Europe Medical Lasers Market Size, Share, Trends & Growth Forecast Report Segmented By Product (Diode Lasers, Solid State Lasers, Gas Lasers, Dye Lasers), Application, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe Medical Lasers Market Size

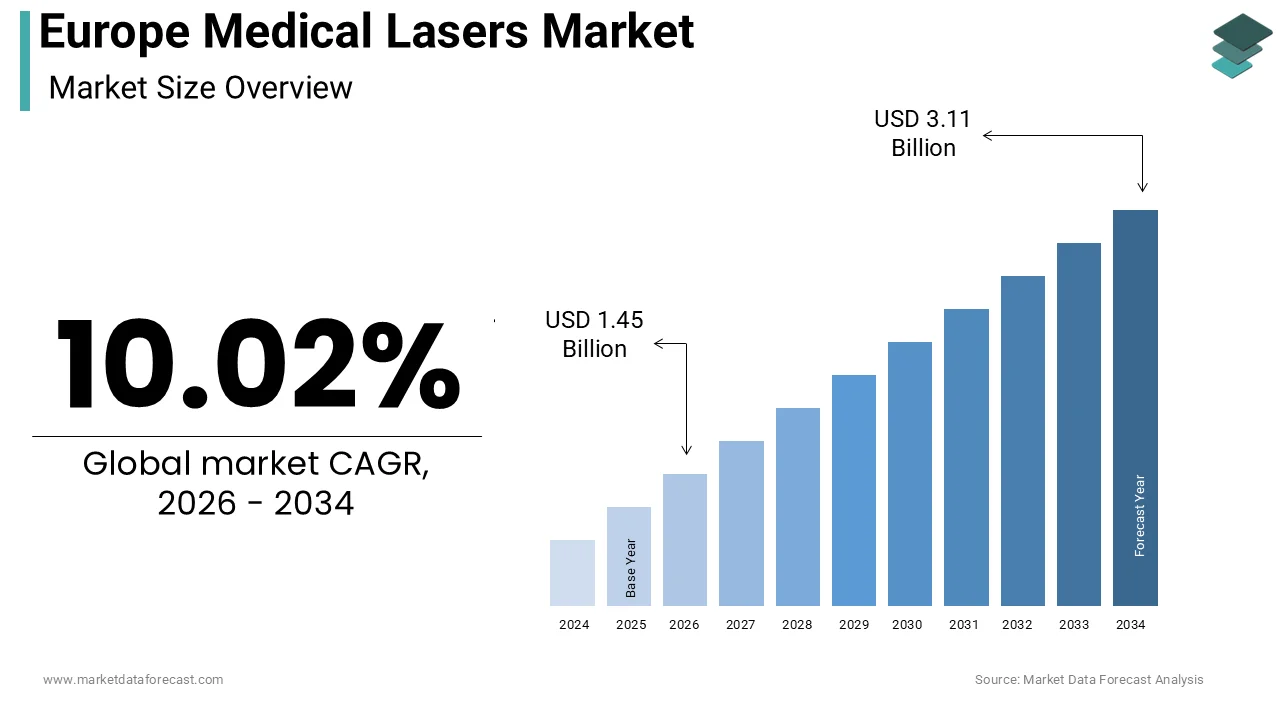

The Europe medical lasers market size was calculated to be USD 1.32 billion in 2025 and is anticipated to be worth USD 3.11 billion by 2034, from USD 1.45 billion in 2026, growing at a CAGR of 10.02% during the forecast period.

Medical lasers are specialized medical devices that use precisely focused, high-intensity light beams to treat or remove tissues. These high-precision instruments leverage specific wavelengths to cut, coagulate, vaporize, or remodel biological tissues with minimal invasiveness, revolutionizing procedures in dermatology, ophthalmology, dentistry, and urology. The market is defined by a rapid transition from traditional scalpel-based surgeries to laser-assisted interventions that offer reduced recovery times and enhanced procedural accuracy. According to Eurostat, the population aged 65 and over in the European Union reached approximately 95.6 million in 2023, representing 21.3 percent of the total population, a demographic shift that significantly increases the prevalence of age-related conditions such as cataracts and skin lesions requiring laser intervention. Furthermore, the European Cancer Information System (ECIS) indicates that skin cancer incidence is rising, with estimates suggesting over 1 million new cases of non-melanoma skin cancer occur annually across Europe, driving the necessity for precise ablative technologies. The regulatory landscape is governed by the stringent European Medical Device Regulation, which mandates rigorous clinical evaluation and safety standards for optical radiation equipment. Advanced laser platforms are becoming essential in modern medicine. They support the prioritization of minimally invasive techniques designed to reduce hospital bed occupancy. These systems offer targeted energy with sub-millimeter precision for modern clinical practice.

MARKET DRIVERS

Rising Prevalence of Dermatological Disorders and Aesthetic Demand

The escalating incidence of dermatological conditions, coupled with a surging demand for cosmetic enhancement,s serves as a key enabler for the expansion of the Europe medical lasers market. Skin disorders ranging from vascular lesions and pigmentation irregularities to malignant growths require precise treatment modalities that only laser technology can provide with optimal aesthetic outcomes. According to the Global Burden of Disease Study and regional dermatological surveys, skin conditions affect a massive portion of the European population, creating a consistent and widespread need for advanced therapeutic interventions. Simultaneously, the aesthetic medicine sector has witnessed exponential growth, driven by a cultural shift towards non-surgical rejuvenation procedures. The International Society of Aesthetic Plastic Surgery notes that Europe accounts for approximately 15% to 20% of global non-surgical cosmetic procedures, with laser skin resurfacing and hair removal ranking among the most performed treatments. Patients increasingly prefer laser therapies due to their ability to deliver visible results with minimal downtime compared to traditional surgical methods. The aging population further exacerbates the demand for anti-aging treatments, as older individuals seek to address wrinkles, sun damage, and uneven skin tone. Clinics and hospitals are investing heavily in multi-platform laser systems capable of addressing a wide spectrum of skin types and conditions, ensuring comprehensive care. This convergence of medical necessity and elective aesthetic desire creates a robust and sustained demand driver, propelling the adoption of advanced dermatological laser systems across both public healthcare facilities and private practices throughout the continent.

Advancements in Minimally Invasive Surgical Techniques

Minimally invasive surgical protocols are being adopted across various medical specialties, which further propels the growth of the Europe medical lasers market. This trend is a significant driver for the integration of medical lasers into standard operating room workflows. Surgeons increasingly favor laser technology for its ability to perform complex procedures through small incisions or natural orifices, resulting in reduced blood loss, lower infection rates, and accelerated patient recovery. The European Association for Endoscopic Surgery (EAES) highlights the increasing integration of energy-based devices in operating rooms across Western Europe, where lasers have become essential tools for delicate soft tissue dissection and blood loss management. In urology, laser lithotripsy has become the gold standard for treating kidney stones, with statistics showing that it accounts for 80% or more of stone fragmentation procedures due to its high efficacy and safety profile. Similarly, in ophthalmology, femtosecond lasers have revolutionized cataract surgery and refractive corrections, offering unparalleled precision that manual techniques cannot match. The push towards day-case surgery and ambulatory care centers further amplifies this trend, as laser procedures often allow patients to be discharged on the same day, optimizing hospital resource utilization. Technological innovations such as fiber-optic delivery systems and robotic integration have enhanced the versatility of lasers, enabling their use in hard-to-reach anatomical areas. Clinical guidelines are continuing to evolve towards less traumatic interventions. Therefore, the reliance on medical lasers as essential surgical tools intensifies, driving consistent market growth and encouraging innovation in power and control mechanisms.

MARKET RESTRAINTS

High Capital Costs and Reimbursement Limitations

The substantial financial burden associated with acquiring, maintaining, and operating advanced medical laser systems is a restraint on the European medical lasers market penetration. This issue is particularly critical for smaller clinics and public hospitals facing budgetary constraints. State-of-the-art laser platforms often require an initial investment ranging from 50000 to over 200000 euros, depending on the wavelength capabilities and application specificity, which strains the capital expenditure budgets of many healthcare providers. According to data from the Organisation for Economic Co-operation and Development, health spending growth in several European nations has stagnated relative to inflation, forcing administrators to prioritize essential life-saving equipment over elective or specialized surgical tools. Beyond the purchase price, the total cost of ownership includes expensive consumables, regular maintenance contracts, and specialized training for staff, which can accumulate to significant annual expenses. Furthermore, reimbursement policies for laser-based procedures vary widely across European countries, with some national health services providing limited or no coverage for certain aesthetic or elective laser treatments. This lack of uniform reimbursement creates uncertainty for providers regarding return on investment, discouraging the adoption of newer technologies. In economically challenging periods, hospitals may delay upgrading legacy laser systems or opt for cheaper, less versatile alternatives, slowing the overall market momentum. The high entry barrier prevents widespread democratization of laser technology, limiting access to advanced care in rural or underfunded regions and restraining the potential market volume despite clear clinical benefits.

Stringent Regulatory Compliance and Safety Concerns

The rigorous regulatory framework in Europe, particularly the new Medical Device Regulation, poses a serious constraint for laser manufacturers and the Europe medical lasers market. It increases compliance costs and extends time-to-market. The classification of medical lasers often falls into higher risk categories requiring extensive clinical evidence, technical documentation, and post-market surveillance plans, which complicates the approval process. According to industry analyses, the average time to obtain CE marking under the new regulations has increased by up to 12 months compared to previous directives, delaying the launch of innovative laser products and restricting market availability Additionally, the inherent risks associated with laser usage, such as accidental eye injury, skin burns, and fire hazards, necessitate strict operational protocols and specialized safety training for all personnel. The European Agency for Safety and Health at Work emphasizes that improper handling of Class 3B and Class 4 lasers can lead to severe occupational accidents, prompting facilities to implement costly safety infrastructure and monitoring systems. This heightened focus on safety can deter some practitioners from adopting laser technologies if they perceive the liability risks or training requirements as too burdensome. The lack of harmonization in national implementation strategies across member states further complicates matters, requiring manufacturers to navigate varying interpretations of safety standards. These regulatory and safety hurdles stifle rapid innovation and slow the pace of market expansion, as companies must allocate significant resources to compliance rather than product development and marketing.

MARKET OPPORTUNITIES

Expansion of Laser Applications in Oncology and Theranostics

The broadening scope of laser applications in oncology and the emerging field of theranostics offer a lucrative opportunity for the Europe medical lasers market growth. Lasers are increasingly being utilized not only for tumor ablation but also for photodynamic therapy (PDT), where light-sensitive drugs are activated by specific laser wavelengths to destroy cancer cells with minimal damage to surrounding healthy tissue. Photodynamic therapy using laser sources has shown promising results in treating early-stage lung, esophageal, and bladder cancers, offering a viable option for patients who are not candidates for surgery. Furthermore, the integration of lasers into theranostic platforms, which combine diagnosis and therapy, allows for real-time monitoring of treatment efficacy. Advances in nanoparticle-enhanced laser therapy enable deeper tissue penetration and higher specificity, opening new avenues for treating deep-seated tumors. Research institutions across Europe are actively conducting clinical trials to validate these novel applications, supported by funding from Horizon Europe programs. As evidence accumulates demonstrating the survival benefits and quality of life improvements associated with laser-based oncology treatments, adoption rates are expected to surge. This expansion into high-value therapeutic areas diversifies the market beyond traditional surgical and aesthetic uses, offering significant growth potential for manufacturers who can develop specialized oncology laser systems.

Integration of Artificial Intelligence and Robotic Assistance

The convergence of medical laser technology with artificial intelligence and robotic assistance paves the way to enhance precision, automate workflows, and improve patient outcomes across the region, which is likely to promote the expansion of the Europe medical lasers market. AI-driven laser systems can analyze tissue characteristics in real-time to automatically adjust power settings, pulse duration, and spot size, ensuring optimal energy delivery while minimizing collateral damage. According to sources, the integration of AI into medical devices is a key priority for modernizing healthcare infrastructure and achieving personalized medicine goals. Robotic arms equipped with laser delivery systems enable surgeons to perform ultra-precise microsurgeries with tremor filtration and enhanced dexterity, particularly in delicate fields like neurosurgery and ophthalmology. These smart systems can also predict potential complications based on historical data and intraoperative feedback, providing actionable insights to the surgical team. The ability to store and analyze procedural data facilitates continuous learning and protocol optimization, leading to standardized high-quality care across different institutions. Manufacturers who offer integrated ecosystems combining hardware, software, and data analytics can differentiate themselves in a competitive market. This technological evolution not only improves clinical efficiency but also supports value-based healthcare models by reducing revision rates and complication costs. As hospitals increasingly invest in smart operating rooms, the demand for AI-enabled and robotically assisted laser platforms is poised to grow exponentially. This trend is creating new revenue streams for innovative market players.

MARKET CHALLENGES

Shortage of Skilled Professionals for Laser Operation

The persistent shortage of adequately trained healthcare professionals capable of safely and effectively operating advanced laser systems constitutes a major challenge to the Europe medical lasers market. The complexity of modern laser devices, which often feature multiple wavelengths, customizable parameters, and integrated safety features, requires a high level of technical proficiency and theoretical knowledge. According to research, there is a critical deficit of specialized nurses and technicians across the continent, with hundreds of thousands of vacancies remaining unfilled, exacerbating the strain on existing workforce capabilities. This staffing crisis leads to situations where inadequately trained personnel must operate sophisticated lasers, increasing the risk of procedural errors, adverse events, and suboptimal patient outcomes. The high turnover rate in healthcare further compounds the issue, necessitating continuous and resource-intensive training programs that many institutions struggle to sustain. Without a sufficiently skilled workforce, the full potential of advanced laser technologies remains unrealized, and hospitals may hesitate to invest in new equipment due to fears of underutilization or misuse. Bridging this skills gap requires collaborative efforts between industry, educational institutions, and professional bodies to develop standardized certification curricula and simulation-based training tools. However, the current scarcity of qualified operators remains a formidable barrier to maximizing market penetration and ensuring the safe deployment of laser technologies across diverse clinical settings.

Risk of Adverse Events and Liability Concerns

The inherent risk of adverse events associated with medical laser procedures, including burns, scarring, and eye injuries, hampers market confidence and adoption rates in the Europe medical lasers market. Despite advancements in safety features, human error or equipment malfunction can lead to serious complications that result in legal liabilities and reputational damage for healthcare providers. According to multiple studies, adverse events related to energy-based surgical devices account for a notable portion of reported incidents in operating rooms, with laser-specific injuries often resulting in permanent disability. The fear of litigation drives some clinicians to avoid using lasers for complex procedures or to stick to conservative settings that may compromise efficacy. Insurance premiums for practices offering laser treatments have risen in recent years, reflecting the perceived risk and adding to the operational costs. Furthermore, high-profile cases of malpractice involving laser aesthetics have garnered media attention, influencing public perception and potentially deterring patients from seeking laser-based treatments. Manufacturers face the challenge of designing fail-safe mechanisms and comprehensive user interfaces to mitigate these risks, yet the ultimate responsibility lies with the operator. The ongoing need to balance innovation with absolute safety requires constant vigilance and investment in risk management strategies. The incidence of preventable laser-related injuries must be significantly reduced through better training and technology. Until then, liability concerns will continue to hinder the growth of medical lasers in European healthcare.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.02% |

| Segments Covered | By Product, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Lumenis Ltd., Candela Corporation, Alma Lasers, Fotona, Biolase Inc., El.En. S.p.A., Bausch Health Companies Inc., Cutera Inc., IRIDEX Corporation, Koninklijke Philips N.V. |

SEGMENTAL ANALYSIS

By Product Insights

The diode lasers segment dominated the Europe medical lasers market and accounted for a 42.9% share in 2025. This dominance of the segment is driven by its compact size, high energy efficiency, versatility across multiple wavelengths, and cost-effectiveness compared to other laser types, making it the preferred choice for dermatology, dentistry, and general surgery applications. One of the major factors driving the diode laser segment is its exceptional versatility, allowing a single platform to address a wide array of clinical indications ranging from hair removal and vascular lesion treatment to soft tissue surgery and pain management. Unlike gas or dye lasers, which are often limited to specific wavelengths, diode lasers can be engineered to emit light across a broad spectrum, typically between 800 nm and 980 nm, catering to diverse chromophore absorption peaks. According to the European Society for Laser Dermatology (ESLD), diode technology is a cornerstone of private aesthetic clinics due to its adaptability across various skin types, particularly for applications like hair removal and vascular treatments. In modern dentistry, diode lasers are increasingly utilized for soft-tissue procedures such as gingivectomies and bacterial reduction. Practitioners favor these systems for their ability to provide bloodless surgical sites and faster healing times compared to traditional scalpel techniques. Furthermore, their application in urology for benign prostatic hyperplasia treatment has grown significantly, offering a less invasive alternative to traditional resection. This cross-specialty utility ensures a consistent and high-volume demand, as hospitals and clinics can maximize their return on investment by using one device for multiple departments, solidifying the diode laser's position as the market leader. The superior operational efficiency and lower total cost of ownership associated with diode lasers significantly bolster their market dominance over competing technologies. Diode lasers convert electrical energy into light with an efficiency rate of up to 50 percent, far surpassing the 1 to 3 percent efficiency of older lamp-pumped solid-state or gas lasers, resulting in substantially lower electricity consumption and reduced heat generation. This energy efficiency translates directly into lower operating costs for healthcare facilities, a critical factor given the budgetary constraints faced by many European public hospitals. Additionally, diode lasers boast extended lifespans, often between 10,000 and 20,000+ hours of operation, which minimizes the frequency and cost of replacements compared to gas lasers that require regular tube refills or dye lasers needing frequent chemical replenishment. Various sources suggest that maintenance costs for diode systems are 30% to 50% lower than those for comparable solid-state systems over afive years. Their compact and portable design also eliminates the need for specialized cooling infrastructure or large dedicated rooms, allowing for easier integration into smaller clinics and mobile surgical units. Healthcare providers are increasingly prioritizing economic sustainability without compromising clinical outcomes. Consequently, the financial advantages of diode lasers drive their widespread procurement and market leadership in Europe.

The solid state lasers segment is predicted to witness the highest CAGR of 8.9% during the forecast due to advancements in crystal technology, the rising demand for high-precision ophthalmic and urologic procedures, and the development of ultra-short pulse lasers for micro-machining tissues. The unparalleled precision offered by solid-state lasers, particularly those utilizing Nd: YAG and Er: YAG crystals, serves as the primary catalyst for their robust growth in the European market. These lasers deliver high peak power with extremely short pulse durations, enabling surgeons to perform delicate procedures with sub-cellular accuracy that is unattainable with continuous wave sources. According to studies, femtosecond solid-state lasers are now used in a notable portion of cataract surgeries performed in Western Europe, a figure expected to rise as the technology becomes more accessible. The ability to create precise corneal flaps and fragment lenses without thermal damage to surrounding tissues has made solid-state lasers the gold standard in refractive surgery. Furthermore, in neurosurgery and ENT procedures, the precision of these lasers allows for the ablation of tumors while preserving critical nerve function, driving adoption in specialized tertiary care centers. As the demand for minimally invasive micro-surgery grows alongside an aging population requiring complex interventions, the unique capabilities of solid-state lasers ensure their status as the fastest-growing segment. Technological breakthroughs in ultra-short pulse (USP) solid state lasers, including picosecond and femtosecond domains, are significantly accelerating market expansion by opening new therapeutic frontiers. These advanced lasers interact with tissue through photodisruption rather than photothermal effects, effectively vaporizing target material without generating heat that could damage adjacent structures. The introduction of tunable solid-state lasers has further expanded their applicability, allowing clinicians to select optimal wavelengths for specific pathologies within a single session. Manufacturers are increasingly integrating these advanced sources into compact, user-friendly platforms suitable for outpatient settings, democratizing access to high-end technology. The growing acceptance of laser lithotripsy using holmium: YAG solid-state lasers for kidney stone fragmentation further drives volume. Innovation is enhancing pulse control and delivery systems, expanding the clinical utility of solid-state lasers. This progress is attracting significant investment and driving rapid adoption across diverse medical specialties.

By Application Insights

The dermatology segment led the Europe medical lasers market and captured a 38.8% share in 2025. This leading position of the segment is attributed to the high prevalence of skin disorders, the booming aesthetic medicine industry, and the widespread availability of laser treatments in both clinical and non-clinical settings across the continent. The staggering prevalence of dermatological conditions and skin cancers across Europe serves as the primary engine for the dermatology segment's dominance. A study indicates that skin diseases affect a considerable share of the European population, creating a massive patient pool requiring effective therapeutic interventions. Specifically, the incidence of non-melanoma skin cancer has risen sharply, with a substantial number of new cases diagnosed annually, necessitating precise ablative techniques for removal and reconstruction. Laser therapy offers a superior alternative to surgical excision for many lesions, providing better cosmetic outcomes and reduced scarring, which is highly valued by patients. Conditions such as port-wine stains, hemangiomas, and severe acne scarring, which affect millions of Europeans, are increasingly treated with pulsed dye and fractional lasers due to their proven efficacy. National health services in countries like Germany and the UK routinely reimburse laser treatments for medically necessary dermatological conditions, ensuring steady demand. The aging population further exacerbates the burden of skin pathologies, driving the need for regular monitoring and intervention. As awareness of early detection and treatment grows, the reliance on laser technology as a first-line therapy for various dermatological ailments continues to solidify its market leadership. The explosive growth of the aesthetic medicine sector and the shifting consumer preference towards non-surgical rejuvenation procedures significantly boost the dermatology segment. European consumers are increasingly seeking minimally invasive solutions for anti-aging, hair removal, and skin resurfacing, driven by social media influence and a cultural emphasis on youthful appearance. Unlike surgical facelifts, laser treatments offer immediate results with minimal downtime, appealing to busy professionals and younger demographics. The proliferation of medical spas and aesthetic clinics across major European cities has democratized access to these technologies, moving them beyond hospital walls into retail-like environments. Technological advancements have also improved safety profiles for darker skin types, expanding the addressable market. Economic data suggests that despite fluctuations in discretionary spending, the aesthetic laser market has shown resilience, with annual growth rates consistently outpacing other elective medical sectors. This robust demand for cosmetic enhancement ensures that dermatology remains the largest and most dynamic application segment for medical lasers in Europe.

The urology segment is estimated to register the fastest CAGR of 9.4% from 2026 to 2034. This rapid expansion of the segment is fueled by the rising incidence of urological stones and benign prostatic hyperplasia, coupled with the definitive shift towards endoscopic laser surgeries as the standard of care. The escalating burden of urolithiasis (kidney stones) and benign prostatic hyperplasia (BPH) across Europe is the foremost driver propelling the urology segment's rapid growth. Epidemiological studies reveal that the lifetime risk of developing kidney stones in Europe is approximately 5% to 10%, with recurrence rates exceeding 50 percent within ten years, creating a perpetual demand for effective fragmentation technologies. Similarly, BPH affects over 50 percent of men aged 50 and above, a demographic that is expanding rapidly due to the aging population. Traditional open surgeries for these conditions are being rapidly replaced by laser-based endoscopic procedures such as Holmium Laser Enucleation of the Prostate (HoLEP) and laser lithotripsy, which offer shorter hospital stays and faster recovery. The clinical superiority of lasers in terms of stone-free rates and reduced bleeding complications drives their adoption. As the prevalence of these conditions rises with lifestyle changes and demographic shifts, the volume of laser-assisted urological procedures is set to surge, making this the fastest-growing application area. The strategic paradigm shift towards minimally invasive endoscopic surgeries in urology is significantly accelerating the adoption of medical lasers. Healthcare systems across Europe are under pressure to reduce hospital bed occupancy and optimize resource utilization, favoring day-case procedures that lasers facilitate. Laser fibers can be passed through flexible ureteroscopes and cystoscopes, allowing surgeons to treat pathologies deep within the urinary tract without external incisions. The versatility of modern laser platforms, which can switch between cutting, coagulating, and fragmenting modes instantly, enhances surgical efficiency and reduces operative time. Furthermore, the development of thulium fiber lasers has introduced even higher frequencies and finer fragmentation capabilities, setting new benchmarks for performance. Hospitals are investing heavily in upgrading their endoscopic suites with advanced laser systems to meet patient expectations for less painful and quicker recoveries. This transition from open and electro-surgical methods to laser-based endoscopy is transforming urological practice, driving sustained double-digit growth for the segment.

REGIONAL ANALYSIS

Germany Medical Lasers Market Analysis

Germany was the top performer in the Europe medical lasers market and occupied a 24.7% share in 2025. Its world-leading engineering sector, robust healthcare infrastructure, and high adoption rate of advanced surgical technologies are the factors supporting this dominance of the German market. The German market is distinguished by its strong domestic manufacturing base, hosting global leaders in laser technology who drive innovation and set international standards. The country's healthcare system, characterized by high reimbursement rates and a dense network of specialized clinics, facilitates rapid adoption of cutting-edge laser devices. Research indicates that Germany performs the highest number of refractive eye surgeries and aesthetic laser procedures per capita in Europe, reflecting a culture that values technological precision and quality of life. The presence of renowned research institutions and university hospitals fosters close collaboration between industry and academia, accelerating the translation of novel laser applications into clinical practice. Strict regulatory oversight ensures only high-quality devices enter the market, building trust among practitioners and patients. Furthermore, the aging population in Germany drives significant demand for laser treatments in oncology, ophthalmology, and urology. The statutory health insurance system covers a wide range of medically necessary laser therapies, ensuring broad patient access. The combination of industrial strength, favorable reimbursement policies, and a tech-savvy medical community cements Germany's status as the dominant force and primary growth engine for the European medical lasers market.

France Medical Lasers Market Analysis

France was the second-largest country in the regional market and accounted for a share of 17.6% in 2025. The French market is propelled by its status as a global hub for cosmetics and aesthetic surgery, driving immense demand for dermatological and aesthetic laser systems. Moreover, the demand for these lasers in France is due to a strong tradition in aesthetic medicine, a centralized healthcare system, and significant government support for medical innovation. France boasts one of the highest densities of aesthetic clinics in Europe, where laser hair removal and skin rejuvenation are routine procedures accepted by all demographics. The national healthcare system provides comprehensive coverage for laser treatments related to vascular anomalies, skin cancers, and ophthalmic conditions, ensuring steady utilization in public hospitals. The government's "France 2030" investment plan includes substantial funding for health tech innovation, supporting the development of next-generation laser devices. French universities are at the forefront of clinical research in laser oncology and photodynamic therapy, validating new protocols that drive adoption. The cultural emphasis on beauty and wellness, combined with a rigorous medical training framework, creates a sophisticated market where high-performance laser systems are highly valued. This blend of aesthetic vibrancy, public health support, and research excellence sustains France's position as a key pillar of the European market.

United Kingdom Medical Lasers Market Analysis

The United Kingdom holds a significant share of the European market due to the dual dynamics of the National Health Service adopting laser technologies for cost-effective day-case surgeries and a robust private sector catering to elective aesthetic and corrective procedures. Also, the UK market has a mix of public NHS procurement, a thriving private healthcare sector, and strong regulatory frameworks governing laser safety. The NHS has increasingly integrated laser lithotripsy and endovenous laser ablation into standard care pathways to reduce waiting lists and hospital stays. The private sector, particularly in London and major cities, is a hotspot for advanced aesthetic laser treatments, fueled by high disposable incomes and medical tourism. The UK maintains some of the strictest laser safety regulations in Europe, enforced by bodies like the Care Quality Commission, which mandates rigorous training and accreditation for laser operators, ensuring high standards of care. This regulatory environment, while demanding, builds confidence in laser safety and efficacy. Furthermore, the presence of leading ophthalmic centers drives the adoption of femtosecond lasers for cataract and refractive surgery. The convergence of public efficiency goals and private luxury demand creates a balanced and resilient market landscape, keeping the UK at the forefront of medical laser utilization in Europe.

Italy Medical Lasers Market Analysis

Italy grew steadily in the Europe medical lasers market. This market position is supported by a robust optical device manufacturing base, a strong fashion heritage, and elevated sun-exposure risks. The Italian market is driven by a deep-seated cultural emphasis on personal appearance and aesthetics, making it one of the largest markets for cosmetic laser procedures in Southern Europe. The high levels of UV exposure in the Mediterranean region contribute to a significant incidence of skin cancers and photo-aging, driving demand for diagnostic and therapeutic laser solutions. The country is also home to several specialized manufacturers of medical laser components and systems, fostering a competitive domestic supply chain. The Italian National Health Service supports laser treatments for essential medical conditions, while the private sector thrives on aesthetic demand. The integration of laser technology in dental practices is also growing rapidly, with Italian dentists increasingly adopting diode lasers for soft tissue management. Regional disparities exist, with northern regions showing higher adoption rates of advanced technologies, but national initiatives aim to bridge this gap. The combination of aesthetic culture, medical necessity, and industrial capability ensures Italy remains a vital and growing segment of the European market.

Spain Medical Lasers Market Analysis

Spain is expected to expand notably during the forecast period for the European market, owing to its emergence as a top destination for medical tourism, particularly for aesthetic and ophthalmic laser procedures, attracting thousands of international patients annually. Its landscape is characterized by a growing medical tourism industry, increasing investment in public healthcare modernization, and a rising awareness of minimally invasive treatments. The country's sunny climate contributes to a high prevalence of skin disorders and sun damage, sustaining strong demand for dermatological laser therapies. Recent government initiatives to modernize public hospitals have led to increased procurement of advanced surgical lasers for urology and gynecology, aiming to reduce surgical wait times and improve outcomes. The private healthcare sector is also expanding, with new clinics opening in major cities like Madrid and Barcelona, equipped with state-of-the-art laser platforms. Spanish researchers are actively contributing to clinical trials in laser oncology and regenerative medicine, enhancing the evidence base for local adoption. The growing middle class and increasing health consciousness are further driving the uptake of elective laser treatments. Spain is boosting its healthcare infrastructure and maximizing its geographic advantage for medical tourism. This surge drives steady, significant growth for the medical laser market.

COMPETITION OVERVIEW

The competition in the Europe medical lasers market is characterized by intense rivalry among established multinational corporations and agile specialized manufacturers striving for dominance in a highly regulated environment. Large incumbents leverage their extensive distribution networks, broad product portfolios, and strong brand reputations to secure major hospital contracts and influence clinical guidelines. These companies differentiate themselves through continuous innovation in laser wavelengths, pulse durations, and delivery systems to meet evolving surgical demands. Conversely, smaller niche players often target specific applications such as dentistry or phlebology with highly specialized and cost-effective devices. Price competition is significant, particularly in public procurement tenders where cost efficiency is a primary decision factor alongside technical specifications. Regulatory compliance with the European Medical Device Regulation acts as a substantial barrier to entry, favoring companies with robust quality systems and resources for lengthy approval processes. The shift towards value-based healthcare drives manufacturers to offer comprehensive service packages, training, and data analytics solutions rather than just hardware. Strategic partnerships and mergers are common as companies seek to consolidate market share and enhance technological capabilities. Overall, the landscape demands constant adaptation to regulatory changes, technological advancements, and shifting healthcare priorities to sustain growth and maintain leadership positions.

KEY MARKET PLAYERS

A few major players of the Europe medical lasers market include

- Lumenis Ltd

- Candela Corporation

- Alma Lasers

- Fotona

- Biolase Inc

- El.En. S.p.A

- Bausch Health Companies Inc

- Cutera Inc

- IRIDEX Corporation

- Koninklijke Philips N.V

Top Strategies Used by Key Market Participants

Key players in the Europe medical lasers market primarily focus on continuous product innovation and the development of multi-platform systems to address diverse clinical needs efficiently. Companies frequently invest in research and development to integrate artificial intelligence and robotic assistance into laser devices for enhanced precision and safety. Another major strategy involves strategic acquisitions of smaller technology firms to expand product portfolios and gain access to novel wavelength technologies or delivery systems. Manufacturers also prioritize extensive clinical training and education programs for healthcare professionals to ensure optimal device utilization and build strong customer relationships. Expanding distribution networks through local partnerships and service centers is crucial for providing timely maintenance and support across various European regions. Furthermore, firms emphasize regulatory compliance by maintaining rigorous quality management systems to navigate the complex European Medical Device Regulation landscape effectively. Collaborations with academic institutions and hospitals help validate new applications and generate robust clinical data. Cost optimization through modular design allows companies to offer scalable solutions that fit different budget constraints while maintaining high performance standards.

Leading Players in the Europe Medical Lasers Market

- Lumenis Ltd stands as a global pioneer in the Europe medical lasers market, renowned for its comprehensive portfolio spanning ophthalmology, urology, and dermatology. The company contributes significantly to the worldwide sector by introducing groundbreaking technologies such as the Pulse 120H laser for kidney stone treatment. Recent actions include the strategic expansion of its digital health ecosystem to integrate artificial intelligence into laser platforms for enhanced procedural precision. Lumenis actively collaborates with European clinical centers to validate new applications for its high-power diode and solid-state systems. The firm has also strengthened its supply chain resilience by establishing regional distribution hubs across key European nations to ensure rapid equipment delivery. By focusing on continuous innovation and robust training programs for surgeons, Lumenis reinforces its reputation as a leader in minimally invasive surgical solutions. These efforts solidify its position as a trusted partner for healthcare providers seeking advanced laser therapies throughout Europe and the global marketplace.

- Alma Lasers Ltd is a pivotal player in the Europe medical lasers market, specializing in energy-based devices for aesthetic and surgical applications. The company plays a crucial role globally by delivering versatile platforms that combine multiple wavelengths for diverse skin treatments and surgical procedures. Recent strategies involve the launch of next-generation hybrid laser systems designed to treat a broader range of skin types with improved safety profiles. Alma Lasers has expanded its footprint in Europe through targeted partnerships with leading dermatology clinics and aesthetic centers to demonstrate clinical efficacy. The firm invests heavily in research and development to create compact, user-friendly devices suitable for both large hospitals and private practices. Additionally, Alma Lasers focuses on sustainability by optimizing energy consumption in its newer models. By prioritizing customer support and offering comprehensive warranty packages, the company builds strong loyalty among practitioners. These initiatives enhance its competitive edge and drive adoption of its innovative laser solutions across the European and international markets.

- Biolitec AG operates as a major force in the Europe medical lasers market, known for its expertise in diode laser technology and flexible fiber delivery systems. The company contributes to the global landscape by providing specialized solutions for phlebology, dentistry, and ENT surgery that emphasize minimal invasiveness. Recent actions include the introduction of radial emitting fibers that allow for 360-degree tissue treatment, revolutionizing procedures like vein ablation and tumor reduction. Biolitec actively engages in educational workshops across Europe to train physicians on the latest laser techniques and safety protocols. The firm has strengthened its market position by acquiring complementary technology firms to broaden its product offerings and enhance system integration. Furthermore, Biolitec emphasizes cost-effectiveness by developing durable, low-maintenance laser sources that reduce operational expenses for clinics. By focusing on niche applications and delivering high-quality German engineering, Biolitec continues to expand its influence. These strategic moves ensure its status as a key innovator and reliable supplier in the evolving global medical laser industry.

MARKET SEGMENTATION

This research report on the Europe medical lasers market has been segmented and sub-segmented based on product, application & region.

By Product

- Diode Lasers

- Solid State Lasers

- Gas Lasers

- Dye Lasers

By Application

- Dermatology

- Ophthalmology

- Gynecology

- Urology

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers of the Europe microphones market?

Growth is driven by increasing podcasting, live streaming, music production, and remote working trends.

2. Which types of microphones are most popular in Europe?

Condenser microphones and dynamic microphones are the most widely used across professional and consumer applications.

3. How is the podcasting trend impacting the market?

The rise of podcasting has significantly increased demand for high-quality USB and condenser microphones.

4. What role does gaming play in market growth?

Gaming and esports are boosting demand for headset microphones and streaming equipment.

5. What are the major challenges in the market?

High competition, price sensitivity, and availability of low-cost imports are key challenges.

6. How is wireless technology influencing the market?

Wireless microphones are gaining popularity due to convenience and mobility in events and performances.

7. What distribution channels are prominent in Europe?

Online retail channels are growing rapidly alongside traditional offline stores.

8. What is the impact of remote work on microphone demand?

Remote work has increased demand for microphones for virtual meetings and communication.

9. What trends are shaping the future of the market?

Smart microphones, AI integration, and noise-cancellation technologies are key trends.

10. What is the future outlook of the Europe microphones market?

The market is expected to grow steadily with increasing digital content creation and technological advancements.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com