Europe Microfluidic Devices Market Size, Share, Trends & Growth Forecast Report, Segmented By Device, Material Composition, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Microfluidic Devices Market Size

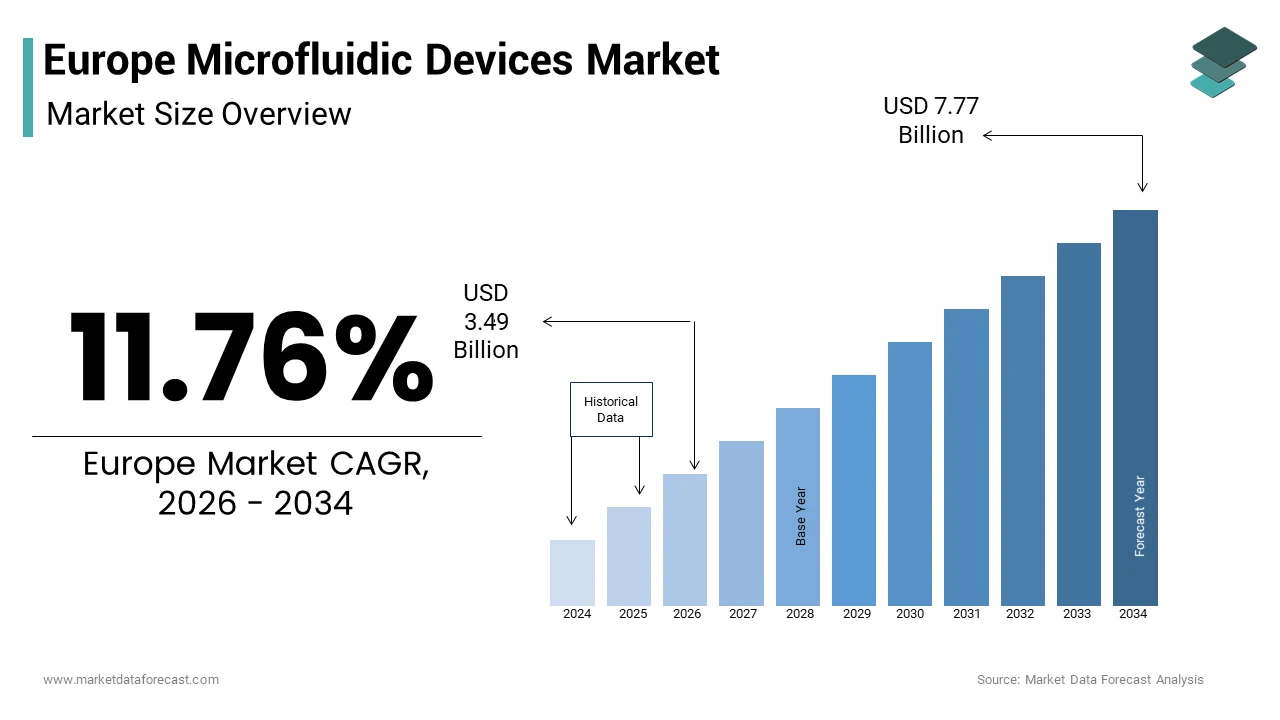

The Europe microfluidic devices market size was valued at USD 3.12 billion in 2025 and is anticipated to reach USD 3.49 billion in 2026 to reach USD 7.77 billion by 2034, growing at a CAGR of 11.76% during the forecast period from 2026 to 2034.

Microfluidic devices, often called "microchips" or "lab-on-a-chip" systems, are miniaturized tools that manipulate extremely tiny amounts of fluid, typically in the range of nanolitres to microlitres, within channels as narrow as a strand of hair. These devices are integral to lab on a chip technologies enabling precise control over chemical and biological processes for diagnostics drug discovery and environmental monitoring. The region serves as a global hub for biomedical innovation driven by robust healthcare infrastructure and significant research funding. According to Eurostat data published in late 2024 and 2025, the European Union's total investment in research and development activities exceeded €403 billion in 2024, with the health sector showing robust growth of 13%, outpacing the U.S. and China. This financial commitment fosters an ecosystem conducive to the adoption of advanced analytical tools. Furthermore, World Health Organization (WHO) reports from 2024 indicate that noncommunicable diseases (NCDs) now account for 90% of all deaths in the European Region, a burden that underscores an urgent need for enhanced diagnostic capacity and early intervention tools. Microfluidic platforms offer rapid point of care testing capabilities that address this growing healthcare burden. The integration of these devices into clinical workflows is further supported by the presence of leading academic institutions and pharmaceutical companies across Germany France and the United Kingdom. The regulatory landscape governed by bodies such as the European Medicines Agency ensures high standards for medical device safety and efficacy thereby enhancing consumer trust and facilitating market penetration for innovative microfluidic technologies.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Drives the Demand for Rapid Diagnostic Solutions

The escalating incidence of chronic conditions across the region acts as a key factor for the adoption of these devices in clinical diagnostics, which contributes to the growth of the Europe microfluidic devices market. Chronic diseases such as cardiovascular disorders diabetes and cancer require continuous monitoring and early detection to manage patient outcomes effectively. According to the World Health Organization (WHO), noncommunicable diseases are the primary cause of death and disability in the European Region, necessitating more advanced and rapid healthcare interventions. Microfluidic technology enables the development of point of care testing devices that provide rapid accurate and cost effective diagnostic results at the bedside or in outpatient settings. This capability significantly reduces the turnaround time for test results compared to traditional laboratory methods which often take several days. For instance, the European Society of Cardiology (ESC) highlights that cardiovascular conditions remain the dominant cause of mortality across its member countries, driving the need for point-of-care diagnostic tools. The ability of microfluidic chips to analyze biomarkers associated with heart attacks using minimal blood samples facilitates timely medical intervention. Additionally the aging population in Europe exacerbates the demand for such technologies. Eurostat demographic data confirms a long-term trend of population ageing across the European Union, a shift that naturally increases the clinical burden of age-related chronic conditions. This demographic shift increases the prevalence of age related ailments thereby driving the utilization of portable and user friendly diagnostic tools. As a result, healthcare providers are increasingly integrating microfluidic based systems into their standard practices to enhance patient care efficiency and reduce overall healthcare costs associated with prolonged hospital stays.

Substantial Government Funding for Biomedical Research Accelerates Technological Innovation

Significant public and private investment in biomedical research and development within the region serves as a critical driver for the Europe microfluidic devices market. Governments and regional bodies recognize the strategic importance of life sciences in maintaining competitive advantage and improving public health outcomes. As per the European Commission Horizon Europe program which is the key funding program for research and innovation with a budget of 95.5 billion euros for the period 2021 to 2027 a considerable fraction is dedicated to health cluster initiatives. This financial support enables academic institutions and startups to conduct pioneering research in microfabrication techniques and bioanalytical applications. For example the German Federal Ministry of Education and Research (BMBF) provides extensive annual funding for health research, prioritizing the development of personalized medicine and the integration of digital health solutions. Such investments facilitate the translation of laboratory discoveries into commercial products by bridging the gap between basic science and industrial application. Moreover countries like France and the United Kingdom have established specialized innovation hubs that foster collaboration between engineers biologists and clinicians. Funding initiatives from the French National Research Agency (ANR) continue to support the expansion of the biotechnology sector, fostering an environment for the advancement of complex research projects and new medical devices. This sustained financial backing encourages the development of next generation microfluidic platforms that offer higher throughput and multifunctionality. So, the vibrant research ecosystem in Europe not only stimulates domestic market growth but also attracts international partnerships thereby reinforcing the region's position as a leader in microfluidic technology advancement.

MARKET RESTRAINTS

High Manufacturing Costs and Complex Fabrication Processes Restrict Market Expansion

The intricate nature of microfluidic device fabrication is a significant restraint to the Europe microfluidic devices market growth. This is due to the associated high production costs and technical complexities. Creating microchannels with precise dimensions requires advanced manufacturing techniques such as photolithography soft lithography and injection molding which demand specialized equipment and skilled personnel. According to the European Association of Research and Technology Organizations (EARTO), establishing the specialized infrastructure required for high-precision microfabrication involves a massive initial capital outlay, creating a significant barrier to entry for smaller firms. This high entry barrier limits the number of manufacturers capable of producing high quality devices at scale. Furthermore the materials used in microfluidics such as polydimethylsiloxane and cyclic olefin copolymer must meet stringent biocompatibility and optical clarity standards which further elevates material costs. Research from the Royal Society of Chemistry (RSC) highlights that the cost of producing individual functional prototypes remains dramatically higher than the per-unit cost of established diagnostic tools produced through high-volume manufacturing. This economic disparity hinders widespread adoption particularly in resource constrained healthcare settings. Additionally the lack of standardized manufacturing protocols leads to variability in device performance which complicates regulatory approval processes. Technical guidelines from the International Organization for Standardization (ISO) emphasize that even minor variations in internal channel architecture or surface chemistry can significantly compromise the reliability and accuracy of fluidic assays. Consequently manufacturers face challenges in achieving economies of scale which keeps end product prices elevated. These financial and technical hurdles slow down the commercialization of innovative microfluidic solutions thereby restricting market penetration and limiting accessibility for potential users across diverse European healthcare environments.

Stringent Regulatory Frameworks and Lengthy Approval Timelines Impede Product Commercialization

The rigorous regulatory landscape governing medical devices in the region poses a substantial barrier to the timely commercialization of microfluidic technologies, which negatively impacts the expansion of the Europe microfluidic devices market. The implementation of the Medical Device Regulation by the European Union has introduced stricter requirements for clinical evidence post market surveillance and conformity assessment. The European Commission notes that the transition to the In Vitro Diagnostic Regulation (IVDR) has significantly extended the time required to bring new products to market, particularly for devices that now require independent oversight for the first time. This prolongation delays market entry and increases development costs for manufacturers. The complexity arises from the need to demonstrate comprehensive safety and performance data through extensive clinical trials which are both time consuming and expensive. Groups like the European Federation of Pharmaceutical Industries and Associations (EFPIA) observe that the heightened requirements for clinical performance data have driven up the total cost of maintaining regulatory compliance for innovative diagnostic platforms. Furthermore the lack of specific guidelines for certain microfluidic applications creates uncertainty for developers regarding the necessary documentation and testing protocols. Notified Bodies which are responsible for assessing conformity often face backlogs due to the heightened scrutiny leading to further delays. Extensive surveys by MedTech Europe reveal that a vast majority of small and medium-sized enterprises face substantial hurdles in interpreting and fulfilling the more rigorous documentation and auditing standards of the current European regulatory environment. These bureaucratic obstacles discourage innovation and limit the diversity of products available in the market. Therefore, companies must allocate substantial resources to regulatory affairs which detracts from research and development efforts thereby slowing the pace of technological advancement and market growth in the European microfluidic sector.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence with Microfluidic Platforms Opens New Avenues for Precision Medicine

The convergence of artificial intelligence and microfluidic technology paves the way for advancing precision medicine and personalized healthcare solutions in the region, which is expected to boost the growth of the Europe microfluidic devices market. AI algorithms can analyze complex data generated by microfluidic assays enabling the identification of subtle patterns and biomarkers that are indicative of specific disease states. EIT Health and its partners emphasize that integrating AI with diagnostic frameworks significantly accelerates the "scan-to-diagnosis" timeline and enhances clinical decision-making by filtering out false positives in complex assays. This synergy allows for the development of smart diagnostic devices that can provide real time insights and predictive analytics for patient management. For example researchers at the Karolinska Institute in Sweden have developed AI enhanced microfluidic chips capable of detecting circulating tumor cells with high sensitivity facilitating early cancer diagnosis. Such innovations align with the growing emphasis on personalized treatment strategies where therapies are tailored to individual genetic profiles. The European Alliance for Personalised Medicine (EAPM) and health economic studies suggest that precision medicine initiatives can generate substantial cost avoidances for healthcare systems by reducing ineffective prescriptions and minimizing hospitalizations due to adverse drug reactions. Furthermore the availability of large datasets from electronic health records and genomic studies provides a robust foundation for training AI models. Eurostat data confirms that near-universal internet access across European households, including high connectivity in rural regions, is establishing the necessary digital infrastructure for widespread health data sharing and tele-diagnostics This digital infrastructure supports the deployment of connected microfluidic devices that transmit data to cloud based platforms for analysis. As a result, the fusion of AI and microfluidics not only enhances diagnostic capabilities but also creates new business models based on data driven healthcare services thereby expanding market opportunities.

Expansion of Point of Care Testing in Remote and Underserved Areas Enhances Market Reach

The growing demand for decentralized healthcare services particularly in remote and underserved regions offers significant growth potential for the Europe microfluidic devices market. Point of care testing enabled by portable microfluidic devices allows for immediate diagnosis and treatment decisions without the need for centralized laboratory facilities. According to the World Health Organization (WHO) and World Bank indicators, a significant quarter of the European population resides in rural areas, creating a sustained need for decentralized diagnostic services that do not rely on urban hospital laboratories. Microfluidic based diagnostic tools are ideal for these settings due to their compact size ease of use and minimal sample requirements. For instance the European Centre for Disease Prevention and Control emphasizes the importance of rapid diagnostic tests for managing infectious disease outbreaks in remote communities. During the recent health crises the deployment of portable microfluidic testers for viral detection demonstrated their effectiveness in controlling spread and guiding public health responses. Additionally the European Union’s Cohesion Policy aims to reduce disparities in healthcare access by investing in infrastructure and technology in less developed regions. Data from the European Structural and Investment Funds indicates that over 10 billion euros were allocated to health infrastructure projects between 2021 and 2027. This financial support facilitates the procurement and distribution of advanced diagnostic equipment in rural hospitals and clinics. Furthermore the rise of telemedicine complements point of care testing by enabling remote consultation and data interpretation. Multiple studies indicate that while the explosive pandemic-era growth has stabilized, the adoption of telehealth and remote monitoring remains a permanent fixture in healthcare delivery, driving demand for connected point-of-care devices that interface directly with virtual consultation platforms. This trend underscores the potential for microfluidic devices to integrate seamlessly into decentralized healthcare networks thereby improving health outcomes and expanding market presence across diverse geographical landscapes in Europe.

MARKET CHALLENGES

Standardization of Manufacturing Protocols Remains a Persistent Technical Hurdle

The lack of uniform standards for the fabrication and performance evaluation of these devices constitutes a major challenge for the Europe microfluidic devices market. Variability in manufacturing processes leads to inconsistencies in device quality which affects reproducibility and reliability of diagnostic results. While the International Organization for Standardization (ISO) has introduced ISO 22916 to harmonize interoperability and connections, universal adoption across all academic and commercial prototypes remains a work in progress. This absence of standardized protocols complicates the comparison of data across different studies and hinders the validation of new technologies. For instance, a review published in the journal Lab on a Chip highlighted that differences in surface treatment methods can result in varying contact angles and flow rates even among devices made from the same material. Such discrepancies pose significant challenges for regulatory approvals and clinical adoption. The European Committee for Standardization has initiated efforts to develop relevant standards but the process is slow due to the rapid pace of technological innovation. As per a report by the European Association of Research and Technology Organizations the lack of standardization increases the time to market for new products by an estimated 6 to 9 months. Manufacturers must therefore invest heavily in internal quality control measures to ensure consistency which raises production costs. Furthermore the diversity of materials and fabrication techniques used in microfluidics makes it difficult to establish universal benchmarks. This fragmentation impedes collaboration between academia and industry as researchers often use proprietary methods that are not easily replicable. Consequently the industry faces difficulties in scaling up production and achieving interoperability between different devices and platforms. Addressing this challenge requires concerted efforts from stakeholders to establish common guidelines that facilitate innovation while ensuring quality and safety.

Shortage of Skilled Professionals Limits Operational Efficiency and Innovation Capacity

The scarcity of trained personnel with expertise in interdisciplinary microfluidics and advanced manufacturing techniques is a serious obstruction to the European microfluidic devices market. Microfluidic technology requires a unique blend of knowledge in physics chemistry biology and engineering which is not commonly found in traditional educational curricula. The European Centre for the Development of Vocational Training (Cedefop) observes a persistent structural imbalance in the labor market, with high-skilled science and engineering roles increasingly difficult to fill as demand outpaces the supply of new graduates. This shortage affects both research and development activities as well as commercial production and maintenance of microfluidic systems. Universities and technical institutes are struggling to keep pace with the evolving demands of the industry leading to a limited pool of qualified candidates. For instance a survey by the European Microfluidics Association revealed that over half of member companies reported difficulties in recruiting engineers with specific experience in microfabrication. This talent deficit slows down the innovation cycle and increases labor costs as companies compete for a limited number of experts. Furthermore the rapid advancement of technology means that existing professionals require continuous training to stay updated with the latest developments. The European Commission’s Digital Education Action Plan aims to address this issue by promoting lifelong learning but the implementation varies across member states. In countries with less developed vocational training systems the gap is more pronounced. Consequently companies may face delays in product development and reduced operational efficiency. To mitigate this challenge industry leaders are collaborating with educational institutions to create specialized programs and internships. However, until a sustainable pipeline of skilled workers is established the shortage will continue to hinder the full potential of the microfluidic devices market in Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.76% |

| Segments Covered | By Device, Material Composition, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Agilent Technologies, PerkinElmer Inc., Danaher Corporation, Bio Merieux SA Thermo Fisher Scientific Inc., Qiagen NV, Bio-Rad Laboratories, Inc., Fluidigm Corporation, Abbott Laboratories, F. Hoffmann-La Roche Ltd, Horizon Microtechnologies, Others |

SEGMENTAL ANALYSIS

By Device Insights

In 2025, the microfluidic chips segment was the prominent segment in the Europe microfluidic devices market and occupied a 58.9% share. This supremacy of the segment is primarily attributed to their widespread integration into diagnostic platforms particularly for point of care testing and genetic analysis. The versatility of chip based systems allows for the miniaturization of complex laboratory processes such as polymerase chain reaction and cell sorting onto a single compact device. Microfluidic chips enable high throughput screening with minimal sample volumes which is crucial for pediatric and geriatric patients. For instance the University of Cambridge developed a chip capable of detecting multiple respiratory viruses simultaneously using less than 10 microliters of blood. This efficiency reduces reagent costs and waste generation aligning with sustainability goals. Furthermore the scalability of chip manufacturing through injection molding techniques has lowered production costs making them accessible to a broader range of healthcare facilities. This widespread adoption is further supported by regulatory approvals for chip based assays by the European Medicines Agency. Consequently the robust demand for accurate and rapid diagnostics continues to propel the microfluidic chips segment to the forefront of the market ensuring its sustained leadership position. The economic advantages associated with microfluidic chips significantly contribute to their market leadership. Mass production techniques such as hot embossing and injection molding allow for the fabrication of thousands of chips at a low unit cost. As per the Fraunhofer Institute for Manufacturing Technology and Advanced Materials the cost per chip can be reduced to under 2 euros when produced at scale. This affordability facilitates widespread deployment in both clinical and research settings. Additionally the disposable nature of many microfluidic chips eliminates the risk of cross contamination which is a critical concern in diagnostic applications. The World Health Organization emphasizes the importance of single use diagnostic tools in preventing healthcare associated infections which affect approximately 4.1 million patients in Europe annually. By providing a sterile and ready to use platform microfluidic chips address this safety concern effectively. Moreover the integration of multiple functions such as sample preparation analysis and detection on a single chip reduces the need for expensive peripheral equipment. A study by the Imperial College London demonstrated that chip based systems could reduce the overall cost of genetic testing by 40 percent compared to traditional methods. This cost efficiency is particularly beneficial for public healthcare systems facing budget constraints. Consequently the combination of low production costs enhanced safety and functional integration drives the extensive adoption of microfluidic chips solidifying their position as the dominant segment in the European market.

The microfluidic sensors segment is likely to experience the fastest CAGR of 14.5% from 2026 to 2034. This accelerated growth of the segment is propelled by the increasing integration of these sensors into wearable health monitoring devices. The rising prevalence of chronic diseases necessitates continuous monitoring of physiological parameters such as glucose lactate and electrolytes. According to the European Diabetes Forum (EUDF) and international health registries, the rising prevalence of diabetes across the continent is a primary driver for the development of continuous and non-invasive monitoring technologies. Microfluidic sensors enable real time analysis of biomarkers in sweat tears and interstitial fluid offering a painless alternative to blood sampling. For example researchers at the Technical University of Munich have developed a wearable microfluidic sensor capable of monitoring cortisol levels in sweat to assess stress responses. This innovation aligns with the growing consumer interest in personalized health and wellness. A study indicates a consistent rise in the adoption of wearable health devices, as consumers increasingly seek tools for real-time physiological tracking and personal wellness management. The ability of microfluidic sensors to provide accurate and continuous data enhances their utility in managing chronic conditions. Furthermore advancements in flexible electronics have improved the comfort and durability of these wearable sensors. Consequently the convergence of microfluidics and wearable technology is driving the rapid expansion of the microfluidic sensors segment offering significant growth opportunities for market participants. The proliferation of Internet of Things connectivity further accelerates the growth of the microfluidic sensors segment. These sensors can transmit data wirelessly to smartphones and cloud based platforms enabling remote patient monitoring and telemedicine applications. This connectivity allows healthcare providers to access real time patient data facilitating timely interventions and personalized treatment plans. For instance the National Health Service in the United Kingdom has initiated pilot programs using connected microfluidic sensors to monitor patients with heart failure at home. These programs have resulted in a reduction in hospital readmissions. The integration of artificial intelligence algorithms with sensor data enhances predictive capabilities allowing for early detection of health deteriorations. Additionally the European Union’s General Data Protection Regulation ensures the security and privacy of health data fostering trust among users. The availability of robust digital infrastructure supports the seamless operation of connected microfluidic sensors. Consequently the synergy between microfluidic sensing technology and Internet of Things connectivity is driving the rapid adoption of these devices across various healthcare settings thereby fueling the segment’s exceptional growth rate.

By Material Composition Insights

The polymer based microfluidic devices segment led the Europe microfluidic devices market and captured a 65.8% share in 2025. This leading position of the segment is supported by the versatility of polymers such as polydimethylsiloxane polycarbonate and cyclic olefin copolymer which offer excellent optical clarity chemical resistance and biocompatibility. The ease of fabrication using techniques such as injection molding and hot embossing allows for mass production at low costs. This economic advantage is crucial for disposable diagnostic devices which require high volume manufacturing. Furthermore polymers enable the integration of various functional elements such as valves and pumps directly into the device structure enhancing functionality. The European Society for Biomaterials shows that polymer based devices are increasingly used in organ on a chip applications due to their ability to mimic biological environments. This versatility extends to diverse applications including drug discovery environmental monitoring and food safety testing. Consequently the combination of cost effectiveness manufacturability and functional versatility ensures that polymer based devices remain the dominant form in the Europe microfluidic devices market. The widespread regulatory acceptance of polymer materials for medical applications further reinforces their market leadership. Agencies such as the European Medicines Agency have established clear guidelines for the use of polymers in medical devices ensuring their safety and efficacy. This regulatory clarity reduces the time and cost associated with product approval encouraging manufacturers to adopt polymer based solutions. Additionally ongoing innovations in polymer science are expanding the capabilities of microfluidic devices. Researchers at the Max Planck Institute for Polymer Research have developed novel hydrogel based polymers that respond to environmental stimuli enabling dynamic control over fluid flow. Such smart materials enhance the functionality of microfluidic systems allowing for more complex biological assays. Furthermore the development of biodegradable polymers addresses environmental concerns associated with disposable devices. This shift towards sustainable materials aligns with the European Green Deal objectives promoting eco friendly manufacturing practices. As a result, the continuous innovation in polymer materials coupled with strong regulatory support sustains the dominance of polymer based microfluidic devices in the European market.

The glass and silicon based microfluidic devices segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 12.8% during the forecast period owing to the demand for high precision and stability in research and specialized diagnostic applications. Glass and silicon offer superior thermal and chemical stability compared to polymers making them ideal for high temperature reactions and harsh chemical environments. Silicon based devices are particularly valued for their ability to integrate electronic components enabling the development of lab on a chip systems with advanced sensing capabilities. For example the Karlsruhe Institute of Technology has developed silicon microfluidic chips for single cell analysis achieving unprecedented resolution and accuracy. These devices are essential for genomics and proteomics research where precise control over experimental conditions is critical. Furthermore glass microfluidics are preferred for applications requiring high optical transparency such as fluorescence microscopy. So, the unique properties of glass and silicon including precision stability and integrability drive their rapid adoption in high end research and diagnostic sectors fueling the segment’s fast growth. Advancements in microfabrication techniques such as deep reactive ion etching and laser ablation have significantly enhanced the performance of glass and silicon microfluidic devices. These techniques allow for the creation of complex three dimensional structures with sub micron precision enabling the development of highly sophisticated devices. This improvement makes glass and silicon devices more accessible for commercial applications beyond research laboratories. Additionally the integration of nanofluidic channels in silicon chips enables the manipulation of molecules at the nanoscale opening new possibilities for DNA sequencing and protein analysis. Furthermore the development of hybrid devices combining glass silicon and polymers leverages the strengths of each material offering optimized performance for specific applications. For instance hybrid chips are used in point of care diagnostics where the stability of glass is combined with the flexibility of polymers. These technological advancements expand the application scope of glass and silicon microfluidics driving their rapid growth. Therefore, the continuous improvement in fabrication technologies and the emergence of hybrid solutions propel the glass and silicon segment forward in the European market.

COUNTRY ANALYSIS

Germany Microfluidic Devices Market Analysis

Germany dominated the Europe microfluidic devices market and occupied a 22.7% share in 2025. This growth of the German market is attributed to its robust medical technology sector and strong emphasis on research and development. According to the Federal Ministry for Economic Affairs and Climate Action (BMWK), the medical technology and pharmaceutical sectors represent a massive component of the national economy, with microfluidic innovation serving as a primary driver for the next generation of diagnostic platforms. The presence of leading pharmaceutical companies and research institutions such as the Max Planck Society fosters a conducive environment for technological advancement. Germany is home to numerous startups specializing in lab on a chip technologies benefiting from extensive government funding and venture capital investment. The German Accelerator program supports these startups in scaling their operations and entering international markets. Furthermore the country’s well established healthcare infrastructure facilitates the rapid adoption of new diagnostic tools. Research confirms that while a small percentage of hospitals maintain large in-house laboratory facilities, the majority rely on a sophisticated network of external diagnostic providers for complex testing services. This widespread infrastructure supports the integration of microfluidic devices into routine clinical practice. Additionally, Germany’s strong export orientation enables local manufacturers to reach global markets enhancing their economies of scale. Therefore, the combination of industrial strength research excellence and healthcare infrastructure solidifies Germany’s position as the dominant player in the European microfluidic devices market.

United Kingdom Microfluidic Devices Market Analysis

The United Kingdom was second largest country in the Europe microfluidic devices market and accounted for a 18.5% share in 2025. The nation’s strong academic base and innovative healthcare system fuel the adoption of microfluidic technologies. UK Research and Innovation (UKRI) continues to serve as the government's primary engine for life sciences, investing heavily in cross-disciplinary programs that connect laboratory discovery to commercial diagnostic tools. The National Health Service plays a crucial role in facilitating the clinical validation and adoption of microfluidic devices. Initiatives such as the NHS Test and Learn program accelerate the integration of innovative technologies into patient care pathways. The UK is also a hub for biotechnology startups with clusters in Cambridge and Oxford leading the way in microfluidic innovation. Data from BioIndustry Association reveals that the UK biotech sector raised over 2 billion pounds in investment in 2023. This financial support enables companies to develop and commercialize novel microfluidic solutions. Furthermore the country’s regulatory framework governed by the Medicines and Healthcare products Regulatory Agency ensures high standards for device safety and efficacy. The post Brexit regulatory alignment with international standards facilitates market access for UK manufacturers. Additionally the growing prevalence of chronic diseases in the UK increases the demand for efficient diagnostic solutions. So, the synergy between academic excellence healthcare infrastructure and supportive policies maintains the United Kingdom’s strong position in the European market.

France Microfluidic Devices Market Analysis

France holds a noteworthy share of the Europe microfluidic devices market due to significant government initiatives aimed at strengthening the healthcare and biotechnology sectors. Under the France 2030 national health innovation strategy, the government provides expansive funding to accelerate biomedical research and enhance the global competitiveness of the French diagnostic sector. France is home to renowned research institutions such as the Pasteur Institute which are at the forefront of microfluidic research. The country’s strong pharmaceutical industry also contributes to the demand for microfluidic tools in drug discovery and development. Sanofi and other major pharmaceutical companies invest heavily in advanced analytical technologies to accelerate drug pipelines. Furthermore the French healthcare system is undergoing digital transformation with the introduction of the Mon Espace Santé platform facilitating the integration of digital health tools including microfluidic diagnostics. The French National Authority for Health (HAS) shows a growing clinical preference for point-of-care testing solutions, which streamline patient management by moving diagnostics closer to the site of care. This trend is supported by reimbursement policies that encourage the use of innovative diagnostic methods. Additionally France’s strategic location in Europe provides access to a broad customer base. Consequently the combination of government support industrial strength and healthcare modernization drives the growth of the microfluidic devices market in France.

Switzerland Microfluidic Devices Market Analysis

Switzerland is moving ahead steadfastly in the Europe microfluidic devices market owing to its reputation for high quality precision engineering and pharmaceutical excellence. The country is home to global pharmaceutical giants such as Roche and Novartis which are major users of microfluidic technologies for drug development and diagnostics. According to the Swiss Federal Statistical Office the pharmaceutical industry contributed over 50 billion Swiss francs to the national economy in 2023. These companies invest heavily in research and development leveraging microfluidics for high throughput screening and personalized medicine applications. Switzerland’s strong academic institutions such as ETH Zurich and EPFL are leaders in microfluidic research producing cutting edge innovations. The Swiss National Science Foundation provides substantial funding for interdisciplinary research projects involving microfluidics. Furthermore the country’s favorable regulatory environment and intellectual property protection attract international companies to establish research and development centers. This innovation ecosystem supports the development of high value microfluidic devices. Additionally the high standard of healthcare in Switzerland ensures early adoption of advanced diagnostic tools. Consequently the synergy between pharmaceutical industry strength academic excellence and supportive policies sustains Switzerland’s significant presence in the European microfluidic devices market.

Italy Microfluidic Devices Market Analysis

Italy is anticipated to expand significantly in the Europe microfluidic devices market from 2026 to 2034 due to a growing focus on healthcare modernization and research collaboration. The country’s market is driven by increasing investments in biomedical research and the expansion of diagnostic capabilities. The National Recovery and Resilience Plan (NRRP) serves as a vital funding source for Italian healthcare, with dedicated resources aimed at modernizing research infrastructure and digitalizing diagnostic services. This funding supports the acquisition of advanced diagnostic equipment including microfluidic systems. Italy has a strong tradition in mechanical engineering which facilitates the manufacturing of microfluidic components. Companies in the Lombardy and Emilia Romagna regions are increasingly involved in the production of precision medical devices. Furthermore the Italian National Health Service is implementing reforms to improve diagnostic efficiency and reduce waiting times. This trend drives the adoption of rapid and accurate microfluidic based solutions. Additionally collaborations between universities and industry partners foster innovation in microfluidic applications. For example the Polytechnic University of Milan collaborates with local companies to develop novel microfluidic chips for environmental monitoring. Consequently the combination of government investment industrial capability and healthcare reforms supports the steady growth of the microfluidic devices market in Italy.

COMPETITIVE LANDSCAPE

The competition in the Europe microfluidic devices market is characterized by intense rivalry among established multinational corporations and innovative startups. Leading companies leverage their extensive research and development capabilities to introduce advanced products that offer superior performance and reliability. The presence of numerous small and medium sized enterprises fosters a dynamic environment where niche innovations frequently emerge. These smaller entities often focus on specialized applications such as organ on a chip or single cell analysis differentiating themselves from broader diagnostic providers. Strategic alliances between technology developers and pharmaceutical companies are common as firms seek to integrate microfluidics into drug discovery pipelines. Regulatory compliance serves as a significant barrier to entry ensuring that only high quality products reach the market. Intellectual property protection plays a crucial role in maintaining competitive advantages with companies actively patenting novel fabrication techniques and device designs. Price competition is moderate as customers prioritize accuracy and speed over cost. However the push for cost effective solutions in public healthcare systems drives manufacturers to optimize production processes. The market witnesses continuous evolution as technological advancements reshape competitive dynamics and create new opportunities for growth and differentiation among participants.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe microfluidic devices market are

- Agilent Technologies

- PerkinElmer Inc.

- Danaher Corporation

- Bio Merieux SA

- Thermo Fisher Scientific Inc.

- Qiagen NV

- Bio-Rad Laboratories, Inc.

- Fluidigm Corporation

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd

- Horizon Microtechnologies

- Others

Top Players In The Market

- F Hoffmann La Roche Ltd stands as a pivotal entity in the European microfluidic landscape leveraging its extensive diagnostics portfolio to drive innovation. The company integrates advanced microfluidic technologies into its cobas systems enhancing the precision and speed of molecular testing. Recent strategic initiatives include the expansion of its manufacturing facilities in Germany to support increased demand for point of care diagnostic solutions. By focusing on personalized healthcare Roche utilizes microfluidics to enable rapid genetic analysis which is crucial for oncology and infectious disease management. Their commitment to research and development ensures continuous improvement in assay sensitivity and throughput. This approach solidifies their reputation as a leader in delivering high quality diagnostic tools that meet the stringent regulatory standards of the European market while addressing global healthcare challenges through technological excellence and operational efficiency.

- Danaher Corporation exerts significant influence in the Europe microfluidic devices market through its diverse life sciences and diagnostics subsidiaries including Beckman Coulter and Leica Biosystems. The company employs its renowned Danaher Business System to optimize operations and foster innovation across its portfolio. Recent actions involve the integration of artificial intelligence with microfluidic platforms to enhance data analysis capabilities in clinical settings. Danaher actively invests in expanding its production capacities in Ireland and the Netherlands to serve the growing European demand for automated laboratory solutions. Their focus on developing compact and efficient microfluidic instruments supports the trend towards decentralized testing. Danaher strengthens its competitive position through customer-centric innovation and strategic acquisitions. These efforts deliver comprehensive solutions that improve laboratory workflow efficiency and diagnostic accuracy for healthcare providers.

- Bio Merieux SA is a prominent French company specializing in in vitro diagnostics and microfluidic technologies for infectious disease detection. The company’s FilmArray system exemplifies its expertise in integrating microfluidics with multiplex polymerase chain reaction for rapid pathogen identification. Bio Merieux recently expanded its research and development center in Lyon to accelerate the development of next generation syndromic tests. Their strategic partnerships with European hospitals facilitate the clinical validation and adoption of their microfluidic solutions. The company focuses on reducing turnaround times for critical diagnostic results thereby improving patient outcomes in emergency settings. By emphasizing automation and ease of use Bio Merieux addresses the staffing shortages faced by many healthcare facilities. Their dedication to public health and continuous innovation ensures they remain a key contributor to the advancement of microfluidic diagnostics in Europe and globally.

Top Strategies Used By The Key Market Participants

Key players in the Europe microfluidic devices market predominantly employ strategic collaborations and partnerships to enhance their technological capabilities and market reach. Companies frequently engage in joint ventures with academic institutions to leverage cutting edge research and accelerate product development cycles. Mergers and acquisitions represent another vital strategy allowing firms to integrate complementary technologies and expand their product portfolios efficiently. Investment in research and development remains central to maintaining competitive advantage through continuous innovation in device design and functionality. Manufacturers also focus on expanding their production facilities within Europe to ensure supply chain resilience and comply with local regulatory requirements. Additionally companies are increasingly adopting digital health strategies by integrating internet of things connectivity into their devices. This approach enables remote monitoring and data analytics which adds value for healthcare providers. Marketing efforts emphasize the cost effectiveness and efficiency of microfluidic solutions to drive adoption in both hospital and point of care settings.

MARKET SEGMENTATION

This research report on the Europe microfluidic devices market is segmented and sub-segmented into the following categories.

By Device

- Chips

- Sensors

- Others

By Material

- Glass

- Silicon

- Polymer

- Others

By Application

- Pharmaceutical & Life Science Research

- Diagnosis & Treatment

- Others

By End-user

- Pharmaceutical and Biotechnology Companies

- Research Institutes

- Diagnostic Centers

- Healthcare Facilities and Others

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe microfluidic devices market?

Increasing demand for advanced diagnostics and lab-on-chip technologies is driving market growth.

Why are microfluidic devices gaining importance in healthcare and research?

They enable precise control and analysis of small fluid samples for faster results.

How would you explain microfluidic devices in simple terms?

They are miniaturized systems that manipulate tiny amounts of fluids for testing and analysis.

Where are microfluidic devices most commonly used across Europe?

They are widely used in medical diagnostics, pharmaceuticals, and research laboratories.

What makes microfluidic devices essential in modern scientific applications?

They improve efficiency, reduce sample usage, and enable rapid testing.

From a practical perspective, are microfluidic devices a valuable investment?

Yes, they enhance testing accuracy and reduce operational costs over time.

What challenges are affecting the Europe microfluidic devices market?

High development costs and technical complexity are key challenges.

How is healthcare demand influencing this market?

Growing need for rapid diagnostics and personalized medicine is boosting adoption.

Which application segments contribute the most to market demand?

Clinical diagnostics and pharmaceutical research are the leading segments.

Is the Europe microfluidic devices market growing steadily?

Yes, it is expanding with increasing adoption in healthcare and research sectors.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com