Europe Hospitality Market Size, Share, Trends, & Growth Forecast Report By Type (Non-Residential Accommodation Services, Food and Beverage Services), Ownership and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Hospitality Market Report Summary

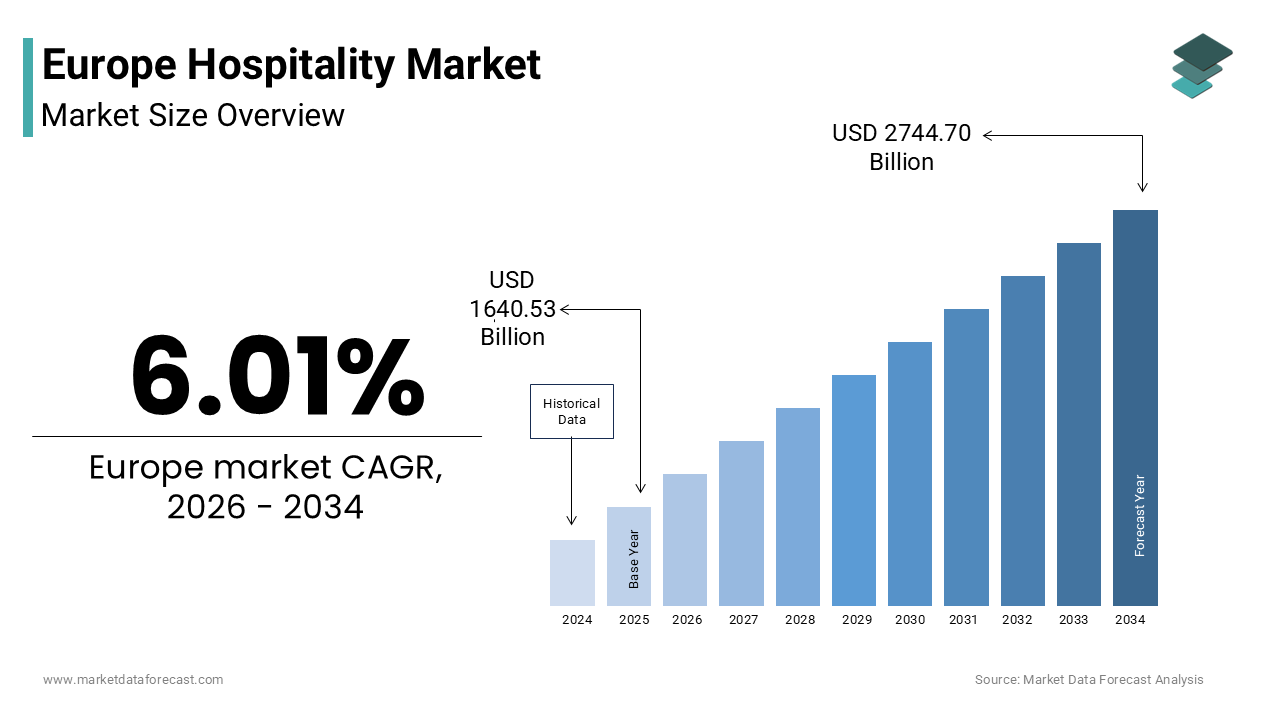

The Europe hospitality market was valued at USD 1640.53 billion in 2025, is estimated to reach USD 1739.23 billion in 2026, and is projected to reach USD 2744.70 billion by 2034, growing at a CAGR of 6.01% during the forecast period from 2026 to 2034. The growth of the Europe hospitality market is driven by the strong recovery of international tourism, increasing cross-border travel demand, and rising consumer interest in cultural and experiential tourism across the region. The presence of diverse cultural heritage sites, well-developed transport infrastructure, and expanding digital travel services is further supporting market growth. Moreover, the integration of advanced technologies such as mobile booking platforms, contactless services, and personalized hospitality experiences is transforming the operational landscape of hotels, restaurants, and event venues across Europe.

Key Market Trends

-

Rising demand for experiential and cultural tourism, where travelers seek authentic local experiences and heritage-based accommodations.

-

Increasing adoption of digital booking platforms and mobile applications for reservations, navigation, and real-time travel services.

-

Growing focus on sustainable hospitality practices, including eco-certified hotels and environmentally responsible tourism initiatives.

-

Expansion of boutique hotels, agritourism properties, and unique accommodation experiences targeting experiential travelers.

-

Increasing integration of smart technologies and AI-driven personalization to enhance guest experiences and operational efficiency.

Segmental Insights

- Based on type, the Food and Beverage Services segment dominated the Europe hospitality market and accounted for the largest share in 2025. The dominance of this segment is attributed to Europe’s strong dining culture, where restaurants, cafés, bars, and quick-service outlets are widely integrated into everyday social and business activities. The popularity of culinary tourism and regional cuisines also contributes significantly to the growth of this segment.

- Based on ownership, the Standalone segment held the largest share of the Europe hospitality market in 2025. This segment’s leadership is driven by the large number of independent and family-owned hotels, boutique properties, and heritage establishments across Europe that offer unique cultural experiences and personalized services. These properties attract travelers seeking authenticity and local charm that large corporate chains often cannot replicate.

Regional Insights

The Europe hospitality market is witnessing strong growth across major countries due to increasing tourism flows, strong domestic travel activity, and the presence of iconic cultural and historical attractions.

-

Germany held the largest share of the Europe hospitality market in 2025, driven by its strong economy, high levels of business travel, and large-scale conferences and exhibitions held in major cities such as Berlin, Frankfurt, and Munich.

-

France continues to be one of the most prominent hospitality markets due to its status as the world’s most visited country and its strong appeal in cultural tourism, gastronomy, and luxury travel.

-

Italy remains a key destination due to its rich cultural heritage, historical landmarks, and growing popularity of agritourism and culinary tourism experiences.

-

Spain is a leading tourism hub driven by its strong sun-and-beach tourism, vibrant nightlife, and increasing urban tourism in cities such as Madrid and Barcelona.

-

The United Kingdom is expected to witness notable growth due to London’s position as a global financial and cultural center and the increasing popularity of heritage tourism across regions such as Scotland and the English countryside.

Competitive Landscape

The Europe hospitality market is highly competitive and fragmented, with a large number of independent hotels competing alongside major global hospitality chains. Large multinational hotel groups leverage their brand recognition, loyalty programs, and technological capabilities to strengthen customer retention and expand their market presence. Meanwhile, independent hotels focus on delivering unique experiences, personalized service, and strong local cultural connections to attract travelers seeking distinctive stays. Leading companies in the Europe hospitality market include Accor, Marriott International, Hilton Worldwide Holdings Inc., InterContinental Hotels Group, Hyatt Hotels Corporation, Meliá Hotels International, Radisson Hotel Group, NH Hotel Group, Whitbread plc, and Louvre Hotels Group.

Europe Hospitality Market Size

The europe hospitality market size was valued at USD 1640.53 billion in 2025 and is anticipated to reach USD 1739.23 billion in 2026 from USD 2744.70 billion by 2034, growing at a CAGR of 6.01% during the forecast period from 2026 to 2034.

Hospitality covers a vast and intricate network of accommodations, food services, and event venues dedicated to hosting travelers and locals alike. This market serves as a critical pillar of the continental economy, blending historical heritage with modern service standards to cater to diverse visitor needs. The landscape is defined by a mix of luxury hotels, boutique establishments, budget chains, and short-term rental properties that adapt to shifting consumer behaviors. As per Eurostat's 2024 business economy report, the accommodation and food services sector employed 10.9 million people across the EU in 2022, representing 6.8% of total employment in the business economy. Furthermore, the European Commission estimates that tourism directly accounts for 4.5% of the EU's total gross value added. When considering the broader "Travel & Tourism" sector (including indirect and induced impacts), the World Travel & Tourism Council notes it contributes approximately 10.5% to the total EU economy. The region benefits from immense cultural diversity. The UNESCO World Heritage List identifies over 500 sites across Europe (with 501 specifically in the Europe region as of 2024), which serve as primary drivers for international arrivals and cultural tourism. Connectivity plays a vital role. According to ACI Europe, European airports welcomed 2.3 billion passengers in 2023, marking a 19% surge from the previous year and reaching nearly 95% of pre-pandemic levels. The market is also increasingly influenced by digital integration. The European Travel Commission highlights that while approximately 55% of travelers now use mobile devices to complete bookings, over 75% of international tourists rely on mobile apps for real-time services, navigation, and on-site activity discovery. Regulatory frameworks regarding safety and sustainability further shape operations, forcing providers to adopt rigorous standards. This dynamic interplay of employment, cultural assets, transport infrastructure, and digital adoption forms the backbone of the contemporary European hospitality ecosystem.

MARKET DRIVERS

Resurgence of International Tourism and Cross-Border Travel Demand

A robust recovery in international tourism is currently boosting the growth of the Europe hospitality market. This growth stems from pent-up demand and the lifting of travel restrictions. After years of disruption, travelers have demonstrated an unwavering desire to explore European destinations, leading to record-breaking arrival numbers in major hubs. As per data from the World Tourism Organization, international tourist arrivals in Europe reached 88% of pre-pandemic levels in 2023 and are projected to surpass 2019 figures by 2024. This surge is fueled by the reopening of Asian markets, particularly China, which historically contributes millions of visitors to European cities annually. Travellers from outside Europe are showing a renewed and growing interest in visiting the continent's major cities and resorts. The removal of health-related entry requirements has simplified logistics, encouraging spontaneous bookings and longer stays. Additionally, the weakening of some currencies against the euro has made certain regions more attractive for specific demographics, balancing flow across the continent. Airlines have aggressively restored capacity, with the International Air Transport Association confirming that seat availability on transatlantic routes exceeded 2019 levels by 10% in the summer of 2023. This influx of global visitors creates immediate occupancy pressure, allowing hospitality providers to increase rates and improve revenue per available room. The return of business travel and large-scale international conferences further amplifies this demand, ensuring a comprehensive recovery across all segments of the market.

Expansion of Experiential and Cultural Tourism Preferences

The evolving consumer preference for immersive experiential and cultural tourism over traditional sightseeing is a major factor shaping the trajectory of the Europe hospitality market. Modern travelers seek authentic interactions with local communities, culinary traditions, and historical narratives, prompting hospitality providers to curate unique stays that go beyond mere accommodation. European tourists are moving away from traditional sightseeing in favour of activities that let them participate in the daily life and traditions of the places they visit. This shift drives demand for boutique hotels, agritourism estates, and heritage properties that can offer personalized and culturally rich environments. The United Nations World Tourism Organization emphasizes that cultural tourism accounts for nearly 40% of all tourism activity in Europe, generating substantial revenue for regions with rich historical assets. Hotels are responding by partnering with local experts to offer exclusive access to museums, private collections, and hidden gems unavailable to the general public. The rise of "bleisure" travel, where business trips are extended for leisure purposes, further fuels this trend as professionals seek meaningful downtime. A majority of corporate travellers in Europe are now extending their work trips into mini-vacations, helping hotels stay full throughout the week. Hospitality operators can command premium pricing and foster strong brand loyalty by catering to this desire for depth and authenticity. In doing so, they distinguish themselves in a crowded marketplace.

MARKET RESTRAINTS

Severe Labor Shortages and Workforce Retention Issues

The acute and persistent shortage of skilled labour across all operational levels is a formidable restraint impeding the full potential and the expansion of the European hospitality market. The sector struggles to attract and retain employees due to perceptions of low wages, demanding working conditions, and limited career progression opportunities, exacerbated by demographic shifts and post-pandemic career changes. As per Eurostat figures from 2023, the accommodation and food service sector faced a vacancy rate of 4.5%, significantly higher than the average for other industries, leaving thousands of positions unfilled. This deficit forces many establishments to reduce operating hours, limit service offerings, or delay expansions despite high demand. The European Hospitality Industry association reported that 75% of hoteliers cite staff shortages as their top challenge, impacting service quality and guest satisfaction. The aging workforce in Western Europe compounds the issue, with fewer young people entering the industry to replace retiring veterans. Furthermore, Brexit has restricted the flow of workers from Eastern Europe to the United Kingdom, creating specific regional crises. The UK hospitality sector has struggled to recover hundreds of thousands of workers who left the industry during the pandemic and subsequent economic shifts. The cost of recruitment and training has skyrocketed as companies compete for a shrinking talent pool, eroding profit margins. Physical capacity cannot be fully utilized without adequate human resources to deliver services. Therefore, without a sustainable pipeline of skilled professionals, the market faces a ceiling on growth.

Escalating Operational Costs and Energy Price Volatility

Rising operational costs are a serious obstacle for the European hospitality market expansion. Volatile energy prices and inflation on essential goods are the main drivers of this trend. The geopolitical instability in Eastern Europe has triggered energy crises that have disproportionately affected energy-intensive sectors like hospitality, which relies heavily on heating, cooling, lighting, and laundry services. As per the European Central Bank, energy prices for industrial and commercial users in the Eurozone surged by over 50% in 2023 compared to previous years, squeezing already thin profit margins. Inflation has also driven up the cost of food, beverages, and linens, forcing operators to either absorb these costs or pass them on to price-sensitive consumers. The Federation of European Hotel Associations noted that utility bills now account for up to 15% of total operating expenses for some properties, a figure that was historically around 5%. Small and independent hotels lack the purchasing power of large chains to negotiate better rates or hedge against price fluctuations, making them vulnerable to insolvency. Additionally, rising interest rates have increased the cost of borrowing for renovations and expansions, stalling investment projects. According to data from the International Monetary Fund, inflation in several European countries remained in double digits during parts of 2023, further dampening consumer spending power. These cumulative financial pressures create a precarious environment where maintaining profitability becomes increasingly difficult, acting as a severe brake on market expansion and modernization efforts.

MARKET OPPORTUNITIES

Integration of Sustainable Practices and Eco-Certification

The widespread adoption of sustainable practices and eco-certifications is a paramount opportunity for the European hospitality market. These initiatives align with the growing environmental consciousness of modern travelers. European consumers are increasingly prioritizing green credentials when choosing accommodations, creating a lucrative niche for operators who can demonstrate genuine commitment to sustainability. As per sources, a clear majority of European travellers now consider the planet's health when picking a destination, though many still struggle with the higher costs of going green. This trend drives demand for hotels that implement energy-efficient systems, waste reduction programs, and locally sourced food options. The European Union's Green Deal provides a framework and funding opportunities for businesses to transition toward carbon neutrality, offering a competitive edge to early adopters. Younger travellers are specifically seeking out hotels with official "green" credentials and are increasingly ignoring those that don't show a commitment to the environment. Operators can leverage this by obtaining recognized labels such as the EU Ecolabel or Green Key, which serve as trust signals for conscious consumers. Furthermore, sustainability initiatives often lead to long-term cost savings through reduced energy and water consumption. The rise of regenerative tourism, where visitors actively contribute to local environmental restoration, opens new revenue streams for hotels offering curated green experiences. Hospitality providers can attract a loyal customer base and enhance their brand reputation by embedding sustainability into their core operations. This strategic shift also future-proofs their businesses against tightening regulatory requirements.

Adoption of Advanced Digital Technologies and Personalization

The burgeoning integration of advanced digital technologies paves the way for the expansion of the Europe hospitality market. This shift will allow businesses to enhance operational efficiency and deliver hyper-personalized guest experiences. From artificial intelligence-driven concierge services to contactless check-in systems, technology enables providers to streamline operations and cater to individual preferences at scale. Most people now expect hotels to remember their past visits and specific likes, feeling disappointed if they are treated like a stranger every time they check in. Hotels leveraging customer relationship management systems and AI algorithms can tailor room settings, dining recommendations, and activity suggestions to each guest, significantly boosting satisfaction and loyalty. Hotels that make it easy to book and check in via a smartphone are successfully convincing guests to bypass big travel websites and book with them directly. Mobile apps allow guests to control room features, order services, and communicate with staff instantly, enhancing convenience and safety. Furthermore, predictive analytics help operators optimize pricing strategies and inventory management in real time, maximizing revenue during peak periods. The adoption of Internet of Things devices enables smart energy management, contributing to sustainability goals while lowering costs. Hospitality businesses can differentiate themselves in a competitive market by embracing these technological advancements. This allows them to offer superior service levels that meet the high expectations of the digital-native traveler.

MARKET CHALLENGES

Geopolitical Instability and Security Concerns

The escalating geopolitical instability and heightened security concerns are limiting the growth of the Europe hospitality market. These factors disrupt travel patterns and dampen consumer confidence. Ongoing conflicts in Eastern Europe and tensions in neighboring regions have created an atmosphere of uncertainty, causing travelers to reconsider plans or avoid certain destinations perceived as risky. As per sources, geopolitical shocks have led to a redirection of tourist flows, with some traditional hotspots experiencing sharp declines in arrivals while others face overcrowding. The threat of terrorism, although statistically low, remains a psychological barrier that influences travel insurance costs and government advisories. According to sources, security threats require constant vigilance and investment in protective measures, adding to operational burdens for hotels and venues. Political unrest in various countries has occasionally led to protests and strikes that disrupt transportation and deter visitors. The volatility of currency exchange rates linked to geopolitical events further complicates financial planning for both operators and international tourists. The need for enhanced security screening and surveillance increases costs and can impact the guest experience by creating friction. This pervasive sense of unpredictability makes long-term forecasting difficult and forces stakeholders to remain agile, often at the expense of strategic growth initiatives.

Regulatory Complexity and Compliance Burdens

The relentless pace of regulatory change and the complexity of compliance requirements pose a significant challenge to the Europe hospitality market. This creates administrative hurdles and financial strain for operators. The region is governed by a dense web of laws covering data privacy, labor rights, health and safety, and environmental standards, which vary significantly between member states. Frequent updates to labor laws, such as minimum wage increases and working time directives, force continuous adjustments to payroll and scheduling systems. The European Commission's push for stricter environmental regulations mandates costly upgrades to building infrastructure and waste management processes. The fragmentation of rules across borders complicates operations for chains expanding into new countries, requiring localized legal expertise for each jurisdiction. The introduction of digital reporting obligations and tax compliance measures adds another layer of complexity. Failure to adhere to these evolving standards can result in severe penalties, reputational damage, and even closure. This regulatory burden acts as a drag on innovation and agility, particularly for smaller players who lack the resources to maintain dedicated compliance teams.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.01% |

| Segments Covered | By Type, Ownership and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Accor, Marriott International, Hilton Worldwide Holdings Inc., InterContinental Hotels Group, Hyatt Hotels Corporation, Meliá Hotels International, Radisson Hotel Group, NH Hotel Group, Whitbread plc, and Louvre Hotels Group. |

SEGMENTAL ANALYSIS

By Type Insights

The Food And Beverage Services segment dominated the Europe hospitality market and captured a 58.3% share in 2025. This supremacy of the segment is driven by the fundamental role that dining plays in European culture, where food consumption outside the home is a daily ritual rather than a occasional luxury. The segment includes a vast array of establishments ranging from quick service restaurants and cafes to fine dining venues and bars, all contributing to a robust revenue stream that often exceeds accommodation spending in urban centers. Apart from these, the primary driver sustaining the dominance of the Food And Beverage Services segment is the deeply ingrained European cultural tradition of socializing over meals and beverages. Unlike regions where dining out is reserved for special occasions, Europeans frequently visit restaurants and cafes for daily meals, business meetings, and social gatherings. As per data from Eurostat, households in the European Union spent an average of 9% of their total consumption expenditure on restaurants and hotels in 2023, with the majority allocated to food and drink services. This habitual behavior ensures a consistent and high-volume demand regardless of seasonal tourism fluctuations. The Mediterranean diet and the café culture of Central Europe further reinforce this trend, with countries like Italy, Spain, and France boasting some of the highest densities of eateries per capita globally. Most Europeans now view eating out as an occasional social event rather than a weekly habit, often choosing home-cooked meals for daily sustenance. The diversity of regional cuisines attracts both locals and tourists, creating a resilient market that thrives on authenticity and quality. Furthermore, the rise of food tourism, where travelers plan trips specifically around culinary experiences, has amplified revenue potential. The sector benefits from the fact that food is a non-discretionary need that has evolved into a discretionary experience, allowing operators to capture value across various price points from street food to Michelin-starred establishments. One more point that adds strength is the rapid expansion and adaptation of quick service and casual dining formats that cater to the fast-paced modern lifestyle. Urbanization and changing work patterns have increased the demand for convenient, affordable, and high-quality meal options that can be consumed quickly or on the go. Fast food is becoming the preferred choice for busy urban residents because it offers a reliable and affordable alternative to traditional sit-down dining. The integration of technology such as self-service kiosks, mobile ordering, and delivery apps has streamlined operations, allowing these establishments to serve higher volumes of customers with reduced labor costs. Smartphone apps are fundamentally changing how Europeans access food, with more people than ever choosing to have restaurant meals delivered directly to their doors. These formats appeal to a broad demographic, including students, young professionals, and families, who seek value and convenience. The flexibility of these models allows them to operate in diverse locations from transport hubs to shopping malls, maximizing visibility and accessibility. Additionally, the continuous innovation in menu offerings, including healthy and plant-based options, keeps these formats relevant to health-conscious consumers. The scalability of quick service and casual dining chains enables them to capture significant market share, driving the overall dominance of the food and beverage segment in the hospitality landscape.

The Non-Residential Accommodation Services segment is estimated to register the fastest CAGR of 7.8% from 2026 to 2034 due to the strong rebound in international tourism, the rising popularity of alternative accommodation types, and the increasing demand for experiential stays that offer more than just a place to sleep. A major factor for the rapid expansion of the Non-Residential Accommodation Services segment is the vigorous recovery and subsequent growth of international leisure and business travel across the continent. After a period of significant disruption, pent-up demand has led to a surge in bookings, with arrival numbers in many European destinations surpassing pre-pandemic levels. As per the World Tourism Organization, international tourist arrivals in Europe reached 95% of 2019 levels in 2024, driving unprecedented occupancy rates for hotels and alternative accommodations. The resurgence of long-haul travel from key markets like the United States and Asia has been particularly beneficial for major city centers and resort destinations. Airlines are aggressively adding more flights between North America and Europe to keep up with the record-breaking number of people crossing the Atlantic. Furthermore, the return of large-scale conferences, exhibitions, and corporate events has revitalized the business travel segment, which typically commands higher average daily rates. Companies are approving more trips to close deals and meet clients in person, though they remain cautious about total spending due to rising costs. The trend of "bleisure" travel, where business trips are extended for leisure, further extends stay durations and increases revenue per guest. This dual engine of leisure and business travel creates a powerful momentum for the accommodation sector, driving its growth rate higher than other hospitality segments. Added support for this segment comes from the explosive popularity of alternative accommodations and short-term rentals, which have reshaped the lodging landscape. Travelers increasingly seek unique, localized, and spacious living arrangements that traditional hotels often cannot provide, leading to a surge in demand for vacation rentals, aparthotels, and boutique guesthouses. Travelers are increasingly escaping overcrowded cities to discover quieter, rural communities through online rental platforms. This shift is driven by the desire for authentic experiences and the practical benefits of kitchen facilities and multiple bedrooms for families and groups. The regulatory environment in many European countries has evolved to accommodate this sector, providing clarity and legitimacy to professional hosts. Although vacation rentals are booming, most tourists in Europe's most famous cities still choose to stay in traditional hotels. The diversification of accommodation types allows the segment to cater to a wider range of budgets and preferences, from budget-conscious backpackers to luxury seekers. The integration of professional management companies has also improved the quality and reliability of these rentals, making them a viable alternative for business travelers. This expansion of supply and variety fuels the rapid growth of the accommodation segment, capturing market share from traditional models and attracting new demographics.

By Ownership Insights

The Standalone ownership segment led the Europe hospitality market and accounted for a 62.4% share in 2025. The foremost driver behind the supremacy of the Standalone segment is the deep-rooted tradition of family-owned heritage properties and boutique hotels that define the character of European hospitality. This dominance is a reflection of the fragmented nature of the European industry, where independent owners, family-run businesses, and boutique operators prevail over large corporate chains, particularly in the rural and heritage-rich regions of the continent. Many of these establishments have been operated by the same families for generations, offering unique architectural features, personalized service, and a sense of history that large chains struggle to replicate. As per research, a notable share of historic hotels and spas in Europe are independently owned, preserving local traditions and craftsmanship. These properties attract travelers seeking authentic and distinctive experiences, often commanding premium prices due to their exclusivity and charm. The flexibility of standalone owners allows them to adapt quickly to local trends and guest preferences without the constraints of corporate standardization. Furthermore, government initiatives in many European countries support small and medium-sized enterprises in the tourism sector, providing grants and tax incentives that help these businesses thrive. The emotional connection guests feel towards these unique properties fosters strong loyalty and positive word-of-mouth marketing. The sheer number of these independent entities across the vast geography of Europe, from coastal villages to mountain retreats, ensures that the standalone segment remains the numerical leader in the market. This segment is also shaped by the exceptional agility of independent operators in adapting to local market conditions and targeting niche customer segments effectively. Unlike chained competitors that must adhere to rigid brand standards and centralized decision-making processes, standalone owners can pivot their strategies rapidly to meet emerging demands. As per a study, independent hospitality businesses are faster in implementing new sustainability practices or digital tools compared to large chains. This responsiveness allows them to capitalize on local events, festivals, and seasonal trends that might be overlooked by broader corporate strategies. They can tailor their offerings to specific niches such as eco-tourism, wellness retreats, or culinary tourism, creating specialized experiences that attract dedicated followings. The ability to build direct relationships with local suppliers and communities enhances their value proposition and reduces costs. Furthermore, standalone operators often leverage personal networks and local knowledge to offer curated recommendations and services that enhance the guest experience. This hyper-local focus and operational flexibility enable them to compete effectively despite limited marketing budgets, securing their dominant position in the diverse European landscape.

The Chained ownership segment is anticipated to witness the fastest CAGR of 6.5% during the forecast period owing to aggressive expansion strategies of international and regional hotel groups, the increasing demand for standardized quality and loyalty benefits, and the consolidation of the market through acquisitions and management contracts. The biggest reason for the rapid growth of the Chained segment is the aggressive expansion strategies employed by major hotel groups that leverage economies of scale to open new properties and acquire existing independents. These chains offer a promise of consistent quality, safety standards, and reliable service that appeals to both leisure and business travelers who seek predictability in their stays. The ability to implement rigorous quality assurance protocols across all locations builds trust and brand equity, driving repeat bookings. The standardization of amenities, from Wi-Fi speeds to bed quality, ensures that guests know exactly what to expect, reducing the perceived risk of travel. Furthermore, chains benefit from centralized procurement systems that lower operational costs for food, linens, and technology, allowing them to invest more in property upgrades and marketing. The rollout of new mid-scale and economy brands specifically designed for the European market has expanded their reach to cost-conscious travelers. This systematic approach to growth and quality control enables chains to capture significant market share rapidly, outpacing the organic growth rates of standalone competitors. A further key driver propelling the swift expansion of the Chained segment is the immense power of integrated loyalty programs and sophisticated digital ecosystems that drive direct bookings and customer retention. Major hotel chains operate global loyalty schemes with millions of members who are incentivized to stay within the brand family to earn points and redeem rewards. These programs are supported by advanced mobile apps that allow seamless booking, check-in, and service requests, creating a frictionless customer journey. The accumulation of big data from these interactions enables chains to personalize offers and optimize pricing dynamically, maximizing revenue management efficiency. The integration of these digital tools with corporate travel policies makes chains the preferred choice for business travelers whose companies mandate preferred vendor usage. The ability to cross-sell services such as dining, spa, and meetings within the ecosystem further enhances profitability. This technological and relational advantage creates a sticky customer base that fuels the rapid growth of the chained segment, making it the most dynamic force in the European hospitality market.

REGIONAL ANALYSIS

Germany Hospitality Market Analysis

Germany was the top performer in the Europe hospitality market and occupied a share of 21.5% in 2025. The dominance of the German hospitality market is primarily fueled by its status as Europe's largest economy, which generates immense volume of business travel and MICE (Meetings Incentives Conferences and Exhibitions) activity. Notably, this area has its powerful economic engine, which drives substantial business travel, coupled with a strong domestic tourism sector that relies heavily on a diverse mix of city breaks and rural holidays. Cities like Frankfurt, Munich, and Berlin serve as global hubs for trade fairs and corporate headquarters, ensuring year-round occupancy for business hotels. Furthermore, the strong purchasing power of the German population supports a vibrant domestic tourism market, with Germans taking millions of holiday trips within their own borders annually. The country's extensive network of well-maintained infrastructure, including highways and railways, facilitates easy access to various regions, from the Bavarian Alps to the North Sea coast. The presence of a highly organized system of classification and quality standards ensures a reliable experience for guests, fostering trust and repeat visits. Additionally, the growing trend of sustainable tourism aligns well with German consumer values, driving demand for eco-certified hotels and green travel options. The combination of robust business demand, strong domestic travel, and high-quality infrastructure cements Germany's position as the undisputed leader in the European hospitality landscape.

France Hospitality Market Analysis

France followed closely in the Europe hospitality market and accounted for a share of 19.6% in 2025. The growth of the French hospitality market is propelled by its unparalleled cultural assets and global brand appeal that attract millions of international visitors annually. It is distinguished by its status as the world's most visited country and a global beacon of culture, gastronomy, and luxury. The market status in France shows a heavy reliance on international leisure tourism, particularly in Paris and the French Riviera, alongside a thriving rural hospitality sector. Paris draws millions of tourists each year, creating immense demand for accommodation and dining services across all price points. As per sources, France welcomed millions of international visitors in 2023, setting a new record and reinforcing its top global position. The country's reputation for haute cuisine and wine tourism further enhances its allure, with gastronomic experiences being a primary motivator for travel. The existence of numerous UNESCO World Heritage Sites in France provides a dense network of attractions that distribute tourist flows beyond the capital to regions like Provence, Normandy, and the Loire Valley. The luxury segment in France is particularly strong, with the country hosting some of the world's most prestigious palace hotels that command ultra-premium rates. Government support for tourism infrastructure and promotion through Atout France ensures sustained visibility in key source markets. The blend of iconic landmarks, culinary excellence, and diverse landscapes creates a resilient and high-value market that maintains France's position as a premier hospitality destination in Europe.

Italy Hospitality Market Analysis

Italy plays a key role in the Europe hospitality market due to its rich historical and artistic legacy that serves as a magnet for cultural tourists from around the globe. The Italian market is also driven by its unique combination of historical heritage, artistic treasures, and coastal beauty, which drives a balanced mix of cultural tourism and sun-and-sea holidays throughout the year. Cities like Rome, Florence, and Venice are perennial favorites, offering an unmatched density of monuments, museums, and archaeological sites. The country's extensive coastline and islands, including Sicily and Sardinia, drive a robust summer season that complements the year-round cultural traffic. The concept of "slow tourism" and agritourism has gained significant traction, with travelers increasingly seeking authentic experiences in rural Tuscany and Umbria. The culinary reputation of Italy, recognized globally, acts as a major pull factor, with food and wine tours becoming increasingly popular. The government's investment in restoring historical properties and converting them into boutique hotels adds unique inventory to the market. The favorable climate allows for an extended tourist season, reducing the impact of winter lows in southern regions. This synergy of culture, nature, and gastronomy ensures Italy remains a cornerstone of the European hospitality industry.

Spain Hospitality Market Analysis

Spain showed steady growth in the Europe hospitality market owing to its status as a premier sun-and-beach destination that attracts millions of Northern European tourists seeking sunshine and relaxation. It is also supported by its dominance in the sun-and-beach tourism segment, vibrant nightlife, and increasingly popular urban cultural destinations. The region has high seasonality in coastal areas but a growing trend of year-round tourism in major cities like Madrid and Barcelona. The Costa del Sol, Balearic Islands, and Canary Islands are iconic brands in themselves, driving massive occupancy during the summer and winter months respectively. The country's well-developed resort infrastructure, ranging from all-inclusive complexes to luxury villas, caters to a wide demographic. Beyond the coast, urban tourism has surged, with Madrid and Barcelona becoming top destinations for city breaks, art lovers, and business travelers. The proliferation of low-cost airlines has made Spain highly accessible, increasing visitor numbers from key European markets. The emergence of gastronomic tourism, bolstered by numerous Michelin-starred restaurants, has diversified the appeal beyond beach holidays. Government initiatives to promote sustainable tourism and de-seasonalize demand are helping to stabilize revenues throughout the year. This combination of natural assets, infrastructure, and strategic marketing secures Spain's place as a top hospitality market in Europe.

United Kingdom Hospitality Market Analysis

The United Kingdom is anticipated to expand notably in the Europe hospitality market during the forecast period. The prominence of the United Kingdom in the hospitality landscape is largely attributed to London's status as a global powerhouse that draws high-spending business and leisure travelers from every corner of the world. In addition, the UK market status is defined by the global appeal of London as a financial and cultural capital, complemented by a strong domestic tourism sector and a growing interest in heritage and countryside experiences across Scotland, Wales, and England. The city hosts major international events, financial summits, and West End theater productions that drive consistent demand for premium accommodation and dining. Beyond the capital, the UK benefits from a strong domestic tourism market, with residents exploring the scenic landscapes of the Lake District, the Scottish Highlands, and the Cornish coast. The heritage sector, including castles, stately homes, and literary landmarks, offers unique selling propositions that attract cultural tourists. The rise of "staycations" post-pandemic has further bolstered regional markets, as travelers opt for local getaways. The diversity of offerings, from historic pubs and boutique hotels to modern serviced apartments, caters to varied tastes. Despite challenges related to labor shortages and Brexit impacts, the underlying demand driven by the strength of the pound in certain periods and the global brand of British culture ensures the UK remains a key player in the European hospitality arena.

COMPETITIVE LANDSCAPE

The competition within the Europe hospitality market is intensely fragmented and characterized by a fierce rivalry between global multinational chains and a vast number of independent local operators. Global brands leverage their immense financial resources and standardized operating procedures to secure prime locations and deploy advanced technology for seamless customer experiences. Conversely, independent hotels compete by offering unique atmospheres, personalized service, and deep local cultural connections that large corporations often struggle to replicate. The market sees constant innovation as players introduce novel concepts such as lifestyle hotels and co-living spaces to differentiate themselves. Price competition varies by segment with budget chains fighting on cost while luxury providers compete on exclusivity and service quality. The rise of short-term rental platforms has further intensified the battle for market share by offering alternative accommodation options. Regional differences in travel preferences require operators to adapt their offerings locally while maintaining brand consistency. The war for skilled talent is also significant as experienced staff become essential assets for delivering superior service. This dynamic environment forces all participants to continuously evolve their strategies and operational models to survive and thrive in a saturated landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Hospitality Market include

- Accor

- Marriott International

- Hilton Worldwide Holdings Inc.

- InterContinental Hotels Group

- Hyatt Hotels Corporation

- Meliá Hotels International

- Radisson Hotel Group

- NH Hotel Group

- Whitbread plc

- Louvre Hotels Group

Top Players in the Europe Hospitality Market

Accor S.A.

Accor S.A. stands as a global hospitality leader with French origins and a massive portfolio spanning luxury, premium, midscale, and economy segments across Europe. The company contributes significantly to the global market by pioneering lifestyle brands and integrating digital services into the guest journey. In Europe, Accor has recently strengthened its position by acquiring distinct boutique hotel groups to diversify its offerings in key cities like Paris and Berlin. The firm is aggressively expanding its loyalty program, ALL, to create a seamless ecosystem for travelers. Accor also focuses on sustainability by committing to net zero emissions and eliminating single-use plastics in all properties. Their strategic partnerships with entertainment and sports entities drive brand visibility. Accor is expanding its European footprint by converting existing buildings and launching new soft brands, avoiding heavy capital expenditure. This strategy ensures the company remains resilient and adaptable in a dynamic market.

InterContinental Hotels Group PLC

InterContinental Hotels Group PLC operates as a British multinational hospitality company that manages some of the most recognized hotel brands globally including InterContinental, Crowne Plaza, and Holiday Inn. The group contributes to the international market through an asset-light business model that focuses on franchising and management contracts rather than ownership. In Europe, IHG has recently accelerated its growth by signing hundreds of new deals in emerging markets and secondary cities to capture untapped demand. The company is strengthening its market position by investing heavily in digital transformation, including mobile check-in and keyless entry systems. IHG also launched enhanced sustainability standards requiring all new hotels to meet rigorous environmental criteria. Their focus on expanding the midscale and extended stay segments addresses the changing needs of modern travelers. IHG leverages data analytics to optimize revenue management and improve guest personalization. This strategy allows the company to maintain a competitive edge and drive consistent performance across its diverse European portfolio.

Marriott International Inc.

Marriott International Inc. is an American multinational giant that operates a vast array of luxury and premium hotel brands throughout Europe, contributing immensely to the global hospitality standards. The company is renowned for its industry-leading loyalty program, Marriott Bonvoy, which drives direct bookings and customer retention worldwide. In Europe, Marriott has recently strengthened its presence by converting historic landmarks into luxury properties and expanding its select-service brands in high-growth regions. The firm is actively pursuing sustainability goals by reducing water usage and carbon emissions across all managed properties. Marriott also invests in technology to enhance the guest experience through contactless services and personalized mobile interactions. Their strategy involves forming strategic alliances with airlines and credit card companies to expand reach. By focusing on high-end luxury and distinctive collections, Marriott caters to affluent travelers seeking unique experiences. These initiatives ensure the company remains a dominant force in the European market while setting benchmarks for service excellence and operational efficiency globally.

Top Strategies Used by Key Market Participants

Key players in the Europe hospitality market primarily employ asset-light expansion strategies that prioritize franchising and management contracts over property ownership to minimize capital risk. Companies frequently pursue mergers and acquisitions of boutique brands to diversify their portfolios and capture niche market segments. Another major strategy involves heavy investment in digital transformation including mobile apps and artificial intelligence to personalize guest experiences and streamline operations. Operators are increasingly implementing comprehensive sustainability programs to meet environmental regulations and attract eco-conscious travelers. Loyalty program enhancement serves as a critical tool to drive direct bookings and reduce reliance on third-party distribution channels. Firms also focus on converting existing commercial or residential buildings into hotels to accelerate growth in urban centers. Strategic partnerships with technology providers and local businesses help create integrated ecosystems that offer added value to guests. These combined approaches enable market leaders to scale efficiently and adapt to evolving consumer demands.

MARKET SEGMENTATION

This research report on the Europe Hospitality Market has been segmented and sub-segmented based on the following categories.

By Type

- Non-Residential Accommodation Services

- Food and Beverage Services

By Ownership

- Chained

- Standalone

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com