Europe Cocoa Market Size, Share, Trends, & Growth Forecast Report By Application (Confectionery Food & Beverages, Cosmetics, Pharmaceutical), Product Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Cocoa Market Report Summary

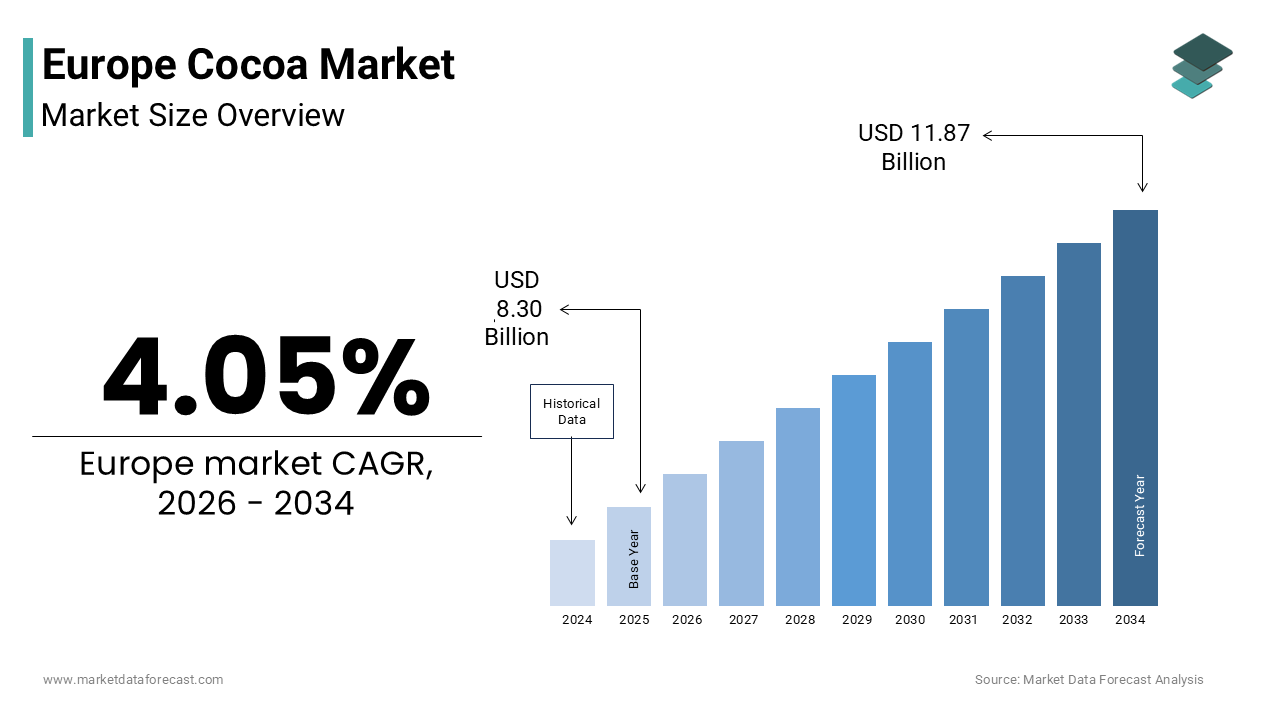

The Europe cocoa market was valued at USD 8.30 billion in 2025, is estimated to reach USD 8.64 billion in 2026, and is projected to reach USD 11.87 billion by 2034, growing at a CAGR of 4.05% during the forecast period from 2026 to 2034. The growth of the Europe cocoa market is driven by the region’s dominance in cocoa processing, strong consumer demand for premium chocolate products, and increasing emphasis on sustainable and ethically sourced cocoa supply chains. Europe continues to function as the global hub for cocoa grinding, value addition, and chocolate manufacturing, supported by advanced processing infrastructure and strategic import networks. Furthermore, rising adoption of traceability technologies, expansion of premium dark chocolate consumption, and innovation in cocoa byproduct utilization across food, cosmetic, and pharmaceutical applications are reinforcing market expansion. While regulatory compliance and supply volatility present challenges, Europe’s leadership in quality standards, sustainability certification, and processing capabilities sustains its position as a central node in the global cocoa ecosystem.

Key Market Trends

-

Strong leadership of Europe in global cocoa grinding and value-added cocoa ingredient production.

-

Rising consumer preference for premium, organic, and ethically sourced chocolate products.

-

Increasing implementation of blockchain and digital traceability systems across cocoa supply chains.

-

Expansion of cocoa byproduct applications in functional foods, cosmetics, and sustainable packaging.

-

Growing demand for high cocoa-content dark chocolate supports premiumization trends.

Segmental Insights

- Based on application, the confectionery segment held 71.2% of the Europe cocoa market share in 2025, supported by strong cultural integration of chocolate consumption, extensive artisanal production, and large-scale confectionery manufacturing across the region.

- Based on product type, the chocolate segment accounted for 63.2% of the Europe cocoa market share in 2025, driven by Europe’s position as a leading chocolate producer and consumer market characterized by innovation, premiumization, and diversified product offerings.

Regional Insights

The Europe cocoa market exhibits strong performance across key countries influenced by processing capacity, chocolate manufacturing heritage, and consumer demand patterns.

-

Germany led the market with 23.4% share in 2025, supported by its position as Europe’s largest chocolate producer, strong import infrastructure, and high domestic consumption levels.

-

The Netherlands plays a pivotal role, functioning as a global cocoa processing and trading hub anchored by the Port of Amsterdam and advanced grinding facilities.

-

France demonstrates steady growth, driven by premium artisanal chocolate production and strong consumer preference for high cocoa-content products.

-

The United Kingdom maintains a stable market, supported by a blend of heritage brands, craft chocolate makers, and growing ethical sourcing initiatives.

-

Switzerland continues to hold a notable influence, leveraging premium chocolate manufacturing, high per capita consumption, and globally recognized confectionery brands.

Competitive Landscape

The Europe cocoa market is characterized by the presence of multinational processors, integrated confectionery manufacturers, and premium artisanal chocolate producers competing across industrial scale, sustainability performance, and product differentiation dimensions. Leading companies are prioritizing digital traceability platforms, deforestation-free sourcing programs, and farmer livelihood initiatives to comply with regulatory frameworks and meet evolving consumer expectations. Technological investments in grinding efficiency, contaminant mitigation, and cocoa butter extraction are enhancing processing capabilities, while strategic diversification into cosmetics, functional foods, and circular economy applications is expanding revenue streams. Market participants are also strengthening partnerships with cooperatives, NGOs, and certification bodies to secure long-term supply and reinforce brand credibility. Prominent players operating in the Europe cocoa market include Barry Callebaut AG, Cargill Incorporated, Olam Food Ingredients (ofi), ECOM Agroindustrial Corp., Sucden Group, Touton S.A., Fuji Oil Holdings Inc., Nestlé S.A., Ferrero International S.A., Mondelēz International, Inc., Chocoladefabriken Lindt & Sprüngli AG, Valrhona S.A.S., Cemoi Group, Puratos Group, and Kerry Group plc.

Europe Cocoa Market Size

The Europe cocoa market size was valued at USD 8.30 billion in 2025 and is anticipated to reach USD 8.64 billion in 2026 from USD 11.87 billion by 2034, growing at a CAGR of 4.05% during the forecast period from 2026 to 2034.

Cocoa represents a sophisticated and highly regulated segment of the global chocolate and confectionery value chain, centred on the import, processing, and consumption of cocoa beans, liquor, butter, and powder. Unlike production driven markets in West Africa or Latin America, Europe functions as the world’s primary cocoa processing hub and premium consumption zone. According to the European Commission, the EU remains one of the largest importers of cocoa beans, primarily sourcing from Côte d’Ivoire and Ghana, which together supply the majority of global output. Europe’s role extends beyond volume, as it sets global benchmarks for quality, sustainability certification, and food safety. The European Food Safety Authority enforces strict limits on contaminants such as cadmium and ochratoxin A, shaping sourcing practices worldwide. Furthermore, as per Eurostat, cocoa products sold in the EU must comply with mandatory origin labeling and deforestation due diligence under the new EU Deforestation Regulation. This confluence of industrial scale, regulatory leadership, and consumer consciousness positions Europe not merely as a market but as the ethical and technical gatekeeper of the global cocoa economy.

MARKET DRIVERS

Europe’s Dominance in Cocoa Processing and Value Addition

Europe maintains unrivalled leadership in cocoa processing, transforming raw beans into high value ingredients that fuel both domestic confectionery industries and global exports, which is one of the major factors propelling the growth of the European cocoa market. As per the European Cocoa Association, the continent grinds more than one third of the world’s total cocoa annually, with the Port of Amsterdam alone handling a significant share of global cocoa trade. This processing supremacy stems from century old industrial infrastructure, strategic port access, and deep integration with chocolate manufacturers like Barry Callebaut and Mondelez. The Netherlands leads in grinding capacity, followed by Germany and France. Processors invest heavily in precision roasting, alkalization, and butter extraction technologies to meet exacting specifications for flavor, color, and fat content demanded by premium brands. As per the German Confectionery Industry Association, most of Europe’s processed cocoa is re-exported as semi-finished goods to Asia and North America. This value addition not only generates significant economic output but also allows Europe to dictate quality standards, influence sustainable sourcing agendas, and capture margin far beyond raw commodity trading, solidifying its role as the nerve center of the global cocoa ecosystem.

Strong Consumer Demand for Premium and Ethically Sourced Chocolate

European consumers increasingly prioritize transparency, sustainability, and craftsmanship in their chocolate purchases, directly shaping cocoa sourcing and processing practices, which is further contributing to the expansion of the European cocoa market. As per the European Commission Special Eurobarometer on Food Safety, a majority of EU citizens consider ethical production and environmental impact when buying chocolate, driving demand for certified cocoa. Labels such as Fairtrade, Rainforest Alliance, and organic certifications now appear widely on chocolate bars sold in Western Europe, according to FiBL. This preference extends to premiumization, with sales of dark chocolate containing higher cocoa content showing strong growth across Germany, France, and Italy. Artisanal bean to bar chocolatiers, numbering in the thousands across the EU, further amplify this trend by highlighting single origin beans and direct trade relationships. Retailers such as REWE and Carrefour have responded with private label lines featuring traceable cocoa from verified cooperatives. This cultural shift transforms cocoa from a bulk ingredient into a story laden commodity, compelling processors to invest in blockchain traceability and farmer income programs to maintain brand trust and shelf space in an ethically conscious marketplace.

MARKET RESTRAINTS

Stringent EU Regulations on Contaminants and Deforestation

The Europe cocoa market faces mounting pressure from rigorous regulatory frameworks that impose significant compliance burdens on importers and processors. The European Union has set maximum levels for cadmium in cocoa products, disproportionately affecting beans from Latin America where volcanic soils naturally elevate cadmium concentrations. As per the European Food Safety Authority, non-compliance among imported batches has triggered rejections and costly reformulations. More transformative is the EU Deforestation Regulation, requiring companies to prove that cocoa was not produced on land deforested after December 2020. As per the Joint Research Centre, many global cocoa supply chains lack geolocation data precise enough to meet this standard. Compliance demands satellite monitoring, digital farmer registries, and audit trails that small cooperatives cannot afford. These regulations, while environmentally justified, fragment supply, increase costs, and risk excluding vulnerable producers, forcing European buyers to consolidate sourcing and invest heavily in verification infrastructure just to maintain market access.

Volatility in Global Cocoa Supply and Price Instability

Extreme price fluctuations and supply shortages stemming from climate shocks and crop diseases in West Africa severely disrupt Europe’s cocoa market stability. As per the International Cocoa Organization, output from Côte d’Ivoire and Ghana fell significantly year on year, forcing European processors to draw down inventories and ration allocations. This volatility erodes margins for confectioners, with companies such as Nestlé reporting increases in raw material costs directly tied to cocoa. Unlike agricultural commodities with deep futures markets, cocoa remains thin and speculative, amplifying swings. European manufacturers, unable to pass all costs to consumers amid inflation fatigue, face squeezed profitability. Without diversified sourcing or long-term farmer investment, Europe remains hostage to ecological fragility thousands of kilometers away, undermining planning certainty and threatening product availability in one of the world’s most beloved food categories.

MARKET OPPORTUNITIES

Expansion of Cocoa Byproduct Utilization in Food and Cosmetic Industries

The valorisation of cocoa byproducts that were historically discarded but now offer sustainable ingredients for circular economies, which is a promising opportunity in the European cocoa market. Cocoa mucilage, the sweet pulp surrounding beans, is being fermented into low alcohol beverages and natural sweeteners. French startup Kaoka launched a mucilage syrup in 2024 now used by patisseries across Paris. Cocoa shells, rich in fiber and polyphenols, are milled into functional food additives for bakery and breakfast cereals. German company Rübezahl introduced a cocoa shell flour in 2024 with reduced sugar content compared to conventional blends. In cosmetics, cocoa butter derivatives and polyphenol extracts feature in anti-aging creams due to high antioxidant content. Brands like L’Occitane and Weleda now source certified shell extracts from Dutch processors. According to the European Bioplastics Association, cocoa husk is also being trialed for biodegradable packaging films. The EU’s Circular Economy Action Plan actively supports such innovations through Horizon Europe grants, recognizing that valorizing waste streams enhances sustainability while creating new revenue channels.

Adoption of Blockchain and Digital Farmer Platforms for Traceability

Digital innovation presents a transformative opportunity for the European cocoa market. Companies are deploying blockchain ledgers and mobile based farmer platforms to link individual farms to final products, satisfying both regulatory mandates and consumer expectations. Barry Callebaut’s “Cocoa Horizons” program uses GPS mapping and digital ID systems to register farmers across Côte d’Ivoire and Ghana, enabling real time monitoring of agroforestry practices. Similarly, Tony’s Chocolonely partners with IBM Food Trust to provide QR code scans showing farm location, income premiums paid, and child labor prevention measures. As per the European Institute of Innovation and Technology, pilot projects in Belgium and the Netherlands have significantly reduced traceability gaps using these tools. The EU Deforestation Regulation further accelerates adoption by requiring geolocation data for every production plot. Beyond compliance, this transparency builds brand equity, with consumers willing to pay more for fully traceable chocolate as per a Wageningen University study.

MARKET CHALLENGES

Dependence on Politically Unstable and Climate Vulnerable Origin Countries

Europe’s cocoa market remains critically exposed to geopolitical and climatic risks in its primary sourcing regions, particularly West Africa, where governance challenges and environmental fragility threaten long term supply security. Côte d’Ivoire and Ghana account for the majority of global cocoa production, yet both nations face recurring political tensions, land tenure disputes, and inadequate rural infrastructure. As per the World Bank, only a minority of Ivorian cocoa farms have formal land titles, complicating sustainability investments and deforestation monitoring. Climate change intensifies the threat, with rising temperatures and erratic rainfall reducing yields over the past decade, as noted by the Intergovernmental Panel on Climate Change. Efforts to diversify sourcing to Latin America or Southeast Asia are hampered by lower volumes and different flavor profiles unsuited to European processing standards. This geographic concentration creates systemic vulnerability—any export restriction, civil unrest, or disease outbreak can trigger immediate price spikes and allocation crises across Europe’s confectionery sector.

Shortage of Skilled Labor in Cocoa Processing and Quality Control

A critical yet often overlooked challenge confronting the Europe cocoa market is the declining availability of specialized technicians and sensory experts essential for maintaining processing excellence and product consistency. Cocoa roasting, winnowing, and conching require nuanced judgment honed over years as skills increasingly scarce as older workers retire and younger generations pursue digital careers. As per the German Confectionery Employers’ Association, many cocoa processing plants reported difficulty filling roles for master roasters and quality assurance chemists. Sensory panels, vital for flavor profiling and batch matching, face similar attrition, with only a limited number of certified cocoa tasters operating across the EU, as per the European Cocoa Trade Group. Training pipelines are weak, with only a handful of vocational schools offering dedicated cocoa processing diplomas. This deficit risks quality drift, inconsistent product performance, and slower innovation in areas like low sugar or allergen free formulations. Without coordinated industry academia initiatives to professionalize and modernize cocoa craftsmanship, Europe’s reputation for premium chocolate may erode despite abundant raw material access.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.05% |

| Segments Covered | By Application, Product Type and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Barry Callebaut AG, Cargill Incorporated, Olam Food Ingredients (ofi), ECOM Agroindustrial Corp., Sucden Group, Touton S.A., Fuji Oil Holdings Inc., Nestlé S.A., Ferrero International S.A., Mondelēz International, Inc., Chocoladefabriken Lindt & Sprüngli AG, Valrhona S.A.S., Cemoi Group, Puratos Group, and Kerry Group plc. |

SEGMENTAL ANALYSIS

By Application Insights

The confectionery segment dominated the Europe cocoa market by holding 71.2% of the regional market share in 2025. The leading position of confectionery segment in the European market is attributed to the Europe’s deep cultural affinity for chocolate as both a daily indulgence and a ceremonial gift, supported by a dense network of artisanal chocolatiers and global confectionery giants. As per the European Commission, the EU produces millions of metric tons of chocolate annually, with Germany, France, and Belgium responsible for a significant share of this output. Iconic products rely heavily on high quality cocoa liquor and butter, driving consistent demand for premium ingredients. Retail channels reinforce this dominance, with supermarkets dedicating extensive shelf space to chocolate and seasonal peaks during Easter and Christmas generating a large portion of annual sales, as per the European Confectionery Association. Furthermore, the rise of premium dark chocolate, now representing a notable share of confectionery sales in Western Europe, fuels demand for high cocoa content formulations. This enduring cultural integration, combined with industrial scale and gifting traditions, ensures confectionery remains the undisputed engine of Europe’s cocoa economy.

The cosmetics segment is the fastest growing application in the Europe cocoa market and is expected to expand at a CAGR of 9.2% over the forecast period owing to the rising consumer preference for natural, bioactive ingredients in skincare and personal care products. Cocoa butter, rich in stearic acid and polyphenols, is prized for its emollient properties and antioxidant capacity, making it a staple in anti-aging creams, lip balms, and body lotions. As per the European Cosmetic Association, thousands of cosmetic products launched in the EU in 2024 featured cocoa derivatives as key ingredients, showing strong growth compared to previous years. Brands like L’Occitane, Weleda, and Rituals highlight ethically sourced cocoa butter in their formulations, aligning with clean beauty trends. The EU’s Chemicals Strategy for Sustainability further favours plant-based actives over synthetic alternatives, accelerating adoption. Additionally, upcycled cocoa shell extracts are gaining traction as sustainable exfoliants and colorants.

By Product Type Insights

The chocolate segment commanded for the largest share of 63.2% of the European market in 2025. The growth of chocolate segment in the European market is attributed to the Europe’s role as both the world’s largest chocolate producer and one of its most voracious consumer regions. As per Eurostat, the average European consumes several kilograms of chocolate annually, with Switzerland leading per capita consumption. Industrial-scale manufacturing hubs in Germany, Belgium, and Italy transform imported cocoa beans into a vast array of products, which is fuelling consistent demand for cocoa liquor, butter, and powder. The segment thrives on innovation, with sugar reduced, plant based, and functional chocolate (enriched with probiotics or collagen) accounting for a growing share of new launches, as per Innova Market Insights. Retailers amplify reach through private label lines and seasonal promotions, while food service channels drive impulse purchases via café hot chocolates and dessert menus. Unlike raw commodities, chocolate carries strong brand equity and emotional resonance, allowing producers to maintain pricing power even amid cocoa price volatility.

The cocoa butter segment is anticipated to register a CAGR of 8.4% over the forecast period in this regional market. The surging demand across multiple high value sectors beyond confectionery is primarily driving the growth of the cocoa butter segment in the European market. In cosmetics, cocoa butter’s superior melting point and skin compatibility make it irreplaceable in premium formulations. As per the European Cosmetic Association, a majority of natural body care brands now use certified cocoa butter as a primary emollient. In pharmaceuticals, it serves as a base for suppositories and ointments due to its stability and biocompatibility. Even within food, demand is rising for high fat cocoa butter in vegan dairy alternatives and specialty baking fats. As per the European Cocoa Association, butter extraction rates have increased as processors optimize bean utilization to meet diversified demand. Additionally, the EU Deforestation Regulation incentivizes full bean valorization, enhancing economic viability for sustainable sourcing programs.

REGIONAL ANALYSIS

Germany Cocoa Market Analysis

Germany led the cocoa market in Europe in 2025 with 23.4% of the regional market share. The dominating position of Germany in the European market is attributed to its position as the continent’s leading chocolate producer and consumer. The country’s market status is defined by industrial scale, technical precision, and a strong tradition of confectionery craftsmanship. As per the German Confectionery Industry Association, Germany produces more chocolate annually than any other European nation, with major facilities operated by Lindt, Storck, and Ritter Sport. The Port of Hamburg serves as a critical cocoa import hub. Consumer demand remains robust, with per capita chocolate consumption among the highest globally. Recent trends emphasize premiumization and sustainability, with organic and Fairtrade chocolate sales showing strong growth. German processors were among the first to implement EU deforestation due diligence systems using satellite verification.

Netherlands Cocoa Market Analysis

The Netherlands held a promising share of the European cocoa market in 2025. The growth of Netherlands is distinguished not by consumption but by its unparalleled role as the global cocoa processing and trading nexus. The country’s market status centers on the Port of Amsterdam, which handles a significant portion of world cocoa trade. As per the Dutch Central Bureau of Statistics, the Netherlands grinds hundreds of thousands of metric tons of cocoa annually, primarily for re-export. Multinational processors like Cargill, Olam, and Barry Callebaut operate state of the art refineries. The Dutch government supports traceability innovation through initiatives such as Cocoa Compass.

France Cocoa Market Analysis

France is anticipated to register a healthy CAGR in the European cocoa market during the forecast period. The French market is characterized by artisanal excellence and premium brand heritage. The country is home to iconic houses like Valrhona, Cémoi, and Michel Cluizel. As per FranceAgriMer, France imports large volumes of cocoa annually, with most sourced from certified sustainable programs. French consumers show strong preference for dark chocolate, with high cocoa content products representing a significant share of sales. The government reinforces quality through geographical indications such as “Chocolat de France.” Paris alone hosts hundreds of artisanal chocolatiers, many emphasizing single origin beans and bean to bar processes.

United Kingdom Cocoa Market Analysis

The United Kingdom is projected to grow at a steady CAGR in the European cocoa market during the forecast period. The UK is notable for its dynamic blend of heritage brands and modern ethical entrepreneurship. Mass market strength is evident, with Cadbury accounting for a large portion of UK chocolate sales. The craft sector is thriving, with hundreds of beans to bar makers nationwide. As per the British Confectionery Association, the UK imports significant volumes of cocoa, increasingly sourced through direct trade models. Consumer activism drives change, with a majority of shoppers prioritizing ethical certifications, as per the Food Standards Agency. Post Brexit, the UK has aligned its deforestation rules with EU standards. Companies like Tony’s Chocolonely and Hotel Chocolat lead transparency initiatives.

Switzerland Cocoa Market Analysis

Switzerland is anticipated to account for a notable share of the European cocoa market during the forecast period. Despite its small population, owing to its outsized influence in premium chocolate manufacturing and export. The country’s market status is built on legendary quality, dairy integration, and global brand power. As per the Swiss Federal Customs Administration, Switzerland exports more chocolate than it consumes, primarily to the EU, United States, and Middle East. Iconic firms like Lindt, Nestlé, and Sprüngli operate vertically integrated supply chains. Per capita consumption is the highest in Europe. Sustainability is embedded in strategy, with Lindt’s “Cocoa Farming Program” covering thousands of farmers with traceability down to the plot level.

Top Players in the Market

Barry Callebaut AG

Barry Callebaut AG is the world’s leading cocoa processor and chocolate manufacturer with a dominant footprint across Europe, supplying industrial clients and gourmet artisans alike. Headquartered in Switzerland, the company operates major grinding facilities in Belgium, Germany, and the Netherlands, processing over 20 percent of global cocoa output. Barry Callebaut contributes significantly to global sustainability efforts through its Cocoa Horizons Foundation, which supports over 200,000 farmers with agroforestry training and income diversification. In recent years, the company strengthened its European position by launching “Forever Chocolate,” a roadmap targeting 100 percent sustainable ingredients by 2025. It also pioneered ruby chocolate and plant-based alternatives to meet evolving consumer preferences. These innovations, combined with end-to-end traceability via digital farmer platforms, reinforce its role as a responsible and forward-looking leader in Europe’s cocoa value chain.

Cargill Incorporated

Cargill Incorporated maintains a formidable presence in the Europe cocoa market through its extensive network of processing plants, sustainability programs, and ingredient solutions. The company operates one of the world’s largest cocoa refineries in Amsterdam and supplies cocoa liquor, butter, and powder to confectionery giants across the continent. Cargill contributes to global supply chain resilience by implementing its “Cocoa Promise” initiative, which promotes child labor monitoring, farmer training, and deforestation free sourcing. Recently, it enhanced its European operations by integrating satellite-based land mapping into its traceability system to comply with the EU Deforestation Regulation. It also expanded its portfolio of low cadmium cocoa powders to meet stringent EU food safety standards. These actions demonstrate Cargill’s commitment to ethical sourcing, regulatory compliance, and technical excellence in a highly scrutinized market.

Olam International Limited

Olam International Limited is a key player in the Europe cocoa market, leveraging its global origination network to deliver traceable, sustainable cocoa ingredients to European processors and brands. The company sources beans from over 20 countries and operates processing facilities in the Netherlands and Germany, specializing in high quality cocoa butter and powder. Olam contributes to global sustainability through its AtSource platform, which provides customers with real time data on environmental and social metrics across the supply chain. In recent years, it strengthened its European position by achieving full alignment with the EU Deforestation Regulation through GPS mapped farm registries and blockchain enabled verification. It also launched upcycled cocoa shell extracts for the cosmetic industry, supporting circular economy goals. These initiatives position Olam as an agile and transparent partner in Europe’s transition toward ethical and innovative cocoa consumption.

Top Strategies Used by the Key Market Participants

Key players in the Europe cocoa market invest heavily in digital traceability platforms that map cocoa from farm to factory to comply with the EU Deforestation Regulation and satisfy consumer demand for transparency. They expand sustainability programs that provide direct income support, agroforestry training, and child labor prevention to secure long term supply and brand trust. Companies innovate in product formulation by developing low cadmium cocoa powders, plant-based chocolates, and upcycled byproducts for cosmetics and food. Strategic partnerships with governments and NGOs enhance credibility and scale impact across origin countries. Additionally, firms optimize processing efficiency through advanced grinding and butter extraction technologies to maximize yield and maintain quality amid volatile raw material costs.

COMPETITIVE LANDSCAPE

Competition in the Europe cocoa market is defined by a dual race: one for industrial scale and efficiency, the other for ethical credibility and premium differentiation. Global processors like Barry Callebaut and Cargill compete on volume, technological sophistication, and regulatory compliance, leveraging massive grinding capacities and integrated supply chains. Simultaneously, artisanal chocolatiers and ethical brands vie for consumer loyalty through storytelling, direct trade, and radical transparency. The EU’s stringent regulations on contaminants and deforestation act as both barrier and catalyst as excluding non-compliant actors while rewarding those who invest in traceability. Retailers exert immense influence, demanding certifications and sustainability proof points that reshape sourcing strategies. Innovation spans beyond confectionery into cosmetics and functional foods, broadening cocoa’s relevance. Ultimately, success hinges on balancing economic viability with demonstrable social and environmental responsibility in a market where ethics are no longer optional but central to commercial survival.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Cocoa Market include

- Barry Callebaut AG

- Cargill Incorporated

- Olam Food Ingredients (ofi)

- ECOM Agroindustrial Corp.

- Sucden Group

- Touton S.A.

- Fuji Oil Holdings Inc.

- Nestlé S.A.

- Ferrero International S.A.

- Mondelēz International, Inc.

- Chocoladefabriken Lindt & Sprüngli AG

- Valrhona S.A.S.

- Cemoi Group

- Puratos Group

- Kerry Group plc

MARKET SEGMENTATION

This research report on the Europe Cocoa Market has been segmented and sub-segmented based on the following categories.

By Application

- Confectionery

- Food & Beverages

- Cosmetics

- Pharmaceutical

By Product Type

- Cocoa Beans

- Cocoa Powder & Cake

- Cocoa Butter

- Chocolate

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe cocoa market?

The Europe cocoa market refers to the production, import, processing, and consumption of cocoa beans and cocoa-derived ingredients used across confectionery, bakery, dairy, and beverage industries.

What factors are driving the Europe cocoa market growth?

Growth is driven by rising chocolate consumption, premium confectionery demand, increasing bakery applications, and expanding specialty cocoa product usage.

Which countries are major cocoa consumers in Europe?

Germany, the UK, France, Italy, Belgium, Switzerland, and the Netherlands are key cocoa-consuming countries due to strong chocolate manufacturing sectors.

What types of cocoa products are commonly used in Europe?

Cocoa butter, cocoa powder, cocoa liquor, and cocoa mass are the most widely used cocoa derivatives.

How does sustainability influence the Europe cocoa market?

Sustainability initiatives such as fair trade sourcing, ethical farming, and traceability programs are significantly shaping purchasing decisions and supply chains.

Which industries use cocoa extensively in Europe?

Confectionery, bakery, dairy, beverages, cosmetics, and nutraceutical industries utilize cocoa and its derivatives.

What role does premium chocolate demand play in the market?

Premium and artisanal chocolate demand supports higher cocoa quality requirements and drives value growth.

How does e-commerce affect cocoa product distribution?

E-commerce enables direct-to-consumer sales of cocoa-based products and specialty ingredients, expanding market accessibility.

What challenges exist in the Europe cocoa market?

Opportunities include premiumization, sustainable sourcing programs, plant-based chocolate innovation, and expansion of specialty cocoa ingredients.

What opportunities exist in the Europe cocoa market?

What opportunities exist in the Europe cocoa market?

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com