Europe Hand Tools Market Size, Share, Trends & Growth Forecast Report, Segmented By Application, End-User, Distributional Channel, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Hand Tools Market Size

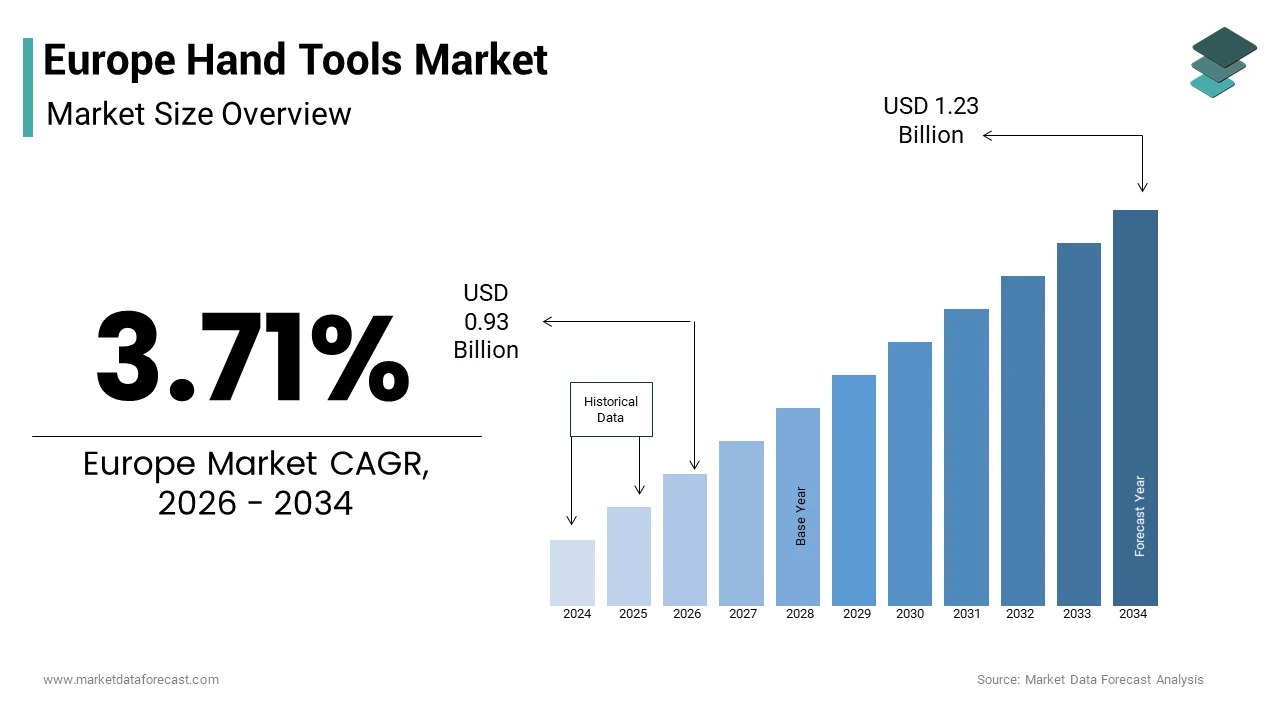

The Europe Hand tools market size was valued at USD 0.90 billion in 2025 and is anticipated to reach USD 0.93 billion in 2026 to reach USD 1.23 billion by 2034, growing at a CAGR of 3.71% during the forecast period from 2026 to 2034.

Introduction and Market Definition

A hand tool is any tool that is powered manually by your own physical strength rather than by a motor, engine, or electricity. These tools include wrenches screwdrivers pliers hammers and cutting implements which remain fundamental to various trades despite the proliferation of power tools. The market dynamics are intrinsically linked to the health of the construction industry and the prevalence of do-it-yourself activities among households. As per Eurostat and European Commission data, the construction sector in the European Union employs nearly 25 million people across its broader ecosystem as of 2025, representing a massive workforce that relies on durable, high-performance hand tools to meet increasingly stringent building standards. Furthermore, the aging building stock in Europe necessitates continuous renovation and maintenance efforts. According to the European Commission buildings account for roughly 40–42% of energy consumption and 35–36% of greenhouse gas emissions driving extensive retrofitting initiatives under the Renovation Wave strategy. This regulatory push creates sustained demand for tools required in insulation installation window replacement and structural repairs. Additionally, the rise of urbanization has led to increased housing density which often requires compact and versatile tools for confined spaces. Research notes that waste prevention and resource efficiency are key priorities influencing the design and material composition of modern tools. Consequently manufacturers are focusing on ergonomic designs and sustainable materials to meet both regulatory standards and user expectations for safety and longevity in a mature market.

MARKET DRIVERS

Robust Growth in Residential Renovation and Do It Yourself Activities

The surge in residential renovation projects and the enduring popularity of do-it-yourself activities contribute to the growth of the Europe hand tools market. Homeowners are increasingly investing in home improvement projects to enhance property value and comfort particularly in the post pandemic era where living spaces have become multifunctional. As per Eurostat expenditure on housing maintenance and repair has shown consistent growth across major European economies with households allocating a larger portion of their budget to home upgrades. The European Construction Industry Federation highlights that renovation activities account for nearly half of the total construction output in the EU indicating a massive base of potential users for hand tools. DIY enthusiasts require a wide array of manual tools for tasks such as furniture assembly painting plumbing fixes and minor carpentry. The accessibility of online tutorials and social media content further empowers individuals to undertake complex projects independently. Trade organizations for the retail sector observe that demand for hardware and maintenance supplies tends to stay stable during periods of economic uncertainty, as individuals choose to fix existing belongings rather than buying new items. This trend is supported by the availability of affordable and high quality tools from both established brands and private labels. The cultural shift towards self sufficiency and cost saving measures ensures a steady demand for basic and specialized hand tools in the residential segment.

Expansion of Industrial Manufacturing and Automotive Repair Sectors

The expansion of industrial manufacturing and the automotive repair sectors greatly drives the demand for professional grade products in the Europe hand tools market. These industries require precise durable and ergonomic tools to ensure efficiency and safety in assembly lines and maintenance operations. As per the European Automobile Manufacturers Association the automotive sector remains a cornerstone of the European economy with millions of vehicles requiring regular maintenance and repair. Professional technicians rely on high quality hand tools for intricate tasks that power tools cannot perform safely or accurately. The manufacturing sector also contributes substantially with factories requiring specialized tools for equipment maintenance and production line adjustments. According to the European Commission the industrial strategy aims to strengthen the single market for goods which includes ensuring the availability of reliable tools for workers. The emphasis on occupational health and safety regulations mandates the use of ergonomically designed tools to reduce workplace injuries and fatigue. This regulatory environment encourages companies to invest in premium hand tools that comply with safety standards. Furthermore the growth of electric vehicle production introduces new maintenance requirements that necessitate insulated and non conductive tools. The continuous need for precision and durability in these professional settings sustains a robust market for high end hand tools.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

Volatility in raw material prices and ongoing supply chain disruptions are one of the major restraints to the Europe hand tools market. The production of hand tools relies heavily on steel aluminum and other metals which have experienced substantial price fluctuations due to geopolitical tensions and energy costs. As per the European Central Bank producer prices for intermediate goods including metals have risen sharply impacting the manufacturing costs of tool makers. These increased costs are often passed on to consumers leading to higher retail prices which can dampen demand particularly among price sensitive DIY users. Supply chain bottlenecks further exacerbate the issue by causing delays in the availability of finished products. According to the European Manufacturing Alliance logistical challenges and port congestions have extended lead times making it difficult for retailers to maintain adequate stock levels. The dependence on imports for certain raw materials and components exposes European manufacturers to global market instabilities. Additionally the energy crisis in Europe has increased production costs for steel mills affecting the entire supply chain. These factors create uncertainty for manufacturers and retailers who struggle to plan inventory and pricing strategies effectively. The market will continue to face high pressure on profit margins and product availability until raw material prices stabilize and supply chains become more resilient. Until these conditions are met, businesses should anticipate continued volatility.

Stringent Environmental Regulations and Compliance Costs

Stringent environmental regulations and the associated compliance costs hinder the expansion of the Europe hand tools market. The European Union has implemented rigorous standards regarding the use of hazardous substances waste management and carbon emissions which manufacturers must adhere to. Regional chemical agencies enforce strict rules regarding the substances allowed in consumer goods, forcing equipment builders to switch to safer materials for protective layers and ergonomic grips. These alternatives are often more expensive and may offer different performance characteristics necessitating additional research and development investments. The Waste Electrical and Electronic Equipment Directive although primarily for power tools influences the broader tool industry by setting precedents for sustainability and recyclability. According to the European Commission the Circular Economy Action Plan encourages the design of durable and repairable products which can increase initial production costs. Small and medium sized enterprises may struggle to meet these regulatory requirements due to limited resources leading to market consolidation. Furthermore the need for certified sustainable sourcing of materials adds complexity to supply chain management. Compliance with these evolving regulations requires continuous monitoring and adaptation which can slow down product launches and increase operational expenses. These regulatory burdens can hinder innovation and competitiveness particularly for smaller players in the market.

MARKET OPPORTUNITIES

Integration of Smart Technologies and IoT in Hand Tools

The integration of smart technologies and the Internet of Things into hand tools opens up new chances for the growth of the Europe hand tools market. Although traditionally manual some advanced hand tools are now being equipped with sensors and connectivity features to enhance precision and data collection. As per the International Data Corporation the adoption of IoT in industrial settings is accelerating with tools that can track usage torque and calibration status gaining traction. These smart tools provide valuable data for predictive maintenance and quality control in professional environments such as aerospace and automotive manufacturing. The European Commission’s Digital Decade policy supports the digital transformation of industries creating a favorable environment for smart tool adoption. According to the European Aerospace and Defence Industries Association the demand for precision and traceability in manufacturing processes is driving the uptake of connected tools. These innovations allow companies to optimize workflows reduce errors and ensure compliance with strict quality standards. Furthermore smart tools can enhance worker safety by providing real time feedback on proper usage techniques. As technology costs decrease and connectivity improves the potential for smart hand tools to penetrate broader market segments increases. This technological evolution offers manufacturers a chance to differentiate their products and capture value in a mature market.

Growing Demand for Ergonomic and Safety Enhanced Tools

The growing demand for ergonomic and safety enhanced tools unlocks potential for the Europe hand tools market. With increasing awareness of occupational health issues there is a strong preference for tools that reduce physical strain and prevent injuries. As per the European Agency for Safety and Health at Work musculoskeletal disorders are among the most common work related health problems driving the need for ergonomic solutions. Manufacturers are responding by designing tools with improved grip shapes weight distribution and vibration damping features. The European Standardization Committee has developed specific standards for ergonomic hand tools which help guide product development and consumer choice. This trend is particularly relevant in industries with high manual labor intensity such as construction and manufacturing. Additionally the aging workforce in Europe requires tools that are easier to handle and less physically demanding. By focusing on ergonomic design and safety features manufacturers can appeal to both professional users and health conscious DIYers. This focus on user well being not only meets regulatory requirements but also enhances brand reputation and customer loyalty.

MARKET CHALLENGES

Counterfeit Products and Intellectual Property Theft

The prevalence of counterfeit products and intellectual property theft is a major challenge to the Europe hand tools market. This undermines brand integrity and consumer safety. Counterfeit tools often fail to meet quality and safety standards posing risks to users and damaging the reputation of legitimate manufacturers. As per the European Union Intellectual Property Office seizures of counterfeit goods at EU borders remain high with tools and hardware being frequent targets. These illicit products are typically sold at lower prices attracting price sensitive consumers who may not recognize the quality difference. Multiple studies found that the presence of imitation products in the market creates unfair competition and leads to substantial financial setbacks for legitimate producers of high-quality equipment. The difficulty in distinguishing between authentic and fake products especially in online marketplaces exacerbates the problem. Consumers who purchase counterfeit tools may experience premature failure or injury leading to mistrust in the brand. Manufacturers must invest heavily in anti counterfeiting measures such as holograms and tracking systems which add to operational costs. Furthermore legal actions against counterfeiters are often complex and costly with varying enforcement levels across different countries. This persistent issue requires coordinated efforts between governments industry bodies and retailers to protect intellectual property and ensure consumer safety.

Shortage of Skilled Labor and Training Gaps

The shortage of skilled labor and training gaps in the use of professional hand tools are a significant impediment to the Europe hand tools market. As the workforce ages and fewer young people enter trades such as plumbing carpentry and electrical work there is a decline in the number of users who fully appreciate the value of high quality tools. As per the European Centre for the Development of Vocational Training there is a mismatch between the skills available and the needs of the industry leading to inefficiencies and potential safety hazards. Unskilled workers may misuse tools leading to faster wear and tear or accidents which can negatively impact the perceived value of premium products. According to the European Construction Industry Federation the labor shortage is a critical issue that affects productivity and project timelines. This situation reduces the demand for specialized professional grade tools as inexperienced workers may opt for cheaper alternatives. Additionally the lack of comprehensive training programs means that new entrants may not be aware of the latest ergonomic and safety features available in modern tools. Manufacturers and industry associations need to collaborate on training initiatives to bridge this gap. The skilled labor shortage must be addressed to stabilize the market. Without action, high-end tool demand may drop and safety risks could increase, according to market analyses.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.71% |

| Segments Covered | By Application, End-User, Distributional Channel, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Akar Auto Industries Ltd., Apex Tool Group LLC, Wiha Werkzeuge GmbH, ementex Products Inc., Channellock Inc., Emerson Electric Co., Estwing Manufacturing Co., IDEAL Industries Inc, Ingersoll Rand Inc., JCBL Group, Klein Tools Inc., Malco Tools Inc., Martin Sprocket and Gear Inc., Snap On Inc., STAHLWILLE Eduard Wille GmbH and Co. KG, Stanley Black and Decker Inc., Swanson Tool Co. Inc., Taparia Tools Ltd., Techtronic Industries Co. Ltd., The L.S. Starrett Co., Toughbuilt Industries Inc., TOYA S.A., Vaughan Manufacturing, Wera |

SEGMENTAL ANALYSIS

By Application Insights

The general-purpose hand tools segment remained in the lead in the Europe hand tools market and secured a 55.8% share in 2025. This leading position of the segment is supported by the universal applicability of these tools across residential DIY projects and professional maintenance tasks. General purpose hand tools such as hammers screwdrivers pliers and wrenches are essential for everyday household repairs and do it yourself projects. The aging housing stock in Europe particularly in countries like the United Kingdom and Germany requires frequent minor repairs which drives the replacement and acquisition of general purpose tools. These tools are perceived as durable goods with long lifecycles but high turnover occurs due to loss damage or the desire for upgraded ergonomic models. The affordability and accessibility of general purpose tools make them impulse purchases in supermarkets and hardware stores. Furthermore the rise of online instructional content empowers homeowners to tackle tasks previously outsourced to professionals increasing the volume of tools sold to non professionals. This widespread utility ensures that general purpose tools remain the backbone of the hand tools market in Europe. In the professional sector general purpose hand tools are indispensable for maintenance repair and operations across various industries including automotive manufacturing and facilities management. As per the European Automobile Manufacturers Association millions of vehicles require regular servicing where basic hand tools are used for inspections and minor adjustments. Industrial facilities rely on these tools for routine equipment checks and emergency repairs where precision power tools may not be suitable or safe. Professional users often purchase higher quality general purpose tools that offer better durability and ergonomics leading to higher value transactions. The standardization of tool sizes and types across industries ensures that these products have a broad and stable customer base. Additionally the expansion of the gig economy has increased the number of independent technicians who require their own sets of reliable general purpose tools. This professional demand complements residential sales ensuring the segment maintains its dominant market share.

The metal cutting hand tools segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 6.8% during the forecast period due to the increasing complexity of industrial fabrication and the need for precision in metalworking applications. This growth of the segment is mainly driven by the expansion of precision manufacturing and the aerospace industry in Europe. These sectors require specialized cutting tools such as hacksaws snips and shears that can handle high strength alloys and composite materials with exacting tolerances. As per research, the aerospace sector continues to invest heavily in advanced manufacturing techniques which necessitate high quality manual cutting instruments for finishing and trimming tasks. The demand for lightweight yet strong materials in aircraft production increases the usage of precise metal cutting tools that do not compromise material integrity. According to sources, the industrial strategy emphasizes the importance of high value manufacturing which supports the adoption of superior hand tools. Professional fabricators and technicians prefer premium metal cutting tools that offer clean cuts and reduced effort leading to higher productivity. The stringent quality standards in these industries ensure that only high performance tools are selected driving value growth in this segment. As manufacturing processes become more sophisticated the need for specialized manual cutting solutions continues to rise. The automotive aftermarket and custom fabrication sectors are also key drivers for the rapid growth of metal cutting hand tools. Custom car enthusiasts and professional mechanics utilize metal cutting tools for modifying exhaust systems body panels and structural components. The trend towards vehicle personalization has created a niche market for high precision manual cutting instruments that allow for intricate work without the risk of heat distortion associated with power tools. Metal cutting tools are essential for removing rusted bolts cutting sheet metal and shaping components during repairs. The availability of advanced materials such as titanium coated blades enhances the performance and longevity of these tools attracting professional users. This combination of repair needs and customization trends fuels the accelerated growth of the metal cutting hand tools segment.

By End-user Insights

In 2025, the industrial end user segment held the majority share of 60.7% of the Europe hand tools market. This supremacy of the segment is attributed to by the extensive use of hand tools in manufacturing construction and automotive sectors. Industrial end users including manufacturing plants construction firms and automotive workshops procure hand tools in large volumes to equip their workforce. As per studies, the industrial sector employs millions of workers across Europe who require reliable tools for daily operations. The construction industry alone accounts for a significant portion of tool consumption due to the labor intensive nature of building and renovation projects. According to research, the sector’s steady growth ensures continuous demand for durable hand tools. Industrial buyers prioritize quality and safety leading to higher average selling prices compared to household purchases. Companies often establish contracts with suppliers for regular replenishment of worn or lost tools creating a recurring revenue stream. The implementation of strict safety standards mandates the use of certified tools which further drives procurement from reputable brands. Additionally the expansion of infrastructure projects under the European Green Deal increases the need for tools in renewable energy installations such as wind farms and solar parks. This sustained industrial activity solidifies the leading position of the industrial end user segment. The emphasis on ergonomics and worker safety regulations significantly contributes to the dominance of the industrial segment. Industrial employers are legally obligated to provide tools that minimize physical strain and reduce the risk of injury. This regulatory pressure drives the replacement of older non ergonomic tools with modern designs that feature soft grips and optimized weight distribution. Industrial users are willing to pay a premium for tools that comply with safety standards and offer superior performance. The focus on occupational health also leads to regular training and tool audits ensuring consistent demand for compliant products. This regulatory and ethical commitment to worker safety ensures that industrial end users remain the primary consumers of high quality hand tools in Europe.

The household end user segment is expected to exhibit a noteworthy CAGR of 5.5% between 2026 and 2034. This quick surge of the segment is propelled by the rising trend of do it yourself projects and home improvement activities. It is experiencing rapid growth due to the increasing popularity of do it yourself culture and home improvement projects among European consumers. As per sources, expenditure on housing maintenance and repair has risen as homeowners seek to enhance property value and comfort. The pandemic accelerated this trend with many individuals investing time and resources into renovating their living spaces. According to sources, sales of DIY products including hand tools have shown resilience and growth even during economic uncertainties. Social media platforms and online tutorials have democratized knowledge making complex tasks accessible to amateurs. This empowerment encourages households to purchase their own toolkits for tasks such as furniture assembly painting and minor repairs. The availability of affordable and user friendly tools in retail stores and online platforms lowers the barrier to entry. Furthermore the trend towards sustainable living encourages repairs over replacements driving the purchase of basic hand tools. This cultural shift towards self sufficiency and home enhancement drives the fast expansion of the household end user segment. Increased urbanization and the prevalence of apartment living in Europe also contribute to the fast growth of the household segment. Apartment dwellers often require compact and versatile hand tools for quick fixes and installations. The density of urban living means that minor repairs such as hanging shelves or fixing leaks are frequently handled by residents themselves. Moreover, the convenience of having a personal toolkit for immediate needs appeals to busy urban professionals. Retailers are responding by offering curated starter kits tailored to apartment living which attract first time buyers. The growing number of single person households also drives demand for basic tool sets as individuals manage their own homes. This demographic and lifestyle trend ensures sustained growth in household hand tool consumption.

By Distribution Channel Insights

The in store distribution channel dominated the Europe hand tools market and accounted for a share of 65.6% in 2025. This dominance of the segment is driven by the consumer preference for physical inspection and immediate availability. Consumers prefer to purchase hand tools in store because they can physically inspect the product for quality weight and ergonomics before buying. Hardware stores and hypermarkets allow customers to test the feel of handles and the balance of tools which is crucial for professional and serious DIY users. The ability to speak with knowledgeable staff who can provide recommendations adds value to the shopping experience. Immediate availability is another key factor as users often need tools for urgent repairs and cannot wait for delivery. This convenience and assurance provided by physical stores sustain their leading position in the market. The established retail networks of hardware chains and home improvement stores contribute significantly to the dominance of the in store channel. These stores often offer promotional deals and bundle offers that attract price sensitive consumers. Professional users who run out of supplies during job sites rely on local hardware stores for quick restocking. The integration of click and collect services further strengthens the appeal of physical stores by combining online convenience with offline immediacy. The trust associated with established brick and mortar brands also plays a role particularly among older demographics. This robust infrastructure and immediate product availability ensure that in store channels remain the primary source for hand tool purchases.

The online distribution segment is predicted to witness the highest CAGR of 8.2% over the forecast period owing to convenience extensive product variety and competitive pricing. In addition, this channel is expanding swiftly due to the convenience of home delivery and the extensive variety of products available. Online platforms allow consumers to compare prices read reviews and access detailed specifications easily facilitating informed decision making. The ability to shop at any time without geographical constraints appeals to busy professionals and younger demographics. Home delivery services eliminate the hassle of transporting heavy tool sets adding to the convenience factor. Furthermore online retailers often offer exclusive deals and bundles that attract price sensitive buyers. This ease of access and broad selection drives the accelerated adoption of online channels for hand tool purchases. Competitive pricing and the influence of digital marketing significantly contribute to the fast growth of the online distribution channel. Online retailers often have lower overhead costs allowing them to offer hand tools at more attractive prices than physical stores. Digital marketing strategies including social media ads and influencer partnerships drive traffic to online stores and stimulate impulse purchases. The ease of returning products and flexible payment options also reduce barriers to online shopping. Additionally the rise of mobile commerce allows consumers to make purchases seamlessly from smartphones. These factors combined create a dynamic and attractive online shopping environment that fuels the rapid expansion of this distribution channel.

COUNTRY LEVEL ANALYSIS

Germany Hand Tools Market Analysis

Germany was the top performing country in the Europe hand tools market and held a 22.4% share in 2025. The country’s strong industrial base and robust construction sector drive the demand for high quality hand tools. Germany is home to several renowned tool manufacturers which fosters a culture of precision and durability. As per the Federal Ministry for Economic Affairs and Climate Action the industrial sector remains a key pillar of the economy requiring reliable tools for manufacturing and maintenance. The German DIY market is also well developed with consumers investing in home improvement projects. Research found that while some segments of the building market face challenges, the maintenance of existing structures continues to provide a baseline requirement for manual equipment. The emphasis on occupational safety and ergonomics drives the adoption of premium tools in professional settings. Government initiatives promoting energy efficient building renovations further boost tool consumption. The presence of specialized trade fairs and exhibitions also stimulates market activity. These factors combine to make Germany the largest market for hand tools in Europe.

United Kingdom Hand Tools Market Analysis

The United Kingdom was the next prominent player in the Europe hand tools market and occupied a 18.4% share in 2025. Also, the UK’s vibrant DIY culture and aging housing stock are key enablers of demand. British consumers are avid participants in home improvement projects often undertaking renovations and repairs themselves. As per the Office for National Statistics expenditure on housing maintenance has remained resilient despite economic fluctuations. The prevalence of older properties requires frequent upkeep driving the sale of general purpose and metal cutting tools. Trade organizations in the UK note that the push for more environmentally friendly and efficient homes is becoming a primary driver for work within the building sector. The retail landscape is dominated by large home improvement chains that offer extensive tool selections. Online sales are also rising rapidly reflecting changing consumer preferences. The strong tradition of craftsmanship and DIY ensures a steady demand for both professional and household tools. These dynamics sustain the UK’s significant position in the regional market.

France Hand Tools Market Analysis

France occupies a significant position in the Europe hand tools market. Its active construction sector and growing DIY interest drive market growth. France has implemented ambitious renovation plans to improve energy efficiency in buildings which increases the need for hand tools. As per the French Ministry of Ecological Transition the MaPrimeRénov scheme incentivizes homeowners to undertake energy saving upgrades. This policy support stimulates demand for tools required in insulation and window installation. The French DIY market is expanding with more consumers engaging in home decoration and repair tasks. Building federations in France highlight that the ongoing demand for professional-grade equipment is increasingly linked to specialized renovation work rather than new large-scale developments. The presence of major retail chains and online platforms facilitates access to a wide range of products. Cultural appreciation for craftsmanship also contributes to the preference for high quality tools. These factors ensure France maintains a strong position in the European hand tools market.

Italy Hand Tools Market Analysis

Italy grew steadily in the Europe hand tools market. The country’s strong manufacturing sector particularly in automotive and machinery drives professional tool demand. Italy is known for its design and quality which influences consumer preference for aesthetically pleasing and durable tools. National statistical agencies in Italy track how changes in manufacturing output influence the overall requirement for supplies and equipment within the industrial sector. The construction sector also contributes with ongoing renovation and infrastructure projects. Regional construction associations emphasize that national efforts to improve building safety and thermal performance have created a specific need for advanced and specialized manual tools. The DIY market is growing albeit at a slower pace than in Northern Europe. Local manufacturers produce high end tools that are exported globally enhancing the domestic market’s sophistication. The emphasis on artisanal skills ensures a continued demand for precision hand tools. These elements support Italy’s significant role in the regional market.

Spain Hand Tools Market Analysis

Spain is likely to expand notably in the Europe hand tools market from 2026 to 2034. The country’s recovering construction sector and tourism driven real estate market drive demand. Spain has seen an increase in residential construction and renovation particularly in coastal areas. Government transportation and urban departments in Spain report a gradual increase in building project initiations following the global health crisis. The DIY culture is emerging among younger demographics who are interested in home customization. According to the Spanish Construction Confederation the sector is benefiting from government incentives for sustainable housing. The automotive industry also contributes to professional tool sales with maintenance and repair activities. Retail expansion and online growth are making tools more accessible to consumers. The climate allows for year round outdoor projects further stimulating tool usage. These factors contribute to Spain’s steady presence in the European hand tools market.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe hand tools market are

- Akar Auto Industries Ltd.

- Apex Tool Group LLC

- Wiha Werkzeuge GmbH

- Cementex Products Inc.

- Channellock Inc.

- Emerson Electric Co.

- Estwing Manufacturing Co.

- IDEAL Industries Inc

- Ingersoll Rand Inc.

- JCBL Group

- Klein Tools Inc.

- Malco Tools Inc.

- Martin Sprocket and Gear Inc.

- Snap On Inc.

- STAHLWILLE Eduard Wille GmbH and Co. KG

- Stanley Black and Decker Inc.

- Swanson Tool Co. Inc.

- Taparia Tools Ltd.

- Techtronic Industries Co. Ltd.

- The L.S. Starrett Co.

- Toughbuilt Industries Inc.

- TOYA S.A.

- Vaughan Manufacturing

- Wera

Top Players In The Market

- Stanley Black and Decker Inc is a global leader in the tools and storage industry with a significant presence in the Europe hand tools market. The company owns iconic brands such as Stanley FatMax and DeWalt which are widely recognized for their durability and innovation. Stanley Black and Decker contributes to the global market by providing comprehensive solutions for professional tradespeople and DIY enthusiasts. Recent actions include the expansion of its manufacturing facilities in Europe to enhance supply chain resilience and reduce lead times. The company has also invested in digital platforms to improve customer engagement and direct sales. By focusing on sustainable product design and ergonomic innovations Stanley Black and Decker strengthens its market position. These initiatives ensure the company remains at the forefront of quality and reliability in the hand tools sector.

- Apex Tool Group LLC is a major manufacturer of hand tools power tools and accessories with a strong footprint in Europe. The company offers a diverse portfolio of brands including Weller Crescent and Lufkin which cater to various industrial and consumer needs. Apex Tool Group contributes globally by delivering high performance tools that meet stringent quality standards. Recent actions involve the launch of new ergonomic tool lines designed to reduce worker fatigue and improve safety. The company has also strengthened its distribution network through strategic partnerships with leading European retailers. Apex Tool Group focuses on innovation in material science to enhance tool durability and performance. These efforts help the company maintain a competitive edge and meet the evolving demands of professional users and hobbyists alike.

- Wiha Werkzeuge GmbH is a renowned German manufacturer specializing in high quality precision hand tools for professional applications. The company is known for its innovative screwdrivers pliers and torque tools which are widely used in the electrical and electronics industries. Wiha contributes to the global market by setting benchmarks for ergonomics and safety in hand tool design. Recent actions include the introduction of insulated tools that comply with the latest international safety standards for electrical work. The company has also expanded its production capabilities in Germany to ensure consistent quality and availability. Wiha focuses on sustainability by using eco friendly materials and processes in its manufacturing operations. These commitments to excellence and responsibility strengthen Wiha’s reputation and market position in Europe and beyond.

Top Strategies Used By The Key Market Participants

Key players in the Europe hand tools market primarily focus on product innovation and ergonomic design to differentiate their offerings. Companies invest in research and development to create tools that enhance user comfort and safety. Strategic expansions of manufacturing facilities aim to improve supply chain resilience and reduce delivery times. Partnerships with local distributors and retailers strengthen market access and brand visibility. Digital transformation initiatives include e commerce platforms and direct to consumer sales channels. Sustainability is a core strategy with firms adopting eco friendly materials and production methods. Brand consolidation through acquisitions allows companies to broaden their product portfolios. These strategies collectively enable key participants to meet diverse customer needs and maintain competitive advantages in the market.

COMPETITIVE LANDSCAPE

The competition in the Europe hand tools market is intense and characterized by the presence of established global brands and specialized regional manufacturers. Leading companies compete on the basis of product quality durability innovation and brand reputation. The market exhibits a moderate level of consolidation as major players acquire smaller firms to expand their product ranges and geographic reach. Differentiation is achieved through ergonomic designs advanced materials and specialized features for specific industries. Price competition is significant particularly in the general purpose segment where private label brands offer lower cost alternatives. Professional users prioritize performance and safety driving demand for premium branded tools. New entrants face barriers due to high capital requirements and established distribution networks. However niche players continue to innovate in specialized segments such as precision tools for electronics. Collaborative partnerships with retailers and online platforms are crucial for market penetration. The focus on sustainability and regulatory compliance shapes competitive dynamics. Companies that balance innovation with cost efficiency and strong brand loyalty are best positioned to succeed in this mature and evolving market landscape.

MARKET SEGMENTATION

This research report on the Europe hand tools market is segmented and sub-segmented into the following categories.

By Application

- General-purpose

- Metal cutting

- Taps and dies and others

By End-user

- Industrial

- Household

By Distribution Channel

- In Store

- Online

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe hand tools market?

Rising construction, DIY activities, and industrial maintenance needs are driving market growth.

Why are hand tools still widely used despite increasing automation?

They offer precision, portability, and cost-effectiveness for many tasks.

How would you explain hand tools in simple terms?

They are manually operated tools used for construction, repair, and maintenance work.

Where are hand tools most commonly used across Europe?

They are widely used in construction, automotive, manufacturing, and household applications.

What makes hand tools essential in everyday and industrial use?

They provide flexibility and control for various manual operations.

From a practical standpoint, are hand tools a necessary investment?

Yes, they are essential for basic repair, maintenance, and professional tasks.

What challenges are affecting the Europe hand tools market?

Competition from power tools and fluctuating raw material costs are key challenges.

How is the DIY trend influencing hand tool demand in Europe?

Growing interest in home improvement is increasing demand for basic tools.

Which segments contribute the most to hand tool demand?

Construction and automotive sectors are major contributors.

Is the Europe hand tools market growing steadily?

Yes, it is expanding with consistent demand from both professionals and consumers.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com