Europe Organic Cotton Market Size, Share, Growth, Trends Research Report, Segmented By Type, Quality, Application, And By Region (U.K France, Germany, Spain, Italy, Sweden, Russia and Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis Forecasts (2026 to 2034)

Europe Organic Cotton Market Report Summary

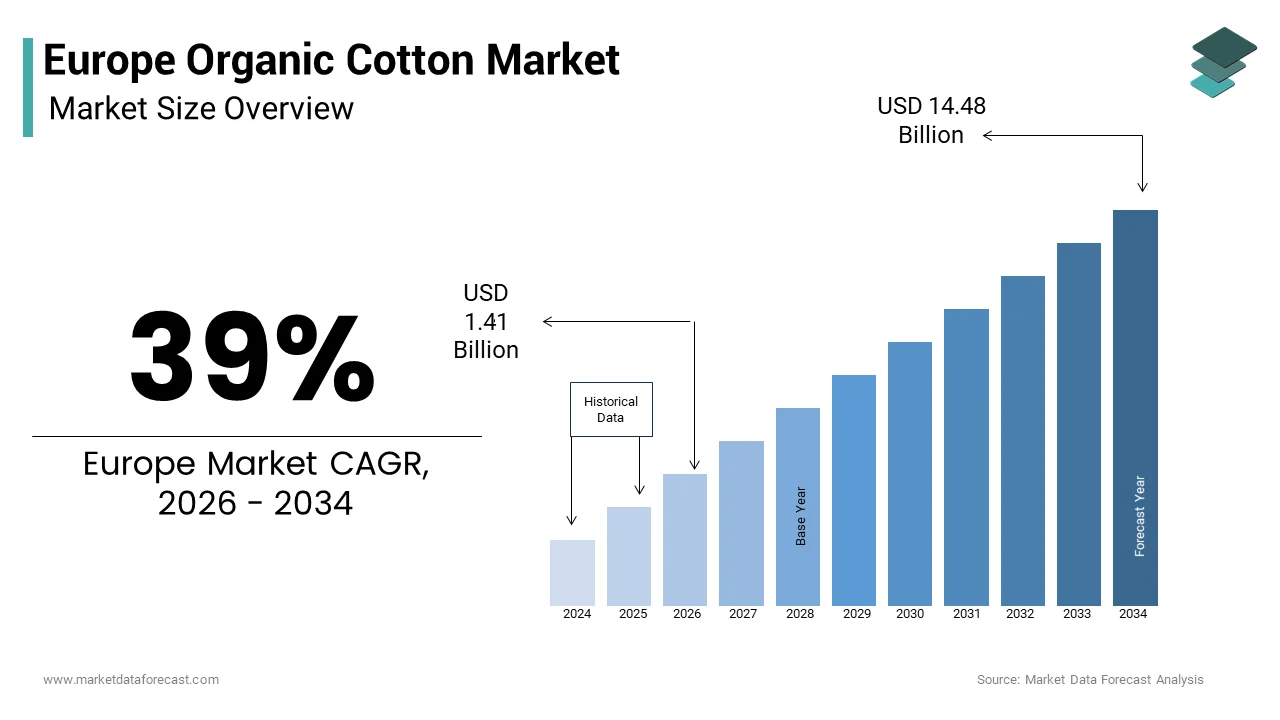

The Europe organic cotton market was valued at USD 1.02 billion in 2025, is estimated to reach USD 1.41 billion in 2026, and is projected to reach USD 14.48 billion by 2034, growing at an impressive CAGR of 39% during the forecast period from 2026 to 2034.

The growth of the market is driven by the increasing consumer preference for sustainable and eco-friendly textiles, rising awareness regarding the environmental impact of conventional cotton farming, and stringent European regulations promoting organic and ethical sourcing practices. The rapid expansion of the sustainable fashion industry, along with growing demand from apparel brands committed to ESG goals, is significantly accelerating market adoption. Additionally, increasing transparency in supply chains and the adoption of certified organic cotton standards are further strengthening market growth across Europe.

Key Market Trends

- Surging demand for sustainable fashion driven by environmentally conscious consumers and ethical purchasing behavior.

- Increasing adoption of certified organic cotton supported by global standards such as GOTS and fair-trade certifications.

- Strong regulatory push in Europe promoting sustainable agriculture and reducing chemical usage in textile production.

- Expansion of eco-conscious apparel brands and retailers integrating organic cotton into mainstream product lines.

- Rising investments in traceability and transparent supply chains, enabling brands to ensure authenticity and sustainability claims.

Segmental Insights

- By Type: The middle staple cotton segment dominated the market, accounting for 55.4% share in 2025, driven by its versatility, cost-effectiveness, and wide usage in textile manufacturing.

- By Quality: The upland cotton segment held a prominent share, supported by its high yield, adaptability, and suitability for large-scale organic cultivation.

- By Application: The apparel segment was the largest in 2026, fueled by the rapid shift of fashion brands toward sustainable materials and growing consumer demand for organic clothing.

Regional Insights

The Europe organic cotton market is witnessing rapid growth across key countries, supported by sustainability initiatives, strong fashion industries, and regulatory frameworks promoting eco-friendly textiles.

- Germany led the market, accounting for 22.3% share in 2025, driven by high consumer awareness and strong demand for sustainable apparel.

- The United Kingdom held the second-largest share at 18.3%, supported by increasing adoption of ethical fashion and retail sustainability commitments.

- France is expected to grow significantly, fueled by its luxury fashion sector and sustainability regulations.

- Italy is emerging as a key market due to its focus on premium textile processing and design excellence.

- Spain is gaining traction, supported by the growing adoption of sustainable practices among major fashion retailers and brands.

Competitive Landscape

The Europe organic cotton market is highly competitive, with key players focusing on sustainable sourcing, supply chain transparency, and strategic partnerships with fashion brands. Companies are increasingly investing in certification, traceability technologies, and organic farming networks to strengthen their market position and meet growing demand.

Prominent players in the Europe organic cotton market include Cargill Incorporated, Plexus Cotton Ltd., Hennes & Mauritz AB, C&A Mode BV, Inditex SA, Calcot Ltd., Remei AG, Arvind Limited, Louis Dreyfus Company, and Texas Organic Cotton Marketing Cooperative.

Europe Organic Cotton Market Size

The Europe organic cotton market size was valued at USD 1.02 billion in 2025 and is anticipated to reach USD 1.41 billion in 2026 to reach USD 14.48 billion by 2034, growing at a CAGR of 39% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Organic Cotton Market

The organic cotton is the cultivation trade and utilization of cotton fibers produced without synthetic pesticides genetically modified organisms or chemical fertilizers. This sustainable agricultural practice aligns with the European Union’s broader environmental objectives and the growing consumer demand for ethically sourced textiles. As per Eurostat, the textile and clothing industry in the European Union employed approximately 1.5 million people in 2023 indicating a substantial industrial base that is increasingly pivoting towards sustainable raw materials. The transition is driven by regulatory frameworks, such as the European Green Deal, which aims to make fashion more circular and environmentally friendly. According to the European Environment Agency, the textile sector is responsible for significant water consumption and pollution prompting stricter regulations on chemical usage in production. The Global Organic Textile Standard provides a recognized certification framework that ensures the organic status of textiles from harvesting to manufacturing. Consumer awareness regarding the health impacts of conventional cotton farming has also risen with studies linking pesticide exposure to various health issues. The Food and Agriculture Organization of the United Nations notes that organic farming practices improve soil health and biodiversity which resonates with European sustainability goals.

MARKET DRIVERS

Stringent Regulatory Frameworks Promoting Sustainable Textiles

The implementation of stringent regulatory frameworks promoting sustainable textiles is boosting the growth of Europe organic cotton market. The European Union has introduced comprehensive legislation aimed at reducing the environmental impact of the fashion and textile industries. According to the European Commission the Strategy for Sustainable and Circular Textiles mandates that by 2030 all textile products placed on the EU market must be durable repairable and recyclable. This legislative push encourages brands to source raw materials that align with these criteria such as organic cotton which is grown without harmful chemicals. As per the European Parliament the Ecodesign for Sustainable Products Regulation will set performance requirements for textiles including durability and reusability further incentivizing the use of high-quality organic fibers. The restriction of hazardous substances under the Registration Evaluation Authorization and Restriction of Chemicals regulation also limits the use of toxic inputs in conventional cotton farming making organic alternatives more attractive. Additionally, the Corporate Sustainability Reporting Directive requires large companies to disclose their environmental impact pushing them to adopt transparent and sustainable supply chains. These regulatory measures create a favorable environment for organic cotton by setting high standards for conventional practices. Brands are compelled to shift towards certified organic sources to comply with these laws and avoid penalties.

Growing Consumer Awareness and Preference for Ethical Fashion

The rising consumer awareness and preference for ethical fashion is additionally propelling the growth of the Europe organic cotton market. Modern consumers are increasingly informed about the environmental and social implications of their purchasing decisions leading to a shift towards sustainable brands. According to a survey by the European Consumer Organisation, over 60% of Europeans consider sustainability when buying clothes indicating a strong market trend. This heightened awareness is fueled by educational campaigns and media coverage highlighting the negative impacts of conventional cotton farming such as water pollution and soil degradation. As per the Textile Exchange, consumer demand for preferred fibers including organic cotton has grown steadily with many shoppers willing to pay a premium for certified products. The rise of digital platforms allows consumers to verify brand claims and trace supply chains enhancing trust in organic labels. Retailers are responding by expanding their organic cotton collections and prominently displaying certifications such as the Global Organic Textile Standard. The younger demographic particularly Generation Z and Millennials are driving this change as they prioritize values aligned with environmental stewardship. Social media influencers and advocacy groups further amplify the message promoting organic cotton as a responsible choice. This cultural shift towards conscious consumption ensures sustained growth for the organic cotton market. Brands that fail to adapt risk losing market share to competitors who embrace transparency and sustainability.

MARKET RESTRAINTS

High Production Costs and Limited Supply Availability

The high production costs and limited supply availability of organic cotton is solely limiting the growth of the Europe organic cotton market. Organic farming requires labor intensive practices such as manual weeding and natural pest control which increase production expenses compared to conventional methods. According to the Food and Agriculture Organization of the United Nations organic cotton yields are typically 20 to 30% lower than conventional cotton due to the absence of synthetic fertilizers and pesticides. This yield gap combined with higher labor costs results in premium pricing for organic cotton fibers. As per the Textile Exchange the global supply of organic cotton remains limited accounting for less than 1% of total cotton production creating a supply demand imbalance. European manufacturers rely heavily on imports from countries like India Turkey and China where supply chain disruptions can further exacerbate shortages. The volatility in raw material prices makes it difficult for brands to maintain consistent pricing strategies potentially dampening consumer demand. Additionally the certification process for organic cotton involves rigorous auditing and compliance costs which add to the overall expense. Small and medium sized enterprises often struggle to absorb these costs limiting their ability to compete with larger players. The lack of domestic organic cotton production in Europe further increases dependency on external sources exposing the market to geopolitical and logistical risks.

Complexity of Supply Chain Transparency and Certification

The complexity of supply chain transparency and certification is additionally degrading the growth of Europe organic cotton market. Ensuring the integrity of organic cotton from farm to finished product requires robust tracking systems and multiple certifications which can be cumbersome and costly. According to the Global Organic Textile Standard maintaining certification involves regular audits and documentation at every stage of the supply chain from ginning to spinning and weaving. As per the European Commission, fragmentation in the textile supply chain makes it challenging to trace the origin of raw materials accurately leading to risks of fraud and mislabeling. The presence of counterfeit organic certificates undermines consumer trust and complicates procurement for brands committed to sustainability. Additionally varying national regulations and certification standards across different countries create inconsistencies that hinder seamless international trade. Smallholder farmers in producing countries often lack the resources and knowledge to navigate complex certification requirements limiting their participation in the organic market. This limitation reduces the overall supply of certified organic cotton available to European buyers. The administrative burden of managing multiple certifications for different markets increases operational costs for suppliers and retailers. Furthermore, the lack of standardized digital tools for traceability slows down the verification process. These logistical and administrative challenges restrict the scalability of the organic cotton market. Until streamlined and universally accepted tracking systems are implemented the complexity of certification will remain a significant barrier.

MARKET OPPORTUNITIES

Integration of Digital Traceability Technologies

The integration of digital traceability technologies by enhancing transparency and consumer trust is ascribed to set up new opportunities for the growth of Europe organic cotton markets. Blockchain and radio frequency identification technologies enable real time tracking of cotton from farm to retail ensuring the authenticity of organic claims. According to the European Commission the Digital Product Passport initiative aims to provide consumers with detailed information about product sustainability and origin fostering greater confidence in organic labels. As per the Textile Exchange digital traceability solutions are being adopted by major brands to verify supply chain integrity and combat fraud. These technologies allow retailers to share verified data with consumers through QR codes or apps enhancing engagement and brand loyalty. The ability to prove organic provenance commands a price premium and differentiates products in a crowded market. Additionally, digital platforms facilitate better communication between farmers and buyers enabling direct partnerships and fairer pricing models. The European Union’s support for digital innovation in the textile sector provides funding and resources for developing these tools. By leveraging technology companies can streamline certification processes and reduce administrative burdens. This technological advancement also helps in identifying inefficiencies in the supply chain leading to cost savings. The adoption of digital traceability aligns with regulatory requirements for transparency and sustainability.

Expansion into Non Apparel Applications and Home Textiles

The expansion of organic cotton into non apparel applications and home textiles is another attribute boosting the growth of Europe organic cotton market. Beyond clothing organic cotton is increasingly used in bedding towels baby products and personal hygiene items due to its softness and hypoallergenic properties. According to the European Home Textiles Association, the demand for sustainable home furnishings is rising as consumers seek to create healthier living environments. Organic cotton’s absence of residual chemicals makes it ideal for baby clothes and bedding where safety is paramount. Retailers are expanding their product lines to include organic cotton towels sheets and curtains catering to this niche but growing segment. The hospitality industry is also adopting organic cotton linens to align with sustainability goals and appeal to eco conscious travelers. Collaborations between organic cotton producers and home textile manufacturers can drive innovation in product design and functionality. Marketing campaigns highlighting the health benefits of organic cotton in home settings can further stimulate demand. The diversification into these applications reduces reliance on the volatile fashion sector and stabilizes revenue streams. This expansion leverages the inherent qualities of organic cotton to capture new customer segments. The trend towards holistic wellness supports the adoption of organic materials in daily life.

MARKET CHALLENGES

Vulnerability to Climate Change and Weather Variability

The vulnerability of organic cotton cultivation to climate change and weather variability poses a major challenge to the Europe organic cotton market expansion. Since organic farming relies on natural rainfall and soil health rather than synthetic inputs it is highly susceptible to droughts floods and extreme temperatures. According to the Intergovernmental Panel on Climate Change, changing weather patterns are affecting agricultural productivity globally with cotton being particularly sensitive to water stress. As per the Food and Agriculture Organization of the United Nations, erratic rainfall and rising temperatures can lead to significant crop failures and reduced yields for organic farmers. Europe’s reliance on imported organic cotton means that climate events in producing countries like India and Turkey directly impact supply stability. The lack of irrigation infrastructure in many organic farming regions exacerbates the risk of water scarcity. These climatic uncertainties make it difficult for suppliers to guarantee consistent volumes and quality to European buyers. Price volatility resulting from supply shocks further complicates planning for brands and retailers. Additionally the transition to organic farming requires a period of soil regeneration during which yields may be lower increasing financial risk for farmers. Without adequate support and adaptation strategies the resilience of the organic cotton supply chain remains compromised. This environmental vulnerability threatens the long-term sustainability of the market. Mitigating these risks requires investment in climate resilient farming practices and diversified sourcing strategies.

Greenwashing and Lack of Consumer Trust

The prevalence of greenwashing and lack of consumer trust is also to degrade the growth of the Europe organic cotton market in coming years. As demand for sustainable products rises some brands make misleading claims about the organic nature of their textiles without proper certification. According to the European Consumer Organisation investigations have revealed instances of conventional cotton being labeled as organic deceiving consumers and undermining legitimate producers. As per the Competition and Markets Authority in the United Kingdom vague environmental claims are common in the fashion industry leading to consumer awareness. This erosion of trust makes it difficult for genuine organic cotton brands to differentiate themselves and justify premium prices. Consumers may become disillusioned with sustainability labels if they perceive them as marketing tactics rather than verified commitments. The proliferation of private labels and self declared certifications adds to the confusion making it hard for shoppers to identify authentic organic products. Regulatory efforts to crackdown on greenwashing are ongoing but enforcement remains inconsistent across Europe. The lack of universal understanding of certification logos further complicates consumer decision making. Brands investing in genuine organic sourcing face unfair competition from those engaging in deceptive practices. Restoring trust requires stricter enforcement of labeling laws and greater education for consumers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 39% |

| Segments Covered | By Type, Quality, Application, Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Cargill Incorporated (U.S.), Plexus Cotton Ltd. (U.K.), Hennes and Mauritz AB, C&A Mode BV, Inditex SA, Staple Cotton Cooperative Association (U.S.), Calcot Ltd. (U.S.), The Rajlakshmi Cotton Mills (P) Limited (India), Remei AG (Switzerland), Arvind Limited(India), Noble Ecotech (India), Louis Dreyfus Company (Netherlands), Texas Organic Cotton Marketing Cooperative (U.S.) |

SEGMENTAL ANALYSIS

By Type Insights

The middle staple cotton segment was the largest by holding 55.4% of the Europe organic cotton market share in 2025 with its versatility and cost effectiveness which make it suitable for a wide range of everyday apparel and home textile products. The high demand for basic clothing items, such as t-shirts jeans and underwear where middle staple organic cotton provides an optimal balance between softness durability and price. According to the Textile Exchange, middle staple varieties such as Upland cotton constitute the majority of global organic cotton production ensuring consistent availability for European manufacturers. As per Eurostat, the retail sales of clothing in the European Union remained robust in 2023 with consumers increasingly seeking affordable sustainable options. Middle staple organic cotton allows brands to offer certified organic products at competitive price points thereby appealing to a broader consumer base beyond the luxury segment. The established supply chains for middle staple cotton facilitate easier integration into existing manufacturing processes without requiring significant equipment modifications. Additionally, the widespread adoption of this type by fast fashion retailers transitioning to sustainable materials further amplifies its market share. The ability to blend middle staple organic cotton with other fibers also enhances its applicability in diverse textile formulations.

The extra long staple cotton segment is projected to register a fastest CAGR of 12.4% from 2026 to 2034, driven by the increasing demand for premium luxury textiles and high end fashion. This rapid growth is attributed to the superior qualities of extra long staple fibers such as exceptional softness strength and luster which are highly valued in luxury apparel and bedding. Also, the growing affluent consumer segment in Europe that prioritizes quality and exclusivity in their purchasing decisions. According to the Luxury Institute, consumers in Europe are willing to pay a significant premium for products made from high quality natural fibers like Egyptian Giza or Supima organic cotton. As per the European Luxury Market Report the luxury goods sector continues to expand with sustainability becoming a key differentiator for high end brands. Extra long staple organic cotton offers the tactile experience and durability required for premium products while aligning with ethical sourcing standards. The rise of direct to consumer luxury brands focusing on transparency and craftsmanship further boosts demand for this specialized fiber. Additionally, the hospitality industry’s shift towards eco friendly luxury linens contributes to market growth. Manufacturers are investing in dedicated supply chains for extra long staple organic cotton to meet the stringent quality requirements of luxury clients.

By Quality Insights

The upland cotton segment was the largest by holding a prominent share of the Europe organic cotton market in 2025 with its widespread cultivation globally and its suitability for mass market applications. The extensive production of organic Upland cotton in major supplying countries such as India Turkey and China, which ensures a steady flow of raw materials to European processors. According to the Food and Agriculture Organization of the United Nations Upland, cotton accounts for the vast majority of global cotton production including organic varieties due to its adaptability to various climatic conditions. As per the Textile Exchange, the availability of certified organic Upland cotton has increased significantly making it the default choice for most brands transitioning to sustainable sourcing. The cost efficiency of Upland cotton compared to specialty varieties like Pima or Giza makes it accessible for large scale production runs. The established infrastructure for spinning and weaving Upland cotton facilitates seamless integration into existing supply chains. Additionally, the versatility of Upland cotton allows it to be used in a wide range of products from casual wear to home furnishings.

The supima pima cotton segment is expected to exhibit a fastest CAGR of 10.8% from 2026 to 2034 owing to the rising preference for premium quality and durable textiles. The growth of the segment is likely to grow with the unique characteristics of Supima and Pima cotton which offer superior softness strength and color retention compared to standard varieties. The expansion of the premium apparel sector in Europe, where brands are distinguishing themselves through higher quality materials. There is a noticeable shift towards long lasting garments which aligns with the durability benefits of Supima and Pima fibers. Consumers are increasingly educated about the benefits of extra long staple fibers and are willing to invest in products that offer better performance and longevity. Additionally, the use of these premium fibers in high end activewear and luxury basics is expanding. The limited supply of organic Supima and Pima cotton creates a sense of scarcity that appeals to luxury buyers.

By Application Insights

The apparel segment was the largest by holding a dominant share of the Europe organic cotton market in 2026 with the extensive use of organic cotton in clothing items ranging from casual wear to formal attire. The strong consumer demand for sustainable fashion driven by environmental awareness and regulatory pressures. According to Eurostat, the household expenditure on clothing and footwear in the European Union remains significant with a growing portion allocated to sustainable brands. As per the European Commission the Strategy for Sustainable and Circular Textiles, encourages the use of eco-friendly materials in apparel production prompting major retailers to increase their organic cotton offerings. The versatility of organic cotton makes it suitable for various garment types including t shirts dresses shirts and denim. The presence of prominent fashion brands committing to 100% sustainable sourcing further amplifies demand. Additionally, the rise of online retail platforms has made organic cotton apparel more accessible to consumers across Europe. The seasonal nature of fashion drives continuous replenishment and new collections ensuring steady consumption. The alignment of organic cotton with current fashion trends towards natural and minimalist aesthetics also supports its dominance.

The packaging segment is likely to witness a fastest CAGR of 14.5% from 2026 to 2034 with the urgent need to replace single use plastics with biodegradable alternatives. The increasing adoption of organic cotton bags and wraps for retail food packaging and gift wrapping is augmented to boost the growth of the segment. The primary driver is the European Union’s Single Use Plastics Directive which bans certain plastic products and encourages the use of reusable and compostable materials. According to the European Bioplastics Association the demand for bio-based packaging solutions is surging as retailers seek compliant and sustainable options. Consumers are increasingly rejecting plastic bags in favor of stylish and eco friendly cotton alternatives. The hospitality and retail sectors are also adopting organic cotton packaging for premium product presentation enhancing brand image. Regulatory incentives for circular packaging solutions further support this trend. The ability of organic cotton packaging to be reused multiple times before composting adds to its value proposition. This shift towards sustainable packaging practices drives the fastest growth in the packaging application segment.

COUNTRY LEVEL ANALYSIS

Germany Organic Cotton Market Analysis

Germany was the largest contributor in the Europe organic cotton market by holding 22.3% of share in 2025 with its strong environmental consciousness and robust retail sector. The country’s market status is characterized by high demand for certified sustainable textiles among both consumers and businesses. According to the German Federal Ministry for Economic Affairs and Climate Action, consumer preference for eco labeled products is among the highest in Europe. As per the Textile Exchange Germany is a leading importer of organic cotton in the region supporting its domestic textile industry. The country’s strict adherence to environmental standards such as the Blue Angel ecolabel promotes the use of organic materials. German consumers are well informed about the benefits of organic farming leading to steady demand for organic cotton apparel and home textiles. The presence of numerous sustainable fashion brands headquartered in Germany further stimulates market growth. Government initiatives supporting circular economy practices also encourage the adoption of organic cotton.

United Kingdom Organic Cotton Market Analysis

The United Kingdom organic cotton market held second position with 18.3% of share in 2025 with its vibrant fashion industry and regulatory framework. The UK’s departure from the EU, which has led to the development of independent sustainability standards, such as the UK Ecolabel. According to the Office for National Statistics, retail sales of clothing have shown resilience with a notable shift towards ethical brands. British consumers are increasingly aware of the environmental impact of fast fashion driving demand for durable and organic alternatives. Major retailers like Marks and Spencer and Next have committed to sourcing more sustainable materials including organic cotton. The government’s Green Industrial Strategy supports the transition to low carbon industries including textiles.

France Organic Cotton Market Analysis

France organic cotton market growth is likely to grow with its luxury fashion sector and regulatory initiatives. According to the French Ministry of Ecological Transition, the law encourages the use of recycled and organic materials to reduce waste. The luxury sector in France values the premium quality of organic cotton particularly extra-long staple varieties for high end garments. French consumers place a high value on provenance and craftsmanship which aligns with the attributes of organic cotton. The government’s support for local textile innovation further boosts the market. Paris Fashion Week has also become a platform for showcasing sustainable fashion trends.

Italy Organic Cotton Market Analysis

Italy organic cotton market growth is likely to grow with the focus on high quality processing and design excellence in organic cotton products. The presence of specialized textile districts in regions like Tuscany and Lombardy that have adopted organic certification standards. According to the Italian National Institute of Statistics, the textile industry remains a key export sector with growing demand for sustainable inputs. The craftsmanship associated with Italian manufacturing adds value to organic cotton garments making them desirable in the luxury segment. Italian consumers are increasingly conscious of environmental issues driving domestic demand for organic products. The government’s National Recovery and Resilience Plan includes funds for green transition in industries including textiles. Italy’s strong design heritage and manufacturing capabilities support the production of high value organic cotton items.

Spain Organic Cotton Market Analysis

Spain organic cotton market growth is likely to grow with the increasing adoption of sustainable practices by major Spanish retailers and brands. The presence of global fashion giants such as Inditex which has committed to using 100% sustainable cotton, including organic by 2025. According to the Spanish Ministry for Ecological Transition consumer awareness of sustainability is rising particularly among younger demographics. The tourism sector also contributes to demand with hotels and resorts adopting organic cotton linens to appeal to eco conscious travelers. Spanish consumers are becoming more discerning about the environmental impact of their purchases driving retail changes. The government’s support for circular economy initiatives further encourages the use of organic materials. Spain’s strategic location facilitates efficient logistics for textile imports and exports.

COMPETITIVE LANDSCAPE

The competition in the Europe organic cotton market is characterized by the presence of large multinational retailers specialized sustainable brands and textile manufacturers. Market leaders compete on the basis of supply chain transparency product quality and sustainability credentials. The high demand for certified organic cotton creates pressure on sourcing capabilities making secure supply chains a key competitive advantage. Companies differentiate themselves through innovative designs exclusive certifications and compelling storytelling about their ethical practices. Price competition is moderate as consumers are often willing to pay a premium for verified sustainable products. Strategic partnerships with farmers and NGOs strengthen market positions and ensure long term material availability. Regulatory frameworks such as the European Green Deal drive standardization and encourage fair competition. The rise of digital platforms allows smaller niche brands to challenge established players by offering unique value propositions. Consumer awareness and loyalty play crucial roles in shaping competitive dynamics. Companies that demonstrate genuine commitment to sustainability and social responsibility gain a competitive edge.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe organic cotton market are

- Cargill Incorporated (U.S.)

- Plexus Cotton Ltd. (U.K.)

- Hennes and Mauritz AB

- C&A Mode BV

- Inditex SA

- Staple Cotton Cooperative Association (U.S.)

- Calcot Ltd. (U.S.)

- The Rajlakshmi Cotton Mills (P) Limited (India)

- Remei AG (Switzerland)

- Arvind Limited(India)

- Noble Ecotech (India)

- Louis Dreyfus Company (Netherlands)

- Texas Organic Cotton Marketing Cooperative (U.S.)

Top Players In The Market

- Inditex SA is a global fashion retailer headquartered in Spain that plays a pivotal role in the Europe organic cotton market through its extensive portfolio of brands including Zara and Massimo Dutti. The company has committed to sourcing 100% sustainable cotton by 2025 with a significant portion being organic. Inditex actively collaborates with suppliers to ensure traceability and adherence to strict environmental standards. Recent actions include expanding its Join Life collection which features garments made from organic cotton and other eco friendly materials. The company invests in innovative recycling technologies to close the loop in textile production. Inditex leverages its massive scale to influence supply chain practices globally promoting better farming methods. By prioritizing transparency and sustainability Inditex strengthens its market position and meets the growing demand for responsible fashion among European consumers.

- Hennes and Mauritz AB commonly known as H&M is a Swedish multinational clothing retailer that significantly contributes to the Europe organic cotton market. The company is one of the largest users of organic cotton globally aiming to source all its cotton from more sustainable sources by 2030. H&M integrates organic cotton into its Conscious Collection offering affordable and stylish options for environmentally conscious shoppers. Recent strategies involve partnering with farmers to support the transition to organic farming practices ensuring long term supply stability. The company utilizes digital tools to enhance supply chain transparency allowing customers to verify the origin of their garments. H&M also invests in circular business models such as garment collecting and recycling initiatives.

- C&A Mode BV is a leading international fashion retail chain with strong roots in the Netherlands and Germany that champions sustainable fashion. The company was an early adopter of organic cotton and continues to be a major player in the Europe organic cotton market. C&A offers a wide range of certified organic cotton products across its stores emphasizing affordability and accessibility. Recent actions include achieving Cradle to Cradle Certified gold level for several of its organic cotton t shirts demonstrating high standards of material health and recyclability. The company works closely with suppliers to improve social and environmental conditions in the supply chain. C&A also engages in consumer education campaigns to raise awareness about the benefits of organic cotton.

Top Strategies Used By Key Market Participants

Key players in the Europe organic cotton market primarily focus on securing sustainable supply chains through direct partnerships with farmers and certification bodies. Companies invest in traceability technologies such as blockchain to ensure transparency and build consumer trust. Product innovation involves integrating organic cotton into diverse collections ranging from basics to luxury items. Marketing strategies emphasize environmental benefits and ethical sourcing to appeal to conscious consumers. Retailers expand their private label organic offerings to control quality and pricing. Collaborations with non-governmental organizations help establish best practices and support farmer livelihoods. Circular economy initiatives including recycling and take back programs are implemented to reduce waste. These strategies enable participants to differentiate their brands and meet regulatory requirements while driving growth in the European region.

MARKET SEGMENTATION

This research report on the Europe organic cotton market is segmented and sub-segmented into the following categories.

By Type

- Long-Staple Cotton

- Short-Staple Cotton

- Middle Staple Cotton

- Extra-long Staple Cotton

- Others

By Quality Type

- Supima/Pima

- Upland

- Giza

- Others

By Application

- Apparel

- Packaging

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

Frequently Asked Questions

How is organic cotton used in the European textile and apparel industry?

Organic cotton is used to produce eco-friendly clothing, home textiles, and sustainable fabric products.

What factors are driving the growth of the organic cotton market in Europe?

Rising consumer demand for sustainable and ethically sourced textiles is a key growth driver.

Which products commonly use organic cotton in Europe?

Apparel, bedding, towels, and baby products widely use organic cotton.

Why are consumers choosing organic cotton over conventional cotton?

It is produced without harmful chemicals and is considered safer for both the environment and human health.

How does organic cotton farming support sustainability?

It reduces chemical usage, conserves water, and promotes healthier soil conditions.

Which industries contribute to demand for organic cotton in Europe?

Fashion, home textiles, and personal care industries are major contributors.

What challenges affect the Europe organic cotton market?

Higher production costs and limited supply can impact market growth.

How are brands responding to the demand for organic cotton products?

They are incorporating sustainable sourcing and transparent supply chains into their operations.

Which countries are key markets for organic cotton in Europe?

Germany, France, the United Kingdom, and Italy are major markets.

What future trend is expected in the Europe organic cotton market?

Increasing focus on sustainable fashion and eco-friendly materials is expected to drive market growth.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com