Europe Military Communications Market Size, Share, Trends & Growth Forecast Report, Segmented By Component, Hardware, Technology, Platform And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Military Communications Market Report Summary

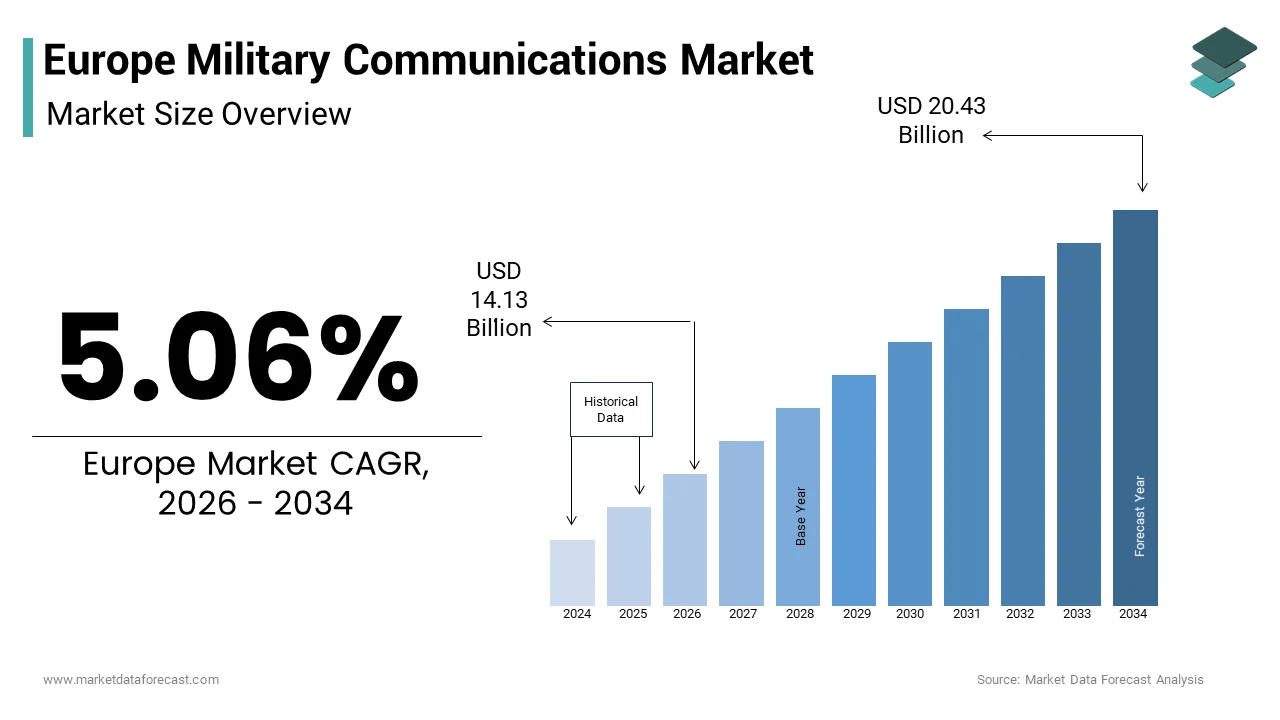

The Europe military communications market was valued at USD 13.45 billion in 2025, is estimated to reach USD 14.13 billion in 2026, and is projected to reach USD 20.43 billion by 2034, growing at a CAGR of 5.06% during the forecast period from 2026 to 2034. The growth of the Europe military communications market is driven by increasing defense modernization programs, rising geopolitical tensions, and the growing need for secure, real-time communication systems across military operations. The adoption of advanced communication technologies such as satellite communication (SATCOM), software-defined radios, and network-centric warfare systems is further accelerating market expansion. Additionally, the emphasis on interoperability among allied forces and the integration of AI-driven communication systems are strengthening the demand for next-generation military communication solutions across Europe.

Key Market Trends

- Rising adoption of satellite-based communication systems for secure and long-range connectivity.

- Increasing investments in defense modernization and digital battlefield technologies.

- Growing demand for secure, encrypted communication systems to counter cyber threats.

- Expansion of network-centric warfare and real-time data sharing capabilities.

- Integration of AI and advanced analytics to enhance communication efficiency and decision-making.

Segmental Insights

By Component

The hardware segment accounted for a significant share of the Europe military communications market in 2025. This is driven by the increasing deployment of advanced communication equipment, including radios, transceivers, and satellite systems.

By Hardware

The transceiver segment dominated the market, holding 38.4% of the Europe military communications hardware market share in 2025. Its leadership is attributed to its critical role in enabling reliable two-way communication across diverse military platforms.

By Technology

The SATCOM segment led the market with a 35.4% share in 2025. The growing reliance on satellite communication for secure, long-distance, and real-time data transmission in defense operations is a key factor supporting this dominance.

Regional Insights

The Europe military communications market is witnessing steady growth across major countries, supported by rising defense budgets and technological advancements in communication systems.

- Germany led the market, accounting for 22.8% of the total share in 2025, driven by strong defense investments and modernization initiatives.

- France ranked second with an 18.4% share, supported by advanced military infrastructure and ongoing defense programs.

- The United Kingdom is expected to witness the fastest growth, fueled by increasing investments in advanced communication technologies and defense digitization.

- Italy is experiencing growth due to its active participation in international missions, driving demand for reliable and interoperable communication systems.

- Spain is expected to present prominent growth opportunities, supported by defense upgrades and technological adoption.

Competitive Landscape

The Europe military communications market is highly competitive, with leading defense and technology companies focusing on innovation, secure communication solutions, and strategic collaborations. Companies are investing in advanced SATCOM systems, software-defined radios, and integrated communication networks to enhance operational efficiency and battlefield connectivity. Partnerships with defense agencies and governments, along with continuous R&D investments, are key strategies adopted by market players to strengthen their position in the market.

Prominent players in the Europe military communications market include ASELSAN, General Dynamics, Thales Group, Leonardo, Rohde & Schwarz, L3Harris Technologies, Viasat, Cobham, BAE Systems, Elbit Systems, Lockheed Martin, Northrop Grumman, and RTX Corporation.

Europe Military Communications Market Size

The Europe military communications market size was valued at USD 13.45 billion in 2025 and is anticipated to reach USD 14.13 billion in 2026 to reach USD 20.43 billion by 2034, growing at a CAGR of 5.06% during the forecast period from 2026 to 2034.

Introduction and Market Definition

The military communications are advanced systems and technologies designed to facilitate secure reliable and real time information exchange among defense forces across land sea and air domains. These systems include tactical radios satellite communication terminals data links and network centric warfare solutions that are critical for command and control operations. As per the European Defence Agency, total defense expenditure in the European Union reached 290 billion euros in 2024 reflecting a significant increase in investment capabilities. This financial commitment underscores the strategic priority placed on modernizing legacy infrastructure to counter evolving hybrid threats. According to the Stockholm International Peace Research Institute military spending in Western Europe increased by 13% in 2024 marking the highest annual growth rate in decades. The integration of artificial intelligence and cyber security measures into communication networks has become imperative to ensure data integrity against sophisticated electronic warfare tactics. Furthermore, the European Commission’s Permanent Structured Cooperation framework encourages collaborative development of defense technologies fostering a unified approach to communication standards. The transition from platform centric to network centric operations enables faster decision making and enhanced situational awareness which are vital for modern battlefield effectiveness.

MARKET DRIVERS

Escalating Geopolitical Tensions and Defense Modernization Initiatives

The intensifying geopolitical instability in Eastern Europe with the expansion of the military communications is substantially boosting the growth of Europe military communications market. Nations are urgently upgrading their command and control systems to ensure seamless coordination during joint military exercises and potential conflict scenarios. According to the North Atlantic Treaty Organization, allied European countries committed to increasing defense spending to 2% of their gross domestic product by 2024 with many exceeding this target. This surge in budget allocation directly translates into procurement of advanced tactical communication equipment, such as software defined radios and secure satellite terminals. The European Defence Agency reported that collaborative defense projects involving communication systems increased by 25% in 2025 indicating a strong trend towards interoperability. The conflict in Ukraine has highlighted the critical importance of resilient communication networks that can withstand electronic jamming and cyber-attacks. As per the German Federal Ministry of Defence, Berlin announced a special fund of 100 billion euros for armed forces modernization with a significant portion allocated to digital connectivity and communication infrastructure. Similarly, France and Poland have initiated multi year procurement programs to replace obsolete radio systems with next generation broadband tactical networks. These national efforts are complemented by joint initiatives under the European Union’s Strategic Compass which aims to enhance rapid response capabilities through improved communication interoperability.

Adoption of Network Centric Warfare and Interoperability Standards

The strategic shift towards network centric warfare doctrines necessitates the adoption of standardized and interoperable communication systems is also leveraging the growth of Europe military communications market. This approach relies on the seamless integration of sensors shooters and command centers to create a unified operational picture. According to the European Defence Fund, over 1.5 billion euros were allocated in 2024 for projects focused on enhancing digital interoperability and secure communications. The implementation of common standards such as the Joint Tactical Radio System ensures that equipment from different manufacturers and nations can communicate effectively during coalition operations. As per the United States European Command, joint exercises involving European allies increased by 30% in 2025 requiring robust and compatible communication infrastructure. The drive for interoperability is further supported by the North Atlantic Treaty Organization’s Federated Mission Networking framework which aims to connect mission networks across allied forces. This initiative requires substantial investment in gateway systems and encryption technologies to maintain security while enabling data sharing. The French Ministry of Armed Forces stated that its Scorpion program which integrates ground combat vehicles into a single network has accelerated the deployment of tactical communication nodes. Similarly, the British Army’s Morpheus program seeks to deliver a flexible and scalable communication system that supports diverse operational needs. These large scale modernization efforts create sustained demand for advanced communication solutions that can integrate legacy systems with new technologies ensuring continuity and effectiveness in complex multi domain operations.

MARKET RESTRAINTS

Complexity of Integrating Legacy Systems with Modern Technologies

The technical and financial complexity associated with integrating modern communication technologies with existing legacy systems is majorly restraining the growth of Europe military communications market. Many European defense forces operate a mix of outdated analog and early digital equipment that lacks the compatibility required for contemporary network centric operations. According to the European Court of Auditors approximately 40% of military equipment in EU member states is considered obsolete posing challenges for seamless integration. Upgrading these legacy systems often requires custom interfaces and extensive testing which increases project costs and timelines. The lack of standardized protocols across different generations of equipment further complicates the interoperability landscape leading to fragmented communication networks. Additionally, the scarcity of skilled personnel capable of managing hybrid systems exacerbates the issue as training requirements become more demanding. The Italian Ministry of Defence noted that workforce retraining programs for new communication technologies accounted for 10% of the total modernization budget in 2025. These factors collectively hinder the rapid adoption of advanced communication solutions as organizations struggle to balance the need for modernization with the constraints of existing infrastructure. The risk of operational disruptions during the transition phase also makes decision makers cautious about implementing sweeping changes too quickly.

Stringent Regulatory Compliance and Security Certification Processes

The rigorous regulatory environment and stringent security certification processes on the speed of innovation and deployment in the military communications sector, which is also degrading the growth of Europe military communications market. Equipment used by defense forces must meet exacting standards for electromagnetic compatibility encryption and resistance to electronic warfare threats. According to the European Union Agency for Cybersecurity, the certification process for critical defense communication components can take up to 24 months delaying market entry for new technologies. This prolonged timeline increases development costs and reduces the competitiveness of smaller innovators who lack the resources to navigate complex bureaucratic hurdles. As per the French General Directorate for Armament, new communication systems must undergo multiple layers of validation including national and North Atlantic Treaty Organization approvals which can extend project durations by several years. The diversity of national regulations across European countries further fragments the market requiring manufacturers to obtain separate certifications for each country. This fragmentation limits economies of scale and discourages cross border collaboration. Moreover, the rapid evolution of cyber threats necessitates frequent updates to security protocols requiring continuous recertification of systems. These regulatory burdens create barriers to entry and slow down the adoption of cutting-edge communication technologies thereby restraining market growth and innovation momentum.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Cognitive Radio Technologies

The integration of artificial intelligence and cognitive radio technologies for enhancing the efficiency and resilience of communication networks is certainly to pose new opportunities for the growth of Europe military communications market. Cognitive radios can dynamically adjust their transmission parameters to avoid interference and jamming ensuring reliable connectivity in contested environments. These smart systems can analyze spectrum usage in real time and switch frequencies automatically to maintain optimal performance. The ability of cognitive radios to learn from environmental conditions and adapt accordingly reduces the workload on operators and enhances situational awareness. Furthermore, the use of machine learning algorithms for predictive maintenance of communication equipment minimizes downtime and extends asset lifespan. The United Kingdom Ministry of Defence launched an initiative in 2025 to incorporate AI enabled communication nodes into its future integrated operating concept. This technology enables faster decision making by providing commanders with accurate and timely information despite adversarial attempts to disrupt communications. The growing sophistication of electronic threats makes the adoption of intelligent communication systems not just an opportunity but a necessity for maintaining operational superiority in modern warfare.

Expansion of Satellite Communication Capabilities for Global Reach

The expansion of satellite communication capabilities by enabling global reach and beyond line of sight connectivity is another attribute elevating the growth of Europe military communications market. As military operations become increasingly expeditionary, the demand for secure and high bandwidth satellite links grows. According to the European Space Agency the development of government owned secure satellite constellations such as IRIS2 is expected to provide enhanced communication services for defense users by 2027. This initiative aims to reduce dependence on commercial providers and ensure sovereign access to communication infrastructure. As per the French National Centre for Space Studies, investments in military satellite communication technologies reached 800 million euros in 2024 supporting the development of anti-jamming and encrypted terminals. The integration of low earth orbit satellites with traditional geostationary systems offers lower latency and higher data rates which are essential for real time video transmission and drone operations. The North Atlantic Treaty Organization has also emphasized the importance of space based communications in its new space policy framework encouraging member states to invest in resilient satellite networks. Companies are developing compact and portable satellite terminals that can be rapidly deployed by special forces and remote units. This flexibility enhances operational versatility and ensures that troops remain connected even in the most challenging terrains.

MARKET CHALLENGES

Vulnerability to Advanced Electronic Warfare and Cyber Threats

The increasing vulnerability of communication networks to advanced electronic warfare and cyber threats is key challenge for the growth of Europe military communication market. Adversaries are employing sophisticated jamming spoofing and hacking techniques to disrupt command and control links compromising mission success. Protecting communication systems against these threats requires continuous investment in encryption frequency hopping and anti-jamming technologies which adds to the complexity and cost of equipment. As per the research, cyber attacks on defense networks have become more frequent and targeted necessitating robust defensive measures. The rapid evolution of threat vectors means that communication systems must be constantly updated to remain secure creating a perpetual cycle of development and deployment. The Polish Ministry of National Defence reported that electronic warfare simulations revealed significant gaps in the resilience of legacy radio systems against modern jamming techniques. Furthermore, the reliance on commercial satellite services introduces additional vulnerabilities as these networks may not meet the same security standards as dedicated military systems. Ensuring end to end security across heterogeneous networks remains a daunting task requiring close collaboration between government agencies and private sector partners.

Supply Chain Disruptions and Dependence on Foreign Components

The supply chain disruptions and dependence on foreign components for communication hardware is additional factor degrading the growth of Europe military communications market. Many European defense manufacturers rely on semiconductors and specialized electronic components sourced from outside the region particularly from Asia and North America. The dependency creates strategic vulnerabilities as geopolitical tensions can disrupt the flow of essential materials. As per the German Association of the Aerospace Industry, lead times for critical electronic components extended by an average of 6 months in 2025 impacting the delivery schedules of communication systems. The European Union has recognized this issue and launched the European Chips Act to boost domestic production but full self-sufficiency remains years away. In the interim manufacturers face difficulties in securing reliable supplies of high-performance processors and memory chips required for advanced communication devices. The French Ministry of Economy indicated that diversifying supply chains has become a top priority but transitioning to new suppliers involves lengthy qualification processes. Additionally, the cost of reshoring production facilities is prohibitive for many companies limiting their ability to mitigate risks. These supply chain constraints hinder the ability of European defense firms to respond quickly to urgent procurement requests and maintain steady production rates thereby challenging market stability and growth prospects.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.06% |

| Segments Covered | By Component, Hardware, Technology, Platform, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | ASELSAN A.S. (Turkiye), General Dynamics Corporation (U.S.), Thales Group, Leonardo S.p.A., Rohde and Schwarz, L3Harris Technologies, Inc. (U.S.), Viasat Inc (U.S.), Cobham PLC (U.K.), BAE Systems PLC (U.K.), Elbit Systems Ltd. (Israel), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), RTX Corporation (U.S.) |

SEGMENTAL ANALYSIS

By Component Insights

The hardware segment was accounted in holding a significant share of the Europe military communications market in 2025 owing to the high capital expenditure required for procuring physical infrastructure such as radios antennas and satellite terminals which form the backbone of defense networks.

Requirement for Robust Physical Infrastructure in Tactical Operations

The necessity for durable and reliable physical communication equipment in harsh tactical environments drives the dominance of the hardware segment. Military operations often take place in extreme weather conditions and contested terrains where equipment must withstand shock vibration and electromagnetic interference. The physical robustness of hardware ensures uninterrupted command and control capabilities, which are important for mission success. These devices are essential for frontline troops who require immediate and secure voice and data connectivity. The lifecycle of hardware components typically spans several years requiring significant upfront investment but offering long term operational stability. Furthermore, the integration of advanced encryption modules into hardware units enhances security against interception and jamming. The tangible performance boost reinforces the preference for high quality hardware solutions. Additionally, the modular design of modern hardware allows for easier upgrades and maintenance reducing long term logistical burdens. The continuous need to equip expanding military forces with standardized hardware ensures sustained demand in this segment.

The software segment is esteemed to witness a fastest CAGR of 9.8% from 2026 to 2034. The shift towards software defined radios and networks is a primary driver for the rapid growth of the software segment. These technologies allow for flexible and reconfigurable communication systems that can adapt to changing operational requirements without hardware modifications. Software defined systems enable the integration of multiple waveforms and protocols into a single device reducing the need for diverse hardware inventory. Furthermore, software updates can be deployed remotely to address security vulnerabilities or add new features extending the lifespan of existing hardware. The ability to dynamically allocate bandwidth and prioritize critical traffic ensures optimal performance in congested spectrum environments. This adaptability is crucial for modern warfare where information superiority depends on rapid and reliable data exchange. The growing complexity of electronic warfare threats also necessitates intelligent software algorithms that can detect and counter jamming attempts in real time.

By Hardware Insights

The transceiver segment was the largest by holding 38.4% of the Europe military communications hardware market share in 2025. Transceivers play an important role in facilitating tactical voice and data communication for ground air and naval forces. Their ability to operate across various frequency bands and support multiple waveforms makes them versatile tools for diverse military applications. The high demand is driven by the need for reliable communication links in dynamic battlefield environments. These devices enable seamless communication between different branches of the military and coalition partners. The miniaturization of transceiver technology has also led to the development of lightweight handheld units that enhance soldier mobility. The ergonomic improvement contributes to better operational endurance and effectiveness. Furthermore, modern transceivers incorporate advanced signal processing capabilities that enhance clarity and range even in noisy or jammed environments. The integration of GPS and navigation features into transceivers further adds to their utility by providing situational awareness.

The antenna segment is likely to expand at an anticipated CAGR of 8.5% from 2026 to 2034 with the growing reliance on satellite communications for beyond line of sight connectivity drives the rapid growth of the antenna segment. High bandwidth data transmission requires specialized antennas capable of maintaining stable links with satellites in geostationary and low earth orbits. These antennas are essential for real time video streaming drone control and large file transfers. As per the French National Centre for Space Studies, the development of phased array antennas for military use received 200 million euros in funding in 2025. Phased array antennas offer electronic steering capabilities that allow for rapid tracking of moving satellites without mechanical movement. This feature enhances reliability and reduces maintenance requirements. These antennas are also resistant to harsh marine environments ensuring consistent performance. The miniaturization of antenna technology has enabled their integration into unmanned aerial vehicles and portable soldier systems.

By Technology Insights

The SATCOM segment was the largest by holding 35.4% of the Europe military communications market share in 2025. SATCOM offers unparalleled global reach and beyond line of sight connectivity which are critical for expeditionary military operations. According to the North Atlantic Treaty Organization, satellite communication usage in joint operations increased by 20% in 2024 due to its reliability in remote areas. This capability is vital for coordinating forces deployed in diverse theaters such as Africa and the Middle East. Satellites enable real time data exchange between headquarters and frontline units ensuring informed decision making. The high bandwidth capacity of modern satellites supports video conferencing intelligence sharing and remote medical consultations. The United Kingdom Ministry of Defence reported that SATCOM links facilitated 5000 hours of video teleconferences in 2024 enhancing strategic coordination. Furthermore, satellite systems are resilient to terrestrial disruptions such as natural disasters or infrastructure damage. The German Federal Ministry of Defence noted that SATCOM remained operational during recent flood relief missions when ground networks failed.

The data link segment is projected to register a fastest CAGR of 10.2% from 2026 to 2034. The imperative for real time data exchange in network centric warfare doctrines fuels the rapid growth of the data link segment. Data links enable the seamless sharing of target information situational awareness and command instructions among diverse military assets. According to the European Defence Fund funding for data link interoperability projects increased by 28% in 2024. This investment aims to create a unified operational picture that enhances decision making speed and accuracy. The rapid exchange of information allows for coordinated attacks and defensive maneuvers is elevating the growth of the segment. Furthermore, data links support the operation of unmanned systems by providing continuous control and telemetry streams. The French Ministry of Armed Forces stated that data links were essential for the successful deployment of swarm drones in recent exercises. The ability to coordinate multiple autonomous units relies heavily on robust and low latency data links. As military operations become more complex and distributed the demand for efficient data exchange mechanisms continues to rise. This strategic importance drives the accelerated adoption of advanced data link technologies across European defense forces.

COUNTRY LEVEL ANALYSIS

Germany Military Communications Market Analysis

Germany was the largest contributor in the Europe military communications market by holding 22.8% of share in 2025 with the presence of industrial base and significant defense budget drive the adoption of advanced communication technologies. The presence of major technology providers such as Rohde and Schwarz fosters innovation and local supply chain resilience. The country’s participation in North Atlantic Treaty Organization initiatives promotes interoperability and joint procurement projects. This focus on technological advancement ensures that Germany remains at the forefront of military communication developments. The integration of artificial intelligence into communication networks is also a priority aimed at enhancing operational efficiency. The strong emphasis on cybersecurity further drives demand for encrypted communication solutions.

France Military Communications Market Analysis

France military communications market was ranked second by holding 18.4% of share in 2025. The country’s independent defense strategy and significant investments in sovereign capabilities fuel market growth. This long term commitment ensures steady demand for advanced tactical networks and satellite terminals. As per the French Directorate General of Armaments, procurement of secure communication equipment increased by 10% in 2024. The presence of major aerospace and defense companies such as Thales and Airbus drives innovation and export opportunities. The country’s focus on strategic autonomy encourages the development of indigenous communication technologies. This support for space based infrastructure enhances global connectivity for French forces. Furthermore, the integration of communication systems into the Scorpion combat vehicle program demonstrates the emphasis on network centric warfare. The strong research and development ecosystem supported by government grants fosters continuous technological improvements. These strategic initiatives and industrial capabilities maintain France’s strong position in the European market.

United Kingdom Military Communications Market Analysis

The United Kingdom military communications market growth is expected to witness a fastest CAGR in coming years with the modernization programs and focus on integrated operating concepts drive demand for advanced communication solutions. According to the United Kingdom Ministry of Defence, the Morpheus program aims to deliver a unified communication system for the armed forces by 2026. This initiative involves the replacement of legacy radios with software defined equivalents enhancing interoperability and security. The country’s participation in Five Eyes intelligence sharing agreements necessitates high security communication standards. The Defence Science and Technology Laboratory reported that research into quantum communication technologies received 20 million pounds in funding in 2025. This investment positions the UK as a leader in next generation secure communications. Furthermore, the Royal Navy’s investment in satellite communication terminals for its carrier strike group enhances global operational capabilities. The strong presence of defense contractors such as BAE Systems and Leonardo supports the development of customized solutions. The government’s focus on cyber resilience also drives the adoption of encrypted communication networks.

Italy Military Communications Market Analysis

Italy military communications market growth is likely to be driven by the efforts and participation in international missions drive the demand for reliable communication equipment. As per the Italian Aerospace Industry Association, exports of defense electronics increased by 8% in 2024 reflecting strong industrial performance. The presence of companies such as Leonardo and Elettronica fosters local innovation and production. The country’s involvement in North Atlantic Treaty Organization missions requires interoperable communication systems enhancing market demand. The Italian National Research Council reported that projects on cognitive radio technologies received 30 million euros in funding in 2025. This research aims to improve spectrum efficiency and resistance to jamming. Furthermore, the modernization of naval communication systems for the aircraft carrier Cavour enhances maritime operational capabilities. The government’s focus on digital transformation in defense encourages the adoption of software defined networks.

Spain Military Communications Market Analysis

Spain military communications market growth is esteemed to have a prominent growth opportunities with the defense modernization plans and participation in European defense initiatives drive market growth. The plan aims to enhance interoperability with allied nations and improve operational effectiveness. The presence of companies, such as Indra Sistemas drives local development and production of communication equipment. The country’s focus on cybersecurity encourages the adoption of encrypted communication solutions. Furthermore, the modernization of air traffic control systems for military airports enhances operational efficiency. The government’s participation in the European Defence Fund supports collaborative projects on communication technologies. These strategic investments and industrial capabilities sustain Spain’s position in the regional market.

COMPETITIVE LANDSCAPE

The competition in the Europe military communications market is characterized by intense rivalry among established defense giants and specialized technology firms. Major players compete on the basis of technological innovation security features and interoperability capabilities. The market is highly consolidated with a few dominant companies holding significant influence due to their extensive research and development resources and long standing relationships with government entities. New entrants face high barriers to entry including stringent security certifications and substantial capital requirements. Competitive dynamics are shaped by the need for continuous innovation to counter emerging electronic warfare threats and cyber attacks. Companies strive to differentiate themselves through unique value propositions such as advanced encryption algorithms and software defined architectures. Strategic alliances and joint ventures are prevalent as firms seek to share costs and expertise in developing complex communication systems. Price competition is secondary to performance and reliability given the critical nature of military applications. The focus on sovereign capabilities and local production further intensifies competition among European manufacturers.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe military communications market are

- ASELSAN A.S. (Turkiye)

- General Dynamics Corporation (U.S.)

- Thales Group

- Leonardo S.p.A.

- Rohde and Schwarz

- L3Harris Technologies, Inc. (U.S.)

- Viasat Inc (U.S.)

- Cobham PLC (U.K.)

- BAE Systems PLC (U.K.)

- Elbit Systems Ltd. (Israel)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- RTX Corporation (U.S.)

Top Players In The Market

- Thales Group stands as a pivotal leader in the Europe military communications market providing advanced secure communication systems for defense forces globally. The company specializes in tactical radios satellite terminals and network centric warfare solutions that ensure reliable connectivity in contested environments. Thales contributes significantly to the global market by leveraging its extensive research and development capabilities to innovate cryptographic technologies. Recent actions include the launch of new software defined radio platforms that enhance interoperability among allied nations. The firm actively collaborates with European defense agencies to develop sovereign communication capabilities reducing dependence on non European suppliers. Thales also invests in artificial intelligence driven cyber security measures to protect military networks from evolving threats. These strategic initiatives strengthen its position as a trusted partner for governments seeking robust and secure communication infrastructure.

- Leonardo S.p.A. is a major contributor to the Europe military communications market offering comprehensive solutions for tactical and strategic communication needs. The company provides advanced radar systems electronic warfare tools and secure data links that are integral to modern defense operations. Leonardo plays a crucial role in the global market by exporting high quality communication equipment to various international clients. Recent efforts to strengthen its market position include the development of next generation satellite communication terminals with enhanced anti jamming capabilities. The company focuses on integrating artificial intelligence into its communication systems to improve situational awareness and decision-making speeds. Leonardo also engages in joint ventures with other European defense contractors to foster collaboration and share technological expertise. These partnerships enable the creation of standardized communication protocols that facilitate seamless interoperability during multinational missions.

- Rohde and Schwarz is a key player in the Europe military communications market renowned for its high performance test and measurement equipment and secure communication systems. The company offers a wide range of tactical radios and network infrastructure solutions that meet the rigorous demands of military applications. Rohde and Schwarz contributes to the global market by providing reliable and durable communication technologies that operate effectively in harsh environments. Recent actions to bolster its market presence include the introduction of advanced software defined radio systems that support multiple waveforms and encryption standards. The company emphasizes cybersecurity by developing robust encryption modules that protect sensitive military data from interception. Rohde and Schwarz also invests heavily in research and development to stay ahead of technological advancements in the defense sector. Its commitment to quality and innovation has earned it a reputation as a preferred supplier for many European governments.

Top Strategies Used By The Key Market Participants

Key players in the Europe military communications market primarily focus on innovation through research and development to create advanced secure and interoperable communication systems. Companies invest heavily in software defined technologies that allow for flexible and upgradable hardware configurations. Strategic partnerships and collaborations with government agencies and other defense contractors are common to develop standardized protocols and enhance interoperability among allied forces. Expansion into emerging markets and diversification of product portfolios help firms mitigate risks and capture new opportunities. Cybersecurity remains a central strategy with significant investments in encryption and anti-jamming technologies to protect against evolving threats. Mergers and acquisitions are utilized to acquire specialized technologies and expand geographic reach. Additionally, companies emphasize sustainability by developing energy efficient communication equipment that aligns with environmental regulations. These strategies enable market participants to maintain competitive advantages and meet the complex requirements of modern military operations effectively.

MARKET SEGMENTATION

This research report on the Europe military communications market is segmented and sub-segmented into the following categories.

By Component

- Hardware

- Software

By Hardware

- Transceiver

- Antenna

- Transmitter

- Receiver

- Others

By Technology

- SATCOM

- VHF/UHF/L-Band

- HF Communication

- Data Link

By Platform

- Airborne

- Ground

- Naval

- Space

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe military communications market?

Increasing defense modernization and need for secure communication systems are driving growth.

Why are advanced communication systems important for military operations in Europe?

They ensure secure, reliable, and real-time information exchange in critical situations.

How would you explain military communication systems in simple terms?

They are technologies used by armed forces to transmit information securely across operations.

Where are military communication systems most commonly used across Europe?

They are widely used in land forces, naval operations, air defense, and command centers.

What makes military communications essential in modern defense strategies?

They enable coordination, situational awareness, and mission success.

From a defense perspective, are communication systems a critical investment?

Yes, they are vital for operational efficiency and national security.

What challenges are affecting the Europe military communications market?

High development costs and cybersecurity threats are key challenges.

How is geopolitical tension influencing this market?

Rising security concerns are increasing defense spending on communication technologies.

Which segments contribute the most to market demand?

Secure radio systems, satellite communication, and network solutions are major contributors.

Is the Europe military communications market growing steadily?

Yes, it is expanding with continuous defense upgrades and modernization programs.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com