circular economy initiatives is also influencing logistics practices. Italy’s strong export orientation drives the need for reliable cross border transport solutions. The integration of digital technologies in logistics is enhancing efficiency and transparency.

Spain Chemical Logistics Market Analysis

Spain chemical logistics market growth is expected to grow with the growing chemical industry and strategic access to Atlantic and Mediterranean trade routes. The country is a significant producer of basic chemicals and refining products, which drive bulk logistics demand. The presence of large refining and petrochemical complexes in Tarragona and Huelva, which require massive inbound and outbound logistics capabilities. These clusters produce large volumes of bulk chemicals that are transported via pipeline ship and rail. The strategic location of Spanish ports, such as Algeciras and Valencia, which serve as hubs for trade with Latin America and North Africa. These ports facilitate the import of raw materials and export of chemical products to emerging markets. As per Puertos del Estado the volume of liquid bulk handled in Spanish ports reached 30 million tonnes in 2023. The increasing investment in renewable energy and green hydrogen is also creating new logistics opportunities.

Netherlands Chemical Logistics Market Analysis

The Netherlands chemical market growth is driven by the world class port infrastructure and central location. The Port of Rotterdam is the largest chemical cluster in Europe and a primary entry point for chemical raw materials. As per the Port of Rotterdam Authority, the port handled over 40 million tonnes of chemical products in 2023 underscoring its pivotal role. The extensive network of chemical storage terminals and processing facilities in the Rotterdam area, which attract global chemical companies. This concentration creates a dense demand for logistics services including tank storage pipeline transport and barge operations. The excellent connectivity via inland waterways and rail networks, which link Rotterdam to industrial centers in Germany, France, and others. The Rhine Meuse and Scheldt rivers provide efficient transport routes for bulk chemicals.

United Kingdom Chemical Logistics Market Analysis

The United Kingdom chemical logistics market growth is driven by the strong focus on specialty chemicals and pharmaceuticals. The country has a well-developed chemical industry concentrated in regions, such as the North West and Scotland. The robust pharmaceutical sector, which requires high precision logistics for active pharmaceutical ingredients and finished medicines. The UK is a global leader in pharmaceutical research and production driving demand for cold chain and secure transport services. The presence of major chemical ports, such as Immingham and Grangemouth which handle significant volumes of bulk chemicals. These ports serve as key nodes for importing raw materials and exporting finished products. The focus on innovation and sustainability is driving investment in green logistics.

COMPETITIVE LANDSCAPE

The Europe chemical logistics market features intense competition characterized by the presence of global integrators and specialized regional providers. Major multinational corporations compete on the basis of network reach technological innovation and sustainability credentials. These large players leverage economies of scale to offer comprehensive end to end solutions that appeal to large chemical manufacturers. Regional specialists counter this by providing deep local expertise and flexible services tailored to specific customer needs. The barrier to entry remains high due to strict regulatory requirements and the need for specialized infrastructure such as tank terminals and certified fleets. Consequently, competition focuses heavily on service quality safety records and reliability rather than price alone. Companies differentiate themselves through advanced digital platforms that provide real time tracking and predictive analytics. The push for green logistics has become a key competitive dimension with firms investing in low carbon technologies to meet environmental mandates. Mergers and acquisitions are frequent as companies seek to consolidate market position and expand service portfolios. The dynamic regulatory landscape further intensifies competition as providers must continuously adapt to new safety and environmental standards. Customer loyalty is driven by trust and consistent performance making operational excellence critical for maintaining competitive advantage in this complex and highly regulated sector.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe chemical logistics market are

- DHL Supply Chain (Germany)

- Kuehne+Nagel (Switzerland)

- BASF SE

- DB Schenker (Germany)

- DSV (Denmark)

- P. Moller – Maersk (Denmark)

- GEODIS (France)

- CEVA Logistics (France)

- DP World (UAE)

- Bertschi AG (Switzerland)

- HOYER Group (Germany)

- Odyssey Logistics & Technology (U.S.)

- H. Robinson (U.S.)

- XPO Logistics (U.S.)

- Nippon Express (NX Group) (Japan)

- Bulkhaul Limited (U.K.)

Top Players In The Market

- BASF SE stands as a global chemical giant with extensive logistics operations integrated into its Verbund production sites. The company leverages its massive infrastructure to optimize supply chain efficiency and reduce transportation costs significantly. Recently, BASF has invested heavily in digitalizing its logistics network to enhance real time tracking and predictive maintenance capabilities. These initiatives strengthen its position by ensuring reliable delivery of hazardous materials across Europe and globally. The company also focuses on sustainable logistics solutions including the use of biofuels and electric vehicles for last mile delivery. This strategic approach reinforces its leadership in providing safe and efficient chemical logistics services while meeting stringent environmental regulations and customer expectations for sustainability.

- DHL Supply Chain is a leading logistics provider specializing in complex chemical transportation and warehousing solutions worldwide. The company offers comprehensive services including hazardous material handling temperature controlled storage and multimodal transport options. DHL recently expanded its specialized chemical logistics facilities in key European hubs to accommodate growing demand for specialty chemicals. It has implemented advanced Internet of Things sensors to monitor shipment conditions ensuring product integrity and regulatory compliance. The company also launched green logistics initiatives aiming to achieve net zero emissions by optimizing routes and using alternative fuels. These actions enhance its competitive edge by offering customers reliable and sustainable supply chain solutions. DHL’s focus on innovation and safety standards solidifies its reputation as a trusted partner for chemical manufacturers seeking efficient and compliant logistics services globally.

- Kuehne+Nagel operates as a premier global logistics provider with a strong foothold in the chemical sector through its specialized Kn Chemicals division. The company provides tailored solutions for hazardous goods including sea air road and rail freight services. Recently Kuehne+Nagel enhanced its digital platform KN Sea Explorer to improve visibility and efficiency in chemical shipments. It also expanded its tank container fleet and storage capabilities in strategic locations to support bulk chemical transport. The firm prioritizes sustainability by offering carbon neutral shipping options and investing in cleaner transport technologies. These efforts strengthen its market position by addressing the increasing demand for transparent and eco friendly logistics services. Kuehne+Nagel’s commitment to safety innovation and customer centric solutions ensures it remains a key player in the global chemical logistics landscape serving diverse industrial needs effectively.

Top Strategies Used by Key Market Participants

Key players in the Europe chemical logistics market primarily employ strategic acquisitions to expand their geographic footprint and service capabilities. Companies actively purchase specialized firms to gain access to niche markets such as temperature controlled storage or hazardous waste management. Another major strategy involves heavy investment in digitalization and automation technologies. Logistics providers implement Internet of Things sensors artificial intelligence and blockchain to enhance supply chain visibility and operational efficiency. Sustainability initiatives form a core strategic pillar with firms transitioning to low emission vehicles and optimizing routes to reduce carbon footprints. Partnerships with chemical manufacturers are also common enabling co development of customized logistics solutions. These collaborations help providers align closely with client needs and secure long term contracts. Additionally,companies focus on expanding multimodal transport networks to offer flexible and cost effective solutions.

MARKET SEGMENTATION

This research report on the Europe chemical logistics market is segmented and sub-segmented into the following categories.

By End-User Industry

- Basic/Commodity Chemicals

- Specialty Chemicals

- Oil & Gas/Petrochemicals

By Mode of Transport

- Road

- Rail

- Sea/Waterways

- Air

By Service Type

- Transportation & Distribution

- Storage & Warehousing

- Green Logistics Services

- Consulting & Management Services

By Cargo Form

- Bulk Form

- Packaged Form

- Temperature-Controlled Form

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe chemical logistics market?

Increasing demand for safe transportation and storage of chemicals is driving market growth.

Why is chemical logistics important in Europe’s industrial sector?

It ensures safe handling and timely delivery of hazardous and non-hazardous chemicals.

How would you explain chemical logistics in simple terms?

It involves the transportation, storage, and management of chemical products.

Where are chemical logistics services most commonly used across Europe?

They are widely used in manufacturing, pharmaceuticals, and petrochemical industries.

What makes chemical logistics essential for supply chains?

It ensures safety, compliance, and efficiency in moving chemical goods.

From an operational perspective, are specialized logistics services necessary for chemicals?

Yes, they are critical for handling hazardous materials safely and efficiently.

What challenges are affecting the Europe chemical logistics market?

Strict regulations and high operational costs are key challenges.

How are safety regulations influencing this market?

Stringent compliance requirements are shaping logistics operations and standards.

Which segments contribute the most to chemical logistics demand?

Bulk chemicals and specialty chemicals are major contributors.

Is the Europe chemical logistics market growing steadily?

Yes, it is expanding with increasing industrial and chemical production activities.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com