Europe Jump Starter Market Size, Share, Trends, & Growth Forecast Report By Product (Jump Boxes, Plug In Units), Battery, Vehicle and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Jump Starter Market Report Summary

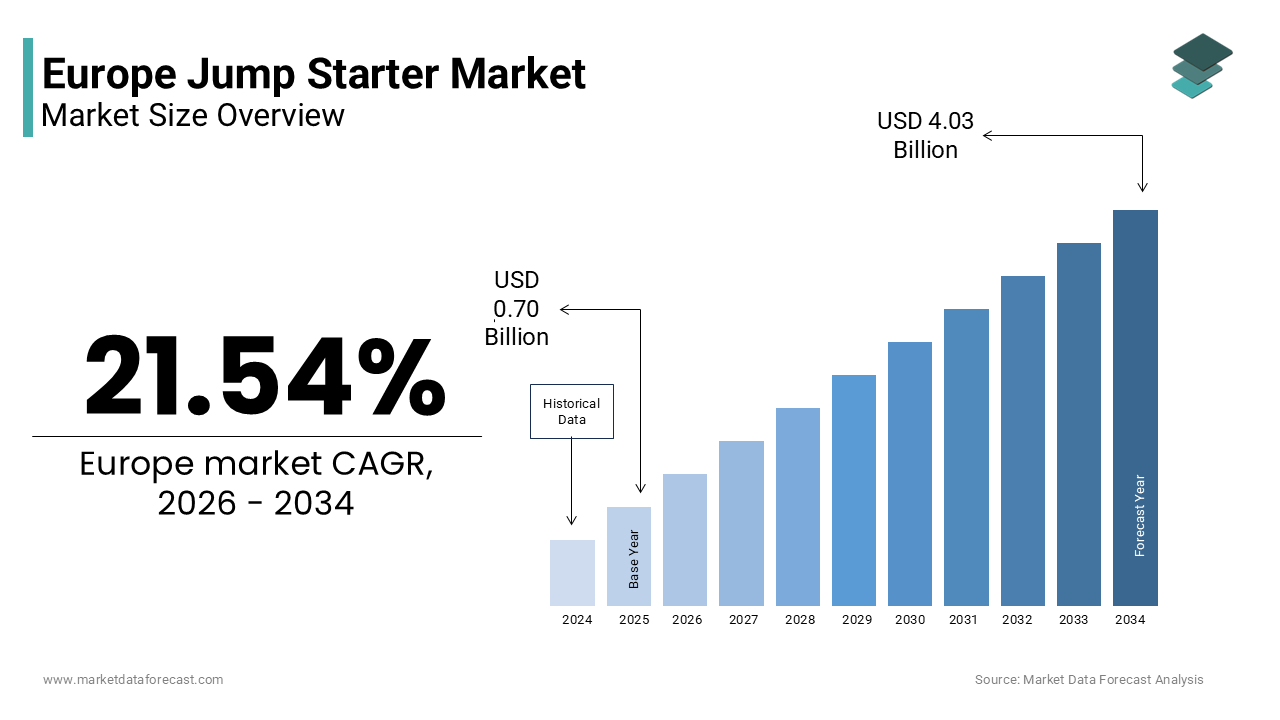

The Europe jump starter market was valued at USD 0.70 billion in 2025, is estimated to reach USD 0.85 billion in 2026, and is projected to reach USD 4.03 billion by 2034, growing at a CAGR of 21.54% during the forecast period from 2026 to 2034. The growth of the European jump starter market is driven by the rising average age of vehicles, increasing battery failure incidents, and growing demand for portable emergency power solutions. The evolution of jump starters from traditional lead-acid units to advanced lithium-ion multifunctional devices with features such as USB charging, air compression, and LED lighting is further fueling market growth. Moreover, increasing consumer awareness regarding roadside safety, self-sufficiency, and outdoor travel needs is expanding adoption across Europe.

Key Market Trends

- Rising adoption of compact lithium-ion jump starters due to portability and high efficiency

- Growing demand for multifunctional devices supporting travel, camping, and outdoor applications

- Increasing integration of smart features such as Bluetooth connectivity and vehicle diagnostics

- Expansion of online retail channels improving product accessibility and price transparency

- Emergence of EV-compatible jump starters aligned with electric mobility growth

Segmental Insights

- Based on battery technology, the lithium-ion segment was the largest and held a significant share of the Europe jump starter market in 2025. The segment’s dominance is attributed to high energy density, compact size, faster charging capability, and longer lifecycle, making it ideal for modern passenger vehicles.

- Based on vehicle type, the passenger cars segment accounted for the largest share of the Europe jump starter market in 2025. This is driven by the large base of passenger vehicles, rising consumer preference for self-reliance, and increasing frequency of battery-related issues in urban driving conditions.

- Based on distribution channel, the online retail segment was the largest, occupying a prominent share of the Europe jump starter market in 2025. The dominance of this segment stems from the convenience of e-commerce platforms, wider product variety, competitive pricing, and increasing digital adoption among consumers.

Regional Insights

The Europe jump starter market is witnessing robust growth across major countries, supported by high vehicle ownership, climatic conditions, and increasing awareness of emergency preparedness.

- Germany was the largest contributor, accounting for 24.2% of the European jump starter market share in 2025, driven by its strong automotive ecosystem, high vehicle ownership, and demand for high-quality automotive accessories.

- The United Kingdom and France continue to perform well, fueled by aging vehicle fleets, seasonal weather conditions, and growing outdoor travel trends.

Competitive Landscape

The Europe jump starter market is characterized by the presence of established automotive brands and specialized electronics manufacturers focusing on product innovation, safety features, and multifunctionality. Leading companies are emphasizing advanced lithium battery technologies, compact designs, and smart integrations to differentiate their offerings. Expansion through online platforms, partnerships with automotive retailers, and digital marketing strategies is strengthening market presence. Prominent players in the Europe jump starter market include Clore Automotive, Stanley Black & Decker, Inc., NOCO Company, Schumacher Electric Corporation, CTEK Holding AB, Ring Automotive Ltd, Robert Bosch GmbH, Einhell Germany AG, DBPOWER, and NEXPOW.

Europe Jump Starter Market Size

The Europe jump starter market size was valued at USD 0.70 billion in 2025 and is anticipated to reach USD 0.85 billion in 2026 from USD 4.03 billion by 2034, growing at a CAGR of 21.54% during the forecast period from 2026 to 2034.

Jump starter comprises portable power devices designed to revive vehicle batteries without the need for a second car or external power source. These devices have evolved from simple lead acid units to sophisticated lithium ion based systems that offer multiple functionalities such as USB charging, air compression, and LED lighting. The market is driven by the increasing complexity of modern vehicles which require stable voltage levels for electronic systems during ignition. According to the European Automobile Manufacturers Association, there were 252 million passenger cars on EU roads in 2023, providing a substantial base for potential users. The prevalence of extreme weather conditions in Northern and Eastern Europe further necessitates reliable starting solutions as cold temperatures significantly reduce battery efficiency. As per data from the International Energy Agency, electric car sales in Europe reached nearly 3.2 million units in 2023, which creates a unique demand for specialized jump starters compatible with high voltage systems. Consumer awareness regarding roadside safety and self-sufficiency has grown, which is leading to higher penetration of these devices among private car owners. Regulatory standards for battery safety and transport of lithium batteries also shape the product landscape, ensuring that manufacturers adhere to strict quality controls. The shift towards compact and user friendly designs reflects the changing preferences of urban drivers who prioritize convenience and portability. This market segment is integral to the broader automotive aftermarket ecosystem, supporting vehicle maintenance and emergency preparedness across the continent.

MARKET DRIVERS

Rising Average Age of Vehicle Fleet Increases Battery Failure Incidents

The increasing average age of the vehicle fleet in Europe is majorly driving the growth of the European jump starter market as older cars are more prone to battery degradation and failure. According to the European Automobile Manufacturers Association, the average age of passenger cars in the EU is 12.3 years. Older vehicles typically feature aging electrical components and batteries that have undergone numerous charge discharge cycles, making them susceptible to sudden failures, especially during cold starts. This demographic trend ensures a consistent demand for reliable emergency starting solutions as drivers seek to avoid the inconvenience and cost of professional roadside assistance. The likelihood of battery failure increases exponentially after the three year mark, which coincides with the typical warranty period of original equipment batteries. As vehicles age beyond this point, owners become more proactive in purchasing backup power sources to ensure mobility. The economic uncertainty in various regions also encourages consumers to maintain their existing vehicles rather than replacing them, further extending the lifecycle of cars and the associated need for maintenance tools. Jump starters provide a cost effective alternative to frequent battery replacements, allowing users to extend the life of their current batteries while having a safety net for unexpected failures. This practical utility drives steady adoption among budget conscious consumers who prioritize reliability and independence in vehicle management.

Growth in Outdoor Recreation and Road Tourism Boosts Portable Power Demand

The surge in outdoor recreation and road tourism across Europe is further contributing to the European jump starter market expansion as versatile power banks for camping and travel. According to Eurostat, tourism in the EU showed 2.9 billion nights spent in tourist accommodation in 2023, with millions of households engaging in road trips and camping activities annually. Modern travelers increasingly rely on electronic devices such as smartphones, tablets, and GPS units, which require regular charging in remote locations where grid power is unavailable. Jump starters equipped with high capacity lithium ion batteries and multiple USB ports address this need by providing a dual purpose solution for both vehicle emergencies and personal device charging. The popularity of van life and overlanding has further amplified this trend as enthusiasts seek compact and efficient power solutions for extended off grid stays. Manufacturers have responded by designing rugged and weather resistant units that can withstand the demands of outdoor environments. The integration of additional features such as LED flashlights and air compressors enhances the value proposition for adventurers who prioritize preparedness. Social media platforms showcase these lifestyles, influencing consumer behavior and driving interest in premium portable power products. As the culture of exploration and self-sufficiency grows, the jump starter market benefits from its positioning as an essential tool for modern explorers who value connectivity and safety in equal measure.

MARKET RESTRAINTS

Stringent Safety Regulations for Lithium Ion Batteries Restrict Product Availability

Stringent safety regulations governing the transport and storage of lithium ion batteries are significantly hampering the growth of the European jump starter market. According to the European Agreement concerning the International Carriage of Dangerous Goods by Road, specific classification and packaging requirements apply to lithium batteries due to their potential fire hazard. These regulations complicate logistics for manufacturers and retailers, requiring specialized handling and documentation, which increases operational expenses. Small and medium sized enterprises often struggle to meet these rigorous standards, which is leading to a consolidation of the market among larger players with greater resources. The risk of non-compliance can result in severe penalties and product recalls, discouraging innovation and rapid market entry for new designs. Consumers may also face restrictions when traveling with certain types of jump starters on public transport or airlines, limiting their utility for some users. The complexity of regulatory frameworks varies across different European countries, creating a fragmented landscape that hinders seamless distribution. Retailers must invest in staff training and infrastructure to ensure safe storage and sale of these products, further adding to overheads. These barriers slow down the proliferation of advanced high capacity models as companies prioritize compliance over feature expansion. The resulting increase in retail prices may deter price sensitive consumers from upgrading to newer technologies, thereby slowing market growth and limiting consumer choice.

High Prevalence of Roadside Assistance Services Reduces Urgency for Ownership

The widespread availability and affordability of roadside assistance services in Europe reduce the urgency for individual consumers to purchase personal jump starters, which is further hampering the regional market expansion. For instance, the General German Automobile Club, ADAC, has over 21 million members who rely on professional help for battery issues. Many new vehicle purchases include complimentary roadside assistance packages for several years and creating a perception of security that diminishes the perceived need for personal emergency tools. Consumers often view jump starters as redundant if they already have access to reliable and timely professional support. The convenience of a phone call versus the effort of maintaining and charging a personal device influences buying decisions, particularly among urban dwellers who rarely venture into remote areas. Insurance policies frequently cover breakdown services, further embedding this dependency in consumer behavior. The high quality of infrastructure in Western Europe means that help is usually never far away, reducing the anxiety associated with battery failure. This cultural reliance on external support structures acts as a psychological barrier to market penetration. Manufacturers must work harder to educate consumers on the immediate benefits of self reliance, such as time savings and independence. Until the value proposition of instant access outweighs the convenience of service contracts, the market faces headwinds from established assistance networks that dominate the breakdown response landscape.

MARKET OPPORTUNITIES

Integration with Smart Vehicle Diagnostics and IoT Offers Growth Potential

The integration of jump starters with smart vehicle diagnostics and Internet of Things capabilities is a significant opportunity for differentiation and value addition in the Europe jump starter market. Modern consumers are increasingly tech savvy and seek devices that provide insights into vehicle health beyond simple power delivery. According to the European Automobile Manufacturers Association, 80% of new vehicles sold in Europe are expected to be connected by 2026, which enables real time monitoring of battery status and performance. Jump starters equipped with Bluetooth connectivity and companion apps can analyze battery health, predict failures, and offer maintenance tips, enhancing user engagement and loyalty. This technological convergence transforms a passive emergency tool into an active vehicle management system, appealing to early adopters and automotive enthusiasts. Manufacturers can leverage data analytics to offer personalized recommendations and preventive care services, creating new revenue streams through subscription models. The ability to diagnose issues before they leave a driver stranded adds substantial value, justifying premium pricing. Partnerships with automotive service providers can facilitate seamless booking of repairs based on diagnostic data, further integrating the device into the broader ecosystem. As vehicles become more connected, the demand for compatible accessories that enhance this connectivity grows. By embracing smart technology, companies can capture a niche segment of consumers who prioritize intelligence and convenience. This innovation pathway allows brands to stand out in a crowded market by offering superior functionality and user experience.

Expansion into Electric and Hybrid Vehicle Support Solutions Drives Innovation

The rapid expansion of the electric and hybrid vehicle sector in Europe creates a unique opportunity for jump starter manufacturers to develop specialized products tailored to high voltage systems. According to the International Energy Agency, electric car sales in Europe increased by nearly 20% in 2023, accounting for a significant share of new registrations. While these vehicles do not have traditional internal combustion engines, they still utilize 12 volt auxiliary batteries that can fail, leaving the car immobilized. Standard jump starters may not be suitable or safe for use with electric vehicles due to different electrical architectures and safety protocols. Developing certified and safe solutions for this growing segment allows companies to tap into a lucrative and underserved market. Educating consumers about the specific needs of electric vehicle batteries positions brands as trusted experts in the evolving automotive landscape. Collaborations with electric vehicle manufacturers can lead to bundled offerings or recommended accessory lists, enhancing visibility and credibility. The premium nature of electric vehicles often correlates with a willingness to invest in high quality accessories, supporting higher margin products. As the fleet of electric and hybrid cars expands, the demand for compatible emergency power solutions will grow in tandem. By focusing on this emerging segment, manufacturers can future proof their portfolios and establish leadership in the next generation of automotive support tools. This strategic pivot aligns with broader sustainability goals and technological trends in the European automotive industry.

MARKET CHALLENGES

Counterfeit Products and Quality Variability Undermine Consumer Trust

The prevalence of counterfeit products and significant variability in quality standards undermine consumer trust and is a serious challenge to the Europe jump starter market. Online marketplaces are flooded with inexpensive imitations that often fail to meet safety and performance specifications, leading to dangerous situations such as fires or explosions. According to the European Union Intellectual Property Office, counterfeiting and piracy cost the EU 16 billion euros in lost sales annually across various sectors, including automotive accessories. Consumers who purchase substandard products may experience failure during critical moments, leading to negative perceptions of the entire category. Legitimate manufacturers struggle to compete with the low prices of counterfeiters who bypass safety testing and quality control measures. This price distortion squeezes margins for compliant companies and reduces incentives for innovation. The lack of uniform enforcement across borders complicates efforts to remove fake products from circulation. Negative reviews and social media reports of faulty devices can damage brand reputations even for reputable companies if consumers confuse them with inferior alternatives. Ensuring authenticity requires significant investment in branding, packaging, and customer education, which adds to operational costs. The risk of liability from unsafe products also increases insurance premiums for legitimate businesses. Addressing this challenge requires collaborative efforts between industry associations, regulators, and online platforms to enforce stricter verification processes. Until consumer confidence is restored through consistent quality and safety assurance, the market faces hurdles in achieving its full potential.

Supply Chain Volatility for Rare Earth Materials Impacts Production Costs

Supply chain volatility for rare earth materials and lithium components impacts production costs and stability in the Europe jump starter market. The manufacturing of high performance lithium ion batteries relies on raw materials such as lithium, cobalt, and nickel, which are subject to geopolitical tensions and fluctuating global prices. According to the European Commission, the EU currently imports 100% of its refined lithium from outside the region, which poses a strategic vulnerability for the European battery industry. Disruptions in supply chains due to trade disputes or logistical bottlenecks can lead to shortages and price spikes, affecting profitability. Manufacturers face difficulties in forecasting costs and maintaining consistent pricing for retailers and consumers. The transition to sustainable sourcing practices further complicates procurement, as companies seek to verify ethical and environmental standards in their supply chains. These complexities require robust risk management strategies and diversification of supplier bases, which can be resource intensive. Small and medium sized manufacturers are particularly vulnerable to these fluctuations as they lack the bargaining power of larger corporations. The resulting instability can delay product launches and limit inventory availability during peak demand seasons. Additionally, the push for local battery production in Europe, while beneficial in the long term, requires significant upfront investment and time to mature. Until domestic supply chains are fully established, the market remains exposed to external shocks that hinder growth and competitiveness. Managing these supply side risks is crucial for sustaining long term viability and meeting consumer demand effectively.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 21.54% |

| Segments Covered | By Product, Battery, Vehicle and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Key Market Players | Clore Automotive, Stanley Black & Decker, Inc., NOCO Company, Schumacher Electric Corporation, CTEK Holding AB, Ring Automotive Ltd, Robert Bosch GmbH, Einhell Germany AG, DBPOWER, and NEXPOW |

SEGMENTAL ANALYSIS

By Battery Technology Insights

The lithium ion segment led the market and accounted for 61.5% of the European market share in 2025. The dominance of lithium-ion segment in the European market is attributed to the superior energy density and compact form factor of lithium ion batteries compared to traditional lead acid alternatives. According to the European Battery Alliance, lithium ion batteries have an energy density that is roughly 125 to 600 Wh/L allows manufacturers to produce devices that are significantly lighter and easier to store in vehicle glove compartments or trunks. The convenience of portability is a critical factor for urban drivers who prioritize space efficiency and ease of handling. Lithium ion jump starters can deliver high peak currents required to start modern engines despite their small size, making them ideal for passenger cars and light commercial vehicles. The rapid charging capability of lithium ion cells also appeals to consumers who value quick turnaround times. As per data from consumer electronics associations, the adoption of lithium based power banks has normalized the use of this technology for automotive applications, reducing consumer hesitation. The longevity of lithium ion batteries with hundreds of charge cycles further enhances their value proposition. Manufacturers have invested heavily in safety features such as smart clamps and reverse polarity protection to mitigate risks associated with lithium chemistry. These advancements have built consumer trust and solidified the segment's leadership. The aesthetic appeal of sleek modern designs also contributes to higher sales volumes among younger demographics who prefer technologically advanced accessories.

However, the lithium polymer segment within the broader lithium category is projected to register the highest CAGR of 8.8% during the forecast period due to the advancements in battery chemistry that offer even greater flexibility in shape and size along with enhanced safety profiles. Lithium polymer batteries can be manufactured in thin and flexible forms, allowing for innovative product designs that integrate seamlessly into multi-functional tools. According to the Journal of Power Sources, lithium polymer batteries are safer due to their gel-like electrolyte, which significantly reduces the risk of leakage and thermal runaway compared to standard lithium ion cylindrical cells. This technological advantage is particularly appealing in the European market where safety standards are stringent. The ability to customize battery shapes enables manufacturers to create ultra-compact jump starters that fit into pocket sizes or integrate with other automotive accessories like tire inflators. The growing demand for multifunctional devices drives this segment as consumers seek all in one solutions for roadside emergencies. Marketing campaigns highlighting the slim profile and premium build quality attract tech savvy buyers. As per retail trends, online sales of compact high performance jump starters have surged, indicating strong consumer preference for these advanced units. The integration of fast charging technologies such as USB C Power Delivery further enhances usability. Collaborations with consumer electronics brands help legitimize these products as essential gadgets rather than just automotive tools. This convergence of automotive and consumer electronics trends propels the lithium polymer segment to the forefront of market growth.

By Vehicle Type Insights

The passenger cars segment held the dominant share of 68.5% of the regional market in 2025. The dominance of passenger cars segment in the European market is attributed to the high volume of private vehicle ownership across the continent. According to the European Automobile Manufacturers Association, there are 252 million passenger cars on EU roads, creating a vast potential customer base. Private car owners are the primary purchasers of portable jump starters as they seek independence from roadside assistance services for minor battery issues. The frequency of short trips and stop start driving conditions in urban areas accelerates battery drain, increasing the likelihood of unexpected failures. This demographic is highly sensitive to convenience and portability, favoring compact lithium ion devices that can be easily stored. The rising cost of professional breakdown services encourages individuals to invest in one time purchase solutions that offer long term savings. Insurance premiums and membership fees for automotive clubs add to the total cost of ownership, making self-sufficiency an attractive alternative. As per consumer surveys, a significant portion of drivers express anxiety about being stranded due to battery failure, motivating proactive purchases. The widespread availability of affordable entry level jump starters in supermarkets and online platforms further boosts penetration in this segment. Marketing efforts targeting family safety and emergency preparedness resonate strongly with this audience. The sheer scale of the passenger car fleet ensures consistent demand regardless of economic fluctuations. Manufacturers focus on user friendly designs with clear instructions to cater to non-technical users. This broad appeal sustains the segment's leadership position in the market.

On the other end, the commercial vehicles segment is expected to grow at a healthy CAGR of 7.2% over the forecast period in the European market owing to the rising need for operational efficiency and minimized downtime in logistics and transport sectors. According to Eurostat, road freight transport in the EU recorded 1,920 billion tonne-kilometres in 2022, highlighting the critical importance of vehicle reliability. Fleet managers prioritize tools that enable quick resolution of battery issues to avoid delivery delays and costly towing services. Heavy duty jump starters with higher capacity and durability are essential for trucks, buses, and vans, which have larger engines and higher electrical loads. The professional nature of this segment demands robust equipment that can withstand frequent use and harsh working conditions. Companies are increasingly equipping their fleets with standardized emergency kits, including high performance jump starters, as part of preventive maintenance strategies. Regulatory requirements for driver safety and emergency preparedness also mandate the presence of such tools in commercial vehicles. As per industry benchmarks, reducing vehicle downtime by even a few hours can result in significant cost savings for logistics operators. The shift towards just in time delivery models increases pressure on maintaining strict schedules, which is further incentivizing investment in reliable starting solutions. B2B sales channels and partnerships with fleet management software providers facilitate targeted distribution. The emphasis on total cost of ownership rather than initial price drives demand for premium durable units. This strategic approach ensures steady growth in the commercial segment.

By Distribution Channel Insights

The online retail segment dominated the market by capturing 51.6% of the regional market share in 2025. This dominance is driven by the convenience of home delivery, extensive product variety, and competitive pricing available on digital platforms. According to Eurostat, 75% of internet users in the EU bought or ordered goods or services online in 2023, with a significant portion of consumers preferring to research and purchase automotive accessories online. Online marketplaces allow customers to compare specifications, read user reviews, and access detailed product information, which is crucial for technical items like jump starters. The ability to find niche products and specialized models that may not be available in local stores attracts enthusiasts and professional users. Competitive pricing strategies, including discounts and bundle offers, further incentivize online purchases. The rise of mobile shopping apps has made it easier for consumers to buy emergency tools on the go. Logistics improvements such as next day delivery services enhance the appeal of online channels for urgent needs. As per data from major e commerce platforms, automotive accessories are among the top growing categories, reflecting changing consumer habits. Direct to consumer brands leverage social media marketing to reach targeted audiences effectively. The transparency of online ratings helps build trust in new brands. The elimination of geographical barriers allows manufacturers to reach customers in remote areas. This accessibility and convenience sustain the online segment's leadership.

On the other hand, the offline retail segment remains relevant for immediate purchase needs. For instance, physical stores account for 45% of sales, primarily driven by consumers who require instant availability during emergencies. Brick and mortar locations provide the advantage of tactile inspection, allowing customers to assess build quality and size before purchasing. Trusted automotive chains offer expert advice and installation services, which add value for less technically inclined buyers. The immediacy of resolving a breakdown situation often outweighs the convenience of online shopping for stranded drivers. Supermarkets and hypermarkets stock entry level jump starters as impulse buys during seasonal promotions. The presence of established brands in physical retail builds credibility and brand recognition. As per retail footfall data, 1 in 5 European consumers still prefer shopping in person for automotive parts to ensure they get the right item. Local partnerships with repair shops also drive sales through recommendations. However, the limited shelf space restricts the variety of models available compared to online platforms. Higher overhead costs often result in slightly higher prices. Despite these challenges, the tangible experience and immediate gratification offered by offline retail ensure its continued relevance in the market ecosystem.

REGIONAL ANALYSIS

Germany Jump Starter Market Analysis

Germany stood as the largest market for jump starters in Europe and occupied 24.2% of the European market share in 2025. The dominance of Germany in the European market is driven by a strong automotive culture and high vehicle ownership rates. According to the Federal Motor Transport Authority, there were 49.1 million passenger cars registered in Germany in 2024, creating a massive user base. German consumers are known for their preference for high quality engineering and reliability, making them willing to invest in premium jump starter brands. The country is home to major automotive manufacturers, which fosters a deep interest in vehicle maintenance and accessories. The well developed infrastructure of autobahns and long distance commuting increases the likelihood of battery related issues, necessitating reliable emergency tools. Strict safety standards enforced by German regulatory bodies ensure that only high quality products reach the market, enhancing consumer trust. The presence of leading auto parts retailers, such as ATU and Bosch Car Service, facilitates wide distribution and accessibility. Economic stability supports discretionary spending on automotive accessories. The popularity of road trips and outdoor activities further boosts demand for portable power solutions. German manufacturers also contribute to innovation in battery technology, influencing global trends. The combination of technical expertise, high ownership, and robust retail networks positions Germany as the dominant player in the European jump starter market.

United Kingdom Jump Starter Market Analysis

The United Kingdom was another major regional segment in the European market in 2025. The growth of the UK in the European market can be driven by an aging vehicle fleet and unpredictable weather conditions. According to the Society of Motor Manufacturers and Traders, the average age of cars in the UK has reached 9 years, increasing the frequency of battery failures. The damp and cold climate exacerbates battery degradation, particularly during winter months, leading to seasonal spikes in demand for jump starters. British consumers increasingly value self sufficiency due to the high cost and variable response times of roadside assistance services. The proliferation of online retail platforms has made it easier for consumers to access a wide range of products. Major automotive clubs, such as the AA and RAC, promote awareness of emergency preparedness, influencing buying behavior. The dense urban population in cities like London creates demand for compact and portable devices suitable for small vehicles. Government initiatives promoting electric vehicle adoption also create opportunities for specialized jump starters compatible with hybrid systems. The strong presence of DIY culture encourages individuals to handle minor vehicle issues independently. Retail partnerships with supermarkets and hardware stores enhance visibility. The combination of climatic challenges and economic factors drives the robust performance of the jump starter market in the United Kingdom.

France Jump Starter Market Analysis

France is predicted to showcase a healthy CAGR in the European jump starter market during the forecast period owing to its extensive road network and vibrant tourism sector. According to the French Ministry of Ecological Transition, France has a road network of 1.1 million kilometers, which is one of the largest in Europe, facilitating millions of journeys annually. The popularity of road trips and holidays in rural areas increases the need for reliable emergency tools among both residents and visitors. French consumers appreciate stylish and multifunctional devices that align with their lifestyle preferences. The presence of major automotive retailers, such as Norauto and Midas, ensures widespread availability of jump starters. Seasonal variations in weather, particularly in mountainous regions, create specific demand peaks during winter. The government's focus on road safety encourages drivers to carry emergency equipment, including jump starters. The growing trend of van life and camping in France boosts sales of portable power banks with jumping capabilities. Manufacturers focus on localized marketing and distribution strategies to capture diverse consumer segments. The emphasis on high safety standards and product durability resonates with French buyers. France’s strategic position as a transit hub for European tourism further supports the consistent demand for vehicle maintenance accessories. The steady growth of the French automotive aftermarket sector provides a favorable environment for the jump starter market.

COMPETITIVE LANDSCAPE

The competition in the Europe jump starter market is characterized by a mix of established automotive brands and specialized electronics manufacturers striving for market share through innovation and brand recognition. Major players compete on the basis of safety features portability and multifunctionality to attract diverse consumer segments. The market sees intense rivalry in the mid range segment where price sensitivity and feature comparison drive purchasing decisions. Companies leverage their existing brand equity in the automotive or tools sectors to gain consumer trust and facilitate market entry. Niche players focus on specialized high performance units for professional use or extreme conditions differentiating themselves from general consumer products. The rise of e commerce has lowered barriers to entry allowing new brands to reach customers directly but also increasing price transparency and competition. Regulatory compliance regarding battery safety and transport serves as a critical differentiator with reputable brands using certification as a marketing advantage. Innovation in battery technology such as solid state batteries presents future competitive opportunities. Strategic alliances with automotive service providers and insurance companies help established players secure recurring revenue streams. The dynamic nature of consumer preferences towards convenience and sustainability drives continuous product evolution. This competitive environment fosters rapid technological advancements and offers consumers a wide variety of reliable and efficient starting solutions.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Jump Starter Market include

- Clore Automotive

- Stanley Black & Decker, Inc.

- NOCO Company

- Schumacher Electric Corporation

- CTEK Holding AB

- Ring Automotive Ltd

- Robert Bosch GmbH

- Einhell Germany AG

- DBPOWER

- NEXPOW

Top Players in the Europe Jump Starter Market

NOCO Company

NOCO Company is a prominent leader in the Europe jump starter market renowned for its ultra-safe lithium ion jump starters and portable power stations. The company contributes significantly to the global market by setting high standards for safety and performance with its Genius Boost series. Recent actions include the expansion of its distribution network across major European retailers and online platforms to enhance product accessibility. NOCO has invested heavily in marketing campaigns that emphasize the reliability and compact design of its devices appealing to both professional mechanics and everyday drivers. The company continues to innovate by integrating advanced features such as USB C fast charging and digital displays into its latest models. Strategic partnerships with automotive clubs and insurance providers have strengthened its brand presence and credibility. By focusing on user friendly designs and robust safety protections NOCO maintains its position as a trusted choice for consumers seeking dependable emergency starting solutions. Its commitment to quality and innovation ensures sustained growth and customer loyalty in the competitive European landscape.

Stanley Black and Decker Inc

Stanley Black and Decker Inc holds a strong position in the Europe jump starter market leveraging its extensive portfolio of tools and automotive accessories under brands such as Stanley and DeWalt. The company contributes to the global market by offering durable and versatile jump starters that appeal to DIY enthusiasts and professional users. Recent actions involve the launch of new lithium ion models with higher peak currents and integrated air compressors catering to diverse consumer needs. Stanley Black and Decker has enhanced its supply chain efficiency to ensure consistent product availability across European markets. The company utilizes its established retail relationships to secure prominent shelf space in hardware stores and automotive centers. Investment in digital marketing and e commerce platforms has expanded its reach to younger demographics. By combining brand recognition with functional innovation Stanley Black and Decker reinforces its market leadership. Its focus on durability and multi functionality resonates with consumers who value practical and long lasting automotive tools.

Michelin Group

Michelin Group is a key player in the Europe jump starter market capitalizing on its strong brand equity in the automotive sector. The company contributes to the global market by offering a range of portable jump starters and battery chargers that align with its reputation for quality and safety. Recent actions include the introduction of smart jump starters with Bluetooth connectivity and mobile app integration for real time battery monitoring. Michelin has expanded its product line to include eco friendly packaging and energy efficient designs reflecting its commitment to sustainability. The company leverages its extensive network of tire centers and service partners to promote and distribute its jump starter products. Strategic collaborations with automotive manufacturers have led to bundled offerings that enhance value for customers. By focusing on technological advancement and brand trust Michelin strengthens its competitive position. Its ability to integrate digital features with traditional automotive expertise appeals to modern consumers seeking smart and reliable solutions for vehicle maintenance.

Top Strategies Used by the Key Market Participants

Key players in the Europe jump starter market primarily focus on product differentiation through the integration of advanced safety features and multifunctional capabilities. Companies invest in research and development to create compact lithium ion devices with high peak currents and rapid charging technologies. Strategic partnerships with automotive retailers and online marketplaces enhance distribution reach and brand visibility. Manufacturers emphasize digital marketing campaigns to educate consumers about the benefits of portable jump starters over traditional methods. Expansion into adjacent product categories such as tire inflators and power banks allows companies to offer comprehensive roadside emergency kits. Sustainability initiatives including recyclable packaging and energy efficient designs align with European regulatory standards and consumer preferences. After sales support and warranty services are enhanced to build customer trust and loyalty. Supply chain optimization strategies mitigate risks associated with raw material shortages and logistical disruptions. These holistic approaches enable companies to maintain competitive advantages and drive market growth in the evolving automotive accessory landscape.

MARKET SEGMENTATION

This research report on the Europe Jump Starter Market has been segmented and sub-segmented based on the following categories.

By Product

- Jump Boxes

- Plug In Units

By Battery

- Lithium-Ion Battery

- Lead Acid Battery

By Vehicle

- Passenger Cars

- Light Commercial Vehicle (LCV)

- Heavy Commercial Vehicle (HCV)

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com