Europe Mice Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Event, Service, Organizer, End-User, And By Region (The UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033.

Europe MICE Market Report Summary

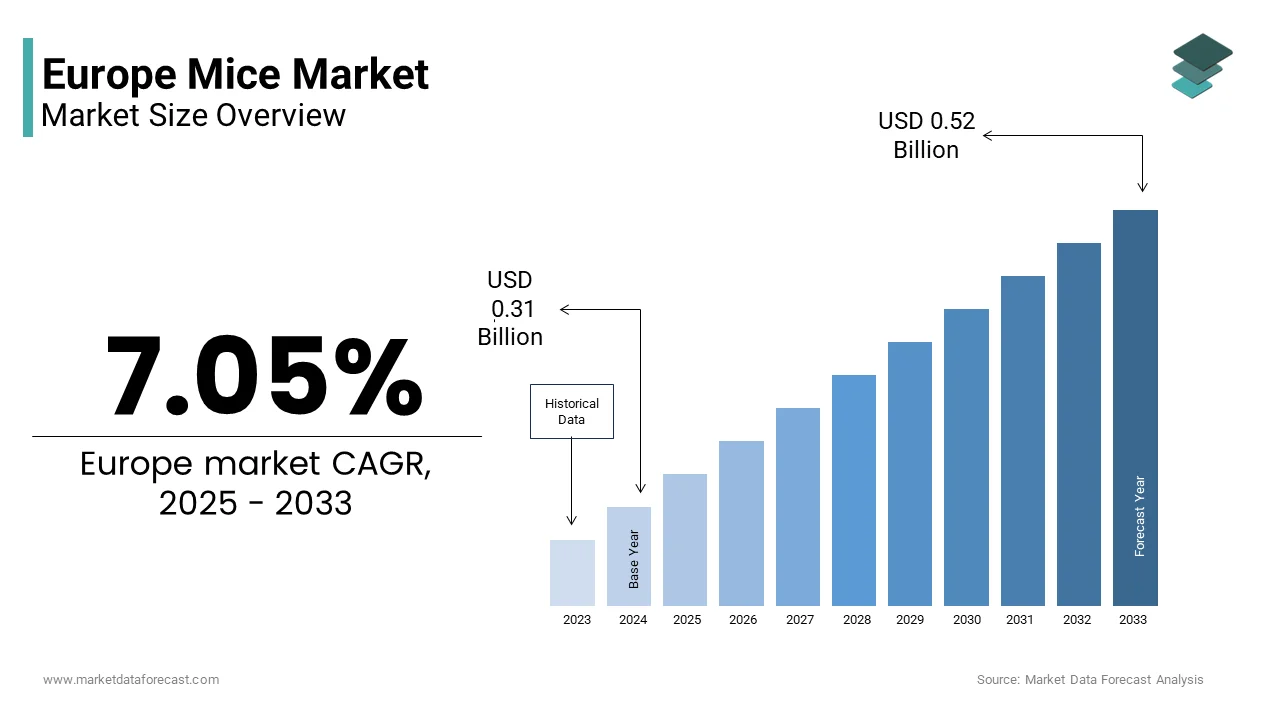

The Europe MICE market was valued at USD 0.29 billion in 2024, is estimated to reach USD 0.31 billion in 2025, and is projected to reach USD 0.52 billion by 2033, growing at a CAGR of 7.05% during the forecast period from 2025 to 2033.

The growth of the Europe MICE market is driven by rising corporate travel, expanding knowledge-based industries, and increasing investments in large-scale international business events. Europe’s strong tourism infrastructure, cultural appeal, and globally recognized convention venues continue to position the region as a preferred destination for meetings, conferences, and exhibitions. Furthermore, the expansion of professional associations, government-led event initiatives, and the integration of digital event technologies are strengthening market demand. Hybrid event formats, sustainable event management practices, and rising interest from multinational corporations further support the market’s long-term expansion across Europe.

Key Market Trends

- Growing demand for large-scale conferences and corporate events as businesses expand cross-border collaboration.

- Rising adoption of hybrid and virtual event technologies enables broader participation and cost efficiency.

- Increasing focus on sustainable event planning, including carbon-neutral venues and eco-friendly logistics.

- Strengthening the role of destination marketing organizations (DMOs) in promoting Europe’s event locations.

- Growth of sector-specific exhibitions, particularly in technology, life sciences, manufacturing, and creative industries.

Segmental Insights

- By Event, the conferences segment held the largest share of 36.6% in 2024, driven by strong participation from multinational corporations, academic institutions, and professional associations seeking high-quality networking and knowledge-sharing environments.

- By Service, the event planning and management segment dominated the market with a 52.4% share, supported by rising outsourcing of event operations, demand for specialized logistics, and the increasing complexity of large-scale corporate events.

- By end-user industry, the IT and Telecom segment led the market at 28.5% in 2024, reflecting the sector’s high frequency of product launches, innovation summits, training programs, and international conferences.

Regional Insights

- Germany, the germany led the market with a 21.4% share in 2024, supported by world-class convention centers, strong trade fair infrastructure, and a well-developed corporate event ecosystem.

- United Kingdom, the UK, followed with a 16.8% share, driven by London’s global event prominence, strong hospitality sector, and high concentration of multinational corporate headquarters.

- France, the france remains a major MICE hub, supported by its cultural prestige, diplomatic presence, and government-backed promotion of international events across cities such as Paris, Lyon, and Cannes.

- Italy, Italy is experiencing rapid growth due to its combination of historical venues, luxury tourism appeal, fashion leadership, and increasing public investment in MICE infrastructure.

- Spain, the spain is projected to expand significantly from 2025 to 2033, driven by the rise of Barcelona and Madrid as international conference hotspots and the country's focus on tourism-led economic development.

Competitive Landscape

The Europe MICE market is highly competitive, characterized by global event management firms, destination management companies, exhibition organizers, and venue operators. Companies are focusing on technological advancements, hybrid event capabilities, sustainable event design, and strategic partnerships with tourism boards and corporate clients. The shift toward experience-driven events, personalization, and seamless digital integration is reshaping competitive strategies across the region.

Major companies operating in the Europe MICE market include CWT Meetings & Events, BCD Meetings & Events, Maritz Global Events, American Express Meetings & Events, FCM Meetings & Events, Conference Care Ltd, ATPI Ltd, Global Cynergies LLC, Creative Group Inc., Reed Exhibitions (RX), Informa Markets, Messe Frankfurt GmbH, GL Events SA, MCI Group, Clarion Events Ltd, Hyve Group plc, Comexposium, dmg events, Messe München GmbH, and Koelnmesse GmbH.

Europe Mice Market Size

The Europe mice market size was valued at USD 0.29 billion in 2024 and is anticipated to reach USD 0.31 billion in 2025 to USD 0.52 billion by 2033, growing at a CAGR of 7.05% during the forecast period from 2025 to 2033.

Mice refer to the computer input devices designed for cursor control, navigation, and command execution across personal, professional, and specialized computing environments. Modern mice in Europe range from basic wired models to advanced wireless, ergonomic, and gaming variants featuring high precision sensors, customizable buttons, and adaptive ergonomics. The category has evolved beyond mere functionality to reflect user identity, workplace wellness priorities, and performance demands. According to Eurostat, the vast majority of European households now have internet access, reflecting high adoption of digital devices that support evolving work arrangements like remote and hybrid models. As per the European Agency for Safety and Health at Work, musculoskeletal disorders remain a significant concern for workers, prompting increased interest in ergonomic solutions and workplace adjustments. Additionally, the rise of digital content creation and competitive gaming has intensified demand for high-performance mice with sub-millisecond response times and programmable profiles. The European Committee for Standardization has also introduced ergonomic design guidelines for computer peripherals under EN ISO 9241, influencing product development. Unlike commoditized electronics, the mice market in Europe is increasingly shaped by human-centered design, regulatory health considerations, and digital lifestyle segmentation.

MARKET DRIVERS

Proliferation of Remote and Hybrid Work Models

The structural shift toward flexible work arrangements has significantly amplified demand for reliable and ergonomic computer mice across European households, which in turn drives the growth of the Europe mice market. As per sources, the prevalence of hybrid and remote work across the European Union has increased significantly since before the pandemic. This decentralization of work has transferred responsibility for ergonomic equipment from employers to individuals, prompting consumers to invest in higher-quality peripherals. Remote work's rise has highlighted the need for proper ergonomic gear, prompting many employees to upgrade their home offices to avoid physical strain. In countries with high rates of remote work adoption, the market has seen a corresponding rise in the sale of ergonomic accessories like vertical and trackball mice, which are designed to support more neutral wrist postures. Further,e to support the shift to remote work, several national governments, including France and Finland, have introduced specific tax guidance or flat-rate allowances that enable citizens to deduct certain work-from-home expenses, though specific limits and rules apply. This policy and behavioral convergence have transformed the mouse from a basic accessory into a critical tool for workplace health and productivity in the post-pandemic European economy.

Growth of Esports and High-Performance Computing Lifestyles

The competitive gaming and digital creator economy has catalyzed demand for premium, feature-rich mice tailored to precision, speed, and customization, which further propels the expansion of the Europe mice market. Europe maintains a large and engaged gaming population, with a notable portion of players participating in or consuming content related to competitive gaming and streaming activities, according to sources. Major esports tournaments, often held in locations like Germany and Poland, heavily influence consumer choices in gaming peripherals, driving a preference for specific features in mice and other gear. The market for advanced gaming mice featuring customizable options such as adjustable polling rates and onboard memory is experiencing significant growth in the European market. Simultaneously, the expanding number of creative professionals across the EU is contributing to an increased demand for specialized computer mice featuring productivity-enhancing functions like programmable buttons and tilt wheels for use in professional software. Creative professionals typically prioritize functional performance, such as sensor accuracy and precision, over cosmetic factors when selecting input devices. This dual engine of entertainment and professional creation has repositioned the mouse as a performance instrument, not merely a utility device.

MARKET RESTRAINTS

Market Saturation and Device Integration Trends

High household penetration and the increasing integration of alternative input methods into mainstream computing devices are degrading the growth of the Europe mouse market. The European market for primary computing devices is highly mature, with internet access and household computer availability reaching very high levels across the EU, especially in Northern and Western Europe. Simultaneously, the ubiquity of touchpads on laptops, touchscreen monitors, and voice-assisted interfaces reduces reliance on traditional pointing devices. Younger consumers show a general preference for versatile, integrated technologies, such as multi-gesture trackpads and touch screen interfaces found on modern laptops and tablets, for daily use and online tasks. Apple’s ecosystem dominance in urban centers like London, Paris, and Copenhagen further suppresses demand, as MacBooks and iPads encourage touch-centric workflows. Besides, the rise of cloud-based computing and thin clients in corporate environments, where IT departments standardize on minimal peripherals, limits replacement cycles. Unlike smartphones or headphones, mice lack frequent innovation triggers that compel upgrades, leading to extended replacement intervals of several years. This combination of saturation and functional redundancy constrains organic market expansion.

Environmental Regulations on E-Waste and Material Use

Stringent European Union directives on electronic waste and hazardous substances impose significant compliance burdens on mouse manufacturers, which inhibit the expansion of the Europe mouse market. This affects design choices and cost structures. The Restriction of Hazardous Substances Directive prohibits lead, mercury, and certain flame retardants commonly used in plastic casings and circuit boards, forcing redesigns that can compromise durability or increase production costs. European Union bodies are increasingly focusing on electronic waste from small peripherals, driving new regulatory scrutiny under expanding ecodesign frameworks. The EU is implementing regulations that mandate increased repairability for various electronic products, including requirements for more modular designs and accessible components. New EU rules will require that portable batteries in many consumer devices are easily replaceable by the end-user by 2027, which necessitates significant product design changes. Companies failing to adapt face restricted market access. National environmental agencies within the EU are actively involved in developing and enforcing stricter market surveillance and compliance checks for electronic goods placed on the market. These regulatory pressures delay product launches and inflate R and D expenses, particularly for smaller brands without dedicated compliance teams.

MARKET OPPORTUNITIES

Expansion of Ergonomic and Health-Focused Product Lines

The growing consumer and corporate emphasis on digital wellness and musculoskeletal health provides new opportunities for the growth of the Europe mice market. This drives demand for ergonomically advanced mice. Vertical mice, trackballs, and finger-operated designs that promote neutral wrist posture are gaining traction, especially in Nordic and Benelux countries, where occupational health is culturally prioritized. Manufacturers like Logitech and Perixx have responded with medical-grade models endorsed by physiotherapy associations in Germany and Sweden. Retailers feature dedicated “wellness tech” aisles, with ergonomic mouse sales growing. This convergence of public health awareness, corporate duty of care, and product innovation positions ergonomic differentiation as a high-margin growth vector beyond conventional performance metrics.

Rise of Subscription and Device as a Service Models in Enterprise

Enterprises across the region are increasingly adopting Device as a Service models that bundle hardware, software, and lifecycle management into operational expenditures, which generates fresh possibilities for the Europe mice market. This creates new channels for mouse deployment. Corporations, particularly large enterprises, are increasingly adopting managed services to achieve operational efficiency, manage costs, and focus on their core business activities. These contracts typically include three-to-five-year refresh cycles with guaranteed ergonomics and compatibility, ensuring steady demand for business-grade mice. Additionally, these services often include end-of-life recycling compliant with WEEE directives, addressing corporate sustainability goals. DaaS platforms enhance logistical efficiency by centralizing integrated provisioning, a crucial solution as tracking physical assets becomes harder with hybrid work models. This shift from capital to operational procurement transforms mice from disposable items into managed assets, opening recurring revenue streams for vendors with enterprise certification and service infrastructure.

MARKET CHALLENGES

Intensifying Price Competition from Asian OEMs

Aggressive pricing pressure from Asian original equipment manufacturers offers near identical specifications at significantly lower costs, which challenges the growth of the Europe mice market. Brands from China and Vietnam now supply white label mice to major European retailers at lower margins, undercutting established players who maintain higher quality controls and compliance overheads. These budget models often mimic the form factor and DPI claims of premium brands but use lower-grade switches, leading to premature failure. However, price-sensitive consumers, particularly students and small offices, prioritize upfront cost over longevity. This dynamic compresses profitability for mid-tier brands and forces premium players to justify higher prices through demonstrable health or performance benefits, fragmenting the market along value and quality lines.

Fragmentation of Connectivity Standards and Compatibility Issues

The coexistence of multiple wireless protocols, Bluetooth, proprietary 2.4 GHz dongles, and emerging Matter over Thread, creates confusion and compatibility barriers for the regional consumers, which hinders the expansion of the Europe mouse market. Unlike keyboards or monitors, mice often require specific drivers or receiver pairing that may not function across operating systems or legacy devices. Gaming mice face additional hurdles; anti-cheating software in titles like Valorant and Fortnite often blocks third-party input devices, limiting cross-platform utility. This technological fragmentation inhibits seamless user experiences and deters casual buyers from upgrading, especially when their current wired mouse remains fully functional. Until universal plug-and-play standards emerge, interoperability will remain a persistent friction point in the European mice ecosystem.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| CAGR | 7.05% |

| Segments Covered | By Event, Service, Organizer, End-User, & Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

| Market Leaders Profiled | CWT Meetings & Events, BCD Meetings & Events, Maritz Global Events, American Express Meetings & Events, FCM Meetings & Events, Conference Care Ltd, ATPI Ltd, Global Cynergies LLC, Creative Group Inc., Reed Exhibitions (RX), Informa Markets, Messe Frankfurt GmbH, GL Events SA, MCI Group, Clarion Events Ltd, Hyve Group plc, Comexposium, dmg events, Messe Munchen GmbH, Koelnmesse GmbH |

SEGMENTAL ANALYSIS

By Event Insights

The conferences segment held the leading share of 36.6% of the Europe mice market in 2024. The prominence of the conferences segment is attributed to academic and professional knowledge exchange that drives conference dominance, and regulatory and policy forums, which reinforce institutional conference demand. Europe’s dense network of universities, research institutions, and multinational corporations creates sustained demand for large-scale academic and industry conferences. Cities like Vienna, Barcelona, and Copenhagen have developed specialized conference infrastructures, including integrated digital platforms for hybrid participation. Besides, professional bodies such as the European Medical Association and CERN regularly rotate major congresses across member states, ensuring consistent venue utilization. Unlike shorter meetings or reward-based incentives, conferences generate significant economic impact, making them a priority for national tourism strategies seeking high-value business travelers. Europe serves as the epicenter for international policy dialogue, hosting permanent institutions like the European Parliament, NATO, and the World Health Organization’s European office. These entities convene recurrent regulatory, diplomatic, and compliance forums that require secure, high-capacity venues. The EU’s Green Deal and Digital Markets Act have further triggered sector-specific compliance summits in finance, energy, and tech, often mandated for industry participation. National governments also host annual economic forums, such as France’s Choose France summit, that blend policy announcements with investment attraction. These events are non-discretionary, recurring, and often subsidized, insulating them from economic volatility that affects discretionary segments like incentives. This institutional anchoring ensures conferences remain the backbone of Europe’s MICE ecosystem.

The exhibitions segment is estimated to register the fastest CAGR of 9.7% from 2025 to 2033 due to the post-pandemic revival of trade and B2B networking imperatives, and integration with national export and industrial policy. After years of virtual alternatives, businesses across Europe have re-recognized the irreplaceable value of face-to-face trade exhibitions for relationship building, product demonstration, and market intelligence. Exhibitions offer tactile engagement impossible in digital formats, critical for sectors like machinery, luxury goods, and automotive, where sensory evaluation drives purchasing. Furthermore, hybrid models now integrate lead capture analytics and AI matchmaking, enhancing ROI and justifying premium exhibitor fees. This blend of emotional, commercial, and technological factors is accelerating the return of large-scale physical showcases. European governments strategically leverage exhibitions as tools for economic diplomacy and export promotion. The EU’s Critical Raw Materials Act and Chips Act have spurred specialized exhibitions focused on semiconductor supply chains and rare earth processing, attracting policymakers and investors. These events function as ecosystem orchestrators, aligning public policy with private sector visibility. Unlike transient meetings or leisure-oriented incentives, exhibitions generate measurable trade outcomes, export leads, joint ventures, and policy feedback, making them a high priority in national competitiveness agendas and driving their accelerated growth.

By Service Insights

The event planning and management segment was the largest in the Europe mice market and occupied a 52.4% share in 2024. The leading position of the event planning and management segment is attributed to the complexity of multinational compliance and stakeholder coordination, and demand for seamless hybrid and technology-integrated experiences. Organizing MICE events in Europe requires navigating a labyrinth of cross-border regulations, labor laws, and sustainability mandates that demand expert orchestration. The EU’s General Data Protection Regulation alone necessitates specialized handling of attendee data, while the Corporate Sustainability Reporting Directive obliges event planners to track carbon footprints per participant. Professional planners bring certified expertise in accessibility standards under the European Accessibility Act, multilingual staffing, and crisis protocols for high-profile gatherings. This regulatory and operational complexity transforms event planning from a logistical task into a strategic risk mitigation function, justifying its dominant service share. Modern MICE events require synchronized physical and digital dimensions, including live streaming, AI-driven networking, and real-time translation, capabilities beyond the scope of in-house teams. These firms manage everything from bandwidth provisioning to virtual booth design, ensuring parity between in-person and remote participants. The rise of “phygital” formats, where physical exhibits trigger digital content, further demands technical fluency. Additionally, post-event analytics on engagement, sentiment, and lead quality are now standard deliverables, requiring data science competencies. Corporations increasingly view planners as innovation partners rather than vendors, embedding them early in strategy. This technology intensity elevates planning from execution to experience architecture, cementing its market leadership.

The venue sourcing and management segment is anticipated to witness the fastest CAGR of 11.2% from 2025 to 2033. The rapid expansion of the venue sourcing and management segment is fuelled by the scarcity of certified sustainable and accessible venues and the rise of decentralized and thematic venue selection. Europe faces a shortage of event spaces that simultaneously meet EU sustainability criteria, accessibility standards, and capacity requirements. Moreover, the European Accessibility Act requires step-free access, induction loops, and gender-neutral restrooms. Professional venue sourcers now use digital twins and carbon calculators to pre-qualify locations, saving clients an average of 200 hours in site visits. Cities have responded by retrofitting convention centers, but demand outstrips supply, especially for mid-sized corporate events. This scarcity elevates venue sourcing from a transactional service to a strategic bottleneck resolution, driving premium adoption. Organizations are moving away from traditional convention centers toward experiential venues, museums, wineries, and historic castles that align with brand narratives. However, these spaces often lack built-in AV infrastructure, catering licenses, or crowd management systems, requiring specialized due diligence. Venue management firms now offer turnkey solutions, including temporary infrastructure permits and local vendor coordination. This shift toward meaningful, story-driven locations increases reliance on expert venue partners, accelerating growth in this specialized segment.

By End User Industry Insights

The IT and Telecom segment led the Europe mice market and captured a share of 28.5% in 2024. The supremacy of the IT and Telecom segment is driven by rapid technology cycles, the demand for physical product launches and developer ecosystems, and cross-border collaboration in EU digital and cybersecurity initiatives. The IT and telecom sector operates on compressed innovation cycles that necessitate high-impact product unveilings and hands-on developer engagement. Events like Mobile World Congress in Barcelona and IFA Berlin serve as global launchpads where companies like Ericsson, Nokia, and SAP announce 5G infrastructure, AI chips, and enterprise software. Developer conferences, such as Google I/O and Microsoft Build, held annually in Europe, train a large number of engineers on new APIs and tools, creating sticky ecosystem dependencies. Unlike sectors with stable product lines, tech thrives on hype and immediacy, making physical gatherings irreplaceable for market signaling and co-creation. This constant need for visibility and technical immersion sustains the IT and telecom sector’s dominance in MICE consumption. Europe’s strategic push for digital sovereignty has triggered a wave of public-private forums on cloud infrastructure, AI ethics, and cybersecurity. The European Cybersecurity Organization hosts annual summits in Brussels attended by ENISA, national agencies, and tech firms to align on threat intelligence and certification frameworks. Similarly, the Gaia X initiative for European cloud federations convenes quarterly stakeholder assemblies across member states. These events are not optional but mandated components of EU regulatory alignment, ensuring consistent participation regardless of economic conditions. This policy-driven ecosystem curation embeds IT and telecom firms in a permanent circuit of high-level MICE engagements.

The healthcare and life sciences segment is likely to experience the fastest CAGR of 12.8% over the forecast period. The swift growth of the healthcare and life sciences segment is attributed to regulatory convergence and clinical trial coordination across the EU, and the rise of medical tourism and cross-border care networks. The European Medicines Agency’s centralized authorization process requires pharmaceutical companies to engage continuously with regulators, clinicians, and patient groups across member states. Major congresses like the European Society for Medical Oncology and ESC Congress attract delegates annually to present trial data and discuss treatment guidelines. The EU’s Clinical Trials Regulation mandates transparency and cross-border collaboration, driving demand for investigator meetings and safety monitoring workshops. These gatherings are essential for harmonizing protocols and accelerating drug access, making them non-negotiable investments even during cost-cutting cycles. Europe’s Directive on Patients’ Rights in Cross-Border Healthcare has stimulated medical tourism clusters that integrate conferences with clinical showcases. Countries like Germany, Spain, and Turkey host “health tourism expos” where hospitals demonstrate robotic surgery and wellness programs to international patients and insurers. Additionally, rare disease networks funded by Horizon Europe organize annual family and physician symposia to share best practices. These hybrid events blend education, care coordination, and commercial outreach, creating a new MICE subcategory that merges clinical rigor with experiential design, fueling exceptional growth in this segment.

COUNTRY ANALYSIS

Germany MICE Market Analysis

Germany dominated the European MICE market and accounted for a 21.4% share in 2024, with its unparalleled infrastructure, central location, and industrial depth. The country hosts flagship global events such as Hannover Messe, IFA Berlin, and CeBIT, drawing millions of business visitors annually. Germany’s federal structure empowers city-states like Frankfurt, Munich, and Düsseldorf to invest heavily in convention centers with integrated rail links and sustainability certifications. Moreover, Germany’s strong manufacturing and engineering base ensures consistent corporate demand for trade exhibitions. With the highest number of ICCA-registered events in Europe and a workforce fluent in multiple languages, Germany remains the undisputed hub for large-scale, high-impact MICE activity.

United Kingdom MICE Market Analysis

The United Kingdom followed closely in the Europe mice market and occupied a 16.8% share in 2024 because of its concentration of global associations, financial institutions, and academic excellence. London alone accounts for a notable share of the UK’s MICE volume, hosting events like the World Travel Market and Farnborough Airshow that leverage the city’s status as a global capital. Despite Brexit, the UK maintains strong ties with European professional bodies and continues to attract EU-funded research conferences through its association with Horizon Europe. Investment in ExCeL London’s net-zero retrofit and hybrid capabilities has further solidified its appeal. The UK’s strength lies not in scale alone but in curating high-value, policy-shaping gatherings that draw elite global audiences.

France MICE Market Analysis

France is moving ahead steadfastly in the Europe market, which is renowned for its blend of cultural prestige, diplomatic infrastructure, and strategic event promotion. Paris ranks among the top three global cities for international association meetings, supported by venues. The Choose France summit, personally hosted by the President, has become a magnet for corporate investment announcements, blending MICE with economic statecraft. The country’s luxury and fashion industries also drive high-end incentive travel to destinations like Cannes and Lyon. France leverages a unified strategy linking tourism, diplomacy, and industry to host superior events that seamlessly blend commerce, culture, and global influence.

Italy MICE Market Analysis

Italy is experiencing rapid growth in the Europe mice market due to its unique combination of historic venues, fashion leadership, and targeted government support. Milan has emerged as Europe’s design and finance MICE capital, hosting Salone del Mobile and the Milan Stock Exchange forums that attract global creatives and investors. Rome and Florence leverage UNESCO heritage sites for high-impact incentives, while Bologna and Rimini offer cost-effective convention facilities with Mediterranean appeal. This renaissance is fueled by a deliberate shift from mass tourism to high-value business events that showcase Italian excellence in fashion, food, and engineering.

Spain MICE Market Analysis

Spain is anticipated to expand notably in the Europe mice market from 2025 to 2033. It is recognized for its year-round climate, modern infrastructure, and success in medical and tech tourism. Barcelona consistently ranks among the top five global cities for international congresses, anchored by venues like Fira de Barcelona and events like Mobile World Congress. Madrid, Valencia, and Seville have invested in sustainable convention districts compliant with the EU Green Public Procurement criteria. Spain’s bilingual workforce and strategic time zone, bridging Europe and the Americas, enhance its appeal for global hybrid events. Aggressive bidding for association meetings and seamless integration of culture and commerce ensure Spain’s continued ascent in the European MICE landscape.

COMPETITIVE LANDSCAPE

Competition in the Europe MICE market is characterized by a mix of global event conglomerates, specialized European associations, and agile local agencies vying for high-value corporate and institutional clients. Large players leverage scale to offer integrated services from venue sourcing to post-event analytics, while regional firms differentiate through cultural fluency and regulatory expertise in specific countries. The market is highly influenced by public policy, with EU directives on sustainability, data protection, and accessibility shaping service expectations. Cities compete aggressively through convention bureau incentives, creating a dynamic bidding environment for international congresses. Differentiation increasingly hinges on demonstrable environmental impact, hybrid readiness, and compliance infrastructure rather than price alone. As organizations demand greater accountability and ROI from business events, providers must combine operational excellence with strategic alignment to Europe’s evolving regulatory and economic landscape to secure long-term client partnerships.

KEY MARKET PLAYERS

A few of the market players in the Europe mice market are

- CWT Meetings & Events

- BCD Meetings & Events

- Maritz Global Events

- American Express Meetings & Events

- FCM Meetings & Events

- Conference Care Ltd

- ATPI Ltd

- Global Cynergies LLC

- Creative Group Inc.

- Reed Exhibitions (RX)

- Informa Markets

- Messe Frankfurt GmbH

- GL Events SA

- MCI Group

- Clarion Events Ltd

- Hyve Group plc

- Comexposium

- dmg events

- Messe Munchen GmbH

- Koelnmesse GmbH

Top Players In The Market

- Reed Exhibitions is a dominant force in the Europe MICE market, operating flagship events such as Iberia Travel Mart, Future Travel Experience Europe, and numerous industry-specific trade shows across technology, healthcare, and sustainability. The company leverages its global portfolio to drive international attendance at European venues while tailoring content to regional regulatory and market dynamics. In recent years, Reed has significantly enhanced its hybrid event capabilities by integrating AI-powered matchmaking and real-time analytics into its platforms. It has also deepened partnerships with European city tourism boards to align event calendars with sustainability certifications and accessibility standards. These initiatives reinforce its role as a catalyst for cross-border business exchange and economic impact across the continent.

- MCI Group contributes extensively to the Europe MICE landscape through its end-to-end management of association congresses, corporate meetings, and incentive programs for clients in pharmaceuticals, finance, and technology. The company operates in many European countries with localized teams that navigate complex compliance requirements, including GDPR and the European Accessibility Act. MCI has recently invested in carbon footprint tracking dashboards for all its European events, enabling clients to meet Corporate Sustainability Reporting Directive obligations. It also launched a digital engagement studio in Amsterdam to design immersive hybrid experiences. Combining specialized knowledge of European regulations with global tech, MCI enhances the region's appeal for secure, compliant business meetings.

- Freeman has established a strong footprint in the Europe MICE market through its comprehensive event production, logistics, and venue services for major exhibitions and conferences. The company supports clients with modular stand construction, audiovisual integration, and on-site staffing across key hubs like London, Frankfurt, and Barcelona. It has also partnered with European convention centers to implement smart badge technology for seamless attendee flow and data security. These sustainability and operational innovations position Freeman as a critical enabler of efficient, compliant, and impactful business events across Europe.

Top Strategies Used By The Key Market Participants

Key players in the Europe MICE market prioritize sustainability compliance by aligning events with EU Green Public Procurement criteria and carbon tracking standards. They invest in hybrid event technologies that integrate physical venues with digital engagement platforms for global reach. Companies form strategic partnerships with national tourism organizations to secure government backing and venue subsidies. They specialize in regulated sectors such as healthcare and technology. Policy-driven gatherings ensure consistent demand. Additionally, they offer end-to-end services, including accessibility planning, data privacy management, and multilingual support to meet Europe’s cross-border requirements.

MARKET SEGMENTATION

This research report on the Europe mouse market is segmented and sub-segmented into the following categories.

By Event Type

- Meetings

- Incentives

- Conferences

- Exhibitions

By Service Type

- Event Planning and Management

- Venue Sourcing and Management

- Accommodation and Hospitality

- Transportation and Logistics

- Catering and FandB

- Event Technology and AV

By Organizer Type

- Corporate

- Government and Public Sector

- Associations and Non-Profits

- Professional Conference Organizers (PCOs)

By End-User Industry

- IT and Telecom

- Healthcare and Life Sciences

- BFSI

- Automotive and Manufacturing

- Energy and Utilities

- Media and Entertainment

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe MICE market?

The Europe MICE market includes meetings, incentives, conferences, and exhibitions hosted across European countries for business, corporate, academic, and professional events.

What drives growth in the Europe MICE market?

Rising corporate travel, strong tourism infrastructure, increased international business collaborations, and government support for event hosting.

Why is Europe a leading region in the global MICE industry?

Europe offers world-class venues, excellent connectivity, cultural attractions, and well-developed hospitality services, making it a preferred destination for global events.

Which countries dominate the Europe MICE market?

Germany, the United Kingdom, France, Spain, and Italy lead due to established convention centers and high international event traffic.

What types of events are most common in the Europe MICE market?

Corporate conferences, trade exhibitions, incentive programs, academic seminars, product launches, and international summits.

What challenges impact the Europe MICE market?

High event-organizing costs, fluctuating travel demand, geopolitical instability, and increased competition from virtual and hybrid event formats.

How has technology influenced the Europe MICE market?

Digital tools, virtual meeting platforms, event management software, and hybrid event formats have expanded participation and improved event planning efficiency.

Why are sustainability efforts growing in the Europe MICE market?

Businesses and organizers are prioritizing eco-friendly venues, low-waste events, and carbon-neutral travel to meet green event standards and sustainability commitments.

Who are the key participants in the Europe MICE market?

Corporate enterprises, event planners, hotels, convention centers, tourism boards, destination management companies (DMCs), and government agencies.

What is the future outlook for the Europe MICE market?

The market is expected to expand as international business travel rebounds, hybrid events become mainstream, and Europe strengthens its position as a global event hub.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com