Europe Distributed Energy Generation Market Size, Share, Trends, & Growth Forecast Report By Technology (CWind Turbine, Solar Photovoltaic, Reciprocating Engine, Fuel Cells, Gas & Steam Turbine) and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Distributed Energy Generation Market Size

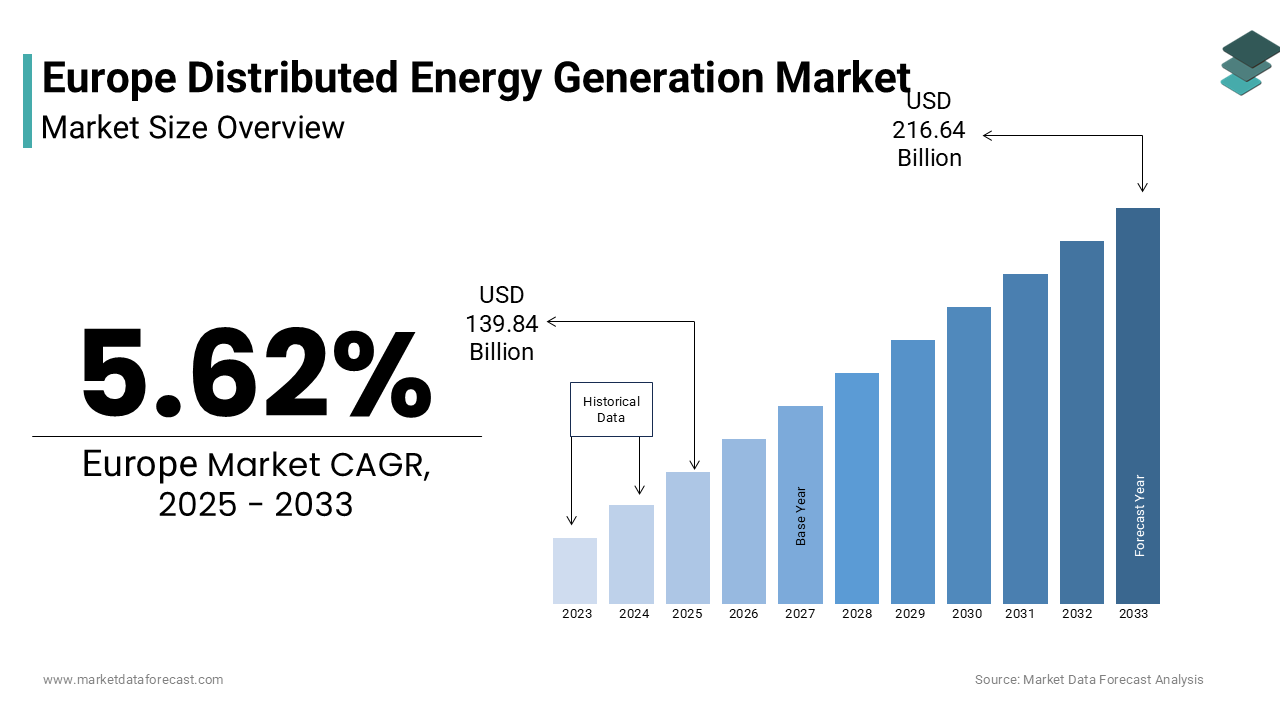

The europe distributed energy generation market size was valued at USD 132.39 billion in 2024 and is anticipated to reach USD 139.84 billion in 2025 from USD 216.64 billion by 2033, growing at a CAGR of 5.62% during the forecast period from 2025 to 2033.

Distributed energy generation refers to the deployment of small to medium scale power systems located close to end users, including rooftop solar photovoltaics micro wind turbines combined heat and power units and small scale biomass installations, that feed electricity directly into local distribution networks or operate in islanded mode. Unlike centralized utility scale plants this model enhances grid resilience reduces transmission losses and empowers consumers to become prosumers. As per sources, A significant trend is the push toward integrating renewable energy sources directly within public, commercial, and residential buildings. Several directives and acts facilitate this shift. For example, EU mandates require all new public and commercial buildings to include on-site renewable generation where feasible. Furthermore, national building codes across the EU are increasingly incorporating mandatory solar provisions for new residential construction.

MARKET DRIVERS

EU Policy Mandates Driving Building Integrated Renewable Deployment

Stringent regulatory requirements under the revised Energy Performance of Buildings Directive are compelling widespread adoption of distributed generation across residential and commercial sectors, which propels the growth of the Europe distributed energy generation market. As per research, European regulations and national laws are driving the adoption of renewable energy sources in new and existing buildings across the continent. New constructions must meet nearly zero energy standards, and a significant portion of their energy needs must come from on-site or nearby renewable sources. Specific mandates in countries like Germany and France require a majority of heat demand to be covered by renewables and large commercial rooftops to feature solar panels or green roofs. These binding national transpositions of EU directives create non-discretionary demand that transcends market price signals and ensures structural growth in distributed generation irrespective of short-term economic fluctuations.

Rising Electricity Prices and Energy Security Concerns Post Geopolitical Disruption

Sustained high retail electricity prices and heightened consumer desire for energy autonomy following the 2022 energy crisis further boost the expansion of the Europe distributed energy generation market. As per research, household electricity tariffs in the eurozone have reached unprecedented levels, which is making payback periods for rooftop solar shorter in Southern Europe. The European Consumer Organisation notes that 68 percent of homeowners in Spain and Italy now cite “protection from price volatility” as the primary reason for installing solar plus storage systems. Consumer interest is high, particularly in Spain and Italy, where a primary motivator for homeowners installing solar-plus-storage systems is protection from price volatility. This convergence of economic incentive and strategic necessity has transformed distributed generation from an environmental choice into a household resilience imperative.

MARKET RESTRAINTS

Grid Interconnection Delays and Capacity Constraints

Chronic barriers in grid connection processes and insufficient distribution network capacity restrain the growth of the Europe distributed energy generation market. Grid operators across the European Union face significant challenges connecting new energy projects, leading to lengthy delays. In various member states, the average time to interconnect distributed generators often exceeds 18 months, resulting in substantial backlogs of queued capacity. National regulators have been slow to mandate dynamic grid access or invest in smart inverters that enable voltage and frequency ride through. The potential of distributed generation will remain stranded, affecting both climate targets and consumer investment confidence, until accelerated grid modernization and streamlined permitting occur.

Lack of Harmonized Net Metering and Remuneration Frameworks

The absence of a unified and stable compensation mechanism for exported surplus electricity across the region discourages investment, which obstructs the expansion of the Europe distributed energy generation market. The regulatory unpredictability increases payback uncertainty especially for apartment dwellers and small businesses reliant on export revenue. Until the EU enforces minimum remuneration standards or mandates time of use pricing aligned with grid value distributed generation will remain economically viable only in high insolation self consumption scenarios.

MARKET OPPORTUNITIES

Expansion of Renewable Energy Communities Under EU Clean Energy Package

The EU’s Clean Energy for All Europeans Package has opened a major opportunity for the growth of the Europe distributed energy generation market. This is through the legal recognition of renewable energy communities that enable collective ownership and local sharing of distributed generation. The entities allow citizens municipalities and small enterprises to jointly invest in solar or wind assets and distribute power within a defined locality without requiring full utility licensing. This participatory model democratizes energy access and aligns decarbonization with social equity objectives, due to dedicated funding from the EU's Just Transition Fund and Innovation Fund.

Integration of Digital Platforms for Virtual Power Plant Aggregation

The region is witnessing rapid growth in virtual power plant platforms that provide fresh prospects for the expansion of the Europe distributed energy generation market. These platforms aggregate distributed energy resources into dispatchable grid assets using cloud-based coordination and smart inverters. Companies use machine learning to forecast generation and optimize bidding into intraday and frequency regulation markets. The EU’s Electricity Market Design reform emphasizes that distribution system operators facilitate third party access to real time grid data enabling smaller aggregators to compete. This digital layer transforms passive rooftop systems into active grid resources creating new revenue streams and enhancing system flexibility without new infrastructure.

MARKET CHALLENGES

Inadequate Financing Mechanisms for Low Income and Multi Family Housing

It remains inaccessible to a significant portion of the region’s population due to upfront capital barriers and regulatory exclusion of non single family dwellings, which challenges the growth of the Europe distributed energy generation market. National programs like France’s MaPrimeRénov exclude photovoltaics from basic renovation grants unless paired with heat pumps. This systemic financing gap perpetuates energy poverty and excludes vulnerable populations from the energy transition, contradicting the principle of a just and inclusive decarbonization enshrined in the European Green Deal.

Cybersecurity Vulnerabilities in Digitally Connected Distributed Assets

The proliferation of smart inverters IoT enabled meters and remote monitoring systems in distributed energy networks has introduced significant cybersecurity risks that threaten grid stability and consumer data privacy. This inhibits the expansion of the Europe distributed energy generation market. Most residential inverters lack mandatory security certification and use default passwords or unencrypted communication protocols vulnerable to spoofing. The EU’s Cyber Resilience Act will require baseline security standards for connected energy devices from 2027 but legacy installations remain unprotected. The digitalization of distributed generation risks creating a fragmented and exploitable attack surface in Europe’s evolving energy landscape unless enforceable cybersecurity protocols and regular firmware update mandates are established

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Technology and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | United Kingdom (UK), France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Engie SA, Maxeon Solar Technologies Ltd., EDF Renewables, Compagnie de Saint-Gobain S.A., WAGNER Solar GmbH, Sunverge Energy, Bloom Energy, Canadian Solar Inc., and Ansaldo Energia SpA. |

SEGMENTAL ANALYSIS

By Technology Insights

In 2024, solar photovoltaic segment dominated the Europe distributed energy generation market by accounting for a 64.3% share. The dominance of the solar photovoltaic segment is driven by dramatic cost reductions and seamless integration into urban and rural building fabrics. National building codes reinforce this trend with some countries requiring solar thermal or photovoltaic on all new residential buildings and Italy enforcing it for structures over 500 square meters. Apart from these, the EU’s Right to Self Consume regulation prohibits discriminatory grid fees for small scale generators enabling fair compensation. Rooftop solar’s modularity scalability and silent operation allow deployment in dense urban environments where wind or thermal systems face zoning barriers. This regulatory tailwind combined with consumer appeal ensures photovoltaic remains the backbone of Europe’s decentralized energy transition.

The fuel cells segment is estimated to register the fastest CAGR of 28.4% from 2025 to 2033 due toits role in clean baseload power and hydrogen ecosystem integration. These systems achieve notable total efficiency by capturing waste heat for space and water heating. The European Commission’s Net Zero Industry Act designates fuel cells as a strategic technology eligible for state aid and fast tracked permitting. Companies are scaling production of polymer electrolyte membrane fuel cells using green hydrogen from local electrolyzers creating closed loop microgrids. Hence, fuel cells are transitioning from niche to mainstream in high value distributed applications.

REGIONAL ANALYSIS

Germany Distributed Energy Generation Market Analysis

Germany led the Europe distributed energy generation market by capturing a 26.4% share in 2024. The prominence of the German market is propelled by its decades long Energiewende policy and robust prosumer framework. ermany is experiencing significant growth in solar power adoption, driven by supportive government policies. The number of photovoltaic systems is increasing, with the majority installed on residential rooftops. Recent amendments to the Renewable Energy Sources Act, which removed the solar tax and simplified grid connection for smaller systems, have accelerated this trend. Homeowners are increasingly pairing their solar installations with battery storage units, allowing for high levels of energy self-consumption. Municipal utilities operate virtual power plants aggregating distributed assets to provide grid balancing services. Germany’s consistent policy signaling stable remuneration and technical standards has created a mature ecosystem where distributed generation is not just viable but expected infrastructure in new and retrofitted buildings.

Spain Distributed Energy Generation Market Analysis

Spain was the next-biggest player in the Europe distributed energy generation market and held a 19.4% share in 2024 by leveraging its exceptional solar resource and progressive regulatory reforms. The country receives significant hours of sunshine annually enabling residential photovoltaic payback periods below five years. Regions offer additional grants covering up to aportion of system costs. Spain’s focus on energy justice and solar democratization has transformed distributed generation from a luxury into a widespread household asset particularly in rural areas where grid reliability is lower.

Italy Distributed Energy Generation Market Analysis

Italy is moving ahead steadfastly in the Europe distributed energy generation market due to powerful fiscal incentives and construction linked mandates. ENEL and local cooperatives have launched “solar condominium” programs enabling apartment dwellers to share roof systems with proportional billing. Southern regions benefit from high irradiation and aging grid infrastructure making distributed solar both economical and resilient. Italy’s blend of financial engineering and regulatory obligation ensures sustained deployment even amid macroeconomic uncertainty.

France Distributed Energy Generation Market Analysis

France is likely to expand in the Europe distributed energy generation market from 2025 to 2033 owing to its emphasis on collective and urban distributed generation models. The Autoconsommation Collective framework enables multi unit buildings and industrial parks to share locally generated power without third party tariffs. France’s approach prioritizes density and equity ensuring distributed generation thrives not only in rural areas but in metropolitan centers where land is scarce and energy demand is highest.

Netherlands Distributed Energy Generation Market Analysis

The Netherlands is another key player in the Europe distributed energy generation market through advanced grid integration and digital aggregation. Grid operator Tennet has pioneered dynamic grid access allowing real time curtailment instead of interconnection denial easing pressure on aging infrastructure. The Dutch Authority for Consumers and Markets mandates transparent time of use tariffs enabling households to optimize self consumption and export. Companies facilitate peer to peer solar trading within neighborhoods using blockchain ledgers.

COMPETITVE LANDSCAPE

The Europe distributed energy generation market features a dynamic mix of global engineering firms specialized inverter manufacturers and integrated energy service providers. Competition is driven by technological sophistication regulatory compliance and service innovation rather than price alone. German and Dutch companies lead in power electronics and grid integration software while French and Italian firms excel in community scale deployment and policy aligned financing. The market is highly fragmented with thousands of local installers but dominated at the technology layer by a few key players who set interoperability and safety standards. Regulatory divergence across member states creates both complexity and opportunity as companies tailor solutions to national net metering grid access and building code requirements. Strategic partnerships with distribution system operators and participation in EU funded pilot projects are critical for validation and scale. Ultimately the competitive edge lies in delivering not just hardware but holistic prosumer ecosystems that combine generation storage control and digital services into seamless experiences.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Distributed Energy Generation Market include

- Engie SA

- Maxeon Solar Technologies Ltd.

- EDF Renewables

- Compagnie de Saint-Gobain S.A

- WAGNER Solar GmbH

- Sunverge Energy

- Bloom Energy

- Canadian Solar Inc.

- Ansaldo Energia SpA

Top Players in the Europe Distributed Energy Generation Market

Siemens Energy

Siemens Energy is a leading provider of integrated distributed energy solutions across Europe offering smart inverters microgrid controllers and hybrid power systems for industrial and municipal applications. The company combines digital grid software with hardware to enable seamless integration of solar wind and storage assets into local networks. Recently Siemens Energy launched its Spectrum Power Microgrid Management System in Germany and Spain enabling real time optimization of distributed resources for hospitals and data centers. It also partnered with European utilities to deploy grid forming inverters that enhance stability in high renewable penetration zones. Through its global engineering footprint Siemens Energy exports European developed microgrid architectures to emerging markets in Africa and Southeast Asia reinforcing its role as a technology standard setter in decentralized energy systems.

ENGIE

ENGIE is a major European energy transition player actively deploying distributed generation through decentralized solar microgrids and renewable energy communities. The company operates over 1 500 decentralized assets across France Belgium and the Netherlands serving industrial parks campuses and social housing complexes. ENGIE recently launched its “Decentralized Energy as a Service” model allowing clients to adopt solar and storage with zero upfront investment while retaining operational control. ENGIE also supports EU renewable energy community frameworks by providing legal technical and financing infrastructure to citizen cooperatives. Its integrated approach bridges utility scale expertise with local energy democracy accelerating adoption across urban and rural landscapes.

SMA Solar Technology

SMA Solar Technology is a German innovator specializing in photovoltaic inverters and energy management systems that form the backbone of Europe’s distributed generation infrastructure. Its Sunny Tripower and Sunny Boy series are widely deployed in residential and commercial solar installations across the continent. SMA recently introduced AI enhanced forecasting in its Energy Management System enabling dynamic self consumption optimization and grid support functions compliant with EU grid codes. The company also developed hybrid inverters compatible with both lithium and emerging solid state batteries ensuring future proofing for prosumers. SMA supplies its technology globally with European safety and interoperability standards often serving as the benchmark for international markets. Its commitment to open communication protocols and cybersecurity certification strengthens trust among installers and grid operators alike

Top Strategies Used by the Key Market Participants

Key players in the Europe distributed energy generation market are developing smart inverters and energy management systems that comply with evolving EU grid codes for voltage and frequency support. They are offering energy as a service models to eliminate upfront costs and accelerate adoption among residential and small commercial users. Companies are forming partnerships with municipalities and housing associations to deploy community scale solar and storage projects under renewable energy community frameworks. They are integrating artificial intelligence for predictive self consumption optimization and virtual power plant participation. Additionally they are designing modular and interoperable systems that support future upgrades to green hydrogen fuel cells and bidirectional electric vehicle charging to ensure long term asset relevance

MARKET SEGMENTATION

The research report on the Europe Distributed Energy Generation Market has been segmented and sub-segmented based on categories.

By Technology

- Wind Turbine

- Solar Photovoltaic

- Reciprocating Engine

- Fuel Cells

- Gas & Steam Turbine

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe distributed energy generation market?

It represents the production of electricity from small-scale, decentralized energy sources located near the point of consumption across Europe.

What technologies are included in distributed energy generation?

Technologies include solar PV, wind turbines, fuel cells, microturbines, CHP systems, biomass, small hydro, and battery energy storage.

What factors are driving market growth in Europe?

Growth is driven by renewable energy targets, decentralization policies, grid modernization, falling solar prices, and energy security concerns.

How does the EU’s energy policy impact distributed energy generation?

EU initiatives like the Green Deal and Fit-for-55 mandate higher renewable penetration, supporting decentralized generation investments.

Which segment dominates the Europe distributed energy generation market?

Solar PV dominates due to widespread adoption in residential, commercial, and industrial applications.

Which countries are leading the market?

Germany, France, the UK, and the Netherlands lead due to strong renewable adoption, incentives, and supportive policies.

What challenges affect market expansion?

Challenges include high initial investment cost, permitting delays, intermittency issues, grid connection barriers, and regulatory complexity.

Who are the major players in the Europe distributed energy generation market?

Major players include Engie SA, Maxeon Solar Technologies Ltd., EDF Renewables, Saint-Gobain S.A., WAGNER Solar GmbH, Sunverge Energy, Bloom Energy, Canadian Solar Inc., and Ansaldo Energia SpA.

What applications use distributed energy generation systems?

Applications include residential rooftop solar, commercial microgrids, industrial CHP units, rural electrification, and backup power systems.

What emerging technologies will shape the future of distributed generation?

Green hydrogen, advanced batteries, peer-to-peer energy trading, microgrid systems, and virtual power plants (VPPs) will play major roles.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com