Europe Electronic Health Records Software Market Size, Share, Trends & Growth Forecast Report, Segmented By Product, Type, End-User, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Electronic Health Records Software Market Report Summary

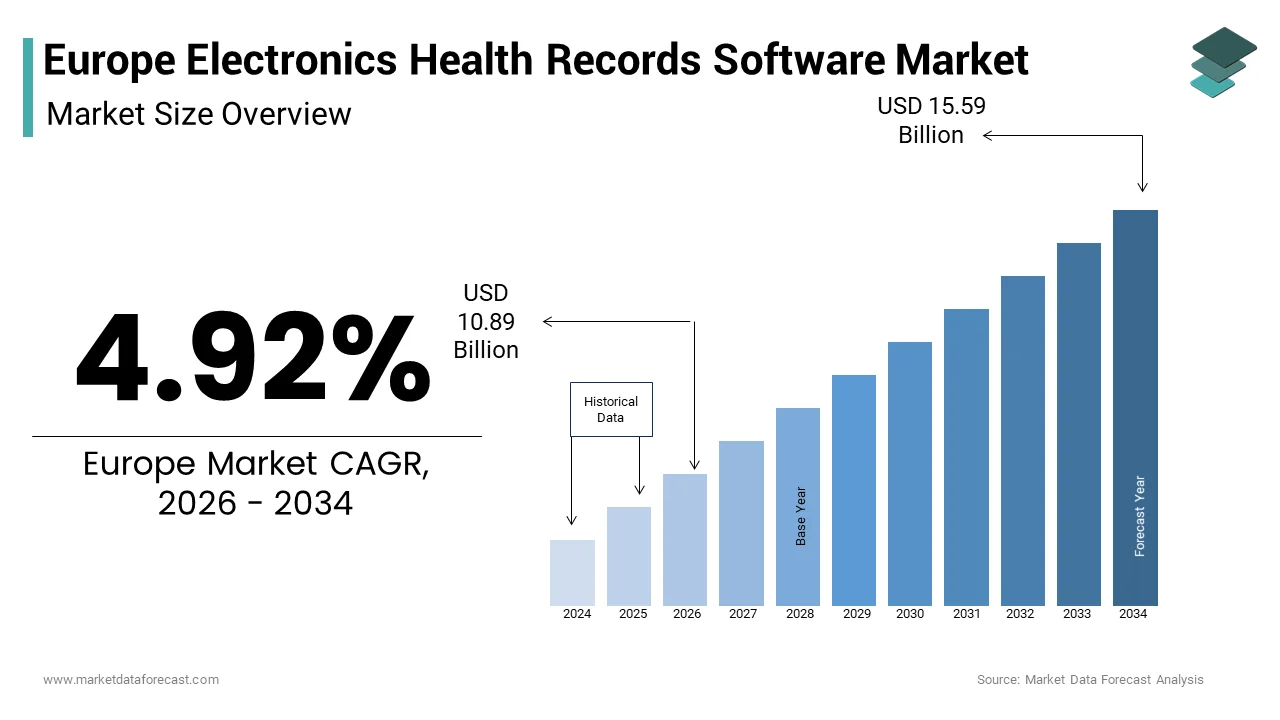

The Europe electronic health records software market was valued at USD 10.38 billion in 2025, is estimated to reach USD 10.89 billion in 2026, and is projected to reach USD 15.59 billion by 2034, growing at a CAGR of 4.92% during the forecast period from 2026 to 2034. The growth of the Europe electronic health records software market is driven by increasing digitalization of healthcare systems, rising demand for efficient patient data management, and supportive government initiatives promoting e-health adoption. The growing need for interoperability, improved clinical outcomes, and streamlined healthcare workflows is further fueling market growth. Additionally, advancements in cloud-based solutions and data analytics technologies are accelerating the adoption of EHR systems across healthcare providers in Europe.

Key Market Trends

- Increasing adoption of web-based and cloud-based EHR solutions for enhanced accessibility and scalability.

- Growing demand for integrated EHR systems enabling seamless data sharing across healthcare networks.

- Rising focus on interoperability and standardized health data exchange across European countries.

- Expansion of digital healthcare infrastructure supported by government initiatives and policies.

- Integration of AI and analytics tools to improve clinical decision-making and patient outcomes.

Segmental Insights

- Based on product, the web-based segment dominated the Europe electronic health records software market by accounting for 60.5% of the market share in 2025. The segment’s dominance is attributed to its flexibility, cost-effectiveness, and ease of access across multiple healthcare settings.

- Based on type, the integrated segment held a substantial share of the Europe electronic health records software market in 2025, driven by its ability to combine multiple healthcare functions into a unified system.

- Based on end user, the hospitals segment was the largest, accounting for 55.6% of the Europe electronic health records software market share in 2025. The growth is driven by the high volume of patient data and the need for efficient record management in hospital settings.

Regional Insights

The Europe electronic health records software market is witnessing steady growth across major countries, supported by digital health transformation initiatives. Germany led the market, accounting for 22.4% of the Europe electronic health records software market share in 2025, driven by strong healthcare infrastructure and adoption of digital solutions. The United Kingdom ranked second with 18.3% share, supported by advanced healthcare IT systems and government support. France holds a noteworthy share due to its centralized health data systems, while Italy is progressing steadily with its regionalized healthcare structure. The Netherlands is expected to expand significantly during the forecast period, driven by increasing investments in healthcare digitization.

Competitive Landscape

The Europe electronic health records software market is highly competitive, with key players focusing on innovation, interoperability, and cloud-based solutions to strengthen their market presence. Companies are investing in advanced technologies such as AI, data analytics, and integrated platforms to enhance healthcare delivery and patient management. Strategic collaborations, mergers, and product developments are common strategies adopted by market participants. Prominent players in the Europe electronic health records software market include Epic Systems Corporation, Veradigm LLC, Oracle, Dedalus, InterSystems, eClinicalWorks, athenahealth, NextGen Healthcare, Medical Information Technology Inc., and Kareo Inc., among others.

Europe Electronic Health Records Software Market Size

The Europe electronic health records software market size was valued at USD 10.38 billion in 2025 and is anticipated to reach USD 10.89 billion in 2026 to reach USD 15.59 billion by 2034, growing at a CAGR of 4.92% during the forecast period from 2026 to 2034.

Europe Electronic Health Records Software Market Overview

Electronic Health Records (EHR) software is a digital platform that stores a patient's comprehensive medical history, including diagnoses, medications, test results, and notes, in a secure, real-time format. These systems replace traditional paper-based records enabling healthcare providers to access comprehensive patient histories laboratory results medication lists and treatment plans instantaneously. The primary objective is to enhance clinical decision making improve patient safety and streamline administrative workflows across hospitals clinics and private practices. According to the European Commission approximately 95% of general practitioners in the European Union utilize electronic health records indicating a high baseline of digital adoption within primary care settings. However the level of sophistication and interoperability varies significantly across member states. As per the Digital Decade 2025: eHealth Indicator Study, the EU has reached a composite eHealth maturity score of 83%; however, significant gaps remain in institutional connectivity, with only 26% of Member States reporting that a majority (60%+) of their hospitals and primary care facilities are actively supplying comprehensive data to national access services. The transition towards integrated care models necessitates that these systems communicate seamlessly with other health information technologies such as ePrescribing and telemedicine platforms. Regulatory initiatives like the European Health Data Space aim to facilitate cross border data exchange ensuring that patient information follows the individual regardless of location. This legislative push underscores the strategic importance of interoperable electronic health records in creating a resilient and efficient healthcare ecosystem. The market is thus characterized by a shift from basic digitization to advanced analytics and patient centric data sharing frameworks.

MARKET DRIVERS

Government mandates and funding for digital health infrastructure

Strong government mandates and substantial financial investments in digital health infrastructure drive the growth of the Europe electronic health records software market. National governments recognize that digitization is essential for sustaining healthcare systems amidst aging populations and rising chronic disease prevalence. According to the European Commission the Digital Europe Programme has allocated significant funds specifically for the deployment of health data spaces and digital services infrastructure. This financial support lowers the barrier to entry for healthcare providers who might otherwise struggle with the high upfront costs of software implementation. As per the OECD's 2025 Digital Health report, while adoption is rising, only 55% of surveyed countries have reached a unified national EHR standard, with the organization urging member states to move beyond "strategies" into detailed accountability and follow-up structures. For instance countries like Denmark and Estonia have achieved near universal coverage through centralized government led initiatives. These policies often include incentives for physicians and hospitals to transition from paper to digital systems. The regulatory pressure ensures compliance with data standards which facilitates interoperability between different healthcare entities. Furthermore public procurement processes increasingly favor vendors who offer compliant and secure solutions. The alignment of national health policies with European Union directives creates a cohesive environment for market growth. Healthcare providers are compelled to upgrade their systems to meet these regulatory requirements ensuring continued demand for advanced electronic health records software. This top down approach accelerates market penetration and standardizes care delivery protocols across the region.

Increasing prevalence of chronic diseases requiring coordinated care

The rising prevalence of chronic diseases such as diabetes, cardiovascular conditions, and respiratory disorders propels the demand for sophisticated EHR software capable of supporting coordinated care, and thereby fuels the expansion of the Europe electronic health records software market. Chronic conditions require long term management and frequent monitoring involving multiple specialists and healthcare facilities. According to the WHO European Health Report 2025, noncommunicable diseases now account for 90% of all deaths in the region, with 1 in 6 people dying before the age of 70 from these conditions. Electronic health records enable seamless sharing of patient data among primary care physicians specialists and hospitals ensuring that all providers have access to up to date information. As emphasized in current digital healthcare research, the integration of Clinical Decision Support Systems (CDSS) into patient data flows is essential for evaluating real-world adherence to best practice standards and improving long-term health outcomes. This continuity of care reduces the risk of medical errors duplicate testing and adverse drug interactions. Healthcare providers rely on these systems to generate alerts for preventive screenings and medication adjustments. The ability to analyze population health data helps in identifying high risk patients and implementing early interventions. Consequently hospitals and clinics are investing in electronic health records software that offers robust chronic disease management modules. The focus on value based care models further incentivizes the use of data driven insights to improve patient health while controlling costs. This clinical necessity ensures sustained demand for advanced functionalities within electronic health records systems.

MARKET RESTRAINTS

High implementation and maintenance costs for healthcare providers

The substantial financial burden associated with implementing and maintaining EHR software is a significant restraint to the Europe electronic health records software market. This is particularly true for smaller healthcare practices and rural hospitals. The initial investment includes not only software licensing fees but also hardware upgrades network infrastructure improvements and staff training. According to analysis by Deloitte's European Healthcare Outlook, many small and medium-sized healthcare providers operate on tight margins, identifying the cost of technology as one of the top four barriers to digital transformation. As emphasized in longitudinal studies on EHR ownership costs, the total cost of ownership for electronic health records can be prohibitive, often exceeding initial acquisition costs by up to 200% when including ongoing maintenance and technical support. Smaller clinics often lack the economies of scale enjoyed by large hospital networks resulting in higher per user costs. Additionally the need for specialized IT personnel to manage these systems adds to the operational expenditure. Many healthcare organizations face budget constraints due to limited reimbursement rates and increasing operational costs. This financial pressure leads to delays in adoption or the selection of less comprehensive software solutions that may not fully meet clinical needs. The return on investment is often realized over a long period which discourages immediate adoption. Consequently financial limitations restrict the market potential among a significant segment of healthcare providers. The widespread deployment of advanced electronic health records remains challenging for resource-constrained entities. This challenge is due to a lack of adequate financial support or subsidies.

Interoperability issues and fragmented health information systems

Persistent interoperability challenges and the fragmentation of health information systems across different regions and institutions hinder the effective utilization of EHR software, which hampers the expansion of the Europe electronic health records software market. Despite technological advancements many existing systems operate in silos using proprietary data formats that do not communicate seamlessly with other platforms. According to the European Health Management Association the lack of standardized data exchange protocols prevents the smooth flow of patient information between primary care providers hospitals and laboratories. As per the European Commission varying levels of digital maturity among member states result in incompatible systems that complicate cross border healthcare delivery. Healthcare providers often struggle to integrate new electronic health records software with legacy systems leading to data duplication and inefficiencies. The absence of universal standards for coding and terminology further exacerbates the problem making it difficult to aggregate and analyze data accurately. Clinicians may find themselves unable to access critical patient history from external sources compromising the quality of care. This fragmentation limits the potential benefits of electronic health records such as comprehensive patient views and coordinated care planning. Vendors face difficulties in developing solutions that can interface with the diverse array of existing systems in the European market. Until robust interoperability frameworks are universally adopted and enforced the full potential of electronic health records will remain unrealized. This technical barrier slows down market growth and frustrates end users.

MARKET OPPORTUNITIES

Integration of artificial intelligence and predictive analytics

The integration of artificial intelligence and predictive analytics into EHR software offers a significant opportunity for enhancing clinical decision support and operational efficiency, which is likely to boost the growth of the Europe electronic health records software market. AI algorithms can analyze vast amounts of patient data to identify patterns predict disease outbreaks and recommend personalized treatment plans. According to the European Society of Radiology the application of machine learning in medical imaging and diagnostics is rapidly expanding offering tools that can assist clinicians in early detection of conditions. Research published in the International Journal of Medical Informatics indicates that predictive analytics embedded within electronic health records can alert providers to patients at high risk of readmission or complications, enabling proactive interventions. This capability improves patient outcomes and reduces healthcare costs by preventing adverse events. Vendors are increasingly incorporating natural language processing to extract structured data from unstructured clinical notes enhancing the completeness of patient records. The ability to automate routine tasks such as coding and billing also reduces administrative burdens on healthcare staff. Healthcare organizations are seeking intelligent systems that provide actionable insights rather than just data storage. The growing availability of large datasets and computing power supports the development of these advanced features. By offering AI driven capabilities software providers can differentiate their products and command premium pricing. This technological evolution aligns with the broader trend towards precision medicine and value based care. The potential for improved diagnostic accuracy and operational efficiency drives interest in next generation electronic health records solutions.

Expansion of patient portals and remote monitoring capabilities

The expansion of patient portals and remote monitoring capabilities within EHR software paves the way for empowering patients and improving engagement. This expansion is expected to accelerate the expansion of the Europe electronic health records software market. Modern healthcare consumers expect easy access to their health information and the ability to communicate with providers digitally. According to the European Patient Forum patient involvement in healthcare decisions leads to better adherence to treatment plans and improved health outcomes. As per the European Commission the MyHealth@EU initiative aims to enable citizens to access their health data across borders fostering trust and transparency. Electronic health records software that includes robust patient portal features allows individuals to view test results schedule appointments and request prescription refills online. The integration of Internet of Things devices enables the continuous monitoring of vital signs such as blood pressure and glucose levels which can be automatically synced to the electronic health record. This real time data flow supports telemedicine consultations and chronic disease management from home. Healthcare providers benefit from reduced office visits and more timely interventions. The shift towards patient centric care models drives demand for software that facilitates bidirectional communication. Vendors who prioritize user friendly interfaces and mobile accessibility can capture a larger share of the market. The growing emphasis on preventive care and wellness further supports the adoption of these features. Electronic health records software serves as a central hub for holistic care delivery. It enables patients to take an active role in their health management.

MARKET CHALLENGES

Data privacy concerns and stringent regulatory compliance

Stringent data privacy regulations and the complexity of compliance requirements are a major challenge for the Europe electronic health records software market. The General Data Protection Regulation imposes strict rules on the collection processing and storage of personal health data requiring robust security measures and explicit patient consent. According to the European Data Protection Board healthcare data is considered special category data warranting the highest level of protection against breaches and unauthorized access. As per the European Union Agency for Cybersecurity healthcare organizations are frequent targets of cyberattacks making data security a critical concern for software vendors and providers alike. Compliance with GDPR requires significant investment in encryption access controls and audit trails which increases the cost and complexity of software development. Any data breach can result in severe financial penalties and reputational damage discouraging some providers from fully embracing cloud based solutions. The varying interpretation of regulations across different member states adds another layer of complexity for multinational vendors. Healthcare providers must ensure that their electronic health records systems are fully compliant with local and international laws. The need for continuous monitoring and updating of security protocols diverts resources from innovation and feature development. Patients growing awareness of privacy rights also leads to hesitation in sharing sensitive health information digitally. Balancing the need for data accessibility with rigorous privacy protection remains a persistent challenge. This regulatory landscape requires vendors to maintain high standards of governance and transparency.

Resistance to change and lack of digital literacy among staff

Resistance to change and insufficient digital literacy among healthcare professionals are serious barriers to the successful adoption and utilization of EHR software, and the expansion of the Europe electronic health records software market. Many clinicians and administrative staff are accustomed to traditional paper based workflows and may perceive digital systems as cumbersome or time consuming. According to reports by the OECD (and supported by health IT literature), the digital transformation of healthcare often creates a "transition phase" where inadequate digital skills training leads to temporary productivity dips and increased burden on health workers. As per extensive research by the American Medical Association (AMA), physicians report that bureaucratic burdens, specifically excessive EHR documentation requirements, are a leading contributor to burnout and significantly reduce face-to-face time with patients. The steep learning curve associated with complex software interfaces can deter older or less tech savvy staff from fully engaging with the system. Lack of user friendly design and poor usability further exacerbate this resistance. Healthcare organizations often underestimate the importance of change management and comprehensive training programs. Without adequate support staff may revert to workarounds that compromise data integrity and safety. The cultural shift towards digital first processes requires strong leadership and ongoing education. Vendor support plays a crucial role but cannot replace internal organizational commitment. The shortage of IT skilled personnel in healthcare settings also hinders effective system management. Overcoming these human factors is essential for realizing the benefits of electronic health records. Until staff feel confident and comfortable with the technology adoption rates may stagnate. This behavioral barrier requires targeted interventions and sustained effort.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | % |

| Segments Covered | By Product, Type, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

| Market Leaders Profiled | Epic Systems Corporation (U.S.), Veradigm LLC (U.S.), Oracle (U.S.), Dedalus, InterSystems, eClinicalWorks (U.S.), Athenahealth (U.S.), NextGen Healthcare (U.S.), Medical Information Technology, Inc. (U.S.), Kareo, Inc. (U.S.) |

SEGMENTAL ANALYSIS

By Product Insights

The web based segment dominated the Europe electronic health records software market and accounted for a 60.5% share in 2025. This dominance of the segment is driven by the increasing preference for cloud hosted solutions that offer accessibility scalability and reduced infrastructure costs for healthcare providers across the continent. The main driver for the dominance of web based electronic health records is the enhanced accessibility they provide which is crucial for modern healthcare delivery models including telemedicine and remote patient monitoring. Healthcare professionals require access to patient data from various locations including clinics homes and hospitals to ensure continuity of care. According to Eurostat and the European Commission, while the availability of digital health policies has reached a majority of EU Member States, actual adoption varies, with teleconsultations representing a minority share of total medical consultations in most nations. Web based systems enable seamless access to electronic health records via internet connected devices without the need for complex local installations. As noted in digital health market reports, remote access to health information is credited with improving response times and facilitating better coordination among multidisciplinary teams. This flexibility is particularly valuable in rural areas where specialist care may be limited. Physicians can review patient histories and update records in real time regardless of their physical location. The ability to support mobile health applications further extends the reach of these systems. Patients also benefit from easier access to their own health information through patient portals. The shift towards value based care requires continuous monitoring and data sharing which web based platforms facilitate effectively. Consequently healthcare organizations are prioritizing web based solutions to support flexible and responsive care delivery. This trend ensures that web based electronic health records remain the preferred choice for modern healthcare institutions. The lower total cost of ownership and superior scalability associated with web based electronic health records software significantly contribute to its market domination. Traditional on premise systems require substantial upfront investment in hardware servers and IT infrastructure as well as ongoing maintenance costs. Web based solutions typically operate on a subscription model which converts capital expenditure into predictable operational expenditure. The financial advantage makes advanced electronic health records accessible to a broader range of healthcare providers. The scalability of web based platforms allows organizations to easily add users or storage capacity as their needs grow without significant additional investment. Software updates and security patches are managed by the vendor ensuring that systems remain current without burdening internal IT staff. This reduces the need for specialized technical personnel which is often scarce in healthcare settings. The automatic backup and disaster recovery features provided by cloud vendors enhance data security and business continuity. These economic and operational benefits drive the widespread adoption of web based electronic health records. Healthcare providers can focus resources on patient care rather than IT management. This value proposition sustains the leading position of the web based segment in the market.

The web based segment is also the fastest growing segment in the Europe electronic health records software market with an anticipated CAGR of 12.5%during the forecast period. This rapid growth of the segment is fueled by the accelerating digital transformation in healthcare and the increasing demand for interoperable and flexible data solutions. The accelerating pace of digital transformation in the European healthcare sector is a primary catalyst for the rapid growth of web based electronic health records. Governments and healthcare organizations are increasingly recognizing the strategic importance of cloud computing in enabling efficient and connected care. According to the European Commission's Digital Decade policy, the adoption of cloud services in the public sector, including healthcare, is targeted for substantial growth to enhance service delivery and efficiency. Web based electronic health records are central to this transformation as they facilitate data sharing and integration with other digital health tools. As per research, the healthcare and life sciences sector is projected to be one of the fastest growing areas for cloud-based integration and Generative AI adoption to support scalable data management. The ability to integrate with artificial intelligence and big data analytics platforms enhances the clinical value of electronic health records. Web based systems provide the necessary infrastructure for these advanced applications. The shift towards centralized health data spaces as promoted by the European Union further supports the migration to cloud based solutions. Healthcare providers are moving away from siloed on premise systems to interconnected web based platforms. This transition enables better population health management and research capabilities. The ease of deployment and rapid time to value offered by web based solutions appeals to healthcare organizations seeking quick improvements in efficiency. The continuous innovation in cloud security and compliance also alleviates concerns about data privacy. These factors collectively drive the sustained high growth of the web based segment. The strong emphasis on interoperability and cross border data exchange initiatives in Europe is significantly accelerating the adoption of web based electronic health records. The European Health Data Space aims to enable the secure sharing of health data across member states requiring systems that are inherently connected and standardized. Web based electronic health records allow for seamless integration with national health information exchanges and other healthcare providers. This connectivity is essential for patients who travel or seek care in different countries. The ability to aggregate data from multiple sources provides a more comprehensive view of patient health. Web based systems support the use of standard protocols such as Fast Healthcare Interoperability Resources which are critical for interoperability. Healthcare organizations are increasingly mandated to participate in these networks driving the replacement of legacy on premise systems. The collaborative nature of web based platforms fosters innovation and the development of new health applications. This regulatory and strategic push ensures that web based electronic health records will continue to grow at a rapid pace. The alignment with European digital health strategies solidifies the growth trajectory of this segment.

By Type Insights

The integrated segment led the Europe electronic health records software market and captured a substantial share in 2025. This leading position of the segment is attributed to the need for comprehensive solutions that combine clinical administrative and financial functions into a single unified platform. A key driver for the dominance of the integrated segment is the significant improvement in workflow efficiency and data consistency it offers to healthcare providers. Integrated electronic health records systems eliminate the need for multiple disparate systems by combining patient records billing scheduling and laboratory results in one interface. The consolidation of data ensures that all departments have access to the same up to date information reducing the risk of discrepancies and improving decision making. Clinicians can view a complete patient history including medications allergies and previous treatments without switching between applications. This holistic view supports better clinical outcomes and patient safety. Integrated systems also streamline billing processes by automatically capturing chargeable services during documentation. This integration reduces claim denials and accelerates revenue cycles. The ability to generate comprehensive reports for regulatory compliance and quality improvement is another key benefit. Healthcare organizations prefer integrated solutions because they simplify IT management and reduce training requirements for staff. The seamless flow of information across departments enhances overall operational efficiency. This comprehensive approach aligns with the goals of modern healthcare delivery. Consequently integrated electronic health records remain the preferred choice for most healthcare institutions in Europe. The superior interoperability and ease of system integration offered by integrated electronic health records software significantly contribute to its leading market position. Modern healthcare environments rely on a variety of technologies including laboratory information systems radiology information systems and pharmacy management systems. Integrated electronic health records are designed to communicate seamlessly with these ancillary systems through standardized interfaces. These systems enable the automatic transfer of test results orders and prescriptions reducing delays and improving care coordination. The ability to integrate with wearable devices and remote monitoring tools further extends the functionality of integrated electronic health records. Healthcare providers can incorporate real time patient generated data into clinical workflows. This connectivity supports proactive care management and chronic disease monitoring. Integrated systems also support third party applications and extensions allowing organizations to customize their solutions. The open architecture of many integrated platforms encourages innovation and collaboration with technology partners. Healthcare organizations value the ability to create a connected ecosystem that supports diverse clinical needs. This flexibility and connectivity make integrated electronic health records indispensable for modern healthcare delivery. The strategic importance of interoperability ensures the continued dominance of this segment.

The integrated segment is also estimated to register the fastest CAGR of 13.2% from 2026 to 2034 due to the increasing complexity of healthcare operations and the demand for holistic patient management solutions. Moreover, the growing demand for holistic patient management solutions is a primary accelerator for the swift expansion of this segment. Healthcare providers are shifting towards value based care models that require a comprehensive view of patient health across multiple dimensions. Integrated electronic health records support this by combining clinical data with social determinants of health and lifestyle information. This comprehensive approach allows for personalized care plans and better health outcomes. The ability to track patient progress over time and across different care settings is essential for effective population health management. Integrated systems facilitate collaboration among primary care physicians specialists and social workers. This multidisciplinary approach is increasingly recognized as vital for addressing complex health needs. Healthcare organizations are investing in integrated solutions to improve care continuity and reduce fragmentation. The demand for patient centric care drives the adoption of systems that support comprehensive data aggregation. Integrated platforms enable the identification of care gaps and opportunities for intervention. This strategic shift towards holistic care ensures sustained growth for the integrated segment. The ability to deliver coordinated and efficient care is a competitive advantage for healthcare providers. The regulatory push for standardized data reporting and quality measurement is accelerating the adoption of integrated electronic health records in Europe. Governments and healthcare authorities are increasingly requiring detailed data on clinical outcomes resource utilization and patient satisfaction. Integrated systems ensure that data is captured consistently and accurately reducing the burden on healthcare staff. The ability to generate real time dashboards and reports supports evidence based decision making. Regulatory frameworks such as the General Data Protection Regulation also require robust data governance which integrated systems facilitate through centralized control. Healthcare organizations must demonstrate compliance with various quality indicators and safety standards. Integrated electronic health records provide the necessary tools for monitoring and improving performance. The alignment with national and European health strategies drives the replacement of standalone systems with integrated platforms. The focus on transparency and accountability in healthcare delivery further supports this trend. Integrated solutions enable healthcare providers to meet regulatory requirements efficiently. This compliance driven demand ensures that the integrated segment continues to grow rapidly. The strategic importance of data quality and reporting solidifies the growth trajectory.

By End-User Insights

In 2025, the hospitals segment was the largest segment in the Europe electronic health records software market and occupied a 55.6% share. This supremacy of the segment is credited to the large scale of hospital operations the complexity of care provided and the significant regulatory requirements they face. The complex operational needs and large patient volumes handled by hospitals are the primary drivers for their dominance in the electronic health records market. Hospitals manage a wide range of services including emergency care surgery intensive care and outpatient clinics requiring robust and comprehensive software solutions. According to the European Hospital and Healthcare Federation (HOPE), while digital technologies should be an integral part of health and care, the full-scale deployment of new digital care models requires more solid clinical data to prove their effectiveness, as initial evidence of benefits for patients and systems remains limited. As per the World Health Organization, integrated health services should be people-centred and organized around the comprehensive needs of individuals throughout their life course, with primary care and essential public health functions serving as the core of the system rather than relying solely on hospital-based models. Electronic health records enable hospitals to streamline workflows reduce wait times and improve patient throughput. The ability to manage complex medication regimes and treatment plans is critical for patient safety in hospital settings. Hospitals also face stringent regulatory requirements for data retention and reporting which electronic health records facilitate. The scale of hospital operations necessitates systems that can handle high transaction volumes and concurrent users. Integrated electronic health records support resource management including bed allocation and staff scheduling. The need for real time access to patient information is crucial in emergency situations. Hospitals invest heavily in advanced electronic health records to support their mission of providing high quality care. The complexity of hospital environments makes them the largest consumers of sophisticated health IT solutions. This operational necessity ensures the continued leadership of the hospital segment. Significant government funding and infrastructure investment in hospital digitalization significantly contribute to the leading position of the hospitals segment. European governments recognize hospitals as critical nodes in the healthcare system and prioritize their digital transformation. According to the European Investment Bank billions of euros have been allocated for modernizing healthcare infrastructure including the implementation of electronic health records in hospitals. As per the European Commission initiatives such as the Recovery and Resilience Facility provide specific funds for digital health projects in public hospitals. This financial support enables hospitals to acquire advanced software and hardware without bearing the full cost. Public hospitals are often mandated to adopt standardized electronic health records systems to ensure interoperability and data sharing. The scale of these investments drives substantial demand for enterprise level electronic health records solutions. Hospitals use these funds to upgrade legacy systems and implement new technologies such as artificial intelligence and predictive analytics. The focus on improving hospital efficiency and patient outcomes guides these investments. Government programs often include training and support components to ensure successful adoption. The strategic importance of hospital digitalization for national health security further reinforces this trend. Hospitals are able to leverage these resources to implement comprehensive and scalable solutions. This sustained financial backing ensures that hospitals remain the largest end user segment in the market. The alignment with public health goals drives continuous investment in hospital IT infrastructure.

The physician offices segment is anticipated to witness the fastest CAGR of 14.8% over the forecast period owing to the increasing number of private practices the availability of affordable cloud based solutions and the shift towards ambulatory care. In addition, the strategic shift towards ambulatory and primary care settings is a primary driver for the rapid growth of the physician offices segment. Healthcare systems in Europe are increasingly focusing on preventing hospital admissions by strengthening primary care services. WHO and OECD policy frameworks emphasize strengthening primary care to deliver services "closer to home," a shift intended to manage aging populations and reduce unnecessary hospitalizations. As per the Organisation for Economic Co operation and Development primary care plays a pivotal role in managing chronic diseases and coordinating patient journeys. Physician offices are adopting electronic health records to manage this increasing workload efficiently. Cloud based solutions have made it affordable for small practices to implement sophisticated systems. The ability to share data with hospitals and specialists improves care coordination and reduces duplication of tests. Patients prefer the convenience of primary care visits which drives demand for efficient office based services. Electronic health records enable physicians to provide personalized and timely care. The integration with patient portals enhances engagement and adherence to treatment plans. Government incentives for digital adoption in primary care further accelerate this trend. Physician offices are recognizing the competitive advantage of offering digital services. The focus on value based care rewards preventive measures and effective management which electronic health records support. This structural shift in healthcare delivery ensures sustained growth for the physician offices segment. The decentralization of care drives the demand for accessible and user friendly software. Furthermore, the availability of affordable and user friendly electronic health records solutions tailored for small practices is accelerating adoption in the physician offices segment. Historically high costs and complexity hindered adoption among smaller providers but the rise of software as a service models has changed this landscape. Market analysis indicates that Cloud-based Electronic Health Records (EHRs) lower barriers to entry for independent physicians by offering subscription-based pricing models with minimal upfront infrastructure costs. Studies published in journals such as JAMIA or reports by KLAS Research demonstrate that improved EHR usability and intuitive interface designs are significantly associated with reduced cognitive load and higher physician satisfaction. Modern solutions require less IT support and can be implemented quickly. The mobility of web based systems allows physicians to access records from tablets and smartphones enhancing flexibility. Automated features such as voice recognition and template customization save time during consultations. Vendor support and training programs are often included in subscription packages reducing the burden on practice staff. The ability to scale features according to practice size allows for cost effective growth. Physician offices are increasingly aware of the benefits of digitization for billing and compliance. The competitive market for electronic health records vendors has led to improved product quality and lower prices. This accessibility removes traditional barriers to entry. The positive user experience encourages wider adoption and retention. These factors collectively drive the rapid growth of the physician offices segment. The democratization of health IT empowers small practices to compete effectively.

COUNTRY LEVEL ANALYSIS

Germany Electronic Health Records Software Market Analysis

Germany was the top performer in the Europe electronic health records software market and accounted for a 22.4% share in 2025. The country’s dominance is supported by its large healthcare economy strong technological infrastructure and recent legislative pushes for digital health adoption. Moreover, the German healthcare system is one of the largest in Europe with significant spending on health information technology. According to the Federal Ministry of Health, the legislative shift to an "opt-out" system under the Digital Act has become the primary driver for the mass adoption of electronic patient records (ePA), addressing the stagnation observed under the previous voluntary model. This secure network connects healthcare providers and enables the exchange of patient data. As per the DigitalRadar consortium (commissioned by the Ministry of Health), German hospitals have exhibited a low average level of digital maturity, prompting the implementation of the Hospital Future Act to fund the digitization of patient records and infrastructure. The recent mandate for the electronic patient record for insured individuals has accelerated adoption among physician offices and specialists. The strong presence of domestic software vendors and international players fosters a competitive market. Germany’s focus on data sovereignty and security influences the selection of electronic health records solutions. The country’s robust industrial base supports the development of advanced health IT innovations. The aging population increases the demand for efficient care management tools. Government funding programs support the digitalization of small and medium sized practices. The integration of electronic health records with statutory health insurance systems enhances their utility. The cultural emphasis on precision and quality drives the demand for reliable and comprehensive software. The ongoing expansion of the telematics infrastructure ensures continued market growth. These factors collectively sustain Germany’s position as the largest market for electronic health records in Europe. The strategic importance of digital health in national policy ensures long term investment.

United Kingdom Electronic Health Records Software Market Analysis

The United Kingdom was the second largest country in the Europe electronic health records software market and captured a 18.3% share in 2025. This growth of the UK market is propelled by its centralized National Health Service and long standing commitment to digital health initiatives. The UK has been a pioneer in electronic health records adoption through the National Health Service which serves the majority of the population. According to NHS Digital general practitioner practices in the UK have achieved near universal adoption of electronic health records systems. This high baseline creates a mature market focused on upgrades and interoperability. As per NHS England, the NHS Long Term Plan emphasizes the use of digital tools to improve patient outcomes and efficiency, mandating compliance with digital standards across the health service. The integration of secondary care systems with primary care records is a key priority driving demand for integrated solutions. The presence of major global electronic health records vendors in the UK ensures a wide range of choices. The regulatory framework supports data sharing while maintaining strict privacy standards. The focus on reducing waiting times and improving access to care drives innovation in digital health. The UK market is characterized by large scale procurement contracts which influence vendor strategies. The emphasis on population health management requires robust data analytics capabilities. The devolved health systems in Scotland Wales and Northern Ireland also contribute to market diversity. The strong digital literacy among healthcare professionals supports effective utilization. The continuous evolution of NHS digital strategies ensures sustained demand. These elements maintain the UK’s strong position in the European market. The legacy of early adoption provides a foundation for advanced applications.

France Electronic Health Records Software Market Analysis

France holds a noteworthy share of the Europe electronic health records software market due to its centralized health data agency and ongoing efforts to standardize electronic health records across the nation. Also, the French healthcare system is undergoing significant digital transformation driven by the Agency for Digital Health. According to the French Ministry of Solidarity and Health the deployment of the shared medical record has been a key initiative to improve care coordination. As per the Agence du Numérique en Santé (ANS), the adoption of electronic health records in hospitals is widespread but remains fragmented, with current efforts focused on enforcing interoperability standards to unify the system. The government is pushing for greater interoperability between private practitioners and public hospitals. The Mon Espace Santé platform aims to provide every citizen with a secure digital health space. This initiative drives demand for compliant and interconnected electronic health records software. The strong regulatory environment ensures high standards for data security and privacy. France has a mix of public and private healthcare providers creating diverse market needs. The focus on reducing administrative burdens through digitization is a key driver. The presence of local and international vendors fosters competition and innovation. The aging population and prevalence of chronic diseases increase the need for efficient data management. Government incentives support the adoption of digital tools in private practices. The strategic plan for digital health outlines clear targets for adoption and usage. These factors support the continued growth of the market in France. The emphasis on patient empowerment through digital access drives innovation.

Italy Electronic Health Records Software Market Analysis

Italy is moving ahead steadfastly in the Europe electronic health records software market owing to its regionalized healthcare system and increasing investments in digital health infrastructure following recent national reforms. Moreover, the Italian healthcare system is decentralized with regions responsible for implementation leading to varied levels of electronic health records adoption. According to the Italian Ministry of Health the National Recovery and Resilience Plan includes significant funding for the digitalization of healthcare services. As per the National Agency for Regional Health Services efforts are underway to harmonize electronic health records across regions. The creation of a national electronic health record repository is a key priority. This initiative drives demand for standardized and interoperable software solutions. The prevalence of small private practices is increasing the demand for affordable cloud based systems. The government is promoting the use of digital prescriptions and referrals which require integrated electronic health records. The focus on improving efficiency and reducing waste drives adoption. The cultural shift towards digital health is gaining momentum among healthcare professionals. The presence of both domestic and international vendors offers a range of solutions. The regulatory framework is evolving to support data sharing and privacy. The need to manage an aging population and chronic diseases supports market growth. The investment in telemedicine and remote monitoring also boosts demand for electronic health records. These dynamics contribute to the steady growth of the market in Italy. The push for national standardization ensures long term potential.

Netherlands Electronic Health Records Software Market Analysis

The Netherlands is likely to expand significantly in the Europe electronic health records software market from 2026 to 2034 due to its high level of digital maturity strong interoperability standards and patient centric approach to health data. Also, the Netherlands is a leader in health IT adoption in Europe with widespread use of electronic health records in both primary and secondary care. According to the Dutch Ministry of Health, Welfare and Sport, the national infrastructure for health information exchange is currently fragmented, with ongoing reforms aiming to replace decentralized systems with a sustainable, integrated national network. As per Nictiz, the national center of expertise for eHealth, technical standards for information exchange have been developed, but actual implementation remains inconsistent, hindering true interoperability between healthcare providers. This high level of interoperability drives demand for compliant and connected software solutions. The strong emphasis on patient privacy and data security influences vendor selection. The Netherlands has a high density of general practitioners who are early adopters of digital tools. The focus on integrated care networks requires robust electronic health records systems. The government supports innovation through funding and policy initiatives. The presence of specialized health IT vendors fosters a competitive market. The high digital literacy among patients and providers supports effective utilization. The shift towards value based care drives the need for data analytics and reporting. The collaborative culture in Dutch healthcare encourages the sharing of best practices. The continuous improvement of digital infrastructure ensures market growth. These factors position the Netherlands as a key player in the European market. The advanced state of digital health provides a model for other countries.

COMPETITIVE LANDSCAPE

The competition in the Europe electronic health records software market is characterized by a mix of large global technology corporations and specialized regional vendors who compete on functionality interoperability and local expertise. Global players leverage their extensive resources and broad product suites to offer comprehensive solutions that integrate with various health IT systems. Regional vendors differentiate themselves through deep understanding of local regulatory requirements and healthcare workflows providing tailored solutions that meet specific national standards. The market sees intense rivalry in areas such as cloud migration services data analytics capabilities and user interface design. Interoperability remains a key competitive factor as healthcare organizations seek systems that can seamlessly exchange data with other platforms. Price competition is moderate as customers prioritize quality reliability and compliance over initial cost. Strategic collaborations with hardware providers and consulting firms are common to deliver end to end digital health solutions. The threat of new entrants is mitigated by high switching costs and complex implementation processes. Regulatory compliance serves as a significant barrier to entry favoring established players with proven track records. The market is consolidating as larger companies acquire smaller innovators to enhance their technological capabilities. This dynamic environment drives continuous improvement and benefits healthcare providers through enhanced features and services.

KEY MARKET PLAYERS

A few of the market players that are in the Europe electronic health records software market are

- Epic Systems Corporation (U.S.)

- Veradigm LLC (U.S.)

- Oracle (U.S.)

- Dedalus

- InterSystems

- eClinicalWorks (U.S.)

- Athenahealth (U.S.)

- NextGen Healthcare (U.S.)

- Medical Information Technology, Inc. (U.S.)

- Kareo, Inc. (U.S.)

Top Players In The Market

- Oracle is a significant player in the Europe electronic health records software market through its Cerner division which provides comprehensive health information technology solutions. The company contributes to the global market by offering integrated platforms that connect clinical financial and operational data for healthcare organizations. Oracle has strengthened its market position by leveraging its cloud infrastructure to enhance the scalability and security of Cerner systems. Recent actions include the migration of legacy systems to Oracle Cloud Infrastructure ensuring better performance and data accessibility for European hospitals. The company focuses on interoperability standards to facilitate seamless data exchange across different healthcare settings. Oracle invests heavily in artificial intelligence capabilities to support clinical decision making and predictive analytics. Their commitment to open standards allows for easier integration with third party applications and medical devices. By combining robust database technology with specialized healthcare expertise Oracle delivers reliable and secure solutions. The company actively collaborates with government bodies to support national digital health initiatives. This strategic alignment with regulatory requirements enhances their appeal to public sector clients. Oracle continues to innovate in population health management tools helping providers improve patient outcomes. Their global reach and local presence ensure consistent service delivery across European markets.

- Dedalus is a leading European provider of healthcare software solutions with a strong footprint in the electronic health records market across the continent. The company contributes to the global market by offering tailored solutions that address the specific regulatory and operational needs of diverse healthcare systems. Dedalus has strengthened its market position through a series of strategic acquisitions that expand its product portfolio and geographic reach. Recent actions include the integration of acquired companies to create unified platforms that offer end to end digital health services. The company focuses on interoperability and data analytics to enable connected care pathways for patients and providers. Dedalus invests in research and development to incorporate artificial intelligence and machine learning into its electronic health records systems. Their solutions support both acute and community care settings ensuring comprehensive coverage of healthcare needs. The company actively participates in European digital health initiatives promoting standardization and cross border data exchange. Dedalus emphasizes user experience and clinical workflow optimization to enhance adoption among healthcare professionals. Their localized support teams provide personalized assistance ensuring successful implementation and ongoing maintenance. By focusing on innovation and customer centricity Dedalus maintains a competitive edge in the European market. The company’s commitment to digital transformation supports the modernization of healthcare infrastructure across Europe.

- InterSystems is a prominent provider of data management and interoperability solutions for the healthcare industry with a significant presence in the Europe electronic health records market. The company contributes to the global market by offering robust data platforms that enable seamless information exchange between disparate systems. InterSystems has strengthened its market position by focusing on high performance data infrastructure that supports complex clinical workflows. Recent actions include the enhancement of their HealthShare platform to improve care coordination and population health management capabilities. The company leverages its expertise in database technology to ensure fast and reliable access to critical patient information. InterSystems prioritizes interoperability standards such as Fast Healthcare Interoperability Resources to facilitate connectivity with other health IT systems. Their solutions are widely used by hospitals and health networks to integrate electronic health records with laboratory and radiology systems. The company invests in artificial intelligence and analytics tools to derive actionable insights from clinical data. InterSystems collaborates with partners to develop specialized applications for specific medical specialties and care settings. Their focus on data security and compliance aligns with stringent European regulatory requirements. By providing a flexible and scalable foundation for digital health InterSystems supports the evolution of healthcare delivery. The company’s reputation for reliability and innovation makes it a trusted partner for healthcare organizations.

Top Strategies Used By The Key Market Participants

Key players in the Europe electronic health records software market primarily focus on enhancing interoperability and data exchange capabilities to meet regulatory requirements and improve care coordination. Companies are increasingly adopting cloud based deployment models to offer scalable and cost effective solutions that reduce the burden on internal IT resources. Strategic acquisitions and partnerships are common strategies used to expand product portfolios and enter new geographic markets within Europe. Vendors are investing heavily in artificial intelligence and machine learning technologies to provide advanced clinical decision support and predictive analytics features. Emphasis on user experience and workflow optimization is crucial to drive adoption and satisfaction among healthcare professionals. Compliance with data privacy regulations such as GDPR is a central strategy to build trust and ensure legal operation in the European market. Providers are also developing modular and flexible platforms that allow healthcare organizations to customize solutions according to their specific needs. Continuous innovation in security features protects sensitive patient data from cyber threats. These strategies collectively enable companies to maintain competitive advantages and deliver value to healthcare providers.

MARKET SEGMENTATION

This research report on the Europe electronic health records software market is segmented and sub-segmented into the following categories.

By Product

- Web-based

- On-premise

By Type

- Standalone

- Integrated

By End-User

- Physician Offices

- Hospitals

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe EHR software market?

Increasing digitalization of healthcare systems and need for efficient patient data management is driving growth.

Why are healthcare providers in Europe adopting EHR software?

They use it to improve patient care, data accuracy, and operational efficiency.

How would you explain EHR software in simple terms?

It is digital software used to store and manage patient health records.

Where is EHR software most commonly used across Europe?

It is widely used in hospitals, clinics, and healthcare institutions.

What makes EHR systems important for modern healthcare?

They enable easy access to patient data and support better clinical decisions.

From a healthcare perspective, is EHR software a worthwhile investment?

Yes, it improves efficiency and enhances quality of care.

What challenges are affecting the Europe EHR software market?

Data security concerns and high implementation costs are key challenges.

How is government support influencing EHR adoption in Europe?

Policies and digital health initiatives are encouraging system implementation.

Which healthcare segments contribute the most to EHR demand?

Hospitals and large healthcare networks are the primary contributors.

Is the Europe EHR software market growing steadily?

Yes, it is expanding with increasing adoption of digital health solutions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com