Europe Embedded Systems Market Size, Share, Trends & Growth Forecast Report By Component, By Application, and By Country (Germany, France, United Kingdom, Italy, Sweden & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Embedded Systems Market Size

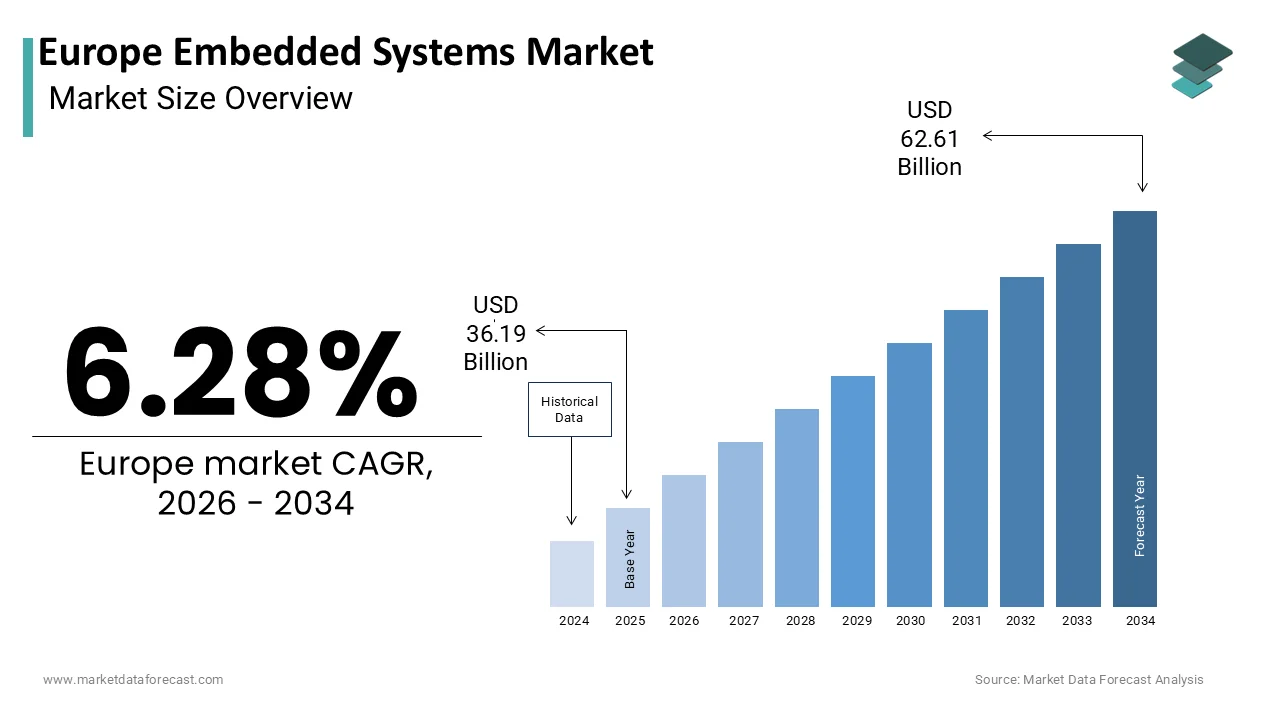

The Europe embedded system market was valued at USD 36.19 billion in 2025, is estimated to reach USD 38.46 billion in 2026, and is projected to reach USD 62.61 billion by 2034, growing at a CAGR of 6.28% from 2026 to 2034.

An embedded system refers to a specialized computing platform engineered to perform dedicated functions within larger mechanical or electrical systems, commonly found in automotive electronics, industrial automation, medical devices, and consumer appliances. In Europe, embedded systems serve as foundational enablers of digital transformation across critical sectors, integrating real-time processing, connectivity, and control logic into compact hardware architectures. The European Union’s strategic emphasis on smart manufacturing, green mobility, and resilient healthcare infrastructure has intensified reliance on embedded technologies. As per Eurostat, a very high proportion of large manufacturing enterprises in the EU now integrate embedded software into their production processes, which reflects the deep digitalization of industrial operations. Additionally, according to the European Environment Agency, most new passenger vehicles registered in the European Economic Area incorporate multiple embedded control units that manage functions ranging from engine performance to advanced driver assistance. These systems are increasingly converging with artificial intelligence and edge computing paradigms, reinforcing their role in enabling responsive, secure, and energy-efficient operations across the continent’s industrial and societal frameworks.

MARKET DRIVERS

Proliferation of Industrial Automation and Smart Manufacturing

The expansion of industrial automation across European manufacturing hubs is majorly propelling the growth of the European embedded system market. Embedded controllers and programmable logic devices form the operational backbone of automated production lines, robotics, and condition monitoring systems. As per the European Commission’s Digital Economy and Society Index, a large proportion of EU manufacturers have implemented advanced automation solutions that rely on embedded real-time operating systems. According to the International Federation of Robotics, Germany alone accounted for a very high number of industrial robots in active operation, each requiring multiple embedded subsystems for motion control, vision processing, and safety compliance. The push toward Industry 4.0 has further embedded intelligence into machinery, with the European Manufacturing Leadership Council noting that a majority of EU-based factories now deploy edge-embedded devices for predictive maintenance and process optimization. This automation surge is not limited to automotive or machinery sectors; food and beverage, pharmaceuticals, and electronics assembly lines increasingly integrate embedded sensors and microcontrollers to meet stringent quality and traceability standards mandated under EU regulations.

Integration of Embedded Systems in Next Generation Automotive Platforms

Europe’s automotive sector remains a dominant catalyst for the European embedded system market due to the regulatory mandates and consumer demand for connected and electrified mobility. Modern vehicles now incorporate a large number of embedded electronic control units on average, managing everything from battery thermal regulation in electric vehicles to over-the-air software updates, as stated by the European Automobile Manufacturers Association. The EU’s General Safety Regulation requires all new vehicle types to include embedded systems for intelligent speed assistance, driver drowsiness detection, and emergency stop assistance. As per the European Transport Safety Council, these mandates are projected to significantly increase embedded hardware content per vehicle in the coming years. Furthermore, the shift toward software-defined vehicles has intensified reliance on high-performance embedded architectures capable of supporting AUTOSAR-compliant middleware and secure boot mechanisms. Volkswagen Group reported that its next-generation electric platforms will feature centralized embedded compute modules replacing dozens of legacy distributed units, which indicates a structural redesign centered on embedded integration.

MARKET RESTRAINTS

Persistent Shortages and Geopolitical Volatility in Semiconductor Supply Chains

The chronic instability in semiconductor procurement, exacerbated by geopolitical tensions and concentrated global manufacturing capacity,y is majorly hampering the European embedded system market growth. As per the European Semiconductor Industry Association, Europe accounts for a notable share of global semiconductor consumption but produces a relatively small portion of chips. The region’s heavy dependence on Asian foundries leaves embedded system developers vulnerable to export controls and logistical disruptions. According to the European Central Bank, lead times for microcontrollers used in industrial embedded applications remained significantly above historical averages throughout 2023. Although the European Chips Act aims to double regional production by 2030, current investments have yet to translate into scalable domestic capacity for mixed-signal and embedded processor fabrication. As per the Centre for European Policy Studies, export restrictions imposed by the United States on certain semiconductor equipment have indirectly affected European access to critical process technologies. These vulnerabilities compel embedded system integrators to maintain elevated inventory buffers, which increases capital expenditure and delays product development cycles.

Stringent and Fragmented Cybersecurity and Functional Safety Compliance Requirements

Regulatory complexity surrounding cybersecurity and functional safety presents a significant barrier to the European embedded system market expansion. Unlike unified frameworks in other regions, the EU enforces a mosaic of directives, including the Machinery Regulation, Radio Equipment Directive, and the upcoming Cyber Resilience Act, each imposing distinct validation protocols for embedded firmware and hardware. As per the European Union Agency for Cybersecurity, many embedded system vendors reported increased certification costs due to overlapping compliance mandates. The introduction of UNECE Regulation No. 155 requires embedded systems to undergo rigorous cybersecurity management system audits, adding months to time-to-market,t according to the European Association of Automotive Suppliers. In medical devices, adherence to IEC 62304 for software lifecycle management further complicates embedded development, with notified bodies experiencing significant backlogs in conformity assessments as documented by the European Commission’s Medical Devices Coordination Group. These regulatory hurdles disproportionately affect startups and niche developers who lack dedicated compliance teams, thereby stifling innovation and fragmenting the embedded ecosystem across national borders despite the EU’s single market ambitions.

MARKET OPPORTUNITIES

Expansion of Edge AI in Embedded Industrial and Healthcare Applications

The convergence of edge artificial intelligence with embedded platforms is unlocking promising opportunities for the European embedded system market. Unlike cloud-dependent AI models, edge AI embedded systems process data locally, ensuring low latency, enhanced privacy, and operational continuity in bandwidth-constrained environments. As per the Fraunhofer Institute for Intelligent Analysis and Information Systems, a significant proportion of German manufacturing firms piloted edge AI-enabled embedded solutions for real-time defect detection, which is reducing inspection errors. In healthcare, according to the European Society of Radiology, many diagnostic imaging centers in Western Europe deployed embedded AI co-processors in ultrasound and X-ray machines to accelerate preliminary analysis, easing radiologists' workload. The European Innovation Council has allocated substantial funding under Horizon Europe to support startups developing energy-efficient neural processing units for embedded edge AI, which is targeting applications in precision agriculture and remote patient monitoring. These systems align with the EU’s data sovereignty objectives by minimizing cross-border data transfers. As semiconductor vendors such as STMicroelectronics and Infineon introduce dedicated AI accelerators compatible with Arm Cortex cores, the cost and power envelope for intelligent embedded nodes continues to shrink, enabling scalable deployment even in cost-sensitive domains like smart building management and distributed energy resources.

Growth of Sustainable Electronics and Circular Economy Initiatives

Europe’s regulatory and societal push toward sustainable electronics is catalyzing innovation in energy-efficient and recyclable embedded system design, which is another major opportunity in the European embedded system market. The Ecodesign for Sustainable Products Regulation mandates that all electronic products placed on the EU market incorporate design features enabling repairability, upgradeability, and material recovery, which directly influences embedded hardware architecture. As per the European Environmental Bureau, a growing proportion of embedded system developers in regions such as Benelux and the Nordics have initiated redesigns to extend product lifespans well beyond previous averages. This shift is accelerating demand for modular embedded platforms with standardized interfaces, such as PC/104 and SMARC form factors, which facilitate component replacement without full system obsolescence. According to the European Commission’s Raw Materials Initiative, increasing the reuse of critical raw materials from end-of-life electronics could significantly reduce the EU’s dependency on imported rare earths by 2030. Companies like NXP Semiconductors have responded by launching embedded microcontrollers fabricated with recycled content, verified through third-party audits. These developments not only align with the EU Green Deal but also open new service-based business models, including embedded system leasing and take-back programs, which are fostering a circular embedded electronics economy.

MARKET CHALLENGES

Escalating Complexity in Multicore and Heterogeneous Embedded Architectures

The rapid evolution toward multicore and heterogeneous computing in embedded systems is challenging the European embedded system market growth. Modern embedded platforms increasingly integrate combinations of CPU, GPU, FPGA, and neural processing units on a single die to meet performance demands in domains like autonomous machinery and medical imaging. As per the Embedded Systems Institute in the Netherlands, a majority of European embedded software teams reported delays due to difficulties in optimizing task scheduling and memory allocation across heterogeneous cores. The lack of standardized toolchains for cross-architecture development exacerbates this issue. According to the VDE Association for Electrical, Electronic, and Information Technologies, only a small proportion of firms had access to validated middleware supporting seamless data flow between diverse cores and accelerators. Moreover, functional safety certification under standards like IEC 61508 becomes exponentially more complex when multiple execution environments coexist, which requires exhaustive fault injection testing and redundancy validation. This complexity inflates development costs and extends validation timelines, particularly for safety-critical applications in rail and aerospace. Without coordinated European initiatives to establish open reference architectures and interoperable development frameworks, the talent and infrastructure gap will continue to hinder the region’s ability to fully leverage next-generation embedded compute paradigms.

Talent Shortage in Embedded Systems Engineering and Firmware Development

A severe and widening gap in skilled embedded systems engineers is constraining innovation and deployment velocity across Europe, which is further challenging the embedded systems market expansion in Europe. Embedded engineering requires mastery of low-level programming, real-time operating systems, hardware abstraction layers, and a domain-specific protocol, which is a multidisciplinary skill set in critically short supply. As per the European Centre for the Development of Vocational Training, the EU faces a significant deficit of embedded and firmware engineers by 2025, with Germany, France, and Italy accounting for the majority of unmet demand. According to the university enrolment data from the European University Association, only a small proportion of computer engineering graduates specialized in embedded systems in recent years, as students gravitate toward higher visibility fields like web and mobile development. This imbalance is particularly acute in real-time Linux and bare-metal programming, where industry surveys by the German Electrical and Electronic Manufacturers Association indicate that most hiring managers struggle to fill senior firmware roles. The shortage impedes not only product development but also post-deployment support, as legacy embedded systems in infrastructure and industrial equipment require continuous maintenance. Without targeted educational reforms, apprenticeship expansion, and incentives to retain talent within the embedded domain, Europe risks ceding leadership in high-value embedded applications to regions with more robust engineering pipelines.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Component, Application, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Intel Corporation, NXP Semiconductors N.V., Texas Instruments Incorporated, STMicroelectronics N.V., Qualcomm Incorporated, Renesas Electronics Corporation, Infineon Technologies AG, Analog Devices, Inc., Microchip Technology Inc., Fujitsu Limited, ARM Holdings plc, Siemens AG |

SEGMENTAL ANALYSIS

By Component Insights

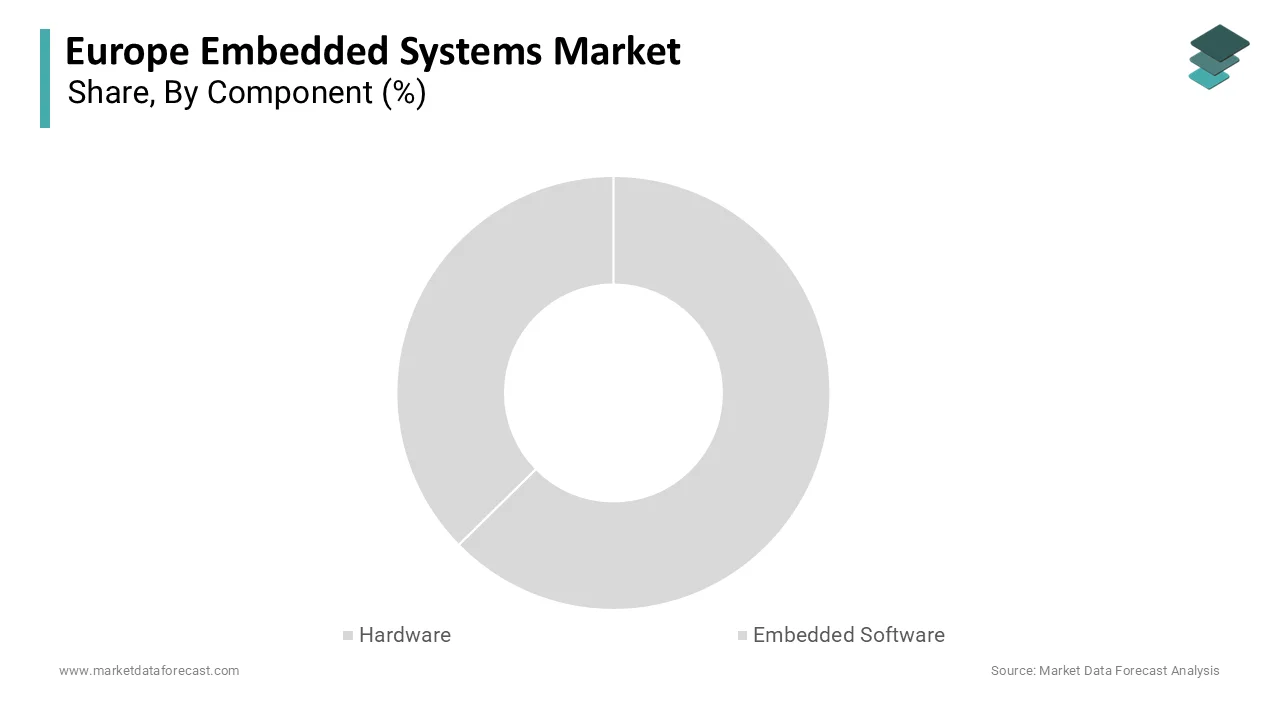

The hardware segment dominated the market by holding61.6% of the European market share in 2025. The leading position of the hardware segment in the European market can be credited to the foundational role of microcontrollers, processors, memory units, and sensors in virtually every embedded deployment across automotive, industrial, and medical domains. The proliferation of electric vehicles and smart factories has intensified demand for high-performance, low-power semiconductor components. According to the European Semiconductor Industry Association, shipments of advanced microcontrollers to European embedded system integrators grew significantly, driven largely by automotive and industrial automation sectors. Additionally, the European Commission’s Chips Act has catalyzed investment in domestic semiconductor packaging and testing infrastructure, reinforcing hardware’s centrality. Legacy systems in energy and transportation infrastructure are also undergoing hardware refresh cycles to meet new cybersecurity and interoperability mandates under the EU Cyber Resilience Act, necessitating the replacement of outdated embedded boards with modern secure elements. These structural and regulatory forces ensure that hardware remains the revenue anchor of the embedded ecosystem despite the rising strategic importance of software.

However, the embedded software segment is on the rise and is estimated to witness the fastest CAGR of 12.2% over the forecast period, owing to the shift toward software-defined functionality in traditionally hardware-bound systems. In the automotive sector, over-the-air update capabilities now require robust real-time operating systems and secure bootloader architectures. As per the European Automobile Manufacturers Association, most new electric vehicle platforms launched in 2024 support full vehicle software updates, necessitating advanced embedded middleware. Concurrently, industrial equipment manufacturers are embedding predictive maintenance algorithms directly into control units, reducing reliance on external analytics platforms. According to the Fraunhofer Institute, a majority of German machinery exporters now deliver embedded analytics software as a standard feature, enhancing product differentiation. Furthermore, the EU’s emphasis on digital sovereignty has spurred demand for locally developed embedded software stacks compliant with GAIA-X data infrastructure principles. These converging trends are transforming embedded software from a support layer into a primary revenue and innovation driver.

By Application Insights

The automotive segment dominated the market by capturing the leading share of 37.7% of the regional market in 2025. The dominance of the automotive segment in the European market is driven by Europe’s position as a global hub for premium vehicle manufacturing and its aggressive regulatory framework for vehicle safety and emissions. Every modern European car integrates dozens of embedded electronic control units managing functions from battery thermal regulation in electric drivetrains to lane-keeping assistance. As per the European Environment Agency, nearly all new passenger cars registered in the EU in 2024 were equipped with advanced driver assistance systems requiring dedicated embedded vision and radar processors. Moreover, the transition to software-defined vehicles has intensified embedded content per vehicle. Volkswagen Group disclosed that its Scalable Systems Platform embeds hundreds of millions of lines of code across centralized compute modules. The EU’s General Safety Regulation mandates embedded systems for emergency stop assistance and driver monitoring, further locking in demand. With automotive OEMs increasingly competing on software features rather than mechanical attributes, embedded systems have become strategic differentiators, which are cementing the sector’s dominance in the regional market.

On the other side, the healthcare segment is the fastest growing in the Europe embedded system market and is anticipated to register a CAGR of 13.3% over the forecast period, owing to the convergence of aging demographics, digital health policy, and miniaturization of diagnostic hardware. As per Eurostat, Europe’s population aged 65 and over is projected to reach 30% by 2030, escalating demand for remote patient monitoring devices that rely on low-power embedded systems for continuous vital sign tracking. The European Commission’s Digital Health Action Plan has allocated billions of euros to support the deployment of connected medical devices in public health systems, accelerating the adoption of embedded electrocardiogram and glucose monitoring platforms. Additionally, regulatory harmonization under the EU Medical Device Regulation has streamlined certification for embedded diagnostics, reducing time to market. Companies like Philips and Siemens Healthineers reported that most of their new portable imaging and infusion systems launched in 2024 feature ARM Cortex-based embedded controllers with integrated cybersecurity modules. These factors are collectively propelling healthcare to the forefront of embedded innovation in Europe.

COUNTRY LEVEL ANALYSIS

Germany Embedded System Market Analysis

Germany dominated the market by holding 25.1% of the European market share in 2025. The dominating position of Germany in the European market is attributed to its dual strength in automotive engineering and industrial machinery, both deeply embedded and intensive sectors. Home to global OEMs like BMW, Mercedes-Benz, and Siemens, Germany has institutionalized embedded system integration through its Industry 4.0 national strategy, which mandates smart factory readiness across the manufacturing base. As per the Federal Ministry for Economic Affairs and Climate Action, a large majority of German manufacturing enterprises with more than 200 employees deployed embedded edge devices for real-time process control in 2024. Furthermore, Germany hosts Europe’s densest cluster of semiconductor design centers, including Infineon and Bosch’s Reutlingen fab, which supplies automotive-grade microcontrollers to the continent. Public investment in embedded R&D reached billions of euros under the High Tech Strategy 2025 program, focusing on secure and energy-efficient architectures. This ecosystem of industrial demand, domestic supply, and policy support solidifies Germany’s position as the embedded technology powerhouse of Europe.

France Embedded System Market Analysis

France had a promising share of the European embedded system market in 2025. The strategic focus of France on aerospace, defense, and nuclear energy is driving the French market expansion. As per the European Defence Agency, French companies like Thales and Safran accounted for a significant portion of Europe’s high-integrity embedded system exports in 2024. Concurrently, France’s automotive sector, led by Stellantis and Renault, is accelerating embedded content in electric and connected vehicles. As per the French Ministry of Transport, most new passenger cars sold domestically in 2024 featured multiple embedded control units for ADAS and telematics. The France 2030 investment plan has committed hundreds of millions of euros to sovereign semiconductor and embedded software development, which aims to reduce reliance on non-EU suppliers. Additionally, France’s strong engineering education pipeline ensures a steady talent supply, which is making the country a high-value and mission-critical node in Europe’s embedded landscape.

United Kingdom Embedded System Market Analysis

The United Kingdom is anticipated to command a prominent share of the European embedded system market over the forecast period. Despite Brexit-related trade adjustments, the UK maintains strength in medical technology, telecommunications infrastructure, and fintech hardware, which are all embedded-reliant domains. According to NHS Digital, over a million remote monitoring units were deployed in 2024, each containing ARM-based microcontrollers with secure boot capabilities. In telecommunications, Ofcom confirmed that most new 5G infrastructure installed in 2024 featured programmable embedded processors for network slicing and edge computing. The UK’s semiconductor design sector, anchored by Arm Holdings in Cambridge, continues to influence global embedded architecture standards. Innovate UK allocated hundreds of millions of pounds in 2024 to support embedded AI and cybersecurity startups. These assets position the UK as a high-innovation, design-led contributor to the European embedded ecosystem.

Italy Embedded System Market Analysis

Italy is estimated to showcase a healthy CAGR in the European embedded system market over the forecast period. The country’s embedded activity is concentrated in industrial automation, luxury automotive, and smart appliances. Companies like CNH Industrial and Ferrari embed sophisticated control systems for precision machinery and high-performance vehicles. As per the Italian National Institute of Statistics, a majority of medium-sized manufacturing firms adopted embedded condition monitoring systems in 2024 to comply with EU energy efficiency directives. The white goods sector, led by Whirlpool Europe and Electrolux Italia, integrates numerous embedded sensors per premium appliance for adaptive cycle control and connectivity. Italy’s National Recovery and Resilience Plan has earmarked billions of euros for digital manufacturing, including grants for embedded system retrofits in legacy production lines. Technical institutes in Emilia Romagna and Lombardy produce thousands of embedded engineering graduates annually, feeding regional supply chains. Italy’s niche excellence in mechatronic embedded solutions ensures its continued relevance in the European market.

Sweden Embedded System Market Analysis

Sweden is projected to record a steady CAGR over the forecast period in the European market due to its telecommunications and clean tech sectors, where embedded intelligence enables network efficiency and sustainability. Ericsson’s 5G base stations deployed across Europe in 2024 each contained numerous embedded processing units for real-time beamforming and latency optimization. In parallel, Sweden’s commitment to fossil-free transportation has accelerated embedded adoption in electric buses and charging infrastructure. As per the Swedish Energy Agency, most public EV chargers installed in 2024 featured embedded secure communication modules compliant with ISO 15118. The nation also hosts a vibrant medtech cluster in Medicon Valley, where firms like Getinge embed real-time control systems in life support equipment. Sweden’s emphasis on green embedded design further differentiates its offerings. Supported by robust R&D funding and a culture of cross-sector innovation, Sweden contributes strongly to high-value embedded applications in Europe.

COMPETITIVE LANDSCAPE

The Europe embedded system market features intense competition among established semiconductor vendors, specialized embedded software firms, and vertically integrated original equipment manufacturers. While global players maintain strong footholds, European companies leverage regional regulatory alignment, engineering expertise, and proximity to key industrial customers to differentiate themselves. Competition centres on performance per watt efficiency, functional safety certification, software toolchain maturity, and supply chain resilience. The push toward software-defined functionality has intensified rivalry in middleware and real-time operating system domains. Simultaneously, smaller firms compete through niche applications in medical devices and renewable energy controls. Consolidation is rising as larger players acquire embedded AI and cybersecurity startups to broaden capabilities. Despite collaborative initiatives under the European Chips Act, competitive pressure remains high due to overlapping customer bases and rapid technological obsolescence in high-growth segments like automotive and industrial automation.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Embedded Systems Market include

- Intel Corporation

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- STMicroelectronics N.V.

- Qualcomm Incorporated

- Renesas Electronics Corporation

- Infineon Technologies AG

- Analog Devices, Inc.

- Microchip Technology Inc.

- Fujitsu Limited

- ARM Holdings plc

- Siemens AG

TOP LEADING PLAYERS IN THE MARKET

- Infineon Technologies is a leading European semiconductor manufacturer deeply embedded in the global embedded systems ecosystem. Headquartered in Germany, the company supplies microcontrollers, power management ICs, and security chips that serve automotive, industrial, and IoT applications. In recent years, Infineon has intensified its focus on AI-enabled edge computing platforms and secure embedded controllers compliant with ISO 26262 and IEC 61508 standards. The company launched its AURIX TC4 microcontroller family in early 2025, targeting next-generation electric vehicle architectures. It also expanded its Dresden fab capacity to address persistent supply chain constraints, reinforcing its role as a strategic supplier for European OEMs seeking supply sovereignty and functional safety.

- STMicroelectronics is a Franco-Italian semiconductor giant with a pivotal role in shaping embedded solutions across Europe and globally. The company specializes in ARM-based microcontrollers, MEMS sensors, and power discrete devices used in automotive, healthcare, and smart infrastructure. Recently, STMicroelectronics strengthened its embedded AI capabilities by introducing the STM32 N6 series featuring an integrated neural processing unit. It also partnered with major European industrial automation firms to co-develop predictive maintenance modules. In 2024, the company inaugurated a new 300 mm wafer plant in Italy dedicated to embedded power ICs, aligning with the EU Chips Act objectives and enhancing its ability to support localized, resilient embedded system production.

- NXP Semiconductors, though headquartered in the Netherlands, operates as a cornerstone of Europe’s embedded technology landscape. The company is renowned for its Layerscape and i.MX application processors, S32 automotive platforms, and secure edge computing solutions. NXP has actively advanced software-defined vehicle architectures by integrating hypervisor-based virtualization into its S32G processors. In 2024, it launched a comprehensive edge AI toolkit for industrial embedded developers and expanded its collaboration with European telecom operators on 5G private network gateways. Its focus on secure, scalable, and energy-efficient embedded platforms continues to position NXP as a critical enabler of Europe’s digital and green transitions.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe embedded system market prioritize vertical integration through in-house semiconductor fabrication to mitigate supply chain risks. They invest heavily in research and development to embed artificial intelligence and cybersecurity features directly into hardware. Strategic partnerships with automotive and industrial original equipment manufacturers enable co-innovation and early design wins. Companies are also aligning product roadmaps with European regulatory frameworks such as the Cyber Resilience Act and Ecodesign Regulation to ensure compliance and market access. Additionally, they are expanding localized software support and developer ecosystems to accelerate time to market for embedded applications across diverse sectors.

MARKET SEGMENTATION

This research report on the europe embedded systems market is segmented and sub-segmented into the following categories.

By Component

- Hardware

- Embedded Software

By Application

- Automotive

- Healthcare

- Industrial Automation

- Consumer Electronics

- Telecommunications

By Country

- Germany

- France

- United Kingdom

- Italy

- Sweden

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com