Europe Infrared Detector Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, Application And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Infrared Detector Market Size

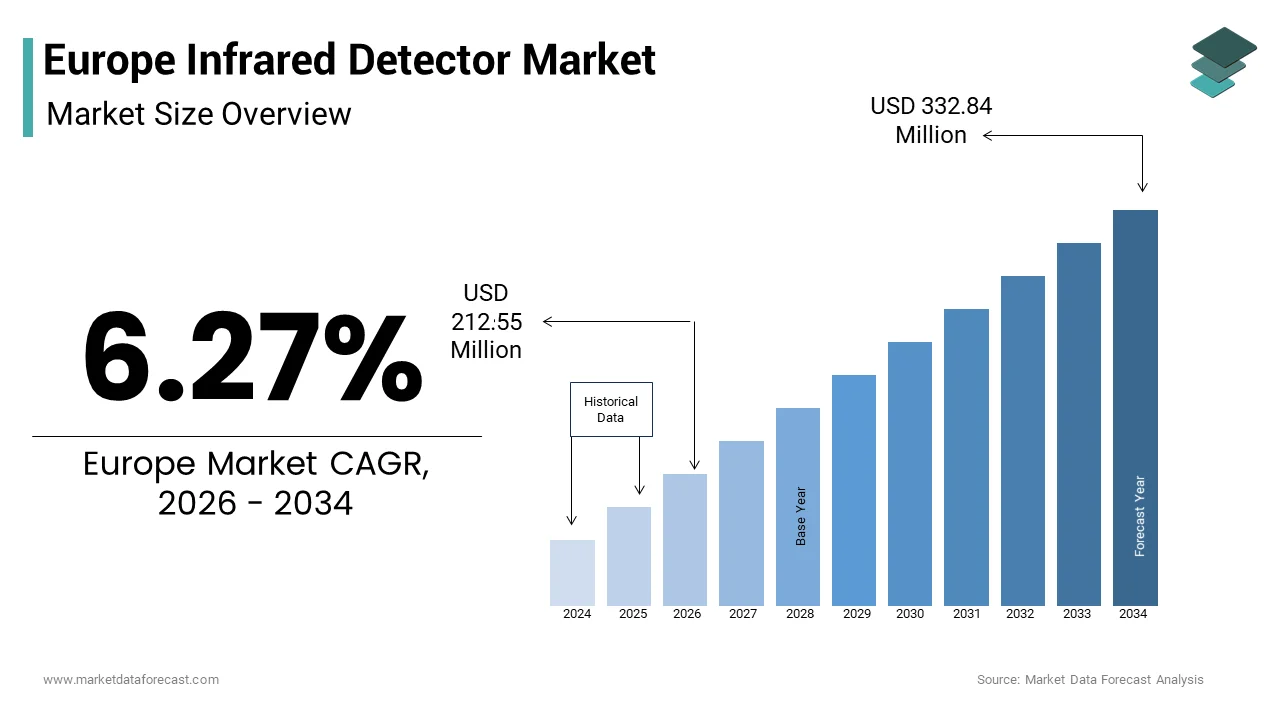

The Europe infrared detector market size was valued at USD 199.98 million in 2025 and is anticipated to reach USD 212.55 million in 2026 to reach USD 332.84 million by 2034, growing at a CAGR of 6.27% during the forecast period from 2026 to 2034.

Introduction to the Europe Infrared Detector Market

The infrared detector is the development and deployment of sensors that convert infrared radiation into electrical signals for thermal imaging and spectroscopic analysis. These devices are integral to defense systems industrial automation medical diagnostics and automotive safety applications across the continent. The strategic significance of this technology is underscored by its role in enhancing situational awareness and operational efficiency. This substantial financial commitment reflects the region's focus on security and technological sovereignty. Furthermore, the European Defence Agency stated in its 2024 capability development plan that over 60% of member states prioritized the acquisition of next generation surveillance systems. This demand drives innovation in uncooled and cooled infrared detector technologies. The widespread adoption of Industry 4.0 principles has also accelerated the integration of infrared sensors in predictive maintenance solutions. According to the International Federation of Robotics the number of industrial robots installed in Europe reached 75000 units in 2024 many of which incorporate thermal vision for quality control. This convergence of robotics and thermal sensing creates a robust ecosystem for detector manufacturers. Additionally the increasing prevalence of electric vehicles necessitates advanced battery monitoring systems where infrared detectors play a critical role in preventing thermal runaway. These diverse applications ensure sustained relevance and growth potential for the infrared detector sector within the European technological landscape.

MARKET DRIVERS

Escalating Defense Expenditures Fuel Demand for Advanced Surveillance Systems

The rising geopolitical tensions and the need for enhanced border security have led to significant increases in defense budgets, thereby driving the demand for sophisticated infrared detectors. The escalating defense expenditures is majorly escalating the growth of Europe infrared detector market. These sensors are essential components in night vision goggles missile guidance systems and unmanned aerial vehicles, which are for modern military operations. This surge in funding directly translates into procurement contracts for advanced electro optical systems that rely on high performance infrared detectors. NATO members are specifically focusing on improving their surveillance capabilities to monitor eastern borders and maritime zones. In France, the Directorate General of Armaments announced a multi year program to upgrade its ground based surveillance networks with thermal imaging capabilities. This initiative requires thousands of high resolution infrared detectors capable of operating in harsh environmental conditions. Similarly, Germany’s Bundeswehr has initiated a modernization plan that includes the deployment of new reconnaissance drones equipped with cooled infrared sensors. The urgency to replace aging equipment with state of the art technology ensures a steady stream of orders for detector manufacturers. Furthermore, the development of autonomous defense systems relies heavily on real time thermal data processing. This strategic imperative compels governments to invest in domestic production capabilities reducing reliance on non European suppliers and fostering a resilient supply chain for critical defense components.

Expansion of Automotive Safety Regulations Mandates Thermal Vision Integration

The stringent safety regulations and the push toward autonomous driving features are compelling automotive manufacturers to integrate infrared detectors into vehicle systems, which is also levelling up the growth of Europe infrared detector market. Thermal cameras provide superior visibility in low light and adverse weather conditions compared to visible light sensors making them indispensable for advanced driver assistance systems. As per the European Commission, new vehicle safety standards implemented in 2024 require all new car models to include enhanced pedestrian detection capabilities. Infrared detectors enable accurate identification of living beings even in complete darkness thereby reducing accident rates. The European New Car Assessment Programme reported that vehicles equipped with thermal vision systems demonstrated a 40% improvement in nighttime pedestrian detection scores during 2025 testing protocols. Major automakers, such as BMW and Mercedes Benz are increasingly incorporating thermal cameras into their premium vehicle lines to meet these higher safety benchmarks. In Sweden, Volvo Cars announced that all its upcoming electric models will feature standard thermal imaging for collision avoidance. This trend is driven by the need to achieve zero fatality goals outlined in national road safety strategies. Additionally the rise of electric vehicles has created a specific demand for infrared sensors to monitor battery temperatures. Thermal runaway in lithium ion batteries poses a significant safety risk which infrared detectors can mitigate through early warning systems. According to the European Automobile Manufacturers Association, over 3 million electric vehicles sold in Europe in 2025 included battery thermal management systems utilizing infrared technology. This regulatory and technological convergence creates a robust growth trajectory for infrared detectors in the automotive sector.

MARKET RESTRAINTS

High Production Costs of Cooled Detectors Limit Mass Market Adoption

The substantial manufacturing costs associated with cooled infrared detectors serve with their widespread adoption in cost sensitive applications is limiting the growth of Europe infrared detector market. Cooled detectors require complex cryogenic cooling mechanisms to reduce thermal noise and achieve high sensitivity, which significantly increases production complexity and expense. According to the European Semiconductor Industry Association, the average cost of a cooled infrared focal plane array remains five times higher than that of uncooled microbolometers. This price disparity restricts the use of cooled detectors primarily to high end military and scientific applications where performance justifies the investment. Small and medium sized enterprises in the industrial sector often find the return on investment insufficient for deploying such expensive sensors for routine monitoring tasks. The reliance on rare materials such as mercury cadmium telluride further exacerbates cost issues and supply chain vulnerabilities. Fluctuations in raw material prices can lead to unpredictable manufacturing expenses affecting overall profitability. Additionally, the maintenance requirements for cooled systems including periodic recalibration and cooler replacement add to the total cost of ownership. These financial barriers hinder the expansion of infrared technology into broader commercial markets such as consumer electronics and affordable home security systems.

Strict Export Controls on Dual Use Technologies Restrict Global Reach

The stringent export controls on dual use technologies on the ability of European infrared detector manufacturers to access globally is also impeding the growth of Europe infrared detector market. Infrared sensors are classified as sensitive items due to their military applications leading to rigorous licensing requirements and trade restrictions. According to the European Commission, over 200 export license applications for electro optical components were denied or delayed in 2025 due to national security concerns. These bureaucratic hurdles increase lead times and create uncertainty for international customers discouraging long term contracts. Companies must navigate a complex web of regulations that vary between member states and destination countries. In Germany, the Federal Office for Economic Affairs and Export Control reported that compliance costs for dual use exports increased by 25% in 2024. This administrative burden disproportionately affects smaller manufacturers who lack dedicated legal resources. Furthermore, geopolitical tensions have led to tighter restrictions on technology transfers to certain regions limiting potential growth opportunities. The United States and other allies have also imposed reciprocal controls creating a fragmented global trade environment. This protectionist trend forces European companies to focus primarily on the domestic market which may not offer sufficient scale to sustain high levels of research and development investment. The inability to freely compete in emerging markets such as Asia and the Middle East restricts revenue potential.

MARKET OPPORTUNITIES

Integration with Artificial Intelligence Enhances Predictive Maintenance Capabilities

The integration of infrared detectors with artificial intelligence algorithms for transforming industrial maintenance practices is certainly creating new opportunities for the growth of Europe infrared detector market. AI powered thermal imaging systems can analyze vast amounts of temperature data to predict equipment failures before they occur reducing downtime and maintenance costs. According to the European Institute of Innovation and Technology the adoption of AI driven predictive maintenance solutions increased by 35% in the manufacturing sector in 2025. Infrared detectors provide the thermal data required for these algorithms to identify anomalies, such as overheating bearings or electrical faults. In the Netherlands, Philips and other tech firms are developing smart factory solutions that combine thermal sensors with machine learning models. These systems enable real time monitoring of production lines ensuring optimal operational efficiency. The energy sector is also leveraging this technology to inspect power grids and wind turbines. The efficiency gain translates into substantial cost savings and improved reliability. The growing emphasis on industrial digitalization under Industry 4.0 initiatives further supports this trend. Governments are providing grants for companies to adopt smart technologies enhancing the business case for infrared sensor integration. As AI models become more sophisticated the accuracy of fault prediction improves making infrared detectors an essential component of modern industrial infrastructure. This synergy between hardware and software opens new revenue streams for detector manufacturers and service providers.

Growing Demand for Energy Efficient Building Inspections Drives Commercial Use

The increasing focus on energy efficiency and sustainability in the construction sector is driving demand for infrared detectors in building inspections and audits, which is also to enhance the growth of the Europe infrared detectors market. Thermal imaging allows for the identification of heat leaks insulation defects and moisture intrusion which are critical for reducing energy consumption. According to the European Performance of Buildings Directive, all member states must ensure that buildings achieve higher energy performance standards by 2030. This regulatory pressure has led to a surge in professional energy audits where infrared cameras are indispensable tools. In France, the Agency for Ecological Transition reported that over 100000 residential buildings underwent thermal inspections in 2025 to qualify for renovation subsidies. Professional inspectors rely on high resolution infrared detectors to produce accurate thermal maps that guide retrofitting efforts. The commercial real estate sector is also adopting this technology to enhance property value and comply with environmental certifications. In the United Kingdom the Royal Institution of Chartered Surveyors noted that thermal imaging surveys became standard practice for commercial property assessments in 2024. This trend is supported by the availability of portable and user-friendly infrared cameras that lower the barrier to entry for smaller inspection firms. The push for net zero emissions further incentivizes building owners to invest in energy efficiency measures. Infrared detectors provide the visual evidence needed to justify these investments and track improvement progress. This expanding application area offers substantial growth potential for manufacturers targeting the construction and facility management sectors.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Critical Raw Materials Pose Production Risks

The reliance on raw materials for infrared detector production creates significant supply chain vulnerabilities that threaten manufacturing stability, which is a major challenge for the growth of Europe infrared detector market. Materials such as indium gallium arsenide and vanadium oxide are essential for fabricating high performance sensors but are sourced from a limited number of suppliers globally. According to the European Raw Materials Alliance, the supply risk for indium was rated as high in 2025 due to geopolitical concentrations in production. Disruptions in these supply chains can lead to shortages and price spikes affecting the availability of infrared detectors. In Belgium, specialized infrared sensor substrates extended to 20 weeks in 2024. This delay hampers the ability of manufacturers to meet customer demand and fulfill contracts on time. Diversifying supply sources is challenging due to the specialized nature of these materials and the high barriers to entry for new producers. Additionally, trade tensions and export restrictions on raw materials further complicate procurement strategies. European manufacturers are exploring recycling and alternative materials but these solutions are not yet commercially viable at scale. The lack of domestic production capacity for key raw materials leaves the industry exposed to external shocks. This structural weakness requires strategic interventions such as stockpiling and international partnerships to mitigate risks. r growth and innovation.

Shortage of Skilled Technicians Limits Deployment and Maintenance Efficiency

A shortage of skilled technicians capable of operating and maintaining advanced infrared detection systems is ascribed to hinder the growth of Europe infrared detector market in coming years. The interpretation of thermal images requires specialized knowledge and training which is currently in short supply across Europe. According to the European Centre for the Development of Vocational Training there is a gap of approximately 50000 qualified thermographers in the EU as of 2025. This skills deficit limits the effective utilization of infrared technology in various industries. Companies often struggle to find personnel, who can accurately diagnose issues based on thermal data leading to misinterpretations and inefficient repairs. In the energy sector, this lack of expertise can result in overlooked defects that may cause catastrophic failures. Educational institutions are slow to update curricula to include thermal imaging techniques exacerbating the problem. This scarcity drives up labor costs and extends project timelines. Manufacturers are attempting to address this issue by developing user friendly software that automates analysis but human oversight remains essential. The complexity of new generations of detectors with higher resolution and spectral ranges further increases the training burden.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.27% |

| Segments Covered | By Type, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Hamamatsu Photonics K.K. (Japan), Murata Manufacturing Co., Ltd. (Japan), Excelitas Technologies (U.S.), Xenics NV, Texas Instruments Incorporated (U.S.), Teledyne Technologies (U.S.), InfraTec GmbH (Germany), Nippon Ceramic (Japan), Lynred (France), Wuhan Guide Infrared Co., Ltd. (China), Raytheon Technologies (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The thermal detector segment was the largest by holding a prominent share of the Europe infrared detector market in 2025. Thermal detectors particularly uncooled microbolometers are favored for their lower manufacturing costs and ease of integration into compact devices. Unlike cooled detectors they do not require bulky and power intensive cooling systems making them ideal for portable and battery-operated applications. The cost reduction has enabled the proliferation of thermal imaging in consumer electronics automotive safety systems and building inspection tools. In Germany, the widespread adoption of handheld thermal cameras for energy audits is a direct result of this affordability. The Federal Ministry for Economic Affairs and Climate Action reported that over 200000 residential energy assessments utilized uncooled thermal detectors in 2024. The robustness of these sensors allows them to operate in harsh industrial environments without frequent maintenance. Their instant start up time further enhances usability in emergency response scenarios where immediate thermal visualization is critical. Firefighters across Europe increasingly rely on lightweight thermal imaging cameras equipped with microbolometers to navigate smoke filled environments.

The photodetector segment is likely to witness a fastest CAGR of 11.2% from 2026 to 2034 with the demand for high sensitivity and fast response times in specialized applications. Photodetectors especially cooled variants, such as mercury cadmium telluride and indium antimonide detectors are essential for high performance defense and aerospace applications requiring superior sensitivity and speed. These detectors can detect minute temperature differences and operate at longer wavelengths making them ideal for long range surveillance and missile guidance systems. NATO countries are upgrading their airborne reconnaissance platforms with advanced photodetectors to enhance situational awareness. In the United Kingdom, the Ministry of Defence announced a procurement program for next generation unmanned aerial vehicles equipped with high resolution cooled infrared cameras in 2024. The aerospace sector also utilizes photodetectors for satellite based earth observation and weather monitoring. The European Space Agency reported that three new earth observation satellites launched in 2025 featured advanced infrared photodetector arrays for climate data collection. The scientific community relies on these detectors for spectroscopic analysis and astronomical research. Research institutions across Europe are investing in specialized laboratory equipment incorporating high sensitivity photodetectors. The unique capabilities of photodetectors to provide detailed spectral information and high frame rates make them irreplaceable in these critical sectors.

By Application Insights

The security and surveillance segment was the largest by holding 35.4% of the Europe infrared detector market share in 2025. The development of smart city infrastructure has significantly boosted the demand for infrared detectors in security and surveillance applications. Municipalities are deploying advanced thermal cameras to monitor public spaces traffic flows and critical infrastructure for enhanced safety and efficiency. These systems provide reliable visibility in low light conditions and adverse weather ensuring continuous security coverage. The integration of infrared detectors with artificial intelligence enables automated threat detection and anomaly recognition reducing the burden on human operators. Airports and railway stations are also upgrading their security systems with thermal imaging to detect unauthorized access and suspicious behavior. The ability of infrared detectors to penetrate smoke and fog makes them invaluable for emergency response scenarios. Fire departments and police forces rely on these systems for situational awareness during incidents. The ongoing investment in public safety infrastructure coupled with technological advancements ensures that security and surveillance remain the leading application segment for infrared detectors in Europe.

The medical application segment is expected to grow at a CAGR of 12.5% from 2026 to 2034. The medical community is increasingly embracing non-invasive diagnostic techniques, such as thermography, which utilize infrared detectors to visualize body heat patterns. This method allows for the early detection of various conditions including breast cancer vascular disorders and musculoskeletal injuries without radiation exposure. The ability to detect subtle temperature changes associated with inflammation and abnormal blood flow provides valuable clinical insights. In Italy several healthcare providers introduced infrared screening programs for early detection of diabetic foot complications in 2024. These programs help prevent severe outcomes by enabling timely intervention. The portability and ease of use of modern infrared cameras facilitate their integration into routine clinical practice. General practitioners and specialists are incorporating thermal imaging into patient examinations to enhance diagnostic accuracy. The European Commission’s support for digital health initiatives further promotes the adoption of innovative diagnostic technologies. Reimbursement policies in countries like France and Germany are evolving to cover infrared based diagnostic procedures. This financial support encourages wider adoption among healthcare providers. Patient preference for non-invasive and painless diagnostic methods also drives demand. As awareness of the benefits of thermography grows its application in preventive medicine and chronic disease management expands.

COUNTRY ANALYSIS

Germany Infrared Detector Market Analysis

Germany was the top performer in the Europe infrared detector market by accounting for 24.3% of the share in 2025. Germany’s market growth is driven by the robust demand from the automotive manufacturing and industrial automation sectors. The country is home to major automotive manufacturers who are integrating infrared detectors into advanced driver assistance systems and electric vehicle battery monitoring. According to the German Association of the Automotive Industry, over 5 million vehicles produced in Germany in 2025 featured infrared sensing technologies. The industrial sector also relies heavily on thermal imaging for predictive maintenance and quality control. Government initiatives promoting Industry 4.0 further support the adoption of smart sensing technologies. The Federal Ministry for Economic Affairs and Climate Action provided grants for digitalization projects incorporating infrared sensors. Germany is also a hub for research and development in photonics and sensor technology. Companies such as Infineon Technologies and Bosch are investing in the development of next generation infrared detectors. The presence of these key players fosters innovation and strengthens the supply chain. The country’s commitment to energy efficiency drives the use of thermal cameras for building inspections and energy audits. Strict environmental regulations encourage industries to adopt technologies that reduce energy consumption and emissions.

United Kingdom Infrared Detector Market Analysis

The United Kingdom infrared detector market was positioned second by holding 18.4% of share in 2025. The United Kingdom’s market growth is likely to grow with the substantial investments in defense and public safety infrastructure. The Ministry of Defence has prioritized the modernization of surveillance capabilities driving demand for high performance infrared detectors. The country’s extensive border security and counter terrorism efforts also contribute to the demand for thermal imaging solutions. The healthcare sector is another key driver with the National Health Service adopting infrared thermography for diagnostic and monitoring purposes. The Life Sciences Industrial Strategy supports the growth of this sector through funding and regulatory facilitation. The construction industry is also increasingly using thermal imaging for energy efficiency assessments. The government’s net zero targets mandate improved building performance driving demand for inspection services. The presence of leading research institutions such as the University of Southampton fosters advancements in infrared sensor technology. Collaborations between academia and industry accelerate the commercialization of new products.

France Infrared Detector Market Analysis

France infrared detector market growth is eventually to have steady opportunities throughout the forecast period with its dominance in aerospace and defense technologies which rely heavily on advanced infrared sensors. Companies, such as Thales and Safran are global leaders in the development of cooled and uncooled infrared detectors for military and civilian applications. The French Armed Forces are modernizing their equipment with state of the art thermal imaging systems for ground air and naval operations. The Directorate General of Armaments allocated significant funds for the development of next generation surveillance drones equipped with infrared cameras. The nuclear energy sector also utilizes infrared detectors for monitoring reactor components and infrastructure integrity. The construction sector is adopting thermal cameras for energy audits supported by government renovation incentives. France is also investing in research and development through national programs focused on photonics and quantum technologies. These initiatives aim to maintain technological sovereignty and competitiveness.

Italy Infrared Detector Market Analysis

Italy infrared detector market growth is propelled with the strong demand from the manufacturing and cultural heritage sectors. The country’s extensive manufacturing base particularly in the automotive and machinery industries utilizes infrared detectors for quality control and predictive maintenance. The preservation of historical monuments and artworks is another unique application area in Italy. Infrared thermography is used to detect structural defects moisture infiltration and material degradation in ancient buildings. This specialized application requires high precision detectors contributing to market value. The energy sector is also a significant contributor with utilities using thermal cameras for inspecting power lines and substations. Terna the national transmission grid operator expanded its drone based inspection programs using infrared sensors in 2024. The government’s National Recovery and Resilience Plan includes investments in digitalization and energy efficiency supporting the adoption of advanced sensing technologies. Small and medium enterprises are increasingly accessing affordable thermal imaging solutions for various applications. The presence of local distributors and service providers facilitates market access.

Spain Infrared Detector Market Analysis

Spain infrared detector market growth is propelled with the renewable energy and agricultural innovation. The country’s extensive solar and wind power installations require regular maintenance and monitoring for which infrared detectors are essential. Drones equipped with infrared cameras are widely used for inspecting solar panels and wind turbine blades. The agricultural sector is also adopting precision farming techniques utilizing thermal imaging to monitor crop health and optimize irrigation. The technology helps farmers reduce water usage and improve yields aligning with sustainability goals. The construction industry is leveraging thermal cameras for energy efficiency assessments driven by European Union regulations. Spain’s warm climate also drives demand for infrared sensors in HVAC systems for efficient temperature control. The tourism sector utilizes thermal imaging for security and safety in hotels and resorts. Government initiatives promoting digital transformation in rural areas support the adoption of advanced technologies.

COMPETITIVE LANDSCAPE

The competition in the Europe infrared detector market is characterized by intense rivalry among established global corporations and specialized regional manufacturers who strive to differentiate themselves through technological superiority and application specific solutions. Market participants face pressure to innovate continuously in order to meet stringent performance requirements for defense and industrial applications. The presence of strong domestic players such as Lynred and Xenics creates a dynamic environment where technological sovereignty and local supply chain reliability are key competitive factors. Companies compete on the basis of sensor sensitivity resolution and cost efficiency while also emphasizing after sales support and customization capabilities. The shift toward uncooled technology for mass market applications has intensified price competition whereas the cooled segment remains focused on high performance niche markets. Strategic collaborations with end users in automotive and healthcare sectors are becoming increasingly important for securing long term contracts.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe infrared detector market

- Hamamatsu Photonics K.K. (Japan)

- Murata Manufacturing Co., Ltd. (Japan)

- Excelitas Technologies (U.S.)

- Xenics NV

- Texas Instruments Incorporated (U.S.)

- Teledyne Technologies (U.S.)

- InfraTec GmbH (Germany)

- Nippon Ceramic (Japan)

- Lynred (France)

- Wuhan Guide Infrared Co., Ltd. (China)

- Raytheon Technologies (U.S.)

Top Players In The Market

- Teledyne FLIR LLC stands as a dominant force in the Europe infrared detector market by providing comprehensive thermal imaging solutions for defense industrial and commercial applications. The company leverages its extensive portfolio of uncooled and cooled sensor technologies to serve diverse sectors including automotive security and healthcare. Recent strategic initiatives include the integration of artificial intelligence into thermal cameras to enhance automated threat detection capabilities. Teledyne FLIR has expanded its manufacturing facilities in Estonia to increase production capacity for microbolometer cores. This expansion supports the growing demand for compact and cost effective thermal sensors across Europe. The company actively collaborates with European automotive manufacturers to integrate thermal vision into advanced driver assistance systems.

- Lynred SAS is a leading European manufacturer specializing in high performance cooled and uncooled infrared detectors for defense and space applications. The company plays a critical role in maintaining technological sovereignty for European nations by developing advanced sensor solutions domestically. Lynred recently announced significant investments in new production lines for second generation cooled detectors to meet increasing defense demands. The company collaborates closely with major aerospace primes such as Thales and Airbus to integrate its sensors into next generation surveillance systems. Lynred has also expanded its presence in the civil market by offering specialized detectors for gas detection and scientific instrumentation. Its focus on miniaturization and power efficiency enables the deployment of infrared sensors in unmanned aerial vehicles and portable devices. The company’s participation in European Union funded research projects fosters innovation in quantum well infrared photodetectors.

- Xenics NV is a prominent Belgian company renowned for its innovative shortwave infrared and thermal imaging solutions. The company serves a wide range of markets including machine vision life sciences and security. Xenics strengthens its market position through continuous product development focusing on high speed and high resolution sensors. Recent actions include the launch of new camera lines tailored for industrial inspection and semiconductor manufacturing processes. The company has established strong partnerships with system integrators across Europe to expand its distribution network. Xenics actively participates in collaborative research initiatives to advance infrared technology for emerging applications such as autonomous driving and medical diagnostics. Its emphasis on customer specific solutions allows for flexible adaptation to unique operational requirements. The company’s state of the art facility in Leuven supports rapid prototyping and scalable production.

Top Strategies Used By Key Market Participants

Key players in the Europe infrared detector market primarily focus on product innovation to enhance sensor performance and reduce costs. Companies are investing heavily in research and development to create smaller more efficient detectors with higher resolution. Strategic partnerships with automotive and aerospace firms are common to integrate thermal imaging into advanced safety and surveillance systems. Manufacturers are also expanding local production capacities to ensure supply chain resilience and comply with regional regulations. Another major strategy involves integrating artificial intelligence with thermal data analytics to provide smarter and more actionable insights for customers. Firms are diversifying their application portfolios by targeting emerging sectors such as renewable energy maintenance and medical diagnostics. Acquisitions of specialized technology startups help established players gain access to novel sensing techniques and intellectual property. These combined strategies enable market participants to maintain competitive advantages and address the evolving needs of European industries effectively.

MARKET SEGMENTATION

This research report on the Europe infrared detector market is segmented and sub-segmented into the following categories.

By Type

- Thermal

- Photodetectors

By Application

- Motion Sensing

- Temperature Measurement

- Security and Surveillance

- Fire Detection

- Medical

- Others

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe infrared detector market?

Increasing demand for advanced sensing technologies in security and industrial applications is driving growth.

Why are infrared detectors gaining importance across Europe?

They enable detection of heat and motion in low-visibility conditions.

How would you explain infrared detectors in simple terms?

They are devices that sense infrared radiation emitted by objects.

Where are infrared detectors most commonly used across Europe?

They are widely used in surveillance, automotive systems, healthcare, and industrial monitoring.

What makes infrared detectors important in modern technology applications?

They provide accurate sensing capabilities for safety, automation, and imaging.

From a practical perspective, are infrared detectors a valuable investment?

Yes, they enhance detection accuracy and system performance.

What challenges are affecting the Europe infrared detector market?

High production costs and technical complexities are key challenges.

How is the automotive industry influencing this market?

Growing adoption of advanced driver assistance systems is boosting demand.

Which application segments contribute the most to market demand?

Security systems and automotive applications are major contributors.

Is the Europe infrared detector market growing steadily?

Yes, it is expanding with increasing adoption of sensing technologies.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com