Europe Patient Blood Management Market Size, Share, Growth, Trends Research Report, Segmented By Product, Component, End-User, And By Region (U.K France, Germany, Spain, Italy, Sweden, Russia and Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis Forecasts (2026 to 2034)

Europe Patient Blood Management Market Report Summary

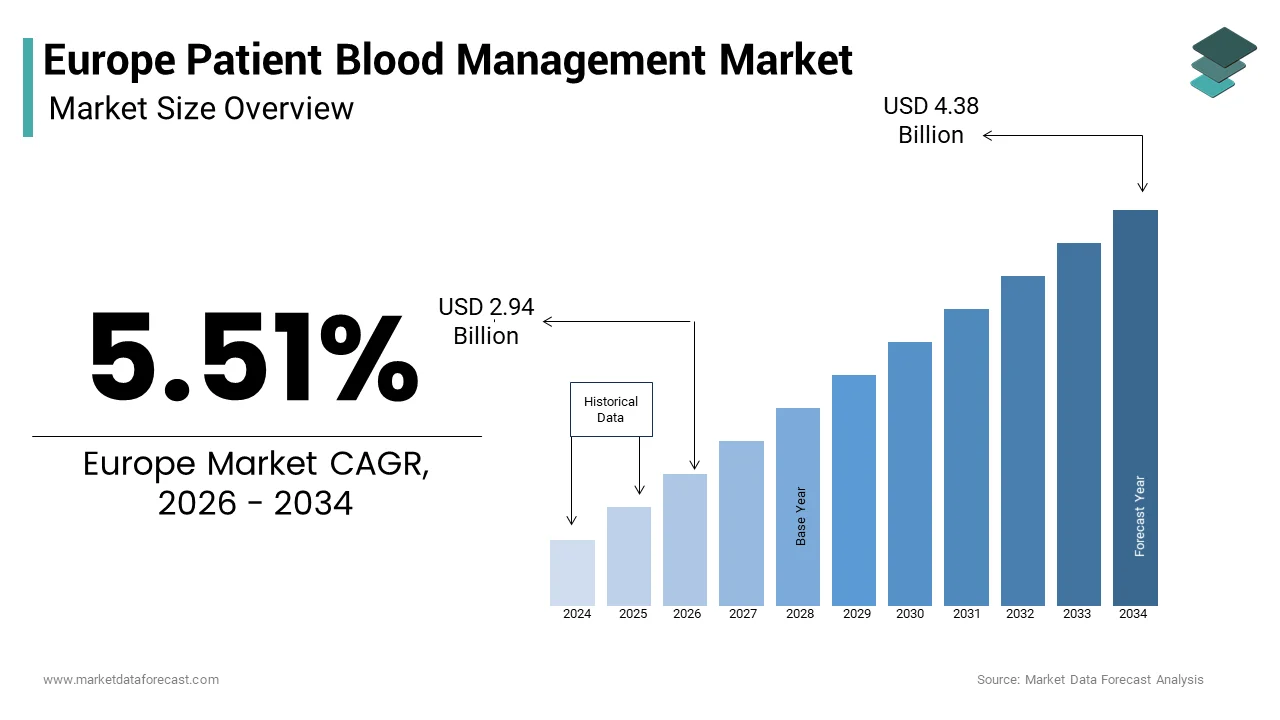

The Europe patient blood management market was valued at USD 2.79 billion in 2025, is estimated to reach USD 2.94 billion in 2026, and is projected to reach USD 4.38 billion by 2034, growing at a CAGR of 5.51% during the forecast period from 2026 to 2034. The growth of the Europe patient blood management market is driven by increasing awareness of blood conservation practices, rising surgical procedures, and the growing need to optimize blood utilization in healthcare settings. The adoption of advanced blood management technologies, along with supportive healthcare policies and improved clinical outcomes, is further accelerating market expansion across Europe.

Key Market Trends

- Increasing adoption of patient blood management programs to reduce transfusion-related risks and improve patient outcomes.

- Rising demand for blood conservation techniques driven by growing surgical volumes and aging population.

- Technological advancements in blood screening, storage, and transfusion management systems enhancing efficiency and safety.

- Growing focus on cost-effective healthcare solutions is promoting the use of optimized blood management practices.

- Expansion of hospital-based blood management initiatives across Europe is supporting market growth.

Segmental Insights

- Based on product, the reagents and kits segment dominated the Europe patient blood management market by holding a share of 42.1% in 2025. The segment’s leadership is attributed to their widespread use in blood testing, screening, and diagnostic procedures.

- Based on component, the whole blood derivatives segment accounted for 65.3% of the Europe patient blood management market share in 2025. The dominance of this segment is driven by its extensive use in transfusion therapies and clinical treatments.

- Based on end user, the hospitals segment was the largest in the Europe patient blood management market in 2025. This is due to the high volume of surgical procedures and the central role of hospitals in blood transfusion and management practices.

Regional Insights

The Europe patient blood management market shows steady growth across key countries.

- Germany led the market by accounting for 24.8% of the share in 2025, supported by advanced healthcare infrastructure and strong adoption of blood management programs.

- The United Kingdom followed with 19.8% of the market share, driven by increasing healthcare investments and awareness initiatives.

- France holds a significant position due to the active involvement of national health authorities in promoting safe blood practices.

- Italy is experiencing steady growth supported by evolving healthcare systems and increased focus on blood conservation.

- Spain is expected to witness notable expansion during the forecast period due to improving healthcare services and rising adoption of advanced medical technologies.

Competitive Landscape

The Europe patient blood management market is moderately competitive, with key players focusing on technological innovation, product development, and strategic collaborations to strengthen their market presence. Companies are investing in advanced blood management solutions and expanding their distribution networks to meet the growing demand. Prominent players in the Europe patient blood management market include Haemonetics, Terumo Corporation, Fresenius Kabi, Grifols, Baxter International, Cerus Corporation, BloodCenter of Wisconsin, Octapharma, and Medtronic.

Europe Patient Blood Management Market Size

The Europe Patient blood management market size was valued at USD 2.79 billion in 2025 and is anticipated to reach USD 2.94 billion in 2025 to reach USD 4.38 billion by 2034, growing at a CAGR of 5.51% during the forecast period.

Patient Blood Management (PBM) is a systematic, evidence-based approach to optimizing the care of patients who might need transfusions, focusing on three core pillars: managing anemia, minimizing blood loss, and harnessing physiological tolerance to anemia. This paradigm shift moves away from reactive transfusion practices toward proactive conservation strategies that prioritize patient safety and resource sustainability. The region faces significant pressure on its blood supply chains. According to the European Commission, millions of red blood cell units are transfused across the European Union every year to support critical care and surgeries. However, donation rates in several member states remain below the levels required for total national self-sufficiency, creating a persistent reliance on cross-border supplies. Statistics from the World Health Organization (WHO) indicate that an aging population in Europe is driving a long-term increase in the need for complex surgical interventions. Since many of these procedures require blood products, the pressure on national blood services is expected to intensify over the coming years. Furthermore, Recent clinical audits and healthcare reviews emphaize that a significant portion of transfusions administered in European hospitals could potentially be avoided. This suggests a major opportunity to improve Patient Blood Management (PBM) strategies to conserve blood resources and reduce the risks associated with unnecessary transfusions. The integration of multidisciplinary teams involving hematologists, surgeons, and anesthetists is becoming standard in major medical centers across Germany and France to address these inefficiencies. This evolving landscape underscores the urgent need for structured protocols that reduce reliance on allogeneic blood while improving clinical outcomes for complex surgical and oncological cases.

MARKET DRIVERS

Rising Prevalence of Surgical Procedures and Trauma Cases

The escalating volume of complex surgical interventions and trauma cases across the region serves as a primary factor for the adoption of PBM protocols and the growth of the Europe patient blood management market. Demographic shifts toward an older population have led to a surge in orthopedic, cardiovascular, and oncological surgeries, all of which carry a high risk of perioperative bleeding. According to Eurostat, the European Union is experiencing a steady increase in its elderly population. This demographic shift is expected to drive a higher volume of major surgeries, which traditionally place a sustained demand on regional blood services. Trauma remains another significant driver, with the European Trauma Course organization reporting that hemorrhage accounts for approximately 30–40% of preventable deaths in trauma patients across the region. Hospitals are increasingly recognizing that traditional transfusion reliance is insufficient to meet this growing demand safely and efficiently. Consequently, there is a mandated shift toward preoperative optimization and intraoperative blood conservation techniques to ensure adequate hemoglobin levels without depleting scarce blood bank reserves. Major multicenter trials in cardiac surgery have demonstrated that implementing restrictive transfusion thresholds significantly lowers the proportion of patients exposed to allogeneic blood without compromising clinical outcomes like mortality or major organ failure. This surge in procedural volume combined with the imperative to maintain blood availability forces healthcare systems to adopt comprehensive management strategies that mitigate bleeding risks and optimize patient physiology before entering the operating theater.

Stringent Regulatory Frameworks and Patient Safety Initiatives

The implementation of rigorous regulatory standards and a heightened focus on patient safety drive the institutionalization of PBM and the expansion of the European patient blood management market. Consequently, this acts as a powerful catalyst across European healthcare systems. Regulatory bodies have increasingly classified unnecessary transfusions as adverse events, prompting hospitals to adopt strict governance protocols to avoid penalties and ensure compliance. As per guidelines issued by the European Directorate for the Quality of Medicines and Health Care, member states are required to maintain traceability and hemovigilance systems that monitor every step from donation to transfusion, exposing inefficiencies in traditional practices. Scientific literature emphasizes that blood transfusions are not without risk, as they are associated with potential immune modulation and longer hospital stays. This evidence has prompted a move away from liberal transfusion strategies in favor of more targeted, patient-specific approaches. In response, national health authorities in countries like the United Kingdom and Sweden have integrated patient blood management into their national patient safety goals, making it a mandatory component of accreditation for surgical centers. The European Society of Anaesthesiology has also released updated guidelines recommending specific hemoglobin triggers that discourage routine transfusion. These regulatory pressures compel hospital administrators to invest in training programs and digital monitoring tools to ensure adherence to best practices, thereby driving the systematic uptake of conservation methodologies throughout the continent.

MARKET RESTRAINTS

High Implementation Costs and Resource Intensity

The substantial financial burden and resource intensity required to establish comprehensive patient blood management programs hamper the growth of the Europe patient blood management market. This is particularly true for smaller community hospitals. Implementing a robust program demands significant upfront investment in specialized diagnostic equipment, such as point of care testing devices for coagulation and hemoglobin analysis, alongside extensive staff training and multidisciplinary team coordination. Furthermore, the ongoing operational costs include maintaining inventory of expensive pharmacological agents like erythropoiesis stimulating agents and tranexamic acid, which may not be fully reimbursed by national insurance schemes in all jurisdictions. The requirement for continuous education and certification for medical staff adds another layer of recurring expense that many institutions struggle to absorb. In regions where healthcare funding is already stretched thin, administrators often prioritize immediate life saving interventions over preventive management strategies, delaying the integration of systematic blood conservation measures. This financial barrier creates a disparity in care quality between wealthy urban centers and resource limited rural facilities, slowing the uniform adoption of these critical practices across the broader European landscape.

Resistance to Cultural Change and Entrenched Clinical Habits

Deep seated resistance to cultural change and entrenched clinical habits among healthcare professionals poses a formidable obstacle to the effective deployment of PBM strategies in the region and the expansion of the Europe patient blood management market. For decades, the prevailing medical culture has favored a liberal transfusion approach, viewing blood products as a safe and readily available remedy for anemia or intraoperative blood loss, despite evidence to the contrary. The psychological barrier is compounded by a lack of awareness regarding the long term risks associated with allogeneic transfusions, leading to skepticism about the necessity of restrictive protocols. Changing these behaviors requires a fundamental shift in mindset that takes time and persistent educational efforts, which are often inconsistently applied across different institutions. In many teaching hospitals, junior doctors learn from mentors who practice traditional methods, perpetuating the cycle of over transfusion. Additionally, the fragmented nature of healthcare delivery in some European countries makes it difficult to enforce standardized protocols uniformly. Even well-funded programs may fail to achieve their full potential without a cohesive strategy to address behavioral inertia issues. After all, the human element remains the most critical variable in the successful execution of blood conservation initiatives.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Predictive Analytics

The incorporation of artificial intelligence and machine learning into patient blood management workflows offers a groundbreaking opportunity to enhance predictive accuracy and optimize resource allocation across the hospitals in the region, which is expected to fuel the growth of the Europe patient blood management market. AI algorithms can analyze vast datasets of electronic health records to identify patients at high risk of severe bleeding or transfusion dependency before surgery, enabling preemptive intervention. As per research, AI driven models have demonstrated the ability to predict massive transfusion requirements with a notable accuracy rate, significantly outperforming traditional scoring systems. This capability allows clinicians to tailor preoperative optimization strategies, such as iron supplementation or erythropoietin therapy, to specific patient profiles, thereby reducing unnecessary procedures and conserving blood stocks. Furthermore, real time analytics can monitor intraoperative blood loss and suggest immediate corrective actions, minimizing waste and improving patient outcomes. The automation of inventory management through predictive modeling ensures that blood banks maintain optimal stock levels, reducing expiration rates which currently stand at approximately 5 percent for red blood cells in some regions. By leveraging these intelligent systems, hospitals can transition from reactive to proactive care models, ensuring that blood products are available precisely when and where they are needed most. This technological evolution not only enhances clinical efficiency but also supports the financial sustainability of healthcare systems by reducing costly complications and optimizing the use of scarce biological resources.

Expansion of Autologous Blood Recovery Technologies

The advancing field of autologous blood recovery technologies creates a pathway for the expansion of the Europe patient blood management market. It provides a viable alternative to allogeneic transfusions while addressing supply chain vulnerabilities. Cell salvage techniques, which collect, wash, and reinfuse a patient own blood during surgery, are gaining traction as a standard of care for procedures with anticipated high blood loss, such as cardiac and orthopedic surgeries. Recent innovations have expanded the applicability of these systems to obstetric and trauma settings, broadening the addressable market considerably. The growing preference for autologous solutions is further fueled by patient demand for safer, infection free options and regulatory push towards self sufficiency in blood supply. Manufacturers are developing portable and cost effective cell salvage devices that make the technology accessible to smaller clinics and emergency response units. Additionally, the integration of automated washing systems reduces the workload on perfusionists and nurses, streamlining the workflow. European healthcare providers are increasingly adopting autologous transfusion systems as a core component of blood management, driven by growing awareness and lower technology costs. Consequently, this shift is creating lucrative opportunities for industry manufacturers and service providers.

MARKET CHALLENGES

Shortage of Skilled Professionals

The acute shortage of skilled professionals trained in the complexities of modern blood conservation techniques and multidisciplinary coordination slows down the growth of the Europe patient blood management market. Effective implementation requires a collaborative team approach involving hematologists, surgeons, anesthesiologists, and specialized nurses, yet there is a significant gap in specialized training programs across the region. The complexity of interpreting coagulation profiles, managing pharmacological agents, and operating advanced cell salvage equipment demands a level of expertise that is currently in short supply. This deficit is exacerbated by the aging workforce in the healthcare sector, with many experienced practitioners retiring without adequate succession planning. The lack of standardized certification courses means that knowledge transfer is inconsistent, leading to variability in care quality between institutions. In rural areas, the scarcity of specialists is even more pronounced, forcing general practitioners to manage complex cases without sufficient support. Until educational institutions and professional bodies expand their curricula to include comprehensive blood management training, the human resource bottleneck will continue to hinder the scalability and effectiveness of these vital programs, limiting their impact on patient outcomes and system efficiency.

Fragmented Regulatory Landscape

The fragmented regulatory landscape across European nations is a major hurdle to the harmonization and standardization of PBM practices, which constrains the expansion of the Europe patient blood management market. This creates inconsistencies in care and market access. While the European Union provides overarching guidelines, individual member states retain significant autonomy in defining their national transfusion policies, reimbursement structures, and approval processes for new technologies. The lack of uniformity complicates the efforts of multinational organizations to implement consistent best practices across their networks. Furthermore, varying definitions of appropriate transfusion thresholds and differing levels of reimbursement for blood conservation therapies create confusion among clinicians and administrators. Some countries offer robust financial incentives for adopting patient blood management, while others provide little to no support, leading to unequal adoption rates. The absence of a unified European database for hemovigilance also limits the ability to share critical safety data and benchmark performance effectively. These regulatory silos foster an environment of uncertainty that slows down the diffusion of innovative solutions and prevents the realization of a truly integrated European approach to blood safety and conservation, ultimately impacting the overall efficiency of the healthcare ecosystem.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.51% |

| Segments Covered | By Product, Component, End-User, Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Haemonetics (US), Terumo Corporation (JP), Fresenius Kabi (DE), Grifols (ES), Baxter International (US), Cerus Corporation (US), BloodCenter of Wisconsin (US), Octapharma (CH), Medtronic (US) |

SEGMENTAL ANALYSIS

By Product Insights

The reagents and kits segment held the majority share of 42.1% of the Europe patient blood management market in 2025. This supremacy of the segment is supported by the consumable nature of these products, which are required for every diagnostic test and surgical procedure involving blood conservation, ensuring a continuous and recurring demand cycle that capital equipment cannot match. The widespread necessity for preoperative anemia screening serves as a primary driver for the sustained leadership of reagents and kits across European healthcare facilities. Clinical guidelines mandate the identification and treatment of iron deficiency anemia before elective surgeries to reduce transfusion requirements, creating a massive volume of daily tests. Hospitals across Germany and France have institutionalized these screening pathways, leading to the consumption of millions of test kits annually. The shift toward point of care testing has further amplified this demand, as these devices rely heavily on proprietary single use cartridges and reagent strips to deliver rapid results within minutes. Unlike durable instruments, these consumables must be replenished constantly, generating a steady revenue stream that outpaces capital equipment sales. Furthermore, the introduction of advanced biomarkers for distinguishing between different types of anemia has expanded the menu of available tests, increasing the average spend per patient. This clinical imperative to optimize patient physiology before surgery ensures that reagents and kits remain the financial backbone of the market sector. The expanding adoption of intraoperative cell salvage technologies significantly bolsters the demand for specialized reagents and kits, reinforcing the segment market dominance. Cell salvage procedures, which recover and reinfuse a patient own blood during surgery, require specific disposable sets including suction lines, reservoirs, and washing centrifuge bowls for every single case. Each procedure generates a predictable and substantial cost in consumables, often exceeding the amortized cost of the machine itself over time. The strict regulatory requirement for single use components to prevent cross contamination ensures that hospitals cannot reuse these items, guaranteeing a captive market for manufacturers. Additionally, the growing application of cell salvage in obstetrics and trauma surgery, sectors previously hesitant to adopt the technology, has opened new avenues for kit consumption. Manufacturers have responded by developing integrated kits that combine anticoagulants and washing solutions, simplifying the workflow for perfusionists. This procedural volume growth, coupled with the mandatory disposable nature of the technology, creates a robust and inelastic demand profile that secures the leading position of the reagents and kits segment.

The software segment is likely to experience the fastest CAGR of 13.8% from 2026 to 2034. Digital adoption in healthcare and the need for data-driven blood inventory management are fueling this segment’s fast-paced expansion. The urgent need to minimize blood product wastage and optimize inventory levels is a primary catalyst for the rapid adoption of patient blood management software solutions. Blood products have limited shelf lives, with red blood cells expiring after 42 days, leading to significant financial losses when units are not utilized in time. Advanced software platforms utilize predictive algorithms to analyze historical usage patterns, surgical schedules, and seasonal trends, enabling blood banks to maintain optimal stock levels and reduce expiry rates. These systems provide real time visibility into inventory across multiple hospital sites, facilitating the redistribution of units before they expire. The integration of barcode scanning and radio frequency identification technology further automates tracking, reducing human error and enhancing traceability compliance. As healthcare systems face increasing pressure to improve efficiency and reduce costs, the return on investment for such software becomes compelling, driving rapid procurement cycles. The ability to generate detailed analytics on transfusion practices also supports quality improvement initiatives, making software an indispensable tool for modern blood management strategies. Stringent regulatory requirements for comprehensive hemovigilance and traceability are propelling the explosive growth of specialized software in the European market. Regulations mandate that every step of the blood transfusion chain, from donation to patient administration, be meticulously recorded and reportable to national authorities. Modern software solutions automate the collection of adverse event data, streamline the reporting process to national hemovigilance agencies, and ensure full compliance with safety standards. These platforms enable the rapid identification of transfusion reactions and facilitate root cause analysis, enhancing overall patient safety. The shift toward electronic health records in countries like Sweden and the Netherlands has created a fertile environment for the integration of dedicated hemovigilance modules that communicate seamlessly with hospital information systems. Furthermore, the ability of software to benchmark performance against national standards encourages hospitals to adopt these tools to maintain accreditation. Regulatory scrutiny is intensifying and data requirements are becoming more complex. Consequently, reliance on sophisticated software solutions will continue to accelerate, making it the highest-growth market segment.

By Component Insights

The whole blood derivatives segment led the Europe patient blood management market and accounted for a 65.3% share in 2025. This leading position of the segment is attributed to the fundamental clinical necessity of red blood cells for treating anemia and acute hemorrhage, which remain the most common indications for transfusion across all medical specialties. The unparalleled demand for red blood cell concentrates in surgical and trauma settings serves as the bedrock for the dominance of the whole blood derivatives segment. Major surgeries such as cardiac bypass, joint replacements, and organ transplants frequently result in significant blood loss that requires immediate replacement to maintain oxygen delivery to vital organs. In trauma care, hemorrhage remains the leading cause of preventable death, and rapid administration of red blood cells is the cornerstone of resuscitation protocols. The physiological irreplaceability of red blood cells in carrying oxygen means that no synthetic alternative currently exists that can match their efficacy in acute settings, cementing their status as the most critical blood component. Furthermore, the aging population in Europe is undergoing more complex procedures that carry higher bleeding risks, sustaining high consumption levels. While patient blood management aims to reduce unnecessary transfusions, the baseline demand for red blood cells in life threatening situations remains inelastic and voluminous, ensuring this segment retains its overwhelming market share compared to other components. The rising prevalence of chronic anemia among the elderly population in Europe drives a consistent and substantial demand for red blood cell transfusions, reinforcing the market leadership of whole blood derivatives. As individuals age, the incidence of conditions such as myelodysplastic syndromes, chronic kidney disease, and gastrointestinal bleeding increases, all of which often necessitate regular red blood cell support. Unlike acute trauma cases which are episodic, chronic anemia requires ongoing management, creating a steady stream of repeat patients who consume significant volumes of red blood cell units over time. Oncology treatments, particularly chemotherapy, frequently induce severe anemia that requires transfusion support to allow patients to continue life saving therapies. The lack of effective long term alternatives for certain types of refractory anemia ensures that red blood cell transfusions remain the standard of care. This demographic tide creates a structural demand that is resistant to short term fluctuations, securing the dominant position of red blood cell concentrates in the component landscape for the foreseeable future.

The plasma derived products segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 9.2% between 2026 and 2034 due to the expanding therapeutic applications of plasma fractions in treating rare coagulation disorders and the increasing recognition of plasma utility in critical care resuscitation. The broadening scope of therapeutic applications for plasma derived factors in treating rare bleeding and immune disorders is a primary engine for the rapid growth of this segment. Advances in biotechnology have led to the development of highly purified and recombinant plasma proteins that offer safer and more effective treatments for conditions like hemophilia, von Willebrand disease, and primary immunodeficiencies. Furthermore, the approval of new indications for intravenous immunoglobulins in neurological and autoimmune diseases has significantly expanded the addressable patient pool beyond traditional uses. Physicians are increasingly prescribing these specialized products earlier in the disease course to prevent long term complications, driving volume growth. The shift toward home based therapy for hemophilia patients has also increased accessibility and adherence, further boosting demand. As research continues to uncover new roles for plasma proteins in modulating the immune system and repairing tissues, the pipeline of innovative therapies promises to sustain this high growth trajectory, making plasma derivatives the most dynamic component segment. The growing adoption of plasma products for critical care resuscitation and the management of coagulopathy in trauma and surgical patients is accelerating market expansion. Clinical evidence increasingly supports the use of fresh frozen plasma and specific factor concentrates as part of balanced transfusion protocols to correct coagulopathy early in the course of massive hemorrhage. The "damage control resuscitation" approach has increased the per patient consumption of plasma in critical care units. Additionally, the use of plasma derived albumin for volume expansion in patients with sepsis or liver failure is gaining traction due to its favorable safety profile compared to synthetic colloids. The standardization of massive transfusion protocols in hospitals throughout the UK and Germany ensures a consistent and rising demand for plasma products in acute settings. Awareness of the benefits of early coagulation management is spreading. As a result, the utilization rates of plasma derivatives are expected to climb steadily, fueling the segment's rapid growth.

By End User Insights

The hospitals segment was the largest segment in the Europe patient blood management market and occupied a substantial share in 2025 because of the fact that hospitals are the primary site for major surgical interventions, trauma care, and complex medical treatments where the majority of blood products are consumed and managed. Hospitals serve as the central hub for the vast majority of high volume surgical procedures that necessitate extensive blood management protocols, driving their overwhelming market share. From elective orthopedic joint replacements to emergency cardiac surgeries and organ transplants, these complex interventions are almost exclusively performed in hospital settings where blood banks and transfusion services are readily available. The concentration of specialized surgical teams, intensive care units, and advanced monitoring equipment within hospitals creates an ecosystem where patient blood management is integral to operational success. The implementation of multidisciplinary blood management committees within hospitals further centralizes decision making and resource allocation, ensuring that hospitals remain the primary consumers of blood products and related technologies. The sheer scale of inpatient care, where patients stay for days or weeks and may require multiple transfusions, dwarfs the volume seen in outpatient or clinic settings. This structural centrality of hospitals in the delivery of acute and complex care cements their position as the dominant end user in the market landscape. The stringent regulatory and accreditation requirements imposed on hospitals act as a powerful force consolidating their leadership in the patient blood management market. National health authorities and international accreditation bodies mandate that hospitals maintain rigorous hemovigilance systems, adhere to strict transfusion guidelines, and implement comprehensive blood conservation programs to ensure patient safety. The regulatory pressure compels hospitals to invest heavily in advanced blood management infrastructure, including automated testing analyzers, cell salvage machines, and sophisticated inventory software, far more than any other end user segment. The requirement for 24/7 availability of blood products and specialized staff further necessitates that hospitals maintain robust internal blood banks and management protocols. The fear of litigation associated with transfusion errors also drives hospitals to adopt the latest safety technologies and best practices proactively. This culture of compliance and the resources dedicated to meeting these high standards ensure that hospitals remain the primary drivers of market demand and innovation adoption in the patient blood management sector.

The diagnostic clinics segment is expected to exhibit a noteworthy CAGR of 10.5% over the forecast period owing to the shift toward outpatient care, the rise of preoperative assessment centers, and the decentralization of diagnostic services. Besides, the strategic shift toward conducting preoperative assessments in specialized outpatient diagnostic clinics is a key driver fueling the rapid expansion of this segment. Healthcare systems are increasingly moving routine pre-surgical evaluations, including anemia screening and coagulation profiling, out of acute hospital settings to improve efficiency and reduce costs. As per health policy reforms in countries like the Netherlands and Sweden, dedicated preoperative clinics are now standard for optimizing patients before they enter the operating room, ensuring that any blood management issues are addressed days or weeks in advance. These clinics rely heavily on rapid diagnostic kits and point of care devices to deliver immediate results, facilitating timely intervention with iron therapy or other treatments. The volume of patients flowing through these specialized centers is growing as surgical waitlists expand and the focus on day-case surgery intensifies. By identifying and treating anemia early in a clinic setting, hospitals can reduce cancellations and improve surgical outcomes, creating a strong economic incentive to expand these facilities. The decentralized nature of these clinics allows for greater accessibility for patients, increasing the overall uptake of preoperative screening services. This structural change in the patient journey places diagnostic clinics at the forefront of the initial phases of patient blood management, driving their high growth rate. The rapid proliferation of point of care testing networks within diagnostic clinics is accelerating market growth by enabling immediate and accessible blood analysis outside traditional laboratory environments. Advances in miniaturized diagnostic technology have made it feasible for clinics to perform complex hemoglobin and coagulation tests with accuracy comparable to central labs but with much faster turnaround times. The capability allows clinicians to diagnose anemia and coagulopathies during a single visit, initiating treatment plans immediately without the delay of sending samples to external labs. The convenience and speed offered by these clinics attract a growing number of patients, particularly those seeking quick pre-employment or pre-surgical clearances. The integration of these testing services with digital health records further enhances their appeal to referring physicians. Technology is growing more affordable and accessible, prompting clinics to adopt new capabilities. This shift is expanding the reach of patient blood management diagnostics and driving rapid market growth.

COUNTRY LEVEL ANALYSIS

Germany Patient Blood Management Market

Germany dominated the Europe patient blood management market and accounted for a 24.8% share in 2025. This dominance of the German market is driven by the rigorous enforcement of national guidelines by the German Medical Association, which mandates strict adherence to patient blood management principles in all accredited hospitals. The country market status is defined by its world class healthcare infrastructure, a high density of specialized surgical centers, and a proactive approach to implementing evidence-based blood conservation protocols. The country also boasts a highly organized blood donation system managed by the Red Cross and university hospitals, ensuring a stable supply chain that supports advanced conservation efforts. Furthermore, the German healthcare reimbursement system increasingly rewards hospitals for reducing complications and length of stay, providing a financial incentive to adopt efficient blood management practices. The presence of leading medical device manufacturers within the country fosters a culture of innovation and early adoption of new technologies like cell salvage and automated testing. This combination of regulatory rigor, high surgical volume, and technological prowess solidifies Germany position as the undisputed market leader in the region.

United Kingdom Patient Blood Management Market

The United Kingdom followed closely behind in the regional market and captured a 19.8% share in 2025. A key driver for the UK market is the leadership of the National Health Service Blood and Transplant organization, which has pioneered national patient blood management collaboratives that provide training, resources, and audit tools to hospitals nationwide. The market status here is characterized by a centralized national health system that actively drives standardization and large scale implementation of patient blood management initiatives across the nation. The UK also faces unique pressures from an aging population and a high prevalence of chronic diseases, which necessitates efficient resource utilization to maintain sustainability. The strong emphasis on clinical governance and the publication of robust national guidelines by the British Society for Haematology ensure that best practices are disseminated rapidly. Additionally, the UK is a hub for clinical research in transfusion medicine, attracting investment and fostering the development of novel blood management therapies. The synergy between centralized policy making and frontline clinical engagement creates a dynamic environment that sustains the UK status as a critical market player.

France Patient Blood Management Market

France is another key player in the European market due to the active role of the French National Authority for Health, which regularly updates and enforces clinical practice guidelines for transfusion and blood conservation. The French market is distinguished by a strong tradition of centralized health planning and a robust network of university hospitals that serve as centers of excellence for hematology and transfusion medicine. The country also benefits from a well established blood establishment system under the supervision of the French Blood Establishment, which ensures high quality and safety standards. Recent government initiatives to modernize hospital infrastructure and digitize health records have facilitated the adoption of advanced blood management software and tracking systems. Furthermore, the French medical community places a high value on continuing education, with frequent national conferences dedicated to transfusion safety and patient blood management. This commitment to quality, combined with a structured healthcare system and high surgical volumes, propels France as a pivotal and stable market in the European landscape.

Italy Patient Blood Management Market

Italy grew steadily in the European market owing to a diverse healthcare landscape with strong regional variations but a growing consensus on the importance of blood conservation. The market status in Italy is evolving rapidly as regional health authorities begin to implement standardized patient blood management protocols to address efficiency gaps and reduce variability in care. One of the major drivers here is the increasing focus on reducing healthcare costs and improving patient outcomes in the context of an aging demographic and rising chronic disease burden. Major academic centers in regions like Lombardy and Emilia Romagna are leading the way, serving as models for the rest of the country by demonstrating significant reductions in blood usage through structured programs. The Italian society of transfusion medicine is also playing a crucial role in harmonizing practices and promoting the use of autologous blood recovery techniques. Additionally, the growing awareness of patient safety and the legal implications of transfusion errors are motivating hospitals to invest in better management systems. This momentum toward standardization and efficiency is transforming Italy into a fast growing and increasingly influential market within Europe.

Spain Patient Blood Management Market

Spain is predicted to expand notably in the Europe patient blood management market from 2026 to 2034 due to rapid modernization and increasing integration of patient blood management into national health strategies. The market status is shifting from a fragmented approach to a more coordinated national effort, driven by the need to optimize resources in a challenging economic environment. A key driver for the Spanish market is the initiative by the Ministry of Health to promote patient blood management as a strategic priority for the national health system, supported by funding for pilot projects and training programs. The country high volume of orthopedic and cardiovascular surgeries, particularly in tourist-heavy regions with specialized private clinics, further stimulates demand for advanced blood management solutions. Spain is also seeing a rise in the use of digital health tools to monitor blood usage and improve traceability, aligning with broader European trends. The collaborative efforts between public and private sectors, along with a strong professional community dedicated to transfusion safety, are creating a fertile ground for market growth. These factors combine to position Spain as a vibrant and emerging market with significant potential for future expansion.

COMPETITIVE LANDSCAPE

The competitive landscape of the Europe patient blood management market is defined by a mix of specialized global leaders and regional manufacturers vying for dominance through innovation and service excellence. Established corporations leverage their extensive distribution networks and broad product ranges to maintain strong relationships with large hospital groups and national blood agencies. However, the market sees increasing pressure from agile niche players who introduce disruptive technologies such as portable cell salvage units and cloud based hemovigilance software. Competition is fierce in the area of digital integration where companies race to offer the most accurate predictive analytics and seamless interoperability with existing hospital systems. Regulatory compliance acts as a significant barrier to entry but also serves as a battleground where firms compete on the speed and ease of adhering to stringent European safety standards. Price competition remains relevant for commoditized consumables while value based selling dominates for high capital equipment. Strategic collaborations with academic institutions for clinical trials further differentiate players by validating efficacy. Overall the environment drives continuous advancement in patient safety and operational efficiency as companies strive to become indispensable partners in the evolving healthcare ecosystem.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe patient blood management market are

- Haemonetics (US)

- Terumo Corporation (JP)

- Fresenius Kabi (DE)

- Grifols (ES)

- Baxter International (US)

- Cerus Corporation (US)

- BloodCenter of Wisconsin (US)

- Octapharma (CH)

- Medtronic (US)

Top Players In The Market

- Haemonetics Corporation stands as a global leader dedicated exclusively to blood management solutions and plays a pivotal role in the European healthcare landscape. The company provides a comprehensive portfolio including automated blood collection systems, cell salvage devices, and software for inventory management. In Europe, Haemonetics actively collaborates with national blood services and major hospital networks to implement patient blood management programs that reduce waste and improve safety. Recent actions involve the launch of advanced analytics platforms that utilize artificial intelligence to predict blood demand and optimize stock levels across large health systems. The firm also invests heavily in educational initiatives to train clinicians on best practices for minimizing allogeneic transfusions. Haemonetics is strengthening its position as a trusted partner for European institutions by continuously innovating disposable kits and integrating digital tools. These advancements directly empower providers to enhance efficiency and patient outcomes in transfusion medicine.

- Fresenius SE & Co. KGaA operates as a diversified healthcare giant with a significant footprint in the European patient blood management sector through its medical technology division. The company offers a wide range of products including therapeutic apheresis systems, blood transfusion devices, and consumables essential for modern blood conservation strategies. In Europe, Fresenius leverages its extensive local presence and manufacturing capabilities to ensure reliable supply chains for hospitals and blood banks. Recent strategic moves include the expansion of its digital health offerings to connect apheresis devices with hospital information systems for real time data monitoring. The corporation also focuses on sustainability by developing eco friendly disposable sets and reducing the environmental impact of its operations. Fresenius is enhancing its ability to deliver integrated patient blood management solutions through targeted acquisitions of niche technology firms. Furthermore, they are strengthening partnerships with European regulatory bodies to address complex continental needs.

- Terumo Corporation is a renowned Japanese multinational that has established a robust presence in the Europe patient blood management market through its high quality medical device portfolio. The company specializes in blood collection sets, transfusion needles, and cell salvage technologies that are widely used in European surgical and emergency settings. Terumo commitment to innovation is evident in its recent introduction of next generation soft shell reservoirs and improved biocompatible coatings that enhance patient safety during extracorporeal procedures. In Europe, the firm actively engages with key opinion leaders and professional societies to promote evidence based transfusion practices. Recent actions include the establishment of new training centers in major European cities to educate healthcare professionals on the latest blood conservation techniques. Terumo continues to build strong relationships with European providers by focusing on product reliability and clinical excellence. This ensures their technologies remain integral to effective patient blood management protocols throughout the region.

Top Strategies Used By Key Market Participants

Key players in the Europe patient blood management market primarily focus on strategic mergers and acquisitions to broaden their product portfolios and gain access to innovative technologies. Companies heavily invest in research and development to create advanced digital solutions such as artificial intelligence driven inventory management systems and automated testing devices. Strategic partnerships with national blood services and hospital networks are common to facilitate the implementation of comprehensive patient blood management programs and ensure regulatory compliance. Market participants also prioritize educational initiatives and continuous professional development to train clinicians on best practices and foster brand loyalty. Expanding manufacturing facilities within Europe helps firms mitigate supply chain risks and meet local content requirements efficiently. Additionally, companies adopt tiered pricing models and flexible financing options to make high end technologies accessible to smaller community hospitals. The integration of sustainability goals into product design and operations is becoming a key differentiator to align with European environmental standards.

MARKET SEGMENTATION

This research report on the Europe patient blood management market is segmented and sub-segmented into the following categories.

By Product

- Instruments

- Accessories

- Reagents and Kits

- Software

By End-User

- Blood Banks

- Hospitals

- Diagnostic Clinics

- Pathology Labs

By Component

- Whole Blood

- Plasma

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

Frequently Asked Questions

What does patient blood management involve in Europe’s healthcare system?

It focuses on optimizing the use of a patient’s own blood to reduce unnecessary transfusions.

Why is patient blood management gaining importance across Europe?

It improves clinical outcomes while minimizing risks associated with blood transfusions.

How can patient blood management be explained in simple terms?

It is a medical approach that conserves blood and enhances patient safety during treatment.

Which healthcare settings adopt patient blood management practices the most?

Hospitals and surgical centers are the primary adopters due to high transfusion needs.

What role does technology play in patient blood management?

Advanced monitoring and diagnostic tools help manage blood usage more effectively.

How does this approach benefit patients directly?

It reduces complications, shortens recovery time, and lowers exposure to transfusion-related risks.

What factors are driving the growth of this market in Europe?

Rising surgical procedures and increasing focus on cost-effective healthcare are key drivers.

How do guidelines and protocols influence adoption?

Standardized clinical guidelines encourage consistent and safe blood management practices.

What challenges exist in implementing patient blood management programs?

Lack of awareness and resistance to change in clinical practices can hinder adoption.

How does patient blood management support healthcare sustainability?

It reduces reliance on donated blood and optimizes healthcare resources.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com