Europe Online Travel Market Size, Share, Trends & Growth Forecast Report By Service Type, By Booking Type, By Platform, and By Country (Germany, United Kingdom, France, Italy, Spain, Netherlands, Sweden & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Online Travel Market Size

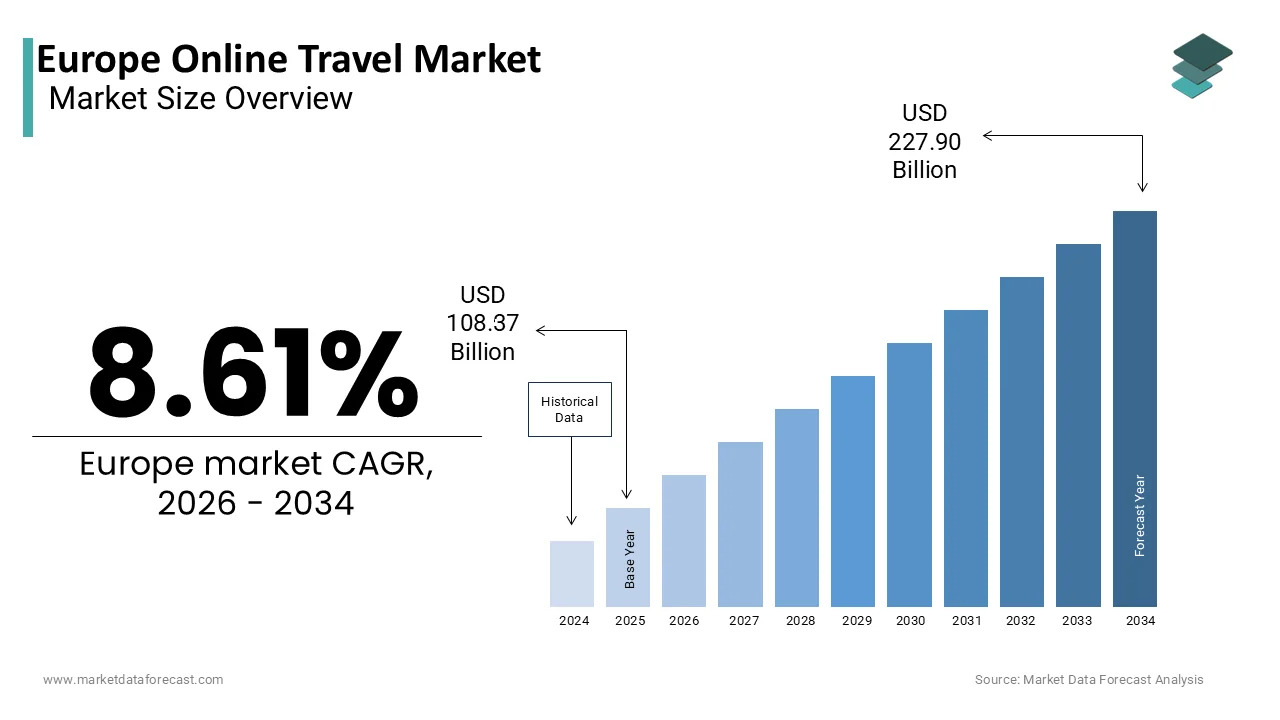

The Europe online travel market was valued at USD 108.37 billion in 2025, is estimated to reach USD 117.70 billion in 2026, and is projected to reach USD 227.90 billion by 2034, growing at a CAGR of 8.61% from 2026 to 2034.

Online travel refers to the digital marketplace where consumers search, compare, and book travel services, such as flights, hotels, car rentals, and vacation packages, directly via the internet. These platforms, known as Online Travel Agencies (OTAs), act as intermediaries connecting travelers with suppliers, offering competitive rates, user reviews, and instant booking confirmation. This sector has evolved from simple static booking engines to dynamic artificial intelligence-driven interfaces that offer personalized itineraries and real-time price optimization. The fundamental shift in consumer behavior toward mobile-first planning defines the current landscape as traditional high street travel agencies continue to lose footfall to digital convenience. According to multiple studies, online platforms, including Airbnb, Booking, and Expedia, are experiencing record-breaking growth in the European Union, with millions of guest nights booked annually. The European Union is experiencing rapid expansion in fixed, very high-capacity networks, with a significant majority of households now having access to high-speed internet. Smartphone usage remains a critical component, with mobile devices accounting for a significant share of all online travel searches among adults. The regulatory environment shaped by the Package Travel Directive influences how operators bundle services and protect consumer funds, making compliance a central operational requirement. This market functions as the primary revenue channel for airlines and hoteliers while enabling small local experience providers to reach global customers without significant marketing expenditure.

MARKET DRIVERS

Ubiquitous Smartphone Penetration Fuels Mobile Booking Adoption

The widespread presence of smartphones gives a boost to the surge in online travel transactions across the region, and thereby fuels the growth of theEuropeane online education market. Consumers increasingly rely on mobile devices for instant access to flight deals, hotel comparisons, and last-minute bookings, which drives unprecedented engagement levels. According to research, European mobile market saturation is high, with the vast majority of the population owning at least one mobile subscription, and growth is driven primarily by IoT connections rather than new unique subscribers. This ubiquity ensures that travel providers can reach users at any moment throughout their journey,y thereby increasing conversion rates significantly. The rollout of fifth-generation networks has further accelerated this trend by enabling high-definition virtual reality tours of hotel rooms and destinations directly within mobile applications without latency issues. A study indicates that fifth-generation coverage now extends to more than sixty percent of the European population, facilitating seamless streaming experiences. Providers specifically capitalize on this connectivity through location-based services that offer relevant recommendations when users are near airports or tourist attractions. The shift is evident in revenue figures, where mobile bookings often account for over fifty percent of total online turnover for major operators. Mobile commerce volumes continue to climb. As a result, the dependency on mobile-optimized interfaces is becoming absolute for business survival. This structural change in device usage patterns guarantees that mobile will remain the dominant channel for travel investment in the foreseeable future.

Rising Disposable Income and Leisure Travel Propensity

Major European economies are seeing a steady recovery in household disposable income, which further propels the expansion of theEuropeane online travel market. As a result, more money is being allocated to leisure and experiential travel. Individuals are prioritizing holidays and cultural experiences as economic stability returns following inflationary pressure. This trend has led to robust demand for online booking platforms. Real income in the Eurozone has begun to recover from the inflation-driven dip, leading to a moderate, though not highly rapid, recovery in household purchasing power and consumer spending. This migration of funds toward experiences necessitates continuous visibility on search engines and social media, where consumers begin their discovery journeys. Brands utilize targeted advertising and dynamic packaging to capture intent-driven traffic, which offers measurable returns on investment compared to traditional broadcast media. The rise of experiential tourism within the single market further intensifies competition as companies target customers seeking unique local activities beyond standard sightseeing. European travelers continue to prioritize leisure travel, showing strong resilience in consumer sentiment despite economic uncertainties. This cross-border dynamic encourages advertisers to adopt multilingualand culturally nuanced marketing strategies to resonate with diverse audiences. The need for real-time analytics to optimize ad spend ensures that marketing budgets remain fluid and responsive to market fluctuations. Consequently, the health of the online travel market is inextricably linked to the vitality of the regional economic ecosystem.

MARKET RESTRAINTS

Stringent Data Privacy Regulations Limit Personalization Capabilities

The implementation of rigorous data protection laws is a major hurdle for the European online travel market. It limits the ability of travel operators to track user behavior and deliver highly personalized offers. The General Data Protection Regulation, along with national implementation,s has fundamentally altered the data landscape, pe forcing companies to obtain explicit consent before collecting personal information. As per the European Data Protection Board, and supervisory authorities issued fines totaling over one point two billion euros in 2024, with a large portion related to improper data handling by technology and travel firms. This regulatory pressure has led to the deprecation of third-party cookies, which were historically the backbone of programmatic advertising and audience segmentation in the travel sector. Major browser providers have followed suit by blocking trackers by default, which reduces the pool of identifiable users available for targeting. A study found that the design of cookie banners significantly impacts user tracking consent, with compliant banners reducing acceptance rates compared to non-compliant, coercive banners. Operators now face higher costs to acquire first-party data and must invest in contextual advertising, which is often less precise than behavioral targeting. The fragmentation of consent mechanisms across different member states adds complexity for pan-European campaigns, requiring legal teams to constantly monitor compliance. These constraints reduce the overall efficiency of marketing spend and limit the granularity of customer insights available to marketers. The industry continues to grapple with balancing effective monetization against the fundamental right to privacy mandated by European law.

Economic Volatility and Inflation Pressures Discretionary Spending

High inflation and economic uncertainty are common across many European countries, which in turn hamper the expansion of theEuropeane online travel market. These pressures are leading consumers to look closer at their travel budgets and often spend less. When consumer confidence wanes due to rising living costs, households prioritize essential operations over discretionary spending, such as international holidays and luxury getaways. Persistent inflation in the service sector continued to put pressure on household purchasing power and discretionary spending in the Eurozone during 2024. This financial strain leads travelers to cut trip frequencies or shift focus entirely to budget options, abandoning long-haul or premium travel investments. Small and medium-sized enterprises, which form the bulk of the European hospitality fabric, are particularly vulnerable and may see booking volumes stagnate or decline during downturns. Rising energy prices and increased operational costs continue to impact consumer spending behavior and travel budgets across Europe. The volatility makes it difficult fo, tr,avel platforms to forecast revenue and plan inventory investments effectively. Travelers demand lower prices and flexible cancellation policies, which compress margins for airlines and hotels. Furthermore, the fluctuating exchange rates between the euro and other major currencies impact the affordability of outbound travel for European residents. This macroeconomic headwind creates a cautious environment where booking growth stagnates or contracts despite the underlying desire to travel.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Enhances Personalization

The rapid adoption of artificial intelligence and machine learning presents a lucrative opportunity for travel providers within the European online travel market. They can now deliver hyper-personalized booking experiences that drive customer loyalty and lifetime value. Since users expect tailored recommendations, operators must adapt. They can do this by using AI algorithms to analyze browsing patterns and suggest relevant destinations in real time. Large EU enterprises are increasingly adopting AI technologies for text analysis and operational efficiency, with adoption rates surpassing half of all large firms, particularly in the information and communication sector. This transition allows brands to create dynamic pricing models and personalized offers that resonate with individual user behaviors, significantly improving conversion rates. The ability to predict churn and intervene with targeted retention offers enhances the relevance of communications and improves customer satisfaction scores. European travel firms are increasing their investment in AI-driven tools to enhance personalized customer recommendations and improve operational efficiency, driven by the need to optimize customer journeys. Providers are increasingly allocating portions of their technology budgets to these digital channels to capture deeper insights into traveler preferences. The format supports chatbot integration that provides instant customer service and itinerary adjustments, ts bridging the gap between planning and execution. More sophisticated algorithms are lowering the barrier to entry for high-performance marketing. Now, smaller players can effectively compete with established giants. This technological leap ensures that the European market remains at the forefront of travel innovation in driving efficiency and effectiveness across all verticals.

Expansion of Sustainable and Eco-Conscious Travel Options

Growing demand for sustainable travel offers big potential for the European online travel market. Online platforms can leverage this shift to differentiate their brand and attract conscientious travelers. These initiatives enable providers to highlight eco-friendly accommodations and low-carbon transport options,s predicting outcomes and automating filtering without human intervention. A growing majority of European travelers express a desire to make more sustainable travel choices, yet this intention is often moderated by price sensitivity, with a significant portion willing to pay only a limited premium. Generative data models allow for the creation of verified green labels tailored to specific criteria, such as energy efficiency and waste reduction, to ensure that each user sees the most relevant ethical options possible. This level of transparency was previously unattainable at scale and significantly boosts booking frequency among environmentally aware demographics while reducing idle time between searches. Predictive analytics help operators anticipate market trends and adjust their inventory proactively rather than reacting to historical data. The technology also improves fraud detection by identifying green claims more accurately, thereby protecting brand integrity and revenue. Natural language processing facilitates better sentiment analysis, allowing companies to gauge public perception and refine their sustainability messaging accordingly. As regulatory pressure for green reporting increases, the barrier to entry for compliant operators lowers, rs enabling responsible businesses to thrive. This technological leap ensures that the European market remains at the forefront of sustainable tourism, driving efficiency and ethics across all verticals.

MARKET CHALLENGES

Fragmentation of Regulatory Landscapes Complicate,s Operations

The European regulatory landscape is highly fragmented, which inhibits the growth of the European online travel market. This poses a significant challenge for operators attempting to maintain compliance and operate efficiently across multiple borders. The continent comprises numerous distinct legal frameworks, cultures, and enforcement mechanisms, sms whnecessitateates localized strategies that complicate unified reporting and analysis. According to the European Travel Agents and Tour Operators Association, the existence of dozens of distinct national markets with varying consumer protection laws and tax regimes makesnecessitatet to establish standardized key performance indicators. Operators often struggle with data silos where information from different platforms a, nd countries does not integrate seamlessly, leading to incomplete pictures of customer journeys. The lack of a single super app or portal means that user attention is scattered across countless websites and applications,ons diluting the impact of broad campaigns. Cross-border payment processing remains problematic, especially with the rise of anti-money laundering directives that limit transaction flows between regulated and unregulated markets. Industry leaders are increasingly concerne,,d that uncoordinated regional policy shifts and new levies could undermine the long-term economic contributions of the travel sector. This fragmentation increases the cost and complexity of running pan-European campaigns, requiring specialized local knowledge and multiple technology stacks. The inability to attribute sales to specific touchpoints accurately undermines confidence in digital channels and hampers strategic decision-making. Overcoming this disjointed ecosystem requires su,,bstantial investment in data integration tools and harmonized measurement frameworks.

Intensifying Competition for Digital Attention Elevates Costs

The digital space is now saturated with an ever-increasing number of travel providers, which holds back the expansion of the European online travel market. This creates intense competition for limited user attention and drives up inventory costs significantly. As more brands vie for the same travelers on popular platforms, the auction dynamics of programmatic advertising result in inflated cost per click and cost per impression rates. Digital marketing spend in the travel industry is expanding as brands leverage major global events to capture heightened consumer demand. This bidding wa,,r disproportionately affects small anmedium-sizeded enterprises that lack the deep pockets of multinational corporations to sustain high acquisition costs. The sheer volume of ads displayed to consumers daily leads to banner blindness, where users subconsciously ignore promotional content,t reducing overall effectiveness. Platforms continuously update their algorithms to prioritize paid content over organic reach, ch forcing brands to spend more just to maintain visibility. The competition extends beyond traditional sectors as industries previously slow to adopt digital marketing now flood the space, adding to the congestion. Attention spans are shrinking. Media consumption is shifting toward rapid, "snackable" formats as digital audiences become more selective in their initial engagement with content. Advertisers must therefore invest morhigh-qualityality creative production to break through the noise, which further escalates campaign budgets. This relentless upward pressure on costs threatens the sustainability of customer acquisition models for many digital native travel businesses.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Service Type, Booking Type, Platform, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Booking Holdings, Inc., Expedia Group, Inc., Trip.com Group Limited, eDreams ODIGEO, lastminute.com Group, Airbnb, Inc., Trivago N.V., Skyscanner Ltd., Trainline PLC, TUI Group, HRS Group, Flix SE, Hostelworld Group PLC, Amadeus IT Group SA, Sabre Corporation, Travelport Worldwide Ltd. |

SEGMENTAL ANALYSIS

By Service Type Insights

The travel accommodation segment led the European online travel market and occupied a 42.7% share in 2025. The leading position of the segment is attributed to the fundamental necessity of lodging for any trip, regardless of purpose or duration, which creates a consistent and high-volume demand stream. Following that, this segment is pushed by the explosive growth of the alternative accommodation sector,r including vacation rentals and home sharing platforms, ms which have diversified inventory beyond traditional hotels. European travelers are increasingly shifting toward digital platforms for short-stay arrangements, driven by the convenience of integrated booking and peer review systems. The ability to filter by specific amenities,s such as kitchens or pet-friendly, ss appeals strongly to families and long-stay visitors who find standard hotel rooms insufficient. Independent hotels are balancing a diverse distribution strategy that increasingly utilizes digital tools to maintain direct relationships with international guests. The integration of instant booking confirmation and secure payment gateways has eliminated friction,ction encouraging spontaneous reservations. Furthermore, the rise of bleisure travel, where business trips extend into leisure stays, has increased average booking values and length of stay. The flexibility offered by various cancellation policies on major platforms also reduces consumer risk,k fostering higher conversion rates. These factors collectively ensure that accommodation remains the cornerstone of the online travel ecosystem.

The vacation packages segment is likely to experience the fastest CAGR of 14.8% over the forecast period, od owing to the increasing consumer desire for convenience and cost certainty in an era of complex travel logistics and volatile pricing. Along with this, the segment is driven by the advanced bundling capabilities of modern algorithms, which allow providers to combine flights, hotels,s and activities into single dynamic offers that are cheaper than booking components separately. Modern travelers are returning to bundled holiday options as a way to secure financial protection and reduce the logistical burden of planning complex trips. The r,ise of experiential tourism has prompted operators to include unique local tours and dining experiences within these packages, adding significant value beyond basic transport and lodging. There is a growing international focus on harmonizing digital standards to create a more efficient and friction-free experience for global travelers. The regulatory clarity provided by the updated Package Travel Directive has restored consumer confidence,e ensuring financial protection in case of operator insolvency. Mobile apps now facilitate easy customization of these packages, allowing users to swap elements in real time to suit personal preferences. The ability to manage an entire trip through a single interfa,ce enhances the user experience and drives loyalty. This convergence of convenience, safety, ty, and personalization ensures the vacation packages segment will outpace other service types in growth velocity.

By Booking Type Insights

The online travel agencies segment dominated tEuropeanope online travel market and accounted for a 6.3% share in 2025. The dominance of the segment is driven by the comprehensive aggregation of options, which allows consumers to compare price schedules and amenities across hundreds of suppliers in a single seEuropeanMarket trends also point to the powerful network effect, where large user bases attract more suppliers,s creating a virtuous cycle of inventory depth and competitive pricing. Digital travel platfo,rms are i,ncreasingly positioned as comprehensive research hubs where consumers leverage peer feedback and rewards to simplify c,omp, lex trip planning. The ability of OTAs to offe,,r cross-selling opportunities such as car rentals and insurance at the point of booking significantly increases average order value compared to direct supplier sites. Mobile technology remains a strategic priority, but consumers continue to favor web-based platforms for the heavy lifting of travel,l comparison, and discovery. Sophis, ticated artificial intelligence engines analyze user behavior to present highly personalized recommendations, ns increasing conversion rates substantially. The financial leverage of major OTAs allows them to negotiate exclusive rates and last-minute deals that individual suppliers cannot match independently. Furthermore, the multilingual support and localized payment methods rem,ove barriers for cross-border travel within Europe. These structural advantages ensure that Online Travel Agencies remain the primary gateway for European travel bookings.

The direct travel segment is on the r,,ise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 12.6% during the forecast period due to the strategic pivot of airlines and hotel chains to reduce commission costs and build direct relationships with customers through enhanced digital ecosystems. A furthfastest-growinghis growth is the implementation of aggressive loyalty programs that offer exclusive benefits such as room upgrades, des free breakfasts,asts or flexible cancellation only when booking directly. Airlines are reporting robust financial performance as they modernize their digital storefronts to capture the surge in global passenger traffic. The rise of brand authenticity campaigns encourages travelers to b, ook directly to ensure they receive accurate information and immediate support during disruptions. Independent hospitality properties are embracing integrated technology stacks to streamline guest experiences and reclaim control over their distribution channels. The ability to offer price match guarantees has effectively neutralized the primary advantage of third-party intermediaries. Direct channels also allow suppliers to collect valuable first-party data for personalized marketing without privacy restrictions associated with third-party cookies. The growing consumer awareness of commission structures has led some travelers to consciously choose direct booking to support local businesses. As technology lowers the barrier to entry for sophisticated direct sales, tools in this segment will continue to capture market share rapidly.

By Platform Insights

The mobile devices segment held the majority share of 58.7% oEuropeanEurope online travel market in 2025. The supremacy of the segment is attributed to the inherent nature of travel, which involves movement and on-the-go decision-making that aligns perfectly with smartphone accessibility. In addition, this segment is supported by the proliferation of dedicated travel apps that offer seamless user experiences, including mobile check-in, digital boarding passes, and real-time itinerary updates. Mobile connectivity in Europe has achieved near-total saturation, allowing for immediate digital communication with the vast majority of the adult population across the continent. The integration of geolocati, on services allows provide, rs to push relevant offers for nearby restaurants, attractions, or last-minute hotel rooms based on the user's current position. The deployment of next-generation mobile networks is steadily expanding across Europe, although the region continues to work toward closing the connectivity gap with other global leaders. Th,,e convenie,nce of biometric authentication, such as fingerprint and face recognition,n simplifies the payment processsignificantly reducing cart abandonment rates. Social media integration within mobile apps enables users to share travel plans and discover destinations through visual content, driving organic traffic. The shift towards micro-moments, where users make quick decisi,,ons during short breaks, favors the immediacy of mobile platforms over desktop computers. These structural changes in consumer behavior guarantee that mobile will remain the primary channel for travel interactions.

The mobile segment is expected to exhibit a noteworthy CAGR of 16.4% from 2026 to 2034. This rapid acceleration is fueled by continuous advancements in mobile hardware and software that enable richer and more immersive planning experiences previously impossible on small screens. Also, this sector is boosted by the adoption of augmented reality features within travel apps that allow users to visualize hotel rooms or navigate airports through their camera lenses. Consumers are gradually upgrading to more capable mobile hardware, which supports richer visual experiences and more sophisticated interactive digital content. The rise of voice-activated assistants integrated into mobile operating systems enables hands-free search and booking, which is particularly useful for travelers managing luggage or navigating transit. Digital engagement in the travel industry is increasingly mobile-centric as users rely on portable devices for the majority of their online interactions. The development of super-apps, which combine messaging, payments, and travel services, creates a sticky ecosystem where users spend more time and complete more transactions. Improved battery life and faster charging technologies ensure that devices remain functional throughout long travel days, supporting continuous enengagements mo,, bile networks become more reliable and affordable, the gap between mobile and desktop capabilities will close entirely, driving further adoption.

COUNTRY LEVEL ANALYSIS

Germany Online Travel Market Analysis

Germany was the top performer in the European online travel market and accounted for a 23.8% share in becauseusese of its status as the largest economy in Europe, with a population that possesses high disposable income and a strong cultural propensity for international travel. A big factor behind the expansion is the sophisticated digital literacy of German consumers who extensively research and book complex multi-destination trips online. Digital tools have become the primary resource for the vast majority of German households when organizing their trips and accommodation. The country serves as a key testing ground for sustainable travel technologies due to heightened environmental consciousness among its citizens. A well-developed logistics and payment infrastructure ensures secure and rapid transactions for both domestic and cross-border bookings. Germany's travel market is experiencing a robust digital expansion as consumers increasingly shift from traditional physical agencies to online booking environments. The presence of major global travel technology headquarters in Berlin fosters innovation in metasearch and booking engine solutions. Strict consumer protection laws have forced platforms to adopt high transparency standards,s enhancing long-term customer trust. This combination of economic strength,th technological readiness, and travel culture ensures Germany retains its top rank.

United Kingdom Online Travel Market Analysis

The UK holds a strong position as the second-largest regional playe,r in the European online travel market and held a 18.1% share in 2025. The d,,emand for online travel in the UK is credited to its mature digital ecosystem and high smartphone penetration. The nation benefits from being a global hub for travel technology startups and eestablished Europeantravel agencies that continuously innovate in user experience and artificial intelligence. The main thing making this grow is the deeply ingrained habit of last-minute booking among British travelers, which relies heavily on mobile applications for instant availability and deals. The UK travel industry has undergone a deep digital transformation, with the vast majority of commercial transactions now occurring through electronic channels. The presence of world-classaviation hubs like Heathrow and Gatwick generates massive volumes of flight searches and ancillary service bookings digitally. Handheld devices are rapidly becoming the dominant medium for travelers to manage their leisure itineraries and secure last-minute reservations. The post-Brexit regulatory environment has led to unique data governance frameworks that challenge operators but also create opportunities for specialized compliance solutions. High English language proficiency allows UK-based platforms to serve as gateways for global expansion. The strength of the financial services sector facilitates seamless cross-border payments and currency exchanges. This blend of creative prowess, technological maturity, t,y and financial capacity cements the UK as a pivotal market.

France Online Travel Market Analysis

France is a vital part of the European travel market due to its status as the world's most visited destination and a robust domestic outbound market. The region see,s a strong emphasis on experiential travel and cultural immersion, which drives demand for specialized online platforms offerinEuropeans and activities. Besides, the market is helped by the government-led initiative to digitize the tourism sector, ensuring that even small rural accommodations and local guides are visible on global onli,ne channels. The French public is steadily integrating digital platforms into their travel planning, though adoption rates remain balanced across different age groups. The ppopularityf domestic tourism during summer months drives significant spikes in online bookings for campsites and vacation rentals. Younger travelers in France are increasingly prioritizing mobile-first discovery for hyper-local activities and spontaneous bookings. The existence of strong national railway networks integrated with online booking platforms facilitates seamless multimodal travel planning. Cross-border e-commerce within the EU allows French travelers to access a wider range of international titles seamlessly. The focus on protecting French cultural heritage ensures that local content remains prominent on digital platforms. This strategic balance between heritage preservation and digital innovation ensures France remains a key growth engine.

Italy Online Travel Market Analysis

Italy is moving ahead steadfastly in the European online travel market revenue by leveraging its immense appeal as a historical and culinary destination to sustain steady demand for both inbound and outbound digital travel services. The market status is defined by a rapid catch-up in digital adoption as traditional family-run hotels and agritourisms increasingly recognize the necessity of online visibility to survive. Italy is seeing a gradual expansion of its digital audience as more households utilize online tools for logistical travel arrangements. A key driving factor is the resurgence of interest in slow travel and rural tourism, which performs exceptionally well on niche online platforms dedicated to authentic experiences. The tourism sector contributes significantly to the economy, prompting heavy investment in digital infrastructure to manage peak season flows efficiently. Smartphone usage is becoming the central pillar for Italian travelers during both the planning and execution phases of their journeys. Government incentivesfor digitalizationn under the National Recovery and Resilience Plan have provided funds for small businesses to upgrade their booking engines. The fragmented nature of the accommodation landscape creates opportunities for online aggregators to offer centralized access to diverse properties. This fusion of cultural wealth with modern digital tools positions Italy for sustained growth.

Spain Online Travel Market Analysis

Spain is likely to expand notably in Europeanrope online travel market over the forecast period, owing to its strategic role as a premier sun-and-beach destination for Northern Europeans and a growing outbound market. The nation has emerged as a critical battleground for online travel providers due to its high seasonality and reliance on international visitors who plan trips digitally. The market status is characterized by rapid growth in mobile bookings and dynamic packaging as young demographics embrace flexible and spontaneous travel formats. Spain’s tourism sector is attracting significant capital for digital modernization to maintain its competitive edge as a global destination leader. A primary driving factor is the intense popularity of all-inclusive resorts and holiday village,s, which are predominantly booked through online channels offering transparent package deals. The government has implemented policies to promote smart tourism destinations utilizing big data and IoT to enhance visitor experiences and manage overcrowding. High general internet penetration in Spain provides a massive infrastructure for digital travel providers to connect with an increasingly tech-savvy adult population. The rise of low-cost carrier connectivity has spurred demand for online flight and transfer bookings. Urban centers like Barcelona and Madrid are becoming hubs for travel tech startups, attracting talent and investment. This dynamic environment ensures Spain plays an increasingly important role in the regional digital travel economy.

COMPETITIVE LANDSCAPE

The competition in the European online travel market is intensely fierce, characterized by a constant battle for user attention and booking volume among global giants and specialized regional platforms. Dominant players leverage vast data ecosystems and proprietary technology to offer superior experiences and competitive pricing tha,t smaller competitors struggle to match without significant investment. However, niche operators thrive by focusing on specific segments such as luxury eco-tourism or local experiences where they can offer curated selections and deeper expertise that multinational corporations often lack. The landscape is further complicated by stringent consumerprotection laws and varying tax regimes across nations,s which force all participants to maintain robust compliance teams and adaptable operational models. New entrants from the metasearch and fintech sectors are disrupting traditional models by offering price comparison tools and buy-now-pay-later options that change, now forcing finance trips. Price wars occasionally erupt in commission rates, but differentiation increasingly relies on user experience, customer support quality, and unique inventory access. Mergers and acquisitions remain common as companies seek to consolidate technology stacks and expand their geographic footprint efficiently. This dynamic v environmentensures rapid evolution where adaptability, technological prowess, hnn, sand ervice excellence determine long-term survival and success in the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Online Travel Market include

- Booking Holding, Inc.

- Expedia Group, Inc.

- Trip.com Group Limi,, ed

- eDreams ODIGEO

- lastminute.com Group

- Airbnb, Inc.

- Trivago N.V.

- Skyscanner Ltd.

- Trainline PLC

- TUI Group

- HRS Group

- Flix SE (FlixBus / FlixTrain)

- Hostelworld Group PLC

- Amadeus IT Group SA

- Sabre Corporation

- Travelport Worldwide Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Booking Holdings operates as a foundational pillar within the European online travel ecosystem through its extensive portfolio, including Booking.com and Priceline. The company leverages its dominant accommodation inventory and sophisticated algorithmic pricing to connect millions of travelers with diverse lodging options across tEuropeanantinent. Recent actions focus heavily on integrating artificial intelligence to enhance personalized search results while simultaneously expanding its transportation and attraction offerings to become a one-stop shop. Booking Holdings has launched new sustainability filters allowing users to identify eco-friendly stays, which align with growing European consumer values. The firm continues to invest in mobile app functionality to ensure seamless last-minute bookings and digital check-in experiences. Global,l y Booking Holdings sets industry standards for cross-border transactions and ultimate support. By refining its loyalty programs, the company helps European travelers access exclusive deals while ensuring property partners achieve higher occupancy rates throughout the year.

- Expedia Group maintains a massive presence in theEuropeane online travel market by utilizing its diverse brands such as Expedia,dia Hotels.co,m, and Vrbo to serve varied traveler segments. The company excels in delivering comprehensive vacation packages that bundle flights, hotels, and car rental, which resonates deeplywith Europeanss and leisure tourists seeking convenience. Recent st,rategic moves in,clude heav,y invest,ment in proprietary technology to streamline the booking journey and reduce friction during payment processes. Exdia,h as, ha nced its ddata an analytics capabilities to offer dynamic packaging options that adjust in real time based on user behavior and demand fluctuations. The firm actively develops partnerships with local tourism boards to promote unique destinations and experiences tailored to specific European markets. Globally, Expedia drives innovation in loyalty integration and B2B distribution solutions. Their commitment to flexible cancellation policies and customer support helps align operations with post-pandemic travel expectations while maintaining robust growth forstakeholder ss.

- Airbnb has rapidly evolved into a critical player in theEuropeane online travel market by capitalizing on its vast network of unique homes and experiential activities. The company offers distinctive alternatives to traditional hotels that target consumers seeking authentic local immersion and flexible living spaces. ReEuropeanctions involve expanding its category filters to include specialized stays like castles or farmhouses, which appeal to niche European travel interests. Airbnb has introduced enhanced verification systems and safety features to build trust among users and comply with strict regional regulatory requirements. The firm leverages its global community to promote long-term stays,tays catering to the rising trend of remote work and digital nomadism across European cities. Globally,y Airbnb reshapes hospitality by proving the value of peer-to-peer sharing and community-based tourism. Their continuous enhancement of host tools and guest services help,s maintain high satisfaction levels. This independent approach allows them to adapt quickly to ch,,anging travel trends while maintaining strong brand loyalty across diverse international regions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the European online travel market primarily focus on mobile-first development to capture the growing segment of travelers who book trips spontaneously using smartphones. Companies heavily invest in artificial intelligence and machine learning to personalize search results and optimize dynamic pricing strategies in real time. Strategic partnerships with airlines, hotels, and local experience providers help secure exclusive inventory and increase brand visibility among targeted demographics. Major participants are expanding their service offerings beyond accommodation to include flight,s car rentals, and tour, creating comprehensive ecosystems that retain users. Development of sustainable travel filters and carbon footprint calculators ensures compliance with environmental regulations and appeals to eco-conscious consumers. Firms also prioritize flexible cancellation popoliciesd transparent refund processes to build trust and reduce booking anxiety among customers. Continuous localization of content and payment methods addresses the diverse cultural and linguistic needs of different European countries. These strategies collectively aim to maximize customer lifetime value while navigating complex regulatory landscapes effectively.

MARKET SEGMENTATION

This research report on the europe online travel market is segmented and sub-segmented into the following categories.

By Service Type

- Travel Accommodation

- Transportation Booking (Flights, Rail, Bus)

- Vacation Packages

- Car Rentals

- Tours & Activities

By Booking Type

- Online Travel Agencies (OTAs)

- Direct Travel Suppliers (Airlines, Hotels, Rail Operators)

By Platform

- Desktop / Laptop

- Mobile Devices

- Tablets

By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Sweden

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com