Europe Manganese Ore Market Size, Share, Trends & Growth Forecast Report Segmented By Application (Alloys, Electrolytic Manganese Dioxide), End Use, Ore Grade, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe Manganese Ore Market Size

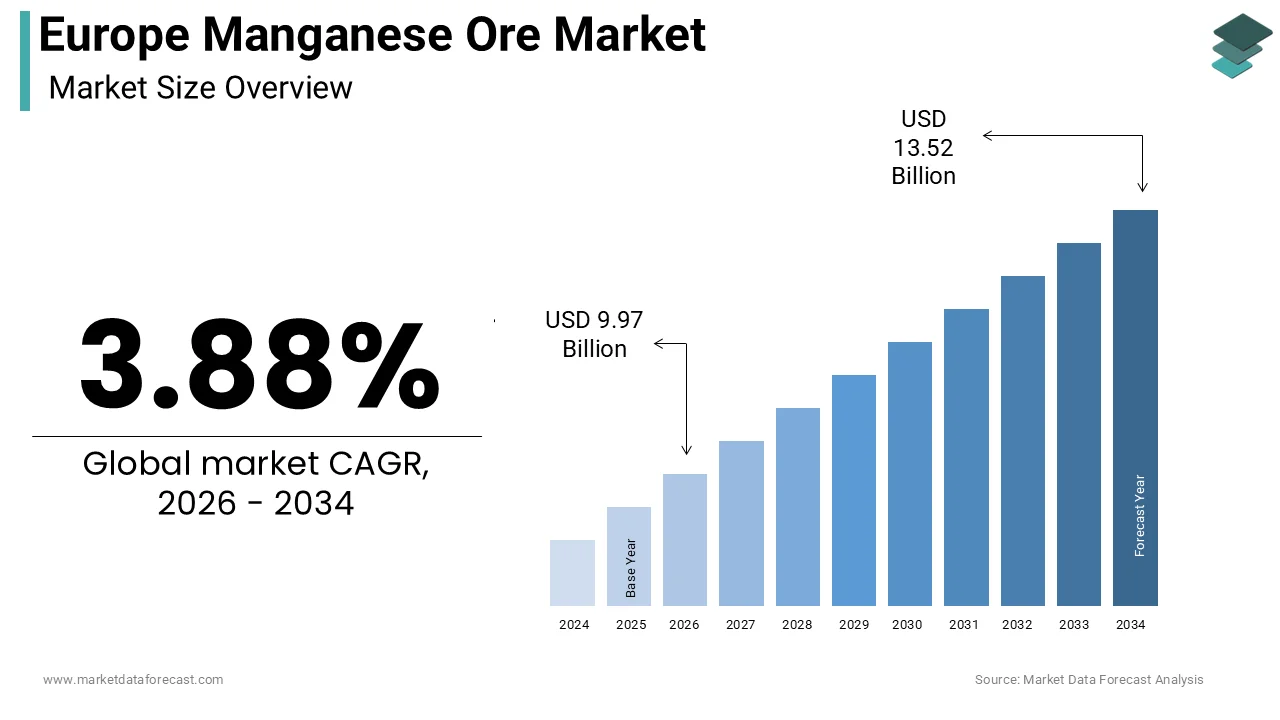

The Europe manganese ore market size was calculated to be USD 9.60 billion in 2025 and is anticipated to be worth USD 13.52 billion by 2034, from USD 9.97 billion in 2026, growing at a CAGR of 3.88% during the forecast period.

The manganese ore is the regional metallurgical industry, primarily functioning as an essential raw material for steel production and emerging battery technologies. Manganese is indispensable in the manufacturing of steel, where it acts as a deoxidizer and desulfurizer, enhancing strength, toughness, and hardness. As per Eurostat, the European Union produced approximately 136 million tons of crude steel in 2023. The transition towards sustainable mobility further amplifies the strategic importance of manganese, particularly in the context of lithium-ion batteries for electric vehicles. According to the International Energy Agency, electric car sales in Europe accounted for over 20% of total new car registrations in 202,3 driving interest in manganese-rich cathode chemistries such as lithium manganese iron phosphate. The European Commission has identified manganese as a critical raw material, highlighting its economic importance and supply risk. Environmental regulations under the European Green Deal influence mining and processing standards, requiring stringent adherence to sustainability criteria. The European Environment Agency notes that industrial emissions from metal processing remain a focus area for regulatory compliance. This landscape necessitates efficient supply chain management and investment in cleaner processing technologies. The interplay between traditional steelmaking needs and modern energy storage requirements defines the current dynamics of the Europe manganese ore market, ensuring its continued relevance in the industrial ecosystem.

MARKET DRIVERS

Robust Demand from the Steel Manufacturing Sector

The sustained demand from the steel manufacturing sector due to the irreplaceable role of manganese in steel production is escalating the growth of Europe manganese ore market. Manganese is added to molten steel to remove oxygen and sulfur, thereby improving the mechanical properties of the final product. According to the World Steel Association, global crude steel production reached 1.89 billion tons in 2023, with Europe maintaining a significant share despite economic fluctuations. The construction and automotive industries are the largest consumers of steel driving continuous demand for high-quality ferroalloys. Infrastructure projects across major economies such as Germany, France, and Italy require vast quantities of reinforced steel which relies on manganese for durability and strength. The renovation wave initiated by the European Union aims to improve energy efficiency in buildings, further stimulating steel demand for structural components. Additionally, the automotive industry’s recovery post pandemic has led to increased vehicle production, necessitating more steel for chassis and body panels. Manganese ore is processed into ferromanganese and silicomanganese, which are then added to steel melts. The inability to substitute manganese with other elements without compromising steel quality ensures steady consumption.

Expansion of Electric Vehicle Battery Production

The rapid expansion of electric vehicle battery production, as manufacturers seek alternative cathode chemistries, is propelling the growth of Europe manganese ore market. Manganese is increasingly utilized in lithium-ion batteries, particularly in lithium manganese iron phosphate and high voltage spinel structures due to itscost-effectivenesss and thermal stability. This surge drives investments in local battery gigafactories across countries, such as Hungary, Poland, and Sweden, creating direct demand for battery-grade manganese. As per the European Automobile Manufacturers Association, the shift towards electrification is accelerating with mandates for zero-emission vehicles by 2035. Manganese offers a safer and cheaper alternative to cobalt and nickel, reducing reliance on scarce and expensive materials. The European Commission’s Critical Raw Materials Act emphasizes securing supply chains for battery metal,s including manganese to support the green transition. Automakers are partnering with mining and processing companies to secure long term supplies of purified manganese sulfate. The development of advanced cathode materials that incorporate higher manganese content enhances energy density and performance. This technological evolution expands the application scope of manganese beyond traditional steelmaking into the high-growth energy storage sector.

MARKET RESTRAINTS

Heavy Reliance on Imports and Supply Chain Vulnerabilities

The heavy reliance on imports is due to the lack of significant domestic reserves, which is limiting the growth of Europe manganese ore market. Europe depends almost entirely on external sources for manganese ore, with major suppliers located in South Africa, Gabon, Australia, and Brazil. According to the United States Geological Survey, global manganese mine production was approximately 20 million tons in 2023, with Europe contributing negligible amounts. This dependency exposes the market to geopolitical risk,s trade disruptions, and logistical bottlenecks. As per the European Commission, supply chain vulnerabilities were highlighted during recent global crises affecting the availability of raw materials. Port congestion, shipping delays, and political instability in producing regions can lead to sudden price spikes and shortages. The concentration of supply in a few countries increases the risk of market manipulation and export restrictions. Additionally, the long transportation distances contribute to higher carbon footprints, conflicting with the European Union’s sustainability goals. Currency fluctuations between the euro and supplier currencies also impact import costs, affecting profitability for downstream processors. The lack of strategic stockpiles further exacerbates the vulnerability of European steelmakers and battery producers to supply shocks. Efforts to diversify supply sources are ongoing, but establishing new trade relationships and logistics routes takes time and investment.

Stringent Environmental Regulations and Compliance Costs

The stringent environmental regulations, by imposing high compliance costs on processing and handling operations is restricting the growth of Europe manganese ore market. Manganese processing can generate dust and wastewater containing heavy metals, which are subject to strict control measures under European law. According to the European Environment Agency, industrial emissions from the metal sector are closely monitored to protect air and water quality. The Industrial Emissions Directive requires facilities to use best available techniques to minimize pollution, leading to substantial capital expenditures for upgrades. As per the European Chemicals Agency, manganese compounds are classified with specific hazard statements requiring careful handling and disposal protocols. Compliance with these regulations increases operational costs for smelters and refineries, potentially reducing competitiveness against regions with laxer standards. The European Green Deal aims to make Europe climate neutral by 205,0 necessitating reductions in industrial carbon emissions. Manganese processing is energy-intensive, and transitioning to cleaner energy sources involves significant investment. Additionally, the Waste Framework Directive mandates rigorous recycling and waste management practices, adding to administrative burdens. Small and medium-sized enterprises may struggle to meet these requirements, leading to market consolidation. The regulatory landscape also influences sourcing decisions, with buyers preferring suppliers who adhere to high environmental standards.

MARKET OPPORTUNITIES

Development of Recycling Technologies for Manganese Recovery

The development of advanced recycling technologies for manganese recovery is expected to boost new opportunities for the growth of Europe's manganese ore market. As the volume of end-of-life electric vehicle batteries and steel scrap increases, efficient recycling methods can supplement the primary supply. According to the European Commission, the Circular Economy Action Plan promotes the recovery of raw materials from waste streams to reduce dependency on imports. Hydrometallurgical processes are being refined to extract manganese from spent lithium-ion batteries with high purity levels suitable for new battery production. As per the study, recycling rates for metals in Europe are improving, driven by technological innovations and regulatory incentives. Establishing closed-loop systems for manganese can enhance supply security and reduce environmental impact. Battery manufacturers are investing in recycling facilities to recover valuable materials, including manganese, nickel, and cobalt. The integration of recycled manganese into new battery cathodes supports sustainability goals and reduces raw material costs. Additionally, advancements in steel scrap processing allow for better recovery of manganese from alloyed steels. The European Union’s Battery Regulation mandates minimum recycled content in new batteries, creating a guaranteed market for recovered materials.

Strategic Partnerships for Secure Supply Chains

Forming strategic partnerships for secure supply chains is expected to escalate new opportunities for the growth of Europe manganese ore market. Collaborations between European manufacturers and mining companies in resource-rich regions can ensure stable access to high-quality ore. According to the European External Action Service, diplomatic efforts are underway to strengthen trade agreements with key partner countries in Africa and Asia. These partnerships often involve joint ventures, technology transfer and infrastructure investments that benefit both parties. As per the study, financing instruments are available to support sustainable mining projects that adhere to environmental and social governance standards. Long-term off-take agreements provide price stability and guarantee supply volumes, mitigating the risks associated with spot market volatility. Additionally, partnerships with logistics providers can optimize transportation routes and reduce lead times. The European Union’s Global Gateway initiative aims to boost smart clean, and secure links in the digital energy and transport sectors, facilitating better connectivity with resource-rich nations. These strategic alliances enhance supply chain resilience and foster mutual economic growth.

MARKET CHALLENGES

Volatility in Global Manganese Prices

The volatility in global manganese prices is affecting cost predictability and profit margins, which is one of the major challenges for the growth of Europe manganese ore market. Prices are influenced by various factors, including supply disruption,s changes in Chinese steel production and currency fluctuations. According to the World B,ank commodity markets experienced significant price swings in recent years due to geopolitical tensions and post pandemic recovery dynamics. As per the London Metal Exchange, manganese alloy prices can fluctuate widely, impacting the cost structure for European steelmakers and battery producers. High price volatility makes it difficult for manufacturers to plan budgets and set competitive product prices. Sudden price spikes can erode profit margins, while sharp declines can lead to inventory write-downs. The dependence on spot markets for a portion of supply exacerbates exposure to price risks. Hedging strategies are complex and not always accessible to smaller players. Additionally, the correlation between manganese prices and other ferroalloys adds another layer of complexity to procurement decisions. Market uncertainty discourages long term investment in processing capacity and technology upgrades. Buyers may delay purchases in anticipation of lower prices disrupting supply chains. This financial instability affects the entire value chain from miners to end users. Managing price risk requires sophisticated financial tools and diverse sourcing strategies, which may be challenging to implement effectively.

Competition from Alternative Materials and Technologies

The competition from alternative materials and technologies, particularly in the battery sector, is greatly influencing the growth oEurope'spe manganese ore market. While manganese is favored for its cost and safety benefits, other cathode chemistries, such as lithium nickel manganese cobalt oxide and lithium iron phosphat,e compete for market share. According to BloombergN,EF the dominance of different battery chemistries shifts based on performance requirements and raw material availability. Advances in nickel-rich cathodes offer higher energy density, appealing to premium electric vehicle segments. As per the International Council on Clean Transportation, technological improvements in lithium iron phosphate batteries have enhanced their range and affordability, reducing the relative advantage of manganese-based alternatives. In the steel industry efforts to reduce alloy content through advanced manufacturing techniques may slightly lower manganese intensity per ton of steel. Additionally, the development of solid-state batteries could potentially alter material requirements in the long term. The rapid pace of innovation in battery technology creates uncertainty regarding future demand for manganese. Manufacturers must continuously adapt to changing specifications and customer preferences. The emergence of new materials with superior properties or lower costs threatens the market position of manganese.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.88% |

| Segments Covered | By Application, End Use, Ore Grade, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Eramet, Anglo American plc, South32, Glencore, Assmang, MOIL Limited, Nippon Denko Co., Ltd., Consolidated Minerals Limited, Vale S.A., OM Holdings Ltd. |

SEGMENTAL ANALYSIS

By Application Insights

The alloys segment was the largest by capturing a dominant share of the Europe manganese ore market in 2025. The indispensable role of manganese in steel production, where it is used to produce ferromanganese and silicomanganese alloys, is enhancing the growth of Europe manganese ore market. The massive scale of the European steel industry relies on these alloys to enhance the strength, toughness, and hardness of steel products. According to the World Steel Association, crude steel production in the European Union remained robust at 136 million tons in 2023, necessitating consistent inputs of manganese alloys. The automotive industry also contributes significantly to vehicle manufacturing, requiring high-strength steel for safety and performance. Manganese acts as a deoxidizer and desulfurizer during steelmaking, improving the quality of the final product. The lack of viable substitutes for manganese in steel production ensures steady demand regardless of minor economic fluctuations. Additionally, the renovation wave across Europe stimulates demand for construction materials further supporting alloy consumption. The established infrastructure for alloy production and the deep integration of manganese into metallurgical processes solidify its dominant position in the market.

The electrolytic manganese dioxide segment is expected to witness the fastest CAGR of 7.8% from 2026 to 2034, with the surging demand for lithium-ion batteries in electric vehicles. The increasing adoption of lithium manganese iron phosphate cathodes, which utilize electrolytic manganese dioxide as a key precursor. According to the International Energy Agency, electric vehicle sales in Europe exceeded 2 million units in 2023, representing a significant share of the global market. This transition drives investments in battery gigafactories across countries such as Hungary Poland and Sweden creating direct demand for battery grade manganese. As per the European Automobile Manufacturers Association the mandate for zero emission vehicles by 2035 accelerates the shift away from internal combustion engines. Electrolytic manganese dioxide offers superior thermal stability and safety compared to other cathode materials, making it attractive for mass market vehicles. The European Commission’s Critical Raw Materials Act highlights the strategic importance of securing manganese supplies for the green transition. Battery manufacturers are seeking reliable sources of high-purity electrolytic manganese dioxide to ensure consistent performance and longevity. The development of advanced battery chemistries that leverage manganese for cost reduction and energy density further supports segment growth.

By End-Use Insights

The industrial sector was accounted in holding 60.3% of the Europe manganese ore market share in 2205 with the extensive use of manganese in heavy industry particularly in steel manufacturing machinery production and chemical processing. The foundational role of steel in industrial infrastructure and equipment is gearing up the growth of the segment. According to Eurostat, the industrial sector including manufacturing and construction represents a significant portion of the European economy with steel being a critical input. As per World Steel Association, the production of crude steel in Europe requires substantial amounts of ferromanganese and silicomanganese alloys to achieve desired mechanical properties. The machinery and equipment manufacturing industry relies on high strength steel for durable components that withstand rigorous operational conditions. Manganese enhances the wear resistance and impact strength of steel making it ideal for industrial applications. The chemical industry also utilizes manganese compounds in various processes including water treatment and fertilizer production. The established industrial base in countries like Germany Italy and France ensures consistent demand for manganese derived products. Regulatory standards for industrial safety and durability further reinforce the need for high quality steel alloys.

The power storage and electricity sector is expected to register a fastest CAGR of 8.2% from 2026 to 2034 with the rapid expansion of renewable energy infrastructure and electric vehicle adoption. The increasing deployment of grid-scale energy storage systems and electric vehicle batteries, which utilize manganese-based cathodes. According to the International Energy Agency, renewable energy capacity in Europe is expanding rapidly, requiring efficient storage solutions to manage intermittency. As per the European Commission the Green Deal initiatives promote the development of sustainable energy storage technologies to support the transition to a climate neutral economy. Lithium-ion batteries with manganese rich cathodes such as lithium manganese iron phosphate are gaining popularity due to their cost effectiveness and safety profile. The establishment of battery gigafactories across Europe creates a localized demand for manganese materials. As per the survey, the demand for battery metals is projected to surge as electric vehicle penetration increases. Manganese offers a sustainable alternative to cobalt and nickel, reducing supply chain risks and environmental impact. The integration of manganese into power storage systems enhances grid stability and supports the electrification of transport.

By Ore Grade Insights

The standard grade segment was the largest by holding a dominant share of the Europe manganese ore market in 2025 with its widespread use in the production of ferromanganese and silicomanganese alloys for the steel industry. The high volume demand from steelmakers who require cost effective and reliable manganese sources is also prompting the growth of segment. According to World Steel Association, the majority of steel produced in Europe utilizes standard grade manganese ores to achieve necessary alloy compositions. As per the United States Geological Survey, standard grade ores with manganese content between 30% and 45% are the most commonly traded varieties globally. These ores provide an optimal balance between manganese content and impurity levels making them suitable for large scale smelting operations. The established supply chains for standard-grade ores from major producers in South Africa and Gabon ensure consistent availability. Steel manufacturers prioritize cost efficiency and process stability, which standard grade ores deliver effectively. The vast scale of steel production in Europe compared to niche applications ensures that standard grade remains the backbone of the market. Regulatory compliance and environmental standards are increasingly met through improved processing techniques for standard ores.

The battery grade segment is expected to grow at a fastest CAGR of 9.5% from 2026 to 2034 with the stringent purity requirements of the electric vehicle battery industry. According to the International Energy Agency, the surge in electric vehicle sales in Europe necessitates a secure supply of battery-grade materials. As per the European Commission, the Raw Materials Act emphasizes the need for domestic processing capabilities for critical battery metals. Battery-grade manganese ore must meet strict specifications regarding impurities such as iron and heavy metals to ensure battery safety and longevity. The establishment of new refining facilities in Europe aims to convert imported ore into battery-grade intermediates. As per Benchmark Mineral Intelligence the demand for battery grade manganese is outpacing supply prompting investments in exploration and processing. Automakers are securing long term contracts for battery-grade materials to mitigate supply risks. The transition towards lithium manganese iron phosphate cathodes further amplifies demand for high-purity inputs. This segment’s growth is supported by technological advancements in purification processes that enable the production of battery-grade materials from various ore sources.

REGIONAL ANALYSIS

Germany Manganese Ore Market Analysis

Germany was the largest contributor of the Europe manganese ore market by holding 22.3% of the share in 2025 with its robust steel and automotive industries. The high demand for manganese alloys used in high-quality steel production is escalating the growth of the market. The presence of major steel manufacturers, such as ThyssenKrupp and Salzgitter who require consistent supplies of ferromanganese and silicomanganese is additionally bolstering the growth of market. According to the German Federal Ministry for Economic Affairs and Climate Action, the automotive sector is transitioning to electric vehicles which increases demand for both high strength steel and battery grade manganese. As per the German Steel Federation, steel production in Germany remains a cornerstone of the industrial economy supporting infrastructure and manufacturing. The country’s focus on advanced manufacturing technologies drives the need for specialized steel grades that rely on precise manganese additions. Germany’s commitment to sustainability influences sourcing decisions with preferences for responsibly sourced ores. The establishment of battery cell production facilities in Germany further diversifies demand towards battery-grade manganese. Regulatory frameworks promoting circular economy practices encourage recycling of manganese from steel scrap and batteries.

Italy Manganese Ore Market Analysis

Italy manganese ore market is likely to grow at an anticipated CAGR in coming years with the presence of major steel producers such as Acciaierie d’Italia who utilize manganese alloys for various steel grades. Also, the construction sector which consumes large volumes of reinforced steel for infrastructure and residential projects is likely to accelerate the growth of market. According to the Italian National Institute of Statistics, construction activity has shown resilience supporting demand for steel and consequently manganese.

France Manganese Ore Market Analysis

France manganese ore market growth is propelled with its aerospace automotive and construction sectors. The aerospace industry, which requires specialized steel and titanium alloys containing manganese for aircraft components. According to the French Aerospace Industry Association, the sector continues to grow, supporting demand for advanced materials. As per the French Steel Industry Federation steel production in France focuses on high value-added products that utilize manganese for enhanced properties. The construction sector also drives demand with ongoing renovation projects requiring reinforced steel. France’s commitment to electric vehicle adoption leads to investments in battery production facilities increasing demand for battery grade manganese. The government’s industrial strategy emphasizes sovereignty in critical raw materials encouraging local processing capabilities. Regulatory standards for environmental protection influence sourcing and processing practices.

Spain Manganese Ore Market Analysis

Spain manganese ore market growth is esteemed to grow with steady demand for steel reinforcement bars and automotive components. The construction sector, which has recovered strongly following recent economic challenges is prompting the growth of market. According to the Spanish National Statistics Institute housing starts and infrastructure projects have increased boosting steel consumption. As per the Spanish Steel Association, the production of long steel products which rely on manganese alloys remains robust. The automotive industry in Spain is a major exporter driving demand for high quality steel sheets and components. Spain’s strategic location facilitates efficient logistics for manganese ore imports. The country’s focus on renewable energy infrastructure also supports demand for steel in wind turbines and solar structures. Environmental regulations promote sustainable sourcing and processing practices.

United Kingdom Manganese Ore Market Analysis

The United Kingdom manganese ore market growth is likely to grow with its steel production and infrastructure projects. The demand for steel alloys used in construction and manufacturing is also elevating the growth of the market. According to the Office for National Statistics construction output has shown signs of recovery supporting steel demand. As per the UK Steel Association the industry faces challenges but remains vital for the economy requiring consistent manganese inputs. The automotive sector in the UK is transitioning to electric vehicles creating new demand dynamics for battery grade manganese. The government’s net zero targets promote the development of green steel technologies which may influence manganese usage.

COMPETITION OVERVIEW

The competition in the Europe manganese ore market is characterized by a reliance on international suppliers due to limited domestic reserves. Major global mining companies compete based on product quality supply reliability and sustainability credentials. The market is influenced by geopolitical factors and trade policies that affect import dynamics. Competitive advantages are derived from established logistics networks and long term contracts with European steelmakers. Companies differentiate themselves through environmental stewardship and adherence to strict regulatory standards. Price volatility remains a key challenge prompting participants to adopt hedging strategies and flexible pricing models. The emergence of battery grade manganese creates new competitive dimensions requiring specialized processing capabilities. Collaboration with downstream industries fosters innovation and secure supply arrangements. Regulatory pressures drive investments in cleaner technologies and circular economy initiatives. Market participants must balance cost efficiency with sustainability commitments to maintain relevance. The competitive landscape encourages continuous improvement in operational performance and environmental responsibility.

KEY MARKET PLAYERS

A few major players of the Europe manganese ore market include

- Eramet

- Anglo American plc

- South32

- Glencore

- Assmang

- MOIL Limited

- Nippon Denko Co., Ltd

- Consolidated Minerals Limited

- Vale S.A

- OM Holdings Ltd

Top Strategies Used by Key Market Participants

Key players in the Europe manganese ore market primarily focus on securing sustainable supply chains through strategic partnerships and vertical integration. Companies invest in low carbon production technologies to meet stringent environmental regulations and customer sustainability goals. Diversification into battery grade manganese products allows participants to capture growth in the electric vehicle sector. Digitalization of logistics and supply chain management enhances operational efficiency and responsiveness. Manufacturers prioritize research and development to innovate high purity manganese solutions for specialized applications. Compliance with international standards such as the Initiative for Responsible Mining Assurance strengthens brand reputation. Long term off take agreements with steel and battery producers ensure stable revenue streams. These strategies enable companies to navigate market volatility and maintain competitive advantages in the European region.

Leading Players in the Market

- Eramet is a leading French mining and metallurgy group with significant operations in the Europe manganese ore market through its Comilog subsidiary. The company produces high quality manganese ore and alloys essential for steelmaking and battery applications. Eramet focuses on sustainable mining practices and innovation to reduce environmental impact. Recent actions include expanding its production capacity in Gabon and investing in low carbon ferroalloy technologies. The company strengthens its market position by securing long term contracts with European steelmakers and battery manufacturers. Eramet actively participates in industry initiatives to promote responsible sourcing and circular economy principles. Their commitment to research and development drives the creation of advanced manganese products for emerging technologies.

- South32 is a globally diversified metals and mining company with a strong presence in the Europe manganese ore market through its high grade manganese alloy operations. The company supplies essential manganese products to European steel and battery industries ensuring reliable material availability. South32 prioritizes operational excellence and sustainability in its mining and processing activities. Recent strategies involve optimizing production processes to reduce energy consumption and carbon emissions. The company invests in digital technologies to enhance supply chain efficiency and customer service. South32 collaborates with European partners to develop innovative manganese solutions for electric vehicle batteries. Their focus on health safety and environmental stewardship strengthens their competitive edge. By maintaining robust logistics networks South32 ensures timely delivery of products to European markets. The company’s commitment to transparency and ethical practices builds trust with stakeholders. These efforts solidify South32’s position as a key supplier in the European manganese landscape.

- Assmang is a prominent manganese mining company that contributes significantly to the Europe manganese ore market through its high quality ore production in South Africa. The company supplies premium manganese ore to European steelmakers and alloy producers supporting their manufacturing needs. Assmang focuses on efficient mining operations and sustainable resource management. Recent actions include upgrading infrastructure to improve production capacity and product quality. The company strengthens its market position by establishing strategic partnerships with European distributors and end users. Assmang invests in community development and environmental conservation projects to minimize its ecological footprint. Their commitment to safety and operational integrity ensures consistent supply reliability. The company’s proactive approach to sustainability aligns with European regulatory requirements. These initiatives enhance Assmang’s reputation and competitiveness in the European manganese ore market.

MARKET SEGMENTATION

This research report on the Europe manganese ore market has been segmented and sub-segmented based on application, end use, ore grade & region.

By Application

- Alloys

- Electrolytic Manganese Dioxide

- Electrolytic Manganese Metals

- Other Applications

By End Use

- Industrial

- Construction

- Power Storage and Electricity

- Other End-Use Sectors

By Ore Grade

- Battery Grade

- High Purity Grade

- Standard Grade

- Technical Grade

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe manganese ore market?

Growth is driven by rising demand from the steel industry, increasing infrastructure development, and expanding applications in battery technologies.

2. Which industries consume manganese ore in Europe?

Key industries include steel manufacturing, construction, automotive, and energy storage (especially batteries).

3. What are the major applications of manganese in steel?

Manganese is used to remove impurities, improve hardness, and enhance the mechanical properties of steel.

4. How is manganese used in batteries?

Manganese is used in lithium-ion and alkaline batteries, improving energy density, safety, and cost efficiency.

5. What are the key trends in the Europe manganese ore market?

Key trends include increased use in EV batteries, recycling of manganese materials, and sustainable sourcing practices.

6. What challenges does the Europe manganese ore market face?

Challenges include supply chain dependency on imports, price volatility, environmental regulations, and geopolitical risks.

7. What is the role of manganese in electric vehicles?

Manganese is a key component in battery chemistries such as NMC (nickel-manganese-cobalt), supporting EV growth.

8. Who are the key players in the Europe manganese ore market?

Major players include Eramet, Glencore, and South32.

9. What are the future opportunities in the Europe manganese ore market?

Opportunities lie in battery-grade manganese production, EV supply chains, and technological advancements in steelmaking.

10. What is the future outlook of the Europe manganese ore market?

The market is expected to grow steadily, supported by demand from steel production and emerging battery technologies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com