Europe LEO Satellite Market Research Report By Type (Small Satellites and Medium Satellites), Application (Earth Observation and Communication), End Use (Military and Government, and Commercial), and Country (France, Germany, United Kingdom, Italy, Sweden, and Rest of Europe) – Industry Analysis, Size, Share, Trends, and Growth Forecast (2026 to 2034)

Europe LEO Satellite Market Size

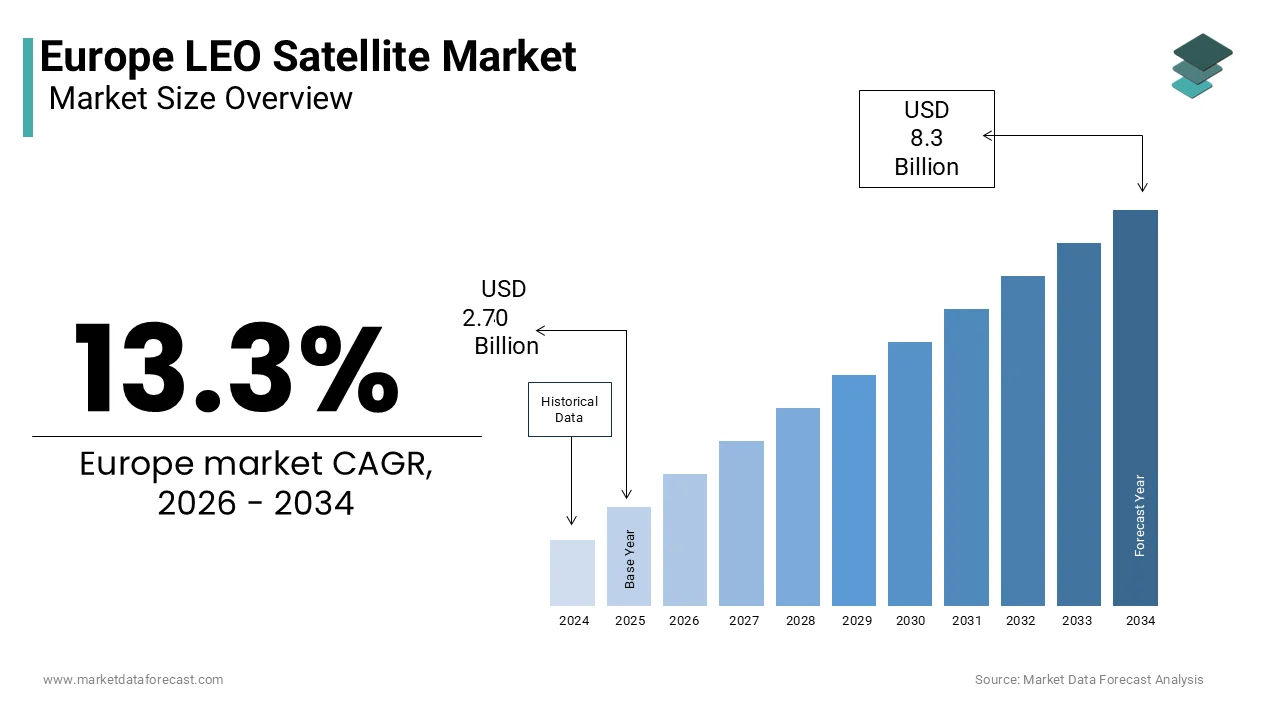

The europe LEO satellite market was valued at USD 2.70 billion in 2025, is expected to reach USD 3.06 billion in 2026, and is growing at a CAGR of 13.3% It is projected to reach USD 8.3 billion by 2034.

A Low Earth Orbit (LEO) satellite is defined as one orbiting at an altitude of 500 to 2,000 kilometers. These satellites are crucial for modern applications because their proximity to Earth allows for low-latency communication, high-resolution Earth observation, and fast data transmission. Unlike geostationary systems, LEO satellites offer lower latency and higher signal strength, enabling real-time applications in defense, maritime monitoring, and rural broadband access. Europe’s strategic interest in sovereign space infrastructure has intensified following geopolitical shifts that underscore reliance on non-European constellations. As per research, the global number of active LEO satellites has risen dramatically, exceeding 11,700 by May 2025, driven largely by commercial initiatives such as SpaceX's Starlink. The European Union’s IRIS² program aims to launch a secure governmental LEO constellation by 2027 to serve defense and critical infrastructure needs. This complements existing European efforts in Earth observation, such as the EU's Copernicus program (managed by the European Commission and ESA), which operates a fleet of Sentinel satellites providing near-real-time data on land use, air quality, and maritime surveillance. National space agencies, including CNES in France and DLR in Germany, have also accelerated smallsat launch cadences through partnerships with Arianespace and emerging launch providers. This institutional foundation, combined with new regulatory frameworks for spectrum allocation and orbital slot coordination, is shaping a distinct European LEO ecosystem focused on resilience, autonomy multi-mission utility.

MARKET DRIVERS

EU’s Push for Digital Sovereignty Is Accelerating Indigenous LEO Constellation Development

The European Union’s strategic imperative to achieve digital sovereignty has emerged as a major driver for the European LEO satellite market. Following disruptions in global supply chains and concerns over reliance on non-European satellite internet providers, the EU launched the IRIS² (Infrastructure for Resilience Interconnectivity and Security by Satellite) initiative, with the regulation adopted in March 2023. The total cost of the project is estimated at €10.6 billion via a public-private partnership (PPP). As per the European Commission and the EU Agency for the Space Programme (EUSPA), this sovereign, multi-orbital constellation will comprise 290 satellites (264 LEO and 18 MEO) by 2030 to provide secure, encrypted communications for government, military, and critical infrastructure entities, including energy grids, transport networks, and healthcare systems. Unlike commercial broadband constellations, IRIS² prioritizes cybersecurity interoperability with existing EU digital infrastructure, such as the GAIA-X cloud framework, and compliance with the EU’s stringent data protection regulations under GDPR. The institutional demand creates a guaranteed market for European satellite manufacturers such as Airbus, Thales, and OHB while fostering a domestic ecosystem for component suppliers and cybersecurity integrators.

Expanding Demand for Real-Time Earth Observation in Climate and Security Applications

The region’s intensifying focus on climate resilience and border security is causing demand for high revisit rate Earth observation from LEO satellites. As per research, the Copernicus program, supported by the European Environment Agency, now uses many low Earth orbit imaging satellites, including the Sentinel series, which continuously collect vast amounts of information about the environment. This data informs EU policy on wildfire monitoring, flood forecasting, and illegal fishing detection with low latency for emergency response. The European Maritime Safety Agency uses satellite radar pictures to watch where ships are going in major European seas, which helps identify a significant number of suspicious unflagged or dark vessels. Similarly, the European Border and Coast Guard Agency, Frontex, has started using satellite monitoring for its border watch efforts, which allows it to find unauthorized migrant boats shortly after they leave from the Northern African coastlines. Individual national agencies are also increasing their capabilities. Germany’s DLR space agency launched a satellite to monitor the health of soil and crops across the EU farming area, while France’s CNES agency runs its own group of satellites that provide very detailed pictures for planning cities and responding to disasters. These applications require frequent orbital passes only achievable through dense LEO constellations, which in turn drive demand for smallsat manufacturing launch services and AI-powered analytics platforms across the European space value chain.

MARKET RESTRAINTS

High Capital Intensity and Fragmented Launch Access Constrain Commercial Scalability

Issues related to capital intensity and limited autonomous launch capacity are constraining the European LEO satellite market. Developing, deploying, and operating a commercial LEO constellation for broadband services requires substantial upfront investment, typically reaching into the hundreds of millions or billions of euros, depending on the network's scale and technology. As per the European Investment Bank, there has been general investor caution in high-tech sectors with long payback horizons, which affects funding for many European space startups, especially in later funding stages. Compounding this financial barrier is Europe’s lack of regular low-cost launch options following the retirement of Vega C in 2023 and delays in Ariane 6 operational readiness. In 2025, European launch capabilities were limited compared to global activity, with the European Space Agency relying on a mix of domestic launches (like the Vega C return to flight) and the use of foreign launch providers such as SpaceX for some missions. This dependence on non-European launch providers introduces schedule risks, export control complications, and higher insurance premiums. European LEO ventures remain vulnerable to external bottlenecks, undermining their ability to compete with vertically integrated U.S. constellations that control both satellites and launch, without reliable, affordable, and sovereign access to orbit.

Spectrum Allocation and Orbital Debris Mitigation Imposing Regulatory Burdens

Intensified regulatory scrutiny on these satellites in the region, particularly around radio frequency spectrum rights and end-of-life deorbiting compliance, hampers the expansion of the European LEO satellite market. The International Telecommunication Union (ITU) requires operators to coordinate frequency usage to prevent interference. However, the proliferation of large non-geostationary orbit (NGSO) satellite constellations in low Earth orbit (LEO) has led to increased congestion and a greater potential for radio interference in key frequency bands such as Ka and Ku. National authorities are implementing extended review periods for new satellite applications, which is slowing down the launch of new services. Simultaneously, the European Space Agency has introduced strict requirements for satellites to leave orbit within 5 years after their mission ends. All low Earth orbit satellites launched must be equipped with a propulsion system for a controlled return to Earth, as enforced by new space legislation. These regulatory layers, while environmentally and technically justifiable, create compliance overheads that disproportionately affect small and medium-sized European space firms lacking dedicated legal and systems engineering teams. Without harmonized EU-wide licensing and streamlined debris mitigation pathways, the administrative burden may stifle innovation and deter private capital despite strong strategic demand.

MARKET OPPORTUNITIES

Integration of LEO Connectivity into EU Smart Agriculture and Rural Broadband Programs

The European Union’s Common Agricultural Policy and Digital Europe Programme are creating new opportunities for the European LEO satellite market. As per sources, a significant number of rural communities across the European Union do not have access to dependable high-speed internet because traditional fiber optic lines are too expensive to install in sparsely populated regions. Also, the EU is providing financial support through specific funding programs to bring satellite-based internet services to public facilities like schools and clinics in these underserved areas. Parallelly, the use of digital tools for field monitoring is now a prerequisite for farmers to receive the majority of their direct financial assistance, which reflects a push by European agricultural policy to encourage modern farming techniques. LEO constellations with high revisit rates and low latency enable real-time data transmission from IoT sensors on tractors and fields to cloud analytics platforms. New technology trials in countries like France have demonstrated that connecting farms using satellites can help optimize resource use, such as reducing the amount of fertilizer needed. These institutional use cases guarantee revenue streams for European LEO operators while demonstrating cross-sectoral value beyond traditional telecom applications. The EU’s emphasis on data sovereignty further ensures preference for constellations under European jurisdiction, accelerating market formation in non-defense segments.

Emergence of On-Orbit Servicing and In-Space Manufacturing as New Value Chains

The region is positioning itself at the forefront of next-generation LEO services through investments in on-orbit servicing and in-space manufacturing capabilities, which are setting up fresh prospects for the expansion of the European LEO satellite market. As per research, European space organizations are developing robotic servicing capabilities, as demonstrated by a project that successfully refueled a simulated satellite in orbit, which helps to extend mission life. This capability is critical for high-value governmental and Earth observation satellites where launch replacement is prohibitively expensive. Concurrently, there is a growing emphasis on the potential for in-space manufacturing, exemplified by a German project aimed at creating materials in microgravity that offer superior performance compared to those made on Earth. Such innovations could transform LEO from a passive infrastructure layer into an active industrial zone. On-orbit assembly is emerging as a significant trend, with some national initiatives supporting commercial companies in building large structures like telescopes in the space environment. The European Union is providing considerable financial support to boost the development of orbital servicing technologies, which emphasizes a commitment to reducing space debris and promoting sustainable space activities. These emerging capabilities create high-margin ancillary markets for European aerospace firms beyond satellite manufacturing and launch, offering resilience against commoditization in broadband LEO segments dominated by global players.

MARKET CHALLENGES

Inter-Satellite Link Standardization Remains Technologically Fragmented

A lack of interoperable inter-satellite link (ISL) standards hinders seamless data relay and network resilience. This poses a major impediment to the European LEO satellite market. Unlike U.S. competitors that have deployed optical laser crosslinks across entire constellations, European missions largely rely on ground station relay, introducing latency and coverage gaps. The absence of a common data routing protocol across civil, IL, military, and commercial European constellations prevents mesh networking, which is essential for time-critical applications like battlefield communications or disaster response. The European Space Agency’s ScyLight program has funded optical ISL development, but progress remains siloed across national champions Airbus, Thales, and Leonardo, with incompatible modulation schemes and encryption frameworks. LEO operators must either build redundant ground infrastructure or accept performance penalties compared to integrated global networks, unless the EU mandates technical harmonization. This fragmentation also complicates participation in international missions such as NATO’s space surveillance initiatives, where data fusion across allied assets is critical. Europe's LEO systems will struggle to achieve the autonomy, throughput, and latency needed for strategic autonomy in space until unified ISL (Inter-Satellite Link) standards are adopted.

Workforce and Supply Chain Gaps Threaten Long-Term Industrial Competitiveness

Acute shortages in specialized aerospace talent and vulnerable component supply chains essential for scalable LEO satellite production, despite strong policy support, further obstruct the expansion of the European LEO satellite market. As per studies, there is a deficit of engineers in RF systems, propulsion, propulsion space-qualified software across EU member states, with only 35 percent of university space programs offering LEO-specific curricula. This talent gap slows innovation and increases reliance on expatriate hiring, which is increasingly restricted under national security regulations and defense-linked programs like IRIS². Simultaneously, Europe imports a share of critical components, including radiation-hardened processors high high-efficiency solar cells, and reaction wheels, primarily from the United States and Japan, as per research. Europe’s goal of strategic autonomy in LEO, despite ambitious constellation plans, is at risk because a lack of coordinated investment in STEM education, dual-use component manufacturing, and trusted foundries leaves it dependent on external suppliers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, End Use, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Airbus Defence and Space, Thales Alenia Space, Surrey Satellite Technology Ltd. (SSTL), OHB SE, RUAG Space, GomSpace Group AB, AAC Clyde Space, ISISPACE Group, EnduroSat AD, NanoAvionics, Exotrail SAS, Telespazio S.p.A., Eutelsat Communications S.A., SES S.A., Leonardo S.p.A., Spire Global Inc., OneWeb Ltd., Planet Labs PBC, SpaceX (Starlink), D-Orbit S.p.A. |

SEGMENTAL ANALYSIS

By Type Insights

The small satellites segment dominated the European LEO satellite market and accounted for a substantial share in 2025. The dominance of the small satellites segment is attributed to their cost efficiency, rapid development cycle, and suitability for constellation deployment. As per studies, many small satellites were launched by European entities between 2020 and 2025, accounting for a share of all European LEO missions. This prevalence stems from institutional reliance on CubeSat and microsat platforms for Earth observation, scientific research, and technology demonstration. Apart from these, national space agencies favor smallsats for agile mission profiles. Europe’s institutional and startup sectors continue to prioritize small platforms for scalable, responsive, and modular space infrastructure, supported by launch providers like Arianespace offering dedicated smallsat rideshare missions on Vega and emerging vehicles.

The medium satellites segment is likely to experience the fastest CAGR of 24.7% from 2025 to 2033. The rapid acceleration of the medium satellites segment is driven by the IRIS² secure communications program and next-generation Earth observation missions requiring higher power propulsion and payload capacity than smallsats can support. Unlike small platforms, medium satellites accommodate advanced phased array antennas high resolution optical payload, and electric propulsion systems essential for multi-year LEO operations. Enhanced radiation shielding, longer design life, and greater data throughput capabilities are enabling medium satellites to become the essential backbone of Europe's strategic LEO infrastructure.

By Application Insights

In 2025, the earth observation segment captured the leading share of 52.1% of the European LEO satellite market. Institutional mandates for environmental monitoring, security surveillance, and agricultural management have mainly contributed to the growth of the earth observation segment. As per sources, the number of European low-Earth orbit (LEO) imaging satellites is increasing, significantly boosting the amount of data available to a growing number of public and private users. This dominance is supported by EU regulations requiring member states to utilize Copernicus data for climate reporting under the European Green Deal. National agencies further amplify demand. The European Union is committed to the continued expansion of these initiatives, as demonstrated by substantial funding and plans for future missions dedicated to new areas like carbon monitoring. Europe’s reliance on OLEO-based Earth observation will continue to anchor the market.

The communication application segment is on the rise and is expected to be the fastest-growing segment in the regional market by witnessing a CAGR of 31.2% during the forecast period, owing to the IRIS² sovereign broadband initiative and rural connectivity mandates. Unlike Earth observation on which is institutionally mat, communication is undergoing rapid transformation as Europe seeks to reduce dependence on non-European mega constellations. As per research, Europe is establishing its own low-Earth orbit (LEO) secure communication network for government, military, and critical infrastructure use, with initial service anticipated to begin in 2027 and full operation around 2030. Significant financial support is being directed towards this initiative, specifically for the development of ground infrastructure and user equipment subsidies. Concurrently, Funding has been set aside to expand satellite broadband access to numerous communities across Europe that currently lack terrestrial internet options. National efforts complement this. Next-generation European LEO satellites are designed to offer high-speed, low-latency connectivity, which indicates an intention to serve a wide range of both strategic public sector and commercial market needs.

By End Use Insights

The military and government segment led the European LEO satellite market by occupying a 61.1% share in 2025. Factors such as Europe’s prioritization of strategic autonomy in space-based security and vital infrastructure have fuelled the expansion of the military and government segment. As per research, a dominant share of newly launched European LEO satellites are now dedicated to defense, intelligence, and civil security roles. The EU’s IRIS² program accounts for a share of planned LEO mass deployment through 2030 with encrypted Ka band services for armed forces energy grids and emergency response networks. National defense ministries reinforce this trend. Institutional procurement cycles are long-term and budget assured, unlike commercial ventures, which face market volatility. The military and government segment will remain the core demand driver for European LEO capabilities, as the EU's Strategic Compass commits member states to increasing space defense investment in the coming years.

The commercial-use segment is expected to exhibit a noteworthy CAGR of 28.9% from 2025 to 2033. The swift growth of the commercial end-use segment is supported by private investment in broadband IoT and precision agriculture applications. Unlike institutional missions, commercial LEO ventures are scaling rapidly to address underserved connectivity markets and data analytics opportunities. As per research, European space startups raised a notable amount in private equity between 2022 and 2025, with many focused exclusively on EO-based services. Companies are deploying proprietary constellations for RF geolocation and maritime tracking, serving logistics, insurance, and fisheries clients. Europe's commercial LEO ecosystem is transitioning from demonstration to sustainable revenue generation, driven by decreasing launch costs, the standardization of smallsat buses, and growing enterprise demand for real-time Earth data.

COUNTRY LEVEL ANALYSIS

France LEO Satellite Market Analysis

France grew steadily in the European LEO satellite market. Strong national investment in sovereign space capabilities and dual-use technologies is among the key factors behind the growth of France in the regional market. According to the French Space Agency CNES, France has led the development or operation of numerous low Earth orbit satellites since 2020, including those for Earth observation and electronic intelligence. The French government is significantly investing in its space strategy, with a large portion directed towards LEO missions supporting defense, broadband, and climate monitoring. French companies are also building satellites for European secure communications, and the National Frequency Agency has simplified spectrum licensing for commercial LEO operators. The country also hosts the largest ground station network in Europe, with many tracking facilities enabling high data downlink rates. The deep integration of CNES, industry, and the Ministry of Armed Forces allows France to maintain its central role in Europe’s strategic LEO infrastructure.

Germany LEO Satellite Market Analysis

Germany was the next-biggest player in the European LEO satellite market by capturing a share of 22.5% in 2025. Factors such as robust engineering capabilities and institutional demand for environmental and defense applications are fuelling the expansion of the German market. It is increasingly focusing on Low Earth Orbit (LEO) satellite activities, backed by substantial public investment and strong industry involvement. German entities have been involved in developing numerous LEO satellites for specific tasks like reconnaissance and climate monitoring. The government is providing significant funding for space initiatives, strategically aiming to use LEO systems for climate services and secure communications. Germany also leads in optical inter-satellite link development through the program enabling future mesh networking. The country’s dense ground infrastructure includes satellite control centers ensuring mission reliability. Germany remains pivotal in advancing Europe’s technical autonomy in LEO (Low Earth Orbit), due to the strong alignment between the DLR, its industry, and relevant ministries.

United Kingdom LEO Satellite Market Analysis

The United Kingdom was the top performer as well as a rapidly growing country in the European LEO satellite market by occupying a 26.5% share in 2025. The dominance of the UK market is primarily driven by its dynamic commercial space sector and post-Brexit emphasis on sovereign capabilities. The number of British-built LEO satellites launched is rising, with many being developed by newer companies. A major global satellite communications company maintains its manufacturing and operational base within the UK, supporting a large number of engineering jobs. The UK government is actively investing in LEO programs, focusing on secure communications and using satellite data for national security analysis. The UK also operates the National Timing Centre using LEO signals for resilient PNT backup. The UK has cultivated a commercially led LEO (Low Earth Orbit) ecosystem that complements continental institutional models, due to streamlined export controls, agile regulatory frameworks, and strong venture capital backing.

Italy LEO Satellite Market Analysis

Italy expanded gradually in the European LEO satellite market, with its command in Earth observation and synthetic aperture radar technology. Leonardo S.p.A. and Thales Alenia Space Italy are key industrial players manufacturing radar payloads and satellite platforms for EU and national missions. Italy also hosts the ESA Centre for Earth Observation in Frascati, which processes large terabytes of LEO data daily for Copernicus users. The country’s geographic position in the Mediterranean makes it a strategic node for ground station coverage over North Africa and the Middle East. With a legacy of radar expertise and strong EU collaboration, Italy remains a cornerstone of Europe’s LEO observation infrastructure.

Sweden LEO Satellite Market Analysis

Sweden is predicted to grow in the European LEO satellite market between 2025 and 2033 due to its focus on sustainable space technology and Arctic monitoring capabilities. The country is home to GomSpace, a leading CubeSat manufacturer that delivers nanosatellites for European clients. Sweden’s Defence Materiel Administration has invested an amount in LEO-based surveillance to monitor Baltic Sea activity and northern airspace under NATO commitments. Apart from these, Sweden champions “green propulsion” with ECAPS developing nontoxic LEO orbit adjustment systems now adopted by ESA. The combination of abundant renewable energy, low population density, and robust academic research connections makes Sweden an ideal ecosystem for ethical, scalable, and climate-conscious LEO operations.

COMPETITIVE OVERVIEW

The European LEO satellite market features a concentrated but dynamic competitive landscape dominated by a few large aerospace integrators supported by a growing base of specialized small and medium enterprises. Competition is less price-driven and more focused on technological differentiation, mission reliability, and compliance with EU regulatory and security standards. Airbus, Thales Alenia Space, and OHB lead through deep institutional ties and end-to-end capabilities, while startups like GomSpace and Unseenlabs carve niches in nanosatellites and RF intelligence. Unlike the US market, where commercial constellations drive scale, European competition is shaped by policy mandates for sovereignty, sustainability, ty, and data protection. This creates a dual-track ecosystem where defense, Earth observation, and secure communications projects dominate near-term demand while commercial broadband and IoT applications gain traction. Collaboration is common with joint ventures across borders and shared participation in EU-funded programs, reducing pure rivalry. The entry barriers remain high due to certification complexity, launch access limitations, and capital intensity, yet the market is evolving toward greater industrial coordination to counter global competitors.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe LEO Satellite Market include

- Airbus Defence and Space

- Thales Alenia Space

- Surrey Satellite Technology Ltd. (SSTL)

- OHB SE

- RUAG Space

- GomSpace Group AB

- AAC Clyde Space

- ISISPACE Group

- EnduroSat AD

- NanoAvionics

- Exotrail SAS

- Telespazio S.p.A.

- Eutelsat Communications S.A.

- SES S.A.

- Leonardo S.p.A.

- Spire Global Inc.

- OneWeb Ltd.

- Planet Labs PBC

- SpaceX (Starlink)

- D-Orbit S.p.A.

TOP LEADING PLAYERS IN THE MARKET

- Airbus Defence and Space is a cornerstone of Europe’s LEO satellite capabilities with deep involvement in both institutional and commercial programs. The company serves as the prime contractor for the EU’s IRIS² secure communications constellation and supplies Earth observation platforms for the Copernicus Sentinel expansion. Airbus integrates advanced payloads, optical inter-satellite links, and radiation-hardened avionics across small, medium, um and large LEO satellites. Airbus strengthens Europe's strategic autonomy through these initiatives, while simultaneously exporting bus technologies and mission services to global customers in Canada, Japan, and the Gulf region.

- Thales Alenia Space is a major European integrator with extensive expertise in LEO satellite manufacturing for Earth observation, navigation, and communications. The company delivers pressurized modules for scientific missions and high-resolution optical radar payloads for defense and environmental monitoring. It plays a leading role in the Copernicus program, providing Sentinel satellites, and is developing next-generation platforms for the CO2M and CHIME missions. The company also established a digital twin facility in Cannes, France, to accelerate satellite testing and reduce time to orbit. Its joint ventures in Italy and France ensure pan-European industrial reach, while its partnerships with global agencies extend its influence beyond continental borders.

- OHB System AG is a key German aerospace company specializing in agile and cost-effective LEO satellite solutions for scientific and institutional clients. The company has built over 100 LEO satellites since 2010, including the SARah reconnaissance fleet and numerous Copernicus contributors. OHB’s SmallGEO and M6 platforms support missions ranging from 100 kilograms to 1,500 kilograms with standardized interfaces for rapid integration. The company also leads the DISCO consortium developing on-orbit refueling capabilities. OHB supports Europe’s independent access to LEO (Low Earth Orbit) by focusing on modular design, European supply chains, and dual-use innovation, all while supporting international science and security objectives.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European LEO satellite market are prioritizing vertical integration to control critical subsystems, including payloads, avionics, and propulsion. They are establishing high-throughput serial production lines to meet constellation-scale demands from IRIS² and Copernicus programs. Strategic partnerships with national space agencies ESA and the European Defence Agency ensure alignment with institutional roadmaps and secure long-term contracts. Companies are also investing in digital engineering, including digital twins and AI-driven testing, to reduce development cycles and failure rates. Furthermore, they are expanding ground segment capabilities and optical inter-satellite link technologies to enhance data autonomy and reduce reliance on foreign infrastructure. These strategies collectively reinforce Europe’s strategic sovereignty while enabling competitive participation in global LEO markets.

MARKET SEGMENTATION

This research report on the europe LEO satellite market is segmented and sub-segmented into the following categories.

By Type

- Small Satellites

- Medium Satellites

By Application

- Earth Observation

- Communication

By End Use

- Military and Government

- Commercial

By Country

- France

- Germany

- United Kingdom

- Italy

- Sweden

- Rest of Europe

Frequently Asked Questions

1. Which companies are leading the Europe LEO Satellite Market?

Leading companies in the Europe LEO Satellite Market include Airbus, OneWeb, Eutelsat, Thales Alenia Space, and SES, actively developing and deploying satellite constellations to enhance European broadband coverage.

2. What are the key applications driving the Europe LEO Satellite Market?

The Europe LEO Satellite Market is primarily driven by satellite internet broadband, earth observation, maritime, aviation, and emergency communication sectors seeking low latency and high speed connectivity.

3. How does the Europe LEO Satellite Market contribute to rural broadband expansion?

The Europe LEO Satellite Market enables rural and remote area broadband by using low Earth orbit satellites that provide faster internet with lower latency compared to traditional GEO satellites, thus expanding internet access in underserved regions.

4. What technological advancements are shaping the Europe LEO Satellite Market?

Technological advancements in small satellite manufacturing, CubeSats, reusable launch vehicles, and dynamic beam steering are significantly shaping the Europe LEO Satellite Market, making satellite internet faster and more reliable.

5. What is the impact of regulatory frameworks on the Europe LEO Satellite Market?

The Europe LEO Satellite Market benefits from the European Union’s digital initiatives, including funding programs like the IRIS2 constellation and national broadband plans promoting satellite broadband infrastructure.

6. How important is satellite constellation deployment in the Europe LEO Satellite Market?

Satellite constellation deployment is critical in the Europe LEO Satellite Market as it allows scalable, global coverage with constellations from players like OneWeb and Starlink enhancing connectivity through hundreds to thousands of satellites.

7. What distinguishes LEO satellites in the Europe satellite market from other satellites?

LEO satellites in the Europe market orbit much closer (500-2000 km) than GEO satellites, resulting in lower latency and higher data transmission speeds, which are essential for real-time applications and broadband services.

8. How does the Europe LEO Satellite Market compare with other global regions?

The European LEO Satellite Market is rapidly growing with significant public and private investments, competing closely with North America and Asia, with Europe focusing on connectivity, security, and advanced satellite services.

9. What are the challenges faced by the Europe LEO Satellite Market?

Challenges include satellite congestion risk, signal interference, high initial investment, regulatory hurdles, and the need for extensive ground infrastructure within the European LEO Satellite Market framework.

10. How does the Europe LEO Satellite Market contribute to the European digital single market?

The European LEO Satellite Market supports the digital single market by providing seamless broadband coverage across borders, enabling consistent internet services without disruption through satellite constellations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com