Europe Commercial Greenhouse Market Size, Share, Trends & Growth Forecast Report, Segmented By Equipment, Crop Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Commercial Greenhouse Market Size

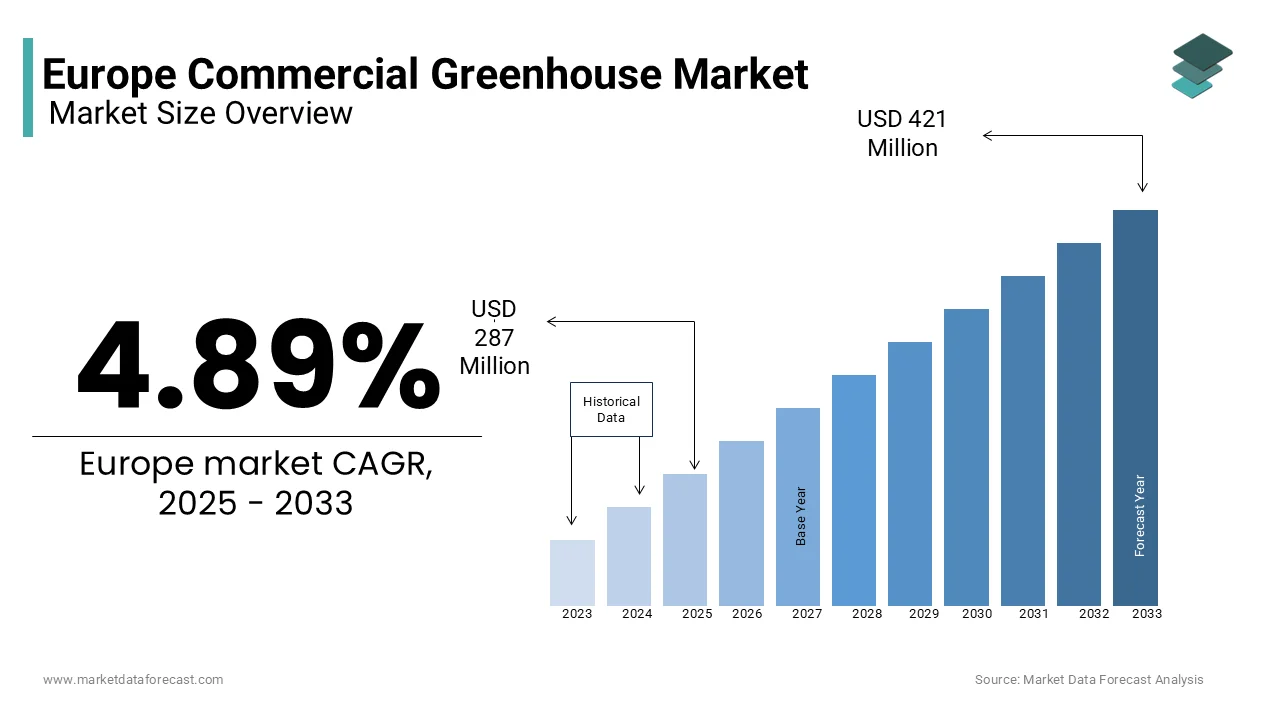

In 2025, the commercial greenhouse market size in Europe was valued at USD 287.33 million and is anticipated to reach USD 301.38 million in 2026 and USD 441.56 million by 2034, growing at a CAGR of 4.89% during the forecast period from 2026 to 2033.

MARKET OVERVIEW

The commercial greenhouse is a controlled-environment agricultural system designed for the large-scale cultivation of high-value crops such as tomatoes, cucumbers, peppers, and leafy greens under engineered glass or polycarbonate structures. These facilities integrate advanced climate control, irrigation, and lighting technologies to optimize yield and resource efficiency year-round, which is independent of external weather fluctuations.

MARKET DRIVERS

Rising Urbanization and Proximity-Based Food Supply Chains

The rise in urban population growth in Europe has intensified demand for fresh, locally grown produce, which reduces dependency on long-haul agricultural imports, and is the primary factor driving the Europe Commercial Greenhouse Market. As per Eurostat, over 75% of Europeans lived in urban areas in 2023, which is projected to rise due to increasing pressure on regional food systems to deliver perishable goods efficiently. Commercial greenhouses are often located near metropolitan centers, which enables year-round cultivation with minimal transportation time. For instance, Denmark’s urban greenhouse operator Nordic Harvest operates one of the world’s largest indoor farms near Copenhagen, producing 1000 tons of leafy greens annually within a 75,000-square-meter facility.

Advancements in Climate-Resilient Crop Production

Europe’s increasing vulnerability to climate extremes has elevated the strategic importance of climate-independent agriculture, which is propelling the Europe Commercial Greenhouse Market growth. Commercial greenhouses mitigate such risks by providing stable microclimates, which enable uninterrupted production despite droughts, floods, or temperature anomalies. As per Spain’s Ministry of Agriculture, in Spain, where prolonged droughts have reduced open-field yields by up to 30% in Andalusia, the greenhouse farms in Almería now produce over 2.5 million tons of vegetables annually, which accounts for 70% of the region’s horticultural output. Integrated systems using desalinated water and solar-powered climate controls have enhanced resilience by making greenhouses an infrastructure for adaptive agriculture in climate-sensitive zones.

MARKET RESTRAINTS

High Initial Capital and Energy Investment

The establishment of a technologically advanced commercial greenhouse requires substantial upfront investment, often exceeding €1.5 million per hectare for fully automated glasshouse facilities. This is a major factor restraining the Europe Commercial Greenhouse Market growth. Energy costs represent a further constraint, with heating and lighting constituting up to 60% of operational expenses in northern European countries during winter months. For example, in the Netherlands, natural gas prices surged by over 300% between 2021 and 2022 due to geopolitical disruptions, which may severely impact greenhouse profitability. The financial burden limits scalability, particularly for small and medium-sized enterprises, by slowing broader market penetration despite long-term productivity gains.

Regulatory and Land Use Constraints

The industry is increasingly hindered by stringent land use policies and environmental regulations. As per the European Environment Agency, the European Union’s Habitats Directive and Natura 2000 network restrict agricultural development in ecologically sensitive zones, which cover nearly 18% of the EU’s territory. The zoning laws in countries like France limit non-agricultural construction on farmland, which complicates the integration of high-tech greenhouse complexes, hindering the Europe Commercial Greenhouse Market. These regulatory hurdles delay project approvals and increase compliance costs by discouraging private investment. As per the European Committee of the Regions, fragmented regional policies further enhance the implementation challenges of cohesive national greenhouse development strategies.

MARKET OPPORTUNITIES

Integration of AI and Precision Agriculture Systems

The integration of artificial intelligence and sensor-based automation is solely to create new opportunities for the growth of the Europe Commercial Greenhouse Market. AI-driven climate control systems can optimize light, humidity, and CO₂ levels in real time, increasing yield efficiency by up to 30% while reducing energy consumption, as per a project by Siemens and Priva in Dutch greenhouses. According to a 2023 study, over 60% of large-scale greenhouse operators in the Netherlands and Germany have adopted AI-enabled irrigation and pest detection systems, reducing water usage by 25% and pesticide applications by 40%.

Expansion of Vertical Farming within Greenhouse Ecosystems

The hybridization of vertical farming techniques within traditional greenhouse frameworks is expected to elevate the growth of the Europe Commercial Greenhouse Market. By stacking cultivation layers, the vertical systems can increase production density by up to 10 times per square meter compared to conventional benches, as evidenced by Infarm’s modular units in Berlin and Paris. As per the Association for Vertical Farming, Europe hosted over 180 commercial vertical farms in 202,3, many integrated into greenhouse complexes to leverage natural light while maximizing output. The urban land scarcity is driving innovation, such as hybrid models, which are gaining traction, and is supported by EU funding under Horizon Europe.

MARKET CHALLENGES

Skilled Labor Shortage in High-Tech Greenhouse Operations

Along with the technological advancements, Europe faces a growing deficit in agritech-skilled personnel capable of managing complex greenhouse ecosystems, which is a major challenge for the Europe Commercial Greenhouse Market expansion. In Poland, half of the greenhouse operators reported difficulty recruiting staff trained in climate control systems and data analytics in a survey. The Netherlands, despite its prominence in greenhouse technology, which relies heavily on seasonal labor from non-EU countries, is creating workforce instability.

Water Resource Scarcity in Southern Europe

Although greenhouses are more water-efficient than open-field farming, their reliance on consistent irrigation poses challenges in water-stressed regions by inhibiting the growth of the Europe commercial Greenhouse Market. Southern Europe, particularly Spain, Italy, and Greece, faces increasing hydrological stress due to prolonged droughts and over-extraction of aquifers, which is hindering the market growth. As per the European Drought Observatory, 38% of EU territory experienced moderate to severe drought conditions in 2022, the greatest recorded extent in four decades. According to Spain’s Geological and Mining Institute, in Almería, Spain, where over 30,000 hectares of greenhouses operate, groundwater levels have declined by an average of 0.8 meters per year over the past decade. While desalination and closed-loop irrigation are being adopted, only 55% of greenhouses in the region recycle irrigation water, which is limiting sustainability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.89% |

| Segments Covered | By Product, Ingredients, Animal Type, and Country |

| Various Analyses Covered | Regional and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Mars, Inc., Del Monte Foods, Hills Pet Nutrition, Inc., Unicharm Corporation, Nippon Formula Feed Manufacturing Company, Ltd, and Pet Center |

SEGMENTAL ANALYSIS

By Equipment Insights

The heating systems segment dominated the European Commercial Greenhouse Market by occupying 38.7% of the market share in 2024. The continent’s climatic necessity for consistent thermal regulation, particularly in northern and continental regions where winter temperatures frequently fall below 5°C for extended periods, is enhancing the market growth. The reliance on heating is amplified by the shift toward year-round production of high-value crops such as tomatoes and cucumbers, which require stable internal temperatures between 18°C and 24°C, promoting the adoption of heating systems. According to Wageningen University & Research, in the Netherlands, the world’s most advanced greenhouse hub, over 90% of commercial glasshouses are equipped with integrated heating systems, which are primarily fueled by natural gas or geothermal energy. The Dutch government’s push for energy-neutral greenhouses has further incentivized the adoption of high-efficiency heating, which includes heat exchangers and district heating networks linked to industrial waste-heat recovery systems.

The cooling systems are projected to register at a CAGR of 7.6% from 2025 to 2033 in the Europe Commercial Greenhouse Market. The rising summer temperatures and prolonged heatwaves across Southern and Central Europeares threatening crop viability if not mitigated. The European Environment Agency confirms that the average number of heatwave days in Europe has more than doubled since the 1980s, with 2022 recording a record 60 million people exposed to extreme heat. In Spain, where greenhouse cultivation spans over 35,000 hectares in Andalusia alone, the adoption of evaporative cooling and fogging systems in new greenhouse constructions is being enhanced.

By Type Insights

The glass greenhouse segment was the largest in the European Commercial Greenhouse Market in 2024. The superior durability, light transmission, efficiency, and compatibility with advanced climate control systems that glass structures provide are enhancing the segment growth rate. As per a report by the Dutch Ministry of Agriculture, Nature and Food Quality, the Netherlands alone operated over 12,000 hectares of greenhouses in 2023, the highest concentration globally, which is enabling it to produce 17.2% of the world’s vegetable seeds and 59.3% of its cut flowers. These structures are increasingly integrated with energy-saving coatings, automated ventilation, and cogeneration units by enhancing their economic and environmental performance.

The plastic greenhouse segment is expected to grow with an expected CAGR of 6.8% from 2025 to 2033 in the Europe Commercial Greenhouse Market. The growth is primarily fueled by their cost-effectiveness and rapid deployment capability, which makes them ideal for small to mid-sized growers and regions with budgetary constraints. Polyethylene film greenhouses require up to 60% lower initial investment compared to glass equivalents, which enables broader access in Eastern and Southern Europe. The modular plastic structures are increasingly adopted in urban peripheries of France and Italy for seasonal crop rotation, which is supported by EU rural development funds that prioritize affordable infrastructure for young farmers.

By Crop Insights

The Fruits and vegetables segment was the largest and held 58.6% of the European Commercial Greenhouse Market share in 2024, with the strong consumer demand for fresh, pesticide-free, and locally grown produce throughout the year. According to Eurostat, tomatoes, cucumbers, and bell peppers dominate greenhouse cultivation, with the EU producing over 62.2 million tons of greenhouse-grown vegetables annually in 2024. Retail chains such as Aldi and Carrefour now source a maximum of their salad vegetables from regional greenhouse farms, which is promoting the economic viability of vegetable-focused operations.

The flowers and ornamentals segment is deemed to grow at an anticipated CAGR of 8.2% from 2025 to 203,3 with the rising demand for cut flowers, potted plants, and decorative greenery in both domestic and commercial spaces, particularly in urban centers. As per the data from Eurostat, the EU exported €100.6 million worth of orchid, hyacinth, narcissus, and tulip bulbs in 2022, and the Netherlands accounted for a significant portion of these bulb exports, with €82 milli, representing 81% of the total EU bulb exports. Advances in LED spectral tuning have enabled year-round blooming of high-value species such as roses, orchids, and chrysanthemums by increasing production cycles. E-commerce platforms like Bloom & Wild have further expanded market reach, creating scalable distribution channels for greenhouse floriculturists.

COUNTRY-LEVEL ANALYSIS

Netherlands Commercial Greenhouse Market Analysis

The Netherlands was the largest contributor in the European Commercial Greenhouse Market by accounting for 7% share in 2024. The integration of agritech innovation, energy efficiency, and export logistics is propelling the market growth. As reported by Wageningen University, Dutch greenhouses produce more than 1.3 million tons of vegetables annually by achieving yields up to ten times higher than open-field farming. Moreover, the country exports €8.6 billion in greenhouse produce yearly, including 60% of the global bell pepper seed trade, cementing its role as Europe’s horticultural engine.

Spain Commercial Greenhouse Market Analysis

Spain held the second position in the Commercial greenhouse market, contributing 18.5% of market share, primarily concentrated in the Almería region, known as the “sea of plastic” due to its vast greenhouse expanse. The region benefits from over 3,000 hours of annual sunlight by enabling near-continuous production with minimal artificial lighting. Recent investments in desalination plants and solar-powered cooling systems are addressing these issues, while EU funding under the NextGenerationEU program has allocated millions to modernize irrigation infrastructure by 2026.

Germany Commercial Greenhouse Market Analysis

Germany is predicted to have prominent growth in Commercial Greenhouse production with a strong emphasis on sustainable and energy-efficient cultivation. As per the report produced by the German Horticultural Society, the country operates over 1,240 hectares, which primarily focuses on tomatoes, peppers, and herbs, where tomatoes occupy 385 hectares in 2024. As per the German Biomass Research Centre, the integration of combined heat and power (CHP) units, which supply to the greenhouse heating needs while reducing CO₂ emissions through enriched air injection. Germany’s proximity to major Central European markets also enhances its logistical advantage, with 90% of production distributed within 500 km, minimizing transport emissions.

France Commercial Greenhouse Market Analysis

France is projected to have the fastest growth in the coming years in the European Commercial Greenhouse Market, with a diverse production base spanning vegetables, flowers, and nursery plants. A growing trend is the adoption of peri-urban greenhouse complexes near cities like Lyon and Marseille by reducing food miles and enhancing freshness. Furthermore, the integration of agrivoltaics, such as solar panels above greenhouses, is being piloted in Provence, where dual-use systems generate renewable energy while maintaining 90% of crop yield. These technological advancements are escalating the nation’s growth.

Italy Commercial Greenhouse Market Analysis

Italy's Commercial Greenhouse Market growth is driven by a strong regional concentration in the southern regions of Puglia, Sicily, and Sardinia. Italy hosts over 26,000 hectares of plastic and glass greenhouses, which produce 1.8 million tons of vegetables annually, including the EU’s off-season eggplants, leading to 33.76 thousand metric tons in 2023. Moreover, the rise of protected Denominazione di Origine Protetta (DOP) greenhouse tomatoes, such as “Pomodoro di Pachino,” has created premium market niches by fetching prices 30–50% higher than conventional varieties. EU rural development funds have allocated millions of euros to modernize southern greenhouse infrastructure, which accelerates technological adoption.

COMPETITIVE LANDSCAPE

The competitive landscape of the Europe Commercial Greenhouse Market is characterized by technological differentiation, regional spe, and strategic consolidation among key players. The dominant firms leverage deep expertise in automation, climate control, and data analytics, cs which provide integrated solutions that enhance yield efficiency and sustainability. Competition is intensifying as companies strive to deliver energy-smart systems amid rising regulatory and cost pressures. While Dutch and German firms maintain a technological edge, the mid-sized innovators from Belgium, Denmark, and France are gaining ground through niche automation tools and AI-driven platforms. The market is witnessing increased collaboration between equipment providers, energy utilities, and agricultural cooperatives to create closed-loop greenhouse ecosystems. Entry barriers remain high due to capital intensity and technical complexity, which favors established players with robust R&D capabilities and extensive service networks across multiple European countries.

KEY MARKET PLAYERS

These are the top players in the commercial greenhouse market.

- Richel Group SA (France)

- Ridder Group

- HortiMaX

- Priva

- Certhon (U.S.)

- Argus Control Systems Ltd. (U.S.)

- Logiqs (The Netherlands)

- Lumigrow (U.S.)

- Keder Greenhouse (U.K.)

- Agra Tech, Inc (U.S.)

- Hort Americas, LLC (U.S.)

- Rough Brothers Inc. (U.S.)

- Heliospectra AB (Sweden)

Top Players In The Market

- Ridder Group, headquartered in the Netherlands, is a leading innovator in integrated greenhouse technologies, which provides advanced climate control, irrigation,n and automation systems. The company plays a significant role in enhancing operational efficiency across European greenhouse farms by delivering data-driven solutions that optimize energy use and crop yield. In recent years, Ridder has intensified its focus on AI-powered decision support tools by launching its Orchid platform in early 2023 to enable optimization of the climate in greenhouses. The company expanded its service network into Eastern Europe and strengthened partnerships with research institutions like Wageningen University to co-develop adaptive control algorithms. Although primarily rooted in Europe, Ridder has extended its technological footprint to the Asia-Pacific region through pilot projects in South Korea and Japan, where high-tech greenhouse adoption is accelerating.

- Priva, a Dutch pioneer in greenhouse automation,n has established itself as significant in smart horticulture through its integrated control systems that synchronize irrigation, climate, and energy management. The company’s Priva Connext platform enables seamless data integration across greenhouse operations by supporting sustainable production in over 100 countries. In Europe, Priva’s systems are deployed in high-efficiency glasshouse clusters, particularly in the Netherlands and Germany. In 2023, the company launched Priva Greenhouse Monitor, a cloud-based analytics tool that leverages machine learning to predict crop stress and optimize resource use. Priva has also deepened its presence in the Asia-Pacific market by partnering with Australian vertical farming startup Agrifyx to deploy energy-efficient climate controls in urban farms. These rising initiatives reflect Priva’s commitment to global scalability and innovation in controlled environment agriculture.

- HortiMaX, based in Belgium, is a key enabler of digital transformation in European greenhouse farming, which specializes in automation and software solutions for climate, irrigation, and lighting control. The company’s HortiMaX Grow platform integrates sensor networks and AI-driven analytics to enhance crop predictability and reduce energy waste. The company has also expanded its R&D collaborations with universities in Flanders to refine AI models for pest detection and yield forecasting. While its core operations remain in Europe, HortiMaX has extended its influence to the Asia-Pacific region through technology licensing agreements with greenhouse operators in China and India. In recent times, it supported the deployment of a smart greenhouse complex in various agricultural areas by integrating its control systems with local renewable energy grids, marking a strategic foothold in emerging agritech markets.

Top Strategies Used by the Key Market Participants

Key players in the Europe Commercial Greenhouse Market are deploying strategic initiatives to integrate their technological growth and expand market reach. Major strategies include product innovation through AI and IoT integration, geographic expansion into high-growth regions, strategic partnerships with research institutions, mergers and acquisitions to enhance innovation in the innovation portfolio, and investment in sustainable technologies such as energy recovery and water recycling systems. Companies are increasingly adopting platform-based business models, which are providing subscription-driven software services for climate monitoring and predictive analytics. Collaborative ecosystem development, which links equipment providers, energy suppliers, and growers, is gaining traction to improve system interoperability. The firms are focusing on modular, scalable solutions to cater to both large-scale commercial farms and emerging urban agriculture ventures by ensuring adaptability across diverse operational environments.

RECENT MARKET NEWS

- In June 2023, Priva partnered with Wageningen University & Research to co-develop predictive crop modeling tools that integrate weather forecasting and plant physiology data by enhancing the accuracy of its Connext control systems and reinforcing its position in data-driven greenhouse automation.

- In February 2024, Priva introduced EnergyPilot, an advanced energy management system that uses machine learning to optimize heating schedules in northern European greenhouses by reducing operational costs and aligning with EU decarbonization targets.

- In January 2024, Ridder Group expanded its service network into Central Europe’s horticulture sector, establishing local technical support hubs to accelerate the adoption of its automation systems.

MARKET SEGMENTATION

This research report on the Europe commercial greenhouse market is segmented and sub-segmented into the following categories.

By Equipment

- Heating Systems

- Cooling Systems

- Others

By Type

- Glass Greenhouse

- Plastic Greenhouse

- Others

By Crop Type

- Fruits and Vegetables

- Flowers and Ornamentals

- Nursery Crops

- Others Crops

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

Frequently Asked Questions

Why are commercial greenhouses gaining popularity in Europe?

Climate variability and a demand for local produce are making controlled-environment agriculture more attractive for growers.

What advantages do commercial greenhouses offer farmers?

They provide steady yields and minimize risk from weather, offering producers greater certainty throughout the seasons.

Which European countries are actively expanding greenhouse farming?

Countries like the Netherlands and Spain are using advanced systems to increase efficiency and crop diversity.

What new technologies are shaping greenhouse operations today?

Automated irrigation, energy-efficient lighting, and sensor-driven climate controls are helping growers optimize production.

What challenges do greenhouse businesses face in Europe?

Initial investment costs, skilled labor shortages, and sustainable energy sourcing remain key obstacles to fast expansion.

How do greenhouses support sustainability goals?

Greenhouses use less land, conserve water, and enable local food supply chains, which reduces emissions and resource waste.

What types of crops are most commonly produced commercially?

Tomatoes, leafy greens, peppers, and cut flowers are popular choices due to their steady year-round demand.

How do regulations impact commercial greenhouse operations?

Policies supporting eco-friendly farms and innovation grants encourage adoption while quality standards shape market access.

Is energy consumption a growing concern for greenhouse owners?

With rising utility costs, many are shifting to renewable energy sources like solar and geothermal to stay competitive.

What does the future look like for commercial greenhouses in Europe?

Growth is set to accelerate as urban agriculture, tech-driven solutions, and consumer demand for fresh local food increase.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com