Europe Gas Engines Market Size, Share, Trends & Growth Forecast Report, Segmented By Application, Fuel, Application, Engine, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Gas Engines Market Report Summary

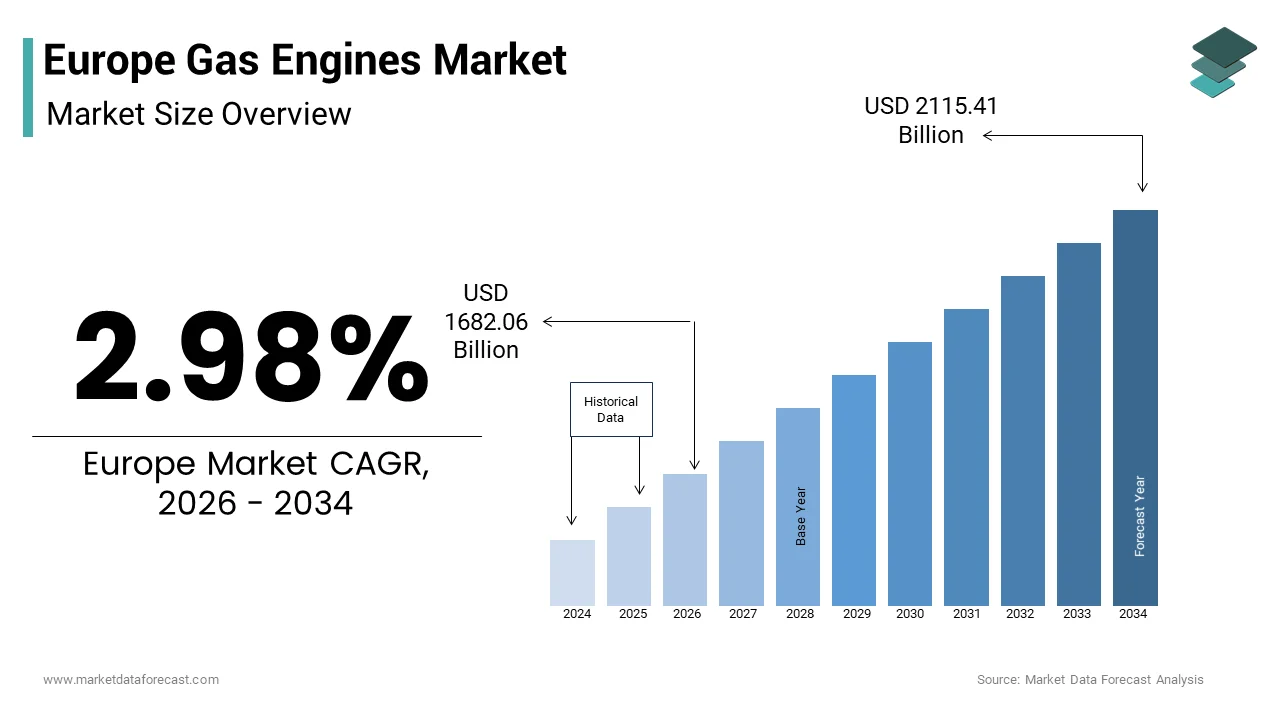

The Europe gas engines market was valued at USD 1,633.07 billion in 2025, is estimated to reach USD 1,682.06 billion in 2026, and is projected to reach USD 2,115.41 billion by 2034, growing at a CAGR of 2.98% during the forecast period from 2026 to 2034. The growth of the Europe gas engines market is driven by the increasing demand for flexible and efficient power generation solutions, rising integration of renewable energy sources, and the need for reliable backup power systems. The transition toward cleaner energy sources, particularly natural gas, along with advancements in engine efficiency and emissions reduction technologies, is further supporting market expansion. Additionally, the growing focus on decentralized energy systems and combined heat and power (CHP) applications is strengthening the adoption of gas engines across Europe.

Key Market Trends

- Increasing demand for gas engines in power generation to support grid stability amid rising renewable energy penetration.

- Growing adoption of natural gas-based engines due to lower emissions compared to conventional fossil fuels.

- Rising deployment of decentralized energy systems and CHP plants across industrial and commercial sectors.

- Technological advancements in four-stroke engines improving fuel efficiency and operational reliability.

- Expanding role of gas engines as backup and peaking power solutions in modern energy infrastructure.

Segmental Insights

By Application

The power generation segment dominated the Europe gas engines market, accounting for 42.3% of the market share in 2025. This dominance is driven by the increasing need for stable and flexible electricity generation, particularly to balance intermittent renewable energy sources such as wind and solar.

By Fuel

The natural gas segment held the largest share of the Europe gas engines market in 2025. Its prominence is attributed to its relatively lower carbon emissions, widespread availability, and strong policy support for cleaner fuel alternatives across Europe.

By Engine Type

The four-stroke engine segment led the market with a dominant share in 2025. These engines are widely preferred due to their higher efficiency, durability, and suitability for continuous and large-scale power generation applications.

Regional Insights

The Europe gas engines market is experiencing steady growth across key countries, supported by energy transition policies and increasing demand for reliable power infrastructure.

- Germany led the market, accounting for 22.3% of the total share in 2025, driven by its strong industrial base and focus on energy efficiency and decentralized power systems.

- Italy ranked second with a 24.3% share, supported by its expanding distributed energy generation and CHP adoption.

- The United Kingdom market is growing steadily due to its advanced electricity grid and increasing investments in flexible power solutions.

- France is witnessing growth driven by niche demand for decentralized energy systems and grid support applications.

- Spain is emerging as a key market, where rapid renewable energy expansion is creating strong demand for flexible gas-based power generation.

Competitive Landscape

The Europe gas engines market is highly competitive, with leading global and regional players focusing on innovation, efficiency improvements, and low-emission technologies. Companies are investing in advanced engine designs, digital monitoring systems, and hybrid energy solutions to strengthen their market position. Strategic partnerships, expansion of service networks, and integration with renewable energy systems are key approaches adopted by market participants to enhance their competitiveness.

Prominent players in the Europe gas engines market include General Electric, Caterpillar, Cummins, Wärtsilä, MAN Energy Solutions, Rolls-Royce, MTU, Perkins, Honda, and Kohler.

Europe Gas Engines Market Size

The Europe gas engines market size was valued at USD 1633.07 billion in 2025 and is anticipated to reach USD 1682.06 billion in 2026 to reach USD 2115.41 billion by 2034, growing at a CAGR of 2.98% during the forecast period from 2026 to 2034.

Introduction to the Europe Gas Engines Market

The gas engines are the design manufacture and distribution of internal combustion engines that utilize natural gas liquefied petroleum gas or biogas as primary fuel sources. These power units are critical for stationary power generation combined heat and power systems and marine propulsion across the continent. The strategic importance of this sector is underscored by the region's extensive energy infrastructure. This substantial reliance on gas infrastructure provides a foundational base for engine deployment. Furthermore, the International Energy Agency stated in its 2025 European energy outlook that over 180 million households in Europe rely on gas networks for heating and industrial processes. This widespread accessibility ensures a consistent fuel supply for gas powered machinery. The transition toward decentralized energy solutions has further cemented the role of gas engines in providing reliable backup power and grid stability.

MARKET DRIVERS

Stringent Emission Regulations Drive Adoption of Cleaner Gas Technologies

The regulatory pressure to reduce carbon footprints for the adoption of advanced gas engines is propelling the growth of Europe gas engines market. Governments are enforcing stricter limits on nitrogen oxides and particulate matter which traditional diesel engines struggle to meet without expensive after treatment systems. Gas engines inherently produce lower emissions making them a compliant choice for industrial and power generation applications. According to the European Environment Agency, industrial facilities reduced their nitrogen oxide emissions by 12% between 2020 and 2024 largely due to fuel switching initiatives. The Industrial Emissions Directive mandates that large combustion plants achieve specific emission thresholds which gas fired units can meet more efficiently than coal or oil counterparts. This regulatory environment compels operators to invest in high efficiency gas engines that offer operational continuity while adhering to legal frameworks. The push for cleaner air in urban centers also drives demand for gas powered combined heat and power units in district heating networks.

Energy Security Concerns Accelerate Investment in Domestic Gas Infrastructure

The geopolitical instability and the need for energy independence have prompted European nations to diversify their energy mix and enhance domestic production capabilities is additionally leveraging the growth of Europe gas engines market. This shift has led to increased investment in local gas processing and distributed generation systems where gas engines play a crucial role. The REPowerEU plan launched by the European Commission aims to eliminate dependence on Russian fossil fuels and accelerate the green transition. According to the European Biogas Association biomethane production in Europe reached 7 billion cubic meters in 2025 representing a 35% increase from 2022 levels. This surge in domestic renewable gas availability creates a robust fuel supply chain for gas engines. Industries are increasingly installing on site gas generators to ensure uninterrupted operations amidst potential grid fluctuations or supply disruptions. In Poland the national energy strategy outlined in 2024 prioritizes the installation of 5000 new decentralized gas power units by 2030 to enhance grid resilience. This strategic move reflects a broader trend, where energy security overrides pure cost considerations. Companies are willing to invest in gas engine technology because it offers fuel flexibility allowing them to switch between natural gas and renewable biogas.

MARKET RESTRAINTS

Rising Penetration of Renewable Energy Sources Limits Baseload Demand

The aggressive expansion of wind and solar power capacities the traditional baseload application of gas engines. As renewable energy sources become more cost competitive and efficient they displace conventional thermal generation during periods of high wind or sunlight. According to study, a European energy think tank renewables generated 43% of the European Union’s electricity in 2025 surpassing fossil fuels for the first time in history. This structural shift reduces the operational hours for gas engines that were previously used for continuous power generation. Grid operators now prioritize zero marginal cost renewable energy, which forces gas fired plants into a residual role. The International Renewable Energy Agency stated that solar photovoltaic capacity in Europe doubled between 2022 and 2024 reaching over 300 gigawatts. This massive influx of intermittent power requires flexible backup rather than constant baseload supply. Consequently, the utilization rate of existing gas engines has declined in several countries. This trend discourages new investments in large scale gas engine installations for primary power. The economic viability of gas engines is thus constrained by the diminishing need for continuous thermal generation as the grid becomes increasingly dominated by variable renewable energy sources that require different types of balancing services.

High Volatility in Natural Gas Prices Erodes Operational Economics

Fluctuating natural gas prices create financial uncertainty for end users with the widespread adoption of gas engines for commercial and industrial applications is also hampering the growth of Europe gas engines market. The European benchmark for natural gas prices experienced significant volatility in recent years affecting the total cost of ownership for gas powered systems. According to the European Central Bank industrial energy prices in the Eurozone remained 25% higher in 2025 compared to pre 2020 averages. This elevated cost structure makes gas engines less attractive compared to electric alternatives powered by increasingly affordable renewable electricity. Manufacturing firms operating on thin margins are hesitant to commit to long term gas engine contracts when fuel expenses can spike unpredictably. In Italy, the Confindustria industry association noted that 40% of small and medium enterprises delayed energy infrastructure upgrades in 2024 due to concerns over gas price stability. This hesitation directly impacts sales volumes for engine manufacturers. Furthermore, the correlation between gas prices and carbon allowance costs under the European Union Emissions Trading System adds another layer of financial risk. When gas prices rise the operational expenditure advantage of gas over coal diminishes and its competitiveness against electricity weakens.

MARKET OPPORTUNITIES

Integration of Hydrogen Ready Engines Offers Future Proof Solutions

The development of hydrogen compatible gas engines for manufacturers to align with the European Union’s long term decarbonization goals is certainly creating new opportunities for the growth of Europe gas engines market. As the region moves toward a hydrogen economy engines that can operate on blends of natural gas and hydrogen or pure hydrogen are gaining traction. This technological evolution allows existing infrastructure to be utilized, while transitioning away from fossil fuels. The European Clean Hydrogen Alliance projected that hydrogen demand in Europe would reach 10 million tons by 2030, creating a viable fuel source for next generation engines. Major engine manufacturers are already testing prototypes that can handle up to 100% hydrogen without significant modifications. According to Siemens Energy, over 60 gas turbines and engines installed in Europe since 2023 are certified as hydrogen ready. This capability provides customers with a clear pathway to net zero emissions without stranded assets. In the Netherlands the Port of Rotterdam authority announced plans to convert 20 industrial power units to hydrogen blending by 2026. This initiative demonstrates the practical application of hybrid fuel technologies in heavy industry. The ability to seamlessly switch between natural gas and hydrogen offers operational flexibility that is highly valued by energy intensive industries. As hydrogen production scales up and costs decline due to electrolyzer advancements the economic case for these dual fuel engines strengthens. This transition phase allows the gas engine market to remain relevant and grow by serving as a bridge technology that supports the gradual integration of green hydrogen into the industrial energy mix.

Expansion of Combined Heat and Power Systems Enhances Efficiency Value

The growing emphasis on energy efficiency drives the adoption of combined heat and power systems powered by gas engines, which offer superior overall efficiency compared to separate heat and power generation is additionally to elevate new opportunities for the growth of Europe gas engines market. CHP units capture waste heat from electricity generation for use in heating or cooling processes achieving total efficiencies of up to 90%. This high level of efficiency aligns with the European Union’s Energy Efficiency Directive which mandates annual energy savings targets for member states. According to study, the installation of new CHP capacity in Europe increased by 8% in 2024 with gas engines accounting for the majority of these installations. District heating networks in Scandinavia and Central Europe are increasingly integrating gas engine CHP plants to provide reliable and efficient energy to residential and commercial buildings. This widespread adoption is driven by the economic benefits of reduced energy bills and lower carbon taxes. Industrial facilities are also leveraging CHP technology to optimize their energy consumption. The textile and food processing sectors in particular are investing in onsite gas engine CHP units to meet both their electrical and thermal demands simultaneously. As energy prices remain elevated the payback period for these systems shortens making them an attractive investment. The regulatory support for high efficiency cogeneration further incentivizes this trend ensuring sustained demand for gas engines designed specifically for CHP applications across various industrial and municipal sectors.

MARKET CHALLENGES

Complex Regulatory Landscape Creates Compliance Uncertainties

Navigating the intricate and evolving regulatory framework for manufacturers and operators is significant challenge for the growth of Europe gas engines market. The interplay between national energy policies European Union directives and local environmental standards creates a fragmented compliance environment. Manufacturers must adapt their products to meet varying emission limits and efficiency requirements across different jurisdictions. The European Green Deal introduces dynamic changes to taxation and subsidy schemes which can alter the economic viability of gas engines overnight. According to the European Commission, over 15 new legislative acts related to energy and climate were proposed or updated in 2025 alone. This rapid pace of regulatory change increases the cost of research and development as companies strive to maintain compliance. In France the introduction of a new carbon tax on industrial combustion sources in 2024 added an unexpected financial burden to gas engine operators. Such policy shifts make long term planning difficult for investors who fear regulatory obsolescence. Additionally, the definition of what constitutes a renewable or low carbon gas varies between member states leading to confusion over eligibility for green subsidies. The lack of harmonization means that a gas engine certified in one country may face additional hurdles in another. This fragmentation increases administrative costs and delays market entry for new technologies. Companies must invest heavily in legal and compliance resources to navigate this complex landscape which detracts from innovation budgets.

Supply Chain Disruptions Impact Component Availability and Costs

The ongoing challenges related to supply chain vulnerabilities, which affect the timely delivery and cost competitiveness of products is also to impede the growth of Europe gas engines market. The reliance on specialized components such as electronic control units high temperature alloys and precision machined parts makes the industry susceptible to global logistical bottlenecks. Recent geopolitical tensions and trade restrictions have exacerbated these issues leading to prolonged lead times and increased material costs. Shortages of semiconductor chips which are critical for modern engine management systems continue to plague manufacturers despite efforts to diversify suppliers. In Germany, major engine producers reported average delivery delays of 16 weeks for key electronic modules in the fourth quarter of 2025. These delays disrupt project timelines for end users who rely on timely installation for operational continuity. Furthermore, the scarcity of rare earth metals used in sensors and magnets adds another layer of complexity to procurement strategies. Fluctuations in shipping costs and port congestion further compound these challenges making it difficult to maintain stable pricing for customers. Manufacturers are forced to hold larger inventories which ties up capital and increases storage costs. This operational inefficiency undermines the competitive position of gas engines against alternative technologies with simpler supply chains, such as battery electric systems which benefit from streamlined manufacturing processes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.98% |

| Segments Covered | By Application, End-User, Fuel, Engine, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | General Electric (US), Caterpillar (US), Cummins (US), Wärtsilä (FI), MAN Energy Solutions (DE), Rolls-Royce (GB), MTU (DE), Perkins (GB), Honda (JP), Kohler (US) |

SEGMENTAL ANALYSIS

By Application Insights

The power generation segment was the largest by holding 42.3% of the Europe gas engines market share in 2025. Gas engines are indispensable for maintaining grid stability as renewable energy sources introduce variability into the electrical network. They provide rapid response capabilities that balance supply and demand fluctuations ensuring uninterrupted power delivery. According to the European Network of Transmission System Operators for Electricity, the requirement for flexible balancing reserves increased by 30% between 2022 and 2025 due to higher wind and solar penetration. Gas engines can start up and reach full load within minutes making them ideal for frequency regulation and backup power applications. In the United Kingdom, the National Grid ESO reported that gas fired reciprocating engines provided over 15 gigawatts of flexible capacity in 2024. This substantial contribution highlights their importance in preventing blackouts during peak demand or unexpected generation drops. Furthermore, industrial facilities rely on these engines for emergency backup power to protect sensitive operations from costly interruptions. The data center industry which is expanding rapidly across Europe requires highly reliable power sources. This consistent demand from both utility scale operators and private industrial users solidifies the leading position of the power generation segment. The ability of gas engines to operate efficiently at partial loads further enhances their value proposition for grid support services.

The biogas application segment is expected to register a fastest CAGR of 9.5% from 2026 to 2034. Government policies promoting the conversion of agricultural waste into energy are accelerating the deployment of biogas powered gas engines. The European Union’s Circular Economy Action Plan encourages the utilization of organic waste streams to produce renewable energy and reduce landfill usage. Biogas engines play a central role in this process by converting methane from anaerobic digestion into electricity and heat. According to the European Biogas Association, the number of biogas plants in Europe exceeded 22000 in 2025 with a total installed electrical capacity of 13 gigawatts. This represents a significant increase from previous years driven by subsidies and feed in tariffs available in countries like Germany, Italy, and France. Farmers are increasingly adopting biogas technology to manage manure and crop residues while generating additional revenue streams. In Denmark, the Ministry of Environment reported that agricultural biogas production doubled between 2020 and 2025 due to targeted government grants. These initiatives make biogas engines an attractive investment for rural communities and agricultural cooperatives. The technology also helps reduce greenhouse gas emissions from livestock farming which is a major source of methane. By capturing and utilizing this methane biogas engines contribute to climate change mitigation efforts. The scalability of biogas plants allows for small farm level installations as well as large industrial facilities.

By Fuel Insights

The natural gas segment was the largest by holding a significant share of the Europe gas engines market in 2025. The widespread availability of natural gas through an extensive pipeline network ensures a reliable and consistent fuel supply for gas engines. Europe has invested heavily in gas infrastructure over decades creating a robust distribution system that reaches industrial commercial and residential areas. The vast network facilitates easy access to fuel for gas engine installations without the need for complex storage solutions. The reliability of pipeline gas is for applications requiring continuous operation such as combined heat and power plants and industrial processes. This stability provides confidence to end users who prioritize operational continuity. The existing infrastructure also lowers the barrier to entry for new gas engine projects as connection points are readily available. Regulatory frameworks support the maintenance and expansion of this infrastructure to ensure energy security.

The biogas segment is expected to grow at a CAGR of 10.2% from 2026 to 2034. National mandates requiring the blending of renewable gases into existing natural gas grids are stimulating demand for biogas compatible engines. Several European countries have set ambitious targets for biomethane injection to decarbonize the gas network. According to the European Biomethane Industry Panel, France aims to inject 10 terawatt hours of biomethane into its grid by 2030. Similar targets exist in Germany and the Netherlands creating a guaranteed market for biogas producers. Gas engines capable of running on high blends of biomethane are essential for utilizing this renewable resource. These engines allow end users to reduce their carbon footprint without changing their existing infrastructure. In Sweden, the Swedish Energy Agency reported that biomethane production increased by 40% in 2025 due to supportive policy frameworks. This growth creates a positive feedback loop where increased biogas availability encourages more engine installations. The certification schemes for renewable gas ensure traceability and quality which boosts consumer confidence. Industries with strict sustainability goals are prioritizing biogas to meet their environmental social and governance criteria. The automotive and transport sectors are also exploring biogas but stationary power generation remains the primary driver for engine demand. The technical compatibility of modern gas engines with biomethane facilitates seamless adoption. Manufacturers are optimizing engine control systems to handle varying methane numbers ensuring efficient performance.

By Engine Insights

The four stroke engine segment was the largest by holding a dominant share of the Europe gas engines market in 2025. Four stroke gas engines are preferred for their superior thermal efficiency and lower emission profiles which align with stringent European environmental regulations. These engines complete the intake compression power and exhaust strokes in four distinct movements resulting in more complete combustion. This high efficiency translates to lower fuel consumption and reduced operating costs for end users. The design also allows for better control of nitrogen oxide emissions through advanced combustion techniques and after treatment systems. This compliance with Euro V and upcoming Euro VI standards makes them the default choice for urban and industrial installations. The smoother operation and reduced vibration of four stroke engines also extend equipment lifespan and reduce maintenance frequency. Industries such as food processing and pharmaceuticals value this reliability and cleanliness. The European Commission’s Best Available Techniques reference documents recommend four stroke technology for new installations in large combustion plants.

The dual fuel engine segment is esteemed to witness a fastest CAGR of 8.8% from 2026 to 2034. Dual fuel engines provide operational flexibility by allowing users to switch seamlessly between natural gas and liquid fuels, such as diesel. This capability is increasingly valued in an era of energy uncertainty and potential supply disruptions. According to the European Energy Security Strategy, diversification of fuel sources is a key priority for infrastructure operators. In Poland, the state owned power company PGE installed dual fuel engines in several remote substations in 2025 to enhance grid resilience. This flexibility mitigates the risk of downtime due to fuel shortages or pipeline maintenance. The ability to store liquid fuel on site provides an additional layer of security for emergency backup applications. Hospitals and data centers are particularly interested in this feature to guarantee uninterrupted service. The technology also allows operators to optimize fuel costs by switching to the cheaper available fuel at any given time. In times of high gas prices users can revert to diesel although this is less common due to emissions considerations. The electronic control systems in modern dual fuel engines manage the fuel mixture precisely to maintain efficiency and emissions compliance.

COUNTRY ANALYSIS

Germany Gas Engines Market Analysis

Germany was the largest contributor in the Europe gas engines market by accounting for 22.3% of the share in 2025. Germany’s market growth is likely to grow with the robust demand for combined heat and power systems in its extensive manufacturing sector. The country’s Energiewende policy promotes efficient energy use and renewable integration which favors gas engine technologies. According to the German Engineering Federation the domestic market for gas engines grew by 6% in 2025 driven by upgrades in the chemical and automotive industries. The presence of major engine manufacturers such as MAN Energy Solutions and Deutz AG fosters innovation and local supply chain strength. These companies are leaders in developing hydrogen ready engines which aligns with national climate goals. The German government’s funding programs for energy efficiency improvements have spurred investments in onsite power generation. Small and medium enterprises are actively adopting gas engines to reduce energy costs and enhance competitiveness. The district heating sector in cities like Berlin and Munich is also expanding its use of gas engine CHP plants.

Italy Gas Engines Market Analysis

Italy gas engines market was ranked second by holding 24.3% of share in 2025 with its geographical location and historical dependence on gas imports which has driven investments in domestic generation capabilities. The country has a dense network of gas pipelines and storage facilities facilitating widespread engine deployment. According to the Italian Ministry of Ecological Transition, natural gas accounted for 40% of the country’s electricity generation in 2025. This high share creates a favorable environment for gas engine applications in both industrial and civil sectors. The agricultural sector in northern Italy is a major driver for biogas powered engines due to abundant organic waste resources. As per the Italian Biogas Consortium, over 2000 biogas plants were operational in 2025, making Italy a leader in this niche. Government incentives such as the Conto Termico scheme support the installation of high efficiency gas engines for heating. The textile and ceramic industries in regions like Lombardy and Emilia Romagna utilize gas engines for process heat and power. These energy intensive sectors benefit from the cost stability and efficiency of onsite generation. The renovation of older industrial facilities with modern gas engines is a ongoing trend supported by EU recovery funds. Italy’s focus on energy security following recent geopolitical events has accelerated plans for decentralized power systems. This strategic shift ensures sustained demand for gas engines in the coming years.

United Kingdom Gas Engines Market Analysis

The United Kingdom gas engines market is steadily growing during the forecast period owing to the advanced electricity grid which requires significant flexible capacity to balance renewable energy inputs. Gas engines are pivotal in providing this flexibility through rapid response power generation. According to the National Grid, ESO flexible power services procured from gas engines increased by 25% in 2025. The country’s commitment to net zero emissions by 2050 has led to the phased out of coal power creating opportunities for gas as a transition fuel. The data center boom in London and surrounding areas is another key driver with facilities installing gas engines for backup and prime power. Regulatory mechanisms such as the Capacity Market ensure revenue stability for flexible generators encouraging investment. The government’s Hydrogen Strategy outlines significant funding for low carbon technologies. This supportive policy environment combined with technical expertise positions the UK as a key market for advanced gas engine solutions.

France Gas Engines Market Analysis

France gas engines market growth is likely to grow with the grid creates a specific niche for gas engines in decentralized applications. The growth is likely to grow with its heavy reliance on nuclear power which limits the role of gas in baseload electricity generation. However, gas engines are increasingly used for peak shaving and backup power in industrial and tertiary sectors. The country’s strict carbon pricing mechanism encourages industries to adopt high efficiency gas engines to reduce their tax burden. The agricultural sector in regions like Brittany is expanding biogas production driving demand for biogas compatible engines. The hospitality and healthcare sectors are investing in gas engines for reliable heating and power during grid stress events. The government’s Multiannual Energy Program emphasizes the development of renewable gases which benefits the gas engine market. France’s focus on energy sovereignty has led to increased interest in local energy production solutions. The renovation of public buildings with efficient heating systems often includes gas engine CHP units.

Spain Gas Engines Market Analysis

Spain gas engines market growth is driven by the country’s rapid renewable energy expansion creates a complementary demand for flexible gas power. The aggressive renewable energy targets which necessitate flexible backup power sources is also fuelling the growth of Europe gas engines market. Gas engines are essential for balancing the intermittent output from its vast solar and wind farms. The industrial sector in Catalonia and the Basque Country utilizes gas engines for combined heat and power to improve competitiveness. As per the Spanish Association of Gas Distributors, natural gas consumption in industry remained stable indicating sustained demand for gas technologies. The tourism sector along the Mediterranean coast relies on gas engines for reliable power in hotels and resorts. Spain’s National Integrated Energy and Climate Plan supports the development of renewable gases including biomethane. This policy framework encourages the adoption of biogas engines in agricultural and waste management sectors. The modernization of Spain’s gas infrastructure enhances the reliability of fuel supply for engines.

COMPETITIVE LANDSCAPE

The competition in the Europe gas engines market is characterized by intense rivalry among established global manufacturers and specialized regional players who strive to differentiate themselves through technological innovation and service excellence. Market participants face pressure to comply with rigorous environmental standards which drives continuous investment in cleaner combustion technologies and alternative fuel capabilities. The presence of well entrenched brands creates high barriers to entry for new competitors although niche opportunities exist in specialized applications such as biogas and hydrogen. Companies compete not only on product performance but also on total cost of ownership including maintenance efficiency and fuel flexibility. Strategic alliances and collaborations are increasingly common as firms seek to expand their solution portfolios and access new customer segments. The shift toward decentralized energy systems has intensified competition in the combined heat and power sector where reliability and efficiency are paramount. Digitalization has emerged as a key competitive frontier with providers offering advanced monitoring and analytics services to enhance value propositions.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe gas engines market are

- General Electric (US)

- Caterpillar (US)

- Cummins (US)

- Wärtsilä (FI)

- INNIO Jenbacher

- MAN Energy Solutions (DE)

- Rolls-Royce (GB)

- MTU (DE)

- Perkins (GB)

- Honda (JP)

- Kohler (US)

Top Players In The Market

- Caterpillar Inc stands as a pivotal entity in the Europe gas engines market by delivering robust power generation solutions tailored for industrial and commercial applications. The company leverages its extensive global distribution network to provide reliable reciprocating engines that support combined heat and power systems across the continent. Recent strategic initiatives include the expansion of its dealer network in Central Europe to enhance service accessibility and customer support. Caterpillar has also invested heavily in research and development to create engines capable of operating on renewable natural gas blends. This innovation aligns with European sustainability goals and strengthens its competitive edge. The company actively collaborates with local energy providers to integrate advanced digital monitoring tools into their engine portfolios. These actions ensure optimal performance and reduced downtime for clients.

- Rolls Royce Power Systems significantly influences the Europe gas engines market through its high quality mtu brand which is renowned for engineering excellence and reliability. The company specializes in providing sophisticated gas engine solutions for decentralized energy systems and marine applications. Its recent efforts focus on developing hydrogen ready engines that support the transition toward carbon neutral energy sources. Rolls Royce has established partnerships with European utilities to pilot hybrid power systems that combine gas engines with battery storage. This approach enhances grid stability and maximizes renewable energy utilization. The company also upgraded its manufacturing facilities in Germany to increase production capacity for low emission engines. These strategic moves demonstrate a strong commitment to innovation and environmental responsibility.

- INNIO Jenbacher maintains a prominent position in the Europe gas engines market by specializing in high efficiency gas engines for power generation and cogeneration. The company is deeply integrated into the European energy landscape with its headquarters located in Austria. INNIO has recently accelerated its development of hydrogen capable engines aiming to enable 100% hydrogen operation in the near future. This forward looking strategy addresses the growing demand for decarbonized power solutions. The company has also expanded its digital services portfolio with the Jenbacher Connect platform which offers predictive maintenance and performance optimization. These digital tools help customers maximize uptime and reduce operational costs. INNIO actively participates in European research consortia focused on renewable gas integration and energy system flexibility.

Top Strategies Used By Key Market Participants

Key players in the Europe gas engines market primarily focus on product innovation to meet stringent environmental regulations and enhance fuel flexibility. Companies are extensively investing in research and development to create engines capable of running on hydrogen and biogas blends. This strategic shift allows them to align with European decarbonization targets while maintaining operational efficiency. Another major strategy involves expanding service networks and digital offerings to improve customer retention and generate recurring revenue streams. Manufacturers are integrating Internet of Things technologies to provide predictive maintenance and real time performance monitoring. Strategic partnerships with energy providers and technology firms are also common to develop integrated energy solutions. These collaborations facilitate the deployment of hybrid systems that combine gas engines with renewable energy sources. Additionally, companies are pursuing organic growth by upgrading manufacturing facilities to increase production capacity for low emission engines. These combined strategies enable market participants to strengthen their competitive positions and address the evolving needs of European customers effectively.

MARKET SEGMENTATION

‘This research report on the Europe gas engines market is segmented and sub-segmented into the following categories.

By End-User

- Residential

- Commercial

- Industrial

- Agricultural

By Fuel

- Natural Gas

- Biogas

- Synthesis Gas

- Landfill Gas

By Application

- Power Generation

- Marine

- Oil and Gas

- Biogas

- Transportation

By Engine Type

- Two-Stroke Engine

- Four-Stroke Engine

- Spark Ignition Engine

- Dual Fuel Engine

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe gas engines market?

Rising demand for efficient and low-emission power generation solutions is driving market growth.

Why are gas engines gaining popularity across Europe?

They offer cleaner energy generation compared to traditional fossil fuel engines.

How would you explain gas engines in simple terms?

They are engines that generate power using natural gas or other gaseous fuels.

Where are gas engines most commonly used across Europe?

They are widely used in power plants, industrial facilities, and combined heat and power systems.

What makes gas engines important in modern energy systems?

They provide reliable, flexible, and efficient power generation.

From an operational perspective, are gas engines a practical investment?

Yes, they offer cost-effective energy solutions with relatively lower emissions.

What challenges are affecting the Europe gas engines market?

Fluctuating gas prices and transition toward renewable energy are key challenges.

How is the energy transition influencing gas engine demand in Europe?

Shift toward cleaner energy is supporting adoption of lower-emission gas technologies.

Which sectors contribute the most to gas engine demand?

Industrial, commercial, and utility sectors are major contributors.

Is the Europe gas engines market growing steadily?

Yes, it is expanding with increasing need for efficient energy solutions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com