Europe Luxury Hotels Market Size, Share, Trends, & Growth Forecast Report By Room Type (Standard Luxury Room, Suites Villas / Bungalows, Penthouses & Presidential Suites), Booking Channel, Service Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Luxury Hotels Market Report Summary

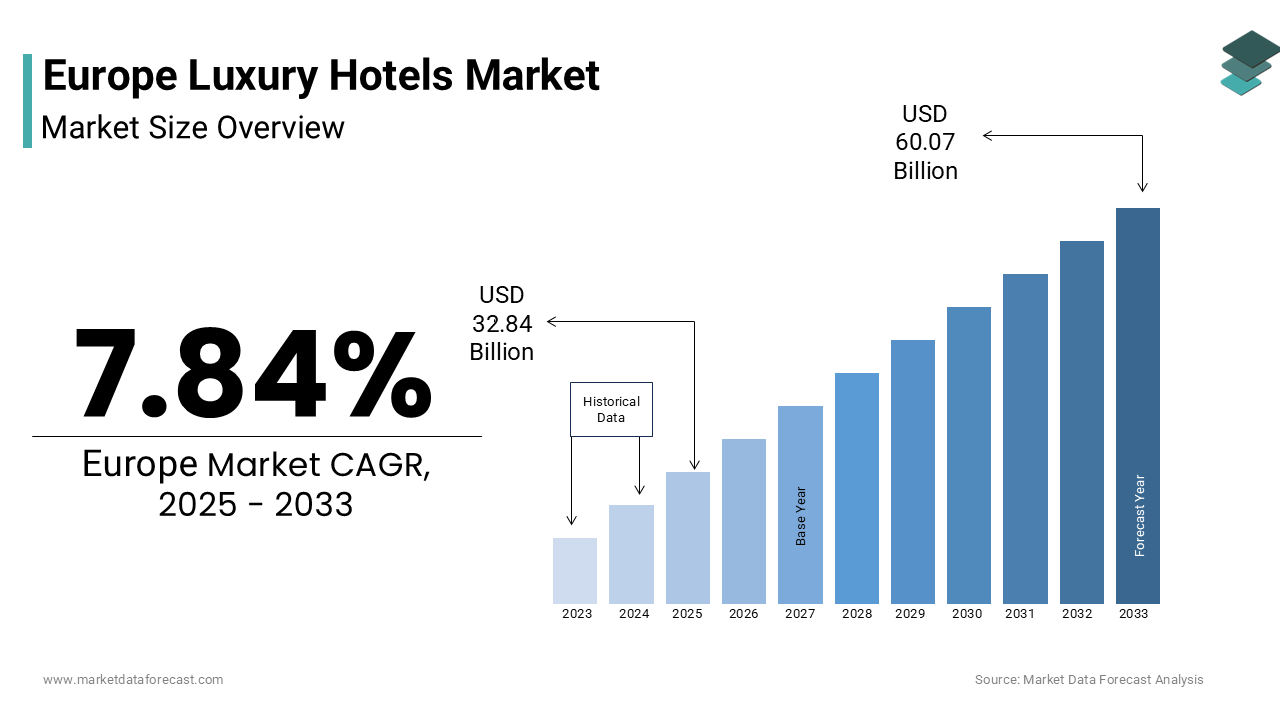

The Europe luxury hotels market was valued at USD 30.45 billion in 2024, is estimated to reach USD 32.84 billion in 2025, and is projected to reach USD 60.07 billion by 2033, growing at a CAGR of 7.84% during the forecast period from 2025 to 2033. The growth of the Europe luxury hotels market is driven by rising affluence among global travelers, increasing demand for personalized and experiential stays, and Europe’s strong heritage appeal that enhances premium hospitality value. Growing interest in wellness tourism, cultural immersion, and high-end architectural heritage further fuels market growth. Moreover, the rise of sustainable luxury travel, direct booking channels, and increased long-haul tourism from the U.S., Middle East, and Asia continues to elevate demand for luxury hotel offerings across Europe.

Key Market Trends

- Rising demand for experiential luxury stays, including heritage immersion, curated cultural experiences, and private bespoke services.

- Growing preference for sustainable and regenerative tourism, with luxury hotels adopting eco-certifications and heritage conservation initiatives.

- Increasing popularity of villas, bungalows, and ultra-private accommodations among high-net-worth and ultra-high-net-worth travelers.

- Expanding wellness and medical tourism offerings, integrating diagnostics, longevity programs, and high-end retreats within luxury hotel spaces.

- Strengthening direct booking channels supported by loyalty programs, AI-driven personalization, and brand-exclusive guest benefits.

Segmental Insights

- Based on room type, the standard luxury room segment was the largest in 2024, driven by its balance of premium comfort, accessibility, and revenue efficiency, especially in heritage-rich cities such as Paris, London, and Rome.

- Based on booking channel, the direct booking segment accounted for the largest share of the Europe luxury hotels market in 2024, supported by hotels’ focus on guest relationship control, personalized engagement, and higher revenue retention.

- Based on service type, the business hotels segment was the largest in 2024 due to Europe’s status as a global hub for finance, diplomacy, and corporate headquarters, complemented by increased hybrid work travel.

Competitive Landscape

The Europe luxury hotels market is characterized by the dominance of global luxury hospitality groups, heritage hotel brands, and exclusive palace hotels with strong brand equity, architectural legacy, and exceptional service standards. Leading companies are investing in sustainable luxury practices, wellness ecosystem integration, direct booking enhancements, and experiential offerings. Brand collaborations with fashion houses, wellness providers, and cultural institutions further strengthen positioning. Prominent players in the Europe luxury hotels market include Accor SA, InterContinental Hotels Group (IHG), Marriott International, Hilton Worldwide, Hyatt Hotels Corporation, Kempinski Hotels, Mandarin Oriental Hotel Group, Four Seasons Hotels and Resorts, The Ritz-Carlton Hotel Company, and Shangri-La Hotels and Resorts.

Europe Luxury Hotels Market Size

The europe luxury hotels market size was valued at USD 30.45 billion in 2024 and is anticipated to reach USD 32.84 billion in 2025 from USD 60.07 billion by 2033, growing at a CAGR of 7.84% during the forecast period from 2025 to 2033.

Luxury hotels are high end accommodation establishments offering exceptional service, personalized guest experiences heritage architecture or design distinction and premium amenities typically classified under five star superior or palace designations. These properties operate in iconic urban centers historic estates alpine resorts and Mediterranean coastal destinations where cultural authenticity and exclusivity define value. In Europe luxury hospitality transcends lodging to become a curated cultural immersion blending gastronomy art wellness and sustainability. International tourist arrivals in the European Union are high, with a significant portion of tourism expenditure coming from high-spending travelers. Travelers from the United States, the Middle East, and Asia make up a substantial share of luxury hotel guests in key European cities. Cultural heritage programs have increased interest in palace hotels located in notable historical sites. Additionally, the European Green Deal’s Sustainable Tourism Initiative encourages luxury operators to adopt certified environmental practices without compromising guest expectations. These intersecting forces of cultural capital global affluence and sustainability expectations shape the distinctive positioning of Europe’s luxury hotel ecosystem.

MARKET DRIVERS

Rising Affluence and Experiential Spending Among Ultra High Net Worth Travelers

The sustained growth in global ultra high net worth individuals who prioritize immersive cultural and personalized experiences over material consumption is a primary driver of the Europe luxury hotels market. The global population of high-net-worth individuals expanded in 2023, with Europe accounting for a significant portion of this growth. As per a study, luxury travelers are increasingly prioritizing experiential travel, dedicating a substantial part of their annual spending to these unique journeys. This cohort seeks hyper personalization such as curated art viewings private vineyard tastings and access to closed museums which Europe’s historic luxury properties uniquely deliver. The average daily expenditure for luxury hotel guests in major European cities like Paris and Venice reached a notable level during 2023. A majority of younger affluent travelers demonstrate a preference for sustainable and ethically certified accommodation options, often indicating a willingness to pay a premium for such features. This convergence of wealth accumulation experiential preference and cultural affinity sustains robust demand for Europe’s most distinguished hospitality offerings.

Revival of Long-Haul International Tourism to Iconic European Destinations

The strong rebound of long-haul tourism from North America, Asia, and the Middle East is significantly accelerating the expansion of the Europe luxury hotels market. This is particularly true in capital cities and UNESCO listed locales. International tourism to Europe is experiencing a significant recovery trend. Arrivals are approaching previous levels, with notable growth from long-haul origin markets. Visitation from the United States and Gulf Cooperation Council regions has shown considerable increases. This growth appears to be influenced by enhanced travel connectivity and streamlined entry processes. In key European cities, hotels in the luxury segment are seeing high demand. Occupancy levels are consistently high, accompanied by an upward trend in average room rates. These travelers often stay longer and spend more. The emotional resonance of Europe’s cultural landmarks post pandemic coupled with pent up demand for authentic in person experiences has reestablished the continent as the premier global luxury destination reinforcing occupancy and pricing power for high end hotels.

MARKET RESTRAINTS

Stringent Heritage Conservation and Urban Zoning Regulations

The complex regulatory environment governing historical buildings and urban development, which limits renovation scope expansion and operational flexibility, is a major restraint affecting the Europe luxury hotels market. Many luxury hotels, particularly those in historic European cities, operate within structures that have protected heritage status. These designations typically restrict certain types of modifications, such as changes to the facade, interior structural work, or additions like rooftop extensions. The process for obtaining restoration and renovation approvals can be time-consuming. Approval requirements often necessitate the use of historically accurate materials and specialized craftsmanship. These specific material and labor requirements typically result in substantially higher capital expenditures compared to constructing a new building. Local regulatory bodies often require approval for both exterior and interior alterations for properties located within designated heritage zones.These constraints make it difficult to install modern amenities such as elevators energy efficient HVAC systems or wellness facilities without compromising historical integrity or incurring prohibitive costs. Consequently, many owners defer upgrades leading to competitive disadvantages against newer properties in less regulated areas. This regulatory friction stifles innovation and limits supply growth in Europe’s most desirable luxury destinations.

Escalating Operational Costs and Labor Shortages in Premium Hospitality

Mounting pressure from sharply rising operational costs and acute shortages of skilled hospitality professionals is eroding margins and service quality, thereby constraining the expansion of the Europe luxury hotels market. Labor costs are increasing, influenced by recent minimum wage adjustments in several European countries where luxury accommodations are prevalent. The hospitality sector is facing significant staffing challenges, with a shortage of trained personnel across the European Union. Specific roles are proving particularly difficult to fill across the industry. Some properties have reported insufficient staffing levels during busy periods, which can lead to operational changes like adjusting service offerings and reducing available inventory. Energy expenses have seen a general increase, prompting some hotel properties to pursue investments in energy efficiency improvements. These combined pressures force operators to raise room rates beyond inflation which risks pricing out loyal clientele. Europe's luxury hospitality risks losing its high-touch edge if it doesn't invest together in education, better pay, and tech.

MARKET OPPORTUNITIES

Integration of Regenerative Tourism and Certified Heritage Stewardship

Regenerative tourism principles are emerging and present a strategic opportunity for Europe luxury hotels market. This allows them to differentiate through verifiable heritage conservation and community co-creation. Travelers are showing a preference for accommodations that contribute positively to local culture or ecology, moving beyond simply minimizing harm. Properties in Europe are collaborating with local craftspeople, historians, and conservation groups to support the preservation of cultural and natural assets, sometimes including guest participation. Certain hotels are facilitating learning opportunities in traditional skills, which are partly funded by lodging revenue. Furthermore, the EU’s Ecolabel and the Global Sustainable Tourism Council have introduced heritage specific criteria that luxury operators can leverage for premium positioning. This shift from passive luxury to active stewardship enables hotels to command higher rates build emotional loyalty and align with Europe’s broader cultural sustainability agenda.

Expansion of Ultra Luxury Wellness and Medical Tourism Offerings

The convergence of high-end wellness and medical tourism is opening a high value segment for the expansion of the Europe luxury hotels market. These hotels can offer integrated health diagnostics, longevity programs, and recovery retreats. Europe shows a strong position in the global health travel market, with several countries leading in premium health services. Luxury accommodation providers in certain destinations are collaborating with healthcare facilities to offer integrated services, which can include advanced diagnostic testing and recovery support within a private, hospitality-focused setting. A directive is in place that helps individuals access healthcare services across European borders, which aims to ensure both treatment accessibility and personal privacy. Spending related to wellness guests in luxury hotels in Europe indicates a focus on specific, high-demand services like wellness therapies and personalized resilience programs. Brands like Six Senses and Aman are embedding medical directors and diagnostic suites into new European properties creating seamless health to hospitality journeys. This integration transforms hotels from transient accommodations into trusted partners in long term wellbeing attracting a loyal global clientele seeking discretion efficacy and holistic care.

MARKET CHALLENGES

Vulnerability to Geopolitical Instability and Travel Perception Risks

Its exposure to geopolitical volatility and shifting travel risk perceptions, which can abruptly disrupt demand from key source markets, is a persistent challenge confronting the growth of the Europe luxury hotels market. Occupancy in London and Paris experienced a decline. The decline occurred over a sequence of months. This trend followed international headlines related to local civil disturbances. Recovery periods from such events can vary. Travelers with high disposable income may choose alternative destinations during periods of perceived instability. Destinations such as Switzerland or Portugal are examples of potential alternatives. Unlike mass market segments luxury guests have lower tolerance for uncertainty and higher switching flexibility. Europe's luxury hotels lack unified crisis response, leaving them vulnerable to uncontrollable external events that damage profits and brand image.

Pressure to Balance Authenticity with Modern Guest Expectations

There is a delicate challenge in preserving historical authenticity while meeting contemporary expectations for digital convenience sustainability and wellness infrastructure, which in turn hinders the expansion of the Europe luxury hotels market. Luxury properties located in older, heritage buildings often face challenges in meeting modern guest expectations. There are frequent guest complaints regarding limitations in connectivity and sound insulation within these historic spaces. Guests also express a desire for contemporary amenities like in-room fitness technology. Younger travelers commonly expect seamlessly integrated smart room controls and contactless services, regardless of the building's age. The availability of amenities such as on-site electric vehicle (EV) charging stations is becoming an expected standard across all luxury accommodations. Retrofitting these features without violating heritage regulations is technically complex and financially burdensome. Moreover, adding wellness facilities like spas or gyms often necessitates basement excavations prohibited in UNESCO zones. This tension forces operators into difficult trade-offs either compromising guest satisfaction or risking historical integrity. Europe's premier hotels risk becoming dusty museums if they don't embrace invisible tech and regulatory flexibility.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Room Type, Booking Channel, Service Type and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Key Market Players | Accor SA, InterContinental Hotels Group (IHG), Marriott International, Hilton Worldwide, Hyatt Hotels Corporation, Kempinski Hotels, Mandarin Oriental Hotel Group, Four Seasons Hotels and Resorts, The Ritz-Carlton Hotel Company, and Shangri-La Hotels and Resorts |

SEGMENTAL ANALYSIS

By Room Type Insights

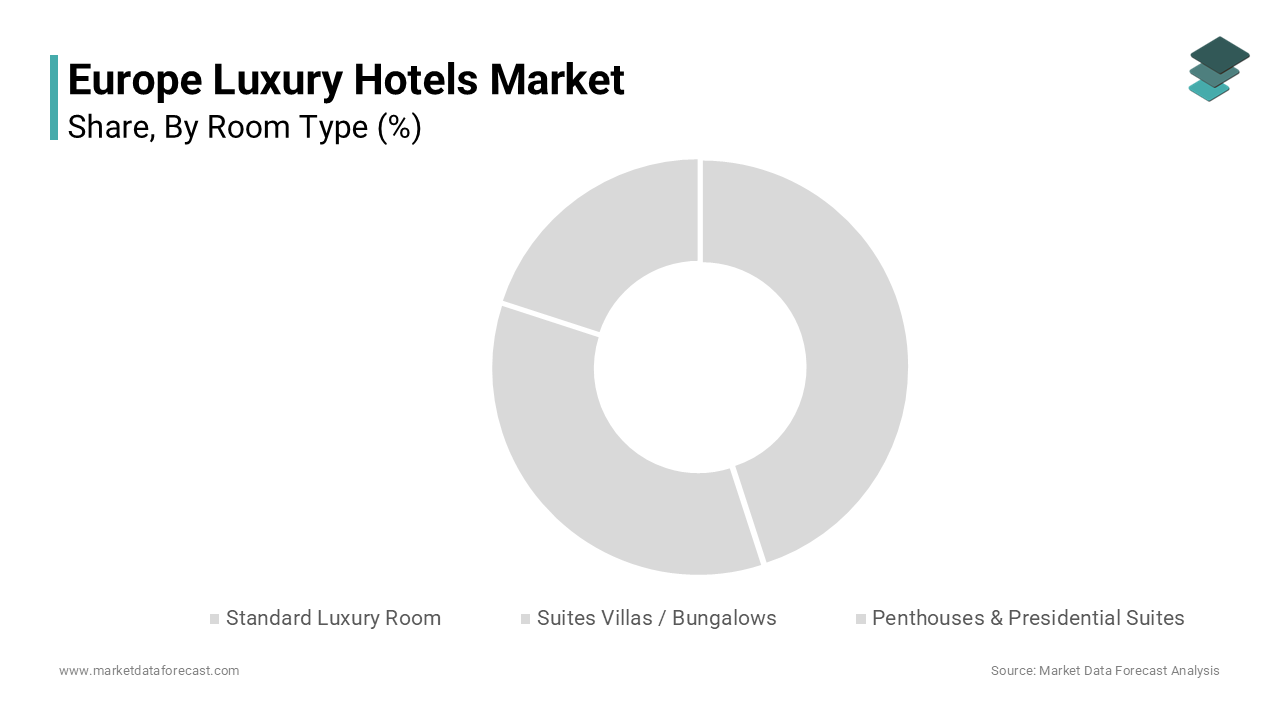

The standard luxury room segment held the largest share of 52.5% of the Europe luxury hotels market in 2024. The supremacy of the standard luxury room segment is credited to its optimal balance of premium comfort accessibility, and revenue efficiency for both guests and operators. These rooms represent the foundational inventory of five star and palace hotels in cities like Paris London and Rome where space constraints and heritage regulations limit the construction of larger accommodations. Luxury properties observe that standard rooms are the primary contributors to total room revenue. The average daily rates for these standard rooms are generally lower compared to suites. A majority of luxury hotel guests, including business and solo travelers, typically favor these well-appointed standard rooms. Guests consistently show a preference for specific amenities within standard rooms, such as premium bedding, high-speed connectivity, and personalized service, over larger room layouts. Furthermore, revenue management systems enable dynamic pricing of these rooms during peak demand periods such as fashion weeks or art fairs maximizing yield without requiring physical expansion. The segment’s dominance is further reinforced by brand consistency as global luxury chains like Four Seasons and Ritz Carlton standardize their entry level luxury experience across European destinations ensuring guest familiarity and loyalty.

The villas and bungalows segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 9.4% from 2025 to 2033 due to rising demand for privacy exclusivity and residential style experiences among ultra-high net worth travelers. Globally, many individuals who are ultra-high net worth now place a higher priority on private accommodations that offer dedicated staff and outdoor space when choosing luxury stays. Bookings for villas in Mediterranean locations like the French Riviera, Italian Amalfi Coast, and Greek Islands have significantly increased, which reflects an ongoing shift in preference towards more secluded and private luxury travel options. Brands have responded by acquiring or developing standalone villa estates with private pools butler service and chef in residence offerings. This convergence of wealth concentration experiential preference and post pandemic safety consciousness establishes villas and bungalows as the highest growth accommodation format in Europe’s luxury hospitality landscape.

By Booking Channel Insights

The direct booking segment led the Europe luxury hotels market and captured a share of 48.4% in 2024 as high end properties prioritize guest relationship control revenue retention and personalized pre arrival engagement. Hotels that manage bookings through their own websites or direct reservation centers are able to retain significantly more of the room revenue compared to using third-party channels. A majority of repeat luxury hotel guests have a preference for booking directly with the hotel. Guests often book directly to gain access to member-only benefits, which can include advantages like room upgrades, early check-in, and personalized amenities. Leading brands like Belmond and Dorchester Collection have invested heavily in proprietary digital platforms featuring virtual room tours AI driven concierge previews and seamless loyalty integration that enhance conversion without sacrificing service depth. Furthermore direct channels enable hotels to collect first party data on guest preferences which is critical for delivering hyper personalized experiences, a key differentiator in luxury hospitality. This strategic focus on ownership of the customer journey ensures direct booking remains the dominant and most profitable channel in the European luxury segment.

The online travel agencies segment is expected to exhibit a noteworthy CAGR of 8.7% from 2025 to 2033 owing to the rise of affluent millennial travelers and the curation capabilities of premium OTA platforms. Younger luxury travelers are increasingly starting their travel planning process using various digital platforms. Travelers show a strong preference for booking decisions based on verified reviews and engaging visual content found online. Specialized online travel agencies have significantly broadened their selection of high-end European accommodations. These platforms are featuring unique, value-added packages, such as private transport and included dining or spa services, which are difficult to find through hotel-direct booking channels. These platforms leverage sophisticated algorithms to match travelers with properties based on aesthetic design wellness focus or sustainability credentials, factors increasingly important to younger luxury guests. Additionally, during periods of travel uncertainty OTAs provide flexible cancellation policies and consolidated billing that appeal to corporate luxury travelers. This blend of digital convenience curated discovery and risk mitigation establishes OTAs as the highest growth channel despite traditional luxury resistance.

By Service Type Insights

The business hotels segment dominated the Europe luxury hotels market and captured a share of 41.4% share in 2024. The supremacy of the business hotels segment is because of Europe’s status as a global hub for finance diplomacy and corporate headquarters. Multiple major corporations have established their European headquarters in key cities across the continent, which helps maintain a steady requirement for premium accommodations. These business travelers frequently seek specific amenities like meeting facilities, executive lounges, and reliable internet connectivity. Business travel represents a significant majority of luxury hotel stays. The average duration of these stays has increased, influenced by the rise of hybrid work models and extended "workations." Luxury business hotels such as The Savoy in London and Hotel de Crillon in Paris have enhanced their offerings with soundproofed boardrooms video conferencing suites and 24-hour butler supported workspaces. This structural reliance on Europe’s economic centrality ensures business-oriented luxury hotels remain the dominant service category.

The airport hotels segment is predicted to witness the highest CAGR of 10.2% from 2025 to 2033 owing to the expansion of long haul air connectivity and the rise of premium transit experiences. European airports have introduced a number of new long-haul routes, primarily connecting with regions in the Middle East, Asia, and North America. This development appears to be linked to an increase in premium passenger volumes at several major hubs. A notable portion of travelers who fly in luxury classes are incorporating an airport hotel stay into their journey. This practice is associated with managing potential jet lag or simply recovering from travel-related circumstances. Luxury brands such as Sofitel and Hilton have responded by developing dedicated airport properties featuring sound insulated rooms in house Michelin dining and expedited security access via partnerships with airport authorities. This synergy of aviation growth premium convenience and operational innovation positions airport hotels as the highest growth service segment in Europe’s luxury hospitality market.

COMPETITIVE LANDSCAPE

The Europe luxury hotels market features intense competition among global luxury groups European heritage operators and independent palace hotels each vying for ultra high net worth clientele through differentiation in authenticity exclusivity and service depth. Global players like LVMH and Four Seasons emphasize brand consistency and lifestyle integration while European leaders such as Accor and Kempinski leverage regional heritage and architectural legacy. Independent properties like Hotel Danieli or The Gritti Palace compete through unparalleled location historical significance and generational staff expertise. Competition is less about price and more about emotional resonance guest memory creation and access to rare experiences such as private museum viewings or vineyard harvests. The rise of regenerative tourism has intensified focus on verifiable sustainability with guests increasingly favoring hotels that actively restore cultural assets. Digital innovation remains secondary to human touch yet seamless connectivity is now a baseline expectation. Ultimately the market rewards those who balance historical integrity with discreet modernity and who transform stays into enduring personal narratives.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe luxury hotels market include

- Accor SA

- InterContinental Hotels Group (IHG)

- Marriott Internationa

- Hilton Worldwide

- Hyatt Hotels Corporation

- Kempinski Hotels

- Mandarin Oriental Hotel Group

- Four Seasons Hotels and Resort

- The Ritz-Carlton Hotel Company

- Shangri-La Hotels and Resorts

Top Players in the Europe Luxury Hotels Market

LVMH Moët Hennessy Louis Vuitton SE (through Belmond and Cheval Blanc)

LVMH has significantly expanded its footprint in the Europe luxury hotels market through its ownership of Belmond and Cheval Blanc, two iconic luxury hotel collections with landmark properties across Italy France and the UK. Belmond operates historic gems such as Hotel Cipriani in Venice and Villa San Michele in Florence while Cheval Blanc offers avant garde urban palaces like Cheval Blanc Paris. The group leverages its luxury ecosystem to integrate hotel stays with fashion experiences spa rituals and fine dining curated by Michelin starred chefs. This vertical integration strengthens brand loyalty among ultra high net worth clients and positions LVMH as a lifestyle orchestrator rather than a conventional hotelier.

Four Seasons Hotels and Resorts

Four Seasons maintains a strong presence in the Europe luxury hotels market with a portfolio of landmark properties in London Paris Madrid and Florence known for personalized service and timeless elegance. The brand caters to discerning international travelers seeking consistency and discretion across European capitals. The company has also enhanced its wellness offerings by partnering with European wellness experts to develop sleep and recovery programs tailored to jet lagged guests. These initiatives reinforce Four Seasons’ reputation for combining heritage sensitivity with modern luxury across the continent.

Accor SA (through Raffles Orient Express and Sofitel Legend)

Accor SA is a dominant European hospitality group with a powerful luxury segment anchored by Raffles Orient Express and Sofitel Legend brands. Its portfolio includes historic properties such as Raffles London at The OWO and Hôtel de Crillon in Paris. Accor leverages its pan European operational infrastructure to deliver seamless luxury experiences while investing heavily in narrative driven hospitality that emphasizes local heritage and craftsmanship. The company also introduced a sustainability charter for its luxury properties requiring certified heritage restoration and zero single use plastics. These actions position Accor as a curator of European cultural luxury with global appeal.

Top Strategies Used by the Key Market Participants

Leading players in the Europe luxury hotels market focus on heritage storytelling by restoring historic buildings with artisanal craftsmanship and local cultural narratives. They integrate wellness and medical tourism through partnerships with premium health providers and in house diagnostic services. Brands leverage their global ecosystems to offer cross category experiences in fashion gastronomy and art exclusively for hotel guests. Sustainability is embedded through verified conservation programs carbon neutral certifications and elimination of single use plastics. Additionally operators invest in direct booking platforms with personalized pre arrival engagement to enhance guest loyalty and revenue retention while reducing reliance on third party channels.

MARKET SEGMENTATION

This research report on the Europe Luxury Hotels Market has been segmented and sub–segmented into the following categories.

By Room Type

- Standard Luxury Room

- Suites Villas / Bungalows

- Penthouses & Presidential Suites

By Booking Channel

- Direct Booking

- Brand Website

- Call Center

- Online Travel Agencies

- (OTA) Travel Agents / Tour Operators

- Corporate Contracts

By Service Type

- Business Hotels

- Airport Hotels

- Suite Hotels

- Resorts

- Other Service Types

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What defines a luxury hotel in the European market?

A luxury hotel offers premium accommodation, personalized services, world-class amenities, fine dining, and exceptional guest experiences. In Europe, luxury hotels often emphasize heritage architecture, cultural experiences, and high service standards.

What factors are driving the growth of luxury hotels in Europe?

Growth is fueled by rising international tourism, higher disposable incomes, and increasing demand for premium travel experiences. Business travel and luxury staycations are also boosting the market.

Which countries dominate the Europe luxury hotel market?

France, Italy, the United Kingdom, Germany, and Spain lead the market. Cities like Paris, London, Rome, and Barcelona are top destinations due to tourism, culture, and business hubs.

What types of luxury hotels are common in Europe?

Popular types include business hotels, boutique hotels, heritage/palace hotels, spa & wellness hotels, and resort hotels. Each type caters to different guest preferences and travel purposes.

How is digitalization influencing the luxury hotel industry?

Digital check-ins, mobile concierge services, AI-powered personalization, and smart-room technologies are enhancing guest experiences. Luxury hotels are adopting tech to remain competitive.

What challenges does the Europe luxury hotels market face?

High operational costs, fluctuating tourism trends, and economic uncertainty are major challenges. Staff shortages and rising customer expectations add further pressure.

What role does business travel play in luxury hotel demand?

Business travel significantly contributes to weekday occupancy rates. Corporate events, MICE tourism, and conferences drive bookings in major European cities.

Who are the major players in the Europe luxury hotels market?

Leading players include Accor SA, IHG, Marriott International, Hilton Worldwide, Hyatt Hotels Corporation, Kempinski, Mandarin Oriental, Four Seasons, Ritz-Carlton, and Shangri-La.

How competitive is the Europe luxury hotel market?

The market is highly competitive, with global chains and iconic heritage hotels competing on service quality, innovation, and guest experience.

What is the future outlook for the Europe luxury hotel market?

Demand is expected to grow steadily due to tourism expansion, experiential travel, and rising luxury consumption. Digital innovation and sustainability will shape the next decade.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com