Europe IoT Medical Devices Market Size, Share, Trends & Growth Forecast Report By Connectivity Technology, By Type, By End User, and By Country (Germany, United Kingdom, France, Italy, Netherlands & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe IoT Medical Devices Market Size

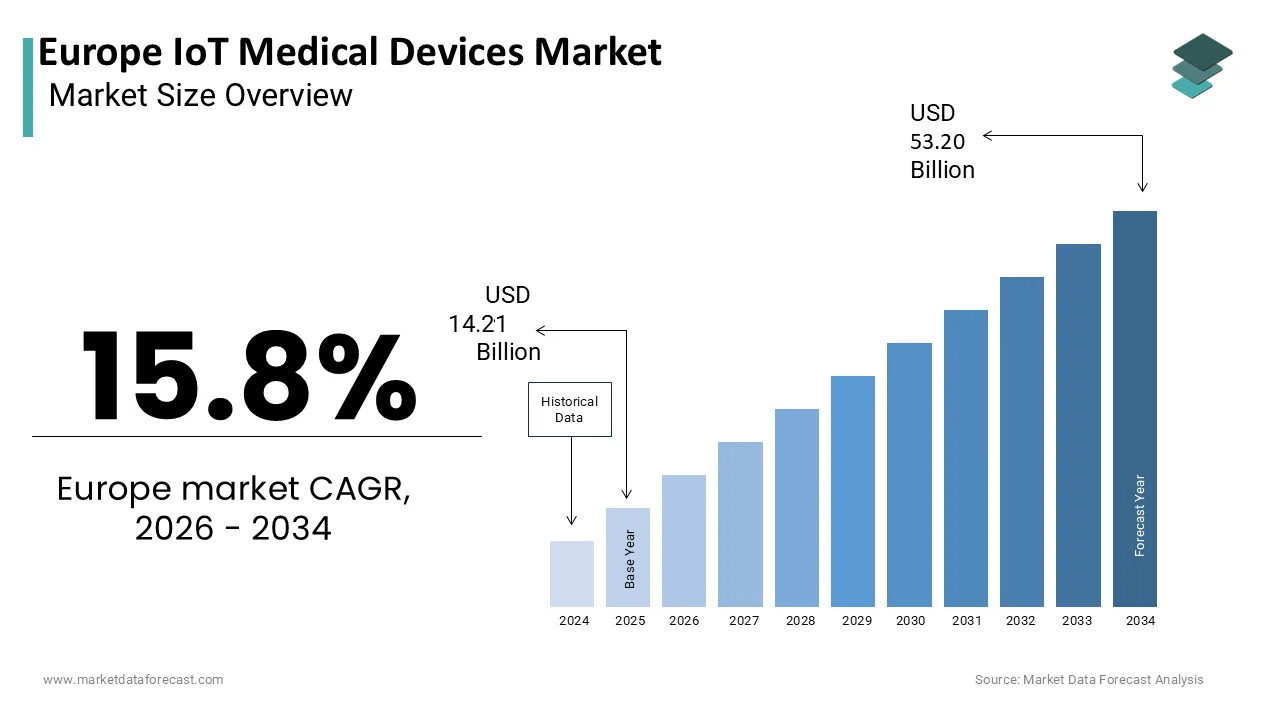

The Europe IoT medical devices market was valued at USD 14.21 billion in 2025, is estimated to reach USD 16.45 billion in 2026, and is projected to reach USD 53.20 billion by 2034, growing at a CAGR of 15.8% from 2026 to 2034.

IoT Medical Devices, often called the Internet of Medical Things (IoMT), are healthcare tools embedded with sensors, software, and network connectivity that allow them to collect, analyze, and transmit patient health data over the internet. These devices include wearable sensors, smart implants,s connected diagnostic equipment, and remote patient monitoring systems that leverage internet connectivity to enhance clinical outcomes. The region is witnessing a paradigm shift from reactive sick care to proactive preventive health management driven by technological integration. As per Eurostat, 21.6 percent of the European Union population was aged 65 or older in 2024, reflecting a rapidly aging demographic that requires continuous medical supervision. This demographic transition places immense pressure on traditional healthcare infrastructures, necessitating scalable digital solutions. According to the World Health Organization, chronic diseases account for 90 percent of all deaths in the European Region, highlighting the urgent need for long-term disease management tools. The European Commission has prioritized digital health transformation through initiatives,, such as the European Health Data Space which aims to empower citizens with cont,,rol over their health data. Furthermore, the prevalence of high-speed internet coverage across the continent supports the seamless operation of connected devices. As per the International Telecommunication Union, 91 percent of the population in Europe used the internet in 2024, enabling high-speed connectivity for medical applications. The integration of artificial intelligence with IoT devices further enhances diagnostic accuracy and predictive capabilities. Consequently, the convergence of demographic trends,, ds regulatory support, rt and technological advancement creates a fertile environment for the expansion of IoT medical devices in Europe.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Necessitates Remote Monitoring

The escalating burden o,f chronic conditions, such as diabetes, cardiovascular diseases, and respiratory disorders, drives the growth of the Europe IoT medical devices market. These conditions require constant monitoring of vital parameters to prevent complications and reduce hospital readmissions. According to the European Centre for Disease Prevention and Control, non-communicable diseases are responsible for nearly 90 percent of all deaths in the European Union. The aging population is particularly susceptible to these ailments, creating a sustained need for home based monitorinnon-communicable devices such as connected glucose meters, smainhalersrss, and cardiac monitors, allowing patients to manage their conditions effectively while remaining in their homes. As per the International Home-Based Federation's 2024 figures, approximately 66 million adults in the European region were living with diabetes, a figure expected to rise to 72 million by 2050. Remote monitoring enables healthcare providers to track patient data in real time and intervene promptly when anomalies are detected. This proactive approach reduces the strain on emergency services and lowers overall healthcare costs. The European Society of Cardiology emphasizes the role of digital health tools in improving adherence to treatment plans and enhancing patient quality of life. Governments are increasingly reimbursing remote monitoring services, recognizing their value in managing chronic care. So, the growing incidence of chronic diseases acts as a primary driver accelerating the adoption of IoT medical devices across the continent.

Government Initiatives Promoting Digital Health Infrastructure Accelerate Growth

European governments are actively investing in digital health infrastructure to modernize healthcare delivery and improve accessibility, which contributes to the expansion of the Europe IoT medical devices market. The European Union has launched several strategic frameworks, ks including the Digital Europe Programme, which allocates substantial funding for the deployment of advanced digital technologies in healthcare. The European Commission actively supports Member States in developing national digital health strategies and mandates investment in digital transition (min. 20%) for Recovery and Resilience Facility funding, while the upcoming European Health Data Space (EHDS) regulation will require implementation of interoperable electronic health record infrastructures by 2030. These initiatives create a supportive ecosystem for IoT medical devices by ensuring interoperability and data standardization. The COVID-19 pandemic accelerated the adoption of telemedicine, with many countries implementing permanent reimbursement schemes for virtual consultations. As per the Organisation for Economic Co-operation and Development, telemCOVID-19COVID-19usage in Europe more than doubled during the pandemic (increasing by over 100% in many nations) and has remained elevated above pre-pandemic levels since. This shift encourages the use of connected devices that can transmit patient data securely to healthcare providers. Countries like Estonia and Denmark have established robust digital health identities, enabling seamless integration of IoT data into patient records. The European Health Data Space regulation further facilitates cross-border data exchange, enabling better coordination of care. These policy measures reduce barriers to entry for manufacturers and encourage healthcare providers to adopt connected solutions. So, a strong government supcross-border regulatory framework serves as a significant driver for the Europe IoT medical devices market.

MARKET RESTRAINTS

Stringent Data Privacy Regulations and Cybersecurity Concerns Hinder Adoption

The handling of sensitive health data by IoT medical devices raises significant privacy and security concerns, which act as a major restraint in the European IoT medical devices market. The General Data Protection Regulation imposes strict requirements on the collection, storage, and processing of personal health information. Compliance with these regulations requires substantial investment in encryption,n secure data transmission protocols, and regular security audits. The European Union Agency for Cybersecurity reveals that healthcare has become the most targeted industry for digital threats, with a surge in complex attacks that threaten to disrupt medical services and compromise private patient records. These threats undermine trust in connected health technologies and make healthcare providers cautious about integrating IoT solutions. The complexity of ensuring end-to-end security across diverse devices and networks poses technical challenges for manufacturers. As per the European Data Protection Board, any breach of health data can result in severe penalties and reputational damage, discouraging some organizations from adopting new technologies. Patients are also increasingly aware of privacy risks and may hesitate to use devices that continuously transmit personal health information. The lack of standardized cybersecurity certifications for medical IoT devices further complicates the procurement process for hospitals. Manufacturers must navigate a complex landscape of legal and technical requirements, ts which increases development time and costs. Hence, concerns regarding data privacy and security remain a critical barrier to the rapid expansion of the IoT medical devices market in Europe.

High Implementation Costs and Limited Reimbursement Policies Restrict Accessibility

The high cost associated with acquiring and implementing IoT medical devices is a significant financial barrier for healthcare institutions and patients in the Europe IoT medical devices market. These devices often require integration with existing hospital information systems, EMS,s which involves additional expenses for software customization and staff training. According to the European Hospital and Healthcare Federation,tion many public hospitals in Europe operate under tight budget constraints, limiting their ability to invest in new technologies. While the long-term benefits of remote monitoring include cost savings through reduced hospitalizations, the upfront investment remains prohibitive for many IoT-enabled devices. Reimbursement policies for IoT-enabled services vary significantly across European countries, creating uncertainty for manufacturers and providers. As per the European Health Management Association,n only a few countries have comprehensive reimbursement frameworks for digital health solutions, leaving many patients to bear the out-of-pocket costs. This lack of financial support limits the accessibility of advanced IoT devices to wealthier segments of the population, exacerbating health inequalities. Small and medium-sized clinics often lack the resources to adopt these technologies, leading to fragmented implementation. The return on investment for IoT devices is not always immediately apparent to payers who prioritize acute care spending. Thus, financial constraints and inconsistent reimbursement landscapes act as a major restraint, slowing down the widespread adoption of IoT medical devices in the European healthcare system.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Enhances Diagnostic Capabilities

The convergence of the Internet of Things with artificial intelligence and machine learning offers transformative opportunities for the Europe IoT medical devices market. AI algorithms can analyze vast amounts of data generated by connected devices to identify patterns, predict health events, and provide personalized recommendations. The European Artificial Intelligence Alliance suggests that the deployment of machine learning models in clinical settings has the potential to significantly enhance the precision of medical screenings and the speed of patient triaging. Smart devices equipped with AI can detect early signs of deterioration in chronic disease patients, enabling timely interventions. For instance, an AI-powered cardiac monitor can distinguish between normal variations and dangerous arrhythmias with high precision. As per the European Society of Radiology, AI-enhanced imaging devices are becoming increasingly common, aiding radiologists in detecting abnormalities earlier. This technological synergy supports the shift towards precision medicine,e where treatments are tailored to individual patient profiles. The European Union is investing heavily in AI research through programs like Horizon Europe to foster innovation in this field. Healthcare providers can leverage these insights to optimize treatment plans and improve patient outcomes. Furthermore, AI-driven analytics can automate routine tasks, reducing the administrative burden on medical staff. Therefore, the integration of advanced analytics with IoT devices creates new value propositions, ns driving innovation and expanding the potential applications of connected health technologies in Europe.

Expansion of 5G Networks Enables Real-Time Data Transmission

The rollout of fifth-generation mobile networks across the region provides the high-speed, low-latency connectivity required for advanced IoT medical applications. This is likely to promote the exReal-Timef the Europe IoT medical devices market. 5G technology enables the real-time transmission of large volumes of medical data, such as high-resolution video and complex sensor readings, without delay. Technical standards from the European Telecommunications Standards Institute define how high-speed, low-latency networks enable the reliable transmission of massive data sets, supporting applications such as remote surgery and real-time patient monitoring. This capability supports the development of remote surgery and telesurgery, where surgeons can operate on patients from distant locations using robotic systems. Research indicates that the rapid rollout of next-generation mobile networks across the continent is ensuring that a vast majority of the population will soon have the connectivity required to utilize sophisticated digital health platforms. The enhanced bandwidth allows for the simultaneous connection of multiple devices in a hospital setting,s improving workflow efficiency. Emergency services can also benefit from G-enabled ambulances that transmit patient data to hospitals before arrival,val allowing medical teams to prepare in advance. The reliability of 5G networks ensures continuous monitoring of critical patients, reducing the risk of data loss. Governments are prioritizing 5G infrastructure development as part of their digital transformation agendas. As a result, the expansion of 5G networks unlocks new possibilities for IoT medical devices, enhancing their functionality and enabling innovative healthcare delivery models.

MARKET CHALLENGES

Interoperability Issues Hinder Seamless Data Integration

The lack of interoperability between devices from different manufacturers and healthcare IT systems is a significant challenge in the Europe IoT medical devices market. Many IoT devices operate on proprietary protocols, making it difficult to integrate data into a unified electronic health record. According to the European Interoperability Framework,k the absence of common standards leads to data sil, os which impede the flow of information between healthcare providers. This fragmentation prevents clinicians from obtaining a holistic view of patient health, potentially leading to fragmented care and medical errors. As per the European Connected Health Alliance, efforts to establish universal standards, such as HL7 FHIR, are ongoing, but adoption remains uneven across the region. Healthcare institutions often struggle to connect legacy systems with new IoT devices, requiring costly custom interfaces. The lack of seamless integration reduces the efficiency gains promised by digital health solutions. Manufacturers face challenges in ensuring their devices are compatible with various hospital systems, which increases development complexity. Patients who use multiple devices from different vendors may experience difficulties in aggregating their health data. Regulatory bodies are working to mandate interoperability standards,s but progress is slow. Hence, interoperability issues remain a persistent challenge that limits the full potential of IoT medical devices in delivering coordinated and efficient healthcare.

Shortage of Skilled Professionals Impacts Operational Efficiency

The effective utilization of IoT medical devices requires a workforce skilled in both healthcare and digital technologies,ies yet the region faces a significant shortage of such professionals, which hampers the expansion of the Europe IoT medical devices market. Healthcare providers often lack the expertise to manage complex IoT infrastructure and interpret the vast amounts of data generated. According to the European Commission, there is a projected shortfall of millions of digital specialists in the EU by 20,30, affecting various sectors,s including healthcare. Clinicians need training to understand how to integrate IoT data into clinical decision-making processes effectively. The European Hospital and Healthcare Federation indicates that the rapid expansion of wearable and connected medical technology is creating a "data deluge" for clinical staff, who require better integrated analysis tools to process this information without added administrative burden. The gap in digital literacy among older medical professionals further exacerbates the issue. Hospitals must invest in continuous education and recruitment to bridge this skills gap,p which adds to operational costs. The lack of specialized IT support within healthcare facilities can lead to prolonged downtime and inefficient use of technology. Additionally,lly the resistance to change among some healthcare staff slows down the adoption of new workflows. Without a competent workforce,orce the potential benefits of IoT devices cannot be fully realized. Hence, the shortage of skilled professionals poses a critical challenge to the successful implementation and scaling of IoT medical devices in the European healthcare system.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Connectivity Technology, Type, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Medtronic plc, Koninklijke Philips N.V., GE HealthCare Technologies Inc., Siemens Healthineers AG, Abbott Laboratories, Johnson & Johnson, Boston Scientific Corporation, Hoffmann-La Roche Ltd, Baxter International Inc., Cisco Systems, Inc., IBM Corporation, Honeywell International Inc. |

SEGMENTAL ANALYSIS

By Connectivity Technology Insights

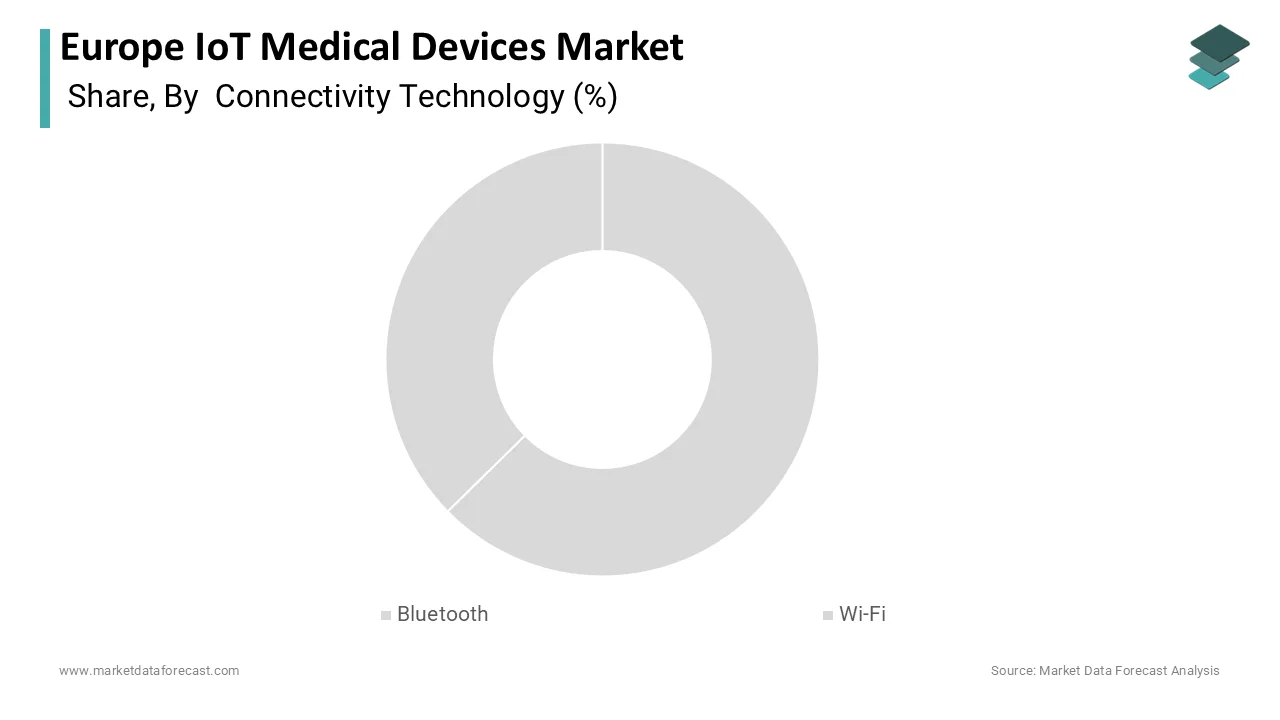

The Bluetooth segment was the largest segment in the Europe IoT medical devices market and secured a 48.8% share in 2025. This prominence of the segment is largely supported by the widespread adoption of wearable health monitors and personal medical devices that require low energy consumption and seamless pairing with smartphones. Bluetooth Low Energy technology enables continuous data transmission from devices such as glucose monitors, heart rate sensors, and fitness trackers to mobile applications without draining the battery quickly. According to the Bluetooth Special Interest Group, over 90% of smartphones sold globally support Bluetooth Low Energy, ensuring broad compatibility for medical device manufacturers. In Europe, the high penetration of smartphones among both younger and older demographics facilitates the use of Bluetooth-enabled health apps for remote patient monitoring. Recent surveys from Eurostat indicate that while internet and smartphone usage is growing among the elderly in Europe, less than half of citizens in the 65-to-74 age range currently use connected devices, suggesting significant room for growth in senior-focused health technology. The ease of integration with existing consumer electronics reduces the barrier to entry for patients managing chronic conditions at home. Furthermore, Bluetooth mesh networking capabilities allow for the creation of scalable sensor networks in hospital environments for asset tracking and patient monitoring. The standardized protocol ensures interoperability between devices from different manufacturers, which is crucial for healthcare systems. Thus, the combination of energy efficiency, universal compatibility, and ease of use sustains the leadership of the Bluetooth segment in the market.

The WiFi segment is anticipated to witness the fastest CAGR of 13.5% from 2026 to 2034 due to the increasing deployment of stationary medical devices in hospitals and home care settings that require high bandwidth for transmitting large volumes of data, such as medical images and video streams. WiFi infrastructure is already ubiquitous in healthcare facilities, es making it a cost-effective solution for connecting multiple devices simultaneously. According to the European Telecommunications Standards Institute, the adoption of WiFi 6 and WiFi 6E standards has significantly improved network capacity and reduced latency, which is critical for real-time monitoring applications. These advancements enable the reliable transmission of high-resolution data from connected imaging equipment and patient monitoring systems. The International Data Corporation highlights that European spending on digital transformation and intelligent health platforms is set to accelerate through the end of the decade, requiring hospitals to upgrade their underlying network infrastructure to keep pace with new software demands. Home care settings are also benefiting from improved home broadband speeds, which support the use of advanced telemedicine platforms and remote diagnostic tools. The ability of WiFi to handle multiple concurrent connections without interference makes it ideal for dense healthcare environments. Furthermore, re the integration of WiFi with cloud-based electronic health records facilitates seamless data sharing among healthcare providers. Therefore, the demand for high-speed reliability for data-intensive medical applications drives the rapid expansion of the WiFi segment.

By Type Insights

The wearable medical devices segment dominated the Europe IoT medical devices market and accounted for a 55.3% share in 2025. This dominance of the segment is driven by the rising consumer awareness regarding health and wellness and the increasing prevalence of chronic diseases that require continuous monitoring. Wearable devices such as smartwatches, non-invasive, and patch sensors offer non invasive a, nd convenient ways to track vital signs, including heart rate, te blood oxygen level,s and physical activity. Projections from the World Health Organization and OECD indicate that the prevalence of non-communicable conditions in Europe will rise significantly over the coming decades, intensifying the need for proactive health management and digital monitoring solutions. The aging population in Europe is increasingly adopting wearables to maintain independence and monitor their health status remotely. A study indicates that European consumers are increasingly adopting wearable health technology, with the sector experiencing steady double-digit growth as users seek more frequent tracking of their vital signs and daily habits. These devices empower individuals to take proactive measures towards their health by providing real-time feedback and alerts. Healthcare providers are also able to use data in clinical decision-making processes, es enhancing the accuracy of diagnoses and treatment plans. The miniaturization of sensors and improvements in battery life have made wearables comfortable and durable for llong-terlong-term usenally, insurance companies are offering incentives for using wearables to promote healthy lifestyles. So, the combination of technological advancement,s demographic trend, and consumer engagement ensures the continued dominance of the wearable segment.

The implantable medical devices segment is likely to experience the fastest CAGR of 15.2% over the forecast period, owing to advancements in bioelectronics and the need for precise internal monitoring. Implantable devices such as pacemakers, neurostimulators,s and glucose sensors provide critical therapeutic and diagnostic functions for patients with severe chronic conditions. According to the European Society of Cardiology, pacemakers remain a critical and high-volume intervention for heart health across the continent, with hundreds of thousands of new procedures performed each year to address rhythmic disorders. The integration of IoT capabilities allows these implants to transmit data wirelessly to external receivers, enabling remote monitoring and timely medical interventions. As per the MedTech Europe association, the adoption of remote monitoring for cardiac implants has reduced hospital visits by 30 percent, improving patient quality of life and reducing healthcare costs. Recent innovations in biocompatible materials and energy harvesting technologies have extended the lifespan of implantable devices, reducing the need for surgical replacements. The development of closed-loop systems that automatically adjust therapy based on real-time physiological data represents a breakthrough in personalized medicine. Regulatory approvals for new generations of smart implants are accelerating their market entry. Furthermore, the increasing prevalence of neurological disorders such as Parkinson’s disease drives the demand for connected neurostimulators. Hence, the clinical benefits and technological innovations in implantable devices drive their rapid adoption and market growth.

By End User Insights

The hospitals and clinics segment held the majority share of 60.8% of the Europe IoT medical devices market in 2025. This supremacy of the segment is attributed to the extensive adoption of connected medical equipment for patient monitoring, asset management,t and operational efficiency in large healthcare facilities. Hospitals are investing heavily in IoT solutions to improve patient outcomes, reduce readmission rates, and optimize resource utilization. The European Hospital and Healthcare Federation shows that while digital monitoring is becoming a standard feature in modern wards, the use of advanced tracking systems for equipment and personnel is a growing trend that is still being rolled out across the region's largest medical centers. Connected devices such as smart beds, DS,s infusion pumps, MPSs, and vital sign monitors enable continuous data collection and integration with electronic health records. As per the European Commission, digital transformation in healthcare is a priority,y with significant funding allocated for modernizing hospital infrastructure.IoT-enabled predictive maintenance helps hospitals avoid equipment downtime and reduce repair costs. The ability to monitor patients remotely within the hospital premises enhances nurse efficiency and allows for quicker response to emergencies. Furthermore, the integration of IoT data supports clinical research and quality improvement initiatives. Government initiatives promoting smart hospitals further accelerate the adoption of these technologies. Thus, the critical need for efficient and high-quality care in institutional settings ensures the continued leadership of the hospitals and clinics segment.

The home care settings segment isfastest-growingd is expected to be the fastest-growing segment in the market with a CAGR of 16.8% fron 2026 to 20344. This swift growth of the segment is fueled by the shift towards home-based care, driven by an aging population and the desire to reduce healthcare costs associated with hospital stays. IoT medical devices enable elderly and chronically ill patients to receive professional monitoring and care in the comfort of their homes. According to Eurostat,t the proportion of people aged 65 and over in the EU is projected to reach 30 perlong-term050 increasing the demand for long-term care solutions. Remote patient monitoring systems allow healthcare providers to track vital signs and detect early signs of deterioration, preventing unnecessary hospitalizations. As per the European Ageing Report,t home care is increasingly preferred by seniors who wish to maintain their independence. Smart home sensors and wearable devices provide safety alerts for falls or medication adherence issues, enhancing patient security. Reimbursement policies in several European countries are expanding to cover remote monitoring services, making home care more accessible. The COVID-19 pandemic accelerated the adoption of telehealth and home monitoring technologies, establishing new standards of care. Therefore, the demographic shift and economic incentives for home-based care drive the rapid expansion of this segment.

COUNTRY LEVEL ANALYSIS

Germany IoT Medical Devices Market Analysis

Germany led the Europe IoT medical devices market and captured a 22.7% share in 2025. The demand for these devices in Germany is driven by its strong healthcare infrastructure, advanced technological capabilities, and significant investment in digital health. Germany is home to leading medical device manufacturers and technology companies that drive innovation in connected health solutions. According to the German Federal Ministry of Health, the Digital Healthcare Act has facilitated the reimbursement of digital health applications, including IoT devices, encouraging widespread adoption. The country’s aging population and high prevalence of chronic diseases create substantial demand for remote monitoring and management tools. The German Association of the Medical Device Industry indicates that the digital health segment is expanding at a rate that outpaces traditional medical hardware, driven by the rapid integration of software-based solutions into a world-class landscape. The presence of world-class research institutions and universities fosters collaboration between academia and industry, accelerating the development of new technologies. Germany’s robust data protection framework ensures patient privacy while enabling secure data exchange. The government’s commitment to establishing a telematics infrastructure supports the integration of IoT devices into the national healthcare system. Hence, Germany’s combination of regulatory support, technological expertise,se and demographic needs sustains its leadership in the European IoT medical devices market.

United Kingdom IoT Medical Devices Market Analysis

The United Kingdom was the second largest country in the Europe IoT medical devices market and accounted for a 18.6% share in 2025. This position of the UK market is propelled by a strong national health service that is actively pursuing digital transformation to improve efficiency and patient care. The National Health Service Long Term Plan emphasizes the use of technology to prevent illness and manage chronic conditions effectively. According to NHS England, millions of patients are now using digital tools, including self-management and remote monitoring, and self-management. The UK is a hub for health tech startups and innovation, attracting significant venture capital investment. As per the Office for Life Sciences, the UK government has invested heavily in life sciences and digital health initiatives to maintain its global competitiveness. The adoption of wearable devices and remote monitoring solutions has been accelerated by the need to reduce hospital congestion and improve access to care. Regulatory frameworks such as those provided by the Medicines and Healthcare products Regulatory Agency ensure the safety and efficacy of medical devices. The UK’s strong research base in artificial intelligence and data analytics further enhances the value of IoT medical devices. Thus, the supportive policy environment and innovative ecosystem maintain the UK’s prominent position in the regional market.

France IoT Medical Devices Market Analysis

France maintains a significant position in the Europe IoT medical devices market owing to its large elderly population and government initiatives to support aging in place. Also, France has implemented various programs to promote the use of telemedicine and connected health devices for chronic disease management. The French Ministry of Health and Prevention is currently driving a comprehensive national modernization plan that prioritizes the interoperability of health data and the digital transformation of the medical workforce to improve care delivery. The country has seen a significant increase in the adoption of remote monitoring devices for patients with cardiovascular and respiratory conditions. As per the French National Authority for Health reimbursement, fo the coverage of telemonitoring services has expanded,ded covering more conditions and devices. The presence of major pharmaceutical and medical device companies in France drives local research and development activities. The country’s strong social security system supports the affordability of healthcare technologies for citizens. Additionally,y France is investing in smart hospital projects to improve operational efficiency and patient experience. The focus on preventive care and early intervention aligns with the capabilities of IoT medical devices. So, France’s strategic priorities and demographic trends drive steady growth in the IoT medical devices sector.

Italy IoT Medical Devices Market Analysis

Italy is moving ahead steadfastly in the Europe IoT medical devices market due to the need to manage a high burden of chronic diseases and an aging population within a constrained healthcare budget. Cost-effective medical devices offer a cost-effective solution for monitoring patients at home and reducing hospital admissions. The National Recovery and Resilience Plan includes substantial investments in digital health infrastructure and telemedicine services. As per the Italian Ministry of Health, initiatives to expand remote monitoring for diabetes and hypertension are gaining traction. The country has a growing number of health tech startups focusing on wearable devices and mobile health applications. Regional healthcare authorities are increasingly adopting IoT solutions to improve coordination, and the cultural preference for family-based care also supports the use of home monitoring technologies. However, challenges related to digital literacy and infrastructure disparities remain. Consequently, Italy’s demographic pressures and policy reforms drive the gradual but steady adoption of IoT medical devices.

Netherlands IoT Medical Devices Market Analysis

The Netherlands is anticipated to grow notably in the Europe IoT medical devices market over the forecast period. The country is recognized for its advanced digital health infrastructure and focus on interoperability and data sharing. The patient-centered care system emphasizes patient-centered care and prevention,n leveraging technology to achieve these goals. Ac, cording, to the Dut,, ch Ministry of Health Welfa,, re and Spo,, rt,, the majority of general practitioners use electronic health records that can integrate with IoT devices. The country has established strict standards for data security and privacy, thereby ensuring trust in digital health solutions. As per Nictiz the national center for efacilitateselopments in the Netherlands facilitate the seamless exchange of health information across different care settings in the Netherlands. The Netherlands is a leader in pilot projects for remote monitoring and virtual wards,, rds demonstrating the effectiveness of IoT technologies. The strong collaboration between government healthcare providers and technology companies fosters innovation. The high level of digital literacy among the population supports the adoption o,f, connected health devices. Additionally, the country’s compact geography and efficient logistics facilitate the distribution and support of medical technologies. Consequently, ultimately, the Netherlands’ commitment to digital integration and patient empowerment maintains its significant role in the European market.

COMPETITIVE LANDSCAPE

The competition in the Europe IoT medical devices market is characterized by the presence of established medical technology giants and innovative startups. Bainn players compete based on technological innovation, product reliability, and integration capabilities with existing healthcare systems. The market sees frequent launches of new connected devices featuring advanced sensors and artificial intelligence algorithms. Differentiation is achieved through comprehensive ecosystems that include hard-wired and analytics services. Companies also compete on the strength of their regulatory approvals and compliance with data privacy laws such as GDPR. Strategic alliances with telecommunications providers and cloud computing firms are common to enhance connectivity and data storage solutions. Price the competition exists,s but is secondary to the value proposition, which includes improved patient outcomes and operational efficiency. Intellectual property protection is crucial as companies strive to safeguard their proprietary technologies and algorithms. The entry of consumer electronics companies into the health monitoring space adds to the competitive dynamics. Overall,l the market demands continuous innovation and collaboration to address the complex needs of healthcare providers and patients in the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe IoT Medical Devices Market include

- Medtronic plc

- Koninklijke Philips N.V.

- GE HealthCare Technologies Inc.

- Siemens Healthineers AG

- Abbott Laboratories

- Johnson & Johnson

- Boston Scientific Corporation

- Hoffmann-La Roche Ltd

- Baxter International Inc.

- Cisco Systems, Inc.

- IBM Corporation

- Honeywell International Inc.

TOP LEADING PLAYERS MARKET

- Medtronic plc is a global leader in medical technology services and solutions with a significant presence in the Europe IoT medical devices market. The company specializes in connected therapeutic devices for chronic disease management, including diabetes care and cardiac monitoring. Its contribution to the global market includes the development of integrated ecosystems that allow seamless data exchange between implants and external monitors. Recent actions involve expanding its remote patient monitoring platforms across European healthcare systems to improve clinical outcomes. Medtronic actively collaborates with hospitals to integrate device data into electronic alth health health-enhancing decision-making. The company invests heavily in cybersecurity to ensure patient data protection, complying with strict European regulationuser-friendlyg on interoperabilit anuser-friendlyly interfaces. Medtronic trengthens decision-makinas g a trusted partner for healthcare providers. This strategic emphasis on connected care solutions enables the company to address the growing demand for remote monitoring and personalized therapy management in the region.

- Philips NV is a prominent health technology company with a strong footprint in the Europe IoT medical devices market. The organization focuses on connected care solutions, including remote patient monitoring, wearable sensors, and telehealth platforms. Its global contribution lies in integrating artificial intelligence with IoT devices to provide actionable insights for clinicians. In Europe, Philips has launched several initiatives to support home healthcare and hospital efficiency through digital innovations. Recent actions include partnerships with European health systems to deploy scalable remote monitoring solutions for chronic conditions. The company emphasizes open standards to ensure compatibility with various healthcare IT systems. Philips also invests in research and development to enhance the accuracy and reliability of patient-centric devices. By prioritizing patient-centric design and clinical validation, Philips reinforces its reputation for quality and innovation. This approach allows the company to meet tthe evolving needsof hhealthcare providers ddriving theadoption of IoT technologies across the continent.

- Siemens Healthineers AG is a leading medical technology provider with a robust presence in the Europe IoT medical devices market. The company offers a wide range of connected diagnostic imaging systems and laboratory diagnostics that leverage IoT capabilities. Its global contribution includes the development of digital health platforms that enable remote access to imaging data and collaborative diagnostics. In Europe, ope Siemens Healthineers focuses on integrating IoT sensors into medical equipment for predictive maintenance and operational efficiency. Recent actions involve expanding its teamplay digital health platform to connect hospitals and improve workflow management. The company collaborates with healthcare institutions to implement smart hospital solutions that enhance patient care and reduce costs. Siemens Healthineers also prioritizes data security and compliance with European regulatory standards. By combining hardware expertise with digital services, the company delivers comprehensive solutions that support clinical excellence. This strategic integration of IoT technology into diagnostic processes strengthens its competitive position and drives innovation in the Europ,e, an healthcare sector.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe IoT medical devices market primarily focus on strategic partnerships and collaborations to enhance product offerings and market reach. Companies frequently engage with healthcare providers, technology firms, and research institutions to develop integrated solutions that meet clinical needs. Investment in research and development is a major strategy to innovate new connected devices and improve existing techno,l,ogies. Manufacturers prioritize regulatory compliance and data security to build trust among users and adhere to strict European standards. Expansion into home care and remote monitoring segments allows companies to tap into the growing demand for decentralized healthcare services. Marketing efforts emphasize the clinical benefits and cost-effectiveness of IoT solutions to encourage adoption by healthcare systems. Additionally, firms invest in user experience design to ensure devices are intuitive and accessible for patients and clinicians. By leveraging cost-effectiveness, participants strengthen their competitive positions and drive the growth of the IoT medical devices market in Europe.

MARKET SEGMENTATION

This research report on Europe IoTIoTt medical devices market is segmented and sub-segmented into the following categories.

By Connectivity Technology

- Bluetooth

- Wi-Fi

By Type

- Wearable Medical Devices

- Implantable Medical Devices

By End User

- Hospitals & ClinicsIoTme Care Settings

By Country

- Germany

- United Kingdom

- France

- Italy

- Netherlands

- Resof Europeee

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com