Europe Co Packaged Optics Market Size, Share, Trends & Growth Forecast Report, Segmented By Data Rate, Component, End-Use Application, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Co Packaged Optics Market Size

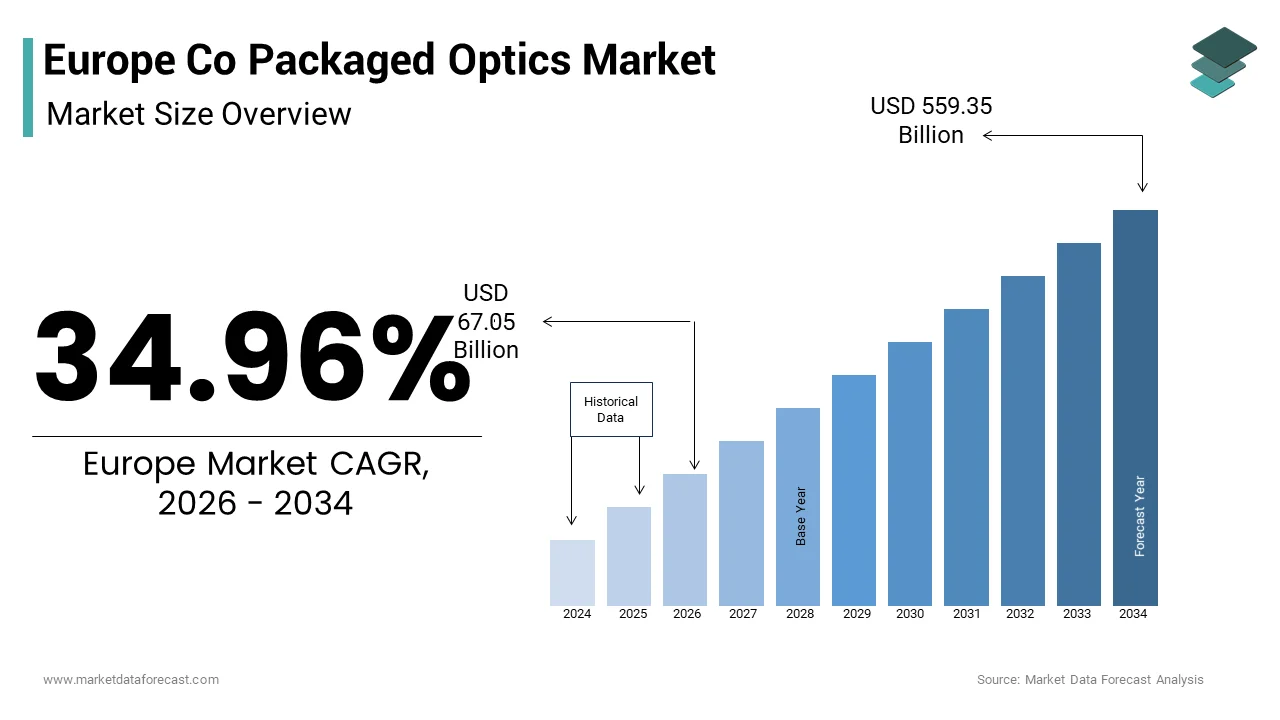

The Europe co packaged optics market size was valued at USD 49.67 billion in 2025 and is anticipated to reach USD 67.05 billion in 2026 to reach USD 559.35 billion in 2034, growing at a CAGR of 34.96% during the forecast period from 2026 to 2034.

Introduction to the Europe Co Packaged Optics Market

Co-packaged optics represents a pivotal technological shift in high-performance computing and data center infrastructure, where optical engines are integrated directly onto the same substrate as the application-specific integrated circuit. This advanced packaging technique significantly reduces power consumption and signal latency compared to traditional pluggable optical modules. The region is witnessing accelerated adoption driven by the exponential growth of artificial intelligence workloads and cloud computing services. According to Eurostat, 74% of enterprises in the European Union with ten or more persons employed used cloud computing services in 2023, indicating a robust digital infrastructure base that demands higher bandwidth efficiency. Furthermore, the European Commission has outlined ambitious targets for climate neutrality, which pressures data centers to reduce their energy footprint. Co-packaged optics offers a viable solution by lowering the energy required per bit of data transmitted. According to the International Energy Agency, data centers and data transmission networks accounted for approximately 1% of global electricity-related greenhouse gas emissions in recent years, highlighting the urgent need for energy-efficient technologies. The integration of photonics with electronics at the package level enables higher density interconnects, which are essential for next-generation switches and routers. This market definition encompasses the design, manufacturing, and testing of these hybrid modules along with the associated supply chain components. The strategic importance of semiconductor sovereignty in Europe further supports investments in advanced packaging facilities. Companies are increasingly focusing on localizing production to mitigate supply chain risks. The convergence of telecommunications advancements and computational demands defines the current trajectory of this specialized sector.

MARKET DRIVERS

Surging Demand for High Bandwidth in Artificial Intelligence and Cloud Computing

The exponential increase in data traffic generated by artificial intelligence applications and cloud computing services is driving the expansion of the Europe co-packaged optics market. Modern AI models require massive parallel processing capabilities, which necessitate high-speed interconnects between processors and memory units. Traditional copper interconnects struggle to meet these bandwidth requirements due to signal integrity issues and high power consumption at longer distances. According to the European Data Centre Association, the demand for data center capacity in Europe is projected to grow significantly as businesses migrate critical workloads to the cloud. Co-packaged optics addresses this challenge by placing the optical engine in close proximity to the switch ASIC, thereby reducing the electrical trace length and improving signal quality. As per Statista, the number of internet users in Europe continues to rise, with over 90% of the population having access to the internet, creating a vast ecosystem of data generation. This trend drives the need for scalable and efficient networking solutions. Hyperscale data centers operated by major technology firms are increasingly adopting co-packaged optics to support 800 gigabit and 1.6 terabit Ethernet standards. The ability to handle larger data volumes with lower latency is crucial for real-time analytics and machine learning tasks. Furthermore, the proliferation of Internet of Things devices adds to the data burden, requiring robust backend infrastructure. European telecommunications providers are upgrading their networks to support fifth-generation services, which also benefit from high-bandwidth optical interconnects. The competitive landscape among cloud service providers encourages continuous investment in superior infrastructure. This relentless pursuit of performance and efficiency sustains the momentum for co-packaged optics adoption across the continent.

Stringent Energy Efficiency Regulations and Sustainability Goals

Regulatory pressure to enhance energy efficiency and achieve sustainability goals is further fuelling the growth of the Europe co-packaged optics market. The European Green Deal sets ambitious targets for reducing greenhouse gas emissions and improving energy efficiency across all sectors, including information and communication technologies. Data centers are major consumers of electricity, and their environmental impact is under intense scrutiny. According to the European Commission, the Code of Conduct on Data Centre Energy Efficiency provides guidelines for best practices in reducing energy consumption. Co-packaged optics technology offers substantial power savings by eliminating the need for long-reach electrical signals and reducing the number of active components in the data path. As per the International Energy Agency, improving the energy efficiency of data centers is a key priority for meeting climate objectives. Traditional pluggable optics consume more power due to the additional digital signal processing required for signal regeneration. By integrating optics directly with the chip, co-packaged solutions minimize these losses. The European Union’s Ecodesign for Sustainable Products Regulation also emphasizes the lifecycle environmental impact of electronic products. This regulatory framework encourages manufacturers to develop technologies that offer lower operational carbon footprints. Corporate social responsibility initiatives further drive companies to adopt green technologies to enhance their brand reputation. Investors are increasingly prioritizing environmental, social, and governance criteria when allocating capital. The financial benefits of reduced energy bills complement the regulatory incentives, making co-packaged optics an attractive investment. The alignment of technological innovation with sustainability mandates ensures long-term market growth. This driver is particularly strong in Northern European countries, where renewable energy integration is advanced.

MARKET RESTRAINTS

Complexity in Manufacturing and Yield Challenges

The intricate manufacturing processes associated with co-packaged optics are impeding the expansion of the Europe co-packaged optics market. Integrating optical components with electronic chips on a single substrate requires precise alignment and advanced packaging techniques that are not yet fully matured for mass production. According to the European Semiconductor Industry Association, the yield rates for complex heterogeneous integration processes remain lower than those for standard semiconductor manufacturing. This results in higher production costs and limited availability of reliable components. The thermal management of co-packaged modules is another critical challenge, as the close proximity of heat-generating electronics and sensitive optical elements can lead to performance degradation. As per imec, a leading research and innovation hub in nanoelectronics and digital technologies and achieving reliable thermal dissipation without compromising optical performance requires sophisticated engineering solutions. The lack of standardized testing protocols further complicates the qualification process for these new devices. Manufacturers must invest heavily in specialized equipment and skilled personnel to overcome these technical hurdles. The supply chain for specialized materials, such as silicon photonics wafers and advanced substrates, is also less developed compared to traditional semiconductor components. This dependency on niche suppliers can lead to bottlenecks and delays. Small and medium-sized enterprises in Europe may lack the resources to navigate these complexities, limiting their participation in the market. The high initial capital expenditure for setting up production lines acts as a barrier to entry. Until manufacturing processes become more streamlined and cost-effective, widespread adoption may be slower than anticipated. These technical constraints require continued research and development efforts to resolve.

High Initial Costs and Limited Economies of Scale

The high initial costs associated with the development and deployment of co-packaged optics solutions is further inhibiting the regional market expansion. Unlike mature pluggable optical modules, which benefit from established supply chains and economies of scale, co-packaged optics are still in the early stages of commercialization. According to the European Investment Bank, the cost of developing new semiconductor technologies is substantial and often prohibitive for smaller players. The custom nature of co-packaged designs means that each implementation may require unique engineering efforts, increasing the overall expense. As per Yole Développement, the total cost of ownership for co-packaged optics is currently higher than traditional solutions due to low production volumes and high research and development amortization. Data center operators are hesitant to replace existing infrastructure without clear evidence of long-term cost benefits. The transition requires significant changes in network architecture and maintenance procedures, which add to the operational burden. Furthermore, the lack of interoperability standards among different vendors creates vendor lock-in risks. Customers are reluctant to commit to a single supplier without guaranteed compatibility with future upgrades. The economic uncertainty in the region also makes companies cautious about large capital expenditures. Budget constraints may force organizations to delay upgrades or opt for cheaper alternatives. The slow ramp-up of production volumes prevents the cost reductions necessary for mainstream adoption. Until the technology reaches a critical mass of deployment, the price premium will remain a significant barrier. This financial hurdle limits the speed at which the market can expand.

MARKET OPPORTUNITIES

Expansion of Fifth Generation Networks and Edge Computing Infrastructure

The rollout of fifth-generation mobile networks and the growth of edge computing present significant opportunities for the Europe co-packaged optics market. Fifth-generation technology requires ultra-low latency and high-bandwidth connections, which co-packaged optics can efficiently provide. According to the GSM Association, the adoption of fifth-generation services in Europe is accelerating, with millions of connections expected in the coming years. This expansion necessitates upgrades to the backhaul and fronthaul networks, where co-packaged optics can enhance performance. Edge computing brings data processing closer to the source, reducing latency for applications such as autonomous vehicles and industrial automation. As per the European Telecommunications Standards Institute, edge nodes require compact and energy-efficient interconnects to handle localized data traffic. Co-packaged optics offers a small form factor solution ideal for space-constrained edge environments. The decentralization of computing resources creates a distributed network architecture that benefits from high-density optical interconnects. Telecommunications operators are investing heavily in network virtualization and software-defined networking, which rely on robust physical layer infrastructure. The integration of co-packaged optics into switching equipment enables more flexible and scalable network designs. Government initiatives supporting digital infrastructure development further stimulate demand. The Smart Cities and Communities initiative in Europe promotes the use of advanced technologies for urban management. This creates a fertile ground for innovative optical solutions. Partnerships between telecom providers and technology vendors can accelerate the deployment of these technologies. The synergy between fifth-generation networks and edge computing drives the need for next-generation optical interfaces. This opportunity extends beyond traditional data centers into diverse industry verticals.

Advancements in Silicon Photonics and Integrated Circuit Design

Recent advancements in silicon photonics and integrated circuit design offer substantial opportunities for the Europe co-packaged optics market. Silicon photonics allows for the integration of optical components using standard complementary metal-oxide-semiconductor fabrication processes, reducing costs and improving scalability. According to imec, Europe is home to world-class research facilities that are pioneering new techniques in silicon photonics integration. These advancements enable the creation of more compact and efficient optical engines that can be seamlessly integrated with electronic chips. As per the European Chips Act, significant investments are being made to strengthen the semiconductor ecosystem in Europe, including photonics technologies. This funding supports the development of pilot lines and demonstration projects that accelerate technology transfer from lab to fab. The improvement in coupling efficiency between fibers and silicon waveguides enhances the performance of co-packaged modules. New materials, such as indium phosphide and lithium niobate, are being explored to expand the functionality of silicon photonics platforms. The development of multi-wavelength lasers and modulators on a single chip increases the bandwidth capacity of optical interconnects. Design automation tools are becoming more sophisticated, allowing engineers to optimize co-packaged designs more effectively. The collaboration between academia and industry fosters a vibrant innovation ecosystem. Startups specializing in photonic integrated circuits are emerging, attracting venture capital interest. These technological breakthroughs lower the barriers to entry and create new application possibilities. The continuous improvement in performance metrics makes co-packaged optics increasingly competitive. This trend positions Europe as a leader in next-generation optical technologies.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Material Shortages

Supply chain vulnerabilities and material shortages pose a major challenge for the Europe co-packaged optics market. The production of co-packaged optics relies on a complex global supply chain for specialized materials, such as high-purity silicon, rare earth elements, and advanced substrates. According to the European Semiconductor Industry Association, disruptions in the supply of critical raw materials can significantly impact production schedules and costs. The geopolitical tensions and trade restrictions affecting semiconductor components exacerbate these risks. As per the European Commission, the dependence on non-European suppliers for key inputs creates strategic vulnerabilities. The shortage of advanced packaging equipment and skilled labor further constrains production capacity. Manufacturers face difficulties in securing consistent supplies of high-quality components necessary for reliable device performance. The long lead times for custom optical components can delay product launches and affect customer satisfaction. The lack of local sourcing options for certain materials forces companies to rely on distant suppliers, which is increasing logistics costs and carbon footprint. The fragility of the supply chain was evident during recent global crises, which highlighted the need for greater resilience. Diversifying suppliers and investing in local production capabilities are essential but require significant time and capital. The interdependence of various industry sectors means that disruptions in one area can ripple through the entire value chain. Managing these risks requires robust supply chain management strategies and contingency planning. The uncertainty surrounding future supply conditions makes long-term planning difficult. This challenge necessitates collaborative efforts among industry stakeholders to build a more resilient ecosystem.

Standardization and Interoperability Issues

The lack of unified standards and interoperability issues are further challenging the growth of the Europe co-packaged optics market. As a relatively new technology, co-packaged optics lacks the mature standardization framework that exists for pluggable optical modules. According to the Optical Internetworking Forum, efforts are underway to define common specifications, but consensus among stakeholders is still evolving. As per the Institute of Electrical and Electronics Engineers, the absence of standardized interfaces leads to proprietary solutions that limit customer choice and increase integration complexity. Different vendors employ varying approaches to thermal management, electrical interfaces, and optical coupling, which hinders seamless interoperability. This fragmentation creates vendor lock-in situations, where customers are tied to specific suppliers for replacements and upgrades. The lack of standardization also complicates the testing and validation process, increasing time to market. Network operators prefer open and interoperable solutions to ensure flexibility and avoid dependency on single sources. The rapid pace of technological advancement outpaces the development of standards, creating a gap between innovation and regulation. Collaborative industry bodies are working to address these issues, but progress can be slow due to competing interests. The uncertainty regarding future standards makes investors and customers cautious. Establishing clear and widely accepted standards is crucial for building confidence in the technology. Without interoperability, the market may remain fragmented, limiting its growth potential. This challenge requires sustained cooperation among manufacturers, service providers, and regulatory bodies. Achieving consensus on key technical parameters is essential for market maturity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 34.96% |

| Segments Covered | By Data Rate, Component, End-Use Application, And Region |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Broadcom Inc., Cisco Systems Inc., Intel Corporation, Ranovus Inc., TE Connectivity Ltd., Furukawa Electric Co., Ltd., Hisense Broadband Multimedia Technology Co., Ltd., POET Technologies Inc., Kyocera Corporation, Huawei Technologies Co., Ltd., SENKO Advanced Components, Inc., Sumitomo Electric Industries, Ltd., Coherent Corp., Taiwan Semiconductor Manufacturing Company Limited, Lumentum Holdings Inc., NVIDIA Corporation, Marvell Technology, Inc., Ciena Corporation, Nokia Corporation, InnoLight Technology (Suzhou) Ltd., Acacia Communications Inc., Hon Hai Precision Industry Co., Ltd., Jabil Inc. |

SEGMENTAL ANALYSIS

By Data Rate Insights

The below 1.6 T data rate segment dominated the market and accounted for 54.5% of the regional market share in 2025. The dominance of this segment in the European market is majorly driven by the widespread deployment of 400-gigabit and 800-gigabit Ethernet switches in existing data center infrastructures, which are currently transitioning to co-packaged optics architectures. According to the European Data Centre Association, the majority of hyperscale facilities in Europe are upgrading their spine-and-leaf networks to support these speeds to handle increasing cloud traffic. The maturity of silicon photonics technology at these data rates ensures higher manufacturing yields and lower costs compared to higher-speed alternatives. As per Yole Développement, the supply chain for components supporting up to 1.6-terabit aggregation is well established, with multiple vendors offering qualified solutions. Telecommunications operators are also adopting these speeds for fifth-generation backhaul applications, where reliability and cost efficiency are paramount. The incremental nature of network upgrades means that many organizations are replacing pluggable modules with co-packaged equivalents at these proven data rates before moving to next-generation standards. The energy-efficiency gains at this level are significant enough to meet immediate sustainability goals without requiring a complete overhaul of network architecture. Furthermore, the availability of design tools and testing equipment for below 1.6 T systems reduces the barrier to entry for manufacturers. This segment benefits from the economies of scale achieved through high-volume production. The steady demand from enterprise data centers undergoing digital transformation further sustains the leadership of this segment. It serves as the foundational layer for the broader adoption of co-packaged optics technology across the region.

However, the 3.2 T data rate segment is anticipated to showcase the fastest CAGR of 26.8% over the forecast period owing to the imminent deployment of next-generation artificial intelligence clusters and high-performance computing systems that require unprecedented bandwidth density. According to the International Supercomputing Conference, Europe is home to several exascale computing initiatives that demand interconnects capable of supporting 3.2-terabit speeds to minimize latency. The transition from 800-gigabit to 1.6-terabit-per-lane technology enables the aggregation of 3.2-terabit capacities within a single co-packaged module. As per the Optical Internetworking Forum, standardization efforts for 3.2 T interfaces are nearing completion, which encourages early adopters to begin pilot deployments. Hyperscale cloud providers are designing new data center architectures specifically for large language model training, which relies heavily on these high-speed connections. The power savings associated with co-packaged optics at 3.2 T are substantial compared to pluggable alternatives, making it an attractive option for energy-constrained facilities. The European Commission’s focus on semiconductor sovereignty includes support for advanced packaging technologies that facilitate these higher data rates. Research institutions and universities are also investing in testbeds for 3.2 T networks to explore new networking protocols. The scarcity of competing technologies at this speed gives co-packaged optics a distinct advantage. Early movers in this segment gain a competitive edge in offering superior performance for AI workloads. The anticipation of widespread commercial availability drives significant pre-orders and strategic partnerships.

By Component Insights

The optical engine segment captured 41.7% of the regional market share in 2025. The dominance of optical engine segment in the European market is majorly attributed to the critical role optical engines play in converting electrical signals to optical signals and vice versa within the co-packaged architecture. The optical engine integrates modulators, photodetectors, and multiplexers that are essential for high-speed data transmission. According to imec, the complexity of integrating these photonic components with electronic chips requires specialized design and fabrication capabilities, which adds significant value to this component. The demand for high-yield and reliable optical engines drive investment in advanced silicon photonics foundries across Europe. As per the European Semiconductor Industry Association, the production of optical engines involves sophisticated packaging techniques, such as flip-chip bonding and fiber attachment, which are key differentiators for suppliers. The performance of the entire co-packaged module depends heavily on the efficiency and linearity of the optical engine. Manufacturers are focusing on improving the coupling efficiency between fibers and waveguides to reduce insertion loss. The integration of multiple wavelengths into a single engine enhances bandwidth density, making it indispensable for high-capacity switches. The supply chain for optical engines is becoming more localized in Europe to reduce dependency on external sources. Collaborations between research institutes and commercial entities accelerate the development of next-generation engines. The continuous improvement in modulation formats, such as pulse-amplitude modulation 4, increases the data throughput of these engines. This segment remains central to the value proposition of co-packaged optics.

However, the laser source segment is estimated to register a CAGR of 25.5% over the forecast period in the European market due to the increasing requirement for external laser sources in co-packaged optics configurations due to thermal constraints on the main substrate. Integrating lasers directly on the silicon substrate can lead to performance degradation due to heat generated by the adjacent application-specific integrated circuit. According to III-V Lab, a joint laboratory in France, external laser sources provide better thermal management and reliability for high-power operations. As per Yole Développement, the shift towards external cavity lasers and distributed feedback lasers mounted on separate submounts is gaining traction among module manufacturers. This approach allows for the use of indium phosphide-based lasers, which offer superior performance compared to silicon-based alternatives. The demand for high-output power and narrow-linewidth lasers increases with higher data rates and longer transmission distances. European companies are investing in the development of hybrid integration techniques to connect external lasers efficiently with silicon photonics chips. The need for redundant laser sources to ensure system reliability further boosts the volume demand. The complexity of aligning and coupling external lasers with the optical engine creates opportunities for specialized packaging services. Government funding for photonics research supports the innovation in laser technologies. The growing emphasis on energy efficiency drives the development of more efficient laser diodes. This segment benefits from the technological necessity of separating heat-generating components from sensitive electronics.

By End-Use Application

The hyperscale cloud data centers segment occupied the major share of 46.4% of the regional market in 2025 due to the massive scale of operations conducted by major cloud service providers who require high-bandwidth and low-latency interconnects to manage vast amounts of data. According to Eurostat, the usage of cloud computing services by enterprises in the European Union has reached record levels, necessitating robust backend infrastructure. Hyperscalers are among the first to adopt co-packaged optics to address the power and space limitations of traditional pluggable modules. As per the Uptime Institute, European data centers are expanding rapidly to meet the demand for digital services, with hyperscale facilities leading the construction activity. These operators have the financial resources and technical expertise to implement cutting-edge technologies like co-packaged optics. The ability to scale network capacity without proportionally increasing power consumption is a key driver for adoption. Hyperscalers operate at a scale where even small improvements in energy efficiency translate to significant cost savings. The integration of co-packaged optics into their switch designs allows for higher port densities and simplified cabling. The competitive pressure to offer faster and more reliable cloud services encourages continuous innovation. Partnerships between hyperscalers and semiconductor manufacturers facilitate the customization of co-packaged solutions. The trend towards centralized data processing in large hubs further concentrates demand in this segment. The strategic importance of data sovereignty in Europe also drives local hyperscale investments. This segment sets the pace for technology adoption in the broader market.

On the other end, the high-performance computing (HPC) and artificial intelligence/machine learning (AI/ML) clusters segment is projected to be the fastest-growing application area in the Europe co-packaged optics market and record a CAGR of 31.5% over the forecast period. The surge in demand for AI training and inference capabilities that require extremely high-bandwidth and low-latency communication between processors is propelling the expansion of the HPC and AI/ML clusters segment in the European market. According to the European High Performance Computing Joint Undertaking, Europe is investing billions of euros in supercomputing infrastructure to maintain its competitive edge in scientific research and industrial innovation. AI models, such as large language models, generate massive data traffic that overwhelms traditional networking solutions. As per the German Research Center for Artificial Intelligence, co-packaged optics offers the necessary bandwidth density to support thousands of interconnected GPUs in AI clusters. The reduction in latency provided by co-packaged optics improves the overall performance of parallel computing tasks. Research institutions and automotive companies developing autonomous driving technologies are also adopting these clusters. The need for real-time data processing in industrial automation drives the adoption of high-performance networks. Government initiatives supporting AI development create a favorable environment for market growth. The specialization of hardware for AI workloads makes co-packaged optics an ideal solution. The ability to handle bursty traffic patterns typical of AI applications further enhances its appeal. This segment represents the frontier of computational demand, driving technological advancement. The convergence of HPC and AI creates a synergistic effect on market expansion.

COUNTRY LEVEL ANALYSIS

Germany Co Packaged Optics Market Analysis

Germany dominated the market in Europe in 2025 with 25.5% of the regional market share. The dominant position of Germany in the European market is attributed to the country’s strong industrial base and leadership in automotive and manufacturing sectors, which are increasingly relying on high-performance computing. According to the Federal Ministry for Economic Affairs and Climate Action, Germany is investing heavily in digital infrastructure and semiconductor technologies to support Industry 4.0 initiatives. The presence of major research institutions, such as the Fraunhofer Society, drives innovation in photonics and advanced packaging. As per the German Semiconductor Industry Association, the country is home to several key players in the optical components supply chain. The automotive industry’s shift towards autonomous driving requires massive data processing capabilities, which co-packaged optics can provide. German data center operators are expanding their facilities to meet the growing demand for cloud services. The government’s support for sustainable technologies aligns with the energy-efficiency benefits of co-packaged optics. Collaborations between universities and industry accelerate the development of next-generation optical interconnects. The strong engineering culture in Germany fosters the adoption of complex technologies. The presence of multinational technology companies with research and development centers in the country further stimulates demand. Regulatory frameworks promoting digital sovereignty encourage local production and innovation. These factors collectively ensure that Germany remains the primary driver of the European co-packaged optics market. The focus on industrial automation and smart manufacturing sustains long-term growth.

United Kingdom Co Packaged Optics Market Analysis

The United Kingdom accounted for a substantial share of the Europe co-packaged optics market in 2025. The UK market is characterized by a vibrant technology sector and significant investments in artificial intelligence and cloud computing. According to the Office for National Statistics, the digital economy in the UK is growing faster than the overall economy, driving demand for advanced networking solutions. London is a global hub for data centers and financial services, which require high-speed and low-latency communication. British researchers at institutions like the University of Southampton are pioneers in photonics, contributing to the development of co-packaged optics technologies. The UK government’s National AI Strategy emphasizes the importance of hardware infrastructure in supporting AI innovation. Startups in the UK are developing innovative silicon photonics platforms, attracting venture capital from around the world. The telecommunications sector in the UK is also an early adopter of advanced optical interconnects for network core upgrades. The emphasis on high-performance computing for scientific discovery, supported by organizations like UK Research and Innovation, further fuels demand. The UK’s open market environment encourages international collaboration and technology transfer. The focus on net-zero targets drives the adoption of energy-efficient solutions in the data center sector. These elements combine to make the UK a key player in the European market, fostering a competitive and innovative landscape for co-packaged optics.

COMPETITIVE LANDSCAPE

The competition in the Europe co packaged optics market is characterized by intense rivalry among global semiconductor giants specialized photonics firms and emerging technology startups. Established players leverage their extensive manufacturing capabilities and existing customer relationships to offer integrated solutions that appeal to hyperscale data center operators and telecommunications providers. These companies focus on performance metrics such as bandwidth density power efficiency and latency to maintain their competitive edge. Meanwhile specialized photonics companies differentiate themselves through innovative designs and customized optical engines that address specific application needs. The market sees frequent collaborations between hardware manufacturers and software developers to create holistic networking solutions. Regulatory compliance particularly regarding energy efficiency and data sovereignty serves as a key differentiator influencing procurement decisions. Vendors that demonstrate robust supply chain resilience and local production capabilities gain a significant advantage. The rapid pace of technological advancement requires continuous investment in research and development forcing competitors to innovate constantly. This dynamic environment fosters a culture of collaboration and competition driving overall market maturity. Intellectual property protection and patent portfolios play a crucial role in maintaining market positions. The presence of strong research ecosystems in countries like Germany and France further stimulates innovation.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe co packaged optics market are

- Ayar Labs Inc.

- Broadcom Inc.

- Cisco Systems Inc.

- Intel Corporation

- Ranovus Inc.

- TE Connectivity Ltd.

- Furukawa Electric Co., Ltd.

- Hisense Broadband Multimedia Technology Co., Ltd.

- POET Technologies Inc.

- Kyocera Corporation

- Huawei Technologies Co., Ltd.

- SENKO Advanced Components, Inc.

- Sumitomo Electric Industries, Ltd.

- Coherent Corp.

- Taiwan Semiconductor Manufacturing Company Limited

- Lumentum Holdings Inc.

- NVIDIA Corporation

- Marvell Technology, Inc.

- Ciena Corporation

- Nokia Corporation

- InnoLight Technology (Suzhou) Ltd.

- Acacia Communications Inc.

- Hon Hai Precision Industry Co., Ltd.

- Jabil Inc.

Top Players In The Market

- Intel Corporation is a pivotal force in the Europe co packaged optics market leveraging its extensive semiconductor manufacturing capabilities and research expertise. The company contributes significantly to the global market by developing integrated silicon photonics solutions that combine optical engines with advanced computing chips. Intel recently expanded its collaboration with European research institutes to advance high volume manufacturing techniques for co packaged optics. This strategic move allows Intel to optimize thermal management and signal integrity for next generation data centers. The company focuses on reducing power consumption and latency which are critical for artificial intelligence workloads. By integrating photonics directly into processor packages Intel enhances bandwidth density and efficiency. Their commitment to open standards facilitates interoperability across diverse networking environments. Intel continues to invest in pilot lines for advanced packaging technologies ensuring scalability and reliability. These initiatives reinforce its position as a leader in hybrid electronic photonic integration. The company’s robust supply chain and technical support strengthen its appeal to European hyperscalers and telecommunications providers seeking innovative connectivity solutions.

- Broadcom Inc plays a critical role in the Europe co packaged optics market through its leadership in semiconductor and infrastructure software solutions. The company offers high performance switching chips and co packaged optics modules that enable ultra low latency and high bandwidth data transmission. Broadcom contributes to the global market by delivering scalable solutions for hyperscale data centers and cloud service providers. Recent actions include the enhancement of its Tomahawk series switches with integrated co packaged optics capabilities to support 51.2 terabit per second capacities. This innovation addresses the growing demand for energy efficient networking in artificial intelligence clusters. Broadcom actively partners with European original equipment manufacturers to customize solutions for specific regional requirements. The company emphasizes reliability and performance ensuring seamless integration into existing network architectures. Its focus on reducing total cost of ownership drives adoption among large scale operators. Broadcom’s continuous investment in research and development ensures it remains at the forefront of optical interconnect technology. These efforts solidify its reputation as a key enabler of next generation digital infrastructure in Europe.

- Nokia Corporation is a prominent player in the Europe co packaged optics market known for its comprehensive portfolio of networking and telecommunications equipment. The company contributes to the global market by integrating co packaged optics into its high capacity routers and switches for service provider networks. Nokia recently launched new platform updates that leverage co packaged optics to enhance spectral efficiency and reduce power consumption in fifth generation and fixed access networks. This development supports the stringent sustainability goals of European telecommunications operators. Nokia collaborates with academic institutions and industry consortia to drive standardization and innovation in silicon photonics. The company focuses on end to end network optimization ensuring that optical interconnects meet the rigorous demands of modern digital services. Its strong presence in the European market allows for close engagement with key stakeholders and regulators. Nokia’s emphasis on open and disaggregated networks promotes flexibility and vendor diversity. These strategic initiatives strengthen its competitive position and drive the adoption of advanced optical technologies. The company’s commitment to innovation and sustainability aligns with the evolving needs of the European telecommunications landscape.

Top Strategies Used by the Key Market Participants

Key players in the Europe co packaged optics market primarily focus on strategic partnerships and collaborative research initiatives to accelerate technology development and standardization. Companies frequently engage with universities and research institutes to advance silicon photonics and advanced packaging techniques. This approach allows them to share risks and leverage specialized expertise in nanoelectronics and optics. Another major strategy involves vertical integration where semiconductor manufacturers expand their capabilities to include optical component production and assembly. This integration ensures better control over quality and supply chain stability. Vendors also emphasize compliance with European sustainability regulations by designing energy efficient solutions that reduce carbon footprints. Investment in pilot manufacturing lines is common to demonstrate scalability and reliability to potential customers. Additionally companies participate in industry consortia to define interoperability standards and promote widespread adoption. These strategies collectively drive innovation and market growth while addressing technical and regulatory challenges effectively.

RECENT MARKET NEWS

- In March 2024, Intel Corporation expanded its silicon photonics manufacturing capacity in Ireland to support co packaged optics production. This expansion is anticipated to allow Intel to meet growing demand and strengthen the Europe co packaged optics market presence.

- In January 2024, Broadcom Inc launched its next generation switching silicon with integrated co packaged optics for AI clusters. This launch is anticipated to allow Broadcom to offer higher bandwidth solutions and strengthen the Europe co packaged optics market presence.

- In November 2023, Nokia Corporation introduced new router platforms featuring co packaged optics technology for sustainable networks. This introduction is anticipated to allow Nokia to reduce power consumption and strengthen the Europe co packaged optics market presence.

- In September 2023, GlobalFoundries partnered with a European research institute to develop advanced packaging techniques for photonics. This partnership is anticipated to allow GlobalFoundries to enhance manufacturing capabilities and strengthen the Europe co packaged optics market presence.

- In June 2023, Marvell Technology acquired a startup specializing in silicon photonics design tools to optimize co packaged modules. This acquisition is anticipated to allow Marvell to improve design efficiency and strengthen the Europe co packaged optics market presence.

MARKET SEGMENTATION

This research report on the Europe co packaged optics market is segmented and sub-segmented into the following categories.

By Data Rate

- Below 1.6 T

- 1.6 T

- 3.2 T

- 6.4 T and Above

By Component

- Optical Engine

- Electrical IC

- Laser Source

- Connector and Packaging

- Other Components

By Integration Approach

- On-board Optics

- Co-packaged Optics

By End-use Application

- Hyperscale Cloud Data Centers

- Enterprise Data Centers

- Telco Central Offices

- HPC and AI/ML Clusters

- Other End-use Applications

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe co-packaged optics market?

Rising demand for high-speed data transmission and efficient data center connectivity is driving growth.

Why are co-packaged optics gaining importance in Europe?

They improve bandwidth performance and reduce power consumption in networking systems.

How would you explain co-packaged optics in simple terms?

It is a technology that integrates optical components directly with electronic chips.

Where are co-packaged optics most commonly used across Europe?

They are widely used in data centers, cloud infrastructure, and high-performance computing systems.

What makes co-packaged optics important for modern networking?

They enable faster data transfer and improve system efficiency.

From a technical perspective, is co-packaged optics a valuable innovation?

Yes, it enhances performance while reducing energy usage and latency.

What challenges are affecting the Europe co-packaged optics market?

High development costs and integration complexity are key challenges.

How is data center growth influencing this market?

Expanding data centers are increasing demand for high-speed connectivity solutions.

Which segments contribute the most to co-packaged optics demand?

Cloud computing and hyperscale data centers are major contributors.

Is the Europe co-packaged optics market growing steadily?

Yes, it is expanding with increasing data traffic and digitalization.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com